Analysis

Iran Ceasefire Opens Strait of Hormuz: What Trump’s Deal Means

The Ceasefire That Nearly Didn’t Happen — and Why It Changes Everything

It was, in the bluntest possible terms, a civilization held to ransom. For forty days, the United States and Israel had struck Iran with a ferocity not seen since the Second World War — bridges, power plants, universities, military installations reduced to rubble. Iran had responded by sealing the Strait of Hormuz, the 21-mile chokepoint through which roughly a fifth of the world’s daily oil supply once flowed freely, triggering what the International Energy Agency has characterized as the single largest disruption to global oil markets in recorded history. Then, with less than two hours before Donald Trump’s deadline to rain “obliteration” on what remained of Iranian civilian infrastructure, Islamabad performed a diplomatic miracle.

Pakistan Prime Minister Shehbaz Sharif asked Trump to extend his deadline by two weeks and simultaneously urged Tehran to reopen the strait as a goodwill gesture, framing the appeal in terms of giving diplomacy time to run its course. CNBC It worked. Trump announced a two-week, double-sided ceasefire on the condition that Iran agree to the “complete, immediate, and safe opening of the Strait of Hormuz,” citing a 10-point Iranian peace proposal as “a workable basis on which to negotiate.” Axios

The phrase “workable basis” — anodyne to the casual reader — is, in the diplomatic lexicon of great-power competition, nothing short of seismic.

What Iran’s 10-Point Plan Actually Contains — and What It Reveals

Strip away the triumphalist messaging from both Tehran and Washington, and Iran’s 10-point proposal reads less like a peace plan and more like a maximalist opening bid from a government that has been bombed back to the pre-digital age and knows it. The plan, as spelled out by Iran’s Supreme National Security Council, includes controlled passage through the Strait of Hormuz coordinated with Iranian armed forces, the necessity of ending the war against all components of the “resistance axis,” and the withdrawal of U.S. combat forces from all regional bases and positions. NBC News It also calls for lifting all sanctions, releasing Iranian assets frozen abroad, and full payment of Iran’s war-related damages. CNBC

This is not, on any plain reading, a document the Trump administration will sign in its current form. But it is a document designed to do something far more subtle: establish Iran as a state with agency, leverage, and a coherent strategic vision — even in defeat. The Supreme National Security Council’s accompanying claim that “nearly all war objectives have been achieved” NBC News is partly face-saving theater, but it also carries a kernel of uncomfortable truth. Iran has demonstrated, unambiguously, that it holds a hand no adversary can entirely trump: physical control over the jugular vein of global energy.

The ten points, read against the backdrop of six weeks of unprecedented aerial bombardment, constitute a negotiating position, not a capitulation. Tehran knows this. Washington, if it is honest with itself, knows it too.

Pakistan’s Quiet Triumph — and the New Architecture of Mediation

Before this week, Pakistan’s role in the great-power theatre of the Middle East was largely peripheral. Islamabad was a regional pivot — important to Washington for counterterrorism cooperation, to Beijing for the China-Pakistan Economic Corridor — but not a player in the first rank of Middle East diplomacy. That calculus has been permanently revised. The truce, brokered by Pakistan, follows fierce exchanges of airstrikes, missile attacks, and threats that saw unprecedented strikes on Gulf nations, disrupted global shipping routes, and heightened fears of a prolonged confrontation. Al Jazeera

Sharif’s intervention succeeded precisely because it offered both parties something neither could offer themselves: a procedural exit. Trump needed a formula that did not look like backing down; Iran needed survival with the rhetorical scaffolding of victory. Pakistan provided the ladder for both men to descend. Peace talks are expected to begin in Islamabad on Friday, with Vice President JD Vance likely to lead the American delegation. Axios

This is diplomatically significant beyond the immediate crisis. It signals that the post-American-unipolar world is not simply a world dominated by Chinese or Russian mediation — as Riyadh’s 2023 rapprochement with Tehran, brokered by Beijing, suggested. Pakistan’s success here introduces a new variable: middle powers, credibly positioned as neither adversaries nor puppets of Washington, may now carry decisive diplomatic weight in conflicts where the principal parties have exhausted their bilateral channels.

Beijing, ever quick to register shifts in multilateral architecture, moved with characteristic swiftness. China’s Foreign Ministry spokesperson said Beijing “welcomes the ceasefire agreement” and will “support the mediation efforts” by Pakistan and other parties, noting that Chinese Foreign Minister Wang Yi had held 26 phone calls with counterparts from relevant countries. ABC News That is not the statement of a bystander — it is the statement of a great power carefully positioning itself as indispensable to whatever comes next.

The Oil Market Shock: Anatomy of a Historic Selloff

The market reaction was, in a word, violent — and that violence was entirely rational.

