Asia

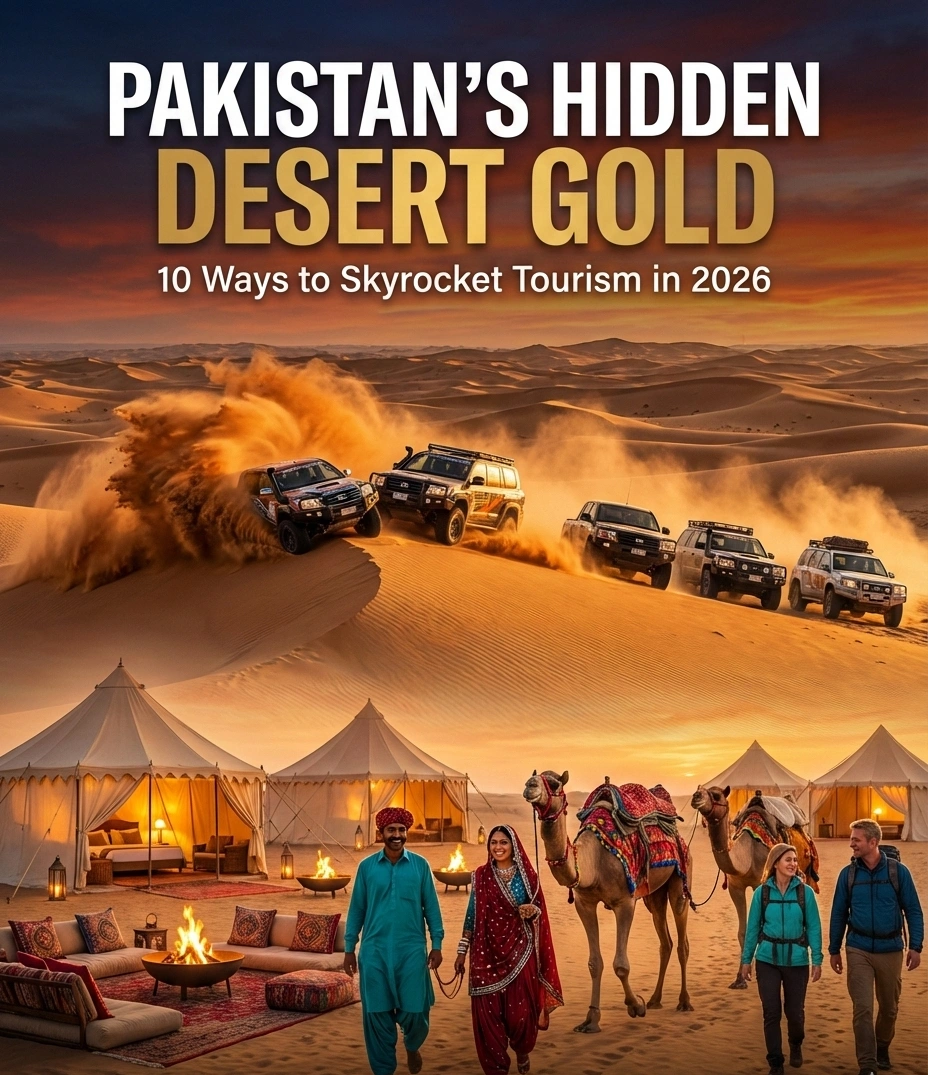

10 Ways to Boost Pakistan’s Tourism Economy in 2026 by Unlocking the Deserts of Cholistan and Thar

The sun rises over the Cholistan Desert, painting endless dunes in shades of amber and gold. A convoy of modified 4x4s kicks up plumes of sand as they race toward the horizon, while nearby, a camel caravan winds its way past ancient Derawar Fort, its 40 towering bastions standing sentinel over centuries of history. Meanwhile, 400 kilometers to the east, the Thar Desert’s “Rohi”—the land of shifting sands—comes alive with the rhythmic beats of traditional music as villagers prepare for the annual Tharparkar Cultural Festival.

These scenes aren’t from some distant fantasy. They’re the untapped reality of Pakistan’s desert economy in 2026—a sector that could transform the country’s tourism landscape if properly leveraged.

Pakistan’s tourism industry generated approximately USD 4.4-4.9 billion in 2025, welcoming around 965,000 international arrivals according to recent government estimates. Yet this represents merely a fraction of the country’s potential. The government has set an ambitious target of reaching $30-40 billion in annual tourism revenue—a goal that seems distant until you consider what neighboring regions have accomplished. Rajasthan’s desert tourism alone contributes over $12 billion annually to India’s economy, while Dubai transformed barren sands into a $45 billion tourism powerhouse.

Pakistan possesses comparable—arguably superior—raw materials: the 26,300 square kilometers of Cholistan (larger than Israel) and the 22,000 square kilometers of Thar (comparable to Slovenia). These deserts contain architectural marvels, biodiversity hotspots, vibrant indigenous cultures, and adventure tourism potential that remains criminally underutilized.

The question isn’t whether Pakistan’s deserts can drive economic growth. It’s how quickly stakeholders can implement the strategies to make it happen. Here are ten evidence-based, actionable approaches to unlock this sleeping giant in 2026.

1. Expand and Internationalize the Cholistan Desert Rally

The Cholistan Desert Rally returned in February 2026 after years of inconsistency, drawing thousands of domestic spectators and adventure enthusiasts to Derawar Fort. This annual motorsport event, organized by the Tourism Development Corporation of Punjab, represents Pakistan’s most established desert tourism brand—yet it operates at perhaps 20% of its potential.

Compare this to the Dakar Rally, which generates over $100 million in direct economic impact for host countries, or the Abu Dhabi Desert Challenge, which attracts 50+ international teams and global media coverage worth millions in destination marketing value. The Cholistan Rally, despite featuring challenging terrain that rivals any international desert race, remains largely unknown outside Pakistan.

The economic opportunity: Transforming Cholistan Rally into an FIA-sanctioned international motorsport event could generate $15-25 million annually in direct spending (participant fees, accommodation, logistics) plus exponentially greater media value. The infrastructure already exists—the 480-kilometer desert track, proximity to Bahawalpur’s hotels, and local support systems.

2026 action steps: The Punjab government should pursue FIA Desert Rally Championship accreditation, offer prize purses competitive with regional events ($500,000+), and create multi-day festival programming around the race (desert camps, cultural performances, food festivals). Partner with international motorsport brands like Red Bull or regional sponsors seeking market entry. The February timing positions it perfectly as the season-opener before Middle Eastern heat sets in.

Early evidence suggests momentum: the 2026 rally saw increased participation from Karachi and Lahore’s motorsport clubs, and social media engagement reportedly tripled compared to previous years. With proper investment, this could become South Asia’s premier desert motorsport destination within three years.

