Analysis

Indonesia’s Rupiah Balancing Act: Growth Surges as Singapore Capital Pours In

Indonesia’s economy just posted its best quarterly performance since 2023, but the central bank’s response to that strength tells a more cautious story than the headline number suggests — one with direct implications for anyone tracking capital flows into Southeast Asia’s largest economy.

The Growth Number

Indonesia’s economy expanded by 5.61 percent in the first quarter of 2026, its fastest pace in more than three years, according to McKinsey’s Southeast Asia quarterly review, boosted by a surge in government spending and strong household consumption tied to the Eid festive period. The Asian Development Bank’s July outlook has since nudged its own 2026 forecast for Indonesia higher by half a percentage point to 3 percent for the year, while separately projecting Indonesia’s growth to hold stable at 5.2 percent in both 2026 and 2027 in its base scenario — reflecting how much forecasts vary depending on the specific window and methodology used.

Why Bank Indonesia Is Playing It Safe

Despite the strong print, Bank Indonesia has kept its benchmark policy rate unchanged at 4.75 percent for a seventh consecutive meeting, prioritising rupiah stability over further easing in the face of external volatility. The central bank has explicitly signalled readiness to step up both onshore and offshore foreign exchange intervention to defend the currency and keep inflation within its 2026–2027 target range — a notably defensive posture for an economy growing at its fastest pace in years.

That caution is paying off on the capital-flow side. Foreign direct investment into Indonesia grew for a second consecutive quarter, rising 8.1 percent to 249.9 trillion rupiah, or roughly $14.5 billion, in the first quarter of 2026.

How fast is Indonesia’s economy growing in 2026?

Indonesia’s GDP grew 5.61% in Q1 2026, its fastest pace in more than three years, driven by government spending and Eid-season consumption, while Bank Indonesia held its policy rate at 4.75% to protect the rupiah amid regional currency volatility.

The Singapore Connection

Much of that capital has a specific source: Singapore. Indonesia’s Coordinating Minister for Economic Affairs, Airlangga Hartarto, confirmed that Singapore’s investment in Indonesia reached approximately $17.4 billion in 2025, calling the city-state “a reliable partner,” with investment into the Batam-Bintan-Karimun corridor specifically reaching $5.7 billion in 2025, up from the prior year. The two governments are now expanding cooperation into the digital economy and green energy, alongside a Young Farmer Development Program launched in June 2026 aimed at deepening agricultural technology ties.

The Regional Context

Indonesia’s performance sits within a broader Southeast Asian picture that is, in McKinsey’s own framing, showing “signs of softening” even as growth foundations remain broadly stable, with higher costs, currency volatility and weaker external demand weighing on households and businesses across the region. Cushman & Wakefield’s Southeast Asia Outlook similarly frames the region as expanding 4.8 percent in 2025 before slowing to a projected 4.3 percent in 2026, citing resilient domestic consumption and moderating interest rates as the main supports.

The ADB’s own assessment is blunter about the source of the regional drag: the Strait of Hormuz-linked Middle East conflict is weighing more heavily on developing Asia than previously anticipated, with higher energy costs, supply disruptions and tighter financial conditions expected to dampen growth in the months ahead even as inflation broadens and stays elevated for longer than earlier forecast.

What It Means for Investors

Indonesia’s combination of strong headline growth, disciplined currency management, and deepening Singapore-anchored capital inflows makes it one of the more structurally sound growth stories in Southeast Asia heading into the second half of 2026 — provided Bank Indonesia’s defensive rate stance succeeds in insulating the rupiah from the broader regional energy-price shock now working through the system.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Uber’s pursuit of Delivery Hero has finally crossed the finish line, and the structure of the winning bid says as much about the state of global food-delivery competition as the headline price itself.

The Deal Terms

Uber will acquire Frankfurt-listed Delivery Hero in a deal valued at €41.50, or $47.59, per share, with Dutch technology investor Prosus offloading its near-17 percent stake in Delivery Hero to Uber as part of the transaction. The improved offer follows a rejected earlier approach: one of Delivery Hero’s major shareholders had turned down a €38-per-share offer from Uber back in May, forcing Uber to sweeten terms by roughly 9 percent to get the deal across the line.

The transaction’s second component is arguably more strategically important than the headline acquisition. Delivery Hero will simultaneously sell its businesses across 14 markets to SSW Partners in a deal worth $1.4 billion, specifically covering territories where Delivery Hero’s operations would otherwise overlap directly with Uber’s existing footprint post-acquisition — a structure clearly designed to pre-empt antitrust objections in those markets.

