Budget

Pakistan Budget 2026-27 Predictions: IMF Curbs & Economy

In the corridors of Islamabad’s Q Block, the mood is less about statecraft and more about pure financial survival. As the government finalises the federal budget for the fiscal year starting in July, policymakers are trapped in an unforgiving straitjacket tailored by the International Monetary Fund. There is zero fiscal space left for political grandstanding. Instead, the upcoming fiscal plan is a brutal arithmetic exercise in managing absolute scarcity. With public debt soaring and the electorate thoroughly exhausted by relentless inflation, the administration must balance the uncompromising demands of foreign creditors against the breaking point of domestic households. The raw numbers reveal a state barely keeping its head above water.

The upcoming presentation on June 10 will not be a celebration of economic strategy, but a stark admission of systemic vulnerability.

To understand the current fiscal paralysis, one must look at the macro constraints choking Pakistan’s policy flexibility. The country narrowly averted a sovereign default in 2023, buying essential breathing room through a $7 billion IMF programme. Yet, that lifeline came with draconian conditions that continue to define every fiscal decision made by Finance Minister Muhammad Aurangzeb and his team.

The structural adjustments—characterised by tight monetary policy, unyielding import controls, and steep energy tariff hikes—have technically stabilised the external account but suffocated domestic growth. The lived economy remains exceedingly harsh. Despite official claims of a recovery, businesses hesitate to invest, and the purchasing power of the salaried class has entirely evaporated. Recent data indicates that while Q3 2025-26 GDP growth crawled to an anaemic 3.99 percent, industrial capacity remains chronically underutilised.

This is the classic low-growth equilibrium. The system is stable enough to avoid a spectacular, cascading collapse, yet fundamentally too weak to generate the jobs required by a swelling, youthful population. As the budget announcement approaches, the tension between appeasing international lenders and pacifying frustrated, tax-burdened citizens has never been more acute.

The Core Development: An Erasure of Public Spending

Any credible analysis of the Pakistan Budget 2026-27 predictions must begin with the utter decimation of public spending. The most revealing metric of the state’s fiscal desperation is the Public Sector Development Programme (PSDP). Historically, this fund has served as the government’s primary engine for long-term infrastructure, financing everything from dams and motorways to provincial hospitals. This year, it has been systematically hollowed out to meet creditor demands.

Planning Minister Ahsan Iqbal recently delivered a stark, unvarnished warning to the Annual Plan Coordination Committee: the government is forced to reject roughly $10.7 billion (Rs3 trillion) worth of project demands. Out of an effective national requirement exceeding Rs4 trillion just to maintain the current pace of work, the federal PSDP has been severely capped at Rs1.126 trillion due to explicit IMF restrictions on the fiscal deficit.

This is not simply a routine belt-tightening measure. It is an effective freeze on the physical future of national development.

When accounting for existing political obligations—such as the Rs125 billion ring-fenced for the critical N-25 highway in Balochistan and mandatory rupee-cover requirements for foreign-funded initiatives—the actual funds available for ongoing, uncommitted schemes drop to a meagre Rs165 billion. The situation represents what planners are calling a new circular debt crisis in physical infrastructure.

The state is currently carrying an unsustainable Rs11 trillion in throw-forward liabilities spread across 800 stalled projects. At the current pace of restricted funding, clearing this monumental backlog would take more than a decade, assuming no new projects are ever approved. Consequently, federal ministries have been told that new schemes are entirely off the table for the foreseeable future. The effective PSDP stands broadly at the same nominal level it was in 2018, completely erasing eight years of inflation, population growth, and escalating infrastructure decay.

For the average citizen, this translates to deteriorating roads, delayed energy projects, and abandoned civic initiatives. For the coalition government led by Prime Minister Shehbaz Sharif, it means entering the new fiscal year entirely stripped of the traditional patronage tools historically used to secure political loyalty. There are no ribbon-cutting ceremonies awaiting them in FY27. They must instead manage the severe political fallout of a budget that structurally prioritises foreign debt servicing over public welfare, raising domestic taxes while freezing the physical development of the nation.

Analytical Layer: The Machinery of Demand Compression

Moving beyond the headline allocations, the upcoming fiscal plan offers a masterclass in macroeconomic constraints. The FY27 budget expectations hinge on a fundamental shift in how the state extracts and deploys its revenue. Because the prevailing framework explicitly demands a primary surplus, the Federal Board of Revenue will be tasked with highly aggressive, almost punitive, tax collection targets.

This brings us to the most pressing question for both the markets and the public:

How will the IMF program affect Pakistan’s FY27 budget?

The IMF program forces the FY27 budget to prioritise heavy taxation and severe expenditure cuts over economic growth. It severely restricts public development spending, mandates aggressive FBR revenue targets through increased indirect taxes, and eliminates broad subsidies, ensuring that debt servicing and external stability consistently supersede all domestic economic relief efforts.

Because taxing politically entrenched, undocumented sectors—like urban real estate, wholesale retail, and agriculture—remains toxic for the ruling elite, the burden will inevitably fall on the already squeezed formal sector. We can expect heavy adjustments to the tax slabs for the salaried class and corporate entities. While there is quiet chatter in financial circles about phasing out the corporate super tax to stimulate market capitalisation on the Pakistan Stock Exchange, any relief granted there will likely be offset by heightened petroleum levies and the aggressive withdrawal of sales tax exemptions on basic goods.

