Asia

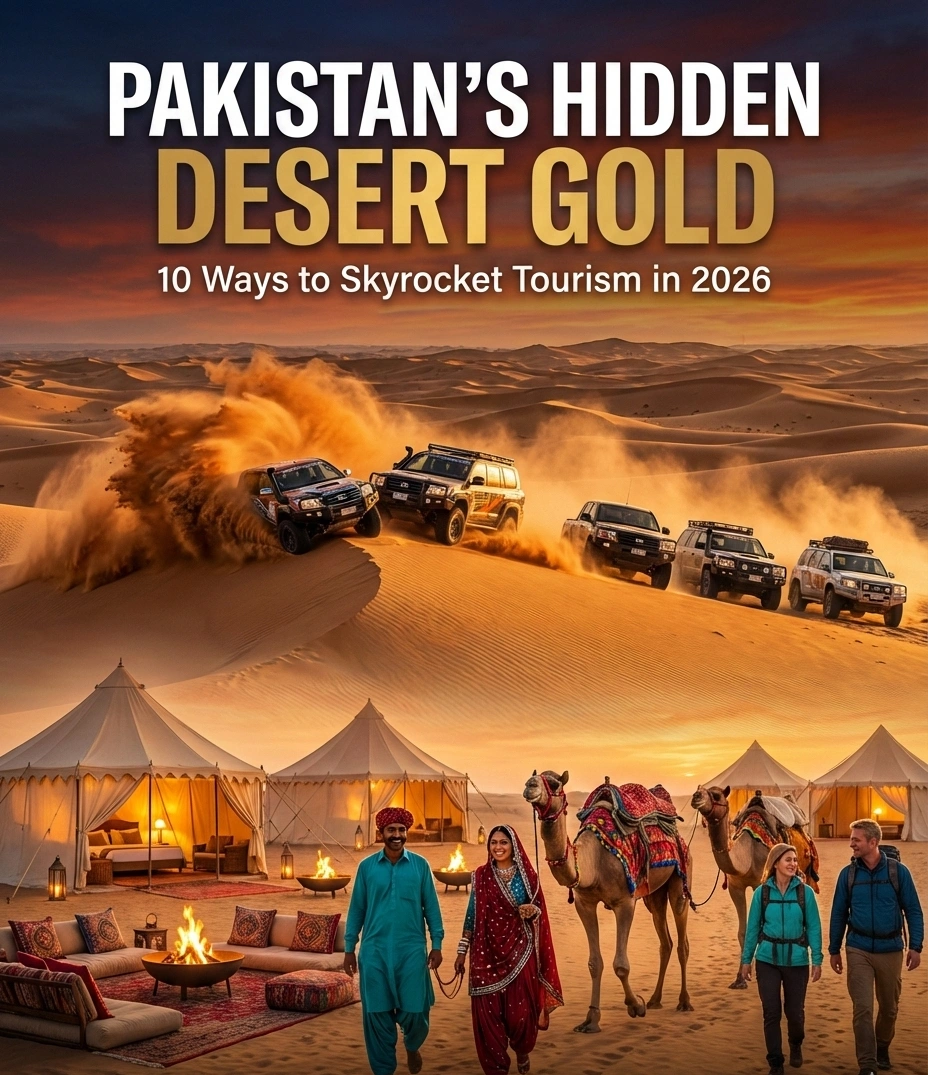

10 Ways to Boost Pakistan’s Tourism Economy in 2026 by Unlocking the Deserts of Cholistan and Thar

The sun rises over the Cholistan Desert, painting endless dunes in shades of amber and gold. A convoy of modified 4x4s kicks up plumes of sand as they race toward the horizon, while nearby, a camel caravan winds its way past ancient Derawar Fort, its 40 towering bastions standing sentinel over centuries of history. Meanwhile, 400 kilometers to the east, the Thar Desert’s “Rohi”—the land of shifting sands—comes alive with the rhythmic beats of traditional music as villagers prepare for the annual Tharparkar Cultural Festival.

These scenes aren’t from some distant fantasy. They’re the untapped reality of Pakistan’s desert economy in 2026—a sector that could transform the country’s tourism landscape if properly leveraged.

Pakistan’s tourism industry generated approximately USD 4.4-4.9 billion in 2025, welcoming around 965,000 international arrivals according to recent government estimates. Yet this represents merely a fraction of the country’s potential. The government has set an ambitious target of reaching $30-40 billion in annual tourism revenue—a goal that seems distant until you consider what neighboring regions have accomplished. Rajasthan’s desert tourism alone contributes over $12 billion annually to India’s economy, while Dubai transformed barren sands into a $45 billion tourism powerhouse.

Pakistan possesses comparable—arguably superior—raw materials: the 26,300 square kilometers of Cholistan (larger than Israel) and the 22,000 square kilometers of Thar (comparable to Slovenia). These deserts contain architectural marvels, biodiversity hotspots, vibrant indigenous cultures, and adventure tourism potential that remains criminally underutilized.

The question isn’t whether Pakistan’s deserts can drive economic growth. It’s how quickly stakeholders can implement the strategies to make it happen. Here are ten evidence-based, actionable approaches to unlock this sleeping giant in 2026.