2. Launch Year-Round Luxury Desert Camp Experiences

The Middle East’s success formula for desert tourism centers on high-value, low-volume luxury experiences. Dubai’s Al Maha Desert Resort commands $1,200+ per night. Oman’s desert camps attract affluent travelers seeking authentic Bedouin experiences with five-star amenities. Morocco’s Sahara luxury camps generate hundreds of millions annually.

Pakistan’s deserts offer comparable (often superior) cultural authenticity, night skies, and landscapes—without the premium pricing or tourist crowds. Yet permanent luxury camp infrastructure remains virtually nonexistent in Cholistan and Thar.

The economic rationale: Luxury desert tourism generates 5-10x more revenue per visitor than budget travel while minimizing environmental impact. A single 20-tent luxury camp in Cholistan could generate $2-3 million annually with strong margins, employing 40-60 local staff year-round. Scale this to 10-15 camps across both deserts, and you’re approaching $40-50 million in new high-value tourism revenue.

What this looks like: Private camps near Derawar Fort, Islamgarh Fort, and Mirpur Khas offering climate-controlled tents with en-suite bathrooms, gourmet cuisine featuring regional specialties, guided heritage tours, stargazing programs led by astronomers, and cultural immersion with local communities. Target international travelers willing to pay $400-800 per night—Chinese honeymooners, European adventure travelers, and wealthy Gulf visitors seeking new experiences.

The infrastructure playbook exists: partner with established luxury hospitality groups (Serena, Movenpick, or international brands like Six Senses exploring Pakistan), ensure sustainable water/waste management, and train local communities in hospitality. The Pakistan Tourism Development Corporation could offer investment incentives—tax holidays, expedited permitting—to attract private capital.

Companies like Concordia Expeditions and Karakoram Club have successfully pioneered luxury adventure tourism in Northern Pakistan. The model works; it simply needs desert application.

3. Establish the Thar Desert Train Safari

Rail-based desert tourism represents one of the most underutilized tools in Pakistan’s arsenal. India’s Palace on Wheels and Maharaja Express generate over $30 million annually, offering week-long luxury rail journeys through Rajasthan’s deserts, with tickets ranging from $4,000-15,000 per person.

Pakistan Railways operates routes directly through Thar Desert via the Mirpur Khas-Khokrapar line and near Cholistan via the Bahawalpur network—yet no tourist-oriented service exists.

The transformative potential: A Thar Desert Train Safari—even a modest 2-3 day service—could attract 10,000-15,000 passengers annually at $300-800 per ticket, generating $5-10 million in direct revenue while catalyzing hotel, guide, and craft sales along the route. Unlike road-based tourism, rail journeys appeal to older, wealthier demographics uncomfortable with desert driving.

2026 implementation blueprint: Pakistan Railways could refurbish 3-5 vintage carriages (dining car, sleeping cars with air conditioning, observation car) for weekend service from Karachi to Mirpur Khas and Nagarparkar, with stops for fort visits, desert walks, cultural performances, and local cuisine. Partner with private tour operators for off-train programming.

The timing aligns perfectly with Pakistan Railways’ reported focus on heritage tourism initiatives and the government’s infrastructure modernization agenda. Modest investment ($2-4 million for carriage refurbishment) could yield significant returns.

Successful models exist globally: Australia’s Ghan, Namibia’s Desert Express, and India’s multiple luxury trains prove the concept’s viability. Pakistan simply needs execution.

4. Develop Sustainable Agritourism and Eco-Villages

Thar Desert supports approximately 1.5 million people, primarily engaged in subsistence agriculture, livestock rearing, and traditional crafts. Rather than viewing tourism as separate from local livelihoods, integrated agritourism and eco-village models could generate income while preserving cultural authenticity.

Countries like Jordan and Morocco have successfully implemented desert community tourism that empowers local populations. Jordan’s Dana Biosphere Reserve generates $8-10 million annually while employing local Bedouins as guides, cooks, and craftspeople. Morocco’s Berber villages attract hundreds of thousands of tourists seeking authentic cultural immersion.

Pakistan’s advantage: Thari and Cholistan communities maintain living traditions—embroidery, pottery, music, cuisine—that appeal enormously to cultural tourism markets, especially Asian travelers valuing authenticity. The Thari horse breeding tradition, famous camel breeding, and indigenous agricultural techniques (traditional wells, drought-resistant farming) offer unique experiential tourism hooks.

Economic model: Establish 15-20 certified eco-villages across both deserts where tourists stay in traditional homes (modernized with basic amenities), participate in daily activities (bread-making, livestock care, craft workshops), and purchase handicrafts directly. Each village could host 500-1,000 visitors annually at $50-100 per day, generating $750,000-2 million directly into local pockets—distributed across 50-100 households per village.

The Thardeep Rural Development Programme has demonstrated success with sustainable development models in Thar. Scaling this with tourism components requires coordination between the Sindh Tourism Development Corporation, local NGOs, and communities to establish quality standards, training programs, and booking platforms.

Critical success factors: respect for local customs, women-led craft cooperatives controlling revenue, and strict environmental standards preventing overtourism. The goal is sustainable, high-value tourism that enriches rather than displaces.

5. Position Derawar Fort as a UNESCO World Heritage Site

Derawar Fort stands as one of Pakistan’s most visually spectacular historical sites—40 massive bastions rising 30 meters from Cholistan’s sands, visible from kilometers away. Yet international awareness remains minimal compared to India’s Jaisalmer Fort or Jordan’s Petra, both UNESCO World Heritage Sites generating hundreds of millions in tourism revenue.

UNESCO designation transforms tourism economics. According to research by Oxford Economics, World Heritage status increases visitor numbers by 30-50% on average and enables premium pricing for experiences. Jaisalmer alone attracts over 800,000 annual visitors, generating an estimated $150 million for local economies.

The Derawar opportunity: UNESCO inscription would legitimize international marketing, attract high-value travelers seeking World Heritage experiences, and justify increased investment in site conservation and visitor infrastructure. Current annual visitors are estimated at 50,000-80,000, primarily domestic day-trippers. UNESCO status could realistically push this to 150,000-200,000 within five years, with per-visitor spending increasing from $20-30 to $80-120.

2026 roadmap: Pakistan’s Department of Archaeology should prioritize preparing the UNESCO nomination dossier, emphasizing Derawar’s unique architecture (influenced by Rajput, Mughal, and local desert traditions), historical significance as a major Abbasi and later princely state stronghold, and the broader Cholistan cultural landscape. Include nearby Jamgarh, Islamgarh, and Maujgarh forts as a serial nomination representing desert fortress architecture.

Parallel investments required: improved road access from Bahawalpur (currently rough desert tracks), visitor center with interpretation facilities, conservation of fragile mud-brick structures, and community engagement ensuring local benefits. The return on investment is substantial—UNESCO sites become tourism anchors around which entire regional economies develop.

