Analysis

7 Ways Tech Startups Are Revolutionizing Pakistan’s Financial Ecosystem in 2026

Let’s Explore how Pakistan’s fintech startups are transforming financial inclusion, payments, SME lending, and digital banking in 2026—with real data, key players, and policy insights driving the country’s $4B startup ecosystem.

Picture Amna, a small-scale textile vendor in Faisalabad’s crowded bazaar. Three years ago, she kept her earnings in a tin box under the shop counter—unbanked, invisible to the formal economy, and locked out of credit. Today, she processes supplier invoices digitally, accesses working capital within 24 hours, and tracks her cash flow on a smartphone app. Amna didn’t walk into a bank branch. A startup came to her.

This is the quiet revolution reshaping Pakistan’s financial landscape. With VC-backed startups now collectively valued at around $4 billion—up 3.6 times since 2020—Pakistan’s growth rate outpaces larger ecosystems including India, New York, and Dubai, positioning it among emerging “New Frontier” tech markets Profit by Pakistan Today. Yet for all the momentum, no unicorn has emerged yet, the funding gap at growth stages remains acute, and roughly 85% of transactions still move in cash. The gap between potential and reality is precisely where startups are doing their most consequential work.

Here are seven ways Pakistan’s tech startups are rewriting the rules of finance in 2026—and why global investors and policymakers should be paying close attention.

1. Expanding Financial Inclusion Beyond Urban Walls

Pakistan’s financial exclusion problem is, at its core, a distribution problem. Traditional banks have concentrated their branch networks in major cities, leaving vast swathes of rural Punjab, interior Sindh, and Balochistan underserved. Pakistan aims to increase adult financial inclusion to 75% by 2028, up from 64% currently, with 143 million broadband and 193 million cellular subscribers forming the digital infrastructure to get there. Invest2Innovate

Startups are filling this gap with mobile-first models that don’t require a bank branch, a credit history, or even a formal ID in some pilots. Easypaisa—Pakistan’s largest mobile wallet—has evolved from simple bill payments into a comprehensive financial super-app covering government disbursements, QR payments, and international remittances. JazzCash serves tens of millions of users across peri-urban and rural markets. Meanwhile, newer entrants like Paymo are targeting digital-native youth with social banking features designed for Gen Z’s financial behaviours.

The economics here are compelling on a global scale. Bangladesh’s bKash built a $2 billion enterprise on mobile financial services for an underserved population—a playbook Pakistan’s ecosystem is now iterating and improving upon. The difference is that Pakistan’s startups are layering artificial intelligence and embedded finance on top of basic wallet infrastructure, building toward something more sophisticated than simple cash transfers.

2. Reinventing B2B Payments and Supply Chain Finance

If consumer fintech is the visible face of Pakistan’s digital finance revolution, B2B infrastructure is its beating engine. Haball is perhaps the most striking example. The Karachi-based fintech has raised a $52 million Pre-Series A round led by Zayn VC and backed by Meezan Bank, scaled its platform to handle over $3 billion in payments, and disbursed more than $110 million in financing to thousands of SMEs and multinational clients. Daftarkhwan

What Haball is doing—digitizing the order-to-cash cycle across Pakistan’s vast informal supply chains—addresses a structural inefficiency that has cost the economy billions in idle working capital and reconciliation errors. By automating invoicing, digitizing trade flows, and embedding Shariah-compliant financing into the transaction itself, Haball turns every payment into a data point for underwriting the next loan.

The implications extend well beyond individual deals. Pakistan’s informal sector accounts for over 40% of GDP, and much of that informality is driven by opaque supply chains and the friction of cash. When startups digitize these flows, they don’t just solve a payments problem—they bring entire economic layers into visibility, taxation, and formal credit assessment for the first time.

3. Accelerating Digital Remittances and Cross-Border Finance

Remittances are Pakistan’s economic lifeline. At roughly $30 billion annually, they outpace foreign direct investment and are equivalent to nearly 8% of GDP. Yet the infrastructure carrying this money has historically been dominated by expensive incumbents—hawala networks and legacy wire services that extract 5–7% in transfer fees from workers sending money home from the Gulf, UK, and North America.

Startups are beginning to disrupt this. Platforms like SadaPay are digitizing international remittances, reducing friction and cost for Pakistani diaspora communities. Invest2Innovate The company’s trajectory also illustrates the ecosystem’s volatility—SadaPay faced staff reductions following its acquisition by Turkish fintech Papara, underscoring how consolidation is beginning to reshape the competitive landscape even in early-stage markets.