1. Expand and Internationalize the Cholistan Desert Rally

The Cholistan Desert Rally returned in February 2026 after years of inconsistency, drawing thousands of domestic spectators and adventure enthusiasts to Derawar Fort. This annual motorsport event, organized by the Tourism Development Corporation of Punjab, represents Pakistan’s most established desert tourism brand—yet it operates at perhaps 20% of its potential.

Compare this to the Dakar Rally, which generates over $100 million in direct economic impact for host countries, or the Abu Dhabi Desert Challenge, which attracts 50+ international teams and global media coverage worth millions in destination marketing value. The Cholistan Rally, despite featuring challenging terrain that rivals any international desert race, remains largely unknown outside Pakistan.

The economic opportunity: Transforming Cholistan Rally into an FIA-sanctioned international motorsport event could generate $15-25 million annually in direct spending (participant fees, accommodation, logistics) plus exponentially greater media value. The infrastructure already exists—the 480-kilometer desert track, proximity to Bahawalpur’s hotels, and local support systems.

2026 action steps: The Punjab government should pursue FIA Desert Rally Championship accreditation, offer prize purses competitive with regional events ($500,000+), and create multi-day festival programming around the race (desert camps, cultural performances, food festivals). Partner with international motorsport brands like Red Bull or regional sponsors seeking market entry. The February timing positions it perfectly as the season-opener before Middle Eastern heat sets in.

Early evidence suggests momentum: the 2026 rally saw increased participation from Karachi and Lahore’s motorsport clubs, and social media engagement reportedly tripled compared to previous years. With proper investment, this could become South Asia’s premier desert motorsport destination within three years.

2. Launch Year-Round Luxury Desert Camp Experiences

The Middle East’s success formula for desert tourism centers on high-value, low-volume luxury experiences. Dubai’s Al Maha Desert Resort commands $1,200+ per night. Oman’s desert camps attract affluent travelers seeking authentic Bedouin experiences with five-star amenities. Morocco’s Sahara luxury camps generate hundreds of millions annually.

Pakistan’s deserts offer comparable (often superior) cultural authenticity, night skies, and landscapes—without the premium pricing or tourist crowds. Yet permanent luxury camp infrastructure remains virtually nonexistent in Cholistan and Thar.

The economic rationale: Luxury desert tourism generates 5-10x more revenue per visitor than budget travel while minimizing environmental impact. A single 20-tent luxury camp in Cholistan could generate $2-3 million annually with strong margins, employing 40-60 local staff year-round. Scale this to 10-15 camps across both deserts, and you’re approaching $40-50 million in new high-value tourism revenue.

What this looks like: Private camps near Derawar Fort, Islamgarh Fort, and Mirpur Khas offering climate-controlled tents with en-suite bathrooms, gourmet cuisine featuring regional specialties, guided heritage tours, stargazing programs led by astronomers, and cultural immersion with local communities. Target international travelers willing to pay $400-800 per night—Chinese honeymooners, European adventure travelers, and wealthy Gulf visitors seeking new experiences.

The infrastructure playbook exists: partner with established luxury hospitality groups (Serena, Movenpick, or international brands like Six Senses exploring Pakistan), ensure sustainable water/waste management, and train local communities in hospitality. The Pakistan Tourism Development Corporation could offer investment incentives—tax holidays, expedited permitting—to attract private capital.

Companies like Concordia Expeditions and Karakoram Club have successfully pioneered luxury adventure tourism in Northern Pakistan. The model works; it simply needs desert application.

3. Establish the Thar Desert Train Safari

Rail-based desert tourism represents one of the most underutilized tools in Pakistan’s arsenal. India’s Palace on Wheels and Maharaja Express generate over $30 million annually, offering week-long luxury rail journeys through Rajasthan’s deserts, with tickets ranging from $4,000-15,000 per person.

Pakistan Railways operates routes directly through Thar Desert via the Mirpur Khas-Khokrapar line and near Cholistan via the Bahawalpur network—yet no tourist-oriented service exists.

The transformative potential: A Thar Desert Train Safari—even a modest 2-3 day service—could attract 10,000-15,000 passengers annually at $300-800 per ticket, generating $5-10 million in direct revenue while catalyzing hotel, guide, and craft sales along the route. Unlike road-based tourism, rail journeys appeal to older, wealthier demographics uncomfortable with desert driving.

2026 implementation blueprint: Pakistan Railways could refurbish 3-5 vintage carriages (dining car, sleeping cars with air conditioning, observation car) for weekend service from Karachi to Mirpur Khas and Nagarparkar, with stops for fort visits, desert walks, cultural performances, and local cuisine. Partner with private tour operators for off-train programming.

The timing aligns perfectly with Pakistan Railways’ reported focus on heritage tourism initiatives and the government’s infrastructure modernization agenda. Modest investment ($2-4 million for carriage refurbishment) could yield significant returns.

Successful models exist globally: Australia’s Ghan, Namibia’s Desert Express, and India’s multiple luxury trains prove the concept’s viability. Pakistan simply needs execution.

4. Develop Sustainable Agritourism and Eco-Villages

Thar Desert supports approximately 1.5 million people, primarily engaged in subsistence agriculture, livestock rearing, and traditional crafts. Rather than viewing tourism as separate from local livelihoods, integrated agritourism and eco-village models could generate income while preserving cultural authenticity.