Why the Divestiture Structure Matters

Regulators across Europe and Asia have grown increasingly wary of food-delivery consolidation given the sector’s history of just two or three dominant platforms per market. By carving out the 14 overlapping markets into a separate sale to SSW Partners before regulatory review even begins, Uber and Delivery Hero appear to be attempting to neutralise the most obvious competition concerns pre-emptively — a playbook increasingly common in large tech-platform M&A globally.

Market Reaction

The market’s initial reaction was muted rather than euphoric: Delivery Hero shares fell about 1 percent on the news, suggesting investors had already priced in a deal at or near these terms following months of on-and-off negotiations, or harboured lingering doubts about regulatory approval timelines given the multi-market divestiture complexity involved.

The Broader M&A Backdrop

The Uber-Delivery Hero transaction lands amid a broader resurgence in large-scale industrial and technology M&A. On the same trading day, Swiss engineering group ABB agreed to acquire UK-listed industrial flow-control specialist Rotork for £4.1 billion, or $5.6 billion — ABB’s biggest-ever acquisition, sending Rotork shares soaring 66.7 percent in morning trading (a deal covered in greater depth in our companion piece on the UK industrial M&A wave). The concurrent timing of two multi-billion-dollar cross-border deals suggests dealmakers are treating current valuations and financing conditions as a window worth acting on before the Fed’s tightening bias, discussed elsewhere in this series, potentially raises the cost of acquisition financing further.

What It Means for Consumers and Competitors

For consumers across Uber’s and Delivery Hero’s combined markets, the immediate practical question is pricing power: fewer major platforms per market historically correlates with reduced promotional intensity and, eventually, higher delivery fees, even as the SSW Partners carve-out is designed to preserve at least nominal competition in the 14 most overlap-sensitive territories. Competing platforms — from DoorDash in the US to regional players across Southeast Asia — will be watching regulatory reception to this deal closely as a signal for how much further consolidation authorities are willing to tolerate in a sector still recovering from pandemic-era overexpansion.

Featured Snippet

How much is Uber paying for Delivery Hero? Uber’s takeover of Delivery Hero values the company at €41.50 ($47.59) per share, an increase from a previously rejected €38 offer. As part of the deal, Delivery Hero will sell its operations in 14 overlapping markets to SSW Partners for $1.4 billion.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