The strategy is essentially demand compression by deliberate design.

The central bank’s tight monetary policy works in perfect, devastating tandem with these fiscal contractions to suppress import demand and carefully maintain foreign exchange reserves. Yet, this approach ignores a glaring structural flaw: a government cannot tax its way out of a solvency crisis if the underlying industrial base is actively shrinking.

Energy costs remain the primary culprit eroding industrial competitiveness. As tariffs rise repeatedly to curb the power sector’s massive circular debt—which has been allocated Rs91 billion in the upcoming plan just to keep the lights on—manufacturers are priced entirely out of international export markets. The government is essentially taxing the productive, export-oriented elements of the economy to finance the operational inefficiencies of the state power apparatus.

It is a textbook vicious cycle. A higher tax burden on a shrinking formal economy invariably leads to capital flight and widespread tax evasion. This, in turn, forces the government to introduce even more regressive indirect taxes to meet its unyielding mandates, further crushing the purchasing power of the lowest income deciles.

Implications & Second-Order Effects: A Frustrated Federation

The downstream consequences of this extreme austerity budget will ripple violently through both the macroeconomic landscape and the daily lives of millions of citizens. Forward-looking indicators suggest that corporate profitability in the large-scale manufacturing sector will remain severely muted for at least the next four quarters.

Businesses simply cannot absorb another year of 20-plus percent borrowing costs combined with exorbitant, globally uncompetitive energy bills. Consequently, we will likely see a continued freeze on capital expenditure across major industries. Firms are rationally opting to park their excess liquidity in risk-free government securities rather than expanding factory floors, hiring new shifts, or upgrading vital technology. This systemic crowding out of private sector credit directly stifles innovation and prevents the very export-led growth the country so desperately needs.

For the middle class, the implications are equally grim, if not worse. The erosion of real wages is accelerating at a terrifying pace. While the government might announce nominal adjustments to pensions and public sector salaries to prevent outright civil unrest on the streets of Lahore and Karachi, these meagre increments will be swiftly consumed by the persistent inflationary pressure driven by indirect taxes and fuel levies. The lived reality for households will be a sustained, painful decline in overall living standards.

Moreover, the geographical disparities in development will rapidly widen. With the federal government severely rationing its PSDP allocations, provincial governments are forced to step in to fill the void, but they possess vastly unequal resources.

Punjab, commanding 46 percent of the provincial development outlay with a substantial Rs1.45 trillion allocation, will continue to outpace the rest of the nation economically. Conversely, regions like Sindh (allocated Rs816 billion) and Khyber Pakhtunkhwa (allocated Rs564 billion), despite their own budgets, will struggle to cover the massive federal shortfall in mega-infrastructure projects.

This dynamic places immense strain on the federation. When the central government withdraws from its foundational developmental role due to relentless macroeconomic stabilisation policies, the social contract fundamentally frays. It breeds deep, lasting resentment in underdeveloped districts, particularly in Balochistan, where the total lack of basic infrastructure fuels broader political instability. The FY27 budget will not just dictate the economic trajectory of the next twelve months; it will silently reshape the political geography of the country, deepening the dangerous fault lines between the affluent urban centres and the historically neglected periphery.

Competing Perspectives: The Austerity Debate

There is, however, a sharply contrasting perspective quietly gaining traction among sovereign bondholders, banking executives, and multilateral technocrats. From their comfortable vantage point, the severe austerity embedded in the FY27 budget is not a tragedy, but a long-overdue triumph of necessary fiscal discipline.

The steel-manned argument for the government’s approach is that Pakistan is finally curing the underlying disease rather than endlessly treating the symptoms. For decades, the country financed artificial, politically motivated growth through unsustainable external borrowing and heavily unfunded subsidies. The current pain, proponents argue, is simply the unavoidable withdrawal symptom of breaking a fatal, debt-fuelled consumption habit. By strictly adhering to the painful prescriptions, the Ministry of Finance is successfully rebuilding the international credibility required to secure future investment.

Proponents of this view point to the recent stabilisation of the rupee and the gradual, hard-fought rebuilding of foreign exchange reserves as definitive proof that the bitter medicine is working. They argue that compressing development spending is the only rational, mathematically sound choice when debt servicing consumes more than half of all federal revenues. You cannot build highways when you cannot afford to pay the interest on the loans that built the last ones.

However, dissenting economists warn that this view is dangerously myopic and self-defeating.

Prominent analysts and former fiscal managers have repeatedly cautioned that structural stabilisation without a coherent, parallel growth strategy is a dead end. The counter-argument posits that the current one-size-fits-all demand compression is actively destroying Pakistan’s long-term productive capacity. By starving the PSDP of critical funds, the government is neglecting the very infrastructure—digital networks, transport logistics, and human capital—required to boost exports and generate the dollars needed to repay future debt. In this view, the current budget isn’t saving the economy at all; it is merely suffocating it slowly to ensure that foreign creditors get paid on time, transferring the entire cost of the sovereign debt crisis onto the backs of the working class.

