Analysis

Pakistan’s 7.3% Inflation Surprise in March 2026: Relief or Red Flag for 2026 Growth?

Economic Analysis · Pakistan

The headline number beat expectations—but with core prices still sticky, oil markets roiling, and an IMF programme watching closely, Pakistan’s policymakers have little room to celebrate.

In a modest flat in Karachi’s Gulshan-e-Iqbal, Fatima Naqvi spent the first morning after Eid ul-Fitr tallying her household ledger. The good news: her grocery bill was noticeably lighter than last year’s—tomatoes back to something approximating reason, chicken no longer a luxury purchase. The unsettling news: the gas cylinder had doubled in cost, the electricity bill arrived with a new surcharge, and her husband’s April salary raise had been swallowed whole by non-food expenses before the month even began. Pakistan’s inflation for March 2026, confirmed by the Pakistan Bureau of Statistics at 7.3% year-on-year, captures both of those realities simultaneously.

The 7.3% CPI Pakistan 2026 reading was, on paper, a genuine positive surprise. The Ministry of Finance had bracketed its forecast at 7.5–8.5%. Brokerage houses Arif Habib Limited and JS Global had pencilled in a range of 7.3–7.6%. Almost every analyst on Karachi’s I.I. Chundrigar Road had warned that March would bring the most punishing base-effect spike of the year, given that Pakistan’s March 2025 CPI had crashed to a six-decade low of 0.7%—a statistical anomaly that made any year-on-year comparison brutally difficult. That the final print landed at the floor of expectations rather than the ceiling is, genuinely, the least bad outcome policymakers could have hoped for.

Yet the Pakistan headline inflation March 2026 figure also carries a caveat as wide as the Indus in monsoon season. Strip away the flattering food components, stare directly at core prices, fuel sub-indices, and the fine print of the IMF’s freshly inked third review, and the story becomes considerably more complicated. This is a moment for sober analysis, not a victory lap.

7.3% — Pakistan CPI, March 2026 (YoY) Below MoF forecast of 7.5–8.5% · Above February’s 7.0% · Versus 0.7% in March 2025 Source: Pakistan Bureau of Statistics (PBS), April 2026

The Numbers Behind the Surprise

To understand why 7.3% qualifies as a surprise, you need to appreciate the arithmetic of base effects. Pakistan’s inflation trajectory over the past 14 months has been defined by comparisons against extraordinarily benign prior-year benchmarks. In February 2026, CPI hit 7.0% year-on-year, up sharply from 5.8% in January—because February 2025’s base was itself only 1.5%. March 2025’s base of 0.7% is even lower, meaning the mechanical arithmetic alone suggested a print north of 8%. The fact that March 2026 avoided that territory reflects genuine underlying price moderation in at least some categories.

| Category / Indicator | March 2026 (YoY) | February 2026 (YoY) | Direction |

|---|---|---|---|

| Headline CPI (National) | 7.3% | 7.0% | ↑ +0.3pp |

| Urban CPI | ~7.1%* | 6.8% | ↑ |

| Rural CPI | ~7.6%* | 7.3% | ↑ |

| Core Inflation (Non-food, Non-energy) | ~7.2–7.4%* | ~7.2% | → Sticky |

| Food & Non-Alcoholic Beverages | ~5.5%* | ~3.9% | ↑ (base-driven) |

| Housing, Water, Utilities, Gas | ~8.5%* | 7.3% | ↑ Elevated |

| LPG (SPI YoY, late March) | +34.7% | — | ↑↑ Severe |

| Petrol (SPI YoY, late March) | +25.8% | — | ↑↑ Severe |

| Diesel (SPI YoY, late March) | +29.9% | — | ↑↑ Severe |

| Wheat Flour (SPI YoY, late March) | +25.8% | — | ↑↑ Persistent |

| Potatoes (SPI YoY, late March) | -45.7% | — | ↓↓ Deflationary |

| Eggs (SPI YoY, late March) | -13.6% | — | ↓ Deflationary |

*Estimated based on February 2026 PBS data and SPI trajectory. Full PBS March CPI release pending. Sources: PBS, Trading Economics.

