Analysis

Digital Economy as Pakistan’s Next Economic Doctrine: A Growth Debate Trapped in the Past

Understanding the Digital Economy: More Than a Sector, a System

There is a persistent category error at the heart of Pakistan’s economic policymaking. Officials speak of the “digital economy” the way an earlier generation spoke of textiles or agriculture — as a discrete sector, a line on an export ledger, a portfolio to be managed rather than a platform to be built. This confusion is not merely semantic. It shapes budget allocations, regulatory frameworks, institutional mandates, and, ultimately, the trajectory of a nation of 240 million people standing at a crossroads between chronic underdevelopment and a genuinely plausible economic transformation.

The digital economy, properly understood, is not a sector. It is the operating system upon which all modern economic activity increasingly runs. It encompasses the digitisation of production processes, the datafication of consumer behaviour, the platformisation of labour markets, and the emergence of knowledge as the primary factor of production. When the World Bank’s April 2025 Pakistan Development Update frames digital transformation as Pakistan’s most credible path toward export competitiveness and sustained growth, it is not advocating for a bigger IT park in Islamabad. It is arguing for a wholesale reimagining of what the Pakistani economy produces, and for whom.

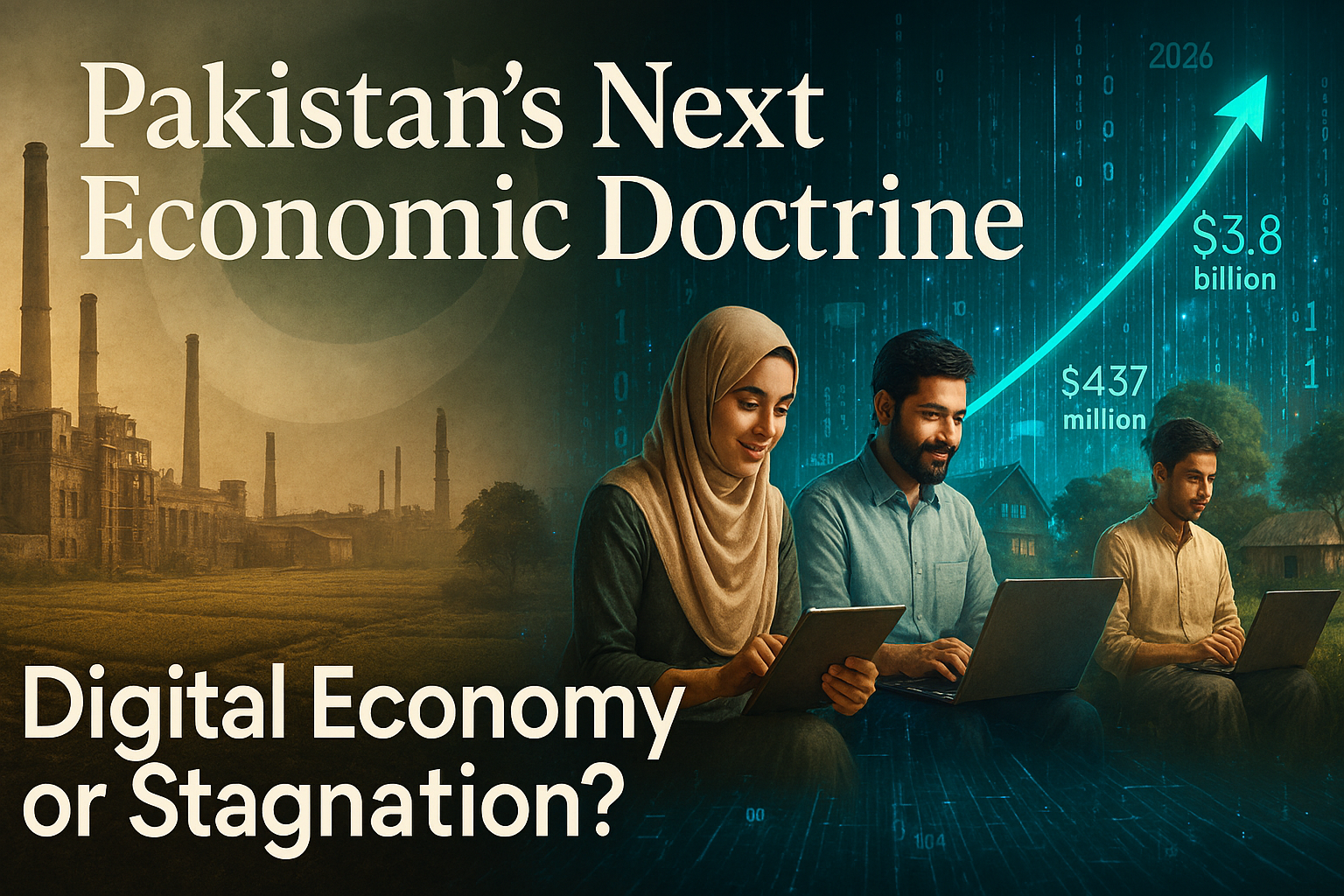

That reimagining has begun — tentatively, unevenly, and against considerable institutional resistance. The numbers, for once, are genuinely exciting. Pakistan IT exports reached $3.8 billion in FY2024–25, with the momentum building sharply into the current fiscal year: $2.61 billion in IT and ICT exports were recorded between July and January of FY2025–26, a 19.78% increase year-on-year, according to data released by the Pakistan Software Export Board (PSEB). December 2025 delivered a record single-month figure of $437 million — the highest in the country’s history. These are not marginal gains. They are signals of structural potential.

The question this analysis addresses is whether Pakistan possesses the institutional architecture, policy coherence, and political will to convert those signals into doctrine — or whether it will allow a historic opportunity to dissolve into the familiar entropy of short-termism, infrastructure neglect, and regulatory dysfunction.

Pakistan’s Emerging Digital Base: A Foundation That Defies the Headlines

The pessimistic narrative about Pakistan — fiscal crisis, security fragility, political instability — dominates international discourse and obscures a digital demographic reality that is, by most comparative metrics, extraordinary. Pakistan now has 116 million internet users, with penetration reaching 45.7% in early 2025 and accelerating. The PBS Household Survey 2024–25 found that over 70% of households have at least one member online, with individual usage approaching 57% of the adult population. Against the baseline of five years ago, this represents a compression of the connectivity timeline that took wealthier economies a generation to traverse.