6. Create Desert Conservation and Wildlife Tourism

Beyond cultural and adventure tourism, Pakistan’s deserts harbor surprising biodiversity that could support lucrative conservation tourism markets. The Thar Desert supports the critically endangered Great Indian Bustard (fewer than 150 worldwide), blackbucks, desert foxes, and unique reptilian species. Cholistan’s Lal Sohanra National Park contains one of South Asia’s last remaining desert forest ecosystems.

Global conservation tourism generates over $120 billion annually, with travelers paying premiums to observe rare wildlife. Kenya’s conservancies demonstrate how community-based conservation creates economic incentives for wildlife protection while generating $350-500 million annually.

Pakistan’s conservation tourism potential: Develop premium wildlife safaris focusing on endangered species observation, birdwatching tours (Thar hosts significant migratory bird populations), and nighttime desert wildlife experiences. Price these at $150-300 per person daily—targeting serious wildlife enthusiasts, photographers, and eco-conscious travelers.

Establish community conservancies where local populations receive direct payments for wildlife protection and earn income from guiding, hospitality, and handicrafts. This model aligns conservation with economic development—when wildlife is worth more alive than dead, communities become fierce protectors.

2026 immediate actions: The Sindh Wildlife Department and Punjab Wildlife & Parks Department should partner with international conservation organizations (WWF, IUCN) to develop wildlife tourism products, train local communities as wildlife guides and trackers, and market Pakistan’s desert ecosystems to international nature tourism operators. Investment in research stations that welcome eco-tourists could generate funding while promoting conservation.

Recent reports indicate the Sindh government has shown renewed interest in Thar biodiversity conservation. Monetizing this through high-value tourism creates sustainable funding for conservation programs.

7. Invest in Digital Infrastructure and Virtual Previews

Pakistan’s tourism marketing suffers from a fundamental problem: expectation gap. International perceptions of Pakistan (security concerns, lack of tourism infrastructure) diverge dramatically from on-ground reality (improving security, stunning undiscovered sites). For desert tourism specifically, potential visitors simply don’t know these destinations exist.

Digital infrastructure solves this through immersive previews that overcome skepticism. Virtual reality tours, 360-degree videos, high-quality documentary content, and strategic influencer partnerships can showcase Pakistan’s deserts to global audiences at minimal cost.

The business case: Digital marketing delivers extraordinary ROI for emerging destinations. Tourism Australia’s “$150 million campaign” generated over $430 million in incremental tourism revenue. Jordan’s strategic digital marketing helped grow tourism from $3 billion (2012) to over $5.5 billion (2019).

Pakistan’s 2026 digital strategy:

- Virtual reality previews: Create VR experiences of Cholistan Rally, Derawar Fort sunset, Thar village stay, and desert camping. Distribute through Google Expeditions, travel platforms, and international tourism exhibitions.

- Influencer partnerships: Invite 50-100 international travel influencers, bloggers, and YouTubers (combined following 100+ million) for subsidized desert experiences. Their authentic content reaches demographics unreachable through traditional advertising.

- Professional video content: Produce BBC/Netflix-quality mini-documentaries on desert culture, wildlife, and adventure opportunities. License to streaming platforms and leverage for tourism marketing.

- Interactive booking platform: Develop a centralized booking system for desert experiences (luxury camps, homestays, guided tours) with secure payment, reviews, and customer support—addressing the “how do I actually book this?” problem.

The Pakistan Tourism Development Corporation should partner with Pakistani tech talent (leveraging the country’s strong digital services sector) and international tourism marketing agencies. Investment of $3-5 million in professional digital content could realistically generate $30-50 million in new tourism bookings within 18-24 months.

8. Establish Desert Adventure Tourism Certifications

Adventure tourism—one of the fastest-growing segments globally, worth over $680 billion—requires safety, quality standards, and professional certification to attract international markets. Currently, Pakistan’s desert adventure offerings (dune bashing, camel treks, sandboarding, desert trekking) lack standardized safety protocols and operator certification.

This isn’t merely bureaucratic; it’s economic. International travelers and tour operators require proof of safety standards before booking. Professional certification enables premium pricing—certified guides command 2-3x higher rates than uncertified operators.

Implementation model: The Pakistan Tourism Development Corporation, in partnership with international adventure tourism associations (Adventure Travel Trade Association), should establish:

- Desert guide certification programs: 200-hour training covering navigation, first aid, cultural sensitivity, environmental ethics, and customer service. Certify 500-1,000 guides across both deserts by end of 2026.

- Operator licensing standards: Safety equipment requirements, insurance mandates, environmental protocols, and regular inspections for companies offering desert tours.

- Equipment rental regulations: Certified 4×4 vehicles for dune bashing, safety-compliant sandboarding equipment, and standardized camel welfare protocols.

Economic impact: Professionalized adventure tourism enables marketing to international operators who pre-book group tours. A single UK or European adventure travel company might send 500-1,000 clients annually at $1,500-3,000 per person—but only to certified, insured operators. Certification unlocks $20-40 million in potential international adventure tourism revenue.

New Zealand’s adventure tourism industry—worth $4.2 billion annually—demonstrates how rigorous safety standards become a competitive advantage rather than a burden. Pakistan should follow this playbook.

9. Develop Desert Arts, Crafts, and Cultural Festivals

Cultural tourism represents Pakistan’s most authentic competitive advantage. Thari and Cholistan communities produce exceptional handicrafts—embroidered textiles, pottery, traditional jewelry, leather goods—and possess rich musical traditions (folk songs, instruments like the morchang) that are completely unknown internationally.

Global cultural tourism generates over $280 billion annually. India’s Pushkar Camel Fair attracts 200,000+ visitors and generates $40-50 million for local economies. Morocco’s cultural festivals drive billions in tourism spending.

Pakistan’s cultural festival opportunity:

- Cholistan Cultural Festival (February, aligned with Desert Rally): Week-long celebration featuring traditional music, dance, camel exhibitions, craft bazaars, culinary festivals showcasing Seraiki and Punjabi desert cuisine, and fort illuminations. Target: 50,000-75,000 attendees generating $8-12 million.

- Thar Heritage Festival (November-December, cooler season): Similar model celebrating Thari culture, featuring folk music competitions, women’s craft cooperatives, traditional sports (camel racing, horse exhibitions), and food courts. Target: 30,000-50,000 attendees generating $5-8 million.

Beyond festivals, establish permanent craft villages where tourists observe artisans at work and purchase directly—similar to Rajasthan’s craft villages that generate hundreds of millions annually. Ensure women control craft cooperative revenues, as they’re primary artisans in many traditional crafts.

