Tariffs

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

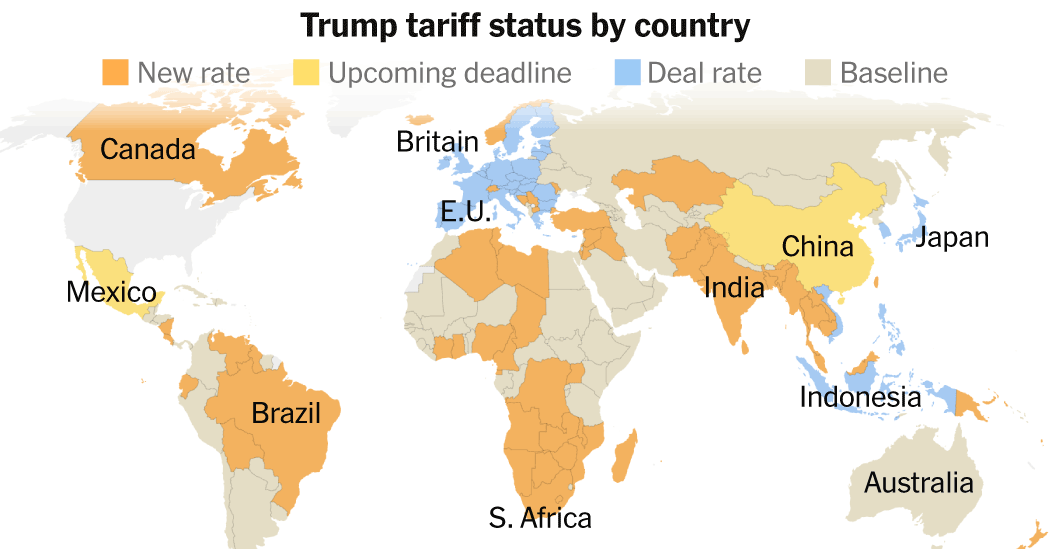

The US administration has launched an investigation into 60 countries — including the European Union — to determine whether they are permitting imports of goods produced with forced labor, setting the stage for new tariffs ranging from 10% to 12.5% and reopening a trade fight many assumed was settled, according to Deloitte’s Weekly Global Economic Update.

From Historic Tariffs to Legal Setbacks to a New Workaround

The administration spent much of 2025 attempting to construct a new global trading regime built around historically high tariffs and the constant threat of additional duties. That effort hit turbulence in 2026 when court decisions challenged the legality of certain tariff actions. Rather than retreat, the administration has pivoted to a forced-labor investigation as an alternative legal basis for imposing new duties — a maneuver that effectively route around the same legal constraints that felled its earlier tariff architecture, according to Deloitte’s tracking of the policy shift.

TD Economics notes the new Section 301 tariffs, covering the 60 countries under investigation, are set to take effect in late July 2026, replacing temporary Section 122 tariffs that had themselves replaced earlier IEEPA-based tariffs back in February — a rapid succession of legal justifications that underscores how central tariff policy remains to the administration’s trade strategy despite repeated judicial pushback, according to TD’s Canadian Quarterly Economic Forecast.

The EU Is Back on the List

Perhaps the most consequential detail is the inclusion of the European Union among the 60 countries under investigation, despite the US and EU having reached a trade agreement the previous year that was subsequently ratified by the European Parliament. The renewed scrutiny threatens to reopen a trade relationship both sides had treated as stabilized, introducing fresh uncertainty for European exporters already navigating elevated energy costs tied to the Middle East conflict.

The Broader Tariff Landscape Businesses Are Now Operating In

TD Economics estimates that despite the legal churn, the overall effective US tariff rate is likely to hold steady around 10% once the new Section 301 measures take effect — meaning that for most businesses, “peak uncertainty” over the shape of US trade policy is now behind them even if the specific legal mechanism keeps changing. Canadian exports, by comparison, face a lower roughly 6% average effective tariff rate given extensive CUSMA-compliance exemptions, according to RBC’s tariff impact analysis.

Knock-On Effects Across Asia and North America

The tariff churn has already reshaped global trade flows. RBC Economics notes that global trade patterns have reoriented dramatically to route around higher-tariff regions such as China, even as global trade volumes overall continued to rise through 2025 and the US trade deficit widened slightly despite the tariff push, according to RBC’s year-one tariff retrospective. For Asian exporters, exposure to the US market varies widely — from around 30% of exports for Vietnam to roughly 15% for China — meaning the forced-labor investigation’s ultimate impact will fall unevenly depending on each economy’s US trade concentration.

