Analysis

inDrive Acquires KRRAVE: What Pakistan’s Grocery Delivery Shift Really Means

When a Siberian ride-hailing unicorn buys a Karachi grocery app, the story is never just about groceries.

On March 11, 2026, the Competition Commission of Pakistan formally authorized one of the more strategically revealing technology transactions in the country’s recent history: the acquisition of a majority shareholding in KRRAVE Technologies Pte. Ltd. by Suol Innovations Limited, the Cyprus-registered holding entity of the global inDrive Group. The price tag, confirmed at approximately $10 million, is modest by Silicon Valley standards. The implications for Pakistan’s digital economy are anything but.

This is, at its surface, a ride-hailing company buying an online grocery startup. Dig deeper and it becomes a case study in emerging-market super-app ambition, the evolving teeth of Pakistan’s competition watchdog, the geopolitics of foreign ownership in Pakistani tech, and a live experiment in whether Karachi — a megacity of 20 million people with notoriously fragmented last-mile logistics — can become ground zero for integrated mobility-commerce platforms.

The Deal Architecture: Cyprus, Singapore, and the Complexity of Modern Tech M&A

To understand this transaction properly, you need to follow the corporate geography. inDrive Holding Inc., headquartered in Mountain View, California, operates through a layered international structure. Its acquisition vehicle, Suol Innovations Limited, is incorporated in Cyprus. The target, KRRAVE Technologies Pte. Ltd., is a Singapore-registered holding entity whose Pakistani subsidiary, KRRAVE Technologies (Private) Limited, operates the Krave Mart platform in Karachi.

This multi-jurisdictional web is not unusual for global tech M&A — it reflects tax efficiency, investor preference for common-law jurisdictions, and the practical realities of capital flows into frontier markets. But it does place an added responsibility on Pakistani regulators to scrutinize not just the domestic competitive impact but the broader architecture of control and beneficial ownership.

The transaction was executed via call option agreements with multiple shareholders — a mechanism that grants the acquirer the right, but initially not the obligation, to purchase shares. That nuance matters: it suggests inDrive moved incrementally, watching Krave Mart’s performance before exercising full majority control, consistent with its broader venture-first, acquire-later playbook described to Bloomberg in December 2024.

The Regulator’s Uncomfortable Discovery: A Deal Done Before Permission Asked

Perhaps the most significant procedural detail in the CCP’s authorization notice is buried in its second paragraph: the transaction had already been completed before the Commission’s approval was sought. This triggered review under the CCP’s ex-post facto merger authorization framework — a mechanism that exists precisely because companies, particularly multinationals unfamiliar with Pakistan’s specific pre-merger notification thresholds, sometimes close deals first and seek clearance afterward.

The CCP did not penalize the parties in this instance, concluding instead that the merger posed no competitive threat. But it explicitly directed inDrive and KRRAVE to ensure strict compliance with merger notification requirements going forward. That directive is worth reading not as a rebuke but as a warning shot: as Pakistan’s digital economy matures, the CCP is signaling that regulatory patience with procedural shortcuts has limits.

This reflects a broader pattern in Pakistani competition law enforcement. The CCP, established under the Competition Act of 2010, has progressively tightened its merger review processes, particularly for technology transactions where market definition — always slippery in platform economics — requires more sophisticated analysis. The Commission’s identification of the “e-commerce B2C delivery platform for grocery” in Karachi as the relevant market demonstrates growing technical fluency. Five years ago, such granular market delineation would have been unlikely.

“The Commission observed that the acquirer operates primarily in mobility and logistics services, while the target operates in online grocery e-commerce — therefore, the transaction constitutes a conglomerate merger between businesses operating in distinct sectors.” — CCP Phase-I Assessment, March 2026

The conglomerate classification is analytically important. Unlike horizontal mergers — where two direct competitors combine — or vertical mergers, where a supplier acquires a customer — conglomerate mergers involve firms in distinct markets. Regulators worldwide have historically been more permissive about conglomerate deals, finding no immediate reduction in competition in any single market. But the economics literature, and recent enforcement in the EU and US, increasingly warns that conglomerate mergers by platform companies can create portfolio effects: the combined entity leverages dominance in one market (here, ride-hailing) to foreclose competitors in another (grocery delivery), through bundling, data integration, or preferential placement.