Quality control critical: Establish Geographical Indication (GI) status for Thari embroidery and Cholistan textiles (like India’s GI-protected crafts), enabling premium pricing and preventing cheap imitations. Market these internationally through partnerships with ethical fashion brands and luxury retailers.

Recent initiatives like the Tharparkar Cultural Festival demonstrate grassroots momentum. Government support—funding, marketing, infrastructure—could scale these to economically significant levels.

10. Implement Solar-Powered Sustainable Tourism Infrastructure

Infrastructure challenges—water scarcity, electricity unreliability, road access—represent primary barriers to desert tourism development. Traditional infrastructure solutions (grid extension, water pipelines) are cost-prohibitive for remote desert regions.

Solar-powered, sustainable infrastructure offers economically viable solutions while positioning Pakistan as a leader in eco-tourism. International travelers increasingly seek sustainable destinations—66% of travelers would pay more for sustainable options according to Booking.com research.

Practical applications:

- Solar microgrids: Power luxury desert camps, homestays, and facilities without grid dependency. Cost: $50,000-100,000 per installation. Already proven at remote tourism sites in Jordan, Namibia, and Chile.

- Solar water pumps and conservation: Efficient water management for tourism facilities using solar-powered desalination (brackish water treatment) and greywater recycling. Reduces water consumption by 60-70%.

- Solar-powered electric safari vehicles: For wildlife tourism and site visits, eliminating diesel generators’ noise and emissions. Tesla and BYD now produce affordable electric 4x4s suitable for desert conditions.

- Sustainable road access: Use innovative materials (recycled plastics mixed with aggregate) for all-weather desert roads, proven in Middle Eastern deserts.

Investment case: Solar infrastructure reduces operating costs by 40-60% versus diesel generators over 10 years, while “sustainable tourism” branding enables 15-20% premium pricing. A $30-40 million investment in sustainable infrastructure across 20-30 tourism sites could support an industry generating $150-200 million annually within five years.

The Asian Development Bank and World Bank have expressed interest in financing Pakistan’s sustainable tourism infrastructure. The funding exists; execution requires coordinated proposals from provincial tourism departments.

The Economic Road Ahead

Pakistan’s desert tourism potential isn’t speculative—it’s proven by comparable success stories globally. Rajasthan’s deserts contribute over $12 billion annually. Dubai built a $45 billion tourism economy on less dramatic desert landscapes. Jordan’s desert regions generate billions while hosting similar security challenges Pakistan once faced.

The mathematics are compelling: if Pakistan captured merely 10% of Rajasthan’s desert tourism market, that would add $1.2 billion annually—25-30% growth over current total tourism revenue. Scale to Dubai-comparable levels (accounting for Pakistan’s larger population and equivalent infrastructure), and you’re approaching $5-8 billion in desert-driven tourism revenue potential by 2030.

These ten strategies require coordinated implementation across federal and provincial governments, private sector investment, and community engagement. The total capital investment needed—approximately $150-250 million across all initiatives—is modest compared to potential returns. Tourism multiplier effects (every $1 in tourism generates $2-3 in broader economic activity) mean actual economic impact could reach $10-20 billion over five years.

The 2026 moment is critical. Global tourism is recovering strongly post-pandemic, with travelers seeking new destinations. Pakistan’s improved security environment, growing international engagement (hosting international cricket, diplomatic reengagement), and infrastructure improvements create unprecedented opportunities.

Political will remains the primary requirement. The federal government’s stated commitment to tourism development must translate into policy reforms: simplified visa procedures (e-visa expansion), tourism infrastructure investment, public-private partnership frameworks, and sustained marketing budgets.

For investors—both Pakistani and international—desert tourism offers exceptional returns in an undervalued market. For local communities, it represents sustainable income diversification from agriculture. For Pakistan’s national economy, it’s a foreign exchange generator requiring minimal imports.

The deserts of Cholistan and Thar have patiently waited centuries to reveal their economic potential. In 2026, with strategic vision and coordinated execution, Pakistan can finally unlock the prosperity hidden in the sands.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Indonesia, Southeast Asia’s largest economy, has committed to importing up to 150 million barrels of Russian crude oil through the end of 2026, a deal that goes well beyond emergency crisis management and increasingly resembles a deliberate, multi-year repositioning of the country’s energy security architecture away from a Middle East supply base that the Strait of Hormuz conflict has exposed as dangerously concentrated.

The agreement, finalized after President Prabowo Subianto‘s April visit to Moscow for direct talks with President Vladimir Putin, involves Russia supplying 100 million barrels of oil at a preferential price, with a further 50 million barrels available if Indonesia’s needs escalate, according to reporting from The Moscow Times. Hashim Djojohadikusumo, the president’s brother and a senior economic adviser, confirmed Indonesia has also secured Russian government commitment to store up to 150 million barrels domestically as a buffer against future volatility.

Why Indonesia Cannot Wait Out the Crisis

Indonesia’s exposure to Middle East supply disruption is structural rather than incidental. The country produces roughly 577,000 barrels of crude per day, according to May 2026 figures — well below the government’s 610,000 barrel target and a fraction of the roughly 1.5 million barrels per day the country produced in the 1990s, before mature field decline eroded domestic output, according to analysis published by OilPrice.com. Against consumption running near 1.6 million barrels per day, Indonesia faces a persistent daily supply deficit approaching one million barrels, forcing continuous reliance on imports for both crude and refined products.

Energy and Mineral Resources Minister Bahlil Lahadalia has been explicit about the scale of this dependence, noting Indonesia requires roughly 300 million barrels of imported crude annually while holding strategic reserves sufficient for only 21 to 23 days of consumption — a dangerously thin buffer for an economy of Indonesia’s size, according to reporting cited by OilPrice.com’s earlier coverage. Roughly 20-25% of Indonesia’s crude imports have historically transited the Strait of Hormuz, a route the ongoing conflict has rendered unreliable at precisely the moment global oil markets can least absorb additional supply shocks.

From Emergency Waiver to Structural Partnership

The diplomatic and commercial mechanics enabling this shift trace back to a US sanctions waiver for Russian crude issued on March 12, 2026 — a decision that, according to OilPrice.com’s analysis, effectively acknowledged that Asia could not balance its oil market without Russian barrels during a major Middle Eastern supply disruption. Successive extensions of that waiver have since encouraged regional buyers to treat Russian crude not merely as emergency supply, but as a legitimate, ongoing tool of energy security — a reframing with significant implications for how Asian governments approach sanctioned commodities going forward.

Indonesia’s pivot did not emerge in isolation. Rystad Energy analyst Prateek Panday characterized the country’s strategy as grounded in supply economics, refinery compatibility, and medium-term energy security logic rather than opportunistic crisis response, a framing echoed by analysts at Indonesia’s own Strategic and Economics Action Institution, who described the approach as a deliberate effort to reduce exposure to a single, highly escalation-sensitive supply cluster. Indonesia became a full BRICS member in January 2025 and subsequently signed a free-trade agreement with the Eurasian Economic Union, diplomatic groundwork that made the current energy partnership commercially and politically easier to execute than it would have been even eighteen months earlier.

