Human Resourcs

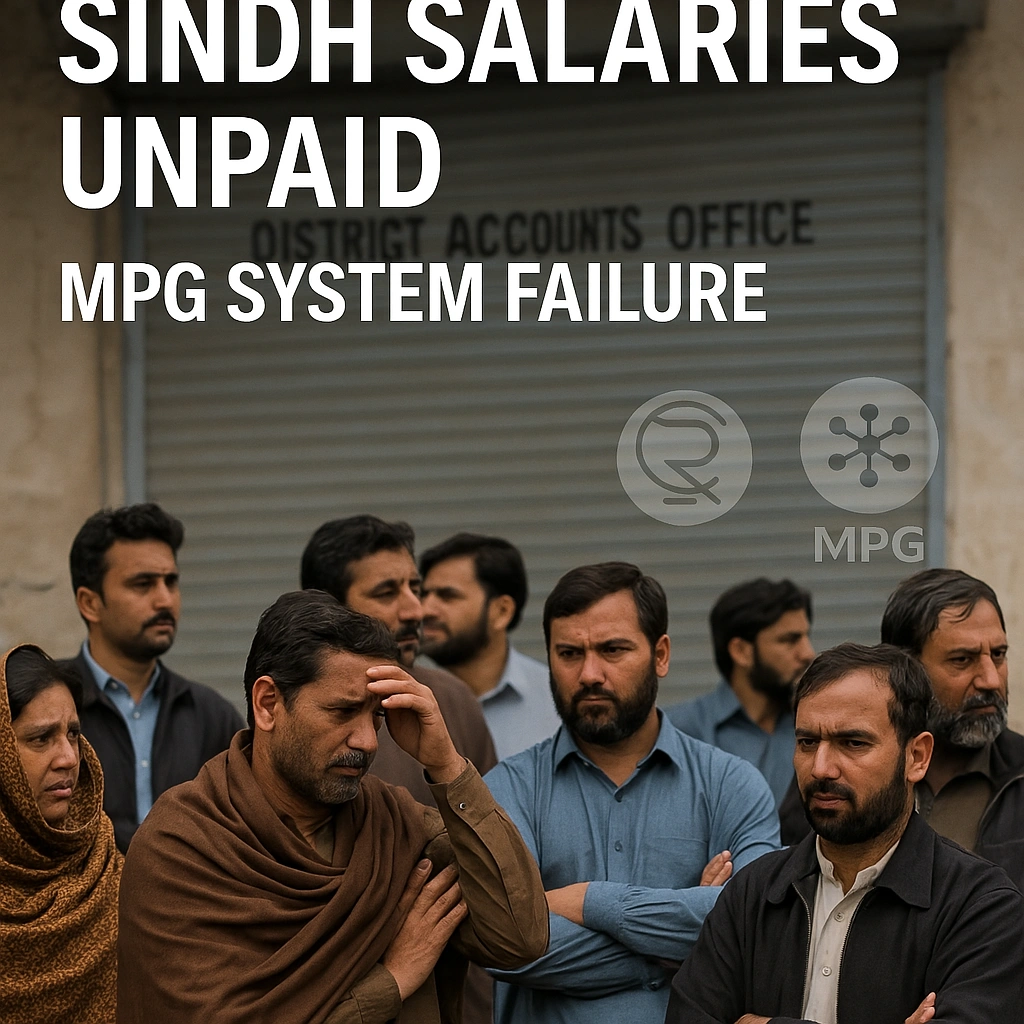

Sindh’s Payroll Crisis: How a Digital Payment System Collapse Left Thousands of Government Employees Without January Salaries

Sindh government employees remain unpaid as MPG payment system fails past January 25th deadline. Exclusive investigation into Pakistan’s digital payment infrastructure breakdown and its human cost.

“The 25th Has Come and Gone—But Salaries Haven’t“

For Muhammad Rasheed, a grade-17 officer in Sindh’s education department, January 28th marks the third day of uncertainty. The 25th—traditionally the day when government salaries illuminate bank accounts across Pakistan—passed without the familiar notification ping. His children’s school fees are overdue. His wife postponed a medical appointment. And like thousands of civil servants across Sindh province, he’s caught in the crossfire of what experts are calling Pakistan’s most significant digital payment system failure in recent memory.

The culprit? The Micro Payment Gateway (MPG), a digital disbursement platform that was supposed to modernize how Sindh pays its 400,000-plus government employees. Instead, it has created a humanitarian and administrative crisis that exposes the fragility of Pakistan’s rush toward digitalization without adequate safeguards.

According to sources within the Accountant General (AG) Sindh office who spoke on condition of anonymity, the system experienced “catastrophic failures” in processing the January 2026 payroll, leaving employees—from junior clerks to senior administrators—in financial limbo. This isn’t merely a technical glitch; it’s a case study in how premature digital transformation can collapse under its own weight.

Understanding the MPG Debacle: What Went Wrong?

The Promise of Digital Transformation

Pakistan’s State Bank of Pakistan (SBP) has been aggressively promoting digital payment infrastructure, including the Raast instant payment system, as part of its National Financial Inclusion Strategy. The MPG was envisioned as Sindh’s answer to efficient, transparent salary disbursement—eliminating intermediaries, reducing corruption, and ensuring timely payments.

The Washington Post recently highlighted Pakistan’s digital ambitions in its Asia economic coverage, noting that “emerging markets face unique challenges in digital payment adoption“—a prescient observation given Sindh’s current predicament.

