Analysis

Top 10 Stocks for Investment in PSX for Quick Returns in 2026

Imagine turning a modest investment into a meaningful gain while Pakistan rewrites its economic story. That’s not wishful thinking — it’s the very real opportunity sitting in the Pakistan Stock Exchange (PSX) right now, in February 2026.

The KSE-100 has staged one of Asia’s most dramatic recoveries over the past 18 months. Backed by IMF support, falling inflation, improving forex reserves, and a central bank that has been carefully unwinding its aggressive rate cycle, Pakistan’s equity market has rewarded the bold. The question is: where does the next wave of gains come from? Which are the best Pakistan Stock Exchange investments short-term heading into mid-2026?

We’ve done the hard work. Drawing on real-time PSX data, earnings releases, sector research, and macroeconomic modeling, we’ve identified the top 10 stocks for quick returns on PSX in 2026. These aren’t long shots. They are fundamentally strong companies in structurally advantaged sectors — banking, energy, cement, technology, and agri-manufacturing — that are positioned to deliver 20–40% upside within 3–6 months based on current valuations and forward catalysts.

“Pakistan’s KSE-100 has been among the world’s best-performing markets over the past 12 months. With GDP growth projected at 4–5% in 2026, the rally may only be in its second inning.” — IMF Article IV Consultation, Pakistan, 2025–26

The IMF’s extended fund facility of approximately $7 billion has stabilized the macroeconomic framework. Inflation, which peaked above 38% in mid-2023, has collapsed toward single digits. The State Bank of Pakistan has cut its policy rate aggressively, injecting liquidity into equity markets. Foreign portfolio investors have returned. And corporate earnings — particularly in banking — have been nothing short of spectacular. As Yahoo Finance and local analysts have both noted, Pakistan’s risk premium is finally compressing.

But macro tailwinds only tell half the story. Stock picking matters. So let’s get into it.

Table of Contents

- UBL — United Bank Limited

- MCB — MCB Bank Limited

- MEBL — Meezan Bank Limited

- HBL — Habib Bank Limited

- MTL — Millat Tractors Ltd.

- PPL — Pakistan Petroleum Limited

- PSO — Pakistan State Oil Co. Ltd.

- FCCL — Fauji Cement Company Limited

- SYS — Systems Limited

- LUCK — Lucky Cement Limited

Data Note: All prices and metrics reflect PSX data as of mid-February 2026. Projected upside figures are analyst consensus estimates and should not be taken as guaranteed returns. Always consult a licensed financial advisor before investing.

🏦 PSX Banking Stocks — The Engine Room of Quick Gains

If you’re looking for PSX banking stocks quick gains, you’ve picked the right sector. Pakistan’s commercial banking industry has been the single biggest beneficiary of the high interest rate era — and even as rates ease, banks are proving their earnings resilience through fee income, digital growth, and improving asset quality. Four of our top 10 picks come from this sector.

1. UBL — United Bank Limited

PSX: UBL | Commercial Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 455–465 |

| P/E Ratio (TTM) | 6.08× |

| 1-Year Return | +121–140% |

| 52-Week Range | Rs. 188–517 |

| Market Cap | ~Rs. 1.24T |

| Projected 3–6M Upside | 15–30% |

If one stock captures the spirit of Pakistan’s financial renaissance, it’s UBL. The bank has delivered a staggering 121–140% return over the past year — and yet, at a trailing P/E of just 6.08×, it remains one of the most undervalued large-cap banking stocks in the region. That’s the paradox of PSX: even after enormous rallies, valuations still look cheap by global standards.

UBL’s Q3 FY2026 earnings, reported February 25, 2026, are expected to show continued momentum. The bank declared an interim dividend of Rs. 8 per share — representing a 160% payout — signaling management confidence in the earnings trajectory. Its Middle East franchise adds geographic diversification that peers simply don’t have, providing a hedge against any domestic policy volatility.

Analyst consensus on Investing.com pegs the 12-month price target at Rs. 475 (low: 391, high: 590), with three analysts unanimously rating it a Strong Buy. Technical analysts identify a breakout zone between Rs. 510–570 if the bank’s earnings beat expectations — a realistic scenario given the revenue momentum. This makes UBL the standout choice for anyone seeking high return PSX stocks in 2026.