What Comes Next

With the investigation’s findings expected to determine tariff levels within the 10%-12.5% range for affected countries, businesses across the EU, and potentially exporters in Asia and Latin America caught up in the 60-country review, face a fresh compliance burden: documenting labor-sourcing practices deep into their supply chains to avoid punitive duties, even in sectors with no direct history of forced-labor allegations.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Having lost its most powerful tariff tool in the Supreme Court, the Trump administration has found a new one — and it comes with a moral argument attached.

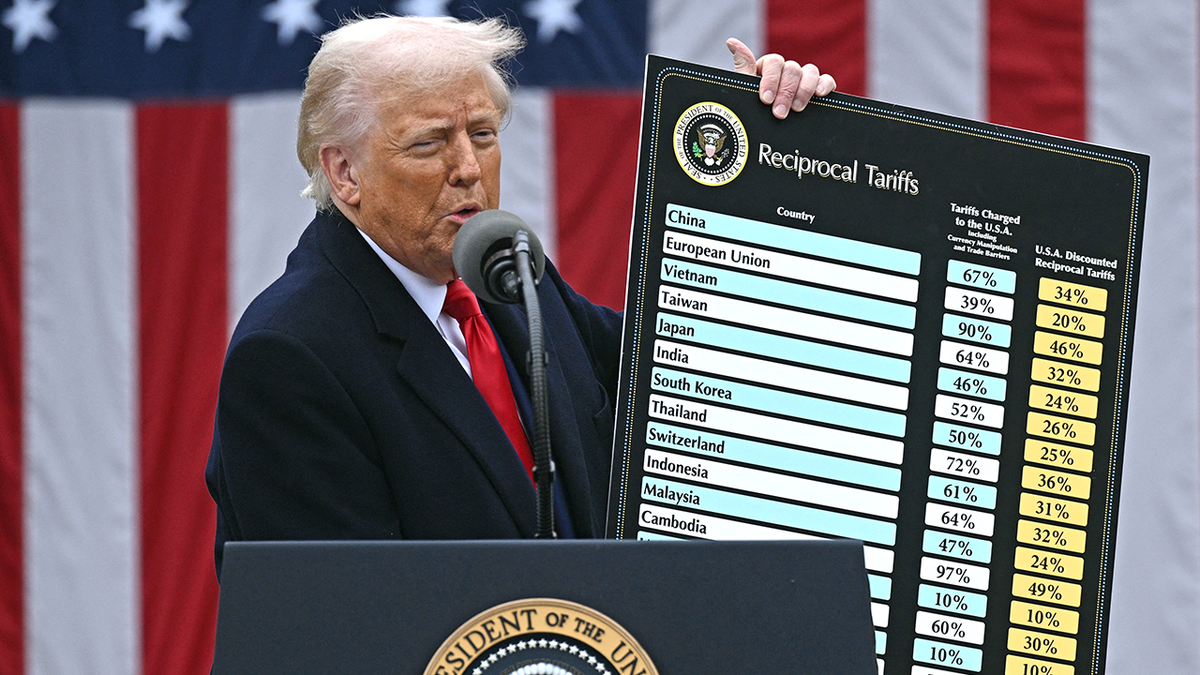

On June 2, 2026, the Office of the United States Trade Representative concluded 60 simultaneous Section 301 investigations, finding that each of the targeted economies had failed to impose or effectively enforce a prohibition on the importation of goods produced with forced labour. The proposed remedy: additional tariffs of 10% to 12.5% on all imports from those economies, covering 99.4% of total US imports by origin. The scope is unprecedented. It sweeps in China, the European Union, Japan, India, Vietnam, Australia, South Korea, and 52 other trading partners in a single action.

The Legal Architecture Post-Supreme Court

The context matters. In February 2026, the US Supreme Court struck down most of President Trump’s “Liberation Day” emergency tariffs, ruling that they exceeded the executive’s authority under the International Emergency Economic Powers Act (IEEPA). That decision dismantled the headline tariff architecture the administration had built over 2025. Rather than abandon the strategy, the Trump administration pivoted to legal frameworks with stronger statutory grounding. Section 301 of the Trade Act of 1974 authorises the president to impose levies to counter foreign trade practices that are “unreasonable or discriminatory and burden or restrict U.S. commerce” — a standard that the USTR has now applied to forced labour enforcement failures.

