Budget

Budget FY2026-27: Traders assured of simplified tax scheme

Traders in Islamabad did something rare on Friday. They said yes.

On May 23, Kashif Chaudhry and a dozen bazaar leaders stood at the National Press Club and backed the government’s draft for the Pakistan FY2026-27 simplified tax scheme — a one-page Urdu return, a flat Rs25,000 yearly floor, and a written promise to keep auditors away. After three decades of shutter-down strikes, failed fixed-tax regimes and midnight raids, the handshake matters. It lands less than two weeks before the federal budget, due in the first week of June, with IMF monitors in town and the treasury hunting for Rs15 trillion-plus.

Pakistan doesn’t collect enough, and it collects it the hard way. The Federal Board of Revenue briefed Prime Minister Shehbaz Sharif last summer that the tax-to-GDP ratio had inched up to 10.6% in FY2025, a 1.5-point gain in a year but still far from the 13% promised to the Fund Pakistan’s tax-to-GDP ratio reaches 10.6%. The IMF’s December review locked in a tougher path: broaden the base, simplify rates, and deliver a primary surplus of 2.5% of GDP in FY2026, up from 1.3% last year IMF Executive Board Completes Second Review.

Retail tells the story. The sector makes up nearly a fifth of the economy but pays less than one rupee in a hundred of direct tax. Past drives — POS machines in 2020, the tier-1 retailer rules, two amnesties — died in protests. With reserves rebuilt to $14.5 billion and inflation back to single digits, the finance team is trying a different bargain: less paperwork for more payers.

What the Pakistan FY2026-27 simplified tax scheme actually offers

The outline isn’t buried in fine print. It’s on a shop wall.

Any retailer, wholesaler or small service provider with turnover up to Rs200 million can opt in. They file one sheet in Urdu, not twelve in English. They pay Rs25,000 a year, no matter what, plus 0.25% to 0.5% of whatever turnover they declare. Taxes already clipped from electricity and phone bills count toward that bill Traders back govt’s simplified tax scheme.

Once in, they get a metal tax plate from the FBR. Hang it, and the rules change.

No audit. No demand for a POS terminal. No questions about the flat you bought in Bahria Town or the Corolla in your cousin’s name — unless investigators already hold hard evidence. That’s the pitch.

Chaudhry, 52, who heads the Central Organisation of Traders, spelled it out on May 23. He wants the same deal for real estate brokers, small factories and farm suppliers, and he wants both first-time filers and old filers to qualify — with one caveat from the government: you can’t pay less than you paid last year Traders want simplified tax system.

The wish list runs longer. Scrap the 5.1% minimum turnover tax. Drop the duty to act as a withholding agent. Redefine tier-1 so only big brands in air-conditioned malls face mandatory POS. Cut property withholding under sections 236C and 236K to 1%, kill section 7E, and chop FBR valuations by 40%. None of that is law yet.

Minister of State for Finance Bilal Azhar Kayani didn’t read the list aloud. At a pre-budget huddle in Rawalpindi on May 24, he said the budget will carry “special measures” for SMEs, stretch the import-input window to 18 months, and enforce “zero tolerance for harassment” Budget relief limited by IMF commitments. Traders say the Rs25,000 figure and the audit shield were agreed after six weeks of back-and-forth in Lahore and Islamabad.

Can a plate on a shop wall buy trust? That’s the bet.

Why traders tax Pakistan 2026 is being rewritten now

Three clocks are ticking at once.

First, the IMF. Pakistan signed up, in writing, to publish a tax simplification strategy by May 2026. The deal commits the finance ministry to cut rate slabs, limit advance and withholding taxes, and move all tax-policy approvals to a new Tax Policy Office Pakistan commits to tax simplification strategy. The Fund’s language is blunt: raise money by taxing more people, not by squeezing the same salaried workers.

Second, the World Bank. In June 2025 it topped up its Pakistan Raises Revenue project with another $70 million, taking the pot to $470 million. The project has already pulled 1.5 million new people into the tax net, built a single portal for sales tax, and trimmed the thicket of withholding lines World Bank Expands Support. Its 2035 goal — 15% of GDP in taxes — is impossible without the bazaar.

Third, exhaustion. After floods, a currency crunch and a $3 billion IMF lifeline, the government can’t afford another nationwide strike. A simple, visible levy is politically cheaper than sending teams into Anarkali with clipboards.