✅ Key Strengths

- Lowest P/E (6.08×) among major banks — deeply undervalued

- Middle East operations provide dollar-revenue diversification

- Strong Rs. 8/share interim dividend declared

- EPS of Rs. 50.62 (TTM), net income Rs. 35.36B in Q3

- All 3 covering analysts rate it Strong Buy

⚠️ Key Risks

- Earnings sensitivity to policy rate cuts compressing margins

- High beta (1.49) — amplifies market-wide volatility

- Significant pullback from ATH of Rs. 517

↑ Projected 3–6 Month Upside: 15–30% | Target: Rs. 520–590

2. MCB — MCB Bank Limited

PSX: MCB | Commercial Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 412–415 |

| P/E Ratio (TTM) | 9.03× |

| 1-Year Return | +47.96% |

| 52-Week Range | Rs. 247–452 |

| YTD Change | +8.82% |

| Projected 3–6M Upside | 15–25% |

MCB Bank is the quiet achiever of Pakistan’s banking sector — less flashy than its peers but relentlessly profitable. With one of the highest return-on-equity ratios in the industry and a legendary history of dividend consistency, MCB is the kind of stock institutional investors quietly accumulate while retail traders chase headlines.

The bank’s YTD performance of +8.82% already puts it ahead of most peer markets globally in just six weeks of 2026. Its 52-week high of Rs. 452 suggests significant re-rating potential from current levels, especially if Q4 FY2025 earnings — which typically coincide with strong full-year dividend announcements — beat the Street’s estimates. MCB’s digital banking transformation has accelerated, with mobile banking active users growing at double-digit rates quarter on quarter.

For investors seeking undervalued stocks PSX for quick profits, MCB’s combination of a sub-10× P/E, above-peer ROE, and an upcoming dividend catalyst makes it a compelling short-term entry. It consistently outperforms sector averages on profitability metrics, as tracked by SCS Trade market valuations.

✅ Key Strengths

- Legendary dividend consistency — a reliable income kicker

- Strong ROE, one of the highest in Pakistani banking

- 8.82% YTD gain signals strong early 2026 momentum

- Lower beta than UBL — relatively defensive upside play

⚠️ Key Risks

- Higher P/E (9.03×) vs. UBL — slightly less compelling on value

- Net Interest Income sensitivity as SBP cuts rates further

- Down ~9% from 52-week high — needs a catalyst to break resistance

↑ Projected 3–6 Month Upside: 15–25% | Target: Rs. 475–515

3. MEBL — Meezan Bank Limited

PSX: MEBL | Islamic Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 485–490 |

| Market Cap | ~Rs. 884B |

| 1-Year Return | +104% |

| 52-Week ATH | Rs. 505 |

| Analyst Target High | Rs. 672 |

| Projected 3–6M Upside | 10–38% |

Meezan Bank is not just a bank — it’s a structural growth story riding one of the most powerful demographic and ideological tailwinds in Pakistan: the shift toward Islamic finance. As Pakistan’s largest Islamic bank, MEBL controls a growing share of a market that by definition cannot go to conventional competitors. That’s a moat you can take to the bank.

The stock surged over 104% in the past year, touching an all-time high of Rs. 505 in January 2026. It’s now consolidating just below that level, setting up what technical analysts describe as a re-accumulation base before the next leg higher. Analyst targets range from Rs. 510 to a bullish Rs. 672 — implying a potential 38% upside from current levels.

MEBL’s beta of 0.89 is the lowest of our four banking picks, meaning it offers smoother, more defensive upside — ideal for risk-aware investors who want exposure to PSX banking stocks quick gains without the full volatility of higher-beta names.

✅ Key Strengths

- Structural moat as Pakistan’s leading Islamic bank

- Lowest beta (0.89) among banking picks — defensive growth

- 104% 1-year return with re-accumulation base forming

- Analyst high target of Rs. 672 implies 38% upside

⚠️ Key Risks

- Islamic finance regulations can shift policy framework

- Valuation premium to peers — less pure value play

- Earnings date delayed to April 28 — near-term catalyst gap

↑ Projected 3–6 Month Upside: 10–38% | Target: Rs. 530–672

4. HBL — Habib Bank Limited

PSX: HBL | Commercial Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 320–345 |

| Market Cap | ~Rs. 500B |

| 52-Week ATH | Rs. 369.99 |

| Dividend Yield (2024) | 9.31% |

| Net Income (Q3) | Rs. 16.91B |

| Projected 3–6M Upside | 10–20% |

Pakistan’s largest bank by assets and deposits, HBL carries the weight of the nation’s financial system on its balance sheet — and has delivered accordingly. With a dividend yield of 9.31% in 2024 and a network spanning over 1,700 branches domestically plus international presence across major financial hubs, HBL is the blue-chip anchor of any serious PSX portfolio.

