Analysis

Fed Rate Hikes 2026: Why Kevin Warsh Is Reversing the Cut Cycle

Six months ago, the consensus on Wall Street was simple: the Federal Reserve would spend 2026 cutting rates toward neutral. That consensus is dead. Under new Chair Kevin Warsh, the Fed’s July 28–29 meeting has become the most consequential monetary policy event of the year — not because a hike is guaranteed, but because the direction of travel has inverted entirely.

From Cuts to Hikes: What Changed

Heading into the June FOMC meeting, futures markets were still pricing a reasonable probability of further easing. That repricing has now reversed sharply, with Bank of America projecting three separate 25-basis-point increases in September, October and December, while Deutsche Bank has penciled in two additional hikes before year-end.

Three forces are driving the shift. First, a labor market that has refused to soften has kept wage growth — and with it, services inflation — stubbornly elevated. Second, the Strait of Hormuz disruption has reintroduced a genuine energy-driven supply shock into an economy that had only just shaken off the last one. Third, the disinflationary tailwind from falling shelter costs, which did much of the Fed’s work in 2025, has largely run its course.

As Bank of America economist Aditya Bhave put it, the Fed had been willing to look through tariff-driven price increases but is losing patience after the latest round of supply shocks compounded them.

Warsh’s Market-First Doctrine

The appointment of Kevin Warsh as Fed Chair has itself become a variable markets are still pricing. Warsh has signaled a distinctly market-focused approach to policymaking, a departure that traders read as less tolerant of above-target inflation than his predecessor. Speaking at the ECB’s Sintra forum in early July, Warsh maintained that inflation risks had eased somewhat but reaffirmed the Fed’s commitment to the 2 percent target, while flagging AI-related demand, the Middle East conflict and tariffs as scenarios that could still force further tightening.

Minutes from the June meeting showed a genuinely divided committee. Officials debated a range of paths, with most agreeing that persistent inflation driven by AI infrastructure spending, geopolitical conflict or tariff pass-through would likely warrant some further policy firming even as the base case for many remained rates ending the year at or near current levels.

Why This Matters Beyond Washington

A genuine reversal toward hikes would ripple far past US Treasury yields. For the UK and Canada — both running their own delicate inflation-growth balancing acts — a hawkish Fed tightens global financial conditions and pressures currencies pegged loosely to dollar sentiment. For Gulf and Asian sovereign funds that price credit off Treasury benchmarks, higher-for-longer US rates raise the cost of the debt financing increasingly used to fund AI data-center buildouts (a theme explored in our companion piece on the AI capex debt cycle).

Equity markets, which have priced in a soft landing for over a year, face the sharpest test since 2022 if the Fed confirms even one hike at the July or September meeting. Credit card and auto loan borrowers, still absorbing rates well above pre-pandemic norms, would see little relief before 2027 at the earliest.

What to Watch Next

The July 29 decision itself is unlikely to produce an immediate hike — most desks still expect a hold — but the accompanying statement and Warsh’s press conference language will be parsed for confirmation of the tightening bias. The September meeting, which does produce a fresh Summary of Economic Projections, is the more likely inflection point.

For investors, the practical takeaway is that the “higher-for-longer” narrative many had assumed was ending in 2026 may instead be entering a second, more hawkish phase — one defined less by inflation left over from the pandemic and more by new supply shocks layered on top of an already-tight labor market.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Uber’s pursuit of Delivery Hero has finally crossed the finish line, and the structure of the winning bid says as much about the state of global food-delivery competition as the headline price itself.

The Deal Terms

Uber will acquire Frankfurt-listed Delivery Hero in a deal valued at €41.50, or $47.59, per share, with Dutch technology investor Prosus offloading its near-17 percent stake in Delivery Hero to Uber as part of the transaction. The improved offer follows a rejected earlier approach: one of Delivery Hero’s major shareholders had turned down a €38-per-share offer from Uber back in May, forcing Uber to sweeten terms by roughly 9 percent to get the deal across the line.

The transaction’s second component is arguably more strategically important than the headline acquisition. Delivery Hero will simultaneously sell its businesses across 14 markets to SSW Partners in a deal worth $1.4 billion, specifically covering territories where Delivery Hero’s operations would otherwise overlap directly with Uber’s existing footprint post-acquisition — a structure clearly designed to pre-empt antitrust objections in those markets.

Why the Divestiture Structure Matters

Regulators across Europe and Asia have grown increasingly wary of food-delivery consolidation given the sector’s history of just two or three dominant platforms per market. By carving out the 14 overlapping markets into a separate sale to SSW Partners before regulatory review even begins, Uber and Delivery Hero appear to be attempting to neutralise the most obvious competition concerns pre-emptively — a playbook increasingly common in large tech-platform M&A globally.