What is the new simplified tax scheme for traders in Pakistan budget 2026-27? The scheme lets retailers with turnover up to Rs200 million file a one-page Urdu return, pay a flat Rs25,000 annual minimum plus 0.25–0.5% of turnover, adjust utility withholding taxes, and avoid FBR audits and POS machines. Participants display a tax plate and face no property or vehicle inquiries without evidence.

That’s 50 words, and it’s the part traders repeat. Yet the arithmetic nags. If a million shops pay just the floor, that’s Rs25 billion — about 0.16% of the Rs15.6 trillion collection target the IMF floated in March talks IMF proposes Rs15.6 trillion tax target. Even with the turnover slice, the scheme won’t close the gap. It might, however, stop the bleeding of trust.

From bazaars to the budget: who wins, who pays

For a cloth merchant in Faisalabad paying Rs6,500 a month in electricity withholding, the math is easy. He files the Urdu sheet, ticks Rs80 million turnover, owes Rs400,000 at 0.5%, subtracts Rs78,000 already deducted on bills, adds the Rs25,000 floor, and walks away. No auditor asks why his sales jumped after Eid. No POS vendor camps in his shop.

For the FBR, the win isn’t cash on day one. It’s names. Filers climbed from 4.5 million in FY2024 to more than 7.2 million by June 2025, with retail POS integration adding Rs45.5 billion alone Pakistan’s tax-to-GDP ratio reaches 10.6%. A fixed trader regime could push the count past eight million, ticking the IMF’s “base broadening” box without a new law.

For the budget, the trade-offs bite. Kayani admitted the fiscal room is thin. “Limited fiscal space under the IMF programme restricts major relief,” he told the RCCI on May 24 Budget relief limited by IMF commitments. The Fund has already balked at exempting fuel from sales tax and wants an 18% levy on existing solar net-billing users to protect revenues IMF proposes Rs15.6 trillion tax target.

That means someone else pays. Salaried workers, who saw their slabs rise to 35%, are lobbying for relief and will likely get only a tweak. Provinces, which must deliver a combined Rs400 billion surplus next year to hit the 2% primary surplus target, could lose if Islamabad caps trader payments while property valuations are cut 40%. Sindh alone is being asked for Rs200 billion — most of it from Karachi’s markets.

And there’s the digitisation paradox. The World Bank project cut customs clearance from 52 hours to 12 and built data tools to spot evasion World Bank Expands Support. Exempting a whole class from POS and invoices blunts those tools. The picture is more complicated than “formalise at any cost.”

The IMF and critics aren’t buying the bargain

The Fund’s staff aren’t hostile to simplicity. They’re hostile to holes.

In March, they proposed an asset-based levy on traders, not just turnover, because turnover is easy to hide. The FBR pushed back, citing weak valuation capacity — the very gap the $470 million World Bank loan is meant to close IMF proposes Rs15.6 trillion tax target.

Pakistani economists echo the worry. The 2019 trader scheme signed up 50,000 shops and died within months. The 2022 fixed tax never collected a rupee after courts stayed it. A flat Rs25,000, they argue, rewards the biggest evaders and punishes the honest mid-size shop that already pays more.

ICMAP, the cost accountants’ body, offered a different menu for FY2026-27: tax second homes at 2%, widen digital services taxes, and fund agriculture through a stability fund. Their point is simple — Pakistan’s revenue potential sits near 26% of GDP, but we collect less than half because we chase turnover, not wealth.

Traders have an answer, too. Ajmal Baloch, who leads the All Pakistan Anjuman-i-Tajiran, called the talks “serious negotiations” after a month and a half, and said the scheme would free small shops from “corruption and blackmail.” He isn’t wrong about the history. Harassment has killed more schemes than bad rates.

Still, the IMF’s December review is clear: any tax cut must be matched by a permanent gain elsewhere, and “tax policy simplification and base broadening is key to achieving fiscal sustainability” IMF Executive Board Completes Second Review. An audit holiday doesn’t look like base broadening to the board.

CLOSING

This budget isn’t about a new rate. It’s about a new contract.

Islamabad is offering the bazaar something it hasn’t had in years: predictability. Pay Rs25,000, file in Urdu, hang the plate, and the state steps back. The bazaar, in turn, offers the state something it desperately needs: a name, an address, a number in the system.