The Reality: A System Unraveling

Multiple technical failures have compounded since late 2025:

District-Level Breakdowns

- Badin District: Complete payroll processing failure affecting 8,000+ employees

- Dadu District: Partial disbursements with unexplained deductions

- Ghotki District: System rejecting employee bank account validations

Sources indicate the MPG’s integration with the Controller General of Accounts Pakistan (CGA) database encountered synchronization errors, particularly affecting employees receiving the Salaries through MPG .

“The system wasn’t stress-tested for scale,” explains Dr. Ayesha Malik, a digital governance expert at Lahore University of Management Sciences. “When you’re processing 400,000 salaries simultaneously, any latency in API calls or database queries creates cascading failures.”

The Federal-Provincial Divide

The crisis highlights a disturbing disparity. Federal government employees in Islamabad received January salaries on schedule through the tried-and-tested systems managed by the Controller General of Accounts. Punjab province, which piloted a hybrid digital-manual approach, reported 99% on-time disbursement according to data tracked by governance monitoring organizations.

Sindh stands alone in its comprehensive failure—a province that accounts for approximately 22% of Pakistan’s GDP but now cannot pay its own workforce.

The Human Toll: Beyond Statistics and Systems

Stories From the Frontlines

Khadija Bibi, Grade 9 Clerk, Health Department, Hyderabad: “I couldn’t pay my electricity bill. When I went to the school to explain why I couldn’t pay my daughter’s fees, I felt humiliated. They know I’m a government employee. They think I’m making excuses.”

Rashid Ahmed, Grade 16 Officer, Irrigation Department, Sukkur: “We took out high-interest private loans just to buy groceries. The irony? I work in a department that manages water resources for millions, but I can’t manage my own household expenses.”

These aren’t isolated incidents. According to preliminary surveys by civil servant unions, approximately 68% of affected employees have resorted to informal borrowing, often at predatory interest rates exceeding 15% monthly.

The Economist’s recent analysis of emerging market labor dynamics noted that “government employment in South Asia functions as both economic stimulus and social safety net”—making salary delays not just administrative failures but potential triggers for broader economic disruption.

Pension Paralysis

The crisis extends beyond active employees. Thousands of retirees dependent on monthly pensions face similar uncertainty. For many elderly recipients without alternative income sources, this represents an existential threat.

“My father served 35 years in the judiciary,” shares Maryam Khan, daughter of a retired civil judge. “His pension hasn’t come through. He has diabetes medication to buy. This is how we treat our retired public servants?”

Administrative Autopsy: Who’s Accountable?

The Blame Cascade

AG Sindh Office: Claims the State Bank of Pakistan infrastructure experienced “unexpected downtime” during critical processing windows.

State Bank of Pakistan: Points to incomplete data submission from provincial authorities and “non-standard file formats” that violated integration protocols.

Provincial Finance Department: Suggests the Controller General of Accounts delayed authorization for January disbursements due to “budgetary reconciliation issues.”

This circular blame game reveals a fundamental problem: no single entity owns the end-to-end payment process. The MPG system exists in a bureaucratic no-man’s-land where technical failures become administrative hot potatoes.

The Reversion Rumors

Multiple sources confirm that senior Sindh government officials have discussed reverting to manual salary disbursement processes—essentially abandoning the MPG experiment. However, this creates its own complications:

- Data Migration Challenges: Employee records have been partially migrated to the digital system

- Timeline Concerns: Manual processing for 400,000+ employees could take 3-4 business days

- Political Optics: Admitting digital transformation failure before upcoming elections

Financial Times’ coverage of government technology implementations in developing economies warns that “premature abandonment of digital systems after initial failures can create worse long-term outcomes than temporary persistence with fixes”—a dilemma Sindh now faces.

Key Takeaways

- 400,000+ Sindh government employees haven’t received January 2026 salaries due to MPG system failure or Deliberate apathy of Accounts Offices .

- District-level breakdowns in Badin, Dadu,Kashmore and Ghotki compound the crisis

- Federal and Punjab governments disbursed salaries on time, highlighting Sindh’s unique failure

- 68% of affected employees have resorted to high-interest informal borrowing

- Reversion to manual systems being considered but faces logistical and political obstacles

- Broader implications for Pakistan’s digital transformation credibility and economic stability

Comparative Analysis: Lessons From Other Provinces

Punjab’s Hybrid Success

Punjab province implemented a gradual digital transition:

- Pilot program with 10,000 employees (6 months)

- Parallel manual and digital processing (12 months)

- Full digital transition only after 98% success rate achieved

Result? Zero salary delays in the past 18 months.

Federal Government’s Conservative Approach

The federal establishment maintains legacy systems with incremental digital enhancements—prioritizing reliability over innovation. While less efficient, this approach has delivered 100% on-time salary disbursement for 47 consecutive months.

Forbes recently profiled successful government digital transformations in Asia-Pacific, emphasizing that “speed of implementation matters far less than thoroughness of testing and redundancy planning”—wisdom Sindh appears to have ignored.

Broader Implications: Pakistan’s Digital Governance Crossroads

The Credibility Crisis

This failure undermines Pakistan’s broader digital transformation initiatives:

- Raast Payment System Adoption: Banks report declining merchant confidence in government-backed digital platforms

- Tax Digitalization: Concerns about FBR’s planned e-filing mandate

- E-Governance Projects: Provincial governments reconsidering aggressive digital timelines

“One high-profile failure creates systemic skepticism,” notes Farhan Mahmood, a Karachi-based technology governance consultant. “It takes years to rebuild trust in digital government systems.”

The Economic Ripple Effect

When 400,000+ government employees lack purchasing power:

- Local Commerce Disruption: Retailers in government employment hubs (Karachi, Hyderabad, Sukkur) report 30-40% sales declines

- Informal Lending Surge: Private money lenders report unprecedented demand

- Household Debt Accumulation: Long-term financial vulnerability for civil servant families

The Washington Post’s economics desk has documented how public sector salary disruptions in developing economies create “multiplier effects that reduce GDP by 0.3-0.5% quarterly”—a potential scenario for Sindh if delays persist.

