Analysis

Tarique Rahman’s Plan to Revive Bangladesh’s Economy: Challenges and Opportunities in 2026

Explore how Bangladesh’s new PM Tarique Rahman aims to boost GDP growth, manage remittances, and navigate China-US relations amid post-election revival.

When Tarique Rahman finally set foot on Bangladeshi soil after nearly two decades in London exile, the crowds that greeted him weren’t merely celebrating a political homecoming. They were, in a very real sense, betting their livelihoods on him. The BNP’s sweeping two-thirds majority in February 2026 — an election made possible only by the extraordinary student-led uprising that drove Sheikh Hasina from power in 2024 — handed Rahman a mandate that is simultaneously historic and terrifying in its weight. Bangladesh’s GDP stands at roughly $460 billion, growth has decelerated to a sluggish 4%, and a geopolitical tightrope stretches in every direction. The question isn’t whether Rahman wants to revive Bangladesh’s economy. The question is whether the tools he has are equal to the task.

The Economic Inheritance: More Fragile Than It Looks

Bangladesh’s macro story has long been one of development economics’ favorite fairy tales — a low-income country that outpaced neighbors through garment exports, microfinance, and disciplined remittance flows. That story has grown considerably more complicated.

The IMF projects GDP growth to rebound to 4.7% in FY2026, a modest recovery from the post-Hasina political turbulence that rattled investor confidence in late 2024 and through 2025. But 4.7% is not the 6–7% Bangladesh needs to absorb its vast young workforce, reduce poverty meaningfully, or finance the public investment that decades of cronyism left underfunded. The structural gaps are significant: private investment hovers well below the 35% of GDP economists identify as necessary for sustained high growth. Public institutions — tax administration, the judiciary, anti-corruption bodies — carry the scars of 15 years of systematic politicization.

Agriculture still employs roughly 44% of the workforce, a share that underscores both the rural depth of economic vulnerability and the limits of an export-led model that has concentrated prosperity in Dhaka and Chittagong. When a cyclone hits the Sundarbans or global cotton prices spike, nearly half the country feels it in their bones.

Then there’s the remittance lifeline. Bangladeshis abroad sent home $30 billion in 2025 — a remarkable surge driven partly by the depreciation of the taka making dollar transfers more attractive, and partly by the expanded diaspora built up across the Gulf, Malaysia, and Europe. Remittances now rival garment export earnings as the backbone of foreign exchange reserves. That’s a double-edged asset: invaluable as a buffer, but structurally fragile because it depends on labor-market conditions in Riyadh and Dubai, not Dhaka.

The Garment Sector: A Crown Jewel Under Pressure

Bangladesh’s readymade garment industry — a $40+ billion export engine that dresses much of the Western world — faces its most complex moment in a generation. The challenges are formidable: automation threatens lower-skill sewing jobs, Western buyers are demanding ESG compliance that many Bangladeshi factories can’t yet afford, and competitors from Vietnam and Ethiopia are chipping away at market share.

US tariff policy adds another layer of uncertainty. Bangladesh’s garment exports to America — its single largest market — flow under preferences that have never been fully secure and are now subject to the broader unpredictability of Washington’s trade posture. Rahman’s government has signaled it will pursue a formal trade framework with the US, a pragmatic move that would reduce vulnerability but requires diplomatic capital Bangladesh is only beginning to rebuild.

The harder domestic challenge is labor. The 2024 revolution was partly ignited by garment workers and students united by economic grievance. Any BNP government that ignores wage stagnation in the sector risks repeating the political miscalculations that ultimately doomed Hasina. Rahman has spoken of a “social compact” with workers — the test will be whether that translates into enforceable minimum wages and functional unions, or remains campaign rhetoric.

Navigating the Great Power Triangle: China, the US, and India

China: Partner, Creditor, or Competitor?

Bangladesh’s trade relationship with China is the defining economic relationship most Western analysts underestimate. Bilateral trade runs at approximately $18 billion, overwhelmingly weighted toward Chinese exports — machinery, raw materials, electronics — that Bangladesh’s industry desperately needs but can’t yet produce domestically. Chinese firms have also financed key infrastructure, from the Padma Bridge rail link to power plants, creating debt obligations that constrain fiscal flexibility.