Will it raise enough? Probably not on its own. A million traders at the floor plus half a percent on Rs50 trillion of declared turnover might yield Rs275 billion — helpful, but still short of the Rs400 billion in fresh measures the IMF expects provinces and centre to find together.

What it might do is break a stalemate. Pakistan has tried force, and force failed. Now it’s trying ease. If the plate stays on the wall past the first audit season, if the Urdu form actually works on a phone, if Kayani’s “zero harassment” line holds, the tax-to-GDP ratio could keep climbing past 10.6% without another street shutdown.

If not, we’ll be back here next May, with a new minister, a new scheme, and the same old question: who pays for Pakistan?

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Russia’s federal budget collected less revenue in 2025 than originally planned for the first time since the pandemic, a shortfall that has pushed the Kremlin to raise its value-added tax rate from 20% to 22% starting January 1 and pull far more small businesses into the VAT system, according to The Moscow Times’ assessment of the country’s 2026 fiscal trajectory.

The Oil Money Is Drying Up

The core of Russia’s budget problem is straightforward: oil and gas revenue, the traditional backbone of Kremlin finances, has fallen by more than 25% as a stronger ruble and tightening Western sanctions squeeze what Moscow can earn from crude exports, according to the New Eurasian Strategies Centre’s analysis. When the 2025 budget was set, revenues were projected at 40.3 trillion rubles; updated forecasts now suggest actual collections closer to 36.6 trillion rubles, a gap of roughly $46 billion at current exchange rates, per The Moscow Times.

The World Bank expects a global oil supply surplus to push Brent crude prices down from an average of $68 a barrel in 2025 to around $60 in 2026, the lowest level in five years, further squeezing the discount Russia must already offer buyers willing to purchase sanctioned crude. With GDP estimated at 217.3 trillion rubles in 2025, total defense spending of around 15.86 trillion rubles, more than $198 billion, now represents a share of the economy that leaves little room for the civilian investment that might otherwise support long-term growth, The Moscow Times reports.

A Central Bank Fighting Inflation on Its Own

Against this fiscal backdrop, the Bank of Russia has pursued an unusually consistent disinflation campaign under Governor Elvira Nabiullina, cutting its key rate eight consecutive times from a record 21% last June down to 14.25% by its June 2026 decision, according to the central bank’s own rate announcement. That June cut of just 25 basis points came in below the market’s median expectation of a 50-basis-point reduction, with the central bank citing persistent pro-inflationary risks tied to higher energy prices from the Middle East war, refinery damage from Ukrainian strikes, and wage growth that continues to outpace productivity, per Trading Economics’ tracking of the decisions.

Annual inflation stood at 5.6% as of mid-June, still well above the Bank of Russia’s 4% target, though down meaningfully from the 9.5% rate recorded in 2025, according to the central bank’s own data. The Moscow Times’ longer analysis of the anti-inflation campaign notes that Russia’s consumer price index rose 39% across the four full wartime years from 2022 to 2025, compared with 61% in Ukraine over the same period, and a staggering 200%-plus in Iran, framing Nabiullina’s inflation-targeting approach as unusually disciplined by wartime standards, per The Moscow Times’ longer profile of the policy.

The Cost of That Discipline

That discipline has not come free. The New Eurasian Strategies Centre describes Russia as moving through the final phase of a familiar economic cycle: downturn, fiscal stimulus, inflation, interest rate rises, downturn again, disinflation, rate cuts, and eventually recovery, a sequence the think tank says has suppressed economic activity across many sectors as interest-rate pressure compounds the drag from sanctions and wartime resource reallocation, according to its analysis of key rate dynamics. Growth forecasts for both 2025 and 2026 now cluster around just 1%, according to Russia’s own Economic Forecasting Institute and the IMF alike, a marked slowdown from the wartime stimulus-driven expansion of earlier years.

A potential end to the war in Ukraine, paradoxically, could increase short-term recession risk by reducing output in defense-related industries and lowering household incomes tied to military production, the New Eurasian Strategies Centre’s analysis notes, underscoring how deeply the war economy has become embedded in Russia’s growth model.

New Taxes on Everything From Laptops to Small Firms

Beyond the VAT increase, Russian authorities are lowering the annual revenue threshold for mandatory VAT registration from 60 million rubles to just 10 million rubles, sweeping far more small and medium-sized enterprises into the tax system, according to The Moscow Times’ January analysis. The government also plans a new levy on finished electronic goods including laptops, smartphones, and lighting products. The head of Russia’s New People party has publicly warned that lowering the VAT threshold will disproportionately hit small and medium-sized enterprises in the regions, according to reporting cited in the same Moscow Times analysis, a rare instance of intra-establishment pushback on fiscal policy.