The investigations were formally initiated on March 12, 2026, with public hearings drawing testimony from nearly 60 witnesses and 500 written comments over April and May. The USTR’s findings drew a direct causal link between inadequate forced labour enforcement and competitive harm to US companies and workers.

The Rate Architecture

The proposed tariff structure creates two tiers. Economies that have adopted full or partial forced labour import prohibitions — notably Canada, Mexico, and a handful of others — would face 10% additional duties. The remaining 45 economies, including China, India, Japan, Vietnam, Australia, and New Zealand, would face 12.5% additional duties. A separate textile mechanism would allow a capped volume of apparel and textile imports from certain economies at a reduced rate. Electronics and AI-related products are widely expected to carry significant exemptions, according to the Economist Intelligence Unit.

The public comment period closes July 6, 2026, with hearings beginning July 7. The duties are not yet in effect — but for companies sourcing from any of the 60 targeted economies, the window to map exposure and file comments is rapidly closing.

Trading Partners Push Back

Responses from affected governments were swift and uniformly dismissive of the USTR’s reasoning. Beijing‘s commerce ministry spokesperson stated flatly that “there is no so-called forced labor in China,” and that Washington and Beijing should “meet each other halfway.” China’s foreign ministry called the accusations politically motivated.

The European Union is in a particularly complex position. Brussels signed a broad bilateral trade agreement with Washington in 2025, which the European Parliament ratified. The proposed new tariffs — which the EU called “unjustified” — would come on top of the existing 15% tariff framework from that deal. The USTR’s own report acknowledged that the EU’s anti-forced-labour regulation only entered into force in December 2027 and lacks certain enforcement elements — giving the administration its statutory foothold. The chair of the European Parliament’s trade committee described the determination as “utterly absurd” given the 2024 EU forced labour import ban law.

France‘s government questioned whether the investigation reflected genuine concerns, with officials suggesting a tariff measure was “sought first, and only then is a suitable legal justification found.”

The Supply Chain Reality for Multinationals

For global supply chain managers, the practical implications are immediate regardless of the final duty levels. The Clark Hill law firm’s trade practice advised clients to map exposure against the 60 targeted economies by HTS code, model the 10% and 12.5% rate scenarios, and test exclusion eligibility before assuming coverage — noting that even partial exposure in electronics supply chains could run to billions in added costs at scale.

Nick Marro of the Economist Intelligence Unit told CNBC that he expects the Trump administration to “unleash further investigations and tariff announcements in preparation for renewed rounds of trade talks,” characterising the Section 301 action as part of a broader pattern of building leverage ahead of bilateral negotiations. The July 24 expiration of the separate 10% baseline tariff imposed under Section 122 adds another inflection point to the calendar.

For the global trading system, the implication is clear: the US high-tariff era is not over; it has simply found a new statutory vehicle.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Trump’s 2026 tariffs represent the largest US tax increase as a share of GDP since 1993, costing households $1,500 on average. Here’s how the trade war is reshaping global supply chains, prices, and growth.

The tariff regime assembled by the Trump administration since 2025 now constitutes the largest U.S. tax increase as a share of GDP since 1993—a fact that took more than a year to fully register in household budgets, but whose full weight is being felt with increasing force in the middle months of 2026.

The average American household will pay an estimated $1,500 more in 2026 as a direct consequence of elevated import duties, according to Tax Foundation analysis—up from roughly $1,000 in 2025. The costs are not distributed evenly. Lower-income households, which spend a higher proportion of their income on goods (particularly apparel, electronics, and food), absorb a larger relative burden.

A Legal Architecture Under Pressure

The tariff program has faced serious legal challenges. On February 20, 2026, the Supreme Court ruled that the President cannot use the International Economic Emergency Powers Act—IEEPA—to impose tariffs. The decision stripped the administration of the legal vehicle it had used to impose much of its most aggressive tariff architecture.