Countries like Jordan and Morocco have successfully implemented desert community tourism that empowers local populations. Jordan’s Dana Biosphere Reserve generates $8-10 million annually while employing local Bedouins as guides, cooks, and craftspeople. Morocco’s Berber villages attract hundreds of thousands of tourists seeking authentic cultural immersion.

Pakistan’s advantage: Thari and Cholistan communities maintain living traditions—embroidery, pottery, music, cuisine—that appeal enormously to cultural tourism markets, especially Asian travelers valuing authenticity. The Thari horse breeding tradition, famous camel breeding, and indigenous agricultural techniques (traditional wells, drought-resistant farming) offer unique experiential tourism hooks.

Economic model: Establish 15-20 certified eco-villages across both deserts where tourists stay in traditional homes (modernized with basic amenities), participate in daily activities (bread-making, livestock care, craft workshops), and purchase handicrafts directly. Each village could host 500-1,000 visitors annually at $50-100 per day, generating $750,000-2 million directly into local pockets—distributed across 50-100 households per village.

The Thardeep Rural Development Programme has demonstrated success with sustainable development models in Thar. Scaling this with tourism components requires coordination between the Sindh Tourism Development Corporation, local NGOs, and communities to establish quality standards, training programs, and booking platforms.

Critical success factors: respect for local customs, women-led craft cooperatives controlling revenue, and strict environmental standards preventing overtourism. The goal is sustainable, high-value tourism that enriches rather than displaces.

5. Position Derawar Fort as a UNESCO World Heritage Site

Derawar Fort stands as one of Pakistan’s most visually spectacular historical sites—40 massive bastions rising 30 meters from Cholistan’s sands, visible from kilometers away. Yet international awareness remains minimal compared to India’s Jaisalmer Fort or Jordan’s Petra, both UNESCO World Heritage Sites generating hundreds of millions in tourism revenue.

UNESCO designation transforms tourism economics. According to research by Oxford Economics, World Heritage status increases visitor numbers by 30-50% on average and enables premium pricing for experiences. Jaisalmer alone attracts over 800,000 annual visitors, generating an estimated $150 million for local economies.

The Derawar opportunity: UNESCO inscription would legitimize international marketing, attract high-value travelers seeking World Heritage experiences, and justify increased investment in site conservation and visitor infrastructure. Current annual visitors are estimated at 50,000-80,000, primarily domestic day-trippers. UNESCO status could realistically push this to 150,000-200,000 within five years, with per-visitor spending increasing from $20-30 to $80-120.

2026 roadmap: Pakistan’s Department of Archaeology should prioritize preparing the UNESCO nomination dossier, emphasizing Derawar’s unique architecture (influenced by Rajput, Mughal, and local desert traditions), historical significance as a major Abbasi and later princely state stronghold, and the broader Cholistan cultural landscape. Include nearby Jamgarh, Islamgarh, and Maujgarh forts as a serial nomination representing desert fortress architecture.

Parallel investments required: improved road access from Bahawalpur (currently rough desert tracks), visitor center with interpretation facilities, conservation of fragile mud-brick structures, and community engagement ensuring local benefits. The return on investment is substantial—UNESCO sites become tourism anchors around which entire regional economies develop.

6. Create Desert Conservation and Wildlife Tourism

Beyond cultural and adventure tourism, Pakistan’s deserts harbor surprising biodiversity that could support lucrative conservation tourism markets. The Thar Desert supports the critically endangered Great Indian Bustard (fewer than 150 worldwide), blackbucks, desert foxes, and unique reptilian species. Cholistan’s Lal Sohanra National Park contains one of South Asia’s last remaining desert forest ecosystems.

Global conservation tourism generates over $120 billion annually, with travelers paying premiums to observe rare wildlife. Kenya’s conservancies demonstrate how community-based conservation creates economic incentives for wildlife protection while generating $350-500 million annually.

Pakistan’s conservation tourism potential: Develop premium wildlife safaris focusing on endangered species observation, birdwatching tours (Thar hosts significant migratory bird populations), and nighttime desert wildlife experiences. Price these at $150-300 per person daily—targeting serious wildlife enthusiasts, photographers, and eco-conscious travelers.

Establish community conservancies where local populations receive direct payments for wildlife protection and earn income from guiding, hospitality, and handicrafts. This model aligns conservation with economic development—when wildlife is worth more alive than dead, communities become fierce protectors.

2026 immediate actions: The Sindh Wildlife Department and Punjab Wildlife & Parks Department should partner with international conservation organizations (WWF, IUCN) to develop wildlife tourism products, train local communities as wildlife guides and trackers, and market Pakistan’s desert ecosystems to international nature tourism operators. Investment in research stations that welcome eco-tourists could generate funding while promoting conservation.

Recent reports indicate the Sindh government has shown renewed interest in Thar biodiversity conservation. Monetizing this through high-value tourism creates sustainable funding for conservation programs.

7. Invest in Digital Infrastructure and Virtual Previews

Pakistan’s tourism marketing suffers from a fundamental problem: expectation gap. International perceptions of Pakistan (security concerns, lack of tourism infrastructure) diverge dramatically from on-ground reality (improving security, stunning undiscovered sites). For desert tourism specifically, potential visitors simply don’t know these destinations exist.