What to Watch Next

The Bank of Russia’s next key rate decision falls on July 24, with a summary of the prior meeting’s discussion published July 1, according to the central bank’s own communications calendar. Nabiullina has reaffirmed that inflation should return to the 4% target sometime in 2026, a view broadly shared by Prime Minister Mikhail Mishustin and Finance Minister Anton Siluanov, though The Moscow Times notes that even Defense Minister Andrei Belousov has, with some reservations, supported the anti-inflation policy, a rare point of consensus across an otherwise divided Russian economic leadership. Whether that consensus survives a second consecutive year of budget shortfalls and rising consumer taxes is the question shaping Russia’s economic trajectory through the remainder of 2026.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The United States government’s gross debt has crossed the $50 trillion threshold, reaching 120% of GDP, according to the Congressional Budget Office’s Long‑Term Budget Outlook released on June 10, 2026 (CBO Long‑Term Budget Outlook, June 2026). The sheer size of the number is arresting, but the market’s focus is on the trajectory: the CBO projects that, under current law, debt will hit 140% of GDP by 2036 and that net interest costs will exceed defense spending by 2029. In response, Fitch Ratings placed the United States’ AAA sovereign rating on negative watch, citing “entrenched political polarization that prevents timely and credible fiscal consolidation” (Fitch Ratings, June 2026). This is the most serious warning on US sovereign credit since the 2011 debt‑ceiling standoff.

The Debt Dynamics

The drivers of the debt surge are not a secret. Mandatory spending—Social Security, Medicare, Medicaid, and other health programs—now consumes 65% of federal outlays. Net interest, propelled by higher rates and a larger debt stock, accounts for another 16%. Discretionary spending on defense, infrastructure, education, and everything else has been squeezed to just 19%. The CBO notes that the retirement of the baby‑boom generation is accelerating: by 2026, the Social Security trust fund’s outlays exceed its payroll‑tax revenue by $350 billion annually, and the Hospital Insurance trust fund is on track to be depleted by 2032.

The Treasury market, the deepest and most liquid in the world, has started to signal discomfort. The term premium on 10‑year notes—the extra yield investors demand to hold longer‑term bonds instead of rolling short‑term bills—has risen to 0.6 percentage points, up from near zero in 2021. This is partly a function of increased supply: the Treasury auctioned a record $4.5 trillion in gross marketable debt in fiscal 2025, and the figure for 2026 is on pace to exceed $5 trillion. A recent auction of 20‑year bonds tailed by three basis points, indicating weaker‑than‑expected demand (US Treasury Department, June 2026 Auction Results).

Foreign Official Buyers Step Back

A critical source of Treasury demand—foreign central banks and sovereign wealth funds—has been pulling back. Data from the Treasury International Capital (TIC) system show that Japan and China, the two largest foreign holders, reduced their combined holdings by $210 billion over the 12 months through April 2026 (US Treasury TIC Data, June 2026). Japan is selling to finance intervention in the yen, while China is diversifying into gold and strategic commodities. OPEC nations, led by Saudi Arabia, have also been net sellers, redirecting petrodollar surpluses into real estate, private credit, and gold (see Article 18). The share of US Treasury debt held by foreigners has fallen to 23%, the lowest since 2003.

This retreat is not a panic sell‑off, but it changes the character of demand. It leaves a greater burden on domestic buyers—pension funds, insurance companies, and mutual funds—who are more price‑sensitive and constrained by regulatory limits. The Fed, which is still reducing its balance sheet through quantitative tightening at a pace of $60 billion per month, is no longer a buyer. The residual buyer of last resort is the Treasury market’s own depth, but episodes of illiquidity, such as the March 2025 flash crash, highlight the fragility under the surface.

The Fitch Warning and Political Paralysis

Fitch’s negative watch is a procedural step that gives the US government a six‑month window to demonstrate credible fiscal reforms before a formal downgrade. The 2011 precedent, when S&P downgraded the US, led to a sharp equity sell‑off and an ironic rally in Treasuries as risk‑aversion spiked. But 2026 is different: inflation is higher, global capital is more mobile, and there is a credible alternative in the euro and digital payment systems. A downgrade this time could trigger a sustained sell‑off in long‑duration bonds and push the 10‑year yield above 6%, according to a stress scenario modeled by the Brookings Institution (Brookings, “Fiscal Risks in an Era of High Debt”, June 2026).