But the administration adapted rather than retreated. In the same week as the ruling, President Trump signed an executive order imposing a 10% tariff on all countries under Section 122—a different statutory authority tied to balance-of-payments deficits—covering approximately $1.2 trillion worth of imports. The administration also initiated multiple Section 301 investigations into 60 countries on March 11, examining whether those nations allow imports of products made by forced labor. The list includes the European Union, positioning both parties for a potential renewal of the transatlantic trade conflict that a deal in 2025 had temporarily paused.

On pharmaceuticals, the administration signaled that tariffs on imported drugs could rise toward 200% by mid- to late-2026—a figure that would represent an extraordinary disruption to global pharmaceutical supply chains, though J.P. Morgan analysts noted that inventory builds and domestic manufacturing announcements by large biopharma companies should limit near-term exposure for major producers.

The China Equilibrium

U.S.-China trade relations have settled into an uneasy equilibrium. Following the June 11, 2025 trade deal announcement that left in place 20% fentanyl-related tariffs and 10% reciprocal tariffs for a combined 30%, and a subsequent series of extensions and escalations that included a 100% tariff imposed in November 2025, the two countries entered 2026 with a tense but functional trading relationship.

Chinese exporters responded to U.S. tariffs not by collapsing but by redirecting. China’s semiconductor exports surged 110% year-over-year in May 2026. That strength reflects both genuine demand from AI-related industries globally and a deliberate Chinese strategy of deepening trade relationships with Southeast Asia, the Gulf, and Europe to reduce dependence on U.S. market access.

The economic cost of U.S. tariffs on China, per J.P. Morgan Global Research, was to reduce Chinese GDP growth by roughly 0.6 percentage points through the combined effect of export drag and weaker domestic investment. But China’s export machine proved more resilient than many forecasters expected, partly because third countries absorbed Chinese goods that could not reach the U.S. market directly.

Inflation Is the Tariff’s Most Persistent Legacy

The clearest economic consequence of the tariff regime is its contribution to inflation. Businesses faced with import tariffs have three choices: absorb the cost and compress margins; pass it to consumers in higher prices; or reshore production in the U.S. at significantly higher labor costs. All three options carry economic costs, and in practice most companies have pursued a combination.

Atlanta Fed President Raphael Bostic noted in research published late 2025 that U.S. firms expected tariffs to account for 40% of their total unit cost growth in 2025 and 2026. That contribution to inflation is structural rather than transitory—unlike oil prices, which can fall as conflict dynamics ease, tariff-driven cost increases remain embedded in supply chain economics until the tariffs themselves are removed or the supply chains are restructured.

The Council on Foreign Relations analysis of tariff-Treasury interactions found that tariff uncertainty—independent of the tariffs themselves—was raising the risk premium in U.S. Treasury markets: “An eventual court ruling against the administration’s reliance on IEEPA could significantly alter the implementation path,” J.P. Morgan’s Nora Szentivanyi noted, adding that even without IEEPA, alternative statutory pathways would keep elevated tariffs in place.

Where the Trade War Goes Next

The Section 301 investigations launched in March against 60 countries—including EU members—signal that the tariff posture is not an emergency measure being wound down but a permanent feature of U.S. trade policy. Many market participants expect that Treasury will need to increase issuance of longer-term bonds starting in Q4 2026 partly to ensure liquidity along the yield curve—with tariff revenue being one of the contested variables in fiscal planning.

For U.S. businesses, the clearest strategic message from the tariff regime’s staying power is that supply chain localization is no longer a nice-to-have contingency plan. It is a competitive necessity in an environment where trade routes can change with a single executive order and where the legal found

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The effective US tariff rate has risen from 2.1% to 11.7% under Trump. Here’s how the tariff regime is reshaping global supply chains, consumer prices, and the trade war outlook for 2026.

In 2025, the Trump administration implemented the most sweeping overhaul of US trade policy since the Smoot-Hawley Tariff Act of 1930. Through executive action — primarily invoking emergency economic powers and national security statutes — the administration raised the effective US tariff rate from 2.1% to an estimated 11.7% as of January 2026.

Eighteen months later, the consequences of that decision are visible across every dimension of the US and global economy: in consumer prices, in supply chain restructuring, in the Federal Reserve’s inflation calculations, and in the diplomatic relationships that underpin global trade.

The tariff regime is not an abstract policy debate. It is a tax — and like all taxes, it has winners, losers, and unintended consequences that took time to manifest and will take years more to fully resolve.

