Analysis

Iran War Singapore Growth & Inflation 2026: Gan’s Warning Explained | A Wake-Up Call for Asia

DPM Gan Kim Yong told Parliament on April 7, 2026 that the Iran war will hurt Singapore’s GDP and push inflation higher. Here’s what it means for Asia’s open economies — and why the forecast revision coming in May could be the most consequential in a decade.

Singapore’s Moment of Reckoning Has Arrived

The chamber was unusually charged for a Tuesday afternoon. More than seventy parliamentary questions had been filed — a volume that, by Singapore’s meticulous standards, signals genuine institutional alarm. When Deputy Prime Minister and Minister for Trade and Industry Gan Kim Yong rose to address Parliament on April 7, 2026, the words he delivered were neither catastrophist nor comforting. They were something more unsettling than both: calibrated, honest, and unmistakably ominous. “As a small and highly open economy,” he said, “Singapore will not be able to insulate ourselves completely from this crisis. Growth in the coming quarters is likely to be affected by the ongoing conflict.”

Outside on Shenton Way, the morning’s trading boards told a parallel story — the Straits Times Index down, freight quotes climbing, electricity tariffs that had already been revised upward on April 1 now looking like a floor rather than a ceiling. For Singapore, a city-state with no hinterland, no domestic energy base, and no insulation from the global price of anything, the Iran war is not a distant geopolitical abstraction. It is an arriving economic storm, and Gan’s parliamentary statement was the clearest official admission yet that the government’s own forecasts — upgraded as recently as February to a bullish 2% to 4% GDP growth for 2026 — will need to be revisited.

This is the story of why that revision matters, and what it reveals about the structural vulnerabilities of every small, trade-dependent economy in a world increasingly shaped by great-power conflict.

Not Ukraine Redux: Why This Shock Is Different in Kind

Experienced market watchers were quick to reach for the 2022 Russia-Ukraine playbook when the US-Israeli strikes on Iran began on February 28, 2026. That instinct is understandable but analytically dangerous. The Ukraine episode was primarily a European energy shock — devastating for the continent’s natural gas grid, but geographically contained in ways that allowed Asian economies to pivot rapidly toward alternative suppliers and routes. The Iran war is something structurally different, and more globally corrosive.

The Strait of Hormuz, through which approximately 20% of the world’s traded oil passes alongside vast volumes of liquefied natural gas, does not have a European bypass. The closure of the strait triggered by the conflict has disrupted roughly a fifth of global oil supply, sending Brent crude surging to over US$82 per barrel — a 30% increase since the start of 2026 and the highest level since January 2025. Unlike the Suez Canal, for which alternative routing around the Cape of Good Hope is slow and costly but physically possible, the Hormuz chokepoint forces rerouting that simply cannot be accomplished at comparable volumes or speed.

More critically, the war’s cascading effects are not bounded by energy markets. Analysts have described the economic impact as the world’s largest supply disruption since the 1970s energy crisis, encompassing surges in oil and gas prices, wide disruptions in aviation and tourism, and volatility in financial markets. That characterisation — the 1970s benchmark — is one that Singapore’s older policymakers understand viscerally. The 1973 oil embargo reshaped the city-state’s energy strategy for a generation. What is unfolding in 2026 is arriving with far greater interconnectedness and far less margin for response.

The Four Channels: How the Iran War Hits Singapore’s Economy

Energy and Chemicals: The First and Loudest Channel

Singapore is one of Asia’s pre-eminent refining and petrochemicals hubs. Its Jurong Island complex processes millions of barrels of crude annually, supplying refined products and chemical feedstocks across the region. When global crude prices surge and Gulf supply contracts abruptly, the feedstock economics of that entire industrial ecosystem are upended. Parliamentary questions filed for the April 7 sitting explicitly asked whether Singapore’s petrochemical and refining sectors face risks to output, margins and competitiveness given the republic’s role as a regional energy and chemicals hub.

Gan confirmed that the spike in global oil and natural gas prices will inevitably raise fuel and electricity costs for Singapore, and that cost increases will “feed through to broader inflation.” He went further, calling the supply disruption from the Hormuz closure “the worst disruption since the 1973 oil embargo” — language that carries particular weight from a minister known for understatement.

Electricity tariffs were already revised upward from April 1. Singaporean authorities have warned of sharper increases to come, with cooking gas prices also rising, though some providers said they may absorb costs for hawker centres. For industrial consumers — manufacturers, data centres, cold-chain logistics — these are not headline distractions. They are margin compressors arriving on top of already elevated input costs.

Manufacturing: The Second-Round Hit

Singapore’s manufacturing sector — which encompasses electronics, biomedical products, and advanced chemicals — does not consume crude oil directly in most of its processes. But energy is embedded in every stage of global supply chains, and when shipping costs and input prices rise simultaneously, the squeeze reaches even the most advanced factories.

Senior economists at DBS Group Research noted that Singapore’s economy is confronting uncertainty from a relatively strong position, with solid growth momentum buoyed by global AI-related tailwinds and still-low inflation at the start of 2026. That strength, real as it is, does not make the republic immune to margin compression in its externally-facing industries. Semiconductor packaging, precision engineering, and pharmaceutical manufacturing all depend on global logistics networks whose costs are now rising sharply.