HBL hit its all-time high of Rs. 369.99 in January 2026 before a modest pullback, which has created a potential buy-on-dip opportunity. An upcoming earnings release on February 19, 2026 is a near-term catalyst — with Q3 net income of Rs. 16.91B and improving non-interest income streams, any positive surprise could spark a fresh leg higher. As the Financial Times has noted in its coverage of emerging market banking recoveries, HBL-type institutions with strong deposit franchises tend to be the last to be sold and the first to re-rate.

✅ Key Strengths

- Pakistan’s largest bank — systemic importance = government backstop

- 9.31% dividend yield (2024) — exceptional income return

- Earnings release Feb 19 is an immediate near-term catalyst

- International network adds revenue diversification

⚠️ Key Risks

- Q3 net income slightly down (-4.92%) from Q2 — watch margin trends

- Regulatory compliance costs remain elevated post-FATF period

- Dividend payout ratio relatively low (40.78%) — upside depends on growth

↑ Projected 3–6 Month Upside: 10–20% | Target: Rs. 355–415

🚜 Agri-Manufacturing: The Underappreciated Performer

5. MTL — Millat Tractors Ltd.

PSX: MTL | Automotive / Agri-Manufacturing

| Metric | Value |

|---|---|

| Sector | Agri-Equipment |

| Market Position | Market Leader |

| Dividend History | Very Strong |

| ROE Profile | High |

| Currency Sensitivity | PKR / USD inputs |

| Projected 3–6M Upside | 15–25% |

Agriculture is Pakistan’s economic backbone, contributing around 22% of GDP and employing nearly half the workforce. That makes Millat Tractors — the dominant domestic manufacturer of Massey Ferguson tractors — one of the most defensible businesses in the country. When farmers invest in mechanization, MTL wins, regardless of the broader economic cycle.

Pakistan’s government has consistently supported agricultural mechanization through subsidized tractor schemes, and with food security remaining a political priority, that support is unlikely to wane. MTL commands a dominant share of the tractor market, benefits from strong brand loyalty, and operates an efficient manufacturing setup that generates consistently high ROE. The stock’s rich dividend history makes it an attractive proposition for investors who want capital appreciation plus income — a rarer combination than most PSX stocks offer.

What gives MTL its edge over competitors like Al-Ghazi Tractors is the sheer depth of its distribution network and its after-sales parts business — a high-margin revenue stream that competitors struggle to replicate. As the IMF-backed economic stabilization filters into rural consumption, MTL’s tractor sales volumes are expected to accelerate through H1 2026.

✅ Key Strengths

- Dominant market share with Massey Ferguson franchise

- Government tractor subsidy schemes are structural tailwinds

- High-ROE business with consistent dividend history

- Agri-revival theme plays into Pakistan’s food security push

⚠️ Key Risks

- Input cost sensitivity — steel and imported components in USD

- Seasonal sales cycle can create quarterly volatility

- Lower free float limits institutional accumulation speed

↑ Projected 3–6 Month Upside: 15–25%

⛽ Energy Sector PSX — High Upside, Underappreciated Value

The energy sector PSX high upside thesis is built on three pillars: recovering global commodity prices, domestic energy transition policies, and historically suppressed valuations that are only now beginning to reflect the sector’s true earnings power.

6. PPL — Pakistan Petroleum Limited

PSX: PPL | Oil & Gas Exploration

| Metric | Value |

|---|---|

| Recent ATH (Jan ’26) | Rs. 284.60 |

| Current Zone | Rs. 255–270 |

| Market Cap | ~Rs. 643B |

| Beta | 1.45 |

| Daily Volatility | 5.00% |

| Projected 3–6M Upside | 15–35% |

Pakistan Petroleum is in the middle of a classic consolidation-after-breakout pattern. After surging to a fresh all-time high of Rs. 284.60 in January 2026, the stock has pulled back toward its strong support zone between Rs. 255–265. Technically, this is precisely the kind of structure that experienced swing traders and medium-term investors love: a high-quality business at a discount relative to its recent peak, with multiple catalysts ahead.

