Analysis

How Beijing’s Block of Meta’s Manus Deal Is Redrawing the Map of Global AI

China’s rejection of Meta’s $2 billion acquisition of agentic AI startup Manus is not merely a regulatory footnote. It is a strategic declaration—one that signals AI has crossed a threshold from commercial asset to national sovereign resource, and that the old playbook for internationalizing Chinese technology is finished.

By the middle of 2025, a new term had entered the quiet lexicon of venture capitalists navigating the US-China technology rift: “Singapore-washing.” The concept was simple enough. A promising Chinese AI startup, wary of rising geopolitical risk, would shift its legal registration to a neutral Southeast Asian jurisdiction, relocate a portion of its team, raise Western capital, and present itself to global markets as a de facto global firm—one that happened to be founded by Chinese engineers but was now safely incorporated outside the dragon’s reach.

Manus looked, for a time, like the paradigmatic success story of this model. Founded as the Monica.im project by Beijing Butterfly Effect Technology, it released its first general-purpose AI agent in March 2025 to breathless comparisons with DeepSeek. The startup had passed $100 million in annual recurring revenue by December 2025—eight months after launching a product—claiming at the time to be the fastest company in the world to reach that milestone from zero. CNBC It had moved staff to Singapore mid-year, raised $75 million in a round led by Silicon Valley’s Benchmark, and attracted the attention of Meta Platforms, which announced a $2 billion acquisition in December 2025.

Then, on April 27, 2026, Beijing slammed the door.

China’s National Development and Reform Commission ordered the deal’s cancellation in a brief statement, citing laws and regulations, without elaborating further. Bloomberg The message, however, was anything but brief in its implications.

The Anatomy of a Blocked Deal

To understand why Beijing intervened, one must look past the Singapore address on Manus’s incorporation documents. According to Chinese regulatory findings, Manus’s core technologies were developed in China and involve processing massive amounts of user data. Its China-based affiliated entities—Beijing Red Butterfly Technology and Beijing Butterfly Effect Technology—remained active, and the technical origin and domestic entities had not been legally separated. TechNode

In Beijing’s legal reading, this was not a Singaporean company selling itself to an American buyer. This was Chinese intellectual property—developed on Chinese soil, using Chinese data infrastructure—attempting to depart through a side door without paying the sovereign toll.

Under China’s Measures for the Security Review of Foreign Investment, the Catalogue of Technologies Prohibited and Restricted from Export, and the Measures for Security Assessment of Data Export, core AI algorithms fall under restricted export technologies, requiring compliance with technology export licensing procedures and data security assessment requirements. TechNode The parties, regulators alleged, had circumvented these procedures entirely.

The human consequences were stark. The Financial Times reported in March that Manus co-founders Xiao Hong and Ji Yichao had been subjected to exit bans—barred from leaving China as the investigation deepened. Meanwhile, Manus employees had already moved into Meta offices in Singapore, capital had been transferred, and exiting investors including Tencent, ZhenFund, and Hongshan had received their proceeds. Business Standard Unwinding the deal, as the NDRC now demands, will be legally and logistically Byzantine.

Singapore-Washing: A Model Under Siege

The Manus affair has exposed what was always the fundamental vulnerability in the Singapore-washing strategy: geography is not sovereignty. A legal address in one of the world’s most business-friendly jurisdictions cannot override the reality of where technology was conceived, where engineers were trained, and where the underlying data originates.

Beijing is sending a message, and it reads clearly: residency in Singapore will no longer insulate Chinese-founded companies from regulatory scrutiny, forcing founders to choose between Western capital and Chinese ties. Yahoo Finance

This represents a seismic shift in the operating assumptions of Chinese entrepreneurship over the past decade. The variable interest entity (VIE) structure, red-chip listings, offshore incorporation, talent relocation—these were all instruments of a system that allowed Chinese innovation to access global capital while remaining, in practice, deeply embedded in China’s domestic ecosystem. Beijing tolerated this ambiguity when the technology in question was consumer internet. It is no longer prepared to do so when the asset in question is frontier artificial intelligence.

The reasoning, while heavy-handed in execution, is not without internal logic. According to Stanford University’s 2026 AI Index report, the long-standing performance gap between US and Chinese AI systems has effectively disappeared, with models from both countries now competing at comparable levels—and Chinese systems like DeepSeek-R1 at times matching leading US models. International Business Times When you are operating in a near-peer technological competition with the world’s largest economy, allowing your most valuable intellectual assets to be acquired by a direct rival is not merely bad commercial strategy. From Beijing’s perspective, it is a national security failure.

The Broader Crackdown: Capital Controls Enter the AI Age

The Manus block did not arrive in isolation. It is the visible tip of a rapidly submerging policy architecture.

Chinese agencies including the NDRC have told several private firms in recent weeks that they should reject capital of US origin in funding rounds unless explicitly approved. Yahoo Finance The scope of these instructions is remarkable. Moonshot AI, which is considering an initial public offering, was among those that received guidance from the state planner. Fellow startup StepFun received similar instructions. Regulators have also decided on similar restrictions for ByteDance, the owner of TikTok, blocking secondary share sales to US investors without government approval. Yahoo Finance

Consider the scale of disruption this implies. Moonshot AI is seeking to raise as much as $1 billion in a funding round that would value the startup at approximately $18 billion. StepFun, which is considering a $500 million float in Hong Kong, is in the process of unwinding its overseas entities and onshoring capital to meet regulatory requirements. Yahoo Finance

The new restrictions risk further isolating China’s recovering tech sector from the venture backing that has underpinned it for two decades, much of which was sourced from American pensions and endowments. Yahoo Finance The parallel move to restrict red-chip firms from seeking Hong Kong IPOs simultaneously closes off two of the primary channels through which Chinese companies have historically accessed Western capital markets. The architecture of financial globalization that powered China’s technology rise is being deliberately disassembled, brick by brick.