Digital infrastructure solves this through immersive previews that overcome skepticism. Virtual reality tours, 360-degree videos, high-quality documentary content, and strategic influencer partnerships can showcase Pakistan’s deserts to global audiences at minimal cost.

The business case: Digital marketing delivers extraordinary ROI for emerging destinations. Tourism Australia’s “$150 million campaign” generated over $430 million in incremental tourism revenue. Jordan’s strategic digital marketing helped grow tourism from $3 billion (2012) to over $5.5 billion (2019).

Pakistan’s 2026 digital strategy:

- Virtual reality previews: Create VR experiences of Cholistan Rally, Derawar Fort sunset, Thar village stay, and desert camping. Distribute through Google Expeditions, travel platforms, and international tourism exhibitions.

- Influencer partnerships: Invite 50-100 international travel influencers, bloggers, and YouTubers (combined following 100+ million) for subsidized desert experiences. Their authentic content reaches demographics unreachable through traditional advertising.

- Professional video content: Produce BBC/Netflix-quality mini-documentaries on desert culture, wildlife, and adventure opportunities. License to streaming platforms and leverage for tourism marketing.

- Interactive booking platform: Develop a centralized booking system for desert experiences (luxury camps, homestays, guided tours) with secure payment, reviews, and customer support—addressing the “how do I actually book this?” problem.

The Pakistan Tourism Development Corporation should partner with Pakistani tech talent (leveraging the country’s strong digital services sector) and international tourism marketing agencies. Investment of $3-5 million in professional digital content could realistically generate $30-50 million in new tourism bookings within 18-24 months.

8. Establish Desert Adventure Tourism Certifications

Adventure tourism—one of the fastest-growing segments globally, worth over $680 billion—requires safety, quality standards, and professional certification to attract international markets. Currently, Pakistan’s desert adventure offerings (dune bashing, camel treks, sandboarding, desert trekking) lack standardized safety protocols and operator certification.

This isn’t merely bureaucratic; it’s economic. International travelers and tour operators require proof of safety standards before booking. Professional certification enables premium pricing—certified guides command 2-3x higher rates than uncertified operators.

Implementation model: The Pakistan Tourism Development Corporation, in partnership with international adventure tourism associations (Adventure Travel Trade Association), should establish:

- Desert guide certification programs: 200-hour training covering navigation, first aid, cultural sensitivity, environmental ethics, and customer service. Certify 500-1,000 guides across both deserts by end of 2026.

- Operator licensing standards: Safety equipment requirements, insurance mandates, environmental protocols, and regular inspections for companies offering desert tours.

- Equipment rental regulations: Certified 4×4 vehicles for dune bashing, safety-compliant sandboarding equipment, and standardized camel welfare protocols.

Economic impact: Professionalized adventure tourism enables marketing to international operators who pre-book group tours. A single UK or European adventure travel company might send 500-1,000 clients annually at $1,500-3,000 per person—but only to certified, insured operators. Certification unlocks $20-40 million in potential international adventure tourism revenue.

New Zealand’s adventure tourism industry—worth $4.2 billion annually—demonstrates how rigorous safety standards become a competitive advantage rather than a burden. Pakistan should follow this playbook.

9. Develop Desert Arts, Crafts, and Cultural Festivals

Cultural tourism represents Pakistan’s most authentic competitive advantage. Thari and Cholistan communities produce exceptional handicrafts—embroidered textiles, pottery, traditional jewelry, leather goods—and possess rich musical traditions (folk songs, instruments like the morchang) that are completely unknown internationally.

Global cultural tourism generates over $280 billion annually. India’s Pushkar Camel Fair attracts 200,000+ visitors and generates $40-50 million for local economies. Morocco’s cultural festivals drive billions in tourism spending.

Pakistan’s cultural festival opportunity:

- Cholistan Cultural Festival (February, aligned with Desert Rally): Week-long celebration featuring traditional music, dance, camel exhibitions, craft bazaars, culinary festivals showcasing Seraiki and Punjabi desert cuisine, and fort illuminations. Target: 50,000-75,000 attendees generating $8-12 million.

- Thar Heritage Festival (November-December, cooler season): Similar model celebrating Thari culture, featuring folk music competitions, women’s craft cooperatives, traditional sports (camel racing, horse exhibitions), and food courts. Target: 30,000-50,000 attendees generating $5-8 million.

Beyond festivals, establish permanent craft villages where tourists observe artisans at work and purchase directly—similar to Rajasthan’s craft villages that generate hundreds of millions annually. Ensure women control craft cooperative revenues, as they’re primary artisans in many traditional crafts.

Quality control critical: Establish Geographical Indication (GI) status for Thari embroidery and Cholistan textiles (like India’s GI-protected crafts), enabling premium pricing and preventing cheap imitations. Market these internationally through partnerships with ethical fashion brands and luxury retailers.

Recent initiatives like the Tharparkar Cultural Festival demonstrate grassroots momentum. Government support—funding, marketing, infrastructure—could scale these to economically significant levels.

10. Implement Solar-Powered Sustainable Tourism Infrastructure

Infrastructure challenges—water scarcity, electricity unreliability, road access—represent primary barriers to desert tourism development. Traditional infrastructure solutions (grid extension, water pipelines) are cost-prohibitive for remote desert regions.

