Analysis

The Ferrari Luce Is Finally Here — and It’s Already Dividing the Room

Ferrari’s first electric car was unveiled in Rome on 25 May 2026. It has 1,035 horsepower, a Jony Ive interior, and a silhouette that looks nothing like any Ferrari that came before it. That was entirely the point.

Rome was chosen with deliberate symbolism. The reveal took place on 25 May 2026, exactly 79 years after Ferrari won its first race victory. The company had booked the Città dello Sport — Santiago Calatrava’s vast, sail-shaped sports complex — for an event sealed under near-total secrecy. Behind the curtain sat an object that had been five years in the making: a five-seat, five-door electric sedan conceived in Maranello and refined in San Francisco, wearing a form that the company’s own global head of product marketing freely admitted would be divisive. Wallpaper*

“The reaction we’re going to have among our customer base,” Emanuele Carando told reporters that day, “is going to be very much mixed. People will love it, and people will hate it.” InsideEVs

That may be the most honest thing a car brand has said at a launch event in years.

A Market Moment That Made the Gamble Bigger

Ferrari didn’t arrive at this moment in a vacuum. The luxury EV space it’s entering is at once crowded with ambition and littered with retreated promises. Lamborghini — Ferrari’s most culturally proximate rival — backed off its EV goals earlier this year amid an uncertain market for all-electric supercars, compounded by parent company Volkswagen Group’s precarious financial situation. Rolls-Royce has pressed on with the Spectre but hedged loudly. Aston Martin has gone quiet on electrification timelines. Into that environment, Ferrari arrived in Rome with a car it had been engineering since at least 2021, a price tag north of $640,000, and a design that makes no apology for looking unlike anything the company has produced before. Gizmodo

The broader picture for luxury EVs is genuinely complicated. Range anxiety has faded as a consumer concern at the high end; design differentiation has become the real battlefield. Yet the Luce’s estimated EPA range — likely between 250 and 300 miles once the less generous American testing cycle is applied to the 530-kilometre WLTP figure — isn’t spectacular in a world where 400 miles and 400-kilowatt charging are quickly becoming expected from the likes of BMW and Porsche. Ferrari is betting that its customers won’t care. InsideEVs

That bet is, historically, a reasonable one. The brand has never competed on value. It competes on myth.

1 — What the Ferrari Luce Actually Is

What is the Ferrari Luce?

The Ferrari Luce is a five-seat, four-door electric performance car powered by four electric engines — one on each wheel — producing 1,050 horsepower, capable of reaching 100 km/h in 2.5 seconds, with a top speed of 310 km/h and a range of 530 km fully charged. It is the first all-electric production vehicle from Ferrari in the company’s 79-year history. Ferrari

The Ferrari Luce electric car arrives with hardware that, by any objective measure, belongs among the fastest automobiles on the planet. The rear motors alone produce 620 kW, spinning at up to 25,500 rpm; the front pair adds 210 kW at 30,000 rpm. The 800V architecture supports fast charging up to 350 kW, and the whole package weighs 2,260 kg — kept manageable in part through extensive use of recycled aluminium alloys, with zero steel in the body. Electrek

That last detail matters. The zero-steel body isn’t incidental engineering — it’s structural philosophy made tangible. Ferrari spent years developing what it calls a bespoke electric platform, built entirely at a new dedicated facility within the Maranello complex. A 122 kWh battery pack is built from 210 cells co-developed with South Korean supplier SK On. The motors are derived directly from the F80 hypercar programme — a deliberate bridge between Ferrari’s most extreme limited-series technology and a car that seats five people in everyday comfort. Electrek

Ferrari chairman John Elkann told the 200-plus media members assembled in Rome: “Ferrari Luce is not a response to change. It’s a decision, a deliberate decision, to lead what comes next with clarity, with courage. Five years ago, we asked ourselves: what would Ferrari be if we imagine that again from a blank sheet?” Robb Report

The answer to that question is, physically, a liftback sedan unlike anything Maranello has ever sanctioned. Gone are the short-wheelbase aggression and haunched rear quarters of every iconic Ferrari you can name. In their place: a long, smooth glasshouse, rear-hinged doors, a deep black S-duct carved across the front face, and proportions that — if the badge were removed — would not immediately read as Italian at all. The upper portion of the vehicle, what Ferrari calls the glasshouse, is enclosed in a large curvaceous structure that includes the windscreen, side windows, rear window, and a panoramic glass roof, paired with aluminium body panels that transition into wide aerodynamic wings at front and rear to create the impression of a single teardrop form. Dezeen

Multiple reviewers reached for the same reference point independently. The Ferrari Luce, designed with Jony Ive and Marc Newson of LoveFrom, is the first car from Maranello to carry the silhouette of an Apple Magic Mouse, with a dash-to-axle ratio of essentially none, an enormous sweeping roofline, and a serious wedge to the beltline. The Autopian

2 — The Ive Effect: Why This Interior Is the Real Statement

Why did Ferrari hire Jony Ive to design the Luce?