A Mirror Image: The Decoupling Is Now Bilateral

To appreciate the full symmetry of what is happening, one must look westward as well. Washington did not wait for Beijing to move first. The US Treasury Department finalized rules in 2025 restricting American outbound investment into Chinese companies operating in AI, semiconductors, and quantum computing. Congressional proposals including the COINS Act have sought to formalize and expand these restrictions. The Committee on Foreign Investment in the United States (CFIUS) has increasingly scrutinized technology transactions involving Chinese counterparties, regardless of where the formal acquirer is registered.

In other words, Beijing’s move is not an unprovoked act of protectionism. It is, in considerable measure, a mirror response to the regime Washington has been constructing for years. China’s escalation mirrors steps taken by Washington months earlier, when US authorities restricted outbound investment into Chinese companies operating in AI, semiconductors, and quantum computing on national security grounds. FX Leaders Both governments now operate from the same strategic premise: advanced artificial intelligence is not a commercially neutral technology. It is a lever of national power, and allowing adversaries to access it—through acquisition, investment, or talent migration—is a strategic error.

What has changed, dramatically and perhaps irreversibly, is the speed at which this mutual calculus is hardening. The Manus affair compressed years of latent tension into months of regulatory escalation. What once required a geopolitical incident to trigger can now be set off by a single startup’s term sheet.

The Chilling Effects on Innovation and Entrepreneurship

None of this, however, occurs without cost—and Beijing’s calculus, however strategically coherent, carries real dangers for the ecosystem it claims to protect.

The founders of Manus did not set out to betray China. They built a remarkable technology, attracted global capital, and attempted to navigate a world in which their homeland’s commercial and regulatory environment had become increasingly inhospitable to internationally ambitious startups. The exit bans imposed on Xiao Hong and Ji Yichao—whatever the legal justification—send a chilling signal to every talented Chinese engineer who might contemplate building for a global market.

Chinese government scrutiny of AI companies could impact other Chinese startups’ strategies for expansion and funding in the United States. The Washington Post The subtler damage is harder to measure but likely deeper: the erosion of the entrepreneurial confidence that produced companies like Manus in the first place. If the reward for building a breakout AI startup in China is an exit ban and a forced transaction reversal, the rational response for ambitious engineers is either to stay entirely within the domestic system—or to leave China earlier and more completely than Manus ever did.

Neither outcome serves Beijing’s long-term interests. The first risks insulating Chinese AI development from the competitive pressure that drives frontier innovation. The second accelerates precisely the kind of talent drain the crackdown is ostensibly designed to prevent.

Implications for Global Investors and the Future of Agentic AI

For the global venture capital community, the Manus block is a hard lesson in jurisdictional risk. The Singapore-registration playbook worked, until it didn’t. Benchmark, which led Manus’s Series A at a $500 million valuation, now finds itself holding an asset caught in one of the most complex geopolitical unwindings in recent startup history. Future investments in companies with significant Chinese technical heritage will require a level of regulatory due diligence that venture firms have historically neither staffed nor priced.

The specific domain of agentic AI—autonomous systems capable of executing complex multi-step tasks across diverse environments—makes this regulatory conflict particularly consequential. Agentic AI is widely viewed as the next major frontier of commercial AI deployment, with applications spanning enterprise automation, scientific research, and consumer productivity. When Meta announced the Manus deal, it said it would look to accelerate AI innovation for businesses and integrate advanced automation into its consumer and enterprise products, including its Meta AI assistant. CNBC The block does not merely deprive Meta of a team and a technology. It delays and fragments the development of a genuinely transformative technology category at the precise moment when the competitive race is most intense.

Recommendations: Navigating the New Landscape

The structural forces driving this bifurcation are not going away. But they need not produce an outcome that is worse for everyone. Several principles should guide policymakers, investors, and technologists in the period ahead.

For governments: Both Washington and Beijing should establish clearer, more predictable frameworks for cross-border technology investment reviews. The opacity of China’s current approach—a one-line NDRC statement, exit bans without charges, informal guidance to portfolio companies—creates uncertainty that harms legitimate commercial activity far beyond the specific deals under scrutiny. Rules that are knowable in advance are less disruptive than rules that arrive by surprise.

For investors: Structural due diligence must now include technology provenance analysis—understanding not just where a company is registered, but where its core intellectual property was developed, where its data originates, and whether its founding team could face legal constraints in either jurisdiction. Geography of incorporation is no longer a sufficient proxy for legal exposure.

For technology companies: The era of the “borderless startup” in AI is functionally over. Companies with genuine global ambitions must make earlier, cleaner decisions about their primary regulatory home. Ambiguity that was once commercially convenient has become a liability that can be weaponized by regulators on either side of the Pacific.

The Longer View

History will likely record the Meta-Manus episode as one of those moments when the underlying logic of an era became suddenly, viscerally legible. For the better part of two decades, the world operated on the assumption that technology and capital were, at their core, cosmopolitan forces—that they would flow toward talent and opportunity regardless of national boundaries, and that this flow was ultimately good for everyone.

That assumption is not dead. But it is seriously wounded. As the NDRC tightens its grip, the digital arteries connecting US and Chinese tech sectors are being severed, one funding round at a time. TechStory

The Manus block is not the end of Chinese AI innovation—China’s engineers are too numerous, too talented, and too well-supported by state capital for that. Nor is it the end of Meta’s ambitions in agentic AI. But it is the end of the comfortable fiction that the US-China technology competition could be navigated by clever corporate structuring. The battle lines are now drawn at the level of technology itself—who built it, where, with whose data, and for whose benefit.