The Path Forward: Five Critical Interventions

1. Emergency Manual Disbursement

Activate legacy systems immediately for critical-need employees (grades 1-11, pensioners, medical emergencies) while debugging MPG infrastructure.

2. Independent Technical Audit

Engage international payment system auditors (similar to those used by State Bank of Pakistan for Raast system validation) to identify root causes and recommend fixes.

3. Transparent Communication Protocol

Establish daily public updates on resolution progress—reducing anxiety and rumor circulation among affected employees.

4. Compensatory Measures

Consider:

- Interest-free advance salary loans through government banks

- Automatic reversal of late payment penalties for employee bills

- Hardship grants for lowest-grade employees

5. Accountability Framework

Commission a formal inquiry with public hearings—not for political theater, but genuine systemic learning. The Economist’s governance research emphasizes that “administrative failures require institutional accountability, not individual scapegoating” to prevent recurrence.

Conclusion: A Cautionary Tale for Digital Governance

The Sindh MPG payment system failure represents more than delayed salaries—it’s a referendum on how governments approach digital transformation in resource-constrained environments. The rush to appear technologically progressive, without adequate testing, redundancy planning, and stakeholder preparation, has created precisely the crisis digitalization was meant to prevent.

For Muhammad Rasheed and hundreds of thousands like him, the promise of efficiency has yielded only uncertainty. For Pakistan’s digital governance ambitions, this is a watershed moment: either a catalyst for genuine reform, or the beginning of a retreat to comfortable but inefficient status quo.

The next 72 hours will determine which path employees go for rights . Still no updates for salaries

As Financial Times noted in its recent analysis of emerging market governance challenges: “Technology is only as good as the systems that implement it, and the people who depend on it.” Sindh’s 400,000 government employees are now the unwilling test subjects of that axiom.

The question remains: Will anyone be held accountable before the February salary cycle begins?

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

SkillsFuture funding reforms signal a strategic pivot toward industry-led upskilling—but at what cost to smaller providers and self-funded learners?

On a humid afternoon in December, Melissa Tan sat in her Jurong West training center watching enrollment numbers tick downward on her computer screen. After fourteen years running a mid-sized vocational training provider, she had weathered economic downturns, policy shifts, and the digitization of Singapore’s workforce. But the new SkillsFuture funding guidelines announced by SkillsFuture Singapore (SSG) in late January felt different. “We’ve built our reputation on serving individuals who want to pivot careers on their own initiative,” she explained over coffee. “Now we need forty percent of our students to be employer-sponsored. That’s a complete business model transformation.”

Tan’s predicament illustrates the complex trade-offs embedded in Singapore’s latest recalibration of its decade-old SkillsFuture initiative. Effective December 31, 2025, SSG has imposed substantially tighter funding criteria on approximately 9,500 training courses across 500 providers—requirements that privilege employer-driven training over individual initiative, data-validated skills over experimental offerings, and quantifiable outcomes over pedagogical innovation. The reforms arrive at a moment when Singapore’s small, open economy faces mounting pressure from technological disruption, an aging workforce, and intensifying regional competition for talent and capital.

The policy shift represents more than administrative housekeeping. It embodies a fundamental question confronting advanced economies worldwide: How do governments balance the democratization of lifelong learning with the imperative to channel scarce public resources toward demonstrable economic returns?

The Mechanics of Tightening

The new guidelines affect what SSG terms “Tier 2” courses—those developing currently demanded skills for workers’ existing roles or professions. (They explicitly exclude SkillsFuture Series courses focused on emerging skills, or career transition programs like Institute of Higher Learning qualifications.) The changes impose three primary gatekeeping mechanisms:

Course approval: Prospective courses must now demonstrate alignment with either (1) skills appearing on SSG’s newly released Course Approval Skills List, derived from data science analysis of job market trends, or (2) documented evidence of industry demand through endorsement from designated government agencies or professional bodies. This represents a marked departure from the previous approach, which permitted a broader range of training offerings to access public subsidies.

Funding renewal threshold: From December 31, 2025 onward, courses seeking to renew their two-year funding cycle must demonstrate that at least 40 percent of enrollments came from employer-sponsored participants. This metric directly measures whether training aligns with enterprise workforce development priorities rather than individual hobbyist pursuits.

Quality survey compliance: Beginning June 1, 2026, courses must achieve a minimum 75 percent response rate on post-training quality surveys, with ratings above the lower quartile. This mechanism aims to eliminate providers who deliver mediocre experiences while gaming enrollment numbers.

A transitional framework softens the immediate impact. Between December 31, 2025 and June 30, 2027, selected course types—including standalone offerings from institutes of higher learning, courses leading to Workforce Skills Qualification Statements of Attainment, and certain other categories—receive a one-year grace period if they fail the 40 percent employer-sponsorship threshold. But the reprieve is temporary; from July 1, 2027, all Tier 2 courses must meet the full criteria.

The Economic Logic: Aligning Supply with Demand

The rationale behind these reforms emerges clearly when viewed against Singapore’s macroeconomic imperatives and recent labor market data. According to SSG’s 2025 Skills Trends analysis, demand for AI-related competencies has surged across industries, with skills like “Generative AI Principles and Applications” experiencing the fastest growth in job postings data. Simultaneously, green economy skills—sustainability management, carbon footprint assessment—and care economy capabilities have gained prominence as Singapore pursues its Green Plan 2030 and grapples with demographic aging.