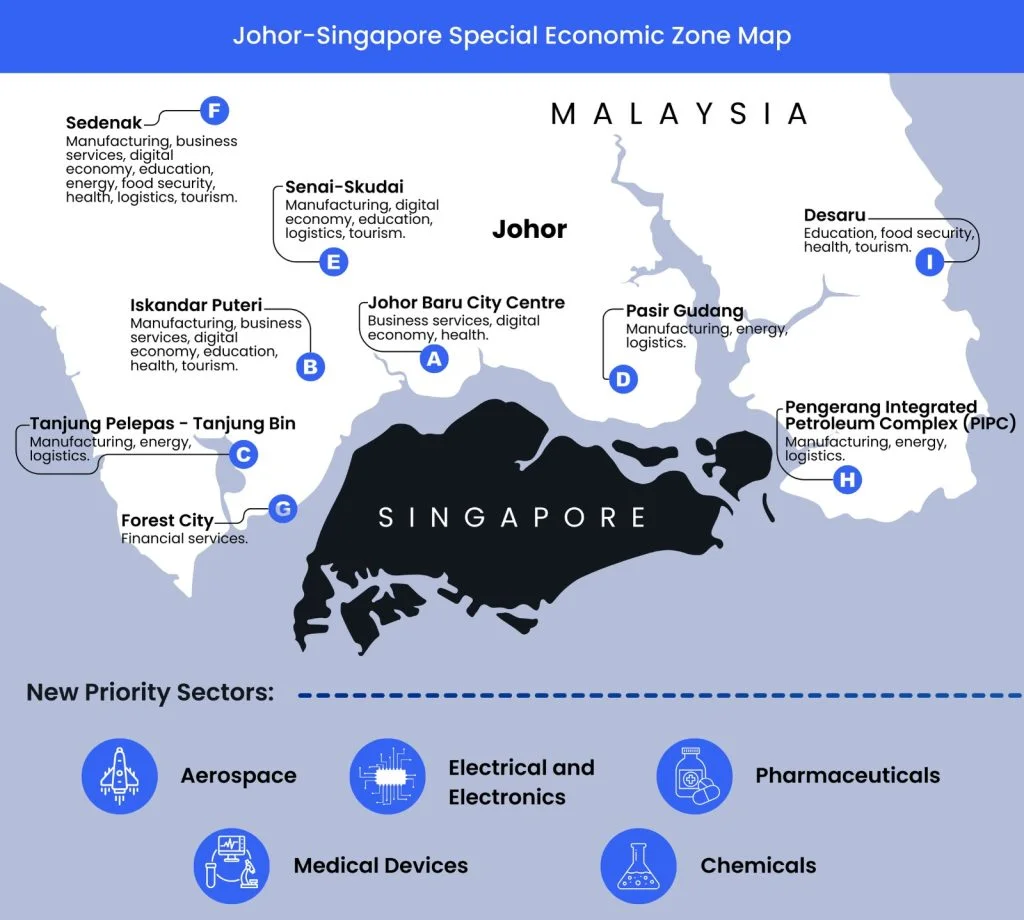

While much of global business coverage has focused on the Strait of Hormuz and Fed policy, one of Southeast Asia’s most significant economic developments has unfolded with comparatively little international attention: the Johor-Singapore Special Economic Zone has become a genuine cross-border investment magnet, even before its formal master plan has been unveiled.

The Scale of the Numbers

The JS-SEZ attracted 19 billion dollars in approved investments in 2025, with more than 57 percent of cumulative approved projects already at the implementation stage — a conversion rate that signals genuine capital deployment rather than speculative announcements. Malaysia’s Minister of Economy, Akmal Nasrullah, confirmed the momentum has continued into 2026, with a further $1.3 billion in newly approved investments recorded in the first quarter alone.

Investor interest continues to build at pace: the Invest Malaysia Facilitation Centre Johor processed 285 investment enquiries worth a combined $18.5 billion during just the first five months of 2026 — a pipeline roughly equivalent to the entire prior year’s approved investment total, suggesting the zone’s growth trajectory is accelerating rather than plateauing.

Why Investors Are Betting Ahead of the Master Plan

What makes the JS-SEZ notable is that this capital is arriving before Malaysia has formally unveiled the zone’s master plan — investors are pricing in the structural logic of the corridor itself rather than waiting for finalised regulatory detail. That logic rests on combining Singapore’s capital markets, legal infrastructure and connectivity with Johor’s land availability, labour costs and manufacturing base — a complementary pairing that Southeast Asia has lacked at this scale until now.

How much investment has the Johor-Singapore Special Economic Zone attracted?

The JS-SEZ attracted $19 billion in approved investments in 2025, with more than 57% of projects already in implementation, plus a further $1.3 billion approved in Q1 2026 — momentum that has continued even ahead of the zone’s formal master plan.

The zone’s momentum is reinforced by the broader institutional interest converging on the region. Maybank’s Invest ASEAN conference, held in Singapore in July 2026, drew roughly 200 institutional investors managing a combined $23 trillion in assets under management, with energy transition, supply chain reconfiguration and AI-led digital transformation identified as the dominant themes shaping capital allocation decisions across the region.

The Malaysia Growth Connection

The JS-SEZ is not an isolated success story — it’s a direct contributor to Malaysia’s broader macroeconomic outperformance in 2026. Maybank IBG’s decision to upgrade Malaysia’s 2026 GDP growth forecast to 4.9 percent cited sustained investment approval momentum in technology, renewable energy, industrial real estate and infrastructure — categories that map closely onto the sectors driving JS-SEZ deal flow.

Regional Comparison

Positioned against other Southeast Asian investment corridors, the JS-SEZ’s growth compares favourably even to Indonesia’s well-established Batam-Bintan-Karimun zone with Singapore, which drew $5.7 billion in investment in 2025 — roughly a third of the JS-SEZ’s total despite BBK’s longer operating history. The comparison underscores how quickly the Johor corridor has scaled since gaining formal momentum.

What to Watch Next

The formal unveiling of the JS-SEZ master plan remains the key near-term catalyst that could either validate or complicate current investment momentum, by clarifying tax incentives, land-use zoning, and cross-border labour mobility provisions. Until then, the zone’s implementation rate — already above 57 percent of approved projects — suggests investors are not waiting for regulatory certainty to deploy capital, a vote of confidence that is increasingly rare in a global environment defined by geopolitical and monetary policy uncertainty.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Four years into a sanctions regime designed to choke off the revenue funding Russia’s war in Ukraine, 2026 has produced an outcome few architects of that policy intended: Russian oil revenue is heading higher, not lower — and the reason has almost nothing to do with sanctions enforcement.

The Numbers Tell an Uncomfortable Story

According to the Kyiv School of Economics Institute, the Middle East conflict has forced a significant upward revision to Russia’s oil revenue outlook. In the base case — current price caps, the sanctions status quo, and a conflict lasting up to three months — Russian oil revenues are now projected to rise from $158 billion in 2025 to $208 billion in 2026. Even under an optimistic scenario of tighter enforcement, revenues are still expected to reach $184 billion — comfortably above 2025 levels. In the most adverse enforcement scenario, revenue could climb as high as $214 billion.