In that contest, there are no neutral flags of convenience, and Singapore is no longer far enough away.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

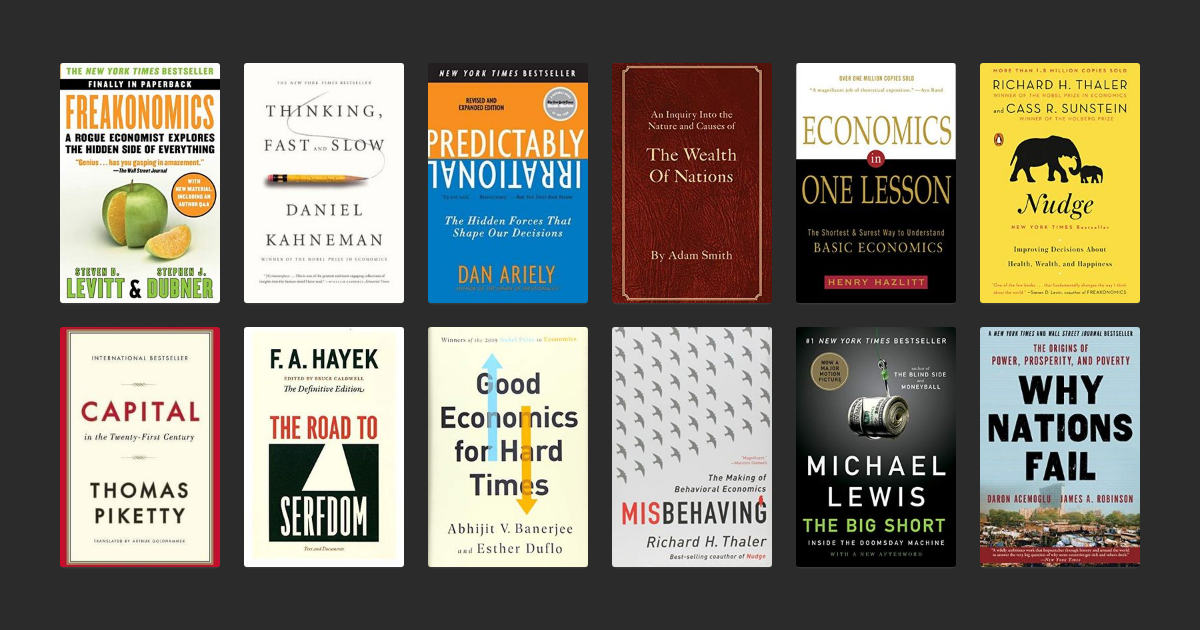

The global economy is operating in a state of suspended animation. Central banks have aggressively paused their tightening cycles, yet the anticipated soft landing remains stubbornly out of reach for much of the developed world. To parse this volatility, professionals need more than daily market briefings; they require deep structural clarity. Selecting the best economics books to read this summer requires filtering out pop-business fluff in favour of rigorous, systemic analysis. This year’s definitive titles tackle the end of the post-Cold War peace dividend, the productivity paradox of artificial intelligence, and the messy, expensive unwinding of globalized supply chains.

We are transitioning from an era of capital abundance to one of persistent, structural friction. The International Monetary Fund’s latest projections cap global growth at a sluggish 3.1% for the medium term, representing the weakest macroeconomic forecast in decades. Simultaneously, global public debt is on track to approach 93% of global GDP by the end of 2026, leaving policymakers with razor-thin margins for error.

Investors and institutional analysts are scrambling to update their mental models. The old correlations between sovereign bond yields and equity valuations have fundamentally broken down. The texts dominating the conversation this season do not offer quick, palliative fixes. Instead, they provide vital historical context for our current stagnation and mathematical frameworks for pricing in geopolitical risk. Understanding these texts is essential for anyone allocating capital, managing institutional risk, or drafting public policy in the latter half of the decade.

The defining economic hangover of our time is the return of structurally higher interest rates. For the past two decades, the Federal Reserve and the Bank of England operated under the core assumption that deflation was the primary enemy of state growth. The brutal inflation shock of the early 2020s shattered that consensus entirely.

To understand the permanent shift in central banking, the standout texts this season argue that the era of zero-interest-rate policy (ZIRP) was an historical aberration, not a baseline. The Organisation for Economic Co-operation and Development (OECD) notes that core inflation across G7 nations remained sticky at 3.8% well into late 2025, consistently defying aggressive rate hikes. This persistent stickiness forces a total re-evaluation of sovereign debt sustainability.

Authors in this space point to a grim reality: governments must now roll over their massive pandemic-era debt at significantly higher yields. In the UK alone, the Office for National Statistics (ONS) reported that debt interest payments hit £111 billion last year. This consumes tax revenue that would otherwise fund domestic growth initiatives or infrastructure projects.

This summer’s essential reading strictly dissects these fiscal constraints. The best analysts trace the direct line from monetary tightening to corporate defaults. They argue that zombie companies, kept alive artificially by a decade of cheap credit, face an imminent reckoning. Corporate bankruptcies in the US surged by 18% year-over-year, according to deeply researched S&P Global data. The books highlighting this trend offer a sobering look at capital reallocation, suggesting that this pain is a necessary feature of returning to sound money principles.

Still, the analysis goes far beyond domestic pain in the US and Europe. It extends to emerging markets, where a historically strong US dollar exports inflation across borders. The structural trap set by a hawkish Fed leaves developing economies with an impossible choice: defend their currencies and kill domestic growth, or let them slide and import hyperinflation. When Jerome Powell testified before the Senate in early 2026, he explicitly abandoned the notion of a quick return to cheap money, a pivot these books examine in forensic detail.