Indonesia is far from alone in this recalibration. The Philippines began importing Russian crude under the same US waiver in March 2026, with state oil company Petron purchasing 2.5 million barrels in its first such deal since 2021 and receiving three cargoes across March and May. Vietnam has reportedly held its own talks with Moscow since March regarding a potential start to Russian oil imports — suggesting a broader regional realignment is underway across Southeast Asia rather than an isolated Indonesian policy choice.

Refinery Compatibility Remains the Critical Variable

Indonesia’s state oil company Pertamina has signaled openness to the deepening relationship while flagging a genuine technical constraint: compatibility between Russian crude grades and Pertamina’s existing refinery configuration. Pertamina spokesperson Fadjar Djoko Santoso (“Baron”) confirmed the company would conduct further studies on processing Russian crude, noting that refinery modernization efforts are expected to eventually give Pertamina’s facilities the flexibility to handle a broader range of crude types, according to reporting from the New Straits Times.

Early shipments offer a preview of the compatibility challenge. Only two vessels carrying Russian crude reached Indonesia in the six months preceding the Moscow summit, each transporting roughly 700,000 barrels of Sakhalin Blend — a light, sweet crude with an API gravity around 45 degrees and low sulfur content that makes it well suited to gasoline-oriented refining, according to OilPrice.com’s analysis. Scaling from two modest cargoes to a 150-million-barrel annual commitment will require substantially more logistics infrastructure, refinery testing, and shipping capacity than the current relationship has yet demonstrated.

Beyond Oil: A Broader Energy Alignment With Moscow

The Prabowo-Putin summit extended well beyond crude oil supply. Indonesia is separately exploring the development of floating nuclear power plants in partnership with Russian state nuclear company Rosatom, with CEO Alexey Likhachev describing commercial discussions following what he characterized as strong Indonesian interest in nuclear technology, according to reporting from Tempo. Indonesian Foreign Minister Sugiono has framed nuclear cooperation with Russia as part of a broader push toward energy self-sufficiency within three years, while stressing that any partnership must prioritize technology transfer and adherence to international safety standards.

Indonesia is also negotiating liquefied petroleum gas imports from Russia to address a widening domestic supply gap — LPG demand is projected to reach 10 million tons in 2026 against domestic production capacity of just 1.6 million tons, according to Minister Lahadalia, a gap previously filled predominantly by US and Middle Eastern suppliers whose reliability the current conflict has called into question.

What This Means for Global Energy Diplomacy

Indonesia’s pivot illustrates a broader pattern reshaping global energy trade in 2026: sanctions architecture designed around a binary compliant-versus-non-compliant framework is proving less durable when a major regional supply disruption forces large importing economies to weigh energy security against geopolitical alignment. What began as an exceptional, waiver-dependent response to the Middle East crisis is increasingly hardening into formal government-to-government infrastructure — storage agreements, refinery studies, and nuclear cooperation — that will likely persist well beyond whatever timeline the underlying Strait of Hormuz disruption eventually follows.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

On a muggy Tuesday in March, Taro Yamamoto — operations director of a mid-sized Osaka precision-parts maker — stepped off a flight into Ho Chi Minh City for the third time in six months. He wasn’t scouting for components. He was scouting for customers. His domestic order book had contracted for the fourth consecutive year. His shop floor was greying, and two machine operators had retired with no replacements in sight. Back in Tokyo, the Tokyo Stock Exchange’s new capital-efficiency requirements had made inaction financially untenable. Across Japan, thousands of mid-sized executives are making exactly this calculation. The destination is almost always the same. The logic, once you see the numbers, is difficult to argue with.

The Arithmetic of Decline: Japan’s Domestic Squeeze

Japan has been living with a slow-motion structural crisis for the better part of three decades. The country’s population has fallen from its 2008 peak of 128 million and, by government projections, is set to slide toward 88 million by 2065. More than 29% of Japanese citizens are already aged 65 or older, making Japan the most demographically aged major economy on earth, as the IMF’s Finance & Development journal has documented. The working-age share of the population — those between 15 and 64 — has already fallen below 60%, the lowest among G7 nations. An aging society, as the IMF bluntly put it, “consumes less than a young one.”

For large multinationals — Toyota, Sony, SoftBank — the pivot overseas happened long ago. Their international revenue insulated them. It’s the mid-tier, the thousands of companies with 50 to 500 employees that form the backbone of Japanese manufacturing, services, and distribution, where the pressure is now acute. These firms were built to serve domestic demand. And domestic demand is structurally, irreversibly shrinking.

Set against this backdrop, Southeast Asia’s growth rates read like an alternate universe. The Asian Development Bank, in its December 2025 Outlook, revised the region’s GDP forecasts upward: growth of 4.5% for 2025, with Vietnam projected to expand by 6.6%, the Philippines at around 6%, and Indonesia at 5%. The IMF, speaking at the ASEAN Summit in October 2025, put it plainly: ASEAN is the world’s fourth-largest economy, with a collective GDP exceeding $4 trillion, growing 25% faster than the global average. For a Japanese mid-sized firm watching its addressable market contract at home, those numbers are not an abstraction. They are a survival map.

Why are Japanese companies expanding into Southeast Asia?

Japanese mid-sized companies are expanding into Southeast Asia because of converging structural pressures: a shrinking domestic consumer base driven by demographic decline, Tokyo Stock Exchange governance reforms compelling capital efficiency, the China-plus-one supply-chain imperative, and Southeast Asia’s sustained GDP growth of 4.5–6.6% across key markets — offering volume that Japan’s home market can no longer supply.

1 — The Core Development: A New Wave of Japanese Mid-Sized Companies Heading to Southeast Asia

The outbound push among Japanese mid-sized companies into Southeast Asia is not a new phenomenon. What’s changed is its scale, its urgency, and critically, the profile of the businesses involved.

For decades, it was Japan’s manufacturing giants — Hitachi, Panasonic, Bridgestone — that staked early positions across Vietnam, Thailand, and Indonesia. Their supply chains came first; their back-office operations followed. The mid-tier watched from the sidelines, constrained by capital, language barriers, and a domestic comfort zone propped up by decades of steady, if modest, home-market demand. That comfort zone has now dissolved.

JETRO’s FY2025 global survey of Japanese companies operating overseas — covering 7,485 valid responses across 82 countries — found that 66.5% of Japanese-affiliated overseas companies expect to be profitable in 2025, rising for the second consecutive year. The direction of expansion intentions tells a clearer story: survey respondents signalled growing appetite for Southwest Asia and ASEAN, while China — once the region’s default destination — continues to lose ground. In China, the proportion of companies anticipating business expansion hit an all-time low. The appetite is shifting, and it’s shifting south.