The Scale of the Tariff Shock

To appreciate the magnitude of the 2025 tariff escalation, the baseline comparison matters. Before the first Trump administration’s tariff actions in 2018, the average US effective tariff rate on imports was approximately 1.5%. The first Trump term raised it to approximately 3%. The second term’s actions pushed it to 11.7% — a level not seen in the US in decades.

The mechanics varied by category:

- China-specific tariffs remained elevated and in many cases were increased further, targeting electronics, machinery, textiles, and consumer goods

- A 10% global baseline tariff on all imports was implemented through executive action, though this was challenged in the courts

- Sector-specific tariffs targeted steel, aluminium, solar panels, electric vehicles, and semiconductors from multiple origin countries

The Supreme Court rejected several of the most aggressive tariff actions in 2025, ruling that some executive tariff applications exceeded statutory authority. This opened the door for importers to seek refunds on improperly collected duties — a complex refund process that the administration has contested aggressively. The Supreme Court’s intervention did not eliminate the tariff regime; it trimmed its most legally exposed elements while leaving the core architecture intact.

A 10% global baseline tariff remains in effect as of June 2026.

Who Is Actually Paying the Tariffs

The most persistent economic misconception about tariffs is that foreign exporters pay them. They do not. Tariffs are paid by importing firms — US companies that purchase foreign goods — and the economic burden is distributed between exporters, importers, and consumers depending on market conditions.

The best available evidence suggests that more than 50% of Trump tariff costs are now being passed through to US consumers — a pass-through rate that has been somewhat slower than the near-100% observed under the first-term tariffs, but is accelerating as inventory buffers built before tariff implementation are depleted.

For the median US household, the effective tariff tax represents a meaningful annual cost increase — concentrated in electronics, clothing, furniture, appliances, and consumer goods where import shares are high and domestic substitutes are limited or more expensive.

The pass-through to prices has been one of the primary contributors to US inflation remaining above 3% — and is a key reason why the Federal Reserve’s task of returning inflation to 2% is more difficult than a simple demand-management problem would suggest.

Supply Chain Restructuring: Three Years In

The tariff regime has succeeded in its stated objective of prompting supply chain diversification away from China. But “diversification” has not meant “reshoring.” The dominant pattern has been near-shoring — shifting production to third countries that are not subject to the highest US tariff rates.

Vietnam, Mexico, India, Bangladesh, and Indonesia have been the primary beneficiaries of China-targeted tariff diversion. US imports from these countries have increased substantially since 2022, with Vietnam in particular becoming a major hub for electronics assembly, textile production, and component manufacturing previously concentrated in China.

The irony is that much of this production still relies on Chinese inputs — materials, components, and intermediate goods that flow through third-country manufacturing before reaching the US market. The tariff regime has in many cases added a processing step to the supply chain without fundamentally reducing Chinese industrial participation in global production networks.

Mexico, benefiting from the US-Mexico-Canada Agreement, has seen a surge of near-shoring investment from both US and Chinese firms seeking US market access through a tariff-advantaged production base. This has created genuine economic activity in Mexico while raising questions about whether the tariff regime is achieving its intended effect on Chinese production capacity.

China’s Response: Export Diversification and the Trade Surplus

China’s trade surplus — the gap between what it exports and what it imports — has actually expanded in 2026, despite (or perhaps because of) the US tariff regime. Chinese exporters have aggressively diversified their market base, deepening trade relationships with:

- Southeast Asia (ASEAN markets, particularly Vietnam, Indonesia, Thailand)

- Latin America (Brazil, Mexico, Argentina)

- Africa (through the Belt and Road infrastructure network)

- Middle East (Gulf states diversifying from Western supply chains)

- Russia (bilateral trade dramatically expanded since Western sanctions)

This market diversification has reduced China’s vulnerability to US tariff pressure while maintaining the export-led growth model. The result is a structural change in global trade flows — with Chinese goods increasingly reaching the world through routes that bypass direct US market entry.

The EU has responded separately. European tariffs on Chinese electric vehicles, implemented in 2025, represent the most significant trade action in the China-Europe relationship in years. But China’s response has been measured — targeting European luxury goods with retaliatory measures while continuing to invest in European market access through investment in non-tariffed segments.

The Inflation Arithmetic

The tariff-inflation relationship is one of the most debated and most significant economic linkages in 2026.