PPL is Pakistan’s second-largest gas producer, with exploration assets across major proven fields. Its earnings are directly leveraged to wellhead gas prices, which remain linked to global energy benchmarks. With Pakistan’s energy import bill remaining a structural burden, domestic gas production is a geopolitical priority — meaning PPL’s assets have strategic value beyond pure commercial metrics. Technical analysts on TradingView project targets between Rs. 290 and Rs. 386 over the next 7–9 months based on Cup-and-Handle breakout patterns.

✅ Key Strengths

- Strategic asset — domestic energy security play

- Pulled back to strong technical support (Rs. 255–265)

- Earnings release April 28 — forward catalyst in sight

- Technical targets Rs. 290–386 on breakout confirmation

⚠️ Key Risks

- High beta (1.45) and 5% daily volatility — not for weak hands

- Circular debt in Pakistan’s energy sector remains a systemic risk

- Government pricing controls can cap realized wellhead prices

↑ Projected 3–6 Month Upside: 15–35% | Target: Rs. 295–385

7. PSO — Pakistan State Oil Co. Ltd.

PSX: PSO | Oil Marketing

| Metric | Value |

|---|---|

| Current Price | Rs. 465–475 |

| 52-Week ATH | Rs. 506.75 |

| 52-Week Low | Rs. 300 |

| Analyst Target (Avg) | Rs. 646 |

| Upside to Consensus | +38% |

| Analyst Rating | Strong Buy (7/7) |

PSO is arguably the single most compelling undervalued PSX stock for quick profits in the energy space right now. Pakistan’s dominant oil marketing company — controlling roughly 50% of the country’s petroleum product distribution — is trading at a massive discount to what 7 covering analysts believe it’s worth: an average target of Rs. 646.47, with a high estimate of Rs. 900. At current prices near Rs. 467, that implies 38% upside to consensus and nearly 93% to the most bullish estimate.

What’s depressing the stock? Historically, PSO has been weighed down by circular debt owed to it by power utilities and the government — a structural problem that the IMF program is specifically addressing. As recoveries from the circular debt pile accelerate, PSO’s free cash flow could inflect sharply upward. The company’s Q3 net income surged 154.87% quarter-on-quarter to Rs. 10.53 billion — a sign that the earnings recovery is already underway. As Economy.com.pk has highlighted, PSO consistently appears in top picks lists for 2026, and the data backs it up.

✅ Key Strengths

- 7/7 analysts rate it Strong Buy — extraordinary consensus

- 38% upside to analyst consensus, 93% to bull case

- 154.87% Q-o-Q net income surge signals earnings inflection

- Circular debt resolution = massive balance sheet catalyst

⚠️ Key Risks

- Circular debt resolution timeline remains uncertain

- Government fuel pricing decisions cap margin upside

- High revenue (Rs. 775B/quarter) but thin EBITDA margins (~1.6%)

↑ Projected 3–6 Month Upside: 20–38%+ | Consensus Target: Rs. 646

🏗️ Cement Sector — Rebuilding Pakistan, Brick by Brick

Pakistan’s infrastructure deficit is well-documented — and the government’s infrastructure push, coupled with private sector housing demand, positions the cement sector as a multi-year growth story. Two picks offer distinct risk-reward profiles within this space.

8. FCCL — Fauji Cement Company Limited

PSX: FCCL | Cement Manufacturing

| Metric | Value |

|---|---|

| Market Cap | ~Rs. 131B |

| Dividend Yield | 2.34% |

| Payout Ratio (2025) | 23% |

| Beta | 1.08 |

| Technical Target | Rs. 57–60 |

| Projected 3–6M Upside | 15–25% |

Fauji Cement is the value pick in the cement space — a mid-cap name backed by the rock-solid Fauji Foundation, one of Pakistan’s largest institutional investors. That institutional backing means better governance, stronger balance sheet discipline, and typically faster access to financing for capacity expansion. Technical analysts have identified a bullish Cup-and-Handle breakout pattern on FCCL, with targets at Rs. 57.80 and Rs. 60 — representing 15–25% upside from current levels.

With earnings due February 25, 2026, FCCL is a near-term catalyst play. Pakistan’s cement dispatches have been recovering with infrastructure spending, and FCCL’s northern market exposure positions it well for CPEC-linked construction activity. A low payout ratio of 23% means the company is reinvesting aggressively — setting up for stronger future earnings growth.