The structural driver is the “China plus one” strategy, which, by 2026, has stopped being a strategy and started being an operating assumption. Sino-American trade tensions, periodic supply-chain shocks, and rising Chinese labour costs have pushed Japanese manufacturers to seek parallel production bases. Vietnam has emerged as the primary beneficiary, attracting Japanese automakers, electronics suppliers, and — increasingly — second-tier parts makers who once fed larger Japanese manufacturers. Thailand, with its mature automotive industrial base and 60-year-old Japanese manufacturing presence, continues to draw mid-sized component makers. Indonesia, with its population of 280 million and a PMI that hit a multi-month high of 53.6 in early 2025 according to S&P Global data, is drawing fresh interest from consumer-goods manufacturers seeking volume markets.

UNCTAD’s 2025 FDI Explorer data shows ASEAN inflows hit a record $225 billion in 2024, up 10%, even as Europe’s FDI collapsed and China’s fell 29%. The region absorbed capital when almost nowhere else did.

What’s different now is who is moving. It’s no longer primarily the large enterprise with a dedicated global-expansion team and a Singapore holding company. It’s the Osaka die-caster, the Nagoya food-equipment manufacturer, the Fukuoka logistics-software firm — businesses that, until recently, had neither the appetite nor the architecture for foreign operations.

2 — The Structural Logic: Why Southeast Asia, Why Now?

The question most analysts ask is why the timing. The answer is a convergence of four pressures that have, in 2025 and 2026, reached simultaneous critical mass.

What is driving Japanese mid-sized companies to expand into Southeast Asia?

Japanese mid-sized companies are expanding into Southeast Asia because of converging structural pressures: a shrinking domestic consumer base driven by demographic decline, Tokyo Stock Exchange governance reforms compelling capital efficiency, the China-plus-one supply-chain imperative, and Southeast Asia’s sustained GDP growth of 4.5–6.6% across key markets — offering volume that Japan’s home market can no longer supply.

First, the demographic arithmetic, already described, is irreversible on any business-relevant time horizon. Companies can adapt temporarily — through automation, productivity gains, pricing — but they cannot manufacture new Japanese consumers. The medium-term demand trajectory at home is fixed. Growth, if it comes, must come from somewhere else.

Second, the TSE’s corporate governance overhaul — which since 2023 has placed intense scrutiny on companies trading below book value — has created a new accountability mechanism. Japanese mid-sized firms, traditionally patient with low returns, are now under pressure from institutional investors to demonstrate capital efficiency. Overseas expansion, with its attendant revenue diversification, has become a credible answer to that pressure. As documented by analysts writing for Insignia Business Review, the TSE’s push on price-to-book ratios is “forcing Japanese companies to think differently about partnerships, including those with international firms.”

Third, U.S. tariff policy has injected a new and urgent variable. Japanese manufacturers heavily embedded in Chinese supply chains face cost exposure that’s now structural, not cyclical. The premium on supply-chain geographic diversification has risen sharply since the Trump administration’s tariff expansions, and ASEAN — with its favourable trade agreements, including RCEP and CPTPP — offers a route around the worst of the exposure.

Fourth, and perhaps least discussed, is the sheer scale of Southeast Asia’s consumer base. The region’s middle class is expanding at a rate that has no parallel in Japan’s recent history. J.P. Morgan research has projected the internet economy across six key ASEAN markets approaching $360 billion in gross merchandising value. For a mid-sized Japanese food manufacturer, a health-care-products company, or a retail-concept operator, that is not a distant opportunity. It’s a currently accessible, rapidly deepening market — and Japanese brands, given the cultural cachet they carry across the region, start with a significant standing advantage.

3 — Implications and Second-Order Effects

The shift carries consequences that extend well beyond the balance sheets of individual companies.

For Japan itself, the most immediate concern is what economists sometimes call the “hollowing out” risk. When large Japanese manufacturers moved production offshore in the 1990s, domestic suppliers suffered. If the current wave of mid-sized firms follows not just with production but with their management, R&D, and commercial operations, the domestic economic base could erode further. Japan’s Ministry of Economy, Trade and Industry has acknowledged this tension in its 2025 White Paper on International Economy and Trade, which frames overseas expansion as necessary for value creation while simultaneously signalling concern about domestic industrial capacity.

For Southeast Asian host economies, the implications are broadly positive but uneven. Vietnam and Thailand, which have the most established Japanese industrial infrastructure, are best positioned to absorb further waves of investment quickly. Indonesia faces more complex challenges: its logistics infrastructure, while improving, still lags Vietnam’s in efficiency for export-oriented manufacturing. Malaysia, meanwhile, is seeing a particular surge — S&P Global’s 2025 Reshoring Special Report found that 28% of Malaysian manufacturers reported increased demand tied to reshoring, up sharply from 20% in 2024, with medium-sized firms particularly optimistic.

For the broader regional trade architecture, the Japanese mid-sized firm’s arrival accelerates something that was already underway: the transformation of ASEAN from a primarily large-enterprise investment zone to a genuine habitat for mid-market global capital. That shift has compounding effects. Japanese SMEs bring with them supplier relationships, technology transfer, and operational know-how that seed local industrial ecosystems. In Vietnam’s industrial provinces, the downstream effect of Japanese mid-tier manufacturers has been the emergence of local sub-suppliers and component fabricators that did not exist a decade ago.

There’s a currency dimension, too, that shouldn’t be underplayed. The yen’s extended period of weakness — a consequence of the Bank of Japan’s historically accommodative stance and the slow pace of normalisation — has paradoxically made overseas investment cheaper in yen terms, even as it erodes repatriated profits. Companies with significant local-currency revenue in baht, dong, or rupiah are, in effect, hedging against further yen weakness. The financial calculus has shifted in ways that favour commitment over caution.

4 — The Counterarguments: Not Every Mid-Sized Firm Should Go

The enthusiasm carries real risks, and anyone advising Japanese mid-sized firms on Southeast Asian expansion would be negligent to paper over them.

The first is operational. Large corporations move to ASEAN with teams of experts, legal counsel, and institutional knowledge accumulated over decades. Mid-sized firms typically don’t. The complexities of establishing a subsidiary in, say, Indonesia — navigating local-ownership rules, labour regulations, tax treaties, and sometimes opaque licensing processes — can overwhelm companies that lack dedicated international capacity. Research published in the journal Asia Pacific Business Review documented that some Japanese firms that expanded into Thailand and Indonesia in the mid-2010s subsequently withdrew, citing rising labour costs, talent shortages, and intensifying competition from Western companies. Those conditions have not uniformly improved.