Furthermore, commercial real estate (CRE) presents the most immediate systemic vulnerability explored in these pages. The Federal Reserve’s Financial Stability Report highlights that over $1.2 trillion in commercial mortgages mature before 2027. Refinancing these depreciated assets at current rates will crystallize massive losses for regional banks. The books dissecting this dynamic do not just forecast a localized crash; they trace the contagion vectors from empty office towers in major metropolitan centres directly into global pension fund portfolios.

Beyond monetary policy, the structural rewiring of the labour market via Artificial Intelligence (AI) dominates the top macroeconomics books 2026 has to offer. The initial euphoria surrounding generative models has cooled significantly in financial capitals, replaced by hard, empirical questions about productivity metrics, capital expenditure, and wage suppression.

The best economics books to read this summer include authoritative texts on inflation dynamics, the macroeconomic impact of artificial intelligence, and the geoeconomic fragmentation of global trade. Top titles provide data-driven frameworks for investors and policymakers to understand the structural end of the zero-interest-rate era.

Economists are currently obsessed with the gap between technological capability and measurable economic output. MIT economist Daron Acemoglu‘s latest collaborative research sets the intellectual foundation for this summer’s most compelling arguments. The core thesis posits that while AI can automate specific cognitive tasks, its aggregate impact on Total Factor Productivity (TFP) remains statistically invisible.

Investment banks initially projected a global GDP boost of 7% over a decade due to AI integration. Yet, the texts emerging this season take a sharply critical view of such optimistic, linear modelling. They point out that capital expenditure on server infrastructure and energy grid expansion is vastly outpacing the actual revenue generated by these software tools.

The picture is more complicated than simple job displacement. The authors argue we are witnessing a massive “task reallocation” that hollows out middle-management while simultaneously creating physical bottlenecks in energy supply chains. Labour economist David Autor provides a necessary counterweight to the prevailing pessimism in his recent working papers, themes echoed heavily in this summer’s curated titles. He suggests AI could theoretically rebuild the middle class by democratising technical expertise, allowing lower-skilled workers to perform higher-value medical or coding tasks.

Yet, the consensus among the top titles remains heavily sceptical. They look at the empirical data showing tech companies aggressively reducing headcount while simultaneously reporting record profits. The productivity gains are currently being captured entirely by capital owners, not labour forces.

This creates a highly bifurcated economy. Companies that successfully integrate proprietary data with localized language models pull away from competitors, creating monopolistic dynamics that antitrust regulators are entirely unequipped to handle. The reading list this summer unpacks how the European Union’s AI Act might actually cement the dominance of incumbent tech giants by raising compliance costs to fatal levels for open-source start-ups. We must look closely at the wage data; real wages for knowledge workers plateaued in the first quarter of 2026, a trend these authors attribute directly to the commoditization of routine cognitive labour.

The third major theme dominating this summer’s reading lists is the aggressive, unapologetic return of state-directed industrial policy. The Washington Consensus, which championed free trade and deregulation for three decades, is officially dead. In its place is a scrambled, multi-trillion-dollar rush for domestic resource security.

Governments are no longer optimizing for cost efficiency; they are optimizing for systemic resilience. The World Bank’s latest Global Economic Prospects report highlights a staggering 20% drop in foreign direct investment (FDI) flowing between geopolitically unaligned nations. This fragmentation has massive downstream consequences for multinational corporations across three distinct vectors:

- Capital Expenditure: A forced, highly inefficient duplication of manufacturing infrastructure across rival trading blocs.

- Compliance Drag: Escalating legal and logistical costs required to navigate divergent export controls and international sanctions.

- Resource Hoarding: State-backed stockpiling of critical minerals, artificially restricting market supply and driving up baseline commodity prices.

Books tackling this subject focus heavily on the semiconductor industry and the chaotic transition to green energy. They detail how the US CHIPS and Science Act and the Inflation Reduction Act (IRA) have triggered a global subsidy arms race. Authors argue this capital misallocation will inevitably suppress global growth over the next decade. When Europe, the United States, and China simultaneously subsidise their own redundant supply chains, the mathematical result is structural overcapacity and severe trade friction.

Germany’s ongoing economic malaise serves as the primary case study in these chapters. The sudden loss of cheap Russian pipeline energy, combined with slowing Chinese demand for heavy industrial exports, has severely broken the European engine of growth. The European Central Bank (ECB) faces the unenviable task of managing localized stagflation within a fractured political union.

That said, these analysts also identify the unexpected winners of this global fragmentation. ‘Connector economies’ like Mexico, Vietnam, and India are rapidly capturing the manufacturing overflow as Western companies execute “China Plus One” derisking strategies. A standout statistic from a heavily cited text notes that Mexico officially surpassed China as the largest exporter to the US in late 2025, moving over $475 billion in physical goods. Investors reading these books will find actionable, data-rich blueprints for identifying which emerging markets stand to gain from the ongoing superpower decoupling. Traditional metrics like the Consumer Price Index (CPI) are suddenly less predictive of sovereign market movements than the shipping tonnage safely passing through the Strait of Malacca.

Competing Perspectives: The Degrowth Dissent

No comprehensive reading list is complete without seriously engaging with its harshest critics. While the mainstream macroeconomic texts focus on restoring sluggish growth and managing sticky inflation, a highly vocal minority of economists argues that the pursuit of infinite GDP expansion is biologically and ecologically bankrupt.

The ‘degrowth’ movement, once relegated to the fringe of academic sociology, has secured serious, mainstream publishing deals this summer. These authors provide a mathematical steel-man against the popular green-growth consensus. Their core argument rests on the absolute decoupling fallacy. The European Environment Agency (EEA) published data showing that while domestic emissions have fallen in developed nations, the total material footprint per capita continues to rise when factoring in imported goods.

Prominent ecological economist Herman Daly laid the theoretical groundwork decades ago, but this year’s authors apply his strict frameworks to the immediate, localized climate crises of 2026. They argue that technological substitution—replacing combustion engines with heavy lithium-ion batteries—merely shifts the ecological bottleneck from the atmosphere to the Earth’s crust.