Average Urals crude prices jumped roughly $21 a barrel month-on-month to around $96 in April 2026, exceeding the ESPO Kozmino benchmark for the first time and trading well above the EU’s revised price cap — a level the cap was explicitly designed to prevent.

Why the Contradiction Exists

The mechanics here are counterintuitive but straightforward. Roughly 20 percent of global oil and LNG flows have been disrupted by the Strait of Hormuz crisis, and that scarcity has pushed Brent crude benchmarks above $100 a barrel. Analysis from Discovery Alert frames this bluntly as a 2026 sanctions paradox: crude benchmarks spiking sharply while Russian oil, still notionally sanctioned, becomes relatively more price-competitive as Gulf-origin supply faces logistical friction and elevated insurance costs.

The same piece notes a deeper irony: the tool built to starve Moscow’s war economy of revenue has, under crisis conditions, been effectively neutralised at the exact moment energy market disruption created ideal conditions for Russian crude to command near-market prices.

The Shadow Fleet Keeps Growing

Enforcement gaps compound the problem. The Centre for Research on Energy and Clean Air found that as of May 2026, 48 percent of Russia’s seaborne oil was transported by “shadow” tankers operating outside the G7-aligned insurance and shipping ecosystem, with fossil fuel export revenues rising 2 percent month-on-month to €726 million per day despite flat export volumes. Crude loadings at Ust-Luga, Russia’s fourth-largest export terminal, jumped 49 percent after a lull caused by Ukrainian drone strikes, while pipeline exports through the Druzhba line to Hungary and Slovakia rose 22 percent following the resumption of southern-branch flows in April.

The Kyiv School of Economics Institute’s tracking also shows sanctioned majors Rosneft and Lukoil regaining control over exports, with their combined share climbing to 57 percent — evidence that sanctioned entities are adapting faster than enforcement mechanisms can respond.

Are Russian oil sanctions still working in 2026?

Russian oil revenue is projected to rise from $158 billion in 2025 to as much as $208–214 billion in 2026, as the Strait of Hormuz crisis drives global crude prices above $100 a barrel, making sanctioned Russian oil more price-competitive despite ongoing Western sanctions.

What Policymakers Are Weighing

The EU’s 20th sanctions package, adopted in April 2026, lays the groundwork for a maritime services ban targeting Russian oil export volumes directly rather than just prices — a first, according to CREA’s tracking, but one that would only take effect with agreement from G7 and Price Cap Coalition members. Until that alignment materialises, Moscow’s revenue trajectory looks set to keep climbing alongside the broader energy-price shock.

The Strategic Bottom Line

For Western policymakers, the episode is a case study in how geopolitical shocks in one theatre can unravel painstakingly built economic pressure in another. For markets, it’s a reminder that sanctions effectiveness is a function not just of design, but of the global price environment they operate within — an environment the Strait of Hormuz crisis has upended entirely.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Uber’s $47.59-a-Share Delivery Hero Deal: Inside the Consolidation Wave

Johor-Singapore Economic Zone: Inside the $19 Billion Investment Boom

Indonesia’s Rupiah Balancing Act: Growth Surges as Singapore Capital Pours In

Malaysia GDP Forecast Raised to 4.9% as $23 Trillion Descends on Singapore

The Bank of England Just Modelled an AI Crash — Here’s What It Found

Pakistan Economy 2026: IMF Growth Warning vs. a Booming KSE-100

Russia’s Oil Sanctions Paradox: Why Revenue Is Rising, Not Falling

China GDP Growth Misses Target: What’s Behind the 4.3% Slowdown

The Strait of Hormuz Shock Nobody Has Priced In Yet

Fed Rate Hikes 2026: Why Kevin Warsh Is Reversing the Cut Cycle

Gold Price 2026: How Central Banks Made Gold Bigger Than US Treasuries in Reserves

Fed Chair Kevin Warsh’s AI Rate Bet 2026: Inside the FOMC Split on Productivity vs Inflation

Dubai Real Estate 2026: Inside the $5.1 Billion Ultra-Prime Boom and the Cooling Mid-Market

Bank of Canada 2026: Why the 0.7% Growth Cut Hides a Deeper Tariff-Adaptation Story

Top 7 Banking Stocks for Investment in PSX: Pakistan’s Lenders Are Still Printing Money

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

JPMorgan Cuts Anthropic AI Access in Hong Kong

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Why China’s Demand Stimulus Still Isn’t Working

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

India Economic Rise 2026: How the Subcontinent Toppled Japan

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025