Market Reaction

The market’s initial reaction was muted rather than euphoric: Delivery Hero shares fell about 1 percent on the news, suggesting investors had already priced in a deal at or near these terms following months of on-and-off negotiations, or harboured lingering doubts about regulatory approval timelines given the multi-market divestiture complexity involved.

The Broader M&A Backdrop

The Uber-Delivery Hero transaction lands amid a broader resurgence in large-scale industrial and technology M&A. On the same trading day, Swiss engineering group ABB agreed to acquire UK-listed industrial flow-control specialist Rotork for £4.1 billion, or $5.6 billion — ABB’s biggest-ever acquisition, sending Rotork shares soaring 66.7 percent in morning trading (a deal covered in greater depth in our companion piece on the UK industrial M&A wave). The concurrent timing of two multi-billion-dollar cross-border deals suggests dealmakers are treating current valuations and financing conditions as a window worth acting on before the Fed’s tightening bias, discussed elsewhere in this series, potentially raises the cost of acquisition financing further.

What It Means for Consumers and Competitors

For consumers across Uber’s and Delivery Hero’s combined markets, the immediate practical question is pricing power: fewer major platforms per market historically correlates with reduced promotional intensity and, eventually, higher delivery fees, even as the SSW Partners carve-out is designed to preserve at least nominal competition in the 14 most overlap-sensitive territories. Competing platforms — from DoorDash in the US to regional players across Southeast Asia — will be watching regulatory reception to this deal closely as a signal for how much further consolidation authorities are willing to tolerate in a sector still recovering from pandemic-era overexpansion.

Featured Snippet

How much is Uber paying for Delivery Hero? Uber’s takeover of Delivery Hero values the company at €41.50 ($47.59) per share, an increase from a previously rejected €38 offer. As part of the deal, Delivery Hero will sell its operations in 14 overlapping markets to SSW Partners for $1.4 billion.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