Japanese philosopher Kohei Saito and his surprising commercial success regarding degrowth frameworks serves as a prime example. His thesis, heavily discussed in serious economic circles, argues that planetary boundaries cannot mathematically support infinite capital accumulation. Mainstream economists are forced to engage with this, not to adopt a radical framework, but to accurately account for hard ecological limits. If physical inputs like arable land, fresh water, and copper become absolute constraints, the standard Solow-Swan economic growth models break down entirely.

Rather than dismissing these texts as utopian fantasy, serious financial analysts are reading them to understand future regulatory risks. If global carbon pricing and aggressive resource taxes escalate, the degrowth models will suddenly look less like radical activism and more like predictive corporate risk modelling. Engaging with this dissenting view signals a refusal to be blindsided by rapidly shifting political realities. Acknowledging that the transition to a low-carbon economy may inherently suppress aggregate demand provides a much sharper edge to any long-term investment thesis than relying on outdated Keynesian multipliers.

The global economy in the latter half of the 2020s refuses to cleanly fit into twentieth-century analytical models. The sheer utility of the best economics books to read this summer is not that they offer perfectly accurate forecasts for the next quarter. Rather, they provide desperately needed, updated heuristics for an era defined by permanently higher capital costs, severe demographic inversions, and localized supply chain warfare.

Relying on out-of-date mental models is the fastest route to capital destruction. The prevailing economic narratives of the past decade—that technological monopolies will naturally democratise wealth, or that central banks can simply print their way out of a sovereign debt crisis—have been empirically and painfully disproven.

Professionals who dedicate time to these rigorous, heavily researched texts will possess a distinct analytical advantage. They will look past the daily, algorithmic noise of equities markets to see the shifting tectonic plates of the real, physical economy. Absolute clarity, not blind market optimism, is the ultimate competitive advantage for the remainder of the decade.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan’s current account surplus came in at $459 million in May 2026, the State Bank of Pakistan reported this week, reversing April’s $276 million deficit and marking the fourth monthly surplus the country has posted so far this calendar year. The rebound rode in on a record $4.25 billion in workers’ remittances — the largest single-month inflow in the country’s history — alongside a retreating import bill as global oil prices eased. Is this the recovery Islamabad has been promising for three years, or just a fortunate month dressed up as one? The data released this week offers a more complicated answer than the headline suggests.

The reading caps an unusually volatile year for Pakistan’s external account. After a $272 million deficit in December, the balance swung to a $68 million surplus in January and $231 million in February, then surged to a $1.13 billion surplus in March — among the strongest monthly outcomes on record — before slipping back into deficit in April. Stitch the eleven months together and the picture is more modest: a cumulative $255 million surplus for July–May FY2026, against a $1.62 billion deficit over the same period a year earlier.

The swings sit at the intersection of three larger stories: Pakistan’s $7 billion-plus IMF programme, a Middle East war that has rattled energy markets since February, and a federal budget unveiled in Islamabad just five days before this release. Khurram Schehzad, the finance minister’s economic adviser who took to social media after January’s, February’s and March’s releases to call each one a milestone, had less occasion to boast about April. May hands him the opportunity again.

It’s worth recalling how different this surplus looks from Pakistan’s last one. When the country first swung into positive territory in March 2023, the driver was a blunt import ban — Shehbaz Sharif’s government froze letters of credit for everything from car parts to mobile-phone components, and the trade gap closed because the economy simply stopped buying. Factories shut down as a side effect. This year’s improvement, by contrast, runs on remittance growth and a genuine, if fragile, dip in global energy costs — a less dramatic story, but a more durable one if it holds.

What’s Driving Pakistan’s Current Account Surplus

Workers’ remittances did almost all of the work. Overseas Pakistanis sent home $4.251 billion in May — up 20.2% from April and 15.4% higher than a year earlier — according to data released by the State Bank of Pakistan. It’s the highest monthly remittance figure on record, and analysts at Topline Securities trace much of the spike to Eid-ul-Adha season transfers, a seasonal pattern that repeats every year but landed with unusual force this time. April’s deficit, recall, reflected a seasonal dip in remittances colliding with a rebound in import demand; May simply reversed both halves of that equation at once.

The geography of those inflows tells its own story:

- Saudi Arabia: $1.025 billion, up 22% from April and 12% year-on-year

- United Arab Emirates: $1.007 billion, up 37% month-on-month and 33% year-on-year

- United Kingdom: $645.5 million, up 15% from April

- United States: $349.8 million, up 10% from April

- European Union: $466 million, up 8% from April

On the trade side, the improvement came from a less cheerful source. Exports of goods slipped to $2.37 billion in May from $2.62 billion in April, while imports eased to $5.69 billion from $5.99 billion, leaving a goods trade deficit of $3.32 billion for the month. A shrinking import bill, not stronger exports, did the narrowing — a distinction worth holding onto before celebrating too hard. Pakistan’s energy import bill benefited in particular from the broader retreat in global crude prices that month, a dynamic worth unpacking on its own.

One export line did genuinely improve. Information technology exports reached $4.19 billion over the first eleven months of FY2026, a 20% year-on-year jump worth an additional $710 million, according to official trade data reported this week. It’s one of the few places in Pakistan’s external accounts where the gain is coming from selling more, rather than simply buying less.

Pakistan’s current account isn’t just exports and remittances, either. The primary income balance — interest payments on external debt, profit repatriation by foreign investors — has been a persistent drag for years, and May’s improvement captures any easing there too. Services trade, dominated by freight, travel and IT-enabled exports, remains a smaller piece of the puzzle, but a growing one, as the IT sector’s pace of growth illustrates.