Mobile is the primary vector. Pakistan’s 190 million mobile connections and 142 million broadband subscribers — figures corroborated by GSMA’s State of Mobile Internet Connectivity — reflect a population that has leapfrogged fixed-line infrastructure entirely and gone straight to smartphone-mediated internet access. Smartphone ownership has surged with the proliferation of affordable Chinese handsets, democratising access in a way that no government programme could have engineered.

The identity infrastructure is strengthening in parallel. NADRA’s digital ID system now covers the vast majority of the adult population, providing the authentication backbone without which digital financial services, e-commerce, and government-to-citizen digital delivery cannot scale. The State Bank of Pakistan’s (SBP) digital payments architecture — including the Raast instant payment system — has facilitated a measurable shift in transaction behaviour, particularly among younger urban cohorts.

What Pakistan has, in other words, is a digital base: not yet a digital economy, but the preconditions for one. The distinction is critical. A digital base is necessary but not sufficient. Converting it into export-generating, job-creating, productivity-enhancing economic activity requires deliberate policy architecture — something Pakistan has so far delivered only in fragments.

Geography Is Being Rewritten: The Location Dividend

For most of economic history, geography was fate. A landlocked country, a country far from major shipping lanes, a country without navigable rivers or natural harbours faced structural disadvantages that compounded over centuries. Pakistan’s geographic position — bordering Afghanistan, Iran, India, and China, with access to the Arabian Sea — has historically been as much a source of strategic anxiety as economic opportunity.

The digital economy rewrites this calculus. In knowledge-intensive digital services, physical location is increasingly irrelevant to market access. A software engineer in Lahore can serve a fintech client in Frankfurt. A data scientist in Karachi can work for a healthcare analytics firm in Houston. A UX designer in Peshawar can deliver to a product team in Singapore. The barriers that historically constrained Pakistani talent to domestic labour markets — or forced emigration — are structurally dissolving.

This is the location dividend: the ability to monetise Pakistani human capital in global markets without the friction costs of physical migration. It is a form of comparative advantage that requires no natural resources, no preferential trade agreements, and no proximity to wealthy consumer markets. It requires only talent, connectivity, and institutional conditions that allow value to flow across borders.

Pakistan’s digital economy growth model, at its most ambitious, is predicated on precisely this arbitrage: world-class technical skill delivered at emerging-market cost, routed through digital platforms, and paid in foreign exchange. The macroeconomic implications — for the current account, for foreign reserves, for wage convergence — are profound. The World Bank’s Digital Pakistan: Economic Policy for Export Competitiveness report identifies this services export channel as among the most scalable dimensions of the country’s growth potential.

The geography dividend is real. The question is whether Pakistan can build the institutional infrastructure to fully claim it.

The Freelancer Paradox: Scale Without Structure

Perhaps nowhere is the tension between Pakistan’s digital potential and its institutional constraints more vividly illustrated than in its freelance economy. The headline numbers are startling. Pakistan’s 2.37 million freelancers — an estimate from the Asian Development Bank (ADB) — generate a scale of digital services exports that places the country consistently in the top three to four globally on platforms including Upwork, Fiverr, and Toptal. Freelance earnings in H1 FY2025–26 reached $557 million, a 58% year-on-year increase from $352 million — a growth rate that no traditional export sector can approach.

This is the “freelancer paradox Pakistan” faces: enormous revealed comparative advantage, operating almost entirely outside formal policy architecture. The vast majority of Pakistan’s freelancers work without contracts, without access to institutional credit, without social protection, and without the kind of professional certification or dispute resolution frameworks that would allow them to move up the value chain from commodity task completion to complex, high-margin engagements.

The income ceiling is real and consequential. A Pakistani freelancer completing logo designs or basic data entry tasks on Fiverr earns at the low end of the global digital labour market. The same talent, operating through a structured agency model, with portfolio development support, client management training, and access to premium platforms, could command rates three to five times higher. The gap between what Pakistan’s freelance workforce earns and what it could earn is, effectively, a measure of what institutional neglect costs.

The foreign exchange dimension compounds the problem. Payments routed through platforms like PayPal — where availability for Pakistani users remains restricted — or through informal hawala networks, often bypass the formal banking system entirely. The SBP has made progress in facilitating formal remittance channels, but significant friction remains. Pakistan freelance exports are growing despite the system, not because of it.

A comprehensive Pakistan digital economy doctrine must address the freelancer economy not as an afterthought but as a strategic asset requiring dedicated institutional support: access to formal banking, skills certification, contract facilitation, and platform-level advocacy.

Infrastructure Reliability as Export Competitiveness: The Invisible Tax

Ask any Pakistani software engineer working on an international client project what their single biggest operational constraint is, and the answer is rarely regulatory. It is the power cut that interrupted a client call. It is the bandwidth throttling that corrupted a code repository push. It is the VPN restriction that prevented access to a cloud development environment. These are not edge cases. They are the daily texture of doing business in Pakistan’s digital economy.

Infrastructure reliability is not a background variable. In digital services exports, it is export competitiveness. A Pakistani IT firm competing against Indian, Ukrainian, or Filipino counterparts is not merely selling talent — it is selling reliable, on-time, high-quality delivery. A single missed deadline caused by a grid outage can cost a client relationship worth hundreds of thousands of dollars. Cumulatively, infrastructure unreliability functions as an invisible tax on Pakistan’s digital exports Pakistan is uniquely ill-positioned to afford.

The electricity crisis is the most acute dimension of this problem. Pakistan’s circular debt overhang — exceeding Rs. 2.4 trillion — continues to produce load-shedding that falls hardest on small businesses and home-based workers, who constitute the backbone of the freelance and micro-enterprise digital economy. Large IT firms in tech parks have access to backup generation; individual freelancers in Multan or Faisalabad do not.