Solar-powered, sustainable infrastructure offers economically viable solutions while positioning Pakistan as a leader in eco-tourism. International travelers increasingly seek sustainable destinations—66% of travelers would pay more for sustainable options according to Booking.com research.

Practical applications:

- Solar microgrids: Power luxury desert camps, homestays, and facilities without grid dependency. Cost: $50,000-100,000 per installation. Already proven at remote tourism sites in Jordan, Namibia, and Chile.

- Solar water pumps and conservation: Efficient water management for tourism facilities using solar-powered desalination (brackish water treatment) and greywater recycling. Reduces water consumption by 60-70%.

- Solar-powered electric safari vehicles: For wildlife tourism and site visits, eliminating diesel generators’ noise and emissions. Tesla and BYD now produce affordable electric 4x4s suitable for desert conditions.

- Sustainable road access: Use innovative materials (recycled plastics mixed with aggregate) for all-weather desert roads, proven in Middle Eastern deserts.

Investment case: Solar infrastructure reduces operating costs by 40-60% versus diesel generators over 10 years, while “sustainable tourism” branding enables 15-20% premium pricing. A $30-40 million investment in sustainable infrastructure across 20-30 tourism sites could support an industry generating $150-200 million annually within five years.

The Asian Development Bank and World Bank have expressed interest in financing Pakistan’s sustainable tourism infrastructure. The funding exists; execution requires coordinated proposals from provincial tourism departments.

The Economic Road Ahead

Pakistan’s desert tourism potential isn’t speculative—it’s proven by comparable success stories globally. Rajasthan’s deserts contribute over $12 billion annually. Dubai built a $45 billion tourism economy on less dramatic desert landscapes. Jordan’s desert regions generate billions while hosting similar security challenges Pakistan once faced.

The mathematics are compelling: if Pakistan captured merely 10% of Rajasthan’s desert tourism market, that would add $1.2 billion annually—25-30% growth over current total tourism revenue. Scale to Dubai-comparable levels (accounting for Pakistan’s larger population and equivalent infrastructure), and you’re approaching $5-8 billion in desert-driven tourism revenue potential by 2030.

These ten strategies require coordinated implementation across federal and provincial governments, private sector investment, and community engagement. The total capital investment needed—approximately $150-250 million across all initiatives—is modest compared to potential returns. Tourism multiplier effects (every $1 in tourism generates $2-3 in broader economic activity) mean actual economic impact could reach $10-20 billion over five years.

The 2026 moment is critical. Global tourism is recovering strongly post-pandemic, with travelers seeking new destinations. Pakistan’s improved security environment, growing international engagement (hosting international cricket, diplomatic reengagement), and infrastructure improvements create unprecedented opportunities.

Political will remains the primary requirement. The federal government’s stated commitment to tourism development must translate into policy reforms: simplified visa procedures (e-visa expansion), tourism infrastructure investment, public-private partnership frameworks, and sustained marketing budgets.

For investors—both Pakistani and international—desert tourism offers exceptional returns in an undervalued market. For local communities, it represents sustainable income diversification from agriculture. For Pakistan’s national economy, it’s a foreign exchange generator requiring minimal imports.

The deserts of Cholistan and Thar have patiently waited centuries to reveal their economic potential. In 2026, with strategic vision and coordinated execution, Pakistan can finally unlock the prosperity hidden in the sands.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

What happened: In early 2026, the United Arab Emirates declined to roll over a $3 billion loan to Pakistan — the first such refusal in seven years. The repayment equalled roughly 18% of Pakistan’s foreign currency reserves, arriving as Islamabad also faced a $1.3 billion bond payment and was waiting on the next IMF tranche.

Why it matters: It’s the clearest sign yet that Gulf sovereign patience with Pakistan’s balance-of-payments cycle is thinning, even as Gulf states simultaneously court China, Saudi Arabia, and each other for capital in a tightening regional liquidity environment.

The Story Nobody’s Connecting

Most coverage of Pakistan’s 2026 external account stress treats the UAE’s loan decision as an isolated liquidity event — a “routine financial transaction,” in the words of Pakistan’s own Ministry of Foreign Affairs. That framing misses the bigger pattern. The same weeks that Abu Dhabi called in its $3 billion, unusual delays began appearing in bank transfers from Saudi Arabia to the UAE itself — friction between the Gulf’s two largest economies, at a moment when both are also managing their own post-war oil price adjustment. (Pakistan & Gulf Economist)

Put those two data points together and a different story emerges: this isn’t just about Pakistan’s creditworthiness. It’s about Gulf capital becoming more selective, more transactional, and less willing to extend informal grace periods across the board — with Pakistan simply the most exposed borrower in the queue.

The Numbers Behind the Pressure

Pakistan’s State Bank held $16.4 billion in reserves as of late March 2026 — enough to cover roughly three months of imports, a threshold economists generally treat as a comfort floor, not a cushion. (Mettis Global News) The UAE’s declined rollover landed at the same time as a looming $1.3 billion international bond payment and dependence on the next $1.2 billion IMF disbursement — a convergence of obligations that left the State Bank with limited room to maneuver beyond import restrictions, rate hikes, or fresh commercial borrowing.