The CCP, for now, found no such risk. That determination may warrant revisiting as the inDrive-Krave Mart integration deepens.

inDrive’s Super-App Ambition: Why Grocery Is the Gateway

To appreciate why inDrive would pay $10 million for a Karachi grocery startup, you need to understand what the company is actually building. Founded in Yakutsk, Siberia in 2012 under the name inDriver, inDrive disrupted ride-hailing by doing the opposite of Uber: instead of algorithmic surge pricing, it lets passengers and drivers negotiate fares directly. That frugal, trust-based model proved magnetic in price-sensitive emerging markets. According to TechCrunch, the company now operates in 982 cities across 48 countries and is the world’s second-most downloaded ride-hailing app, having completed over 6.5 billion transactions globally.

But ride-hailing, even at scale, has a fundamental economics problem: low frequency. Most users summon a car a few times per week at most. Grocery delivery, by contrast, is a daily or near-daily behavior. It is the core insight behind every super-app thesis from Grab in Southeast Asia to WeChat in China: anchor users with high-frequency services, then monetize through lower-frequency, higher-margin verticals.

inDrive announced its $100 million venture capital arm in November 2023, specifically to fund startups aligned with this super-app vision. The Krave Mart investment, initially disclosed by Bloomberg in December 2024, was the most prominent deployment of that strategy to date in South Asia. Andries Smit, inDrive’s chief growth business officer, has been explicit about the logic: grocery delivery generates over 41 million orders globally for inDrive’s delivery segment annually, with more than 14 million in Q2 2025 alone, making it the fastest-scaling category in the company’s portfolio.

The planned integration is equally telling. Krave Mart is slated to be listed directly within the inDrive app, giving Karachi users the ability to order groceries through the same interface they use to book rides. That is the super-app flywheel in miniature: a single login, a shared customer profile, unified payment infrastructure, and — critically — a shared dataset on consumer behavior that neither company could generate alone.

Krave Mart: The Target’s Profile and Pakistan’s Quick-Commerce Landscape

Founded in 2021 by CEO Kassim Shroff, Krave Mart entered a market dominated by Delivery Hero’s Foodpanda and a constellation of informal delivery services. Its differentiation has been speed, product range — including hundreds of private-label items from bread to personal care — and a ruthlessly lean cash-burn model that allowed it to survive Pakistan’s brutal 2022–2023 funding winter, when venture capital dried up across South Asia as interest rates rose globally and inflation in Pakistan touched historic highs.

The $10 million from inDrive was transformative. Shroff confirmed to Profit Pakistan that Krave Mart tripled in size following the investment, improving delivery times and product assortment. The company currently serves urban households in Karachi, Pakistan’s largest city and commercial capital, through a quick-commerce model — meaning orders fulfilled in under 30 minutes from dark stores or micro-warehouses positioned close to demand clusters.

The broader market context is compelling. Pakistan’s B2C e-commerce market reached $14.11 billion in 2025, growing at a 22.2% CAGR between 2020 and 2024. It is projected to reach $20.41 billion by 2029. Online grocery, while still a fraction of that total, is among the fastest-growing sub-categories, driven by urban middle-class consumers, smartphone penetration exceeding 70% for mobile commerce traffic, and the rapid adoption of digital wallets like JazzCash and Easypaisa. Karachi, with its concentration of income and digital infrastructure, is the natural proving ground.

The Vertical Integration Question: Logistics as the Moat

The most strategically interesting dimension of this merger is what happens after the app integration. inDrive already operates courier delivery services in Pakistan through Sobo Tech (SMC-Private) Limited, its local subsidiary. Krave Mart operates its own last-mile logistics infrastructure in Karachi.

The combination creates the architecture for vertical integration across the mobility-delivery stack: a single company controlling the driver network, the logistics infrastructure, and the consumer-facing grocery marketplace. This is precisely the model that has made Grab a dominant force in Southeast Asia — and it is equally what makes competition regulators nervous when they look beyond the immediate market definition.

Consider the network effects at play. Drivers who ferry passengers also deliver groceries during downtime. That shared driver pool reduces idle time, increases earnings, and makes the combined platform more attractive to workers than any single-vertical operator. Consumer data gathered from grocery orders — what people buy, when, how often, at what price points — informs ride demand patterns and vice versa. Over time, a fully integrated inDrive-Krave Mart platform could offer personalization and pricing precision that standalone rivals simply cannot match, regardless of their product quality.

This is not a hypothetical concern. It is exactly the dynamic that led regulators in Singapore and the European Union to scrutinize Grab’s acquisitions more carefully after its initial super-app pivot. The CCP’s Phase-I clearance is a necessary but not sufficient determination. A Phase-II or follow-on review may eventually be warranted if the integrated platform begins to show market-foreclosing behavior.

Geopolitical Texture: Foreign Ownership, Digital Sovereignty, and the Emerging-Market Playbook

There is a broader geopolitical frame worth applying to this deal. Pakistan is a country where foreign investment in digital infrastructure is simultaneously courted — the government’s IT export targets, Special Technology Zones, and fintech liberalization signal genuine openness — and periodically scrutinized for sovereignty implications.

inDrive’s origins in Russia (the company relocated its headquarters to the US following the 2022 invasion of Ukraine) add a layer of complexity that Pakistani policymakers have not yet been required to articulate publicly but almost certainly discuss privately. The company’s VC arm, its super-app ambitions, and its accumulation of mobility and delivery data across 48 countries collectively constitute a data asset of considerable strategic value. That Pakistan’s competition law, unlike the EU’s Digital Markets Act or India’s emerging data localization frameworks, does not yet have robust provisions for data-related competitive concerns is a gap that will become increasingly relevant as this integration proceeds.

The more immediate sovereignty question is economic: as inDrive deepens its position in both ride-hailing and grocery delivery in Pakistan’s largest city, what leverage does that give a foreign-owned platform over Pakistani SME suppliers, local delivery workers, and ultimately Pakistani consumers? The answer depends entirely on how quickly domestic alternatives can scale, and on whether the CCP develops the analytical toolkit to monitor post-merger market dynamics rather than simply clearing transactions at the point of deal closure.

What This Means for Karachi Consumers — and Pakistan’s Startup Ecosystem

For the average Karachi household, the near-term picture is probably positive. Greater investment in Krave Mart means faster delivery times, wider product selection, better pricing from scale efficiencies, and the convenience of a single app for transport and groceries. Competition with Foodpanda should intensify, likely producing promotional pricing and improved service standards.

For Pakistan’s startup ecosystem, the signal is more complex. On one hand, inDrive’s $10 million bet validates the Pakistani grocery delivery market, potentially catalyzing further foreign investment interest. On the other, the acquisition path — a global unicorn acquiring a local startup as a distribution channel for its own platform ambitions — raises the perennial question of whether Pakistani tech companies are being built to be acquired rather than to become independent champions.

That question has no clean answer. Acquisition is a legitimate exit, provides liquidity for founders and early investors, and recycles capital into new ventures. But a digital economy that produces primarily acquisition targets rather than global-scale operators of its own is a structurally weaker one.

Key Takeaways

- The $10M deal is strategically asymmetric: For inDrive, it buys a distribution channel, a grocery dataset, and local logistics infrastructure in a market of 20 million potential users. For Krave Mart, it provides survival capital, global network effects, and a route to super-app integration.

- The CCP’s ex-post review is a procedural warning: The regulator’s directive for future compliance suggests it is watching this space carefully. Companies operating in Pakistan’s digital economy should treat pre-merger notification as non-negotiable.

- Conglomerate classification offers short-term protection, not permanent immunity: As the integration deepens, portfolio effects may warrant re-examination under Pakistani competition law.

- The super-app thesis faces execution risk: Every major platform that has attempted the super-app model outside of Asia — from Uber to Lyft to Rappi — has found that users resist forced bundling. inDrive’s success depends on genuine value creation in each vertical, not just cross-promotional mechanics.

- Pakistan’s regulatory framework needs to evolve: The CCP’s market definition capabilities are improving, but data-related competitive concerns and post-merger market monitoring remain underdeveloped relative to the speed of digital market consolidation.

Forward Scenarios for 2027

Scenario A — Successful Integration: Krave Mart becomes a top-three grocery delivery platform in Karachi within 18 months. The inDrive app’s grocery feature drives a 20–25% increase in monthly active users. inDrive expands Krave Mart to Lahore and Islamabad, replicating the model. Pakistan becomes inDrive’s showcase emerging-market super-app case study. Foreign VC interest in Pakistani grocery-tech reignites.

Scenario B — Execution Stumble: Integration complexity, regulatory friction, and competition from a resurgent Foodpanda (backed by Delivery Hero’s deeper pockets) slow momentum. Krave Mart remains a Karachi-only product. inDrive’s super-app ambition stalls in Pakistan, though the company retains its ride-hailing dominance. The acquisition is reclassified internally as a data and talent acquisition rather than a commercial scaling play.

Scenario C — Regulatory Tightening: The CCP, emboldened by the procedural precedent set in this review, introduces pre-merger notification thresholds that capture smaller digital transactions. Pakistan follows the broader global trend toward stricter scrutiny of platform conglomerate mergers. The cost of M&A in Pakistani tech rises, potentially cooling inbound acquisition interest but creating conditions for more domestically-owned scale players to develop.

The most likely outcome is a blend of Scenarios A and C: partial integration success combined with a more assertive regulatory posture. What is certain is that the inDrive-KRRAVE transaction is the opening move in a much longer game — one whose outcome will help determine whether Pakistan’s digital economy is built for its citizens or merely through them.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

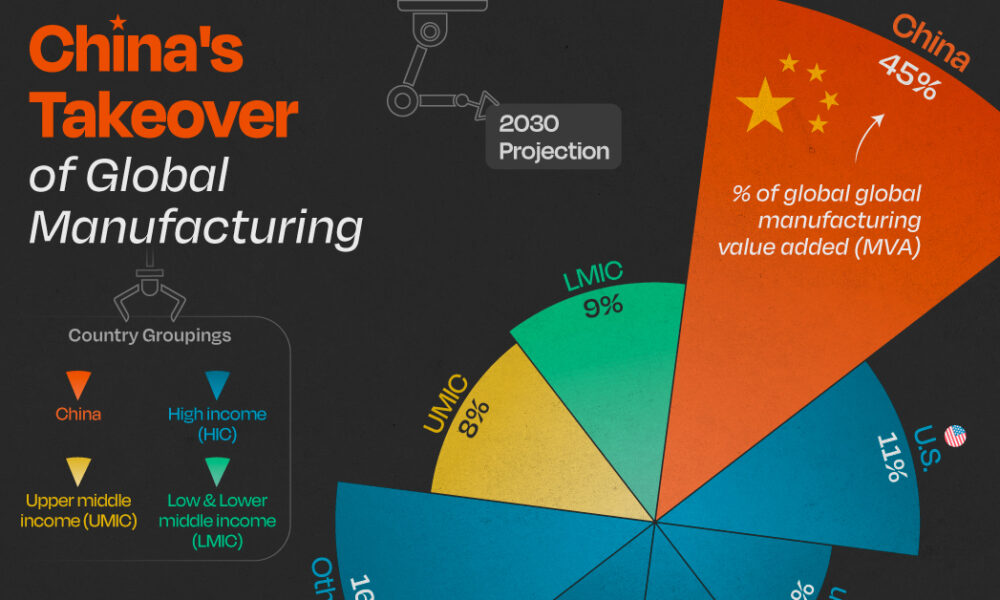

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025