✅ Key Strengths

- Institutional Fauji Foundation backing — governance premium

- Cup-and-Handle breakout forming — bullish technical setup

- Earnings catalyst February 25, 2026

- CPEC infrastructure exposure is a structural tailwind

⚠️ Key Risks

- EPS missed estimates by 12.58% last quarter — execution risk

- Cement sector overcapacity puts pressure on pricing

- Coal price spikes (imported fuel) can compress margins

↑ Projected 3–6 Month Upside: 15–25% | Target: Rs. 57–62

💻 Technology: Pakistan’s Hidden Gem in the Global IT Race

9. SYS — Systems Limited

PSX: SYS | Information Technology

| Metric | Value |

|---|---|

| Sector | IT / IT Export |

| Revenue Currency | USD-Dominated |

| Export Growth | Strong (20%+ YoY) |

| Business Type | Software / Services |

| Currency Hedge | Natural (USD revenues) |

| Projected 3–6M Upside | 20–35% |

In a market dominated by banks and commodity plays, Systems Limited stands apart as Pakistan’s premier technology exporter — and arguably the most underappreciated growth story on the entire PSX. SYS earns a significant portion of its revenues in US dollars through software development and IT services exports to North American and European clients, giving it a natural hedge against any rupee weakness. That’s a quality you won’t find in any bank or cement stock.

Pakistan’s IT sector has been one of the standout performers of the country’s post-stabilization recovery. IT exports have been growing at double-digit rates, supported by a young, tech-literate workforce and government incentives for digital exporters. Systems Limited — as the sector’s largest listed player — is the most direct proxy for this theme. Its consulting and enterprise software capabilities put it in competition with Indian IT firms, but at a fraction of the valuation multiples that peers like Infosys or Wipro command in Mumbai.

For investors seeking high return PSX stocks 2026 with a growth rather than value orientation, SYS is the standout pick. As highlighted by Seeking Alpha’s emerging markets coverage, Pakistani IT exporters represent one of the most compelling frontier market tech plays globally right now.

✅ Key Strengths

- USD-denominated revenues — natural currency hedge

- Sector tailwind: Pakistan IT exports growing 20%+ annually

- Trades at discount to regional IT peer multiples

- AI/digital transformation demand drives enterprise software growth

⚠️ Key Risks

- Higher valuation multiples than PSX peers — growth must deliver

- Brain drain / talent retention is a sector-wide challenge

- Geopolitical uncertainty can affect client confidence in offshore work

↑ Projected 3–6 Month Upside: 20–35%

10. LUCK — Lucky Cement Limited

PSX: LUCK | Cement / Diversified Manufacturing

| Metric | Value |

|---|---|

| Recent Price | Rs. 475–500 |

| Q3 Net Income | Rs. 22.62B |

| Q2 Net Income | Rs. 21.99B |

| 52-Week Support | Rs. 450–460 |

| Technical Target | Rs. 550–600 |

| Projected 3–6M Upside | 15–25% |

Lucky Cement is not just a cement company — it’s Pakistan’s most formidable industrial conglomerate in the making. Through its parent ICI Pakistan and subsidiaries in power generation, chemicals, and consumer goods, LUCK has quietly diversified beyond the commodity-driven cyclicality of pure-play cement peers. That diversification premium is only now beginning to be recognized by the market.

Quarter-on-quarter earnings growth has been steady and consistent: Q3 net income of Rs. 22.62 billion compared to Rs. 21.99 billion in Q2 signals a business firing on all cylinders. Technical analysts have identified a symmetrical triangle breakout above Rs. 470, pointing toward Rs. 550–600 — the key resistance cluster where LUCK would be testing multi-year highs. The stock is consolidating in the Rs. 480–500 zone, which historically has been a reliable base for the next leg up.

LUCK’s competitive advantage over FCCL lies in scale, geographic diversification (it exports cement to Afghanistan and Iraq), and subsidiary-driven earnings diversification. It is the higher-quality, larger-cap choice in the cement sector, suitable for investors who want cement exposure with a conglomerate safety net. As Bloomberg’s company coverage has noted, diversified industrials in frontier markets tend to outperform single-sector peers during economic recovery cycles.