The backdrop matters too. The rupee had been trading in a comparatively narrow 278–282 band before the escalation of the Iran conflict pushed global oil prices higher, squeezing Pakistan’s import bill precisely when its Gulf safety net began to wobble. The KSE-100 benchmark, meanwhile, had already shed around 15% amid the broader pressure. (Mettis Global News)

This is not Pakistan’s first Gulf-dependency cycle. The IMF’s own record shows a now-familiar pattern: staff-level agreements reached in Dubai, UAE pledges of multibillion-dollar investment arriving alongside IMF tranches, and Gulf bridge financing used to stave off sovereign default in periods when reserves cover shrinks toward zero. (Business Standard) What’s different in 2026 is that the bridge itself is showing cracks.

Islamabad’s Official Line vs. the Structural Reality

Pakistan’s government has leaned into a “stability to sustainable growth” narrative around its FY2026–27 federal budget, with the finance minister framing the transition as export-driven rather than reserve-dependent. Business groups have broadly welcomed the budget, and the current account posted a $459 million surplus in May 2026, an improvement attributed to strong remittance inflows. (Business Recorder) The Monetary Policy Committee has held rates steady rather than reaching for emergency tightening, which is itself a signal that the central bank does not yet see the UAE episode as a systemic trigger.

But a current account surplus built substantially on remittances is different from one built on export competitiveness or durable FDI. Pakistan’s trade structure still leans heavily on a narrow set of partners: China supplies over a quarter of its imports and a meaningful share of its exports, the UAE is both a top export destination and its second-largest import source, and Gulf states collectively remain the primary channel for both remittances and emergency liquidity. (Wikipedia — Economy of Pakistan) That concentration is precisely what makes a single Gulf lender’s changed appetite so consequential.

Why the Oil Backdrop Compounds the Risk

None of this is happening in a vacuum. The IMF’s own July 2026 commentary noted that global oil markets “absorbed the war shock” from the Iran conflict, but cautioned that buffers — spare production capacity, strategic reserves, shipping insurance capacity — are running low. (IMF Blog) For an oil-importing, reserve-constrained economy like Pakistan, a second energy price shock without deeper buffers would land directly on the same reserves the UAE loan was meant to protect.

What to Watch Next

- Whether Saudi Arabia steps in as an alternative bridge lender, or whether the Riyadh–Abu Dhabi transfer friction signals a broader Gulf liquidity tightening that limits everyone’s appetite to backstop Pakistan.

- The pace and size of the next IMF tranche, and whether Fund conditionality shifts to demand deeper reserve buffers given the UAE precedent.

- Whether China increases its role as lender of last resort, deepening Pakistan’s dependency in exactly the direction Gulf financing was historically meant to offset.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Introduction

The European Council formally extended its economic sanctions against Russia for another full year on 25 June 2026, keeping restrictive measures in place until 31 July 2027 (Council of the EU). More than four years into the war, the headline story of Russia’s economy has shifted from whether sanctions would work to a more nuanced question: how much longer can the Kremlin keep financing the war before the accumulated strain becomes impossible to hide behind favorable official statistics.

The Sanctions Architecture, Renewed Again

The EU’s economic measures against Russia, first introduced in 2014 and dramatically expanded after the February 2022 full-scale invasion, now span trade, finance, energy and dual-use technology restrictions, alongside asset freezes and travel bans on a broad range of individuals and entities (Council of the EU). Since February 2022, the EU has adopted 20 separate sanctions packages, and the European Council has explicitly stated it remains determined to keep weakening Russia’s war economy by further reducing its energy revenues, curbing shadow-fleet oil shipping operations and constraining its banking system (Council of the EU). Separately, on 3 July 2026 the EU sanctioned six individuals connected to the poisoning and death of opposition figure Alexei Navalny, underscoring that the sanctions regime continues to expand on human-rights grounds as well as economic ones (Council of the EU Sanctions Timeline).

The Headline Numbers Beijing-Style Optimism Can No Longer Explain Away

Russia’s GDP is now put at roughly $2.51 trillion, the world’s eleventh-largest economy — comparable in size to South Korea despite Russia’s vastly larger landmass and resource base — with 2026 growth projected at just 1.0% and inflation running at 5.2% (Statistics of the World). More pessimistic estimates put full-year 2026 growth even lower, at around 0.4%, which would be worse than 2025’s already-weak 1% expansion and would mark a sharp deceleration from the 4.1% growth Russia posted in 2023 as it forged new trading relationships to route around initial sanctions (Forbes).

Oil and gas revenues — historically around half of Russia’s state income — have fallen to roughly a quarter, a deliberate outcome of Western sanctions strategy that targets how much Russia earns from exports rather than blocking those exports outright (Stockholm School of Economics/SITE). Russia’s oil and gas budget revenues reportedly halved in January 2026 alone, with crude prices falling below $73 a barrel before the Middle East conflict briefly reversed the trend, sending Brent surging more than 55% to near $120 a barrel at its peak (Forbes).

The Middle East War: A Temporary Lifeline With Long-Term Costs

The spike in oil prices tied to the Iran conflict, combined with a period of eased US sanctions enforcement on Russian oil under President Trump, offered Moscow unexpected fiscal breathing room in mid-2026 (Forbes). But that same conflict has undermined Russia’s longer-term energy diversification ambitions in the region: two Russian-backed power plant projects in Iran have been put on hold, along with oil and gas exploration work and plans to build new transit routes linking Russia to India via Iran (Forbes).