Broadband quality is the second constraint. Pakistan’s average fixed broadband speed, while improving, remains well below regional competitors. Mobile data costs have declined, but network congestion in urban cores during peak hours frequently degrades the quality of experience to levels incompatible with professional digital work. The GSMA has consistently highlighted last-mile connectivity gaps as the primary barrier to realising Pakistan’s mobile internet dividend.

A credible Pakistan digital economy doctrine must treat infrastructure investment — in power stability, fibre optic expansion, and spectrum management — not as a public works programme but as export infrastructure, directly analogous to port expansion for goods trade.

Cyber Risks and the Trust Deficit: The Hidden Vulnerability

Digital economies are only as robust as the trust that underpins them. Trust operates at multiple levels: consumer trust in digital financial services, business trust in cloud infrastructure, investor trust in data governance frameworks, and international partner trust in Pakistan’s regulatory environment. On all of these dimensions, Pakistan faces a significant trust deficit that constrains the Pakistan digital economy growth trajectory.

Cybersecurity incidents affecting Pakistani financial institutions have multiplied. The banking sector has faced card data breaches, phishing campaigns targeting mobile banking users, and SIM-swap fraud at scale. The Pakistan Telecommunication Authority’s (PTA) record of internet shutdowns and platform restrictions — including prolonged access restrictions to major social media platforms during periods of political tension — has created a perception among international digital businesses that Pakistan’s internet governance is unpredictable.

This unpredictability carries a direct economic cost. International clients contracting Pakistani firms for sensitive data processing work — healthcare records, financial data, personal information — conduct due diligence on the regulatory and security environment. A country with a history of arbitrary platform restrictions and limited data protection enforcement does not inspire confidence for high-value data contracts.

Pakistan’s Personal Data Protection Bill, in legislative limbo for several years, represents the most visible symptom of this institutional gap. Without a credible, enforced data protection framework, Pakistan cannot credibly bid for the categories of digital services work — cloud processing, AI training data, health informatics — where the highest margins and fastest growth lie. Closing this gap is not merely a legal formality; it is a prerequisite for moving up the digital value chain.

Institutional Constraints and Policy Incoherence: The Structural Brake

Pakistan’s digital economy governance is fragmented across a proliferation of bodies — the Ministry of IT and Telecom (MoITT), PSEB, PTA, the National Information Technology Board (NITB), provincial ICT authorities, and the Special Investment Facilitation Council (SIFC) — with overlapping mandates, inconsistent coordination, and chronic under-resourcing. This fragmentation is not accidental; it reflects the accumulation of institutional layering that characterises Pakistan’s economic governance more broadly.

The policy incoherence is manifested in contradictions that would be almost comic if they were not so economically costly. Pakistan simultaneously promotes itself as a top destination for IT outsourcing while maintaining VPN restrictions that its own IT workers require to access client systems. It celebrates freelance export earnings while allowing the forex payment infrastructure for those earnings to remain dysfunctional. It announces ambitious digital skills programmes while underfunding the higher education institutions that produce the graduates those programmes are supposed to train.

The Pakistan IT exports 2026 growth trajectory — impressive as it is — is occurring largely in spite of, rather than because of, this governance architecture. The question for policymakers is not whether the current momentum can continue; it can, for a time, on the basis of demographic dividend and individual entrepreneurial energy alone. The question is whether that momentum can be compounded into the kind of structural transformation that moves Pakistan from an exporter of digital labour to an exporter of digital products and platforms.

That transition requires a qualitatively different institutional environment: one capable of regulating without strangling, facilitating without distorting, and investing at the horizon of a decade rather than the cycle of a fiscal year.

Digital Sovereignty and Platform Dependency: The Strategic Dimension

Beneath the growth narrative lies a geopolitical and strategic question that Pakistan’s digital economy debate has been slow to engage: the question of digital sovereignty Pakistan must navigate. As Pakistani businesses and individual workers increasingly integrate into global digital platform ecosystems — Upwork, Fiverr, AWS, Google Cloud, Microsoft Azure — they gain access to markets, infrastructure, and tools that would be impossible to replicate domestically. They also incur structural dependencies that carry long-term risks.

Platform dependency is not a uniquely Pakistani problem. Every country that has embraced the global digital economy faces some version of this tension. But for Pakistan, the risks are heightened by the country’s limited regulatory leverage, its absence from the standard-setting bodies that govern international digital trade, and the concentration of critical digital infrastructure in the hands of a small number of US-headquartered technology corporations.

The practical implications are significant. When a major freelance platform adjusts its fee structure or payment policies, Pakistani freelancers — who have no collective bargaining mechanism, no government-backed alternative platform, and no domestic digital marketplace of comparable scale — absorb the consequences. When a cloud provider raises prices or discontinues a service, Pakistani startups that have built their infrastructure on that provider face switching costs that can be existential.

Digital sovereignty does not mean autarky. It means building sufficient domestic digital capacity — in cloud infrastructure, in payment systems, in data storage, in platform development — to maintain meaningful optionality. It means participating in the governance of the global digital economy rather than passively receiving its terms. It means developing the regulatory expertise to negotiate with platform giants on terms that protect Pakistani economic interests.

This is a long-game strategic agenda, not a short-cycle policy fix. But without it, Pakistan’s Pakistan digital economy growth risks being permanently extractive — generating value that is captured elsewhere.

Government as Digital Market Creator: The Enabling State

One of the most durable insights from the comparative study of digital economy development — South Korea, Estonia, Singapore, Rwanda — is that the private sector alone does not build digital economies. Governments create the conditions: the infrastructure, the standards, the skills pipeline, the procurement signals, and the regulatory certainty without which private investment cannot take root at scale.

Pakistan’s government has the opportunity — and, given the fiscal constraints, the obligation — to be a strategic market creator rather than a passive regulator. Government digitalisation is not merely an efficiency play; it is a demand-side signal to the domestic digital industry. When the government digitises land records, health systems, tax administration, and public procurement, it creates contract opportunities for Pakistani IT firms, validates the commercial viability of digital solutions, and builds the reference clients that domestic companies need to compete internationally.