Yet training providers, responding to consumer demand rather than labor market signals, have often proliferated courses in saturated or declining sectors. The mismatch represents a classic market failure: individual learners, lacking perfect information about employment prospects, gravitate toward familiar or fashionable topics rather than areas of genuine skills shortage. Training providers, incentivized to maximize enrollment volumes, oblige. Public subsidies then inadvertently subsidize this misalignment.

The 40 percent employer-sponsorship requirement cleverly leverages employers’ superior information about workforce needs. Companies investing real money in their employees’ training create a demand-side filter that SSG believes will naturally favor courses addressing actual productivity gaps. “Employers vote with their wallets,” one SSG official noted at the January 27 Training and Adult Education Conference announcing the changes. “If a course can’t attract employer sponsorship, we need to ask whether it’s truly addressing labor market needs.”

From a public finance perspective, the logic is straightforward. Singapore, despite its fiscal strength, operates under self-imposed constraints: a balanced budget requirement, limited borrowing for current spending, and a cultural aversion to expansive welfare states. SkillsFuture expenditures have grown substantially since the program’s 2015 launch—Singaporeans aged 25 and above have collectively claimed over S$1 billion in SkillsFuture Credits, with enhanced subsidies for mid-career workers (aged 40-plus) adding further fiscal pressure. Ensuring these outlays generate measurable employment and productivity outcomes becomes imperative as the government contemplates longer-term structural challenges: an aging society requiring expanded healthcare spending, investments in digital infrastructure and green transition, and resilience measures against external economic shocks.

Global Context: Singapore’s Experiment in Comparative Relief

To appreciate the boldness of Singapore’s approach, consider its divergence from other advanced economies’ lifelong learning models. Denmark’s flexicurity system combines generous unemployment benefits with extensive active labor market policies, including subsidized adult education. But Denmark can afford this largesse through high taxation (total government revenue exceeds 46 percent of GDP, versus Singapore’s 20 percent) and a homogeneous, highly unionized workforce. South Korea’s K-Digital Training initiative, launched in 2020, channels subsidies toward digital skills bootcamps—but targets primarily youth and unemployed workers, not the broader workforce Singapore aims to reach.

France’s Compte Personnel de Formation (CPF) offers perhaps the closest parallel: a portable training account funded through payroll levies, giving workers autonomy over skill development. Yet France’s system has faced criticism for fraud, low-quality providers gaming the system, and inadequate alignment with labor market needs—precisely the pathologies Singapore’s reforms seek to preempt. A 2021 report in The Economist examining retraining programs across OECD countries found that success correlated strongly with employer involvement and labor market relevance, rather than mere accessibility.

Singapore’s model occupies a distinctive middle ground: universal entitlements (every citizen aged 25-plus receives credits), but channeled through market mechanisms and employer validation. The SkillsFuture reforms effectively tighten the alignment mechanism without abandoning the universalist principle—a pragmatic compromise characteristic of Singapore’s technocratic governance style.

The Squeeze on Training Providers: Winners and Losers

The employer-sponsorship threshold creates clear winners and losers among training providers. Large, established players with existing corporate relationships—polytechnics, ITE, private training centers serving multinational corporations—possess natural advantages. They can leverage long-standing contracts, industry advisory boards, and placement track records to attract employer-sponsored enrollments.

Smaller providers face steeper challenges. Many built their businesses serving self-funded mid-career professionals seeking new skills or side ventures—precisely the demographic segment the reforms indirectly penalize. “We’ve invested heavily in emerging areas like blockchain development and sustainability consulting,” explained one boutique training center director who requested anonymity. “These are forward-looking skills, but companies aren’t yet sponsoring at scale because the roles barely exist in their organizations. Under the new rules, we’re essentially being told to wait until the demand becomes mainstream—by which point the opportunity has passed.”

The enrolment cap mechanism, while intended to prevent gaming, compounds the squeeze. Courses reaching their enrollment limit before the funding renewal check (six months prior to the end of the two-year validity period) must pass quality checks before accepting additional students. High-demand courses thus face bureaucratic friction at the worst possible moment—when they’ve demonstrated market appeal. Lower-demand courses, by contrast, may never hit enrollment thresholds requiring scrutiny, creating a perverse incentive structure.

Training providers serving niche industries face particular vulnerability. Specialized sectors like maritime law, conservation biology, or heritage preservation generate modest enrollment volumes and limited employer-sponsorship rates (small firms in these fields often lack formal training budgets). Yet these represent precisely the differentiated capabilities that sustain Singapore’s position as a diversified, knowledge-intensive economy beyond the big four sectors (finance, logistics, technology, manufacturing).

Access and Equity: The Self-Funded Learner’s Dilemma

The employer-sponsorship emphasis raises important equity questions. Not all workers enjoy employer-sponsored training opportunities equally. Research by Singapore’s Ministry of Manpower shows that company-sponsored training tends to concentrate among degree-holders, professionals, and employees of large firms. Rank-and-file workers in SMEs, gig economy participants, and those in precarious employment—precisely the groups most vulnerable to technological displacement—face significant barriers.

Consider Raj Kumar, a 47-year-old logistics coordinator whose employer, a small freight forwarding company, lacks a formal training budget. Kumar has used SkillsFuture credits to complete courses in data analytics and digital supply chain management, hoping to transition into a more technology-oriented role. Under the new guidelines, his preferred courses may lose funding eligibility if they fail to attract sufficient employer sponsorship—forcing him to either pay full cost or choose less relevant but better-subsidized alternatives.

Women reentering the workforce after caregiving breaks present another equity concern. These mid-career returners often invest in self-funded retraining to compensate for skills atrophy or career pivots. Employer-sponsorship requirements create a catch-22: they need training to become employable, but courses require employer interest to remain subsidized.