Beyond the Headline Number: Is Pakistan’s Current Account Recovery Sustainable?

Two forces converged in May, and only one of them is built to last. Remittances have grown on a year-on-year basis for nine straight months and are on pace to clear $41 billion for the full fiscal year — a structural feature of the balance of payments at this point, not a one-off windfall. The import retreat is a different story entirely.

What Caused Pakistan’s Current Account Surplus in May 2026?

Pakistan’s May 2026 surplus was driven primarily by record workers’ remittances of $4.25 billion, up 20% month-on-month on Eid-related transfers, combined with a falling import bill as Brent crude dropped roughly 19% on optimism over a lasting US-Iran ceasefire and Strait of Hormuz shipping.

That energy windfall is the half analysts are watching most closely. Brent crude fell to around $92.56 a barrel by the close of May, down nearly a fifth for the month and roughly 20% from its 2026 peak, as traders priced in a durable end to the standoff that had largely shut the Strait of Hormuz since February. Pakistan imports the overwhelming majority of its crude and refined products, so a softer oil price shows up almost immediately in the import line — and reverses just as quickly if the price snaps back.

Still, the truce it depends on has been anything but settled. Within days of oil’s late-May decline, fresh US strikes on Iranian targets revived fears the strait could close again, a reminder that Pakistan’s gains rest on a fragile geopolitical pause rather than a structural fix to its trade deficit. The same volatility shows up in prices: the Asian Development Bank has flagged that energy-driven inflation, already pushed back into double digits this spring according to Pakistan’s own Economic Survey, complicates the State Bank’s task of holding rates low enough to support growth while a surplus this fragile holds together.

The government’s own FY2027 budget — tabled by Finance Minister Muhammad Aurangzeb in the National Assembly on June 12, five days before this data — effectively concedes the point: it targets a $3.6 billion current account deficit for the year ahead, an implicit admission that May’s number is the exception rather than the new baseline.

What This Means for Markets, Policymakers and Pakistan’s FY2027 Budget

For the IMF, May’s data reinforces a case the Fund has already made. When its Executive Board completed Pakistan’s third EFF review and second RSF review on May 8, it described the external position over the first nine months of FY2026 as “broadly balanced” rather than triumphant, and released a combined $1.32 billion tranche regardless — $1.1 billion under the Extended Fund Facility and $220 million under the Resilience and Sustainability Facility. The review also credited Pakistan with a primary fiscal surplus on track for 1.6% of GDP in FY2026, the kind of detail that matters more to the Fund’s board than any single month’s current account print.

Gross reserves had climbed to $16 billion by end-December, up from $14.5 billion a year earlier, and Deputy Prime Minister Ishaq Dar said the disbursement reflected the Fund’s continued confidence in the government’s measures. That financing cushion matters because Pakistan has been spending reserves on debt repayment even as remittances flow in.

The country settled a $1.43 billion international bond and a $3.45 billion repayment to the Abu Dhabi Fund for Development within weeks of each other this spring, leaning on $3 billion in fresh Saudi deposits and a $5 billion rollover to keep reserves intact. A $750 million Eurobond — Pakistan’s first after a four-year gap in international capital markets — added a further sign that creditors are, cautiously, coming back.

Equity investors had already priced in much of this optimism. The KSE-100 closed near 179,000 points on June 16, up nearly 11% over the preceding month and 46% higher than a year earlier — one of the best-performing major indices anywhere in 2026. A current account surprise this size is unlikely to move a market already trading at multi-year highs on reform momentum and falling interest rates.

The bigger test arrives over the next twelve months. The Asian Development Bank warned in April that a prolonged Middle East conflict could still push FY2027 inflation to 6.5%, widen the trade deficit through higher energy and fertiliser costs, and squeeze the very remittance flows now propping up the external account.

Islamabad’s $3.6 billion deficit target is, in effect, a bet that the war doesn’t reignite. The same Economic Survey that flagged a spring inflation rebound also put FY2026 GDP growth at 3.7%, the fastest pace in four years but still short of the government’s own 4.2% goal — evidence that the recovery, like the current account, is real but incomplete. May’s data buys the government time. It doesn’t yet buy certainty.

The Skeptics’ Case: Why Some Economists Aren’t Celebrating

Not every economist reads May’s number as unambiguous good news. The recurring critique, voiced loudest around this month’s budget, is that Pakistan’s external stability rests on remittances rather than on the country actually producing and selling more to the world. Former finance minister Hafeez Pasha has argued that the economy is showing signs of a mild Dutch disease — remittance-fuelled household spending crowding out investment in tradable sectors, with a disproportionate share of that money flowing into real estate rather than manufacturing.

The numbers lend the critique some weight. Pakistan’s own State of the Economy report projects remittances at up to $42 billion this fiscal year against goods and services exports of just $30.5 billion, a gap that’s widened rather than narrowed even as the current account has improved. Analysts made a related point when the account briefly slipped into deficit earlier this year, cautioning that reliance on remittances and external financing cannot substitute for the structural reforms Pakistan’s export sector still needs.

Brokerage research desks tend to land somewhere in between. Topline Securities has welcomed the remittance trend while still describing the broader external position as one that needs export diversification to be considered fixed, rather than financed. That’s a more cautious read than the finance ministry’s own messaging, even if it stops well short of the structuralist critique coming from Islamabad’s academic economists.

Pakistan Bureau of Statistics trade figures for June, due in early July alongside the SBP’s own current account release, will be the next checkpoint. A fifth consecutive monthly surplus would start to look like a trend; a return to deficit would vindicate the sceptics faster than anyone in the finance ministry would like.

The counter-argument, favoured inside the finance ministry, is that a dollar earned is a dollar earned regardless of channel, and that sequencing matters: external stability has to come first if reform-minded investment is ever going to follow it. Neither side disputes the immediate numbers — only what they’re supposed to mean for the year ahead.