The Arithmetic of Survival

Ultimately, the budget document scheduled for June 10 will serve as a stark mathematical reflection of a state comprehensively backed into a corner. The fundamental tension between the sovereign requirement to invest in the prosperity of its people and the binding contractual obligation to satisfy international creditors has been decidedly won by the latter. The coalition government is executing a fiscal plan largely devoid of hope, designed solely to buy another 12 months of survival in the unforgiving arena of global finance.

Citizens and corporate investors alike must prepare for a year of structural stagnation. There will be no grand economic stimulus packages, no sweeping, transformative tax reliefs for the exhausted salaried class, and no monumental infrastructure rollouts to celebrate.

Instead, the administration will continue its precarious high-wire act. It will attempt to extract just enough tax revenue to appease the watchful eyes in Washington without triggering a total, irreversible collapse of the formal domestic economy. The numbers will balance on a spreadsheet, but the streets will feel the deficit. It is a budget built entirely for endurance, abandoning all immediate illusions of prosperity.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

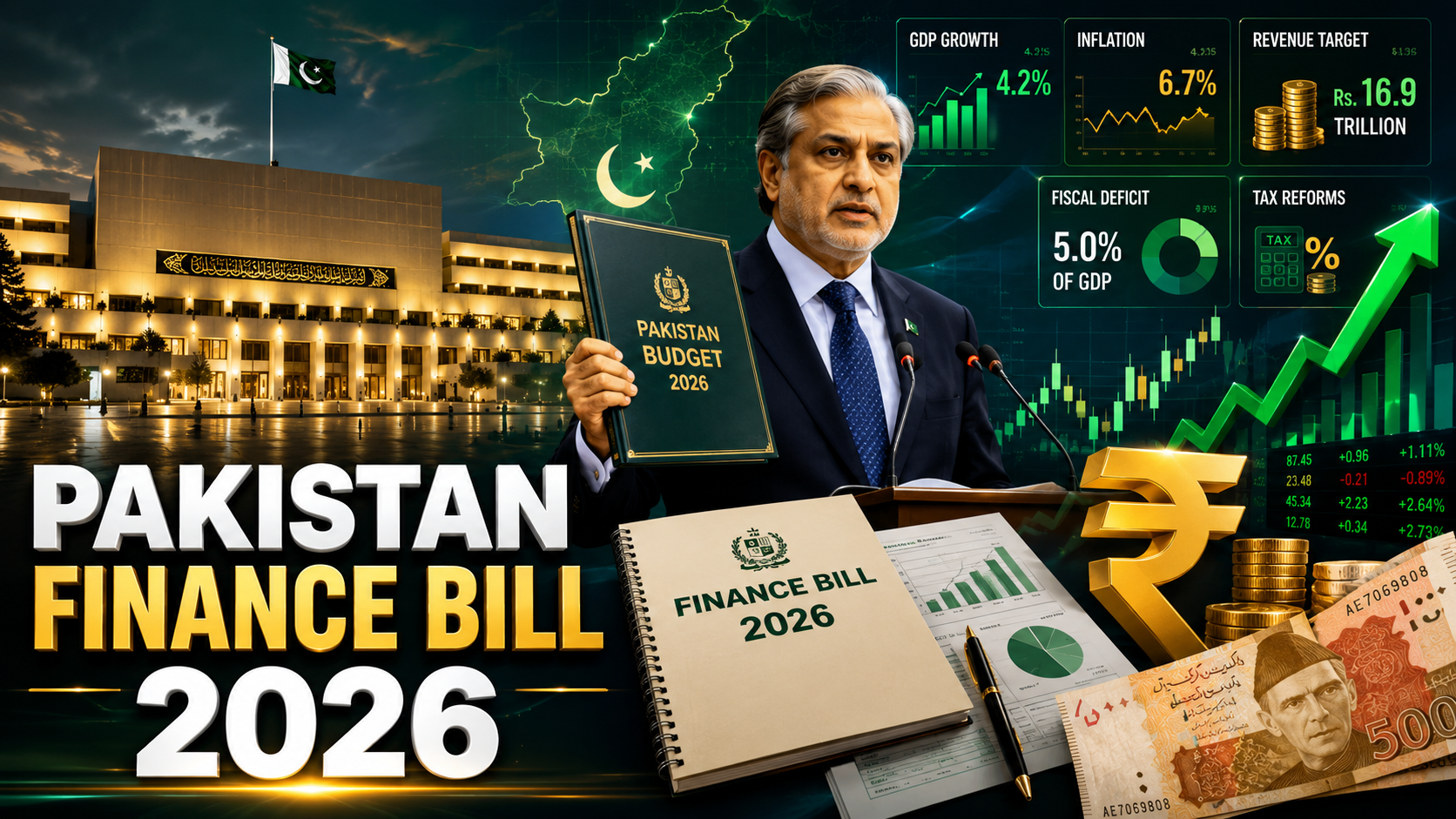

Islamabad’s revenue machine is grinding, and the gears are stripping. The Finance Bill 2026 arrived with a headline FBR target near Rs15.3 trillion for the new fiscal year — an extraction-first model layered atop one that has already missed its FY26 goal by roughly Rs868 billion. Politicians call it reform. The arithmetic says something blunter: Pakistan is squeezing the same documented taxpayers harder, year after year, while the tax-to-GDP ratio barely moves. That gap between rhetoric and result is the story.