The second risk is the competitive environment itself. Japanese mid-sized firms arriving in Vietnam or Indonesia in 2026 are not entering empty markets. Chinese manufacturers — displaced by tariffs or simply pursuing their own internationalisation — are competing aggressively for the same factory sites, the same skilled workers, and the same distribution channels. The JETRO survey noted that concerns about “intensifying competition with Chinese companies” ranked among the top worries for Japanese manufacturers in Asia.

Third, the World Bank’s April 2026 East Asia and Pacific update flagged that Southeast Asian growth itself faces a slower trajectory — projecting a regional moderation to 4.2% in 2026, down from 5%, partly because of the conflict in the Middle East and its effect on energy prices. Thailand, in particular, is struggling, with forecast growth of just 1.3% in 2026, dragged by high household debt and political uncertainty. A company that entered Thailand’s market betting on strong consumer growth may find the reality more complicated than the prospectus suggested.

The picture is more complicated still for firms without a clear competitive differentiation. Japanese brand cachet travels far in Southeast Asia, but it is not infinite. It doesn’t automatically compensate for a product that’s 30% more expensive than a local equivalent, or a distribution model that was built for Japanese retail formats and doesn’t translate.

Closing: The Point of No Return

There is something close to inevitability in what is happening. Japan’s mid-sized companies are not choosing to internationalise so much as accepting that the alternative — remaining anchored to a structurally contracting domestic base — is its own form of decline. The question isn’t whether to move, but whether to move with enough preparation and self-awareness to avoid the mistakes of those who moved before.

Southeast Asia will absorb this capital. The region has the demographic momentum, the infrastructure investment trajectory, and the trade architecture to sustain Japanese mid-tier ambitions for at least the next decade. What the region cannot guarantee is that every company that arrives will thrive. The mid-sized firms that succeed will be those that treat the region as a set of distinct, demanding markets — not as a single, grateful alternative to the one they left behind.

Japan’s corporate middle is heading south. The question that will define the next chapter is not whether, but how well.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

On 28 February 2026, the first US-Israeli strikes on Iran effectively closed the Strait of Hormuz to normal shipping. Within six weeks, Brent crude had recorded its largest single-month price rise in recorded history, surging roughly 65 percent to above $106 a barrel. For most of the world, that was a severe financial shock. For South-east Asia — a region of 700 million people that depends on the Middle East for 56 percent of its total crude oil imports — it was something closer to a structural emergency. Governments reached for the familiar toolkit: subsidies, price caps, rationing. It isn’t working.

The timing is particularly brutal. South-east Asia had entered 2026 on what looked like solid ground. The region had weathered US tariffs better than feared; export front-loading and resilient private consumption kept growth humming at roughly 4.7 percent across developing ASEAN in 2025. Inflation was subdued. Central banks had room to manoeuvre.

That cushion is now gone.

The World Bank’s April 2026 East Asia and Pacific Economic Update projects regional growth slowing to 4.2 percent this year, down from 5.0 percent in 2025, with the energy shock explicitly cited alongside trade barriers as a primary drag. The IMF, for its part, forecasts that inflation across emerging Asia will climb from 1.1 percent in 2025 to 2.6 percent in 2026 — a projection that assumes the most acute phase of supply disruption ends by May. Few analysts believe it will.

The Southeast Asian Energy Shock: What Hit, and Why It Hurts So Much

The mechanism is straightforward, even if the scale is not. The Strait of Hormuz — a 33-kilometre passage between Iran and Oman — serves as the transit point for roughly 20 percent of the world’s daily seaborne oil and up to 30 percent of global LNG shipments. When that artery seizes, South-east Asia feels it fastest. The region imports nearly all of its crude; it holds strategic reserves measured in weeks, not months. Most ASEAN economies sit on fewer than 30 days of emergency oil stocks. The Philippines and Thailand are exceptions, with roughly 45 and 106 days respectively — still a narrow buffer against a conflict that US officials privately suggest could persist through year-end.

The impact of the Southeast Asian energy shock has been immediate and sharp. According to an analysis by JP Morgan cited widely across regional media, the Philippines declared a national energy emergency after gasoline prices more than doubled. Indonesia and Vietnam introduced fuel rationing. Thailand’s fisheries sector — an industry that generates billions in export revenue and employs hundreds of thousands — began shutting down as marine diesel costs became unviable.

The fiscal arithmetic compounds the pain. Fossil fuel subsidies across five major ASEAN economies — Indonesia, Malaysia, Thailand, Vietnam, and the Philippines — reached $55.9 billion, or 1.3 percent of combined GDP, in 2024, before the current crisis. Indonesia alone spent the equivalent of 2.3 percent of GDP on explicit fuel price support. Now, with Brent crude above $100 and the World Bank’s commodity team forecasting an average of $86 a barrel across 2026 even in a best-case recovery scenario, those subsidy bills are rising faster than governments budgeted for.

The ASEAN Economic Community Council convened an emergency session on 30 April 2026, held by videoconference, in which ministers cited “growing instability along key maritime routes” as driving volatility in energy prices and sharply increasing freight, insurance, and logistics costs. The communiqué warned of spillover effects on food security and business confidence, particularly for small and medium enterprises — the backbone of most ASEAN economies.

Why Policy Options Are Narrowing — and Who Is Most Exposed

The question South-east Asian governments face isn’t whether the energy shock hurts. It’s whether they have enough fiscal and monetary space to absorb it.

The answer varies sharply by country, and understanding those differences matters for anyone assessing the ASEAN investment landscape.

Which Southeast Asian countries are most vulnerable to oil price spikes? Thailand and the Philippines face the gravest pressure. Both import nearly all their fuel, lack meaningful commodity export revenue to offset higher import bills, and carry domestic vulnerabilities — elevated household debt in Thailand, structural current-account exposure in the Philippines — that amplify the macro damage. Indonesia and Malaysia are better insulated: coal exports and palm-oil revenues provide a partial natural hedge, and their domestic energy production reduces import dependency. Vietnam sits somewhere in between, with growing industrial exposure but a more activist state ready to deploy price stabilisation funds.

Thailand’s predicament illustrates the bind. The country’s National Economic and Social Development Council reported GDP growth of 1.9 percent year-on-year in the first quarter of 2026, well below the government’s own 2.6 percent projection, even as tourist arrivals held firm. The Oil Fuel Fund empowers Bangkok to subsidise pump prices during international oil spikes — but that mechanism has a fiscal cost, and with the budget already stretched, sustaining it without cutting other expenditure is a genuine political and economic dilemma. The World Bank forecast that Thailand’s full-year growth will slow to just 1.3 percent in 2026, down from 2.4 percent last year — the weakest major economy in the region by a significant margin.