What May’s surplus actually proves is narrower than the headline suggests. Pakistan’s external account didn’t get healthier in any structural sense this month; it got luckier, on an oil price it doesn’t control and a remittance season that arrives every year around Eid. That’s not nothing — $459 million is real money, and a fourth surplus in five months is a genuine improvement on the chronic deficits that defined the decade before the current IMF programme began.

Yet the government’s own budget makes the more honest argument here, conceding a $3.6 billion deficit for the year ahead even while celebrating the data behind it. Three years into a fund programme built on rebuilding reserves and credibility, Pakistan’s economy can now absorb a bad month without it becoming a crisis. May was a good one. In an economy this exposed to a war being fought eight time zones away, that is closer to genuine progress than any single surplus figure could ever capture.

SEO & CTR Package

[ 3x TITLE TAG VARIATIONS ]

- — 54 chars

- Pakistan’s $459M Current Account Surplus, Explained — 51 chars

- Why Pakistan’s Current Account Surplus Won’t Last — 49 chars

[ META DESCRIPTION ]

Pakistan’s current account surplus hit $459M in May 2026 on record remittances. But the FY2027 budget already targets a $3.6B deficit. H

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Inside a nondescript San Francisco warehouse, mechanical arms are learning to fold laundry, clear tables, and assemble boxes. They are not executing hardcoded scripts, but learning by observing human physics in real-time. This is the frontline of the next computing paradigm, where silicon meets gravity. The recent $400 million funding round for Physical Intelligence, heavily backed by Jeff Bezos and OpenAI, signals a definitive pivot from generative text to embodied cognition. This Amazon physical AI investment fundamentally alters the timeline for autonomous automation across global logistics. Software is no longer content to merely eat the world; it actively wants to touch it.

The Macro Landscape: Moving From Text to Torque

For the past three years, capital markets obsessed over large language models confined to climate-controlled server racks. Generative systems can write complex code and compose passable poetry, but they cannot turn a doorknob or catch a falling glass. Now, the macro landscape is violently rebalancing toward Embodied AI. Silicon Valley venture funds and corporate treasuries poured billions into robotics and spatial computing throughout early 2024, desperately seeking the bridge between digital intelligence and physical execution.

The economic calculus driving this shift is brutal and remarkably clear. Global supply chains remain deeply vulnerable to chronic labor shortages and wage inflation. According to recent demographic analyses, manufacturing vacancies will cost the US economy roughly $1 trillion annually by 2030. Amazon recognises that retaining its e-commerce supremacy requires automating the unpredictable, chaotic spaces within its sprawling fulfilment centres.

This transformation requires artificial intelligence that intrinsically understands gravity, friction, torque, and spatial reasoning. The transition from predicting text tokens to predicting physical force trajectories represents the most capital-intensive arms race in modern technological history. It’s a fundamental recognition that the digital economy sits atop a highly fragile physical foundation.

The Core Development: Hardware-Agnostic Intelligence

The strategy behind backing startups like Physical Intelligence reveals a crucial shift in how tech conglomerates approach automation. Historically, robotics required bespoke software written for a specific piece of hardware. A robotic arm designed to weld car doors could not be repurposed to pack grocery bags without millions of dollars in reprogramming. Karol Hausman, the startup’s CEO and a former Google robotics executive, is pioneering an entirely different approach called Pi0, a general-purpose foundation model for physical machines.

This model learns how the physical world operates by ingesting massive datasets of robotic telemetry, video feeds, and physics simulations. Rather than programming a machine to perform a task, the machine queries the model to understand the physical dynamics of the task itself. This decouples the intelligence from the hardware.

Amazon’s strategic interest in this decoupling is immense. The company deploys over 750,000 robots across its global network, traditionally relying on closed, proprietary systems like Kiva Systems. By funding external foundation models, Amazon aims to commoditize the hardware layer. If the intelligence lives in the cloud, the physical robot becomes a cheap, interchangeable vessel.

To grasp the scale of this development, consider the core technological hurdles being cleared:

- Cross-Embodiment Learning: A model trained on data from a quadruped robotic dog can apply spatial reasoning to a bipedal humanoid or a stationary picking arm.

- Physics Tokenisation: Converting physical actions—like the pressure required to grip a ripe tomato without crushing it—into mathematical tokens that neural networks can process.

- Zero-Shot Execution: Allowing a machine to encounter a novel object it has never seen before and accurately deduce how to manipulate it.

This shift severely threatens incumbent industrial robotics manufacturers. If intelligence becomes hardware-agnostic, the margin profile of traditional robotics collapses. Data from the International Federation of Robotics indicates a 30% surge in software-first automation deployments, validating this architectural pivot.

Why is Amazon Investing in Robotic Foundation Models?

The integration of spatial AI into enterprise infrastructure represents a structural evolution in cloud computing. Andy Jassy, Amazon’s chief executive, understands that the future of AWS relies on hosting the compute-heavy simulations required to train these robotic models. The physical world is infinitely more complex than language, generating exponentially more data per second of interaction.

Hosting the environments where Artificial General Intelligence (AGI) learns physics will require unprecedented server capacity. Amazon isn’t just buying better robots for its warehouses; it is actively securing its position as the default compute provider for the coming era of physical automation. The company wants AWS to be the central nervous system for every automated factory, delivery drone, and hospital robot on earth.

What are physical world AI models?

Physical world AI models, or spatial intelligence systems, are foundation algorithms trained on physics, robotics telemetry, and visual data rather than just text. They allow machines to understand three-dimensional space, predict material behaviour, and autonomously execute complex mechanical tasks in unpredictable real-world environments.