The PSEB’s facilitation role — connecting international clients with Pakistani IT firms, providing export certification, and advocating for payment infrastructure improvements — represents the embryo of a more active industrial policy. The SIFC’s mandate, if properly operationalised for the digital sector, could provide the high-level coordination that has been missing. But these institutions need resources, autonomy, and political backing to function at the scale the opportunity demands.

The most immediate lever available is public digital procurement: a committed pipeline of government IT contracts awarded to domestic firms under transparent, merit-based processes. This single policy — properly designed and consistently executed — could do more to develop Pakistan’s digital industry than any number of incubator programmes or innovation fund announcements.

From Factor-Driven to Knowledge-Driven Economy Pakistan: The Structural Leap

Pakistan’s economic growth model has, for most of its history, been factor-driven: growth generated by deploying more labour, more land, more capital, in sectors with relatively low productivity — agriculture, low-complexity manufacturing, commodity exports. The digital economy represents the most credible pathway to a fundamentally different model: one in which growth is driven by increasing productivity, accumulating human capital, and generating returns from knowledge rather than from raw inputs.

The knowledge-driven economy Pakistan needs is not a distant aspiration. The ingredients exist, in nascent form: a young population with demonstrated aptitude for digital skills, universities producing engineers and computer scientists at scale, a diaspora with global networks and capital, and a domestic entrepreneurial ecosystem generating startups in fintech, healthtech, agritech, and edtech that are beginning to attract international venture investment.

The transition from factor-driven to knowledge-driven growth is not automatic or inevitable. It requires deliberate investment in research and development, in higher education quality, in intellectual property protection, and in the kind of long-term institutional stability that allows firms to make multi-year investment commitments. Pakistan’s R&D expenditure as a share of GDP remains among the lowest in Asia — a structural constraint that no amount of IT export promotion can overcome if sustained.

The ADB’s research on Pakistan freelancers earnings and digital service exports consistently emphasises that the earnings ceiling for task-based freelance work is far lower than for product-based or IP-based digital exports. Moving Pakistani digital workers up this value curve — from executing tasks to building products, from selling hours to licensing software — is the central challenge of knowledge economy transition.

Policy Priorities for a Digital Doctrine: What Must Be Done

A credible Pakistan digital economy doctrine for the period to 2030 requires six interlocking policy commitments, each necessary but none sufficient in isolation.

First, infrastructure as export policy. Pakistan must treat reliable electricity supply and high-quality broadband as preconditions for digital export competitiveness, not as welfare goods. This means prioritising digital economic zones with guaranteed power supply, accelerating fibre optic backbone expansion into secondary cities, and reducing spectrum costs for business-grade mobile broadband.

Second, the forex plumbing must be fixed. The SBP must complete the liberalisation of digital payment channels, enabling Pakistani freelancers and digital firms to receive, hold, and deploy foreign currency earnings without the friction that currently drives significant volumes into informal channels. Every dollar that flows through informal networks is a dollar that does not build Pakistan’s foreign reserves or generate formal tax revenue.

Third, data protection legislation must be enacted and enforced. The Personal Data Protection Bill must be passed in a form that meets international standards — not as a regulatory box-ticking exercise, but as a genuine market access instrument. Pakistan cannot compete for high-value data services contracts without credible data governance.

Fourth, skills investment must match ambition. Pakistan’s Pakistan IT exports 2026 targets require a quantum expansion of the technical skills pipeline — not through low-quality short courses, but through sustained investment in computer science education at the tertiary level, curriculum modernisation, and industry-academia partnerships that ensure graduates enter the workforce with market-relevant capabilities.

Fifth, institutional consolidation. The fragmented governance architecture for the digital economy must be rationalised. A single, adequately resourced Digital Economy Authority — with a clear mandate, cross-ministerial coordination powers, and direct accountability to the Prime Minister — would reduce the transaction costs of doing business in Pakistan’s digital sector by orders of magnitude.

Sixth, a digital sovereignty strategy. Pakistan needs a national cloud strategy, a digital platform policy, and active participation in international digital trade negotiations. These are not luxury items for a mature digital economy; they are foundational choices that, once deferred, become progressively more expensive to make.

Conclusion: A Decisive Economic Choice

Pakistan’s Pakistan digital economy moment is real, and it is now. The combination of demographic scale, demonstrated digital talent, accelerating connectivity, and record IT and freelance export earnings constitutes a rare convergence of factors that, in other economies, has served as the launching pad for durable structural transformation.

But potential is not destiny. History is littered with countries that glimpsed the digital transformation horizon and then allowed institutional inertia, political short-termism, and infrastructure neglect to ensure they never reached it.

The debate Pakistan is currently having about its digital economy is, at its deepest level, a debate about what kind of economic future the country chooses to construct. The old paradigm — commodity exports, remittances, periodic IMF bailouts, growth that barely keeps pace with population — has delivered recurrent crisis and chronic underinvestment in human capital. The digital paradigm offers something genuinely different: a pathway to prosperity grounded in the one resource Pakistan has in abundance, its people, and their capacity for knowledge work in a globally connected economy.

Digital sovereignty Pakistan must claim is not merely about technology. It is about economic agency — the ability to participate in the global economy on terms that capture value domestically rather than exporting it. Every reform deferred, every institutional bottleneck left unaddressed, every dollar that flows through informal channels rather than the formal banking system, is a cost Pakistan cannot afford.

The choice between a Pakistan whose digital economy remains a promising footnote and one whose Pakistan digital economy growth becomes the defining story of the coming decade is not a technical question. It is a political one. And it must be answered decisively — before the window that demographics, technology, and global market demand have opened begins, once again, to close.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

UK in Political and Economic Flux: Reeves Faces Demotion, OBR Gets New Chair, EG Group Eyes US Listing

Britain faces political turbulence as Rachel Reeves is reportedly set for Cabinet demotion, a new OBR chair is named, a Shein tax loophole stays until October, and EG Group files confidentially for a billion-dollar US IPO. Full analysis.

Introduction: A Pivotal Week for British Finance and Politics

While global attention has been fixed on the US-Iran peace deal and the Federal Reserve’s hawkish pivot, Britain has had a turbulent week of its own — with political realignments at the top of government, a significant appointment at the fiscal watchdog, a major corporate IPO filing, and an embarrassing delay in closing a tax loophole exploited by fast-fashion giant Shein.