Pakistan’s tax-to-GDP ratio has hovered between 9 and 11 percent for years — among the lowest in South Asia. The IMF’s $7 billion programme made fiscal consolidation non-negotiable, and the FBR’s own mid-year numbers tell the compliance story bluntly: during July–April of FY26, the agency collected around Rs10.25 trillion against a target of Rs10.90 trillion, a shortfall of nearly Rs683 billion, with income tax missing by roughly Rs210 billion and sales tax by Rs382 billion. By the eleven-month mark, that gap had widened further — Rs868 billion behind target, with Rs11.23 trillion collected against a revised Rs12.10 trillion goal. The Bill doesn’t fix the structure that produced this. It raises the ask.

The numbers behind Budget 2026-27 are, in a word, aggressive. The IMF-supported framework envisages an FBR target of nearly Rs15.3 trillion, alongside a petroleum levy target of Rs1.73 trillion — even as the outgoing year limped to a close roughly Rs868 billion short. Provincial governments are following the same playbook. Punjab’s finance minister told reporters his province had achieved 99 percent of its tax collection target in the outgoing fiscal year, while raising the FY27 target by 46 percent, with own-source revenue expected to climb 30 to 40 percent.

The Finance Bill’s enforcement architecture has hardened to match those ambitions. The bill expands FBR’s enforcement powers, raises the cost of ATL restoration fivefold, and puts businesses at risk of having their premises sealed for non-compliance. A new digital layer compounds it: the FBR is proposed to be empowered to operate an algorithmic settlement mechanism, with a National Faceless Centre conducting income tax, sales tax, and federal excise proceedings without direct officer contact.

The justification, officially, is efficiency. The effect, structurally, is more pressure on the same compliant base:

- Withholding-heavy collection remains the default tool, not a stopgap.

- Faceless audits centralise discretion rather than removing it.

- Provincial mimicry of the FBR model multiplies the points of contact, not the tax base.

This is extraction dressed as modernisation — and the FBR’s own mid-year shortfall numbers suggest the dressing isn’t fooling markets.

Why Pakistan’s tax-to-GDP problem resists Finance Bill fixes

Move past the headline target and the deeper issue is structural, not seasonal. Pakistan’s formal sector — salaried employees and registered corporations — is taxed at source, with zero room for deferral. The informal economy, by contrast, operates largely outside the net.

What is Pakistan’s current tax-to-GDP ratio in 2026?

Pakistan’s tax-to-GDP ratio sits near 10.3–10.6%, among the lowest in South Asia and well below the IMF’s original 11% target for FY26. The shortfall stems from narrow documentation, not insufficient rates — informal retail, real estate, and agriculture remain largely outside the formal tax net.

The Pakistan Business Council has made the structural critique explicit, warning that the current system taxes turnover as a proxy for profit, burdening even loss-making businesses, while the formal sector is treated as unpaid tax collectors through withholding obligations. The Council goes further, noting salaried employees pay significantly higher taxes than their Indian counterparts, a factor in brain drain, while Capital Value Tax on overseas assets is pushing wealthy Pakistanis to surrender nationality — undermining the very FDI inflows the budget needs.

A World Bank policy note cited in recent coverage put the inequity plainly: a narrow, compliant segment — primarily salaried workers and large corporations — carries a disproportionate share of the tax burden while large portions of the economy remain outside the net. Yet the Finance Bill’s enforcement upgrades target documentation that already exists, rather than the 40% of GDP the Business Council estimates operates undocumented. That’s the information gap competing coverage keeps missing: more enforcement technology aimed at the same compliant 60% doesn’t change the denominator.

The salaried class did receive something this cycle — a partial olive branch buried inside an otherwise extractive bill. Salaried individuals get lower rates across four brackets and lose an unpopular surcharge, with the GDP growth target set at 4% and inflation projected at 8.2%, a number attributed largely to ongoing Middle East tensions affecting energy markets. The fiscal logic behind the relief is unusually candid: a recent analysis noted the IMF itself concluded that overtaxing the most compliant sector while the informal economy remains undertaxed is counterproductive — a salaried class under unsustainable burden sees purchasing power erode, consumption contract, and revenues ultimately decline.

But that relief was financed, not gifted. The compensating measures required by the Fund include Rs430 billion expected from provincial agricultural income tax mechanisms and an expanded fixed tax scheme for the retail sector — precisely the informal-sector reforms that have proven politically hardest to enforce in past budget cycles. If they underperform, as agricultural and retail levies typically have, the FBR has only one lever left: withholding agents, who are already absorbing the bulk of FY26’s shortfall.

For SMEs and documented businesses, the second-order effect is a tightening compliance cost spiral — fivefold ATL restoration penalties, faceless algorithmic audits, and sealed-premises risk arrive at the same moment the government is asking for 46% more revenue at the provincial level. Markets reading this Bill should expect compliance costs to rise faster than actual base-broadening, at least through FY27.

Government officials frame the target as achievable discipline. The Punjab finance minister expressed confidence that the 46% increase would be met, citing the province’s near-perfect FY26 collection rate and a projected 30 to 40 percent rise in own-source revenue. Officials defending the federal numbers point to the FBR’s recent history of double-digit growth in some collection heads as proof the system can scale.