The AI demand tailwind that powered Singapore’s manufacturing resilience through early 2026 remains intact — demand for advanced chips has not diminished. But when energy and transport costs rise across the supply chain, even AI-driven production is not entirely insulated. Earnings risk for Singapore’s listed manufacturers is real and, as yet, inadequately priced by equity markets.

Transport and Travel: The Visible Daily Pain

Here is where the economic shock becomes humanised. Jet fuel prices have climbed in lockstep with crude, squeezing airline operating margins and threatening the air connectivity on which Singapore’s Changi Airport — the city’s most strategically important piece of infrastructure — depends. Parliamentary questions addressed fare adjustments by ride-hailing operators Grab and ComfortDelGro, asking whether the Ministry of Transport was consulted and what regulatory oversight is in place to prevent private-hire and taxi operators from passing on fuel costs unchecked. The fact that cab drivers received a S$200 fuel subsidy in the April 7 package is telling: the government recognises that transport cost pass-throughs are already live.

Aviation and tourism were singled out among the sectors facing wide disruptions from the conflict. For Singapore, which has positioned itself as Asia’s premier transit hub and whose aviation-adjacent services — hospitality, MICE, retail — form a meaningful slice of services GDP, a sustained softening in air traffic flows is a multi-quarter drag that GDP models may not yet fully capture.

Domestic Services: The Inflation Spiral That Begins in Changi Road

The most economically insidious channel is the one that receives the least analytical attention: the inflationary pass-through into domestic services. When fuel prices rise, school bus operators raise fares — something already visible in Singapore’s local reports. When electricity tariffs rise, restaurants’ operating costs rise; when food import costs climb because freight is more expensive, hawker centre prices follow. These are the mechanisms through which an energy shock migrates from the oil market to the heartland household.

As school bus driver V. Parath put it plainly: “The price of everything in Singapore is increasing.” That is not merely anecdote. It is a leading indicator that core inflation is beginning to broaden from energy and transport into services — a broadening that, once embedded in wage expectations, becomes structurally stickier.

Pull Quote: “This is not a standard energy shock. It is a simultaneous hit to feedstock costs, freight rates, exchange-rate dynamics and consumer confidence — arriving in an economy that was already managing multiple transition pressures. Singapore’s buffers are real and substantial. But buffers are finite.”

The Macro Ripple: MAS, the SGD, and an Unenviable Policy Dilemma

The Monetary Authority of Singapore’s principal policy instrument is the exchange rate, not the interest rate. The central bank manages the Singapore dollar against an undisclosed basket of trading partner currencies within a policy band, adjusting the slope, width, and centre of that band to target imported inflation. In a standard energy shock, the textbook response is to allow or even encourage modest SGD appreciation to absorb imported price increases.

MAS confirmed in early March that it is conducting a formal assessment of the domestic financial system’s exposure, and that the Singapore dollar nominal effective exchange rate remains within its established appreciating policy band — positioning intended to dampen imported inflationary pressures.

But the policy dilemma is more complex than the textbook suggests. Broader dollar strength driven by safe-haven demand and reduced US Federal Reserve rate-cut expectations — with futures markets now pricing the first fully priced Fed cut as late as September, two months later than the July consensus prevailing before the conflict — has compressed Singapore’s room to manoeuvre. A SGD that appreciates against the USD provides some imported-price relief but simultaneously hits the competitiveness of Singapore’s export-facing industries at precisely the moment when their margins are already being squeezed.

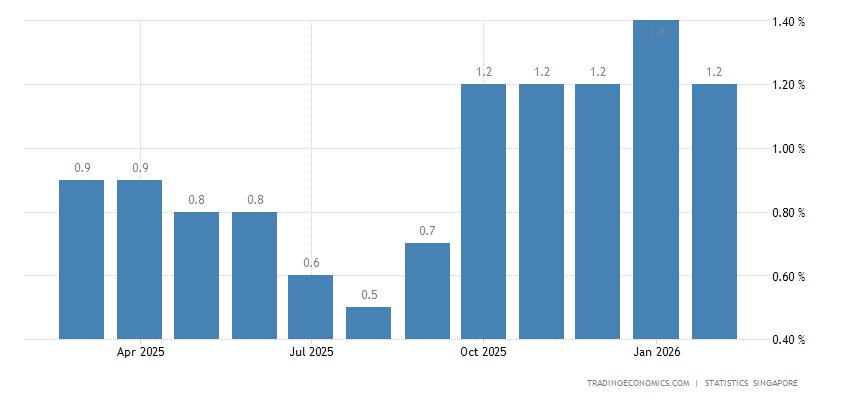

Maybank economist Chua Hak Bin had flagged inflation as an underappreciated risk in 2026, citing rising semiconductor prices and the unwinding of Chinese export deflation — a deflationary cushion that had kept manufactured goods prices suppressed for several years. A Gulf supply shock superimposes an energy cost surge on top of those pre-existing pressures. If the conflict persists beyond four to six weeks, Singapore’s core inflation could break above MAS’s 1–2% forecast band, creating pressure on the central bank to shift its exchange-rate policy.

