Analysis

HSBC Cuts China Retail Sales Forecast Nearly in Half — and the Real Problem Is Bigger Than One Bad Month

China’s shoppers were supposed to be the engine of recovery. April just showed how badly that engine is misfiring.

On May 22, 2026, HSBC slashed its forecast for China’s retail sales growth to 2.8% from 5.2% — a revision of nearly 46% — after April data came in at a barely-there 0.2% year-on-year, the weakest reading since December 2022 and well below economists’ consensus forecast of 2%. The revision wasn’t a routine trimming. It was a signal: Beijing’s bid to rebalance its economy toward domestic consumption is running into structural walls that no subsidy programme has yet managed to breach. MarketScreener

The timing matters. China’s first-quarter GDP expanded 5%, putting the full year on track for Beijing’s target. April suggested that pace may already be slipping.

The HSBC China Retail Sales Forecast Cut Explained

HSBC researchers Erin Xin and Taylor Wang, writing on May 22, didn’t mince their assessment. The April retail sales print was, in their words, “inconsistent with the recent calls for rebalancing growth towards domestic demand.” That’s diplomatic language for: the policy architecture isn’t delivering.

The bank cut its retail sales growth forecast to 2.8% from the 5.2% projected in March, after official April data came in below expectations at 0.2% year-on-year — the softest reading since late 2022 during the coronavirus pandemic. South China Morning Post

Three converging forces drove that downgrade, and each one is structural rather than cyclical.

First, the labour market. HSBC’s researchers noted that the purchasing managers’ index and other indicators pointed to weakness in the job market, while youth unemployment was “still elevated” amid growing concerns that AI could displace some jobs. China’s urban youth unemployment rate for 16- to 24-year-olds stood at 16.1% as recently as February 2026 — still among the highest readings since the National Bureau of Statistics revised its methodology in 2024, and far above the pre-pandemic baseline. Young workers don’t buy sofas, cars, or apartments when they’re uncertain about next month’s rent. South China Morning Posttradingeconomics

Second, the property sector. China’s property downturn began in 2021 and continues to pressure economic growth and consumer confidence. Housing traditionally served as both a place to live and a major store of household wealth. The wealth effect runs in reverse: falling home values make families more cautious, not less. Property investment contraction widened in April on an annual basis, extending a drag on growth that has persisted for several years, while fixed-asset investment contracted 1.6% in the first four months of 2026, reversing a 1.7% expansion in the January-March period. U.S. BankInvestinglive

Third — and perhaps most telling — the trade-in programme is losing its grip. Automobile sales dropped 15.3% in April from a year earlier, while home appliance sales declined 15.1% and building materials fell 13.8%. These are precisely the categories that Beijing’s trade-in subsidies were designed to protect. IndexBox

The collapse in durables spending is the most revealing data point in the April release. These are not luxuries. They are the categories that Beijing specifically targeted with its two-year-old trade-in programme — and their sharp declines suggest the programme’s demand-pulling effect has been largely exhausted.Why China’s Consumption Problem Won’t Be Fixed by Another Subsidy Round

Why did HSBC cut China’s retail sales forecast so sharply? The simplest answer is that April’s 0.2% growth rate revealed a consumption shortfall that March’s more flattering 1.7% reading had temporarily obscured. But the structural diagnosis goes deeper: China’s trade-in subsidies, however well designed, have a fundamental design flaw.

ING economists warned earlier this year that the trade-in policy “essentially front-loads consumption and has limited lasting power. While households may choose to buy a new car or washing machine when it comes with a nice discount, they likely won’t immediately buy another one next year, even if the discount remains.” After a surge in sales during the early stages of the trade-in policy, sales flatlined in subsequent years — a pattern now repeating with household appliances. ING THINK

Beijing appeared to recognise this dynamic. For 2026, the trade-in programme budget was scaled back from RMB 300 billion in 2025 to RMB 250 billion. That’s a significant signal: even the architects of the programme are acknowledging its diminishing returns. ING THINK

The deeper issue is the wealth-confidence-spending cycle. Household consumption accounts for roughly 39% of Chinese GDP — significantly lower than in most developed economies. In 2022, people aged 20 to 39 accounted for 26.7% of the population but contributed 29.1% of total consumption, making them the highest-spending demographic. This cohort is also among the most exposed to youth unemployment, falling home values, and AI-driven job anxiety. Their caution isn’t irrational; it’s a rational response to genuine wealth and income uncertainty. Asia Society

What follows from that is a structural trap: households won’t spend confidently until property stabilises and jobs feel secure; property won’t stabilise until demand recovers; and demand won’t recover until households feel confident enough to spend. Subsidies can interrupt this cycle temporarily — they did, through much of 2024 and early 2025 — but they can’t resolve it.

Implications: What a 2.8% Retail Sales Year Means for Markets, Policy, and the Growth Target

A 2.8% retail sales growth year isn’t a disaster in isolation. It is, however, a serious obstacle to the broader ambition of rebalancing China’s economy away from investment and exports and toward household consumption. The World Bank has noted that China faces headwinds including a protracted property sector downturn, subdued confidence, deflationary pressure from weak domestic demand, and heightened uncertainty from shifting global trade policies — and April’s print makes each of those headwinds feel more entrenched than Beijing’s official messaging would suggest. World Bank Group

For policymakers, the immediate pressure is on the People’s Bank of China. Rate cuts and reserve requirement ratio reductions remain the most obvious levers. As of late 2025, HSBC’s own private banking arm expected the PBoC to deliver 20 basis points of interest rate cuts and 50 basis points of RRR reductions through 2026. That expectation looks more urgent now. HSBC Private Bank

Yet monetary easing alone won’t fix a confidence problem. Cheaper credit doesn’t compel households to borrow if their biggest asset — their home — is still falling in value and their employer feels uncertain about the year ahead. The IMF, in its December 2025 Article IV consultation, was blunt: China needs to move toward a “more consumption-oriented, more services, job-rich” growth model. That requires structural reform, not just the rate cycle.