Pakistan’s Raast instant payment system, launched by the State Bank of Pakistan and inspired by India’s Unified Payments Interface, is now the backbone connecting digital remittance platforms to beneficiary accounts in real time. The combination of a robust central rails infrastructure and agile startup players building on top of it creates the conditions for the kind of remittance cost compression India achieved within five years of launching UPI—a development that could redirect hundreds of millions of dollars in annual transfer fees back into Pakistani household budgets.

4. Unlocking Capital for Small and Medium Enterprises

SMEs account for roughly 90% of businesses in Pakistan and contribute around 40% of GDP, yet they receive less than 10% of total bank credit. The reasons are well-documented: lack of collateral, informal accounting, no credit history, and risk-averse bank lending desks that simply aren’t calibrated for small-ticket loans. This is where Pakistan’s credit-tech and embedded finance startups are making their most economically significant interventions.

Startups like CreditBook provide micro-loans to SMEs and individuals excluded from traditional banking, while Abhi innovates payroll financing, NayaPay supports SME financial management, and Mahana Wealth promotes saving among the underserved. Invest2Innovate Abhi, founded in 2021, has now raised $57.8 million for its financial wellness platform—making it one of the best-capitalised fintech startups in the country.

The pivot toward hybrid financing models is itself a structural innovation. Pakistan’s startups raised approximately $74.2 million in reported funding in 2025, almost double the funds mobilised in 2024, with the increase driven by hybrid financing—combinations of equity and debt—replacing the previous equity-only funding approach. Business Recorder This mirrors what development finance institutions have long advocated: blended finance structures that reduce first-loss risk and unlock private capital at scale. When applied at the SME lending level, the same logic holds.

5. Building Regulatory Infrastructure That Enables—Not Just Constrains—Innovation

A startup ecosystem is only as strong as the regulatory framework it operates within. Pakistan has not always been known for nimble financial regulation, but the State Bank of Pakistan has been quietly constructing an architecture that is beginning to attract serious attention.

The SBP’s regulatory sandbox, launched to allow fintechs to test innovations under controlled conditions without full licensing requirements, has been central to this shift. SBP’s frameworks have created a supportive environment, positioning Pakistan as a promising fintech market. Invest2Innovate The central bank’s digital banking licensing framework, which has drawn applications from a growing cohort of neobank candidates, represents a further commitment to structured innovation rather than arbitrary prohibition.

Globally, the contrast with peer markets is instructive. Bangladesh’s fintech growth was turbocharged by its own regulatory openness to mobile financial services—a decade ago, a decision considered brave at the time. Nigeria’s central bank took a more restrictive path and watched significant fintech capital flow to Ghana and Kenya instead. Pakistan’s regulators appear to have absorbed these lessons, even if implementation speed remains a work in progress. One of the most notable structural shifts in 2026 is the rise of hybrid financing models and growing interest from bilateral and multilateral development finance institutions in supporting Pakistan’s startup ecosystem. Startup

6. Driving Islamic Fintech as a Global Differentiator

Pakistan is home to 230+ million Muslims, and its financial system has a constitutional obligation to move toward interest-free models. This is not merely a regulatory constraint—it is a market opportunity of extraordinary scale that global Islamic finance players have barely begun to exploit at the retail level.

Haball’s Shariah-compliant supply chain financing is one marker of this trend. But the opportunity extends much further: Murabaha-structured digital lending, Musharaka-based equity crowdfunding, and Sukuk tokenization on blockchain rails are all adjacent spaces where Pakistani startups have structural advantages that competitors in secular financial systems simply don’t possess.

Islamic fintech, AI-driven credit systems, open banking, and cross-border payments are identified as the four major growth frontiers for Pakistan’s fintech ecosystem. Startup With the global Islamic finance industry valued at over $3 trillion and growing at 10–12% annually, Pakistani startups that develop credible, scalable models in this space are building for an export market as much as a domestic one—positioning Pakistan as a potential hub for Islamic fintech products serving markets from Indonesia to Morocco.

7. Creating Jobs, Skills, and a Self-Sustaining Innovation Flywheel

Economic ecosystems don’t grow linearly—they compound. The most durable contribution Pakistan’s tech startup sector is making to its financial ecosystem isn’t any single product or funding round. It is the accumulation of human capital: engineers, product managers, compliance specialists, data scientists, and founders gaining experience that will seed the next generation of ventures.

There are now 170+ VC-backed startups across Pakistan, with 13 “Colts” generating $25–100 million in annual revenue and 17 breakouts having raised between $15 million and $100 million. Startup Each of these companies is a training ground. When engineers leave Haball or NayaPay to start their own ventures, they carry institutional knowledge—of regulatory navigation, of underwriting logic, of enterprise sales in a cash-heavy economy—that accelerates their next company’s time to product-market fit.

Funding to female-founded or co-founded startups nearly doubled, rising from $5.5 million in 2024 to $10.1 million in 2025 Business Recorder, though the average deal size for women-led ventures remains smaller, signalling that inclusion in the ecosystem is widening even as capital parity remains elusive. This trajectory matters: research from McKinsey and the IFC consistently shows that more diverse founding teams produce more resilient companies and broader economic multipliers.

The Road Ahead: From Momentum to Transformation

Pakistan’s fintech story in 2026 is one of real but fragile progress. The country’s $4 billion ecosystem could scale rapidly over the next five to seven years with deeper growth capital and large exits—but the funding gap at later stages remains the primary bottleneck, with no company yet earning more than $100 million in annual revenue or reaching unicorn status. Profit by Pakistan Today

The comparison with India is both inspiring and sobering. India’s fintech ecosystem generated over $9 billion in venture funding in 2021 alone, supported by a government that treated UPI as strategic infrastructure and built policy frameworks that pulled private capital in behind. Pakistan’s policymakers have the blueprint. What they lack is the same scale of conviction in execution.

For international investors—particularly development finance institutions, Gulf sovereign wealth funds, and impact-oriented funds looking at frontier markets—Pakistan represents a rare combination: a massive underserved population, a young and mobile-connected demographic pyramid, a regulatory environment trending toward openness, and startup teams with demonstrably world-class technical ambition. The risk is real. So is the asymmetry.

A Call to Action

For policymakers: Accelerate the implementation of open banking frameworks and extend the SBP’s digital banking licensing to include regionally focused neobanks targeting rural communities. Treat financial infrastructure—Raast, digital identity, data-sharing rails—as public goods requiring sustained government investment, not one-time pilot programmes.

For investors: The window for early growth-stage capital in Pakistan’s fintech sector is open and underappreciated. The startups that survive the current funding gap will emerge stronger, leaner, and with defensible market positions. Patient capital with local ecosystem partnerships is the model that will generate both returns and development impact.

For entrepreneurs: The infrastructure is improving. The regulatory environment is becoming more navigable. The market is enormous, largely untapped, and increasingly digital. Pakistan’s first fintech unicorn is not a question of whether—it is a question of when, and who.

Amna in Faisalabad is already there. The rest of Pakistan’s financial system is catching up to her.

Sources and data cited from: Pakistan Tech Report, Dealroom.co & inDrive, January 2026; invest2innovate (i2i) 2025 Ecosystem Report; i2i Fintech Landscape Report; Tracxn Pakistan FinTech Data, January 2026; Daftarkhwan: Top Pakistani Startups 2026; Startup.pk VC Ecosystem Report; World Bank Financial Inclusion Data.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

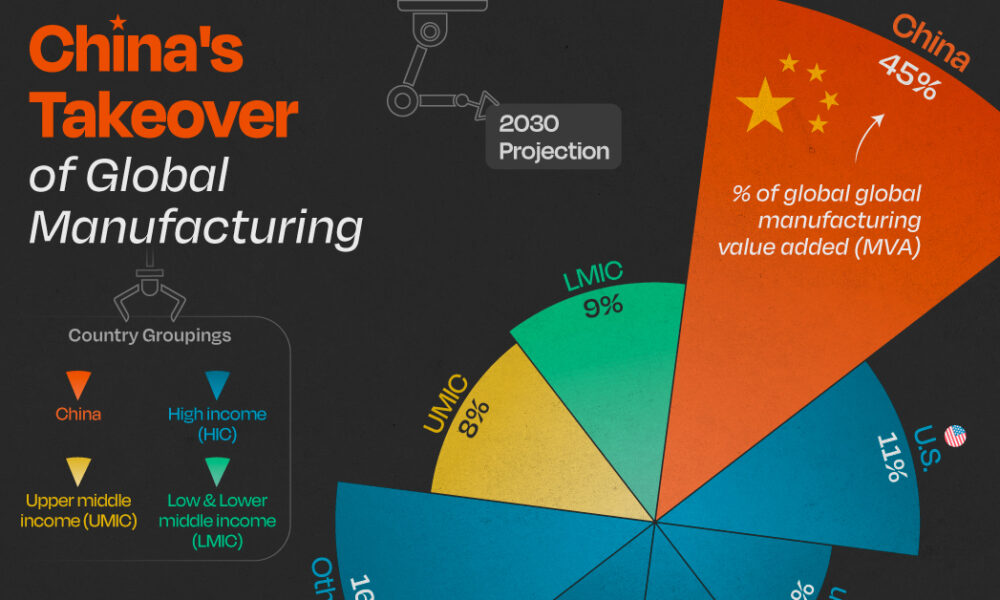

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025