WTI, the U.S. crude benchmark, tumbled almost 16% to $95 a barrel — still well above the $67 level it settled at on February 27, before the war began. Brent crude futures, the global oil benchmark, dropped 14% to $93.8 a barrel. CNN For context: Dated Brent — the global benchmark for physical barrels — had reached its highest recorded price of $144.42, according to S&P Global Platts, surpassing even the 2008 financial crisis peak. Axios And the selloff itself made history: analysts described it as the biggest one-day free fall in oil prices since the 1991 Gulf War. Axios

The arithmetic of the disruption explains the arithmetic of the relief. The war in the Middle East — and the effective closure of the crucial Strait of Hormuz — has caused the biggest oil supply shock on record, choking off roughly 12 million to 15 million barrels of crude oil a day. CNN As of Tuesday, 187 tankers laden with 172 million barrels of seaborne crude and refined oil products remained inside the Gulf, according to Kpler, a global trade intelligence firm. CNN

That backlog does not clear overnight. Ports are congested, tanker routing is scrambled, and insurance premiums — which had rendered the Strait commercially prohibitive — will not normalize until underwriters are satisfied that the ceasefire is durable. Tehran has in recent weeks reportedly charged some shipping companies a $2 million fee to guarantee safe passage through the strait. CNN Iranian foreign minister Araghchi’s confirmation that safe transit would be possible “via coordination with Iran’s Armed Forces” Axios is careful language — it preserves Iranian control as a structural fact, regardless of the ceasefire’s duration. As one economist noted, that amounts to a de facto partial nationalization of the world’s most important shipping corridor.

For investors navigating the aftermath: the relief rally is real, but it is pricing in a best-case scenario that two weeks of fragile diplomacy has not yet warranted. Energy sector equities that surged 40-100% year-to-date will face significant profit-taking. Airlines, petrochemical manufacturers, and consumer-facing retailers stand to benefit materially from every dollar of sustained oil price decline. But position sizing in either direction should be calibrated to the probability of the Islamabad talks collapsing — which, given the chasm between Washington’s core demands on Iran’s nuclear program and Tehran’s insistence on full sanctions relief, remains non-trivial.

The Stock Market Surge: Reading the Signal Correctly

Stocks surged across regions: South Korea’s Kospi jumped over 5%, Japan’s Nikkei rose 4%, Hong Kong’s Hang Seng gained more than 2%, and the pan-European Stoxx 600 climbed 3.6%. Futures tied to the Dow Jones Industrial Average rose by 967 points, S&P 500 futures added 2.1%, and Nasdaq 100 futures climbed 2.3%. CNBC

The equity market’s interpretation is straightforward: lower energy costs are a global stimulus. But sophisticated investors should separate the signal from the noise here. The stock market is not pricing a peace deal — it is pricing the possibility of a peace deal, which is a materially different thing. As one market analyst from eToro observed, “TACO is becoming less of a joke and more of a trading strategy across markets. Investors have seen enough last-minute pivots to know that a two-week deadline isn’t necessarily what it seems.” CNBC

The persistence of gold’s bid — spot gold rose 2.2% to $4,803.83 per ounce even as risk assets rallied CNBC — tells the more cautious half of the story. Institutional money is hedging. The relief rally and the haven bid are running simultaneously, which is the market’s elegant way of saying: we want to believe this, but we’ve been burned before.

The Quiet Winners — and the One Uncomfortable Loser Nobody Is Naming

History’s great turning points always redistribute power in ways that the initial headlines obscure. This ceasefire is no exception.

Pakistan emerges with diplomatic capital it will spend for years. Islamabad is now, demonstrably, a credible interlocutor between Washington and Tehran — a status no amount of lobbying or bilateral summitry could have purchased.

China emerges with its multilateral positioning validated. Beijing’s five-point Chinese-Pakistani peace framework, its 26 diplomatic phone calls, its quiet shuttle diplomacy in the Gulf — all of it contributed to the architecture that made the Pakistani intervention possible. The belt-and-road world, Beijing will quietly argue, is a more stable world.

Tehran — counterintuitively — emerges with its deterrence posture partially rehabilitated. The clerical establishment that many analysts, not least in Tel Aviv and Washington, expected to collapse under military pressure has survived. Its control over the Strait of Hormuz has been demonstrated as real, not rhetorical. Whatever the outcome of the Islamabad talks, that leverage does not disappear when the ceasefire expires.

The uncomfortable loser — the entity most conspicuously absent from the diplomatic success narrative — is Israel. The office of Israeli Prime Minister Benjamin Netanyahu announced that while Israel supports the United States’ two-week ceasefire with Iran, the deal does not include the fighting between Israel’s military and Iranian-backed groups in Lebanon. CBS News Netanyahu’s carve-out on Lebanon reveals a government that found itself outmaneuvered by a diplomatic process it could not control — partners in the military campaign, bystanders in its resolution.

The Road to Islamabad: What a Durable Deal Would Actually Require

The next two weeks are not, as Trump’s Truth Social effusions might suggest, a straightforward path to the “Golden Age of the Middle East.” They are a negotiation of extraordinary complexity, with parties whose core demands are structurally incompatible at the outset.

Washington’s irreducible minimum — shared explicitly by Netanyahu, who said the U.S. “is committed to achieving” the goal of ensuring Iran “no longer poses a nuclear, missile and terror threat” ABC News — is a verifiable end to Iran’s nuclear program. Tehran’s irreducible minimum, embedded in its 10-point plan, is the lifting of all sanctions and the normalization of its economy. Bridging those positions in fourteen days is not diplomacy; it is alchemy.

What Islamabad can realistically deliver is a framework agreement — a set of principles broad enough for both sides to claim success, specific enough to extend the ceasefire and return tanker traffic to the Strait, and ambiguous enough to defer the hard questions about nuclear verification, sanctions architecture, and Iran’s regional proxy network. That is not nothing. In the history of this particular conflict, it would be a great deal.

Vice President Vance, addressing critics within the Iranian system who are “lying about the nature of the ceasefire,” said: “If the Iranians are willing, in good faith, to work with us, I think we can make an agreement.” Axios That conditional is doing a lot of work. It is also, for now, the most honest assessment available of where things actually stand.

What This Means for Global Energy Security — the Structural Question That Survives Any Deal

Even if the Islamabad talks succeed beyond all reasonable expectation, this crisis has exposed a structural vulnerability in the architecture of global energy security that no ceasefire can paper over.

A single nation — Iran — demonstrated that it could, with conventional military and asymmetric naval tools, effectively halt nearly a quarter of the world’s seaborne oil trade and push global benchmark prices to record highs within weeks. The response from OPEC, from Washington, from the IEA’s emergency reserves mechanism, from alternative routing through the Cape of Good Hope — none of it came close to compensating for what the Strait’s closure removed.

The strategic conclusion is unavoidable: the concentration of global energy transit through the Strait of Hormuz is an unacceptable systemic risk, and the post-ceasefire world — whatever shape it takes — will accelerate investments in alternative infrastructure, strategic reserve capacity, and the long-term energy transition away from Persian Gulf dependence. For sovereign wealth funds, infrastructure investors, and the energy majors themselves, the crisis of 2026 has clarified the investment case for resilience in ways that no analyst report could have achieved.

The Hormuz gambit may be over. The lesson it taught the world is just beginning to sink in.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

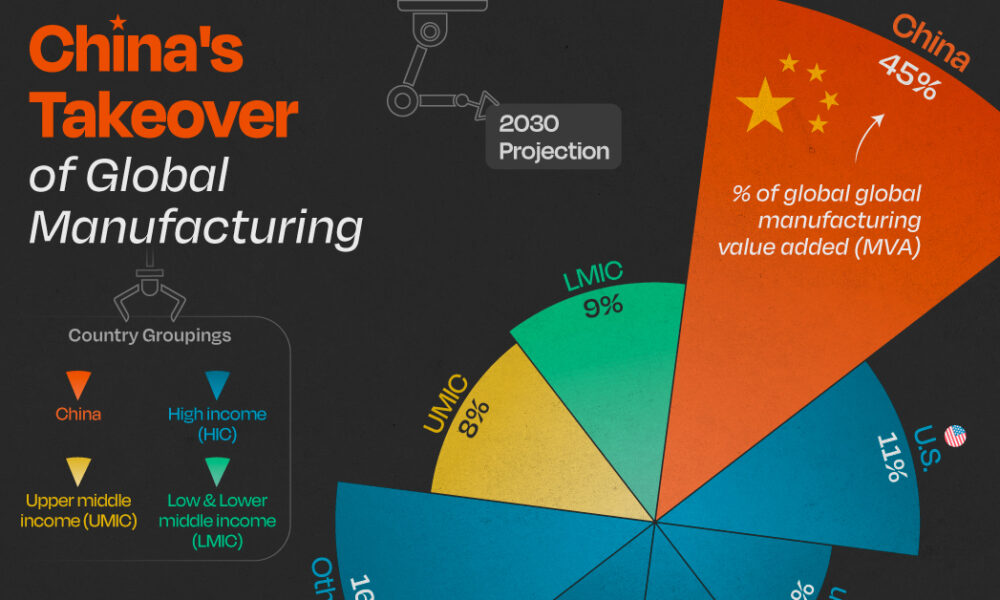

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025