The Gap Between Official Statistics and Underlying Reality

Perhaps the most important analytical point from recent research is not about any single data point but about the reliability of Russian statistics themselves. Torbjörn Becker of the Stockholm Institute of Transition Economics has argued the real test of sanctions is not whether they end the war overnight, but how much they erode the Kremlin’s capacity to finance it — and by that measure, the evidence points to deeper strain than headline GDP figures suggest (Stockholm School of Economics/SITE). Becker notes that Russia’s economy grew only modestly in 2022 despite oil prices rising sharply that year — a gap between expected and actual performance that implies a considerably larger hidden economic hit than the official contraction figures showed (Stockholm School of Economics/SITE). Compounding the problem, Russian authorities have stopped publishing several key statistics since 2022, making independent assessment of inflation, consumption and real economic conditions increasingly difficult — leading Becker to conclude that “statistics have become part of the narrative” rather than a neutral measure of economic reality (Stockholm School of Economics/SITE).

The Military-Civilian Economic Split

A recurring theme across recent analysis is the growing bifurcation between Russia’s overheating military-industrial sector and a stagnating civilian economy. This imbalance has pushed interest rates higher and forced the liquidation of a striking 71% of Russia’s gold reserves to help fund continued war spending (Forbes). Russia’s total fossil fuel export revenue is estimated at roughly €734 million per day, underscoring just how central hydrocarbon income remains to the entire war financing model even as that revenue stream shrinks (Forbes).

The Counter-Narrative: Wages Still Rising

It would be inaccurate to describe Russia’s economy as in freefall. CSIS research notes that Russian salaries rose 17.8% in nominal terms and 8.7% in real terms in 2024 compared to 2023, with disposable incomes up 6.1% in 2023 and 7.3% in 2024 — growth rates not seen in Russia in almost two decades (CSIS). Government budget projections still expect real salaries to rise, albeit at a decelerating pace: 7% in 2025, 5.7% in 2026 and 4.1% in 2027 — a marked slowdown from the 2024 peak but still roughly double the pre-invasion decade average (CSIS). This wage growth, driven substantially by wartime labor shortages and military-adjacent spending, is precisely the kind of headline-stabilizing data point that has allowed Putin to argue publicly that sanctions have failed to cripple his economy (Fortune) — even as think tanks describe the broader trajectory as pushing Russia toward what one report calls an “economic, political, and military abyss” (Fortune).

What Comes Next

Renewed legislative pressure in Washington — including the Sanctioning Russia Act introduced with strong bipartisan support — signals appetite in the US for tightening the screws further, even as the loss of a key congressional champion for that effort has complicated the political path forward (TIME). Whether the EU’s renewed sanctions regime, continued oil price pressure, and constrained reserves ultimately force a shift in Kremlin calculus toward negotiation remains the central open question for 2027.

Key Takeaways

- The EU has extended Russia sanctions for a further year, through 31 July 2027, continuing a regime built from 20 separate packages since 2022.

- Russia’s 2026 GDP growth is forecast between 0.4% and 1.0%, a sharp deceleration from 2023’s 4.1% post-shock rebound.

- Oil and gas revenue’s share of Russian state income has fallen from roughly half to about a quarter as Western sanctions target export earnings specifically.

- Russia has liquidated a large share of its gold reserves to sustain war financing amid a widening split between an overheating military sector and a stagnating civilian economy.

- Official Russian statistics likely understate the true economic strain, according to independent economists who cite a widening gap between reported and expected performance.

Sources: Council of the EU, Council of the EU Sanctions Timeline, Stockholm School of Economics/SITE, Forbes, Statistics of the World, CSIS, Fortune, TIME

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Singapore’s non-oil domestic exports rose 20.7% year-on-year in June 2026, driven by a 115.4% surge in integrated circuit shipments tied to AI demand, even as a separate and less-covered trade story unfolds next door: Malaysia-Indonesia bilateral trade is projected to grow 10% to US$29.3 billion in 2026, powered by expanding halal-sector cooperation.

The story most coverage is missing

Regional business press has extensively covered Singapore’s semiconductor export boom. What’s had far less coverage is the parallel, non-tech growth engine developing in the halal trade corridor between Malaysia and Indonesia — a structural, policy-driven trade relationship that is scaling steadily even as the AI trade headlines dominate attention.

Singapore: the AI supply chain’s export barometer

Singapore’s June non-oil domestic exports climbed 20.7% year-on-year, with integrated circuit exports jumping 115.4% and disk media products and personal computers rising 170.9% and 95.8% respectively — a direct read on how deeply the AI infrastructure buildout is flowing through the city-state’s electronics trade (VietnamPlus/VNA). Non-electronic exports told a different story, falling 2.9% in June after a 17.7% rise in May, mainly on weaker shipments of non-monetary gold, petrochemicals and food preparations — evidence the export strength is narrowly concentrated in the AI-linked segment rather than broad-based.

Singapore’s economic gravitational pull on its neighbours is intensifying too: a joint study by the Singapore Business Federation, Restaurant Association of Singapore and Singapore Retailers Association found Singaporean consumers are projected to spend an additional S$1.05 billion (roughly US$810 million) annually in Johor Bahru, just across the Malaysian border — a cross-border consumption pattern that is becoming a meaningful line item in regional retail planning (VietnamPlus/VNA).