The Financial Times’s press digest for June 24, 2026 captures a country navigating deep economic uncertainty while its political center of gravity continues to shift (FT/Reuters via DevDiscourse).

Rachel Reeves Set for Cabinet Demotion: The Political Economy of a Reshuffled Treasury

Perhaps the most dramatic story in the FT’s digest: British lawmaker Andy Burnham is reportedly planning to remove Finance Minister Rachel Reeves from her position and offer her a lesser Cabinet role (FT/Reuters).

If confirmed, this would represent a significant political shake-up at the heart of British economic policy. Reeves has been a defining figure in the current government’s fiscal strategy — overseeing a period of considerable economic challenge for the UK, including the inflationary hangover from the Iran war, a fragile economic recovery, and persistent pressure on the public finances.

Why Does This Matter Economically?

Changes at the top of a government’s finance ministry send immediate signals to bond and currency markets. A Chancellor of the Exchequer transition — even a managed, non-crisis reshuffle — raises questions about:

- Fiscal continuity: Will Reeves’s successor maintain the same deficit reduction targets?

- Market credibility: UK Gilts markets have been sensitive to any perception of fiscal loosening since the 2022 Truss mini-budget crisis, which remains a fresh cautionary tale in British financial memory

- Business investment confidence: Companies making long-term investment decisions in the UK will want clarity on the government’s tax and spending trajectory before committing capital

The timing is also politically significant. With global inflation elevated due to the Iran war, any incoming Finance Minister immediately inherits a difficult macroeconomic environment with limited fiscal headroom.

Jonathan Haskel Named as New OBR Chair: Who Is He?

In a more procedurally straightforward development, Reeves herself has nominated Jonathan Haskel — a distinguished economics professor and former Bank of England Monetary Policy Committee member — as the new Chair of the Office for Budget Responsibility (OBR) (FT/Reuters).

The OBR is the UK’s independent fiscal watchdog, responsible for producing the economic and fiscal forecasts that underpin the government’s Budget. Its credibility is foundational to UK government borrowing costs — a well-respected OBR reassures Gilt investors that the government’s fiscal projections are independent and rigorous.

Who Is Jonathan Haskel?

Haskel is a highly credentialed economist with deep institutional knowledge of British monetary policy. As a member of the Bank of England’s MPC, he participated in some of the most consequential rate decisions of the post-pandemic era. His academic work on productivity, intangible assets, and economic measurement makes him well-suited for an institution whose core function is producing robust economic forecasts.

His appointment will be broadly welcomed by financial markets as a signal of institutional continuity at the OBR — particularly important given the political uncertainty around Reeves.

EG Group Files Confidentially for US Listing: A Billion-Dollar British Petrol Play in America

One of the most significant corporate finance stories out of the UK this week: EG Group — the British petrol station and convenience retail operator founded by the Issa brothers — has confidentially filed for a US listing that could value the company at more than $1 billion (FT/Reuters).

Background: EG Group’s Rise

EG Group is one of the UK’s most remarkable private equity-backed success stories. Founded by brothers Mohsin and Zuber Issa, the company grew from a single petrol station in Blackburn to become a global fuel retail, food service, and convenience operator with thousands of sites across Europe, North America, and Australia. Their most high-profile acquisition — buying ASDA, one of Britain’s biggest supermarkets, in 2021 — brought EG Group into the mainstream British business press.

Why a US Listing?

EG Group’s decision to file confidentially in the US — rather than London — reflects a structural trend that has been concerning British financial regulators for years: the flight of large British companies toward American capital markets.

The reasons are well-documented: the US commands higher valuations for comparable businesses, has deeper liquidity, a larger retail investor base, and a more favorable regulatory environment for many corporate structures. For a company with significant US operations — EG Group has a major American convenience and fuel retail footprint — listing on Nasdaq or NYSE also aligns their listing currency with their operational footprint.

A valuation above $1 billion would make this one of the more significant UK-origin IPOs in the US market in 2026.

The Shein Tax Loophole: Closed — But Not Until October

A third story from the FT’s digest underscores the political complexity of modern trade regulation: the UK tax loophole exploited by Shein — the Chinese ultra-fast fashion giant — will not be closed until October 2026 (FT/Reuters).

What Is the Loophole?

The loophole relates to the de minimis threshold — a customs rule that exempts very low-value imports from import duties. Shein and similar platforms have structured their logistics around this exemption, shipping individual items directly from warehouses in China to UK consumers below the value threshold that triggers duty assessment, effectively circumventing the import taxes that UK-based retailers must account for in their pricing.

The result is a structural cost advantage for Shein over domestic UK retailers — a competitive distortion that the UK government has acknowledged but has not yet been able to close.

Why the Delay?

Closing the de minimis loophole requires HMRC to update customs processing systems capable of handling millions of low-value individual parcels at scale — a non-trivial logistical and technological challenge. The October 2026 implementation date reflects the time needed to build out this infrastructure.

The business implication: UK fashion retailers and high street stores will continue to compete at a disadvantage against Shein and similar platforms for at least another four months.

The Bigger Picture: UK Economic Vulnerabilities in 2026

This week’s collection of UK finance stories paints a picture of a country managing multiple simultaneous economic pressures:

- Political uncertainty at the Treasury at a time of elevated global inflation and constrained fiscal space

- Fiscal credibility challenges that require robust independent institutions like the OBR

- Capital market competitiveness concerns as major UK companies increasingly prefer American listings

- Trade policy complexity in navigating the competitive dynamics of global fast fashion and e-commerce

These are not new problems — but they are intensifying in the current global environment. The UK’s post-Brexit economic framework, the legacy of the 2022 gilt crisis, and the ongoing challenge of productivity growth all remain unresolved background conditions for whatever Finance Minister succeeds Reeves.

Frequently Asked Questions (FAQ)

Q: Is Rachel Reeves being replaced as UK Finance Minister?

Reports from the Financial Times indicate that Andy Burnham is planning to remove Reeves from the Finance Minister role and offer her a lesser Cabinet position. This has not been formally confirmed.