For markets, the implications are asymmetric. Consumer-facing sectors — retail, food services, household durables, auto — face a tougher earnings environment than the 2025 trade-in bounce implied. Yuhan Zhang, principal economist at the Conference Board’s China Center, noted that consumers are concentrating spending on “selective discretionary and upgrade categories rather than broad-based consumption.” The practical read: premiumisation stories may hold up; volume-dependent mass-market brands face real pressure. MarketScreener

The Counterargument: April May Be Noise, Not Signal

Not every analyst accepts the gloomy read. The more optimistic case deserves a fair hearing.

April was a genuinely unusual month. The Iran conflict shock sent energy costs higher and added a layer of uncertainty that compressed business sentiment globally, not just in China. Better-than-expected exports and domestic fuel price controls provided some insulation from the energy shock, and China’s Q1 GDP expansion of 5% was real, not manufactured. A single month’s retail print — particularly one distorted by an external shock — may not capture the underlying demand trajectory. Investinglive

The bulls point to several mitigating factors. Urban unemployment ticked down to 5.2% in April from 5.4% in March. Services consumption, specifically catering revenues, grew 2.2% even as goods sales dipped. And Beijing has consistently demonstrated its willingness to deploy fiscal tools when growth slips — the special government bond programme, infrastructure spending, and local government financing support are all still on the table.

As one analysis noted, Beijing has “plenty of policy tools left, including rate cuts, infrastructure spending, and easier credit for local governments. The question is whether it pulls the trigger fast enough to keep 2026 on track for its 5% growth target.” Briefs Finance

The counterargument is worth taking seriously. What it can’t fully explain, however, is why the HSBC downgrade — from 5.2% to 2.8% — was so large. Single-month volatility doesn’t typically produce a 46% forecast revision. That scale of adjustment implies the bank’s researchers believe they were previously underestimating something structural.

The Deeper Reckoning

There is a tension at the heart of China’s 2026 economic narrative that April’s data has made impossible to ignore. Beijing has staked its domestic growth story on consumption-led rebalancing — a pivot away from the investment and export model that powered three decades of expansion but now faces diminishing returns and global pushback. Yet the April retail data, and HSBC’s stark downgrade in response, shows that consumption isn’t simply waiting to be unlocked by the right policy mix.

The problem isn’t stimulus design. China’s trade-in programme was technically sophisticated and reasonably well targeted. The problem is that households saving in a falling property market, with elevated youth unemployment and creeping AI anxiety, don’t spend because the government asks them to. They spend when they feel financially secure.

That security will eventually return. Property markets bottom. Labour markets tighten. Confidence rebuilds. The question is whether Beijing’s policy toolkit can compress that timeline — or whether China’s consumers, like consumers across history, will simply wait until the fundamentals do the work themselves.

The April data suggests, uncomfortably, that the wait isn’t over yet.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

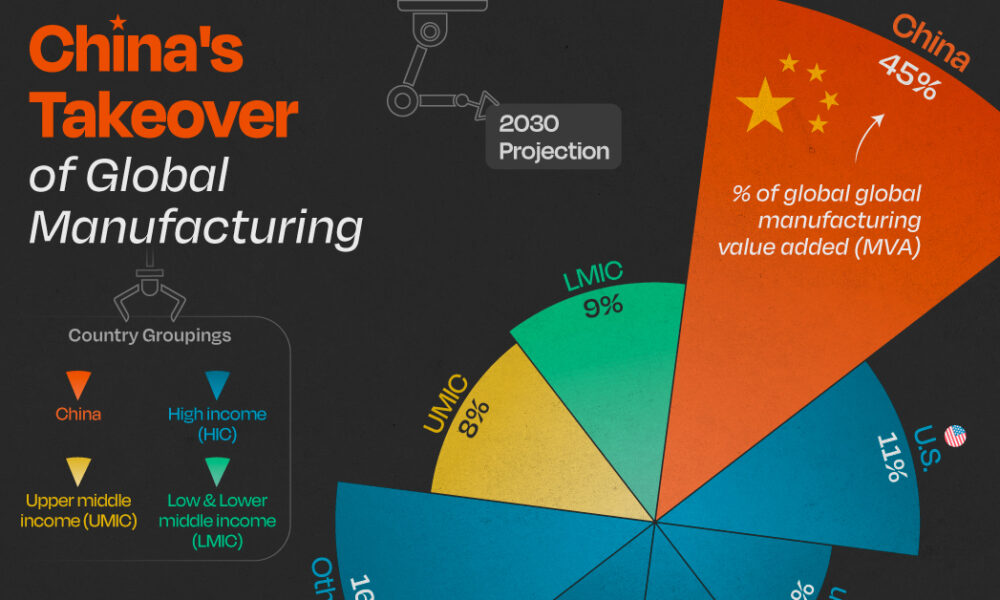

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025