SSG officials argue that alternative pathways remain available—SkillsFuture Career Transition Programs explicitly serve career switchers, and mid-career enhanced subsidies (covering up to 90 percent of course fees for Singaporeans aged 40-plus) continue supporting self-funded learning. But the distinction between “career transition” and “skills upgrading” proves blurry in practice. Many mid-career workers pursue incremental skill acquisition that doesn’t constitute wholesale career change yet enables internal mobility or role evolution. The new framework may inadvertently penalize this gray zone of professional development.

Data-Driven Skill Identification: Promise and Pitfalls

The Course Approval Skills List represents one of SSG’s more innovative elements. Using natural language processing and machine learning algorithms, SSG analyzes job posting data, wage trends, and hiring patterns to identify skills experiencing demand growth. The 2025 Skills Trends report reveals that 71 skills—spanning agile software development, sustainability management, and client communication—demonstrated consistently high demand and transferability across 2022-2024, with trends expected to continue into 2025.

This data-driven approach offers significant advantages over traditional expert panels or industry surveys. It’s faster, more comprehensive, and less subject to lobbying by incumbent industry players. The methodology also permits granular analysis—SSG now tracks not just skill categories but specific applications and tools (Python libraries, ERP systems, design software) required in job roles.

However, data-driven skill identification harbors limitations. Job postings reflect current employer preferences, not future needs. Emerging disciplines—quantum computing applications, circular economy frameworks, AI ethics—may barely register in job posting data until they’ve already achieved critical mass. By then, first-mover advantages have vanished. If training providers can only offer courses on SSG’s approved list, Singapore risks systematically underinvesting in forward-looking capabilities.

The methodology also privileges skills easily described in job postings. Tacit knowledge, soft skills, and creative competencies prove harder to quantify through algorithmic analysis. Yet these capabilities—judgment, cross-cultural communication, ethical reasoning—often determine long-term career success and organizational adaptability. A training ecosystem optimized for algorithmically identifiable skills may inadvertently neglect the human qualities most resistant to automation.

The Broader Stakes: Singapore’s Competitiveness Calculus

The SkillsFuture reforms must be understood within Singapore’s broader economic development strategy. The city-state has staked its future on becoming a hub for advanced manufacturing, digital services, sustainability innovation, and high-value professional services—sectors requiring a workforce that continuously upgrades capabilities. With neighboring countries investing heavily in technical education (Vietnam’s IT workforce, Thailand’s Eastern Economic Corridor initiative) and established hubs like Hong Kong and Seoul competing for similar industries, Singapore cannot afford complacency.

Yet the tightening carries risks. If Singapore’s training ecosystem becomes too employer-driven and algorithmically determined, it may sacrifice the experimental, entrepreneurial energy that has historically fueled its adaptive capacity. Many of Singapore’s successful industry pivots—from petrochemicals to biotech, from port logistics to digital banking—emerged from individuals and organizations pursuing capabilities ahead of obvious market demand.

The reforms also reflect broader tensions in Singapore’s governance model. The technocratic state excels at efficiency, optimization, and resource allocation toward measurable objectives. These strengths propelled Singapore from third-world poverty to first-world prosperity in two generations. But efficiency-maximizing systems can become brittle when confronted with uncertainty and ambiguity. Training that produces clear, quantifiable outcomes in stable domains may underperform when facing discontinuous change or nonlinear technological shifts.

Forward-Looking Implications: What Comes Next

The January 2026 announcement likely represents the opening salvo in a longer recalibration of Singapore’s lifelong learning architecture. Several trends warrant attention:

Increased emphasis on outcomes-based funding: Expect SSG to develop more sophisticated metrics beyond employer sponsorship—wage progression, job placement rates, productivity enhancements. The agency has already signaled interest in tracking post-training employment outcomes. Future iterations may adjust subsidy levels based on demonstrated impact.

Evolution of the Skills List methodology: As SSG refines its algorithmic approaches, the Course Approval Skills List will likely become more dynamic—updated quarterly rather than annually, incorporating leading indicators beyond job postings, and potentially using predictive modeling to anticipate emerging needs.

Differentiated treatment by sector: SSG may recognize that employer-sponsorship patterns differ across industries. Creative sectors, startups, and SME-dominated fields may receive adjusted thresholds or alternative validation mechanisms.

Greater integration with immigration and talent policy: The skills identified through SkillsFuture’s data infrastructure will increasingly inform Singapore’s employment pass criteria, tech.pass requirements, and sectoral talent initiatives. Training subsidies and immigration policy will converge into a unified human capital strategy.

Experimentation with training innovation zones: To preserve space for experimental offerings, Singapore may designate sandbox environments where providers can test new course concepts with lighter regulatory oversight before scaling.

The Danish Comparison: Lessons from Flexicurity

It’s instructive to contrast Singapore’s approach with Denmark’s vaunted flexicurity model, often cited as a gold standard for lifelong learning. Denmark spends approximately 2.5 percent of GDP on active labor market policies, including extensive adult education subsidies. Workers displaced by technological change or trade shocks can access generous retraining programs with income support.

But Denmark’s system operates in a fundamentally different institutional context. High trust between labor unions, employers, and government enables coordinated approaches to workforce adjustment. Collective bargaining determines training priorities. Social insurance funds (financed through high payroll taxes) cushion income shocks during reskilling. Cultural norms around equality and solidarity legitimize substantial transfers to support individual skill development.

Singapore lacks these institutional preconditions. Its tripartite labor relations model (government-union-employer cooperation) provides some coordination, but stops short of Nordic-style corporatism. The country’s fiscal conservatism precludes Danish-level spending. And Singapore’s multicultural, immigrant-heavy society (40 percent of the population are foreign workers or residents) complicates solidarity-based social insurance.