Q: Who is the new OBR Chair?

Jonathan Haskel — an economics professor and former Bank of England Monetary Policy Committee member — has been nominated as Chair of the Office for Budget Responsibility by Rachel Reeves.

Q: What is EG Group and why is it listing in the US?

EG Group is a British petrol station and convenience retail operator founded by the Issa brothers. It has confidentially filed for a US listing that could value it above $1 billion. The US listing reflects broader trends of UK companies seeking higher valuations and deeper liquidity in American capital markets.

Q: What is the Shein tax loophole in the UK?

Shein exploits a de minimis customs exemption that allows very low-value imports to avoid import duties. The UK government plans to close the loophole in October 2026 pending HMRC system upgrades.

Q: What does a UK Finance Minister change mean for markets?

A change at the top of the UK Treasury introduces short-term uncertainty around fiscal policy continuity, potentially affecting Gilt yields and the pound. Markets will focus on whether the successor maintains existing deficit reduction commitments.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

With homeownership out of reach and AI threatening their careers, Gen-Z retail traders are pouring record sums into oil ETFs, meme stocks, and options. Is this rational adaptation — or a dangerous gamble?

Introduction: When the Market Becomes the Only Ladder Left

For previous generations, the path to financial security was well-marked: get an education, land a stable job, buy a house, and build equity over time. That ladder still exists — but for millions of Gen-Z Americans, many of its rungs have become unreachable.

Home prices require 30% or more of median income. Student loan defaults are surging. AI threatens to automate broad swaths of white-collar work. And traditional savings accounts, after years of near-zero rates, are only now offering yields that barely keep pace with inflation.

Against this backdrop, a growing cohort of young Americans is making a different calculation: if the rules of the game have changed, why not play the game differently?

The answer, increasingly, is: lottery-like meme stocks, leveraged options, and — most recently — crude oil exchange-traded funds. And the sums of money flowing into these instruments are breaking records (Bloomberg).

The Oil Trade: Retail’s Biggest Bet of 2026

The 2026 Iran war and the subsequent closure of the Strait of Hormuz created an event-driven trading opportunity of unusual clarity: a geopolitical crisis with obvious supply implications for a commodity with massive global demand. Retail investors recognized it immediately.

According to data from Vanda Research, net retail buying of oil ETFs hit a record $211 million in a single day on March 12, 2026 — surpassing the previous peak during the May 2020 market crash. The record set on March 6 — $42 million for the United States Oil Fund (USO) alone — was broken within days (CNBC).

“Oil is now definitely a retail ‘meme theme.’ Retail investors have been piling into the major pure-play oil ETFs ever since the start of the Iran conflict,” said Viraj Patel, global macro strategist at Vanda Research (CNBC).

Tom Sosnoff, CEO of financial technology platform Lossdog, described the phenomenon in blunt terms:

“Physical commodities like crude oil have become the speculative meme plays for 2026. First, it was silver and gold, and now it’s oil. The markets love noise and volatility. The perception among retail traders is: where there is the most activity, there is the most opportunity.” (CNBC)

What Drives This Behavior? The Economic Logic of a Cornered Generation

To understand why Gen-Z is gravitating toward high-risk trading, it helps to look at the economic environment they have inherited:

1. Homeownership: The Math Doesn’t Work

Purchasing the average-priced American home now requires roughly 30% of median household income — up 50% from pre-pandemic levels (Washington Examiner). For many young workers, the traditional wealth-building strategy of buying a home and holding it for decades is simply not financially accessible. Without real estate as an equity-building vehicle, the stock market becomes the primary path to asset accumulation.

2. AI and the Job Security Crisis

The threat of artificial intelligence to white-collar employment is not hypothetical for Gen-Z — it is the context of their entire early career. From software developers to paralegals to writers, entire career tracks that once offered stable middle-class trajectories are under pressure. The perception — whether accurate or premature — that stable employment is increasingly precarious drives a “swing for the fences” mentality in investing.

3. Student Debt and Its Aftermath

Approximately 2.6 million additional federal student loan borrowers defaulted in Q1 2026 alone, with average credit scores dropping 91 points (Experian). For the millions more who are current but stretched thin by loan payments, building wealth through conventional savings requires years of patience that feels incompatible with the pace of economic change.

4. Inflation Eroding Patience

At 4.2% CPI, every year of inaction in a savings account is a year of declining real purchasing power. The urgency this creates — whether conscious or intuitive — pushes toward higher-risk, higher-return strategies.

The Meme Stock Playbook Comes to Commodities

The parallels between the oil trading frenzy of 2026 and the GameStop/AMC mania of 2021 are striking — but with a crucial difference. Meme stocks were typically driven by narrative and social media momentum disconnected from fundamental value. The oil trade, by contrast, was grounded in a genuine supply disruption.

“Unlike a meme stock, oil supply disruption is real and based on actual production shutdowns,” noted Andy Lipow, president of Lipow Oil Associates (CNBC).

But the behavior of retail participants — the herding, the FOMO (fear of missing out), the leveraged ETF positions, the real-time coordination on social platforms — maps precisely onto the meme stock playbook. And the risks are just as severe.

“Retail investors need to remember that trading crude oil is like playing musical chairs. When the music stops, it is not going to be pretty,” Lipow warned (CNBC).

Indeed, many retail investors who bought oil ETFs at peak prices in April — when Brent surged above $120 — are now sitting on substantial paper losses as oil has retreated toward $78. The same volatility that attracted them is now working against them.

Bloomberg’s Broader Frame: Options and the Wealth Gap

Bloomberg’s analysis of the phenomenon goes beyond oil, situating it within a broader structural story: Gen-Z retail traders are using options and lottery-like instruments as a mechanism to overcome the wealth gap (Bloomberg).

The logic is mathematically coherent, even if risky:

- If you have $5,000 in savings and a house costs $500,000, conventional investing will not close the gap in a reasonable timeframe

- But a leveraged options trade on the right asset at the right moment could — at least in theory

- The expected value calculation shifts when the baseline scenario (conventional wealth accumulation) looks increasingly unattainable

This is not irrational behavior — it is a rational response to a structurally unfair starting position. But it creates systemic risk. When millions of young investors concentrate in the same volatile instruments at the same time, the resulting price swings can cause cascading losses that wipe out precisely the financial foundation they were trying to build.