The direct mechanism is straightforward: tariffs raise the cost of imported inputs, which businesses pass through to consumer prices. The indirect mechanism is subtler: tariffs reduce import competition, allowing domestic producers to raise prices without competitive constraint. Both channels are operational in the current US economy.

Stanford’s Institute for Economic Policy Research estimated that tariff pass-through to consumers now exceeds 50%, with the full pass-through taking 12–18 months from tariff implementation. Given the tariff escalation of 2025, the full inflationary impact is still working its way through the system as of mid-2026.

This creates a structural floor on US inflation that makes the Federal Reserve’s 2% target difficult to achieve without either reversing the tariff regime (a political impossibility under the current administration) or engineering a significant recession that reduces demand enough to offset the supply-side price pressure.

The Fed cannot solve a tariff-driven inflation problem with interest rate tools alone. This is the core of the policy trap that Kevin Warsh inherited upon taking the Fed chair position.

The WTO and the Multilateral Trade Framework

The US tariff regime has created significant strain on the World Trade Organization framework. Multiple WTO dispute settlement proceedings have been filed by trading partners including the EU, China, Japan, South Korea, and Canada. The US has contested these proceedings and has maintained its practice of blocking WTO Appellate Body appointments — a practice that began in the first Trump term and has effectively disabled the WTO’s binding dispute resolution mechanism.

The practical consequence: the global trading system has fragmented into a series of bilateral and regional arrangements, with the WTO’s rules-based framework increasingly supplemented or supplanted by power-based bilateral negotiations.

For businesses operating across borders, this fragmentation creates compliance complexity, supply chain uncertainty, and strategic risk that has no precedent in the post-war era of multilateral trade liberalisation.

What Comes Next: The Second Half of 2026

Several tariff-related developments are likely to shape the trade environment in the second half of 2026:

Supreme Court refund proceedings — the ongoing dispute over duty refunds for imports collected under executive actions that courts ruled as exceeding statutory authority. Resolution will affect importers’ balance sheets and the effective tariff rate going forward.

EU-US tariff negotiations — the Biden-era tariff truce framework has partially frayed under the Trump administration’s more aggressive posture. EU-US talks on steel, aluminium, and digital services remain ongoing and unresolved.

China-US trade dynamics — with China’s trade surplus expanding and US domestic pressure for further action on Chinese imports growing, additional tariff escalation cannot be ruled out. The November 2026 midterm elections create political incentives for trade action.

WTO dispute outcomes — while the Appellate Body remains disabled, preliminary panel rulings could create diplomatic pressure points with major trading partners.

The Bottom Line

The Trump tariff regime has fundamentally altered the US and global trade landscape. The effective tariff rate of 11.7% represents the most significant barrier the US has erected to international commerce in generations, with consequences that run from consumer prices and Federal Reserve policy to supply chain geography and WTO institutional legitimacy.

The tariff regime is not going away. Political economy — domestic manufacturing interests, national security framing, and electoral incentives — makes tariff rollback extremely unlikely under the current administration.

The relevant questions for investors and businesses are not whether tariffs will be reversed, but how supply chains adapt, how much of the inflationary pass-through remains ahead, and whether the trade war escalates or stabilises in the second half of 2026.

FAQ

Q: What is the current US tariff rate in 2026?

A: The US effective tariff rate rose from approximately 2.1% before the Trump administration to an estimated 11.7% as of January 2026. A 10% global baseline tariff on all imports remains in effect after the Supreme Court struck down some of the most aggressive executive tariff actions.

Q: How do tariffs affect inflation in 2026?

A: More than 50% of tariff costs are now being passed through to US consumers, according to Stanford SIEPR research. This represents a structural supply-side inflation pressure that the Federal Reserve cannot resolve through interest rate policy alone.

Q: What happened to US-China trade in 2026?

A: US-China direct trade has declined under tariff pressure, but China has diversified its export markets significantly — increasing flows to Southeast Asia, Latin America, Africa, and the Middle East. China’s overall trade surplus has actually expanded in 2026.

Q: How are tariffs affecting US consumers in 2026?

A: US consumers are facing higher prices on electronics, clothing, appliances, and consumer goods as tariff costs are passed through the supply chain. This contributes to the inflation reading of 4.2% in May 2026 and reduces household purchasing power.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

Germany Rail Network Upgrade: Inside the €100bn Rescue Plan

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025