The SkillsFuture reforms implicitly recognize these constraints. Rather than expand public spending, they aim to spend existing resources more strategically. Rather than rely on trust-based coordination, they deploy data analytics and market mechanisms. This represents neither a superior nor inferior model, but an adapted solution to Singapore’s particular constraints.

The Economist’s Verdict: Calculated Risk or Overreach?

From a pure economic efficiency standpoint, the reforms possess clear merits. Channeling training subsidies toward employer-validated, data-confirmed skills should improve returns on public investment. The employer-sponsorship threshold creates skin-in-the-game dynamics that filter out marginal or dubious training offerings. And the quality survey requirements introduce accountability mechanisms previously absent.

Yet efficiency gains come with potential costs. By privileging current labor market demand over forward-looking capability building, Singapore may diminish its adaptive capacity. The employer-sponsorship threshold, while logical, risks excluding individuals in precarious employment or career transition phases. And the centralization of skill identification—however data-driven—concentrates epistemic power in a single agency that, like all institutions, harbors blind spots.

The optimal balance remains elusive. Singapore’s technocratic governance has historically navigated such trade-offs adeptly, adjusting policies as evidence accumulates. The transitional provisions built into the reforms suggest policymakers recognize implementation risks. Whether these safeguards prove sufficient will emerge over the next eighteen months as providers, employers, and individual learners respond to the new incentives.

What This Means for Stakeholders

For employers: The reforms create opportunities to influence training supply by directing sponsorship toward strategically valuable skills. Forward-thinking HR departments should inventory critical competencies, identify skill gaps, and proactively engage training providers to develop relevant curricula. SMEs, often lacking structured training budgets, may face disadvantages unless industry associations or government intermediaries help aggregate demand.

For training providers: Survival requires pivoting toward corporate partnerships and employer-sponsored enrollments. This means investing in business development capabilities, building industry advisory boards, and potentially consolidating to achieve scale. Providers serving niche or emerging fields face particularly acute pressures—they must either find creative ways to demonstrate industry demand or accept exit from the subsidized market.

For individual learners: Self-funded skill development becomes costlier and riskier. Prudent strategies include leveraging Career Transition Programs when making significant pivots, prioritizing employer-sponsored opportunities where available, and focusing SkillsFuture credits on courses appearing on SSG’s approved skills list. Mid-career workers should proactively discuss training needs with employers to access sponsorship.

For policymakers elsewhere: Singapore’s experiment offers lessons beyond its borders. The employer-sponsorship threshold provides a demand-side filter without abandoning universal access—a model potentially applicable in other advanced economies facing similar efficiency-equity trade-offs. The data-driven skills identification methodology, while imperfect, represents an improvement over purely expert-driven approaches. And the transitional framework demonstrates how aggressive policy reforms can incorporate adjustment periods to mitigate disruption.

The Bigger Picture: Singapore’s Perpetual Adaptation

Step back from the technical details, and the SkillsFuture reforms embody a deeper pattern: Singapore’s continuous recalibration in response to shifting circumstances. The 2015 SkillsFuture launch represented an initial bet on individual empowerment and lifelong learning. A decade’s experience has revealed implementation challenges—misaligned incentives, quality concerns, sustainability questions. The 2025-26 reforms adjust the model based on this learning.

This adaptive approach—launching initiatives, monitoring outcomes, adjusting parameters—characterizes Singapore’s developmental trajectory. The country pivoted from entrepôt trade to manufacturing to services to knowledge economy not through prescient master plans, but through iterative experimentation and course correction. The SkillsFuture reforms continue this tradition.

Yet adaptation has limits. Each course correction narrows future options. Path dependencies emerge. The shift toward employer-driven training may prove difficult to reverse if individual-initiative learning atrophies. Data-driven skill identification, once institutionalized, creates constituencies defending existing methodologies. Singapore’s policymakers must balance the need for optimization with preserving optionality.

Conclusion: The Test Ahead

The SkillsFuture funding tightening represents a calculated bet: that aligning training subsidies with employer demand and labor market data will enhance returns on human capital investment without unduly compromising access or innovation. It’s a quintessentially Singaporean solution—technocratic, efficiency-oriented, data-driven, yet wrapped in rhetoric of lifelong learning and social mobility.

Whether the bet pays off depends on execution and adaptation. Will the employer-sponsorship threshold effectively filter quality while preserving access for vulnerable workers? Will the Skills List methodology prove sufficiently forward-looking, or will it systematically underweight emerging capabilities? Will training providers adapt successfully, or will the sector consolidate in ways that reduce diversity and experimentation?

The answers will emerge gradually as the reforms take effect. Melissa Tan, the training provider director pondering her center’s future that humid December afternoon, exemplifies the stakes. Her ability to navigate the new landscape—finding corporate partners, aligning offerings with approved skills, maintaining quality—will determine not just her business survival but the aggregate health of Singapore’s training ecosystem.

For a small, open economy in a volatile world, the quality of that ecosystem matters immensely. Singapore’s prosperity rests not on natural resources or scale, but on its people’s capabilities. As artificial intelligence reshapes work, climate imperatives transform industries, and geopolitical tensions fragment global markets, continuous skill upgrading becomes not a policy choice but an existential imperative.

The SkillsFuture reforms, whatever their shortcomings, recognize this reality. They represent not the final word on lifelong learning policy, but another iteration in Singapore’s ongoing experiment in sustaining adaptability at the national scale. The city-state’s track record suggests it will continue adjusting, learning, and recalibrating as conditions evolve.