Rahman’s stated approach is “multipolar pragmatism” — maintaining strong economic ties with Beijing while signaling openness to Washington and Tokyo. It’s a reasonable strategy, and it reflects a broader trend across Southeast and South Asia. But it requires a diplomatic dexterity that Bangladesh’s foreign ministry has not traditionally needed to exercise. The risk is that both great powers interpret hedging as hostility rather than prudence.

The India Question: Thaw or Freeze?

Relations with India are the most emotionally charged variable in Rahman’s foreign policy inbox. New Delhi was perceived as Hasina’s patron — a relationship Bangladeshi nationalists resented and the BNP stoked for electoral advantage. Border tensions have flared since the revolution, with incidents along the fencing that runs most of the 4,000-kilometer frontier. The Teesta water-sharing agreement, long in diplomatic limbo, remains unsigned.

And yet the economics of India-Bangladesh interdependence are powerful enough to compel engagement regardless of political temperature. Indian goods flood Bangladeshi markets via both formal and informal channels. Bangladesh’s northeast-facing connectivity — ports, power grids, transit routes — cannot be optimized without Indian cooperation. A sustained chill with Delhi would cost Rahman more than it costs Modi. The smart money is on a gradual, face-saving thaw: enough symbolism to satisfy nationalist sentiment at home, enough pragmatism to keep the border economy functioning.

ASEAN: The Aspiration That Requires Homework

Bangladesh’s ASEAN aspirations have been discussed for years with more enthusiasm than strategy. Joining ASEAN — even as a dialogue partner — would require institutional reforms, trade liberalization, and a regional diplomatic posture that Dhaka has not historically prioritized. Rahman’s team has floated ASEAN engagement as part of a broader Indo-Pacific pivot. It’s an appealing vision. Translating it into policy requires, first, getting the basics right at home.

The Political Economy of Reform: Who’s Really in the Room?

Any honest assessment of Bangladesh’s economic outlook has to grapple with the coalition Rahman is governing within. The BNP’s two-thirds majority is a powerful instrument — but it came partly on the back of Jamaat-e-Islami’s organizational muscle in constituencies where the BNP had been weakened during the Hasina years. Jamaat’s social conservatism and ambiguous attitude toward Bangladesh’s secular liberal elite creates real tension with the reform agenda that investors and multilaterals are expecting.

Youth are the other critical constituency. The students who brought down Hasina want jobs — real ones, not patronage positions — transparency, and an end to the culture of political violence that has made Bangladeshi politics so costly to its own institutions. Rahman’s government has promised a crackdown on corruption and civil service reform. These are not merely good governance talking points; they are the precondition for private investment to grow toward that 35% of GDP target. Foreign capital follows institutional credibility, and Bangladesh’s institutional credibility is currently being rebuilt from a low base.

The Awami League, despite its electoral collapse, commands deep roots in parts of the bureaucracy, the military officer class, and civil society. A wise BNP government manages this not through purges — which historically backfire — but through transparent accountability processes that don’t look like victors’ justice.

LDC Graduation: The November 2026 Cliff

Looming over everything is Bangladesh’s scheduled graduation from Least Developed Country status in November 2026. This is, in development terms, a success story — Bangladesh has met the income, human assets, and economic vulnerability thresholds for graduation. But success brings a cost: the erosion of preferential trade terms that have underpinned garment export competitiveness for decades.

Duty-free access to the EU under the Everything But Arms initiative will phase out. WTO-TRIPS flexibilities on pharmaceuticals will tighten. The IMF and World Bank have urged Bangladesh to negotiate transition arrangements and diversify its export base before the preferences expire. Rahman’s government has approximately two years of post-graduation transition runway — time that must be used to move up the value chain, attract technology-intensive investment, and build the trade infrastructure that makes Bangladeshi exports competitive on merit rather than preference.

This is where the $460 billion economy’s future is genuinely being written. Not in political speeches, but in whether Chittagong port gets the upgrades it needs, whether the power grid can reliably supply the industrial zones, and whether the education system starts producing graduates with skills the 21st-century economy demands rather than the 20th.