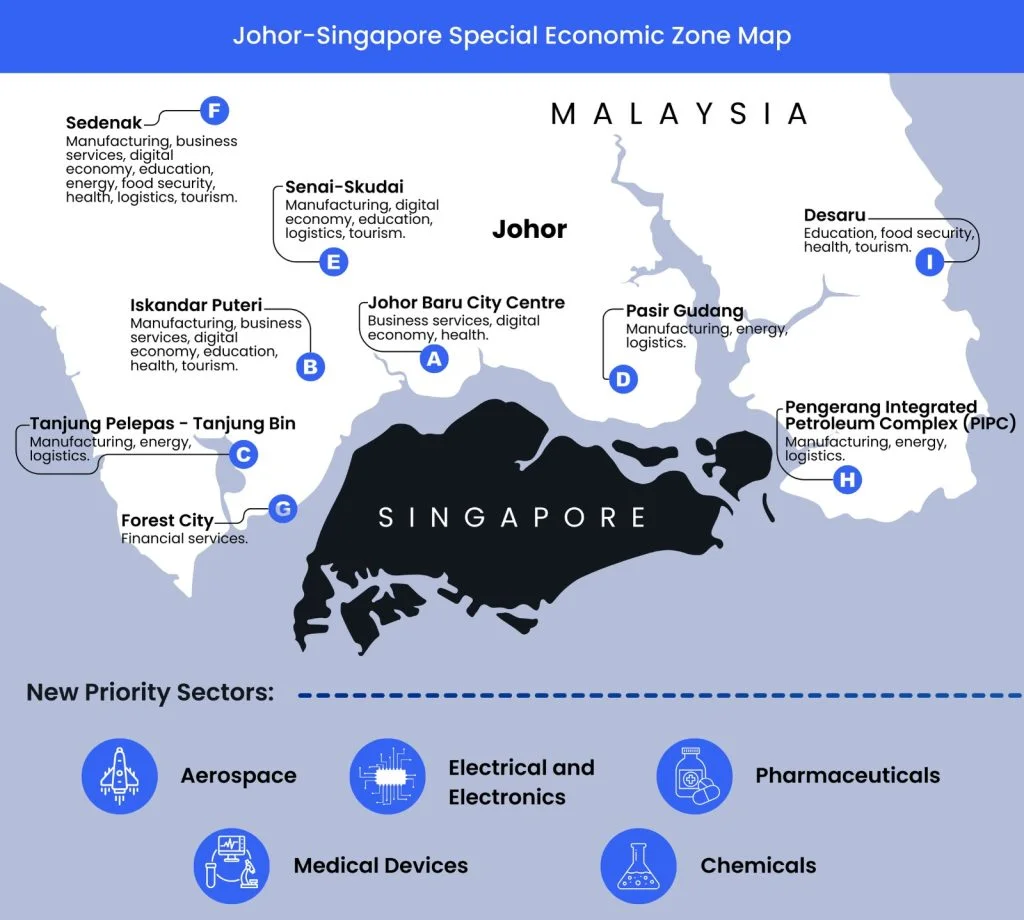

While much of global business coverage has focused on the Strait of Hormuz and Fed policy, one of Southeast Asia’s most significant economic developments has unfolded with comparatively little international attention: the Johor-Singapore Special Economic Zone has become a genuine cross-border investment magnet, even before its formal master plan has been unveiled.

The Scale of the Numbers

The JS-SEZ attracted 19 billion dollars in approved investments in 2025, with more than 57 percent of cumulative approved projects already at the implementation stage — a conversion rate that signals genuine capital deployment rather than speculative announcements. Malaysia’s Minister of Economy, Akmal Nasrullah, confirmed the momentum has continued into 2026, with a further $1.3 billion in newly approved investments recorded in the first quarter alone.

Investor interest continues to build at pace: the Invest Malaysia Facilitation Centre Johor processed 285 investment enquiries worth a combined $18.5 billion during just the first five months of 2026 — a pipeline roughly equivalent to the entire prior year’s approved investment total, suggesting the zone’s growth trajectory is accelerating rather than plateauing.

Why Investors Are Betting Ahead of the Master Plan

What makes the JS-SEZ notable is that this capital is arriving before Malaysia has formally unveiled the zone’s master plan — investors are pricing in the structural logic of the corridor itself rather than waiting for finalised regulatory detail. That logic rests on combining Singapore’s capital markets, legal infrastructure and connectivity with Johor’s land availability, labour costs and manufacturing base — a complementary pairing that Southeast Asia has lacked at this scale until now.

How much investment has the Johor-Singapore Special Economic Zone attracted?

The JS-SEZ attracted $19 billion in approved investments in 2025, with more than 57% of projects already in implementation, plus a further $1.3 billion approved in Q1 2026 — momentum that has continued even ahead of the zone’s formal master plan.

The zone’s momentum is reinforced by the broader institutional interest converging on the region. Maybank’s Invest ASEAN conference, held in Singapore in July 2026, drew roughly 200 institutional investors managing a combined $23 trillion in assets under management, with energy transition, supply chain reconfiguration and AI-led digital transformation identified as the dominant themes shaping capital allocation decisions across the region.

The Malaysia Growth Connection

The JS-SEZ is not an isolated success story — it’s a direct contributor to Malaysia’s broader macroeconomic outperformance in 2026. Maybank IBG’s decision to upgrade Malaysia’s 2026 GDP growth forecast to 4.9 percent cited sustained investment approval momentum in technology, renewable energy, industrial real estate and infrastructure — categories that map closely onto the sectors driving JS-SEZ deal flow.

Regional Comparison

Positioned against other Southeast Asian investment corridors, the JS-SEZ’s growth compares favourably even to Indonesia’s well-established Batam-Bintan-Karimun zone with Singapore, which drew $5.7 billion in investment in 2025 — roughly a third of the JS-SEZ’s total despite BBK’s longer operating history. The comparison underscores how quickly the Johor corridor has scaled since gaining formal momentum.

What to Watch Next

The formal unveiling of the JS-SEZ master plan remains the key near-term catalyst that could either validate or complicate current investment momentum, by clarifying tax incentives, land-use zoning, and cross-border labour mobility provisions. Until then, the zone’s implementation rate — already above 57 percent of approved projects — suggests investors are not waiting for regulatory certainty to deploy capital, a vote of confidence that is increasingly rare in a global environment defined by geopolitical and monetary policy uncertainty.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Indonesia’s economy just posted its best quarterly performance since 2023, but the central bank’s response to that strength tells a more cautious story than the headline number suggests — one with direct implications for anyone tracking capital flows into Southeast Asia’s largest economy.

The Growth Number

Indonesia’s economy expanded by 5.61 percent in the first quarter of 2026, its fastest pace in more than three years, according to McKinsey’s Southeast Asia quarterly review, boosted by a surge in government spending and strong household consumption tied to the Eid festive period. The Asian Development Bank’s July outlook has since nudged its own 2026 forecast for Indonesia higher by half a percentage point to 3 percent for the year, while separately projecting Indonesia’s growth to hold stable at 5.2 percent in both 2026 and 2027 in its base scenario — reflecting how much forecasts vary depending on the specific window and methodology used.