The political response has been underwhelming. The June 2026 budget resolution passed by the House calls for a commission to study “fiscal sustainability options,” a mechanism that has failed repeatedly in the past. The Senate is gridlocked over whether to raise revenues through tax increases on corporations and high‑income individuals—the Biden administration’s preferred path—or to cut mandatory entitlements, which remains a political third rail. The debt limit, suspended in June 2023 until January 2025, was extended again until March 2027 in a late‑night deal that avoided default but added $1.2 trillion in new spending over two years. “We are in the classic ‘too little, too late’ danger zone,” noted a former CBO director in an op‑ed for the Wall Street Journal.

Treasury Market Stress and Investor Hedges

For investors, the rising risk of a sovereign credit scare is translating into portfolio adjustments. The classic hedge—gold—has rallied to $2,500 per ounce, supported not just by geopolitical uncertainty but also by a structural shift in central bank reserve management. Treasury Inflation‑Protected Securities (TIPS) have underperformed due to weak inflation breakeven demand, but short‑duration nominal Treasuries are still viewed as safe. The real innovation is in outcome‑based hedging: several large institutional investors have purchased long‑dated options on US rates volatility, betting that a fiscal confidence shock will cause a spike in the MOVE index (CME Group, June 2026 Options Open Interest Data).

Equity‑wise, sectors with pricing power and low reliance on government contracts are favored. Defense stocks are a paradox: they benefit from rising budgets but are vulnerable to a fiscal crunch that targets discretionary spending. International diversification, particularly into Indian and Southeast Asian assets, is being pitched as a hedge against a US‑centric debt problem.

The Bottom Line

America’s $50 trillion debt is not an immediate crisis, but it is a steadily tightening vice. The CBO’s projections are not worst‑case scenarios; they assume no recession, no major war, and interest rates that gradually moderate—all optimistic assumptions. The Fitch warning is a shot across the bow, a reminder that the world’s reserve currency issuer does not have an infinite credit card. The path to stabilization requires an unlikely combination of political courage and economic luck. Without it, the US will find itself in a slow‑motion fiscal trap that erodes the dollar’s primacy and raises borrowing costs for every American household and business.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