Central banks are caught in a similar bind. The IMF’s Andrea Pescatori put it plainly in April: the energy shock is “raising inflation, weakening external balances, and narrowing policy options.” Cutting rates to support growth risks stoking inflation and pressuring currencies already weakened by the dollar’s safe-haven surge. Raising rates to defend currencies risks tipping fragile economies into contraction. The Philippine peso and Thai baht have both depreciated this year, which means the energy shock arrives at an exchange rate that makes every dollar-denominated barrel of oil cost even more in local terms.

That is not a problem easily subsidised away.

Implications: Fiscal Strain, Food Prices, and the Coal Comeback

The second-order effects of the ASEAN oil crisis are where the real long-term damage accumulates.

The most immediate downstream risk is food inflation. Higher marine fuel costs don’t just shut down Thailand’s fisheries; they push up the price of fish for 70 million Thais and complicate the region’s food-export economics. Fertiliser prices — heavily tied to natural gas — are rising in parallel. Vietnam, a major rice and agricultural exporter, is watching input costs erode margins across its farm sector. Thailand, according to reports cited in regional media, is even exploring fertiliser purchases from Russia to manage costs — a geopolitical trade-off that puts ASEAN countries in an awkward position as the EU and US press them to limit economic lifelines to Moscow.

Then there’s the energy mix reversal. Vietnam and Indonesia are re-optimising towards coal to reduce LNG import dependence — a rational short-term response that directly undermines both countries’ climate commitments and their eligibility for concessional green finance. The IEA’s 2026 Energy Crisis Policy Response Tracker documents this shift across multiple Asian economies, noting a wave of emergency fuel-switching from gas to coal-powered electricity generation.

For businesses, the pressure is both direct and indirect. Singapore Airlines reported a 24 percent increase in fuel costs year-on-year in recent filings, a squeeze that hits one of the region’s most profitable and strategically important carriers. Logistics firms across the region are repricing contracts, with knock-on effects for the export-oriented manufacturers in Vietnam, Malaysia, and Thailand who depend on predictable freight rates to compete in global supply chains.

The Asian Development Bank’s April 2026 Outlook projects inflation across developing Asia rising to 3.6 percent this year, as higher energy prices feed through to consumer prices. For the urban poor across Manila, Bangkok, and Jakarta, who spend a disproportionate share of income on transport and food, that number translates into a genuine fall in real living standards.

The Case for Optimism — and Why It’s Incomplete

It would be unfair to write off ASEAN’s resilience entirely. The region has navigated severe external shocks before — the Asian financial crisis of 1997, the global financial crisis of 2008, the Covid-19 supply chain fractures of 2020–21 — and each time it emerged with stronger institutional frameworks and deeper reserve buffers.

The OMFIF notes that ASEAN+3 entered 2026 from a position of relative strength, with growth of 4.3 percent in 2025 and inflation at just 0.9 percent — conditions that gave central banks some room to absorb a supply shock without immediately tightening. Several governments are using the crisis to accelerate structural shifts that were already overdue: Indonesia is pushing its B50 biodiesel programme, blending palm-oil biodiesel with conventional diesel to reduce petroleum imports. Vietnam is expanding petroleum reserves and evaluating renewable energy deployment. Malaysia is prioritising industrial upgrading.

Some economists argue, too, that the region’s AI-related export boom — identified by the World Bank as a “bright spot” in 2025, particularly in Malaysia, Thailand, and Vietnam — provides a partial growth offset that didn’t exist in previous energy shock episodes. Semiconductor and electronics exports are less fuel-intensive than traditional manufacturing, offering a degree of natural hedge.

Yet this optimism has limits. Most of the structural diversification being contemplated operates on timescales of years, not months. Biodiesel programmes and renewable energy buildouts don’t lower this quarter’s fuel bill. And the fiscal space being consumed by subsidy programmes today is space that won’t be available for infrastructure investment, healthcare, or education tomorrow. Analysts at Fulcrum SGP, reviewing the region’s policy responses, concluded that “the reactive nature of most policy responses risks locking the region into structural fragility” — a diagnosis that captures the fundamental tension between managing the immediate crisis and building long-term resilience.

The Reckoning That Keeps Getting Deferred

South-east Asia’s energy vulnerability didn’t begin on 28 February 2026. For decades, the region’s economies grew rapidly on a diet of cheap imported oil, building infrastructure and industrial capacity calibrated to abundant fossil fuels and open sea lanes. The Hormuz closure has made visible what was always structurally true: that a region of 700 million people, with combined GDP approaching $4 trillion, had built its prosperity on a supply chain that runs through a 33-kilometre passage controlled by a third party.

Governments are responding, as governments do, with the instruments closest to hand — subsidies, rationing, emergency reserves. Those measures will blunt some of the pain. They won’t resolve the underlying architecture.

The World Bank’s Aaditya Mattoo put the challenge with unusual directness in launching the April update: “Measured support for people and firms could preserve jobs today, and reviving stalled structural reforms could unleash growth tomorrow.” The operative word is “stalled.” The reforms — energy diversification, grid integration, renewable deployment — were the right answer before the crisis. They remain the right answer during it. The distance between knowing that and doing it, at pace and at scale, is where South-east Asia’s next decade will be decided.

The Strait of Hormuz may reopen. The structural exposure won’t close itself.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Canada’s Central Bank Holds the Line at 2.25% as Tariffs and a Middle East Oil Shock Collide

China Economy 2026: Property Crash Meets Record AI-Driven Export Boom

Pakistan IMF Deal 2026: Third Review Cleared, Budget 2026-27 and Inflation Outlook

Bank of England Interest Rates 2026: Why Inflation Is Rising Again Despite a Hold

Fed Ends Forward Guidance: What Kevin Warsh’s Policy Shift Means for Markets

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Russia Raised VAT to 22% to Pay for the War. It Still Isn’t Enough

Six Straight Quarters of Falling Prices: Inside China’s Deflation Trap

Canada Missed Its CUSMA Deadline. Now Its Economy Is “On Pause”

UK Stagflation 2026: Why the Bank of England May Hike Rates, Not Cut Them

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Nasdaq Tumbles 4% as Chip and Memory Stocks Sink: A $1.2 Trillion Wipeout

How to Fix Pakistan’s Debt Economy: A Structural Blueprint

Grinding the Already Ground: Pakistan’s Inflation Crisis

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

JPMorgan Cuts Anthropic AI Access in Hong Kong

Smash Capital Leads $200M Funding for Allen Control Systems

New Investment Super-Cycle: AI, Green Energy & Re-Shoring

Middle East Conflict Oil Prices: The $4 Surge Explained

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

Germany Rail Network Upgrade: Inside the €100bn Rescue Plan

The End of the Chatbot: Why OpenAI is Tearing Up Its Most Successful Product

The Global Sovereign Debt Crisis: Fiscal Strain in a High-Rate Era

Fiscal Policy under Pressure: High Debt, Rising Risks

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025