✅ Key Strengths

- Diversified conglomerate structure beyond pure cement

- Export revenues from Afghanistan/Iraq add FX diversification

- Consistent Q-o-Q earnings growth — Rs. 22.62B in Q3

- Technical breakout above Rs. 470 targets Rs. 550–600

⚠️ Key Risks

- Higher price point (Rs. 475–500) limits value argument vs. FCCL

- Regional export markets (Afghanistan) carry geopolitical risk

- Low dividend yield (0.84%) — pure capital gain play

↑ Projected 3–6 Month Upside: 15–25% | Target: Rs. 555–600

💡 Investment Tips: How to Play PSX for Quick Returns in 2026

Pakistan’s economic recovery is real, data-backed, and still early in its equity market re-rating cycle. But “quick returns” in emerging markets require discipline as much as conviction. Here’s how to approach these top 10 PSX picks intelligently:

- Position Sizing: No single stock should represent more than 10–15% of a portfolio allocated to PSX. High-beta plays like PPL and UBL should be sized more conservatively.

- Earnings Catalysts: HBL (Feb 19), UBL (Feb 25), and FCCL (Feb 25) all have imminent earnings releases. Consider entering before announcements with tight stop-losses.

- Sector Balance: Combine banking stocks (UBL, MCB, MEBL, HBL) with energy (PPL, PSO) and diversified exposure (SYS, MTL, LUCK, FCCL) for a robust short-term PSX portfolio.

- Rate Cycle Awareness: The SBP’s rate-cutting trajectory is a tailwind for equities broadly, but watch the pace — faster-than-expected cuts could squeeze bank NIM and require portfolio rebalancing.

- Technical Entry Points: For momentum traders, confirm entries with volume. UBL’s Rs. 455–465 zone and PPL’s Rs. 255–265 support are high-probability entry bands based on February 2026 data.

- PSO as a Conviction Play: With 7/7 analysts rating it Strong Buy and 38% upside to consensus, PSO is the highest-conviction call in this list for patient investors willing to wait 3–6 months for circular debt resolution catalysts.

- SYS for Growth Seekers: If you’re a growth investor comfortable with technology sector dynamics, SYS offers the only USD-revenue hedge in this list — an underappreciated quality in a PKR-denominated market.

⚠️ Important Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. Stock prices, P/E ratios, and projected returns cited reflect data available in mid-February 2026 and are subject to change. Past performance — including 1-year returns cited for UBL (+121%), MEBL (+104%), and others — does not guarantee future results. Investing in equity markets involves risk, including the possible loss of principal. Always consult a licensed financial advisor, stockbroker, or wealth manager before making any investment decisions. The Pakistan Stock Exchange is an emerging market subject to heightened volatility, regulatory changes, and macroeconomic risks.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

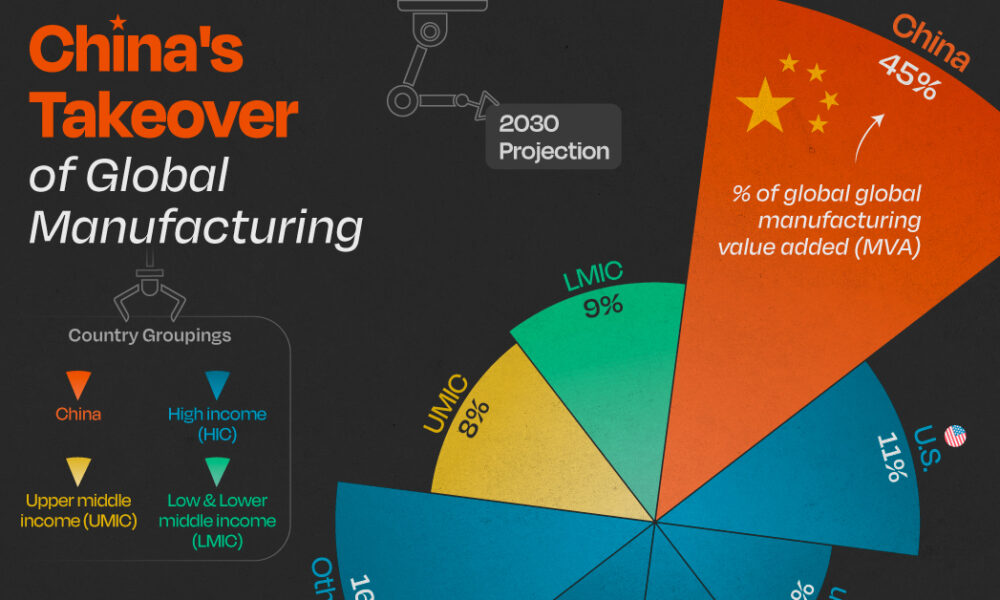

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Asia6 months ago

Asia6 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech