Analysis

Foreign Central Banks Are Dumping US Treasuries in the Wake of the Iran War

The $82 billion exodus from America’s debt market signals more than wartime liquidity stress — it may mark the beginning of a structural reckoning for the dollar’s exorbitant privilege.

As oil prices pierced $110 a barrel and Iran’s blockade of the Strait of Hormuz choked the arteries of global energy trade, something quieter — and potentially more consequential — was unfolding in the marble-floored corridors of the New York Federal Reserve. Foreign central banks were liquidating American debt at the fastest pace in more than a decade.

Federal Reserve custody data shows that holdings of US Treasuries by foreign official institutions at the New York Fed have plunged by $82 billion since February 25, collapsing to $2.7 trillion — the lowest level since 2012. All-Weather Media The timing is not coincidental. The sell-off began almost precisely as the first missiles fell on Iranian soil, and it has accelerated with every week of conflict that grinds on. What began as a wartime liquidity scramble now carries the contours of a deeper structural shift — one that has economists in Frankfurt, Washington, and Beijing quietly updating their long-term models.

This is not merely a story about bond markets under pressure. It is a story about the foundations of American financial power.

The Mechanics of a Wartime Sell-Off

To understand why central banks are selling Treasuries into a crisis that would historically have driven buying, one must follow the energy channel rather than the geopolitical headline.

After Iran blocked the Strait of Hormuz, global oil prices soared, and oil-importing countries were hit hardest. Foreign exchange reserves shrank passively, combined with the need to intervene in currency markets, prompting central banks in many countries to accelerate the liquidation of US Treasuries. All-Weather Media

The logic is grimly circular. An oil-importing nation — say, India or Thailand — suddenly faces a surging import bill denominated entirely in dollars. Its currency weakens under the pressure of that trade shock. To defend the exchange rate and prevent a domestic inflationary spiral, the central bank must sell dollar assets to buy its own currency. The most liquid, deep dollar asset most central banks hold? US Treasuries. Brad Setser, senior fellow at the Council on Foreign Relations, pointed out that Turkey, India, Thailand, and other oil-importing countries are likely the main participants in this round of selling, because these countries must pay higher oil prices in dollars. All-Weather Media

Meghan Swiber, US rate strategist at Bank of America, confirmed the dynamic bluntly: “Foreign official institutions are selling US Treasuries.” All-Weather Media

The distinction that animates debate among market participants is whether this selling is passive — a mechanical consequence of reserve depletion — or active, reflecting a more deliberate choice to reduce dollar exposure. Stephen Jones, Chief Investment Officer at Aegon Asset Management, described the selling as countries “raising war funds,” saying, “They are drawing on emergency reserves.” All-Weather Media In practice, it is likely both, and the combination is what makes the current episode remarkable.

The Scale of It: A Data Table in Words

The numbers are stark and merit clear articulation.

Official data shows that since February 27 — the day before Iran was attacked — the Turkish central bank alone has sold $22 billion in foreign government bonds from its foreign reserves. All-Weather Media Turkey, battling a persistently weak lira and an energy import dependency that leaves it acutely exposed to oil shocks, has been the most aggressive seller. But it is hardly alone.

Independent data from the central banks of Thailand and India also show that both countries’ foreign exchange reserves have declined after the outbreak of the conflict. All-Weather Media Whether the drawdown came from Treasuries specifically or dollar deposits held elsewhere remains partially unclear, but the directional signal is unambiguous: oil importers across Asia and the emerging world are under intense balance-of-payments stress.

At the other end of the oil equation, Gulf exporters face a different calculus. Saudi Arabia held $149.5 billion in US Treasuries as of December 2025. The Gulf states collectively maintain over $2 trillion in dollar-denominated assets. Saudi Arabia, the UAE, Kuwait, Qatar, and Bahrain all peg their currencies to the US dollar, requiring them to keep vast amounts of dollars to support that peg and, in doing so, help sustain Treasury demand. Middle East Eye Their behavior in the weeks ahead — whether they hold, or quietly reduce — will be among the most consequential signals to watch in global bond markets.

Yields Surge: America’s Borrowing Costs Bite Back

The sell-off is not happening in a vacuum. It is coinciding with — and amplifying — a broader repricing of US government debt that has unsettled investors and policymakers alike.

The 10-year US Treasury yield has risen from around 3.9% to a peak of 4.4%, while the 2-year yield climbed from 3.35% to above 4% — both hitting eight-month highs. Euronews That may not sound catastrophic in isolation, but it arrives against a backdrop of acute fiscal vulnerability. The US national debt crossed $39 trillion on March 18, 2026 — a milestone reached just weeks into the war in Iran — with interest costs projected to become the fastest-growing line item in the federal budget, after credit downgrades from all three major ratings agencies. Fortune

RSM Chief Economist Joseph Brusuelas captured the market’s collective anxiety: “The US Treasury bond market has finally responded to the Mideast war, giving its assessment of the energy shock’s severity and the war’s effect on US fiscal imbalance and inflation.” The MOVE index, which tracks volatility in the Treasury market, has spiked to levels consistent with price instability and policy dysfunction. Fortune

BCA Research’s Chief Fixed Income Strategist Robert Timper has characterized the pattern as “aggressive bear flattening of yield curves,” reflecting a hawkish monetary policy repricing in response to inflation fears stemming from the Iran war. Euronews On a conventional reading, this is stagflationary: energy-driven inflation pushes short-term rates higher even as growth expectations deteriorate. The Fed, caught between an oil shock and a slowing labor market, finds itself precisely where it least wants to be — with no clean policy option.

Central banks are concerned that another inflation shock, even if caused by a temporary spike in oil, might convince consumers and businesses that inflation is going to be high for a long time. Marketplace The confidence channel, in other words, may matter as much as the oil price level itself.

The Petrodollar’s Perfect Storm

Here is where the analysis shifts from cyclical to structural — and where the Iran conflict becomes geopolitically transformative rather than merely disruptive.

Deutsche Bank FX strategist Mallika Sachdeva has argued that the conflict could be remembered as a key catalyst for “erosion in petrodollar dominance, and the beginnings of the petroyuan.” CNBC That is a remarkable sentence to see in a research note from a major Western bank, and it demands unpacking.

The petrodollar system — born from a secret 1974 agreement between the US and Saudi Arabia — is elegantly simple in its design. Riyadh agreed to price its oil exports in dollars and invest its petroleum windfalls into US Treasuries; in return, Washington provided military protection and security guarantees for Gulf infrastructure. Other OPEC members followed, locking the dollar in as the indispensable currency of the modern world. Fortune That recycling loop allowed Washington to borrow cheaply, run persistent deficits, and still command the world’s reserve currency — what the French famously called America’s “exorbitant privilege.”

The Iran war has directly challenged every pillar of that arrangement. US military assets and bases in the Gulf have come under attack. Oil infrastructure in the Gulf has been hit. And the US ability to provide maritime security to ensure the global flow of oil has been challenged by the closure of Hormuz. The US security umbrella has been fundamentally tested. The Canary

Deutsche Bank’s Sachdeva wrote that the conflict “may expose further fault lines, by challenging the US security umbrella for Gulf infrastructure and maritime security for global trade in oil,” adding that “damage to Gulf economies could encourage an unwind in their foreign asset savings held largely in dollars.” Middle East Eye

The most concrete manifestation of this risk is already visible. Reports from multiple outlets confirm that Iran has been negotiating tanker passage through the Strait of Hormuz only when transactions are settled in yuan — a policy Deutsche Bank flags as a potential watershed moment. Bitcoin News At least 11.7 million barrels have moved through Chinese-linked tankers since late February, with many vessels going dark to avoid tracking. Discussions with at least eight non-Middle Eastern countries on yuan-based oil trade for safe transit have also been reported. Bitcoin News

This is not yet the petroyuan. But it is its audition.

Dedollarization: Accelerant, Not Origin

It would be analytically sloppy to present the Iran war as the singular cause of dedollarization. The trend predates the current conflict by years — accelerated by US sanctions on Russia in 2022, the rise of BRICS payment alternatives, and China’s persistent push to internationalize the renminbi through mechanisms like the mBridge central bank digital currency project.

Even before the Iran war, hypotheses about the petrodollar’s erosion had been building. US sanctions on Russian and Iranian oil had already created illicit trade routes settled in yuan and roubles. Saudi Arabia had joined mBridge, taking a seat in China’s alternative payment infrastructure. Fortune

What the Iran war has done is compress the timeline. Structural shifts that might have taken a decade now have a geopolitical accelerant behind them. And critically, this wave of selling reflects a deeper trend: global reserve management institutions have been diversifying dollar asset allocations for years, and the status of US Treasuries as the primary global reserve asset is being increasingly eroded. All-Weather Media

That said, the dollar doomsayers deserve scrutiny alongside the dollar optimists. The offshore dollar credit market stood at $2.5 trillion in 2000 and has hit $14.2 trillion more recently — evidence of structural resilience that should temper apocalyptic narratives. Fortune The dollar index is on track to gain around 3% in March, with energy-driven stagflation risks supporting the greenback in the near term, according to OCBC strategists. CNBC Crises, paradoxically, often strengthen the dollar even when they degrade its long-term foundations.

The distinction — between short-term safe-haven demand for the currency and long-term diversification away from the asset — is exactly what makes this moment so analytically treacherous. Central banks may be buying dollars even as they sell Treasuries. As Wells Fargo’s Brendan McKenna noted, investors who want dollar safety have plenty of options beyond Treasuries — money market funds, savings accounts, corporate bonds — all dollar-denominated, none of which require holding sovereign debt. Marketplace

What Comes Next: The Fed’s Dilemma and the Gold Trade

The Federal Reserve finds itself boxed in on multiple fronts. Prediction markets now price only a 23.5% probability of a Fed rate hike in 2026, and only 37% probability of zero cuts — meaning the majority of investors still expect the Fed to remain relatively more dovish compared to major central banks like the ECB, which markets now give an 85% probability of hiking. Benzinga

That divergence matters for Treasury markets. If the Fed stays patient while inflation creeps higher, the risk premium on longer-dated Treasuries will widen further. If it hikes preemptively, it risks tipping a slowing economy into recession — and potentially triggering exactly the kind of demand destruction that would crash oil prices and resolve the inflationary shock anyway. Neither path is comfortable.

Meanwhile, the private investment alternatives are multiplying. Gold — the original reserve asset, abandoned by Bretton Woods but never fully forgotten — has surged as central banks globally have accelerated purchases. For emerging market central banks now questioning the sanctity of US sovereign debt, gold offers something Treasuries currently cannot: an asset without geopolitical counterparty risk.

The deeper implication, the one that keeps Treasury officials awake, is about the fiscal term premium — the extra yield investors demand to hold long-duration US debt given fiscal and policy uncertainty. Brusuelas warned that if uncertainty continues, it could trigger broader funding stress in debt markets already under pressure from concerns about private credit — with total investment-grade supply coming to market in 2026 estimated at around $14 trillion. Fortune The competition for global capital has never been fiercer, and the US no longer bids from a position of unquestioned supremacy.

The Long View: A Privilege Under Audit

The $82 billion drop in foreign official Treasury holdings is, in isolation, manageable. The US Treasury market is the deepest and most liquid in the world; $82 billion is noise in a $28 trillion market. What is not manageable — if it continues — is the structural message embedded in the data.

For fifty years, the petrodollar system functioned as a self-reinforcing cycle: oil exported in dollars, dollars recycled into Treasuries, cheap US borrowing reinforcing dollar dominance, dollar dominance reinforcing oil pricing. The Iran war has not broken that cycle. But it has introduced friction into every link of the chain simultaneously — energy shock, currency stress, reserve drawdown, yield surge, and a nascent yuan-for-oil experiment at the world’s most critical chokepoint.

Policymakers in Washington should be paying close attention not just to where Treasury yields are today, but to where foreign central bank buying will be in six, twelve, and twenty-four months. The exorbitant privilege was never guaranteed. It was maintained by confidence — in American institutions, American security commitments, and American fiscal restraint. The Iran war is testing all three at once.

For now, the dollar holds. The question is whether it holds the same thing it did before the war began.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

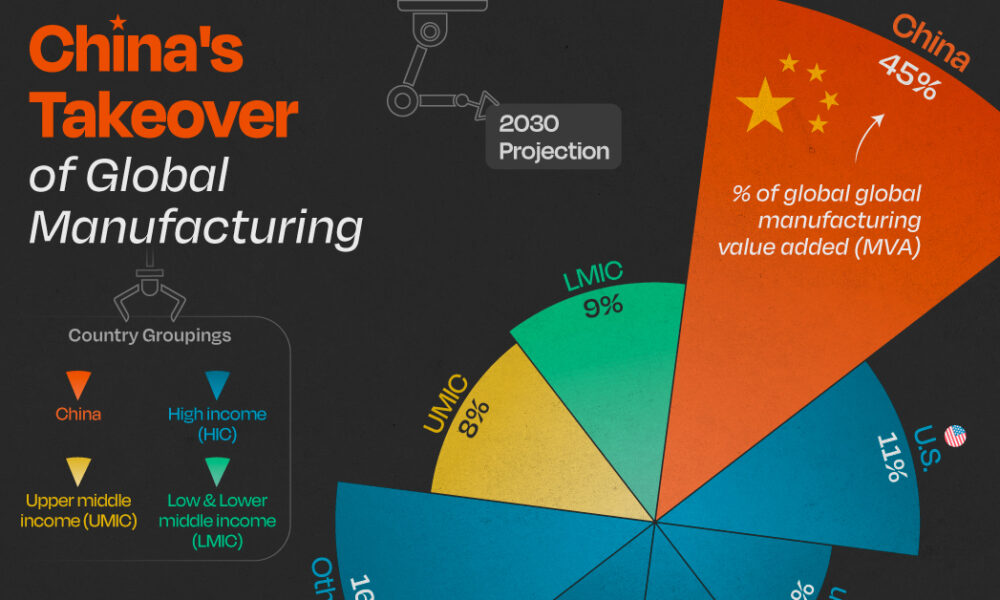

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025