That confidence runs against the IMF’s own posture. Mid-year negotiations reportedly moved toward cutting, not raising, the FY26 target — from an original Rs14.13 trillion down toward Rs13.45 trillion, with the tax-to-GDP ratio projected at just 10.6% rather than the originally agreed 11%. The Fund’s own caution about over-relying on withholding-driven collection — the rationale behind the salaried-class relief — sits awkwardly beside provincial governments doubling down on identical withholding-heavy models. Two arms of the same fiscal programme are, in effect, pulling in opposite directions: one easing pressure on the documented base, the other expanding the apparatus that squeezes it.

The tension at the centre of Finance Bill 2026 isn’t really about rates or targets. It’s about whether Pakistan can broaden a tax base that has resisted broadening through three IMF programmes running. Faceless centres, algorithmic settlement, and fivefold penalty increases are administrative upgrades to an extraction model — not a redesign of it. The agricultural and retail levies the IMF is counting on to offset salaried relief have a thin track record. Extraction has carried Pakistan’s fiscal arithmetic this far. It’s running out of room to carry it further.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

For years, registering a commercial vessel under the national flag was an act of financial self-sabotage. Shipowners faced an immediate, punishing math problem: the moment a vessel entered the domestic registry, an 18% general sales tax was slapped onto the capital asset and its associated services. It was an upfront penalty for patriotism. Unsurprisingly, maritime capital fled. Operators sought refuge in Panama, Liberia, and the Marshall Islands, leaving domestic ports serviced almost entirely by foreign-flagged fleets.

That era of structural disadvantage has ended. The sudden 18% shipping sales tax abolition marks a definitive pivot from revenue extraction to sector expansion. It is a calculated gamble by policymakers. By walking away from immediate tax receipts, governments are betting on a massive influx of vessel registrations, job creation, and a drastic reduction in the outward flow of foreign exchange.

The immediate reaction on trading floors and in shipping boardrooms has been electric. Yet, policy shifts of this magnitude take time to filter through the physical economy.

The Macro Landscape: Taxing a Mobile Asset

To understand the weight of this policy change, one must look at how maritime commerce actually functions. Capital in the shipping industry is violently mobile. Ships are assets that can change jurisdictions with a few keystrokes and a repainted stern.

Historically, tax authorities viewed shipping as a captive cash cow. If goods needed to move, the logic went, the transport mechanism could be taxed. But the 18% levy created a profound market distortion. It did not just tax the profits of the shipping lines; it taxed the sheer act of participating in the maritime economy. According to data tracking global trade friction, high indirect taxation on logistics acts as a direct drag on export competitiveness. When a local exporter pays an inflated freight bill because the local shipping line has to cover its 18% tax burden, that exporter loses ground to rivals in Vietnam, Bangladesh, or Mexico.

This was not a theoretical loss. Economies with high maritime taxation routinely watch billions bleed out of their balance of payments. Because the domestic fleet was artificially stunted by the 18% tax, local businesses had to hire foreign shipping conglomerates to move their goods. They paid in dollars. The World Bank’s logistics performance tracking consistently shows that reliance on foreign fleets increases vulnerability to external supply chain shocks.

Now, the math reverses.

The Core Development: Scrapping the 18% Penalty

The 18% shipping sales tax abolition fundamentally rewrites the business case for domestic vessel ownership. Previously, a shipping firm purchasing a $50 million Panamax bulk carrier faced a potential $9 million tax liability simply for bringing the asset under the national flag. That capital could have purchased fuel, hired crew, or covered dry-docking maintenance. Instead, it went straight to the treasury.

By removing this barrier, the state is aligning itself with global best practices. The world’s most successful maritime hubs—Singapore, London, Athens—do not penalise vessel acquisition with crippling sales taxes. They use tonnage tax regimes, taxing the carrying capacity of the ship rather than its purchase price or gross freight receipts.

This shipping industry tax relief is already triggering a repatriation of maritime assets. Fleet operators who previously utilised flags of convenience to shield their margins are now calculating the benefits of returning home. Flying the national flag provides vessels with sovereign protection, easier access to domestic coastal trade (cabotage), and simplified regulatory oversight.

But the real victory is on the balance sheet. Freeing up 18% of working capital allows shipping firms to upgrade aging fleets. It pushes them toward greener, more efficient vessels that comply with the International Maritime Organization’s strict new emissions targets. You cannot force an industry to decarbonise while simultaneously suffocating its cash flow. The tax cut provides the necessary oxygen.

Analytical Layer: The Microeconomics of Freight

How does removing sales tax affect the shipping industry? Removing the 18% sales tax directly lowers the capital threshold for vessel acquisition and reduces operational freight costs. It incentivises shipowners to register vessels under the national flag, repatriates foreign currency spent on international shipping lines, and lowers the final cost of imported industrial goods.

This dynamic is vital for understanding the broader maritime economy growth. In shipping, costs compound. The 18% tax was never just a flat line item. It cascaded through the entire supply chain.

Consider a shipment of raw cotton intended for textile manufacturing. Under the old regime, the shipping line paid tax on its vessel. It passed that cost to the freight forwarder. The forwarder applied their margin on top of the inflated cost and passed it to the textile mill. The mill paid more for the cotton, increasing the cost of the finished garment. By the time the shirt reached a retail shelf, the ghost of that 18% tax had been marked up three separate times.