Opportunities and Pitfalls: A Forward Look

Where the optimists have a point:

- The remittance surge provides a genuine foreign exchange cushion that buys reform time.

- Bangladesh’s demographic dividend — a young, urbanizing population — is a real asset if youth employment programs gain traction.

- The global supply chain diversification away from China creates an opening for Bangladesh in electronics and light manufacturing if the enabling environment improves.

- The BNP’s large majority, paradoxically, gives Rahman room to absorb short-term political pain from reform — a luxury narrow coalition governments rarely have.

Where the pessimists may be right:

- Jamaat-e-Islami’s influence in the coalition could slow liberal economic reforms and deter Western investors with ESG mandates.

- India-Bangladesh tensions, if they deepen, could disrupt the connectivity projects that unlock northeastern Bangladesh’s economic potential.

- LDC graduation without adequate preparation could trigger a garment sector shock that reverberates across the 4 million workers — mostly women — who depend on it.

- Institutional rebuilding takes longer than election cycles. The IMF’s 4.7% projection is predicated on policy continuity and reform progress that is far from guaranteed.

The Bottom Line

Tarique Rahman inherits a Bangladesh that is more resilient than its critics acknowledge and more fragile than its boosters admit. The $460 billion economy has real foundations — a hardworking diaspora, an adaptable garment sector, a tradition of pragmatic policymaking that survived even the Hasina years’ worst excesses. But those foundations need serious maintenance: institutional reform, investment in human capital, and a foreign policy sophisticated enough to manage great power competition without becoming a casualty of it.

The students who made this government possible are watching with the same energy they brought to the streets in 2024. They are not an audience to be managed with press releases. They are Bangladesh’s most important economic asset — and its most demanding constituency. Getting the economy right, for Rahman, is not just a technocratic challenge. It’s the condition of his political survival, and the measure by which history will judge whether the 2024 revolution delivered on its promise.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

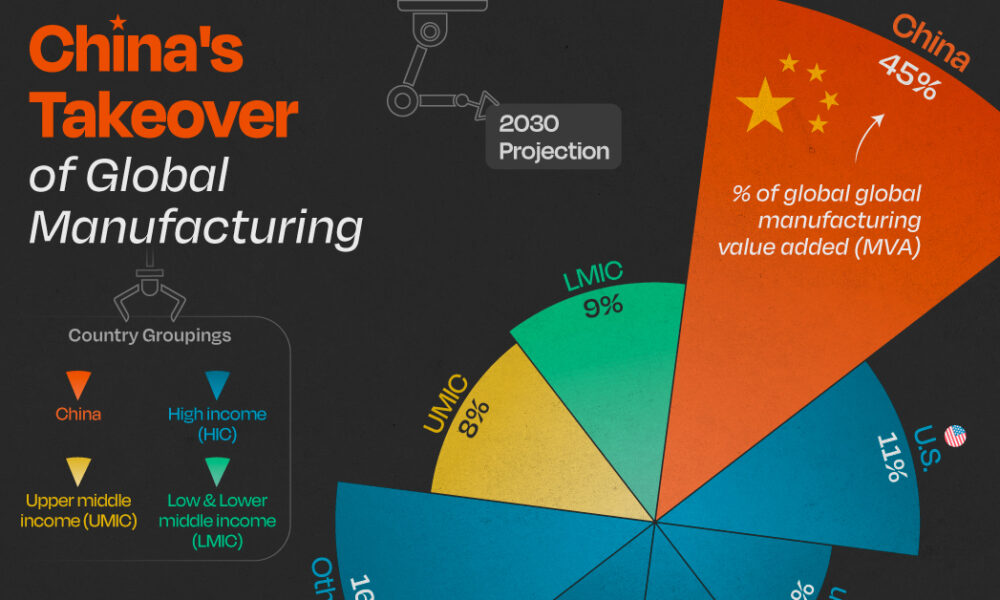

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Bank Indonesia Rate Hike 2026: New Mandate’s First Market Test

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025