Simulating the physical world efficiently creates a massive competitive moat. When a physical robot drops a package, the failure data is uploaded, simulated millions of times in a virtual environment to find a solution, and then pushed back down to the entire fleet as an over-the-air update. The physical world becomes a continuous training loop.

The downstream consequences of successful physical AI models will aggressively rewrite the economics of logistics, manufacturing, and small-to-medium enterprise (SME) operations. Currently, automation is a luxury reserved for massive corporations capable of amortizing multi-million-dollar capital expenditures over decades. Embodied AI democratizes this capability by shifting the cost from hardware acquisition to cloud inference.

For policymakers, the implications are staggering. If general-purpose robots become affordable, reliable, and intelligent, the economic incentive to offshore manufacturing to low-wage jurisdictions evaporates. The OECD projects that advanced autonomous systems could reshore up to 15% of critical supply chain manufacturing back to Western markets by 2035. Factories will move closer to the consumer, drastically altering global trade deficits and shipping volumes.

Yet, this reshoring will not necessarily bring back working-class manufacturing jobs. The new factories will be highly autonomous, requiring a small workforce of machine supervisors and AI technicians rather than assembly line workers. Local economies will face the dual shock of increased industrial output and stagnant blue-collar employment.

Furthermore, this accelerates the convergence of the digital and physical security realms. When enterprise AI systems can physically interact with their environments, cybersecurity breaches manifest in the physical world. A hacked language model produces bad text; a hacked physical foundation model could instruct a factory of robotic arms to tear themselves apart.

The picture is more complicated than Silicon Valley pitch decks suggest. Skeptics point to Moravec’s paradox, an observation made by researcher Hans Moravec in the 1980s: high-level reasoning requires very little computation, but low-level sensorimotor skills demand immense computational resources. It is computationally easier to simulate a Wall Street trader than a one-year-old child learning to walk.

Dissenting experts argue that simulating reality with sufficient fidelity to train reliable robots is a computational pipe dream. Demis Hassabis and other prominent AI researchers have repeatedly noted the “sim-to-real gap”—the persistent failure of models trained in perfect virtual environments to handle the messy, unpredictable friction of the actual physical world. In a simulation, a sensor never gets covered in dust, and a gear never suffers from microscopic metal fatigue.

“You cannot perfectly compress the chaos of an unstructured physical environment into a matrix of weights and biases,” argues a recent critical engineering analysis from MIT. Relying on simulations creates edge cases that machines cannot handle gracefully. When a generative text model hallucinates, it invents a fake legal precedent. When a two-ton industrial robot hallucinates its physical coordinates, it destroys equipment or endangers human lives.

Still, the sheer velocity of capital being thrown at this problem suggests that tech giants believe the sim-to-real gap is a data problem, not an insurmountable law of physics. They are betting that massive parameter scaling, championed by figures like Jensen Huang at Nvidia, will eventually brute-force a solution to Moravec’s paradox.

The aggressive capital allocation toward physical foundation models represents the final frontier of the digital revolution. Amazon’s strategy reveals a profound understanding that the next trillion dollars in enterprise value will not be created by generating better emails, but by manipulating atoms. The tech industry has spent three decades building an immaculate, frictionless digital universe, only to realise that the real world—messy, heavy, and governed by gravity—is the only market that truly matters.

Ultimately, the race to simulate physical reality is less about building smarter machines and more about mastering the economic chokepoints of the twenty-first century. Those who control the foundation models of the physical world will dictate the cost of moving, building, and creating everything.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Best Economics Books to Read This Summer: Analysts’ Top Picks

Pakistan’s Current Account Surplus Hits $459 Million in May 2026

Amazon’s Physical AI Investment: Inside the $400M Tech Pivot

JLR Targets US Millionaires & Billionaires With Hybrid Cars

US Chip Export Controls on China: How Huawei & SMIC Defy Sanctions

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

HSBC Global Market Access for Mainland Investors: The 2026 Shift

Oil Prices Plunge: Strait of Hormuz Reopens Following Framework Deal

Grinding the Already Ground: Pakistan’s Inflation Crisis

The Architecture of Fiscal Strain: Global Debt and the Middle East Crisis

Import Price Shock: May’s 0.8% Rise Exposes Sticky Inflation Risk

Amex Buys Tripadvisor Restaurant Booking Unit in $700M Deal

SpaceX Valuation Overtakes Amazon: The $2.3T Shift

The SpaceX Factor: Hong Kong Stocks Face Liquidity Test From Mega IPO

China Overhauls the World’s Biggest Surveillance Network with Advanced AI

Kevin Warsh Takes the Fed’s Helm — and Walks Straight Into a Rate-Hike Storm

SpaceX, OpenAI & Anthropic IPOs: Wall Street’s $200B AI Test

SpaceX IPO: Inside the $2 Trillion Market Debut

How AI Is Forcing McKinsey and Its Peers to Rethink Pricing

KPMG Australia CEO Resigns After Whistleblower Claims Exposed Investigation Failures

PwC China Partner Payouts Cut Amid Evergrande Audit Fraud

Pakistan Budget FY 2026-27: Relief, Prospects, and the Tightrope Walk

The Guardrails Are Down: How Meta and Google’s AI Models Fold Under Pressure

Broadcom Market Value Loss: Revenue Forecast Disappoints

Stock Market Correction Risk Mounts as Bond Yields Defy the Bull Case

Benefitbay Raises $18M to Build the Plumbing for America’s ICHRA Shift

Nasdaq Tumbles 4% as Chip and Memory Stocks Sink: A $1.2 Trillion Wipeout

China Warns of ‘Severe’ Global Conditions as Economy Shows Weakness

-

Markets & Finance5 months ago

Markets & Finance5 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 months ago

Analysis4 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis4 months ago

Analysis4 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks5 months ago

Banks5 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment5 months ago

Investment5 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025