Eliminating the tax flattens this curve. It removes the frictional cost of moving goods. It is a deflationary move in an era where global supply chain inflation has been a persistent headache for central bankers.

Still, it is crucial to temper expectations. Freight rates are dictated globally by the Baltic Dry Index and container spot rates. A domestic tax cut will not insulate an economy from global shipping shortages or geopolitical blockades in the Red Sea. What it does, however, is provide local operators with a shock absorber. When global rates spike, a domestic fleet operating without the 18% tax burden can offer more competitive pricing to local industries, ensuring that vital exports do not grind to a halt due to prohibitive logistics costs.

Implications & Second-Order Effects: Rebuilding an Ecosystem

The abolition of the tax does not just benefit the men and women who own the ships. A registered vessel is a floating economic ecosystem. When a ship returns to the national registry, it brings its ancillary services with it.

First, marine insurance. For decades, the premiums paid to insure domestically owned but foreign-flagged ships flowed directly to syndicates in London or underwriters in Scandinavia. With vessels returning to the domestic flag, local insurance markets suddenly have a massive new asset class to underwrite. This deepens the local financial sector.

Second, legal and banking services. Ship financing is a highly specialised field. When fleets are registered abroad, the legal contracts, escrow accounts, and syndicated loans are managed abroad. Repatriating the fleet forces local banks to develop maritime financing desks, building institutional knowledge that generates high-value jobs. The Bank for International Settlements (BIS) has noted that deep, localised corporate financing markets are crucial for insulating emerging economies from global liquidity shocks.

Third, the blue-collar maritime economy. Ships require maintenance. They require provisioning, crew training, and dry-docking. A vibrant national registry fleet demands physical port infrastructure. Shipyards that have sat idle or underutilised for a decade are now fielding inquiries for refits and repairs. It creates a virtuous cycle: more ships lead to better port facilities, which in turn attract larger international vessels seeking transshipment hubs.

We are witnessing the architectural planning of a maritime renaissance. But it requires the government to hold its nerve. Capital intensive industries do not make 20-year vessel investments based on temporary tax holidays. The abolition must be legally enshrined and politically untouchable.

Competing Perspectives: The Treasury’s Dilemma

Not everyone views this policy shift as a masterstroke. The pushback, predictably, comes from the revenue collection authorities and international structural lenders.

The arithmetic of the Ministry of Finance is brutally short-term. They look at the ledger and see an immediate vacuum. If the shipping sector was generating $200 million annually in sales tax receipts, that money is now gone. In an environment of fiscal deficits and tight budgets, cutting a tax on wealthy shipowners appears politically perilous.

Multilateral lenders share this scepticism. Institutions like the Organisation for Economic Co-operation and Development (OECD) generally despise sector-specific tax exemptions. They argue that broad-based consumption taxes with zero exemptions are the most efficient way to run an economy. Carving out the shipping industry, they warn, invites lobbyists from the aviation, trucking, and rail sectors to demand their own 18% cuts. It risks unravelling the entire fiscal framework.

There is also the cynical, yet entirely plausible, argument regarding corporate behaviour. Will shipowners actually pass these savings down the supply chain? Economic history is littered with tax cuts that executives quietly funnelled into share buybacks and dividends rather than price reductions for consumers. If freight forwarders maintain their current pricing and simply absorb the 18% margin, the broader economic benefits—cheaper exports, lower inflation—will fail to materialise.

That said, the counter-argument is compelling. The 18% tax was yielding diminishing returns precisely because the fleet was shrinking. Taxing 18% of nothing is nothing. By pivoting to a volume-based growth model, the state will inevitably recoup its losses through corporate income tax, port duties, and the income tax paid by the thousands of new workers entering the maritime logistics sector.

The Horizon

The 18% shipping sales tax abolition is not a panacea for every logistical woe. It will not dredge shallow ports, and it will not automate outdated customs terminals. But it removes the single largest artificial barrier to maritime economy growth.

Governments have finally recognised that you cannot tax an industry into prosperity. By surrendering the 18% levy, the state has effectively invited maritime capital back to the table. The burden of proof now shifts from the policymakers to the shipowners. They have the tax environment they spent a decade lobbying for.

What follows, however, will be the true test of this policy. If the local fleet expands and freight costs genuinely compress, this abolition will be studied as a masterclass in supply-side economics. If the capital simply vanishes into corporate profit margins, it will be remembered as a costly surrender. The anchor has been lifted. Now, the industry actually has to sail.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Islamabad’s fiscal arithmetic for 2026-27 tells two stories at once. One is a government insisting the worst of the inflation crisis has passed, with growth ticking back toward 4%. The other is a security state absorbing more than Rs3 trillion in defence outlays, its largest allocation on record, against a regional backdrop still rattled by the Iran-Israel-US conflict that erupted in February. Finance Minister Muhammad Aurangzeb presented both numbers in the same breath, and that juxtaposition is the story.

A Budget Shaped by War, Reserves, and the IMF

Pakistan’s FY27 budget didn’t emerge in a vacuum. It was drafted while an IMF mission led by Iva Petrova was still in Islamabad picking through the numbers, and while the State Bank was nursing reserves that had only just climbed back toward $17 billion after years of near-default anxiety. The IMF’s Executive Board completed the third review of Pakistan’s Extended Fund Facility arrangement and the second review of its Resilience and Sustainability Facility on May 8, 2026, releasing roughly $1.1 billion and $220 million respectively, and bringing total disbursements under the two programmes to about $4.8 billion.

That context matters because it’s the IMF’s framework, more than domestic politics, that has shaped the headline targets. Pakistan’s economy grew 3.7% in FY2025-26, up from 3.2% in FY2024-25, with nominal GDP reaching Rs126.9 trillion ($452.1 billion) and per capita income rising to $1,901. The FY27 numbers are calibrated against that base, with the government betting that a fragile recovery can be nursed along without breaking the fiscal discipline Washington has demanded.

Section 1: The Numbers Behind Pakistan’s FY27 Budget

The Pakistan FY27 budget sets out a GDP growth target of 4%, up from an estimated 3.7% this year, alongside an inflation projection of 8.2%. The budget deficit is projected at 3.6% of GDP, with the government aiming for a primary surplus of 2% of GDP and a federal deficit of Rs7.02 trillion. Those are not small ambitions for a country that, less than three years ago, was weeks away from default.

The revenue side carries the heaviest lift. The Federal Board of Revenue has been handed a tax collection target of Rs15.26 trillion for FY27, an increase of more than 8% from Rs14.13 trillion in the outgoing year. That’s a number the IMF effectively wrote into the programme months ago, and it leaves little room for the kind of populist tax relief that often appears in election-adjacent budgets.

Then there’s defence. Defence spending has been raised to over Rs3 trillion for FY27, up from Rs2.56 trillion last year, with Aurangzeb telling parliament that “defence spending has been increased considerably to make the country invincible due to the uncertainty in the region.” It’s the second consecutive year of double-digit increases to the military budget — last year’s allocation itself had jumped sharply after the brief but intense conflict with India in May 2025.

Development spending, by contrast, has been held tight. The federal Public Sector Development Programme has been set at roughly Rs1 trillion, with provincial Annual Development Programmes adding a further Rs2.2 trillion, taking the national development outlay to about Rs3.7 trillion. Social protection got a modest boost: the Benazir Income Support Programme allocation rises to Rs838 billion, up 17% from last year, with coverage extended to 12 million families.

Section 2: What Does Pakistan’s Rs3 Trillion Defence Budget Actually Mean?

Pakistan’s defence budget for 2026-27 isn’t just a line item — it’s a statement about how the security establishment views the regional environment, and about where the civilian government’s bargaining power ends. At over Rs3 trillion, defence spending now equals roughly 2.1% of GDP, up from 2.03% in the FY26 revised estimate. On paper that’s a modest shift in the ratio. In rupee terms, though, it’s an 18% jump in a single year, layered on top of the 20% increase the previous government approved after the May 2025 clashes with India.

What is Pakistan’s GDP growth target for FY27? Pakistan has set a GDP growth target of 4% for fiscal year 2026-27, up from an estimated 3.7% in the outgoing year. The target rests on sectoral projections of 3.6% growth in agriculture, 4.5% in industry, and 4.2% in services — all modest accelerations from FY26 outturns.

The defence allocation didn’t arrive in isolation, either. Aurangzeb framed it alongside a diplomatic flourish: he lauded the role of Pakistan’s armed forces, calling them a source of foreign exchange earnings, and described the strategic defence agreement between Pakistan and Saudi Arabia as “a moment of pride,” adding that Pakistan would “always steadfastly stand alongside KSA.” That’s not boilerplate. It’s a budget speech doing double duty as a signal to Riyadh, to New Delhi, and to a domestic audience that has spent a year absorbing the costs of a conflict most Pakistanis didn’t choose.

What’s harder to square is how a government under an IMF primary-surplus mandate finds room for both a record defence bill and a 14% jump in core tax collection without squeezing development spending into irrelevance. The answer, so far, appears to be: it doesn’t fully square. The Rs1 trillion federal PSDP is essentially flat in real terms once 8.2% inflation is stripped out — meaning roads, dams, and digital infrastructure projects are being asked to do the same job with less purchasing power than last year.

Section 3: Markets, the IMF, and the Citizen’s Wallet

The immediate audience for this budget isn’t really the Pakistani public — it’s the IMF board, which has another review scheduled for the second half of 2026. An IMF mission led by Iva Petrova concluded a staff visit to Islamabad on May 20, 2026, focused specifically on “the FY2027 budget formulation, and progress on the reform agenda under the Extended Fund Facility (EFF) and the Resilience and Sustainability Facility (RSF),” with the next full review mission expected later this year. If Islamabad’s numbers diverge too sharply from what was discussed in those meetings, the budget could become a negotiating problem before it’s even fully implemented.

For markets, the signal is broadly reassuring — at least on paper. A fourth consecutive primary surplus, a stated commitment to fiscal consolidation, and a tax target that’s already been pre-cleared with the Fund all point toward continuity rather than rupture. The State Bank’s decision to raise its policy rate by 100 basis points to 11.5% in April, the first hike since June 2023, suggests the central bank is already pricing in the inflationary drag from higher global oil prices since the Middle East war began.

For ordinary citizens, the picture is more complicated. The budget does carve out some relief for salaried workers, with income tax rates cut across several brackets — for instance, the rate on annual salaries between Rs3.2 million and Rs4.1 million falls to 25% from 30%, and the bracket from Rs4.1 million to Rs5.6 million drops to 29% from 35%. But with inflation forecast at 8.2% — itself a figure many independent economists consider optimistic — those gains could be eaten up quickly if energy and food prices track anywhere near the trajectory seen since the conflict began.

Energy remains the wildcard that could unravel the whole framework. Circular debt in the power sector alone sits close to Rs1.84 trillion even after a major bank refinancing facility, and the combined energy sector shortfall — including gas — has reportedly climbed past Rs5 trillion. Any subsidy reintroduced to cushion consumers from cost-reflective tariffs would directly threaten the 2% primary surplus target the entire IMF arrangement is built around.

Section 4: Not Everyone Buys the Optimism

The government’s framing — 4% growth, 8.2% inflation, a primary surplus locked in for a fourth straight year — assumes the Middle East conflict’s economic fallout stays contained. Not every economist agrees that’s the safer bet.

Dr Hafiz Pasha’s recent analysis places FY27 growth at just 2.5% against the government’s 4% and the IMF’s earlier 3.5% baseline, inflation at 12% against the official 8.2%, and the current account deficit at $10 billion rather than the roughly $4 billion implied by Fund projections — with reserves declining rather than continuing to build. The gap between these scenarios isn’t academic. If Pasha’s stress case is closer to reality, the tax revenue assumptions underpinning the entire budget — that 14% jump in FBR collections — become much harder to deliver, and the primary surplus the IMF is counting on could evaporate.

Even the IMF’s own staff report, published in mid-May, hedged its bets. The Fund’s third review noted that GDP growth had accelerated in the first half of FY26 and the current account was broadly balanced, but acknowledged that “the impact of the war in the Middle East clouds Pakistan’s near-term outlook and there is great uncertainty about how developments will unfold.” That report was written before the worst of the oil-price shock had fully filtered through to Pakistan’s import bill — and the gap between that baseline and the budget presented weeks later suggests the government chose to project confidence rather than caution. Whether that confidence survives contact with a second IMF review later this year is an open question that won’t be settled by a budget speech, however carefully worded.

The Bigger Picture

What Pakistan’s FY27 budget really reveals is a government trying to hold two contradictory commitments at once: a security posture that demands ever-larger defence outlays in a volatile region, and an IMF programme that demands fiscal restraint as the price of continued solvency. For now, both demands have been met — on paper, through a combination of aggressive tax targets, modest development spending, and a growth forecast that several independent economists consider generous. The real test arrives not in parliament, where the budget will pass with the government’s majority, but in the months ahead, when oil prices, energy subsidies, and the next IMF mission will decide whether 4% growth and 8.2% inflation were a forecast — or a wish.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

US Section 301 Tariffs 2026: 60 Countries Face 12.5% Duties on Forced Labour Goods

China Economy 2026: 87% Semiconductor Surge, Property Crisis

Kevin Warsh Fed 2026: Rate Hold, Hawkish Dot Plot, and the End of Forward Guidance

SpaceX IPO 2026: $2 Trillion Valuation, Retail Frenzy, and the Risks

Oracle AI Debt Crisis 2026: $130 Billion Gamble Triggers Worst Stock Crash Since Dot-Com Bust

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Trump Tariffs 2026: Economic Impact, Household Costs & Trade War Outlook

China Economy 2026: Export Boom Masks Property Crisis & Investment Slump

US Inflation 4% May 2026: Is the Worst Over? Fed, Oil Prices

AI Memory Chip Shortage 2026: Nvidia, Apple & What Comes Next

US $39 Trillion National Debt 2026: Bond Market Warning Signs Explained

Ray Dalio US Suez Moment 2026: Dollar Decline, $39 Trillion Debt & Empire’s End

Kevin Warsh Fed Rate Hike 2026: What His Hawkish Pivot Means for Markets

Gold Price 2026: Will Gold Hit $6,000? JPMorgan Forecast, Drivers & Investment Guide

PwC China Partner Payouts Cut Amid Evergrande Audit Fraud

Broadcom Market Value Loss: Revenue Forecast Disappoints

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Here’s How Much It’ll Cost You to Be Part of SpaceX’s Record-Breaking $75 Billion IPO

Nasdaq Tumbles 4% as Chip and Memory Stocks Sink: A $1.2 Trillion Wipeout

Smash Capital Leads $200M Funding for Allen Control Systems

How to Fix Pakistan’s Debt Economy: A Structural Blueprint

Democrats Draw a Red Line Around Military AI — And the Pentagon Is Already Pushing Back

New Investment Super-Cycle: AI, Green Energy & Re-Shoring

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

Middle East Conflict Oil Prices: The $4 Surge Explained

Grinding the Already Ground: Pakistan’s Inflation Crisis

The End of the Chatbot: Why OpenAI is Tearing Up Its Most Successful Product

Musk’s SpaceX Lines Up Retail Investors for Record IPO Allocation

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 months ago

Analysis4 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks5 months ago

Banks5 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025