Ferrari didn’t hire Jony Ive to produce a more beautiful car in the conventional sense. It hired him to solve a philosophical problem: what should the human environment of an electric Ferrari feel like, when the defining sensory input — the noise of a combustion engine — has been removed?

The short answer to that People Also Ask question: Ferrari recruited LoveFrom because Jony Ive had already done something analogous with the Apple Watch — converting an analogue product category into a digital one without destroying its identity. Ferrari chairman John Elkann, a member of the Agnelli family that owns the brand, specifically admired how the Apple Watch had transformed a traditional timepiece into a digital product. He wanted the same thinking applied to Ferrari’s electric future. The collaboration began around 2021. LoveFrom was given creative autonomy across every dimension of the Luce’s design — interior, exterior, interface — working directly alongside Ferrari’s own Centro Stile team under design director Flavio Manzoni. techradar

The interior is where Ive’s influence is most unambiguous and, arguably, most counterintuitive. At a moment when virtually every premium EV maker is filling cabins with ever-larger touchscreens, the Luce pushes hard in the opposite direction. “So much of what we did,” Ive said at the San Francisco interior preview in February, “was so that you could use it intuitively, enjoy it and use it safely. We use some touch in the central screen, but it’s very thoughtful, and the vast majority of the interfaces are physical. Every single switch feels different, so you don’t need to look.” aol

The result, in physical terms, is a cabin machined from recycled aluminium, wrapped in premium leather, with a three-spoke steering wheel that carries the iconic Manettino dial — the driving mode selector that has been a Ferrari signature for decades — alongside torque-control paddles and a binnacle cluster. The analogue needle in the digital speedometer isn’t nostalgia; it’s Ive’s considered answer to the question of how humans maintain situational awareness at speed without reading a number off a screen.

Yet the picture is more complicated than simple retro comfort. An Apple aficionado watching the interior reveal could spot Ive’s handiwork in the Apple Watch-like crown on the screens, the iPad-like infotainment panel, and the use of Gorilla Glass — hardware choices that echo Apple’s philosophy more than Ferrari’s. The Luce isn’t purely analogue. It isn’t purely digital. It’s the product of someone who has spent a career arguing that the two don’t need to be in opposition. aol

3 — What the Luce Means Beyond Maranello

The arrival of the Ferrari first EV carries implications that extend well past the supercar market, which is, by any realistic measure, a rounding error in global automotive volumes. The Luce matters structurally for three reasons.

First, pricing. The Ferrari Luce’s price ranges from $640,000 to $647,000, which puts it in a bracket where the competition isn’t the Porsche Taycan Turbo S or the Rimac Nevera — it’s the Bugatti Chiron and Ferrari’s own limited-series special editions. Ferrari has, in effect, positioned the Luce not as a concession to electrification but as an expansion of its collector-tier offer. That’s a fundamentally different commercial argument than the one Porsche is making with Taycan, or that Lotus made with the Eletre. It’s not “EVs are the future, so here’s ours.” It’s “here is a new kind of Ferrari, available only to those who can afford to ask what a blank-sheet Ferrari could be.” Tech Times

Second, production strategy. Ferrari has been unambiguous that the Luce is an addition, not a transition. CEO Benedetto Vigna has framed it explicitly: “This is an addition to the lineup, not a transition” to all-electric. The automaker’s strategy for 2030 calls for 20% electric vehicles, 40% hybrids, and 40% internal combustion vehicles in annual sales. That’s a company keeping its options open with considerable discipline. Ferrari has watched rivals make sweeping electrification pledges and then retreat under market pressure. It chose instead to move slowly, precisely, and expensively — one car, built at one new factory, delivered to one carefully curated customer list. Go-Electra

Third, the supply chain signal. The decision to co-develop the Luce’s battery cells with SK On — and to assemble the complete pack within Maranello — is a statement about vertical integration at the luxury end of the EV market. Where mainstream brands are increasingly dependent on external cell suppliers for entire packs, Ferrari is insisting on assembly ownership. The Luce stands, in the assessment of Electrek’s Rome correspondent, as the most ambitious performance EV any legacy automaker has attempted, and possibly the strongest endorsement of electrification that a performance legacy brand has ever offered. Electrek

First deliveries are expected in October 2026. US customers won’t receive their cars until spring 2027.

4 — The Counterargument: What Ferrari May Be Getting Wrong

There is a steel-man case against the Luce, and it deserves a serious hearing.