The disaggregated picture is clarifying. The national headline number was rescued by dramatic declines in perishable vegetables—potatoes down nearly 46%, eggs off 14%, garlic falling 13%. This reflects good crop supply and normal seasonal correction post-winter. But these are precisely the categories that reverse fastest. Meanwhile, the structural pain points—fuel, gas, utilities, processed food—are not only elevated but trending upward. Rural households, who spend a larger share of income on food staples like wheat flour (up 26%), experienced considerably more pressure than the 7.3% aggregate implies. Rural CPI in February was already running at 7.3% against urban’s 6.8%; March likely widened that gap.

“A 7.3% headline masks a tale of two Pakistans: urban middle-class shoppers who benefited from cheap vegetables, and rural households still crushed by wheat flour and fuel costs running at 25–35% above last year.”

Why Lower Than Expected? (And Why It Still Matters)

Three forces pushed the March print below consensus. First, the Eid ul-Fitr effect on food supply—remittance inflows ahead of the holiday, combined with improved cross-border trade flows and a reasonable winter crop, helped dampen the post-Ramadan food spike that markets had feared. Second, the global oil correction: Brent crude pulled back from its March peak following brief US-Iran diplomatic signals, providing transitory relief on pump prices at precisely the measurement moment. Third, and most importantly for the analytical record, the statistical contribution of volatile perishables in the PBS CPI basket—weighted at roughly 35% for food and non-alcoholic beverages—proved more disinflationary than models projected.

None of these forces is durable. Remittance-driven food demand is seasonal. Oil diplomacy in the Middle East is fragile—at the time of writing, the region remains in active conflict with ongoing supply disruptions. And the crop year’s perishable surplus will normalise by Q2. This is why the Pakistan CPI vs Finance Ministry estimate March 2026 miss, while welcome, should not be read as a trend break.

📊 Context: The Base Effect Explained

Pakistan’s March 2025 CPI of 0.7% was the lowest reading in six decades, the result of aggressive SBP rate hikes (peak: 23% in May 2024), rupee stabilisation, and a global commodity correction. Any March 2026 reading was statistically guaranteed to look high against that base. A 7.3% print therefore still represents genuine easing relative to a purely mechanical-base scenario—but the absolute level of prices Fatima Naqvi faces in her kitchen has not fallen. The index has just risen more slowly than feared.

Comparatively, Pakistan’s trajectory holds up reasonably against its peer group. India’s CPI has been hovering around 4–5%, benefiting from more diversified energy supply and larger agricultural buffers. Bangladesh has faced its own food inflation pressures above 9%. Among IMF programme countries in emerging Asia, Pakistan’s 7.3% sits in the middle of the distribution—not alarming, not reassuring.

Global and Domestic Headwinds Looming

The timing of the March CPI release could not be more loaded with context. Just days earlier, on March 27, 2026, the IMF completed its third review of Pakistan’s 37-month Extended Fund Facility—reaching a staff-level agreement that unlocks approximately $1.2 billion in disbursements ($1.0 billion under the EFF and $210 million under the Resilience and Sustainability Facility). The IMF’s statement was diplomatically careful but strategically explicit: the Middle East conflict “casts a cloud over the outlook” as volatile energy prices and tighter global financial conditions risk pushing inflation higher and weighing on growth.

The Fund went further. The SBP was explicitly reminded to stand ready to raise interest rates “should price pressures intensify.” That is not boilerplate language; it is a conditional threat embedded in a bilateral agreement. Pakistan’s policymakers understand that the 7.3% March print—while below forecast—does not represent the all-clear.

⚠️ Risk Radar: What Could Push Inflation Back Above 9%

The SBP’s own March 2026 policy statement cited analysts warning of inflation reaching approximately 9.25% by Q2 FY2026. The key transmission mechanisms: (1) oil price pass-through via petrol and diesel—already at +26% and +30% YoY respectively on weekly SPI data; (2) electricity and gas tariff adjustments required under IMF energy sector viability conditions; (3) currency depreciation pressure if Middle East tensions tighten global dollar liquidity; (4) wheat flour stubbornly at +26% YoY, an anchor commodity in the rural poor’s consumption basket.

Pakistan’s energy situation deserves particular attention. The SBP held its benchmark policy rate at 10.5% in March, extending the pause in its easing cycle—but the reasons cited were almost entirely external. Oil prices had surged amid Middle East escalation. Pakistan, as a heavy importer of refined fuels, transmits global energy shocks directly into its CPI with a lag of four to eight weeks. The LPG price spike visible in the SPI data—up 35% year-on-year by the final week of March—is a leading indicator, not a coincidence. Energy sector circular debt remains the structural ulcer that no monetary policy can treat.

Remittances, by contrast, remain a genuine bright spot. The SBP’s January 2026 monetary policy statement noted that worker remittances continue to run strongly, and the IMF’s third review acknowledged their role in containing current account pressures. Eid-season inflows in late March 2026 provided a real demand buffer. With SBP foreign exchange reserves expected to surpass $18 billion by June 2026, the external account is in its healthiest position in years. But reserves and food-price relief are not the same thing for the 60% of Pakistanis who live on incomes below the median.

What This Means for Pakistanis and Policymakers

The gap between the headline statistic and the lived experience of ordinary Pakistanis is the central policy communication failure of this moment. Core inflation—which strips out volatile food and energy—has been running at approximately 7.2–7.4% since late 2025, unchanged despite the headline number oscillating. Core inflation is the signal; it tells you what employers are implicitly pricing into wage offers, what landlords are building into rent reviews, and what service-sector firms are assuming about input costs. At 7.2–7.4%, core inflation remains above the SBP’s 5–7% target band’s midpoint. Real wages for formal-sector workers—assuming nominal raises of 10–12%—are barely keeping pace. For the informal sector, which accounts for the majority of Pakistan’s labour force, real purchasing power has not recovered to 2022 levels.

For the State Bank, the SBP policy rate after March 2026 inflation is an easier decision than it was three months ago, but not a comfortable one. The 10.5% rate was held in March; a cut before June looks nearly impossible given the IMF’s explicit hawkish guidance. The earliest credible window for easing is late FY2026—June or July—and only if energy prices stabilise and the Q2 CPI print does not validate the 9.25% projection. The SBP’s own December 2025 rate cut, which surprised markets, now looks like a calculated bet that the base-effect spike would be temporary. The March 2026 data gives that bet a modest early validation—but not yet vindication.

For fiscal policy, the picture is sharper still. The IMF requires Pakistan to achieve a primary budget surplus of 1.6% of GDP in FY2026, progressing toward 2% in FY2027. The Federal Board of Revenue’s tax collection growth has slowed to approximately 9.5%, well below last year’s 26% pace, creating a Rs 329 billion shortfall. Lower-than-expected inflation mathematically reduces nominal tax revenues. That fiscal tightness, combined with energy sector tariff obligations, means the government has very little room for consumer-protecting interventions—even as middle-class purchasing power remains under real strain.

| Indicator | Value | Status |

|---|---|---|

| Headline CPI, March 2026 | 7.3% YoY | ✓ Below MoF forecast |

| Core Inflation (Jan 2026, latest) | ~7.2–7.4% | ⚠ Above SBP target midpoint |

| SBP Policy Rate | 10.5% | → On hold (Mar 2026) |

| SBP Inflation Target Range | 5–7% | ⚠ Breached on upper end |

| FX Reserves (SBP) | $15.8B+ | ✓ Rising; target $18B by Jun |

| IMF EFF Status | 3rd review SLA signed | ✓ $1.2B unlocked (Mar 27) |

| GDP Growth Target, FY2026 | 4.2% | ⚠ At risk; SBP sees 3.75–4.75% |

| LSM Growth, Q1 FY2026 | +4.1% YoY | ✓ Broad-based recovery |

| FBR Tax Revenue Growth | +9.5% YoY | ⚠ Rs 329B shortfall |

Sources: PBS, SBP Monetary Policy Statements, IMF Third Review Staff-Level Agreement (March 27, 2026), Trading Economics.

Lessons for 2026 and Beyond: The Reform Imperative

Here is the honest, uncomfortable truth that Pakistan’s inflation data keeps telling us, month after month: the stabilisation is real, but it is shallow. Pakistan has achieved headline inflation below double digits by combining IMF-conditioned fiscal discipline, SBP rate hikes that briefly hit 23%, and the extraordinary statistical luck of an ultra-low comparison base. None of that is structural disinflation. None of it addresses why wheat flour costs 26% more than a year ago, why LPG has become a luxury item in rural Sindh, or why electricity tariffs must keep rising to service a circular debt that has been accumulating for three decades.

The countries that have genuinely conquered inflation—India in the 2010s, Indonesia post-2015, even Bangladesh through much of the 2010s—did so by investing heavily in agricultural supply chains, diversifying energy sources away from imported fossil fuels, and broadening the tax base so that fiscal deficits did not repeatedly force monetary tightening. Pakistan has undertaken partial versions of all three under the current EFF, but partial is the operative word. The IMF’s third review noted progress on energy sector reforms while flagging that circular debt prevention requires “timely tariff adjustments that ensure cost recovery”—a polite formulation for: tariffs will keep rising, and the poor will bear a disproportionate share of that burden unless social protection scales accordingly.

The Benazir Income Support Programme has been expanded, with inflation-adjusted transfers and broader coverage explicitly acknowledged in the IMF staff-level agreement. That is meaningful. But BISP reaches approximately 9 million households; Pakistan’s population is 245 million. The middle class—the salaried professionals, the small traders, the schoolteachers—falls precisely in the gap between BISP eligibility and meaningful real wage recovery. They are the group for whom 7.3% inflation is not relief; it is just a slower form of erosion.

This is where opinion must be plainly stated: Pakistan cannot afford to treat a below-forecast CPI print as an excuse to delay structural reform. The window that the current IMF programme, rising reserves, and recovering industrial output has opened is narrow. Energy sector privatisation, agricultural investment, tax base broadening, and exchange rate flexibility as a genuine shock absorber rather than a managed decline—these are not optional supplements to the stabilisation programme. They are the programme, in its meaningful form.

The bottom line on Pakistan inflation March 2026: 7.3% is genuinely lower than feared, and analysts, policymakers, and ordinary households alike are entitled to take a moment’s breath. Pakistan has come a long way from the 30.8% inflation peak of 2023. But core prices are sticky, fuel costs are brutal, rural households remain under severe pressure, and the IMF’s own assessment warns that Middle East volatility could still push Q2 CPI toward 9%. The SBP will hold rates. The government must hold its fiscal nerve. And Pakistan’s political economy must find the courage to push through energy and agricultural reforms while the external account is, for now, in reasonable shape.

Fatima Naqvi’s ledger tells you what the index cannot: stability is not the same as relief, and relief is not the same as prosperity. The next six months will determine which of those three words defines Pakistan’s 2026.

Frequently Asked Questions

Was Pakistan’s inflation lower than expected in March 2026? Yes. Pakistan’s headline CPI inflation for March 2026 registered at 7.3% year-on-year, below the Ministry of Finance’s forecast range of 7.5–8.5% and at the lower end of brokerage estimates of 7.3–7.6%. The positive surprise was driven largely by steep declines in perishable vegetable prices (potatoes -46%, eggs -14%) that offset persistent fuel and utility inflation.

What is the impact of 7.3% inflation on Pakistan’s economy in 2026? The reading provides the SBP justification to keep the policy rate on hold at 10.5% rather than hiking, supporting the IMF EFF programme narrative. However, core inflation remains sticky at 7.2–7.4%, real wage growth for informal workers is barely positive, and Pakistan’s 4.2% GDP growth target for FY2026 is under pressure from Middle East-related supply chain disruptions and a Rs 329 billion tax revenue shortfall.

How does Pakistan’s CPI compare to the Finance Ministry estimate for March 2026? The Ministry of Finance had forecast March 2026 inflation at 7.5–8.5%, anticipating a base-effect spike from March 2025’s historically low 0.7% CPI. The actual 7.3% print came in below the floor of that range—a roughly 20–30 basis point positive surprise—reflecting better-than-expected food supply conditions and a temporary Brent crude correction.

Will the SBP cut rates after the March 2026 inflation data? A near-term rate cut is unlikely. The SBP held at 10.5% in March 2026, citing Middle East oil risks. While the CPI surprise reduces hike pressure, the IMF’s explicit call for “appropriately tight” monetary policy and sticky core inflation mean the earliest realistic window for easing is late FY2026 (June–July) or into FY2027, and only if Q2 CPI avoids the feared 9%+ range.

What are the main risks to Pakistan’s inflation outlook for the rest of 2026? The primary risks are: (1) Middle East-driven oil price volatility transmitting through LPG (+35% YoY), petrol (+26%), and diesel (+30%); (2) mandatory electricity and gas tariff increases under the IMF’s energy sector viability conditions; (3) rupee depreciation pressure amid global financial tightening; and (4) any monsoon-related agricultural disruption in H2 2026 that reverses the current perishable price relief.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

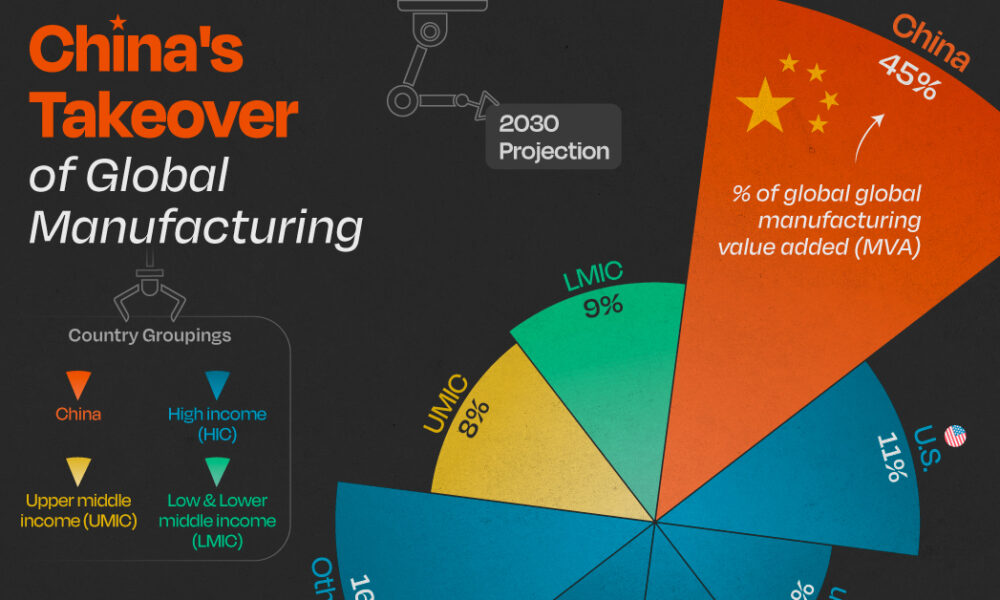

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025