Analysis

The Disappearing American Mortgage: A Generation Priced Out of the Dream

Mortgage applications hit a 25-year low as first-time buyers collapse to 21% of market share. Why young Americans face a future as perpetual renters — and what it means for the economy. “Mortgage applications hit a 25-year low. First-time buyers are a record-low 21% of the market. Why young Americans face life as perpetual renters.

The Numbers No One Wants to See

Consider what it takes to close on a home in America right now. You need a household income approaching six figures to qualify for the median-priced existing home. You need a down payment that, at the current median of 10% for first-time buyers, amounts to more than $43,000 in cash — at the highest level since 1989. You need the nerve to lock into a 30-year fixed mortgage rate of 6.43% — more than double the pandemic-era lows that millions of existing homeowners are still sitting on, quite contentedly, with no intention of surrendering. And you need the good fortune of finding something for sale in the first place.

If you’ve managed all of that, congratulations. You are, in a measurable and increasingly literal sense, one of the lucky few.

The American mortgage — that foundational instrument of middle-class wealth, the financial backbone of the postwar suburban compact — is vanishing. Not gradually, and not quietly. Data released by the Mortgage Bankers Association on March 25, 2026 showed mortgage applications tumbling another 10.5% in a single week, with the Purchase Index falling 5% week-over-week. The week prior — ending March 13 — had already seen a 10.9% collapse, the steepest single-week drop since September 2025. These aren’t blips. They are the fingerprints of a structural transformation so deep that it risks redrawing the sociological map of American wealth for a generation.

Worse Than the Great Recession — Without the Excuse

To grasp how extraordinary the current freeze is, it helps to recall what the housing market looked like during the worst economic catastrophe of living memory. In 2009 and 2010, as the subprime bubble imploded and unemployment breached 10%, mortgage originations cratered. The MBA’s Market Composite Index — which tracks total loan application volume — fell to what seemed like unthinkable lows. The housing market was broken, the country agreed, and policymakers mobilized accordingly.

Today, unemployment sits at roughly 4%. The economy has, by standard macroeconomic measures, recovered. And yet 96 of the 100 lowest readings of the MBA’s weekly mortgage application index have occurred in the past three years — a span that began not with a financial crisis but with the Federal Reserve’s campaign to tame post-pandemic inflation. The market is not broken in the way 2009 was broken. It is frozen, seized by a structural contradiction: the people who own homes have every incentive to stay put, and the people who want homes cannot afford to enter.

The MBA’s weekly Purchase Index — which isolates new home purchase applications from refinancing activity — was only 5% higher than the same week one year ago as of late March 2026, a derisory gain that barely registers against years of suppressed demand. Elevated Treasury yields, driven in part by geopolitical oil-price pressures, have kept mortgage rates stubbornly high. The 30-year conforming rate closed the week at 6.43%, with jumbo balances carrying 6.45%. The window in early 2026 when some lenders briefly offered rates approaching 6.25% — hailed breathlessly at the time as a turning point — has snapped shut.

The Rate-Lock Prison

To understand why the supply side of the housing market has frozen so completely, follow the math of the existing homeowner. The median American seller has now owned their home for a record 11 years before listing — an all-time high in data stretching back to 1981. Roughly 60% of outstanding mortgages in the United States carry rates below 4%. Trading a 3% mortgage for a 6.4% one, on a more expensive house, in a market with higher property taxes and insurance premiums, requires a powerful motivating force — a job relocation, a family expansion, a death, a divorce. For tens of millions of Americans, the math simply doesn’t pencil out, and so they stay. Their inertia is perfectly rational. Its aggregate effect is devastating.

The NAR’s 2025 Profile of Home Buyers and Sellers — a survey of transactions conducted between July 2024 and June 2025 — captures the downstream consequences with clinical precision. The typical seller age hit a record 64. The typical buyer age hit a record 59. The median age of first-time buyers climbed to an all-time high of 40 — up from the late twenties in the 1980s, and from 30 as recently as 2010. By NAR’s accounting, a decade of deferred homeownership costs a typical buyer roughly $150,000 in accumulated equity on a standard starter home. That is not a financial setback. That is a generational wealth transfer, running in reverse.

Redfin, using a different methodology that draws more directly on Federal Reserve microdata, places the first-time buyer median age at 35 in 2025 — lower than NAR’s figure, and a modest improvement from the prior year. Even at 35, the typical first-time buyer is significantly older than at any point in the postwar era, and the methodological debate between NAR and Redfin only underscores the point: by any honest accounting, Americans are buying their first homes later, under more financial duress, with lower long-term equity gains ahead of them.

The First-Time Buyer Collapse

The most alarming data point in the NAR survey is not the age figure — it is the share. First-time buyers accounted for just 21% of all home purchases over the 12-month survey period — a record low in data going back to 1981, and a figure that has been cut in half since 2007, when first-timers made up around 40% of the market. Before the Great Recession, 40% was considered the structural norm. The NAR’s deputy chief economist, Jessica Lautz, did not mince words: “The implications for the housing market are staggering. Today’s first-time buyers are building less housing wealth and will likely have fewer moves over a lifetime as a result.”

The vacuum left by absent first-time buyers has been filled, predictably, by those with the deepest pockets. Repeat buyers now constitute 79% of all home purchases, with a median age of 62 and a median down payment of 23% — the highest since 2003. Thirty percent of repeat buyers paid all cash, bypassing the mortgage market altogether. In a healthy housing ecosystem, first-time buyers feed the lower rungs of the ladder, creating demand that allows existing owners to trade up. When that base collapses, the entire market ossifies. Turnover falls. Supply dwindles. Prices, absent the corrective pressure of a functioning bottom of the market, hold or rise despite unaffordable conditions. This is not a market failure in the traditional sense. It is a market succeeding — extraordinarily well — for a narrow slice of older, already-wealthy participants, at the expense of everyone else.

Key Generational Homeownership Data (2025)

| Generation | Homeownership Rate (2025) | Boomer Rate at Same Age |

|---|---|---|

| Gen Z (ages 19–28) | 27.1% | ~40–44% |

| Millennials (ages 29–44) | 55.4% | ~60–65% |

| Gen X (ages 45–60) | 72.7% | — |

| Baby Boomers (ages 61–79) | 79.9% | — |

Sources: Redfin analysis of Census Current Population Survey, 2025; Scotsman Guide

Gen Z’s homeownership rate reached 27.1% in 2025, up marginally from 26.1% the year before. That modest gain deserves context: when Gen Xers and baby boomers were the same age, homeownership rates for 28-year-olds stood at 42.5% and 44.4%, respectively. Gen Z is tracking 15 percentage points behind its parents’ generation at the same stage of life. Meanwhile, racial gaps remain stark: the homeownership rate for Gen Z Black Americans stood at just 14.2% in Q4 2025, a figure that compounds the racial wealth gap with brutal efficiency.

Among young adults broadly, the under-35 homeownership rate rose from 36.3% to 37.9% in the fourth quarter of 2025 — a genuine uptick, but one that remains below the 25-year average, and one achieved not because the market opened up but because a fraction of younger buyers made extraordinary sacrifices to enter it. As Redfin senior economist Asad Khan noted, “Gen Zers and millennials are making small gains in homeownership because they’re eager to buy, they’re making sacrifices, and because affordability has improved a bit at the margins — not because homes suddenly became affordable.”

Even at current levels, the median household income lags nearly $25,000 behind the earnings required to purchase a median-priced home. That gap is not a rounding error. It is a structural chasm.

The Supply Catastrophe Underneath

Every discussion of housing affordability eventually circles back to supply — and the supply picture in America is not improving fast enough. Single-family housing starts averaged 943,000 units in 2025, down from 1.02 million in 2024, with MBA projecting a roughly flat 2026 at around 930,000 units. That number falls far short of the estimated 1.5 to 2 million new units economists say are required annually to close the supply deficit built up over the past decade and a half of underbuilding.

Homebuilders face a perfect storm of their own: elevated input costs, persistent labor shortages, zoning and permitting barriers that add months and hundreds of thousands of dollars to project timelines, and — critically — an elevated inventory of unsold new homes sitting at 472,000 units as of December 2025, equivalent to an 8-month supply. Builders are not inclined to break ground aggressively into a market where completed homes sit unsold. The result is a construction industry operating at a cautious pace precisely when the country needs urgency.

The rental alternative provides cold comfort. Rents have softened in some Sunbelt markets as a surge of multifamily completions finally came to market, but vacancy rates in major East Coast metros remain tight. For young Americans priced out of ownership, renting is not a temporary waystation — it is increasingly a permanent condition. Apartment List’s 2025 Millennial Homeownership Report found that nearly 25% of millennials expect to always rent — a figure that has roughly doubled since 2018. That psychological shift matters: when a generation stops believing homeownership is attainable, the political and social pressure to fix housing markets loses one of its most powerful engines.

A Global Pattern, an American Inflection

The United States is not alone in this predicament. The housing affordability crisis plaguing American millennials and Gen Z has close cousins in Canada, Australia, the United Kingdom, and across Western Europe, where a toxic combination of years of low interest rates inflating asset prices, NIMBYist planning regimes restricting supply, and demographic demand from large young cohorts has pushed homeownership rates for people under 40 to multi-decade lows. In London, Sydney, Toronto, and Auckland, the conversation about a permanently renting younger class is years further along than in Washington or New York. The political backlash — housing as a central election issue — is already transforming party platforms in the U.K. and Australia.

What distinguishes the American case is the mortgage itself. The 30-year fixed-rate mortgage, a product unique to the United States among major economies, has historically functioned as an extraordinary wealth-building tool and a form of consumption smoothing — allowing households to lock in a predictable housing cost for three decades, building equity through forced savings, and eventually owning an asset outright. The product was explicitly designed, through the government-sponsored enterprises Fannie Mae and Freddie Mac, to democratize capital access. When that instrument becomes unaffordable to the bottom half of the income distribution — and then the bottom 60%, 70% — it stops serving its designed purpose and begins functioning as a wealth-concentrating tool for those already inside the system.

What Comes Next — and What Policy Must Do

The Federal Reserve’s rate-cutting cycle, which saw three quarter-point reductions in 2025, has done remarkably little to ease mortgage rates, which respond primarily to 10-year Treasury yields rather than the fed funds rate. MBA forecasts rates averaging around 6.4% through 2026, while Fannie Mae has projected a more optimistic path toward sub-6% rates by year’s end — a divergence that reflects genuine uncertainty about the trajectory of inflation, fiscal deficits, and global capital flows. Even if rates fell to 5.5% tomorrow, the affordability math for a 28-year-old earning the median income would remain deeply challenging. Rate relief alone cannot fix a market distorted by a decade of underbuilding.

What would fix it — or at least bend the curve — is a policy agenda serious enough to match the scale of the problem:

- Zoning reform at scale. States that have moved to override restrictive local zoning — Montana, California’s recent legislative efforts, and several New England states — are showing early signs that supply can respond when the regulatory cage is opened. Federal incentives tied to zoning liberalization deserve serious legislative attention.

- Expansion of first-time buyer tools. Down payment assistance programs exist in every state, with over 2,200 initiatives nationally — yet 80% of eligible FHA borrowers fail to access them, simply because awareness is catastrophically low. A federally coordinated information campaign, combined with direct first-generation buyer subsidies, could meaningfully move the needle.

- Rate-lock portability. The most counterintuitive policy idea gaining traction is allowing homeowners to transfer their low-rate mortgages to new properties when they sell. If sellers feel less trapped by their existing rates, more would list. More listings means more supply. More supply means lower prices. The mechanism is financially complex, but the logic is sound.

- Long-term institutional investor accountability. The growing share of single-family homes purchased by institutional investors — and converted to rentals — deserves rigorous scrutiny. While the macroeconomic evidence on investor impact is mixed, the political economy of housing requires that policymakers be seen to address what has become a legitimate public grievance.

The Closing of the American Dream

There is a particular cruelty to the present moment that the aggregate data obscures. For three generations, the mortgage was the mechanism by which an ordinary family — a teacher, a mechanic, a nurse — converted labor into permanent wealth. It was imperfect, racially exclusionary in its early decades, and frequently predatory at the margins. But it worked, on balance, as an engine of intergenerational mobility. The children of homeowners were statistically more likely to attend college, accumulate savings, and buy homes themselves. The equity built in a home served as start-up capital for businesses, as a buffer against medical emergencies, as the inheritance that smoothed the generational transfer of modest prosperity.

When 87% of millennials tell pollsters they believe government should do more to make homeownership accessible — a figure significantly higher than older generations — they are not articulating an abstract ideological preference. They are describing a locked door. They grew up watching their parents build equity in appreciating homes. They graduated into a labor market reshaped by the Great Recession. They came of age as borrowers just as rates rose from 3% to 7%. And now, as the MBA’s weekly surveys confirm week after week, they are applying for mortgages at a rate lower than any seen in 25 years — lower than during the depths of the worst economic collapse in living memory.

The homeownership rate for all Americans under 35 stands at 37.9%. It is slightly higher than it was a year ago, and the analysts at Realtor.com are careful to note it. But the 25-year average for that demographic is 39.7%. And when previous generations were the same age, under-35 homeownership ran closer to 42–44%. The gap is not closing. The structural headwinds — rates, prices, supply, debt, stagnant wages relative to home values — are not resolving themselves on a timeline that will save the housing mobility of the generation currently in its prime buying years.

If a 30-year-old in 2026 waits until 40 to buy — as the NAR data suggests is now the median outcome — they will spend a decade paying someone else’s mortgage, building no equity, and arriving at ownership with 10 fewer years of compounding appreciation ahead of them. Multiplied across 80 million millennials and the Gen Z cohort now entering the labor force behind them, that delay represents an almost incalculable transfer of wealth from the young to the already-propertied.

The mortgage is not gone. It is still being written, still being signed, still closing on homes across America every day. But it is becoming a luxury product — a credential of the already-arrived rather than a ladder for the aspiring. That transformation, if left unaddressed, will not merely reshape household balance sheets. It will reshape the country.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

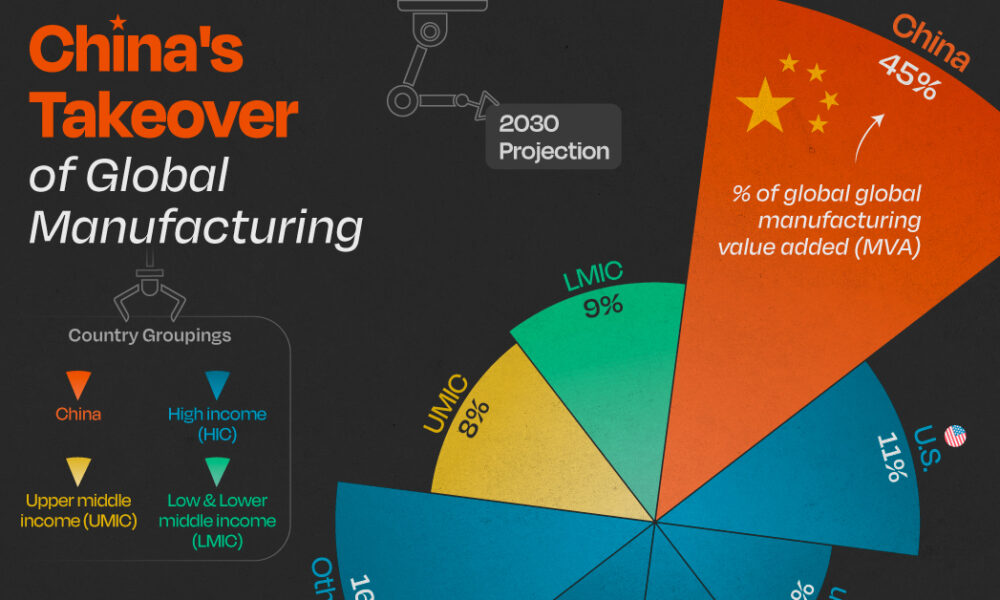

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025