That flexibility—the institutional capacity to course-correct without abandoning core commitments—may prove Singapore’s most valuable skill of all.

Sources:

- SkillsFuture Singapore Official Announcement, January 27, 2026

- Skills Demand for the Future Economy Report 2025

- TPGateway SSG Funding Guidelines

- The Economist, “Retraining Low-Skilled Workers,” Special Report, January 2017

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Weather Stations

The Political Economy of Weather Stations: How They Help Mitigate Approaching Disasters

Explore how weather stations and early warning systems deliver 9:1 returns on investment, saving thousands of lives annually—yet remain chronically underfunded amid rising climate disasters and political battles.

When Cyclone Remal barreled toward Bangladesh on May 26, 2024, meteorologists had already tracked its path across the Bay of Bengal for days. The Bangladesh Meteorological Department, drawing on data from three radar stations and satellite feeds from NOAA and Japanese sources, issued warnings that cascaded through government channels, mobile networks, and 76,000 trained volunteers. By the time 400 square kilometers of coastline faced storm surges twelve feet above normal levels, over 4 million people had received early warnings, and 9,424 evacuation centers stood ready. The death toll, though tragic, numbered in the dozens rather than the thousands that similar cyclones once claimed.

Six months earlier and half a world away, the Los Angeles wildfires unfolded under different circumstances. Despite California’s sophisticated meteorological infrastructure, a confluence of severe Santa Ana winds, unprecedented drought conditions, and aging weather monitoring networks created blind spots in forecasting. The fires became the most expensive wildfire in U.S. history, causing over $60 billion in damage.

These contrasting narratives expose a fundamental tension in disaster preparedness: weather stations and early warning systems represent one of humanity’s most cost-effective shields against natural catastrophes, yet they remain chronically underfunded, politically contentious, and unevenly distributed across the globe. As climate change intensifies the frequency and severity of extreme weather, the political economy of meteorological infrastructure has emerged as a critical determinant of who lives and who dies when disaster strikes.

The Architecture of Anticipation: How Weather Stations Enable Disaster Mitigation

At its core, a weather station is deceptively simple—sensors measuring temperature, humidity, wind speed, atmospheric pressure, and precipitation. Yet these modest instruments form the foundation of a sophisticated global architecture that transforms raw atmospheric data into lifesaving intelligence.

Modern early warning systems operate on four interdependent pillars, according to the World Meteorological Organization: risk knowledge, monitoring and warning services, dissemination and communication, and preparedness and response capability. Weather stations anchor the second pillar, providing the real-time observational data that feeds into numerical weather prediction models.

Consider the cascading chain of information that precedes a hurricane warning. Ground-based weather stations across coastal regions continuously transmit data on atmospheric pressure drops and wind speed increases. These measurements integrate with Doppler radar systems—71% of newly commissioned meteorological hubs now use Doppler technology to differentiate particle velocity and storm direction. Satellite observations from geostationary platforms add macro-scale atmospheric imaging. Ocean buoys relay critical information about sea surface temperatures and wave heights.

This multi-source data flows into supercomputers running global circulation models that simulate atmospheric physics with increasing precision. The European Centre for Medium-Range Weather Forecasts and the National Centers for Environmental Prediction crunch millions of observations daily, producing probabilistic forecasts that cascade down to national meteorological services, then to regional offices, and finally to local communities.

The effectiveness of this system depends on data density and quality. Research indicates that just 24 hours of advance warning can reduce storm or heatwave damage by up to 30%. In India’s LANDSLIP project, improved rainfall detection has enabled authorities to collaborate with local NGOs in developing national landslide forecasting, with detection advances allowing warning lead times to improve by up to eight hours in Nepal’s flood-prone regions.

Yet despite these technological capabilities, the system’s weakest link remains its physical infrastructure. Weather stations require consistent maintenance, regular calibration, and continuous power supplies—mundane requirements that become politically fraught when budgets tighten and priorities shift.

The Public Goods Problem: Why Weather Data Is Chronically Underfunded

Weather information exemplifies what economists call a “pure public good”—non-excludable and non-rivalrous. When Bangladesh’s meteorological service issues a cyclone warning, it cannot exclude non-payers from receiving the information, nor does one person’s use of the forecast diminish its availability to others. This creates the classic free-rider problem that plagues public goods provision.

The political consequences manifest starkly in funding debates. In the United States, the Trump administration’s 2026 budget proposal sought to eliminate NOAA’s Office of Oceanic and Atmospheric Research entirely, cut nearly 50% of NASA’s Earth science missions, and reduce overall NOAA spending by $100 million below congressional appropriations. Congress pushed back, but bureaucratic delays have created operational chaos. Multiple regional climate centers shut down in April 2025 when contract reviews stalled, leaving 21 states without crucial drought monitoring and historical temperature data services.

The problem extends beyond partisan politics. NOAA’s Integrated Ocean Observing System, which provides critical data for coastal forecasts through a network of buoys and sensors, has faced chronic underfunding despite bipartisan congressional support. Authorized in 2009 with an independent study recommending $715 million annually, the program has received at most $42.5 million—a level at which it has stagnated for years. As Jake Kritzer of the Northeast Regional Association of Coastal Ocean Observing Systems noted, “Think of it like a car”—aging equipment eventually fails without maintenance, and aging ocean monitoring buoys are beginning to show their limits.

The underfunding creates a perverse dynamic. When disasters strike areas with inadequate early warning systems, the human and economic costs vastly exceed the investment required to prevent them. Yet politically, it’s far easier to secure emergency disaster relief funding after catastrophes than to appropriate money for preventive infrastructure that operates invisibly when successful. As Rick Spinrad, former NOAA administrator, observed regarding congressional funding stabilization efforts: “I’m glad Congress is providing a voice of reason, but real improvement in services will require more than just a stabilization to levels of past investments.”