The design, whatever its merits, represents a genuine rupture with the visual language that made Ferrari valuable in the first place. The Luce’s roots lie in tech design rather than automotive design — there is, critics have noted, very little typical Ferrari DNA visible in its form. For a brand whose secondary market prices depend almost entirely on the ability of a car to look like a Ferrari in the rearview mirror of history, that is not a trivial concern. If the Luce fails to appreciate — or worse, depreciates — on the collector market, it damages not just its own resale story but the carefully maintained scarcity narrative that underpins every other car in the range. The Autopian

Then there is the question of what the Luce is actually competing against. Its range and charging figures — impressive in isolation — are not spectacular in a world where 400 miles of EPA range and 400-kilowatt charging are becoming table stakes for luxury offerings from BMW and Porsche. Ferrari’s counterargument is that the Luce was engineered to deliver driving emotions that no spec sheet can capture, and that its customers will not be cross-shopping against a BMW i7. That’s probably true. But the brand has also opened itself to a new kind of buyer — someone drawn by the electric credentials and the Jony Ive cachet — who may well cross-shop on exactly those terms. InsideEVs

And the Ive appointment itself carries risk. Apple’s design language, for all its brilliance, is now omnipresent. When the interior of a $640,000 Ferrari is described by multiple reviewers as looking like an Apple product, that’s not necessarily a compliment. It suggests the car may be too legible — too immediately readable as the output of a known aesthetic — in a segment where the whole point is to be unlike anything else.

Ferrari knows all of this. The fact that Carando said it publicly — “people will love it, and people will hate it” — suggests the company has made its peace with division as the price of ambition.

The Weight of the Blank Sheet

The deeper tension in the Ferrari Luce story isn’t about whether Jony Ive’s design is good or whether the range figure is competitive with the Porsche Taycan. It’s about what happens when a brand built on one sensory world — the scream of a V12, the smell of hot aluminium, the feedback of an unassisted steering rack — attempts to build emotional authority in a world defined by silence and software.

Ferrari’s answer, assembled over five years, is essentially this: we believe the emotions are separable from the engine. That driving a machine of extraordinary capability, wrapped in materials of genuine craft, controlled through interfaces that reward the human hand — that this produces feeling regardless of what propels it. Ive clearly believes the same. His life’s work has been the argument that technology, made right, creates attachment.

Whether the Luce’s buyers agree will become clear in October, when the first cars leave Maranello. Whether the rest of the automotive world agrees will take rather longer to determine.

One thing is not in doubt. On 25 May 2026, in a hall chosen to honour 79 years of racing history, Ferrari put a car on a stage that looks nothing like its past and claimed it nonetheless carries everything that made Ferrari matter.

That is either the bravest thing the company has done in a generation, or the most expensive creative argument in the history of motoring.

Possibly both.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

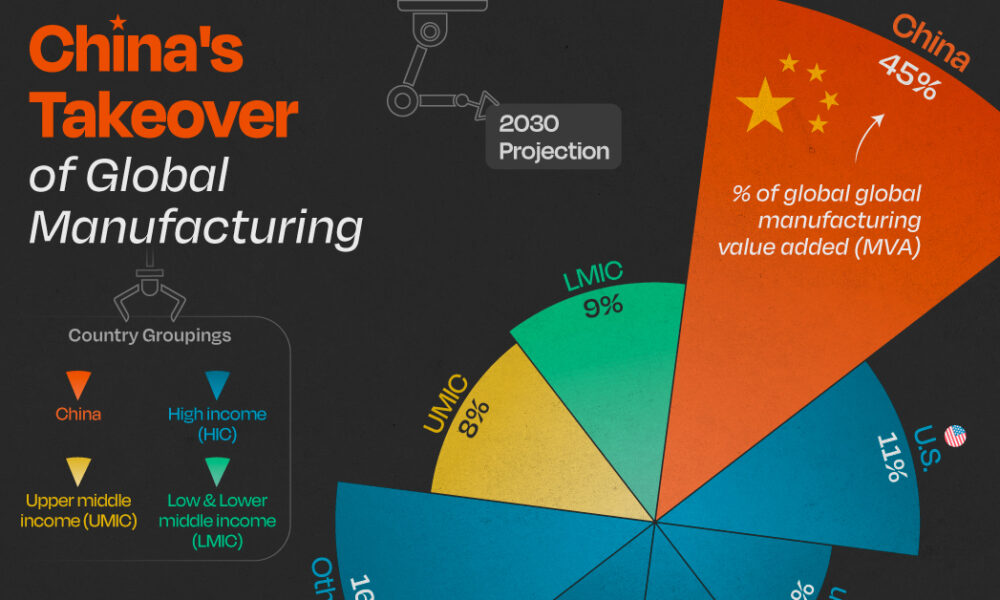

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025