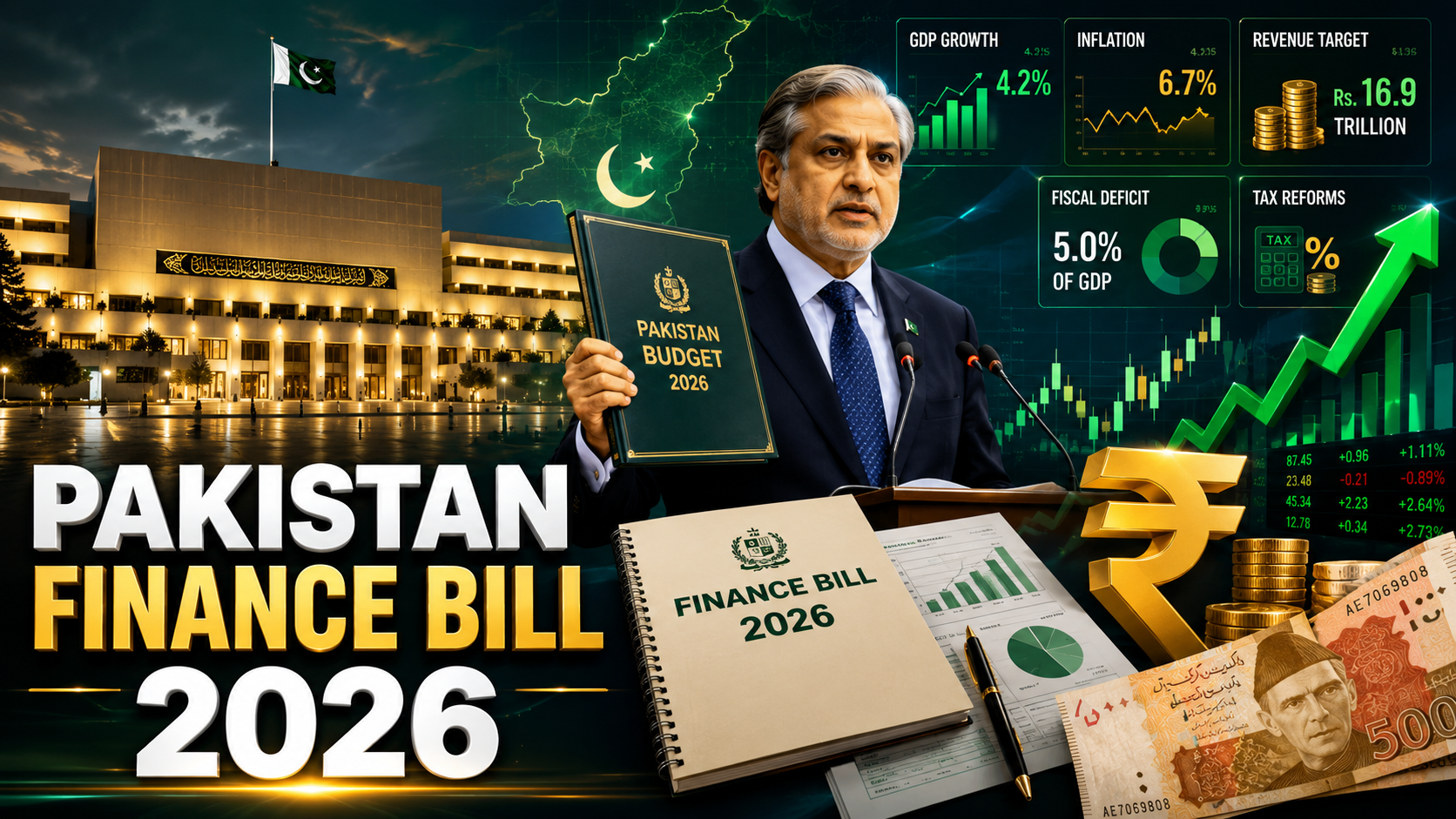

Islamabad’s revenue machine is grinding, and the gears are stripping. The Finance Bill 2026 arrived with a headline FBR target near Rs15.3 trillion for the new fiscal year — an extraction-first model layered atop one that has already missed its FY26 goal by roughly Rs868 billion. Politicians call it reform. The arithmetic says something blunter: Pakistan is squeezing the same documented taxpayers harder, year after year, while the tax-to-GDP ratio barely moves. That gap between rhetoric and result is the story.

Pakistan’s tax-to-GDP ratio has hovered between 9 and 11 percent for years — among the lowest in South Asia. The IMF’s $7 billion programme made fiscal consolidation non-negotiable, and the FBR’s own mid-year numbers tell the compliance story bluntly: during July–April of FY26, the agency collected around Rs10.25 trillion against a target of Rs10.90 trillion, a shortfall of nearly Rs683 billion, with income tax missing by roughly Rs210 billion and sales tax by Rs382 billion. By the eleven-month mark, that gap had widened further — Rs868 billion behind target, with Rs11.23 trillion collected against a revised Rs12.10 trillion goal. The Bill doesn’t fix the structure that produced this. It raises the ask.

The numbers behind Budget 2026-27 are, in a word, aggressive. The IMF-supported framework envisages an FBR target of nearly Rs15.3 trillion, alongside a petroleum levy target of Rs1.73 trillion — even as the outgoing year limped to a close roughly Rs868 billion short. Provincial governments are following the same playbook. Punjab’s finance minister told reporters his province had achieved 99 percent of its tax collection target in the outgoing fiscal year, while raising the FY27 target by 46 percent, with own-source revenue expected to climb 30 to 40 percent.

The Finance Bill’s enforcement architecture has hardened to match those ambitions. The bill expands FBR’s enforcement powers, raises the cost of ATL restoration fivefold, and puts businesses at risk of having their premises sealed for non-compliance. A new digital layer compounds it: the FBR is proposed to be empowered to operate an algorithmic settlement mechanism, with a National Faceless Centre conducting income tax, sales tax, and federal excise proceedings without direct officer contact.

The justification, officially, is efficiency. The effect, structurally, is more pressure on the same compliant base:

- Withholding-heavy collection remains the default tool, not a stopgap.

- Faceless audits centralise discretion rather than removing it.

- Provincial mimicry of the FBR model multiplies the points of contact, not the tax base.