The halal corridor: a steadier, policy-built growth story

While AI exports grab headlines, Malaysia’s bilateral trade with Indonesia is forecast to grow 10% to US$29.3 billion in 2026, according to Malaysia’s Chargé d’Affaires in Jakarta, Farzamie Sarkawi — up from US$26.61 billion in 2025, itself a 5.3% increase on the year before (BusinessToday Malaysia).

The driver is structural rather than cyclical: a halal Memorandum of Cooperation signed by the two countries in 2023 established mutual recognition of halal certification, easing product movement and market access across sectors. Sarkawi described the arrangement as delivering “positive progress” through knowledge exchange, training and improved market access for businesses in both countries (BusinessToday Malaysia). The ambition extends beyond the bilateral relationship: intra-D-8 trade — spanning the eight-nation Developing 8 bloc of Muslim-majority economies — currently runs between US$150 billion and US$160 billion annually, with a stated target of US$500 billion by 2030.

The macro backdrop: a region growing, unevenly

The Asian Development Bank’s July 2026 outlook shows Indonesia’s growth forecast holding steady at 5.2% for both 2026 and 2027, while Malaysia’s outlook is unchanged at 4.6% for 2026 and 4.5% for 2027 (ADB). Regional growth leadership, per McKinsey’s Q1 2026 review, sits with Indonesia, Singapore and Vietnam, while the Philippines lagged as domestic challenges weighed on activity (McKinsey).

Indonesia’s investment story has particular momentum: foreign direct investment grew for a second consecutive quarter, rising 8.1% to 249.9 trillion rupiah (roughly US$14.5 billion) in the first quarter of 2026, with Singapore remaining Indonesia’s largest single foreign investor at US$4.6 billion, ahead of China, Japan, Hong Kong and the United States (McKinsey). Realised investment for full-year 2025 reached a record Rp1,931.2 trillion (about US$120.7 billion), exceeding the government’s own target, driven by downstream industrial projects outside Java (BERNAMA).

Indonesia’s central bank has flagged currency management as an active watch item, signalling readiness to step up both onshore and offshore FX intervention to curb rupiah weakness and keep inflation within its 2026-2027 target band (McKinsey). Foreign investment in Indonesian government bonds has nonetheless rebounded, with net inflows of 17.7 trillion rupiah following outflows in the first quarter, alongside cumulative foreign holdings of 174 trillion rupiah in Bank Indonesia Rupiah Securities (BERNAMA).

Institutional context: Singapore’s coming ASEAN chairmanship

Adding a governance dimension to the economic picture, Singapore is set to take over the ASEAN chairmanship from the Philippines in 2027, with Prime Minister Lawrence Wong pledging a smooth transition — a leadership handover that will shape how the bloc coordinates trade and investment policy, including the halal-corridor and semiconductor-trade dynamics described above, through the second half of the decade (BERNAMA).

The bottom line

Southeast Asia’s 2026 growth story is not a single narrative but two distinct, converging tracks: a high-velocity, AI-linked export boom concentrated in Singapore’s electronics trade, and a steadier, policy-engineered halal-sector trade corridor between Malaysia and Indonesia that is quietly scaling toward a $500 billion bloc-wide target by 2030. Investors and policymakers tracking only the semiconductor headlines risk missing the second, structurally more durable growth engine sitting right alongside it.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan IMF Program 2026: Inside the Push Toward an Interest-Free Economy

Russia Oil Revenue 2026: How Sanctions on Rosneft and Lukoil Are Draining the War Chest

Canada US Trade War 2026: Inside Carney’s Push to Cut Ties With Trump’s Tariffs

Rachel Reeves’s £25 Billion Problem: What the Autumn Budget Gap Means for Britain

Inside the Fed’s Most Divided Vote in Years: Why Warsh Held the Line on Rates

Pakistan Passed Its Third IMF Review

The Fed Is Fractured — And a New Chair Just Made It Louder, Not Quieter

The UK Economy in 2026 Is Neither Recession Nor Recovery :Stagflaton

Indonesia’s $121 Billion Nickel Bet Is Facing a Battery Chemistry

Why Ultra-Wealthy Families Are Splitting Between Singapore and Dubai inmarkets 2026

China Chose Political Control Over Fixing Its Deflation Trap in 2026

Oil Markets Are Oversupplied and Geopolitically Explosive at the Same Time

Russia’s Budget Deficit Blew Past Its Full-Year Target in Three Months

Malaysia’s Rare Earth Bet: Six Powers Are Negotiating for Kuantan at Once

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gold Price Forecast 2026: Fed’s July 29 Decision and Record Central Bank Buying Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

China Politburo July 2026: Stimulus Signals Explained

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Pakistan Economy 2026: GDP Grows 3.7% as IMF Completes EFF Review Amid Middle East Risk

Apple vs OpenAI Lawsuit: The Economic Story Behind the Headline

Global Stock Market Selloff 2026: Stagflation Fears Return as Iran Conflict Reignites

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

The Yuan Now Settles 67% of Russian Oil Payments — Quiet De-Dollarization in Action

AI Capex Bubble 2026: The Hidden $662B Debt Nobody Reports

Pakistan’s Economic Survey FY26: Inflation Spike Insights

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis6 months ago

Analysis6 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks7 months ago

Banks7 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025