The Zuckerberg Wildcard: Crypto, Meme Coins, and the Trillionaire Race

Adding further texture to the Gen-Z investment landscape, prediction market platform Kalshi’s traders have identified Meta CEO Mark Zuckerberg as the “best shot to join the trillionaire club with Elon Musk” (CNBC). This kind of predictive wagering — on the outcomes of business competitions and wealth rankings — represents another dimension of the financialization of everyday life for a generation that has grown up with sports betting normalization, crypto, and real-money fantasy finance.

What Should Young Investors Actually Do?

The structural problem — that conventional wealth-building paths are increasingly inaccessible — is real. But the response matters enormously:

What carries disproportionate risk:

- Leveraged ETFs (2x or 3x oil, volatility products) — designed for short-term trading, decay rapidly if held

- Single-stock options without risk management — can go to zero

- Concentrated meme positions — subject to sudden reversals

What remains valid even in a high-risk environment:

- Low-cost index funds in tax-advantaged accounts (IRA, 401k) — compound over time with minimal fees

- I-bonds and TIPS — inflation protection for savings

- High-yield savings accounts and short-term CDs — with rates at 3.5–3.75%, the opportunity cost of holding cash has never been lower

- Fractional real estate platforms — offer exposure to real estate without a $500,000 entry point

Frequently Asked Questions (FAQ)

Q: Why are Gen-Z investors buying oil ETFs?

The 2026 Iran war and Strait of Hormuz closure created a clear supply-disruption thesis that attracted record retail investment into crude oil ETFs. Net retail buying hit $211 million in a single day in March 2026.

Q: Is oil trading like meme stocks?

In terms of retail behavior — herding, social media coordination, leveraged instruments — yes. But unlike classic meme stocks, the oil price move was grounded in a real supply disruption, making it more of a legitimate trade that attracted speculative excess.

Q: Why are young Americans taking more investment risk?

A combination of unaffordable housing, student debt, AI-driven job insecurity, and persistent inflation has made conventional wealth-building feel inaccessible. Higher-risk strategies feel rational when the baseline scenario is bleak.

Q: What happened to retail investors who bought oil at peak prices?

Investors who bought oil ETFs at peak prices (April–May 2026, when Brent exceeded $100–120/barrel) are sitting on paper losses as prices have retreated to ~$78 following the Hormuz reopening.

Q: What are safer alternatives for Gen-Z investors?

Index funds in tax-advantaged accounts, I-bonds, high-yield savings, and diversified portfolios remain the most reliable long-term wealth-building strategies — even if the returns feel inadequate relative to the scale of the housing and wealth gap.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Home prices in Denver and other US cities are falling in 2026. Renters celebrate cheaper housing — but economists ask a harder question: Is this affordability relief, or the early signal of economic decline? Here’s the analysis.

Introduction: When Cheaper Housing Isn’t Simple Good News

At first glance, falling home prices sound like exactly what a country with a severe housing affordability crisis needs. For Denver renters who have watched costs escalate relentlessly since the pandemic, the recent softening in housing costs is welcome relief.

But economists have a more complicated reaction. When home prices fall — particularly in cities that were recently among the hottest housing markets in America — they don’t always signal that the affordability problem has been solved. Sometimes, they signal something more troubling: that the underlying economy is weakening.

Denver is now at the center of this analytical debate. And as home prices soften in other cities across the country, it’s a question worth examining carefully (NPR).

What Is Happening to Denver’s Housing Market?

Denver was one of the standout boomtowns of the 2020s housing surge. Remote work migration, a young professional demographic, and a thriving tech and energy economy drove prices to levels that became increasingly unaffordable for the city’s residents. Median home prices in metro Denver surged dramatically from pre-pandemic levels, and rents followed.

Now, that dynamic is shifting. As of mid-2026, Denver is reporting falling housing costs — one of a number of US metropolitan areas where the post-pandemic price surge is unwinding. The question that economists are debating is the why.

Two competing explanations exist:

Explanation 1: Supply-Side Normalization (Positive)

Denver and cities like it built more housing during the construction boom of 2022–2025. Combined with slowing in-migration as remote work norms stabilized, and some cooling in the labor market, supply may simply be catching up with demand. If this is the driver, falling prices represent genuine affordability relief — exactly what the housing market needs.

Explanation 2: Demand-Side Weakness (Warning Signal)

Alternatively, if prices are falling because economic conditions in Denver are deteriorating — layoffs, slowing business formation, rising unemployment, or declining consumer confidence — then the price decline is a symptom of economic distress, not a healthy market correction. In this scenario, cheaper housing accompanies a weaker job market, eroding the financial position of the very households who benefit from lower rents.

The National Pattern: Denver Isn’t Alone

Denver is not an isolated case. Across the United States, a divergence is emerging between housing markets:

- Cities with supply surplus (Austin, Phoenix, parts of Florida and the Mountain West): Prices are declining as pandemic-era construction catches up with demand

- Supply-constrained cities (New York, San Francisco, Seattle): Prices remain sticky despite affordability stress

- Economically cooling cities (Denver, parts of the Midwest): Price declines may reflect both supply and demand factors simultaneously

The national picture is complicated by a mortgage rate lock-in effect. With the Federal Reserve holding rates at 3.5%–3.75% and potentially raising them further, the millions of homeowners who locked in sub-3% mortgages during 2020–2021 have almost no incentive to sell — dramatically constraining housing inventory in most markets even as prices soften at the margin.

The Affordability Backdrop: Still Crisis-Level Nationally

Even with some local softening, the national housing affordability picture remains dire. Purchasing the average-priced American home now requires about 30% of median household income — up approximately 50% from pre-pandemic levels (Washington Examiner).

The newly passed 21st Century ROAD to Housing Act aims to address this structurally through supply increases and zoning reform. But housing economists project that even the most optimistic supply-side reforms will take two or more years to meaningfully move the national affordability needle.

In the interim, what happens to housing markets in cities like Denver serves as an early-warning system for the broader economy.