That band adjustment, if it comes, will be one of the most significant MAS signals in years — and it is coming into view.

The Limits of “Safe Haven”: Why Singapore Is Not Immune to Structural Fragmentation

For a generation, Singapore cultivated — and largely deserved — a reputation as Asia’s most resilient small open economy: deep reserves, AAA fiscal credibility, trade agreements with virtually every major partner, and an uncanny institutional capacity to navigate geopolitical turbulence without becoming its casualty. That reputation is not false. But this crisis is exposing its conditionality.

Coordinating Minister for National Security K. Shanmugam warned on April 7 that markets have yet to factor in the worst-case scenario — and that Singapore cannot rule out power disruptions if the conflict in Iran further disrupts global energy supplies. A sitting minister explicitly raising the spectre of power disruption in a city whose every competitive advantage rests on the reliability of its infrastructure is not rhetoric — it is a risk disclosure.

The structural issue is one that Singapore shares with a cohort of ultra-open economies whose prosperity was architected for a rules-based, multilateral trade order. Taiwan, South Korea, and the Netherlands are the most obvious analogues. Each is deeply integrated into global supply chains, each imports most of its energy needs, and each has built extraordinary competitiveness precisely by maximising openness rather than pursuing autarky. In a world of discrete shocks — a pandemic here, a trade dispute there — openness is the right bet. In a world where great-power conflict is becoming endemic rather than episodic, that calculus deserves harder scrutiny.

The Iran war’s economic impact is not merely a supply shock. It is a signal that the frequency and geographic scope of geopolitical disruptions may be structurally higher going forward than the models that underpin Singapore’s growth forecasts were calibrated for. When Gan says growth in the coming quarters will be “affected,” he is describing an outcome. The deeper question is whether Singapore’s — and Asia’s — planning frameworks are being updated to account for a world where such statements become a recurring feature rather than an exception.

May’s Forecast Revision: What to Expect — and Fear

Singapore’s GDP advance estimate for the first quarter is due on April 14, with a full economic outlook update scheduled for May. The first-quarter numbers will almost certainly show resilience — Gan himself acknowledged that early data indicate economic activity held up well through Q1. That resilience, largely built on AI-driven electronics demand and services strength, will briefly reassure markets.

May’s revision is another matter. The 2% to 4% full-year GDP forecast issued in February was calibrated for a world in which the Iran conflict was either resolved or contained within weeks. Singapore’s predicament is shaped by geography as much as policy — the republic sits far from the conflict zone, yet its economy is tied tightly to global trade, imported food and imported fuel. Any threat to Gulf energy production or maritime passage through strategic chokepoints can ripple quickly into Asian benchmark prices, freight costs and business sentiment.

A sustained conflict — and with over a month of fighting already in the books, “sustained” is no longer a tail risk — points to a revised growth forecast closer to the lower end of the current range or potentially below it. Inflation forecasts, already tracking against MAS’s 1–2% core target band, are likely to be revised upward. For households and SMEs that have not yet felt the full pass-through of April’s electricity tariff increase, the coming months will be measurably harder.

What Policymakers Must Do — and What Singapore Offers as Model

The S$1 billion support package unveiled on April 7 — boosting the corporate income tax rebate from 40% to 50%, advancing grocery vouchers to June, and providing S$200 supplements to both eligible households and cab drivers — is competent crisis management. It cushions the immediate pain, demonstrates governmental responsiveness, and signals institutional credibility to markets. It is not, however, a structural solution.

For Singapore specifically, the priorities are now fourfold. First, accelerate energy diversification — Shanmugam noted that Singapore is studying alternatives including nuclear power to broaden its fuel mix, a move that was politically contentious eighteen months ago and is now strategically urgent. Second, extend supply-chain diplomacy aggressively: the Singapore-Australia joint energy security statement of March 23, 2026 is exactly the kind of bilateral redundancy-building that needs to be replicated across multiple partners and commodity categories. Third, provide targeted, time-limited support for SMEs facing acute energy and freight cost pressure — the risk of SME failures compressing domestic employment and spending is underappreciated. Fourth, and most importantly, begin recalibrating the medium-term planning framework to assume a structurally less stable geopolitical environment than the one that informed Singapore’s last decade of growth strategy.

For the broader cohort of open Asian economies — South Korea, Taiwan, Vietnam, Thailand — Singapore’s predicament is a live case study in vulnerabilities they share. The lesson is not to retreat from openness, which remains the correct long-term bet for small economies without large domestic markets. It is to build genuine redundancy into energy, food, and supply-chain systems; to cultivate multiple geopolitical relationships that provide diplomatic buffer in crises; and to hold fiscal capacity in reserve precisely for moments like this one.

Singapore has those reserves. Its institutions are among the world’s most capable. The response so far has been measured, credible, and appropriately scaled. But Gan’s words in Parliament on April 7 should be read not only as a situational update but as a structural warning — to Singapore, and to every economy that built its prosperity on the assumption that the global order would remain permissive. That assumption is now, unmistakably, in question.

The bumpy ride ahead is not Singapore’s alone.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025