Why Bank Indonesia Is Playing It Safe

Despite the strong print, Bank Indonesia has kept its benchmark policy rate unchanged at 4.75 percent for a seventh consecutive meeting, prioritising rupiah stability over further easing in the face of external volatility. The central bank has explicitly signalled readiness to step up both onshore and offshore foreign exchange intervention to defend the currency and keep inflation within its 2026–2027 target range — a notably defensive posture for an economy growing at its fastest pace in years.

That caution is paying off on the capital-flow side. Foreign direct investment into Indonesia grew for a second consecutive quarter, rising 8.1 percent to 249.9 trillion rupiah, or roughly $14.5 billion, in the first quarter of 2026.

How fast is Indonesia’s economy growing in 2026?

Indonesia’s GDP grew 5.61% in Q1 2026, its fastest pace in more than three years, driven by government spending and Eid-season consumption, while Bank Indonesia held its policy rate at 4.75% to protect the rupiah amid regional currency volatility.

The Singapore Connection

Much of that capital has a specific source: Singapore. Indonesia’s Coordinating Minister for Economic Affairs, Airlangga Hartarto, confirmed that Singapore’s investment in Indonesia reached approximately $17.4 billion in 2025, calling the city-state “a reliable partner,” with investment into the Batam-Bintan-Karimun corridor specifically reaching $5.7 billion in 2025, up from the prior year. The two governments are now expanding cooperation into the digital economy and green energy, alongside a Young Farmer Development Program launched in June 2026 aimed at deepening agricultural technology ties.

The Regional Context

Indonesia’s performance sits within a broader Southeast Asian picture that is, in McKinsey’s own framing, showing “signs of softening” even as growth foundations remain broadly stable, with higher costs, currency volatility and weaker external demand weighing on households and businesses across the region. Cushman & Wakefield’s Southeast Asia Outlook similarly frames the region as expanding 4.8 percent in 2025 before slowing to a projected 4.3 percent in 2026, citing resilient domestic consumption and moderating interest rates as the main supports.

The ADB’s own assessment is blunter about the source of the regional drag: the Strait of Hormuz-linked Middle East conflict is weighing more heavily on developing Asia than previously anticipated, with higher energy costs, supply disruptions and tighter financial conditions expected to dampen growth in the months ahead even as inflation broadens and stays elevated for longer than earlier forecast.

What It Means for Investors

Indonesia’s combination of strong headline growth, disciplined currency management, and deepening Singapore-anchored capital inflows makes it one of the more structurally sound growth stories in Southeast Asia heading into the second half of 2026 — provided Bank Indonesia’s defensive rate stance succeeds in insulating the rupiah from the broader regional energy-price shock now working through the system.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Uber’s $47.59-a-Share Delivery Hero Deal: Inside the Consolidation Wave

Johor-Singapore Economic Zone: Inside the $19 Billion Investment Boom

Indonesia’s Rupiah Balancing Act: Growth Surges as Singapore Capital Pours In

Malaysia GDP Forecast Raised to 4.9% as $23 Trillion Descends on Singapore

The Bank of England Just Modelled an AI Crash — Here’s What It Found

Pakistan Economy 2026: IMF Growth Warning vs. a Booming KSE-100

Russia’s Oil Sanctions Paradox: Why Revenue Is Rising, Not Falling

China GDP Growth Misses Target: What’s Behind the 4.3% Slowdown

The Strait of Hormuz Shock Nobody Has Priced In Yet

Fed Rate Hikes 2026: Why Kevin Warsh Is Reversing the Cut Cycle

Gold Price 2026: How Central Banks Made Gold Bigger Than US Treasuries in Reserves

Fed Chair Kevin Warsh’s AI Rate Bet 2026: Inside the FOMC Split on Productivity vs Inflation

Dubai Real Estate 2026: Inside the $5.1 Billion Ultra-Prime Boom and the Cooling Mid-Market

Bank of Canada 2026: Why the 0.7% Growth Cut Hides a Deeper Tariff-Adaptation Story

Top 7 Banking Stocks for Investment in PSX: Pakistan’s Lenders Are Still Printing Money

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

JPMorgan Cuts Anthropic AI Access in Hong Kong

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Why China’s Demand Stimulus Still Isn’t Working

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

India Economic Rise 2026: How the Subcontinent Toppled Japan

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025