This is extraction dressed as modernisation — and the FBR’s own mid-year shortfall numbers suggest the dressing isn’t fooling markets.

Why Pakistan’s tax-to-GDP problem resists Finance Bill fixes

Move past the headline target and the deeper issue is structural, not seasonal. Pakistan’s formal sector — salaried employees and registered corporations — is taxed at source, with zero room for deferral. The informal economy, by contrast, operates largely outside the net.

What is Pakistan’s current tax-to-GDP ratio in 2026?

Pakistan’s tax-to-GDP ratio sits near 10.3–10.6%, among the lowest in South Asia and well below the IMF’s original 11% target for FY26. The shortfall stems from narrow documentation, not insufficient rates — informal retail, real estate, and agriculture remain largely outside the formal tax net.

The Pakistan Business Council has made the structural critique explicit, warning that the current system taxes turnover as a proxy for profit, burdening even loss-making businesses, while the formal sector is treated as unpaid tax collectors through withholding obligations. The Council goes further, noting salaried employees pay significantly higher taxes than their Indian counterparts, a factor in brain drain, while Capital Value Tax on overseas assets is pushing wealthy Pakistanis to surrender nationality — undermining the very FDI inflows the budget needs.

A World Bank policy note cited in recent coverage put the inequity plainly: a narrow, compliant segment — primarily salaried workers and large corporations — carries a disproportionate share of the tax burden while large portions of the economy remain outside the net. Yet the Finance Bill’s enforcement upgrades target documentation that already exists, rather than the 40% of GDP the Business Council estimates operates undocumented. That’s the information gap competing coverage keeps missing: more enforcement technology aimed at the same compliant 60% doesn’t change the denominator.

The salaried class did receive something this cycle — a partial olive branch buried inside an otherwise extractive bill. Salaried individuals get lower rates across four brackets and lose an unpopular surcharge, with the GDP growth target set at 4% and inflation projected at 8.2%, a number attributed largely to ongoing Middle East tensions affecting energy markets. The fiscal logic behind the relief is unusually candid: a recent analysis noted the IMF itself concluded that overtaxing the most compliant sector while the informal economy remains undertaxed is counterproductive — a salaried class under unsustainable burden sees purchasing power erode, consumption contract, and revenues ultimately decline.

But that relief was financed, not gifted. The compensating measures required by the Fund include Rs430 billion expected from provincial agricultural income tax mechanisms and an expanded fixed tax scheme for the retail sector — precisely the informal-sector reforms that have proven politically hardest to enforce in past budget cycles. If they underperform, as agricultural and retail levies typically have, the FBR has only one lever left: withholding agents, who are already absorbing the bulk of FY26’s shortfall.

For SMEs and documented businesses, the second-order effect is a tightening compliance cost spiral — fivefold ATL restoration penalties, faceless algorithmic audits, and sealed-premises risk arrive at the same moment the government is asking for 46% more revenue at the provincial level. Markets reading this Bill should expect compliance costs to rise faster than actual base-broadening, at least through FY27.

Government officials frame the target as achievable discipline. The Punjab finance minister expressed confidence that the 46% increase would be met, citing the province’s near-perfect FY26 collection rate and a projected 30 to 40 percent rise in own-source revenue. Officials defending the federal numbers point to the FBR’s recent history of double-digit growth in some collection heads as proof the system can scale.

That confidence runs against the IMF’s own posture. Mid-year negotiations reportedly moved toward cutting, not raising, the FY26 target — from an original Rs14.13 trillion down toward Rs13.45 trillion, with the tax-to-GDP ratio projected at just 10.6% rather than the originally agreed 11%. The Fund’s own caution about over-relying on withholding-driven collection — the rationale behind the salaried-class relief — sits awkwardly beside provincial governments doubling down on identical withholding-heavy models. Two arms of the same fiscal programme are, in effect, pulling in opposite directions: one easing pressure on the documented base, the other expanding the apparatus that squeezes it.

The tension at the centre of Finance Bill 2026 isn’t really about rates or targets. It’s about whether Pakistan can broaden a tax base that has resisted broadening through three IMF programmes running. Faceless centres, algorithmic settlement, and fivefold penalty increases are administrative upgrades to an extraction model — not a redesign of it. The agricultural and retail levies the IMF is counting on to offset salaried relief have a thin track record. Extraction has carried Pakistan’s fiscal arithmetic this far. It’s running out of room to carry it further.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025