Rents vs. Home Prices: Different Dynamics

It is important to distinguish between falling home prices and falling rents:

- Home prices primarily affect buyers, sellers, and homeowner wealth. Falling prices help first-time buyers enter the market, but harm existing owners who bought near the peak.

- Rents affect the much larger population of renters who do not benefit from asset appreciation. Falling rents provide immediate household budget relief.

In Denver, both are reportedly declining — which suggests excess inventory is building in both the purchase and rental markets. This dual softening is the pattern most consistent with economic cooling rather than purely supply-side normalization.

The Inflation Paradox: Shelter Costs Still Rising Nationally

While Denver-specific costs are softening, the national shelter inflation component of the CPI rose 3.3% year-over-year in May 2026 (Experian). This reflects the lag built into the way shelter costs are measured in the CPI — rental contracts signed in 2023–2024 at high rates continue to flow through the index even as new leases may be pricing lower in certain markets.

This creates a policy challenge for the Fed: shelter inflation looks elevated in the data even as market rents in softening cities like Denver are actually falling. It means the CPI may be overstating actual housing cost pressures for current renters in those markets — but will only correct with a lag.

What Falling Prices Mean for Key Stakeholders

First-Time Homebuyers in Denver

Falling prices are genuinely positive for first-time buyers who have been locked out. With the new housing bill also expanding small-dollar mortgage programs, Denver could become more accessible — provided the local economy remains healthy enough to support new homeownership.

Recent Buyers (2021–2024)

Those who bought near the peak face the prospect of negative equity — a situation where their mortgage balance exceeds their home’s current market value. This constrains mobility (can’t sell without a loss) and can trigger financial stress if accompanied by income shocks.

Landlords and Investors

Landlords in markets with falling rents face margin compression, especially if they financed acquisitions at peak valuations and current rates. The institutional investor cap in the new housing bill adds another dimension — restricting the ability of large investors to absorb excess inventory.

The Broader Economy

Housing wealth effects matter. When homeowners see their property values decline, they typically reduce consumption. If Denver’s price declines spread to a significant share of the US housing market, the negative wealth effect could meaningfully slow consumer spending — a potential drag on GDP.

How to Read the Signal: Four Indicators to Watch

To determine whether Denver represents healthy correction or economic warning, analysts will track:

- Local unemployment data — Rising unemployment alongside price falls confirms demand-side weakness

- Rental vacancy rates — Rising vacancies suggest supply surplus; stable vacancies with falling rents suggest demand weakness

- New household formation rates — Are young adults forming households or doubling up? The latter signals economic stress

- Foreclosure and delinquency trends — An increase would confirm that price declines are stress-driven rather than supply-driven

Frequently Asked Questions (FAQ)

Q: Are home prices falling nationally in 2026?

Prices are falling in select markets including Denver and parts of the Mountain West and Sun Belt. They remain sticky in supply-constrained major metros. There is no nationwide uniform price decline.

Q: Why are Denver home prices falling?

A combination of factors: post-pandemic construction catching up with demand, slowing in-migration, remote work normalization, and possible economic cooling. Economists are debating the relative weight of each factor.

Q: Is falling home prices good or bad for the economy?

It depends on the cause. Supply-driven price declines are healthy — they improve affordability. Demand-driven declines signal economic weakness. Denver’s situation may involve both.

Q: Does the new housing bill help Denver?

Indirectly. The 21st Century ROAD to Housing Act focuses on national supply-side reform. In a market like Denver where supply is already loosening, the bigger near-term factor will be the trajectory of the local economy and interest rates.

Q: How does shelter inflation stay high if Denver rents are falling?

The CPI’s shelter component lags market conditions by 12–18 months due to the way rental contracts are measured. Falling market rents in Denver today will only appear in the shelter CPI months from now.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

US Household Debt Hits $18.8 Trillion as Student Loan Defaults Surge

UK in Political and Economic Flux: Reeves Faces Demotion, OBR Gets New Chair, EG Group Eyes US Listing

How Oil ETFs, Meme Stocks, and Options Became the New American Dream

Denver Home Prices Are Falling — Is This Housing Relief or Economic Warning Sign?

How the 2026 Iran War Reshaped the Global Economy

US Inflation Hits 4.2%: A Three-Year High Squeezing American Households and Cornering the Fed

Iran Nuclear Deal in Limbo: Trump Claims Inspection Agreement, Tehran Denies It

Oil Falls, Stocks Surge — But Analysts Warn Markets Are Pricing in Too Much Hormuz Optimism

Congress Passes Landmark Housing Affordability Bill

Kevin Warsh’s Fed Delivers “Regime Change”: Rate Hike Now Looms Over US Economy

Goldman Sachs: “The Circulatory System Is Not Working”

Why the U.S. Budget Airline Model Is Running Out of Runway

China’s Oil Shock Absorber: How Beijing Kept Crude Prices Half of What Analysts Predicted

CRH Nears Biggest-Ever Deal to Acquire Arcosa

China Overhauls the World’s Biggest Surveillance Network with Advanced AI

SpaceX IPO: Inside the $2 Trillion Market Debut

KPMG Australia CEO Resigns After Whistleblower Claims Exposed Investigation Failures

PwC China Partner Payouts Cut Amid Evergrande Audit Fraud

Broadcom Market Value Loss: Revenue Forecast Disappoints

Pakistan Budget FY 2026-27: Relief, Prospects, and the Tightrope Walk

Benefitbay Raises $18M to Build the Plumbing for America’s ICHRA Shift

Here’s How Much It’ll Cost You to Be Part of SpaceX’s Record-Breaking $75 Billion IPO

Nasdaq Tumbles 4% as Chip and Memory Stocks Sink: A $1.2 Trillion Wipeout

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Japanese Mid-Sized Firms Flock to Southeast Asia for Growth

Smash Capital Leads $200M Funding for Allen Control Systems

The Ferrari Luce Is Finally Here — and It’s Already Dividing the Room

How to Fix Pakistan’s Debt Economy: A Structural Blueprint

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 months ago

Analysis4 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks5 months ago

Banks5 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment5 months ago

Investment5 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025