International cooperation compounds these challenges. The World Meteorological Organization facilitates the exchange of millions of weather observations worldwide daily, underpinning the accuracy of global forecasts. Yet this system depends on all countries maintaining adequate observing networks and sharing data freely—a commitment that strains when nations face budget pressures or perceive meteorological data as commercially valuable.

The Systematic Observations Financing Facility (SOFF) addresses this gap by providing long-term financing and technical assistance to support countries in generating and exchanging basic surface-based observational data. Through peer advisor programs, 20 national meteorological services with strong expertise now offer technical support to 62 beneficiary countries. Yet even these collaborative mechanisms struggle against the fundamental economics: weather infrastructure generates diffuse benefits that accrue to everyone, making concentrated political constituencies for sustained funding difficult to mobilize.

The Cost-Benefit Case: Quantifying the Value of Early Warnings

If public goods problems create political challenges for weather infrastructure funding, the economic evidence for investment remains overwhelmingly compelling. Multiple rigorous studies have demonstrated that early warning systems deliver among the highest returns of any disaster risk reduction measure.

The Global Commission on Adaptation established a cost-benefit ratio of 9:1 for early warning systems—higher than investments in resilient infrastructure or improved dryland agriculture. This means every dollar invested in early warning capability generates an average of nine dollars in net economic benefits. The Commission also found that providing just 24 hours’ notice of an impending storm or heatwave reduces potential damage by 30%, and that an $800 million investment in such systems in developing countries could prevent annual losses of $3 billion to $16 billion.

World Bank research provides even more granular estimates. A 2012 policy research working paper analyzed upgrading hydrometeorological information production and early warning capacity in all developing countries to developed-country standards. The potential benefits include:

- Between $300 million and $2 billion per year in avoided asset losses due to natural disasters through better preparedness and early protection of goods and equipment

- An average of 23,000 saved lives annually, valued between $700 million and $3.5 billion using Copenhagen Consensus guidelines

- Between $3 billion and $30 billion per year in additional economic benefits from optimizing economic activities using weather information (agriculture, energy, transportation, water management)

Total annual benefits reach between $4 billion and $36 billion globally. Because expensive components like earth observation satellites and global weather forecasts already exist, the incremental investment cost is relatively modest—estimated at approximately $1 billion annually, yielding benefit-cost ratios between 4 and 36.

More recent analysis confirms these findings. Ongoing World Bank research estimates that between 1978 and 2018, early warning systems averted $360 billion to $500 billion in asset losses and $600 billion to $825 billion in welfare losses. Universal access to early warning systems could prevent at least $13 billion in asset losses and $22 billion in well-being losses annually.

The benefits extend beyond disaster avoidance. Crop advisory services boost agricultural yields by an estimated $4 billion annually in India and $7.7 billion in China. Research demonstrates that a 1% increase in forecast accuracy results in a 0.34% increase in crop yields. Similarly, fisherfolk earnings optimize when supported by fishing zone advisories that account for changing climate conditions.

Heat warning systems, though less studied, show equally impressive returns. Ahmedabad’s Heat Action Plan averts an estimated 1,190 heat-related deaths annually, while Adelaide’s Heat Health Warning System demonstrates a benefit-cost ratio of 2.0 to 3.3 by reducing heat-related hospital admissions and ambulance callouts.

Perhaps most telling is the mortality differential. Countries with limited to moderate Multi-Hazard Early Warning System coverage have nearly six times higher disaster-related mortality compared to those with substantial to comprehensive coverage—a mortality rate of 4.05 per 100,000 population versus 0.71 per 100,000.

Global Success Stories and Persistent Gaps

Bangladesh stands as the paradigmatic success story in disaster risk reduction through early warning systems. In 1970, Cyclone Bhola killed an estimated 500,000 people. By 2007, when Cyclone Sidr struck with comparable intensity, deaths had fallen to 4,234—a more than 100-fold reduction. This transformation resulted from sustained investment in the Cyclone Preparedness Programme, operated jointly by the government and Bangladesh Red Crescent Society since its approval by Prime Minister Sheikh Mujibur Rahman in the 1970s.

The program now operates through 203 employees and approximately 76,020 volunteers across seven zones, 13 districts, 42 sub-districts, and 3,801 units. When Cyclone Remal approached in May 2024, this network swung into coordinated action. The Bangladesh Meteorological Department tracked the storm using three radar stations in Dhaka, Khepupara, and Cox’s Bazar, supplemented by satellite data from NOAA and Japanese sources. Warnings cascaded through extensive telecommunication networks, mobile alerts, and face-to-face volunteer communications. The result: despite displacing 800,000 people and affecting 4.6 million, the death toll remained minimal thanks to timely evacuations and 9,424 evacuation centers opened by the government.

India has made comparable strides in high-altitude monitoring. Following major glacial lake outburst floods in 2013 and 2023, the National Disaster Management Authority established the National GLOF Risk Mitigation Programme. The program installed solar-powered automatic weather stations at sites more than 5,000 meters above sea level, deployed unmanned aerial vehicles for localized hazard mapping, and created a dynamic risk inventory identifying 195 high-risk glacial lakes among 28,000 in the Himalayas—7,500 within India.

Yet these successes highlight persistent gaps. As of 2024, 108 countries report some early warning capacity—more than double the 2015 level—but this still leaves approximately one-third of the global population without adequate multi-hazard warning systems. The gap concentrates in least developed countries and small island developing states, precisely the regions most vulnerable to climate change impacts.

The Climate Risk and Early Warning Systems (CREWS) initiative has invested over $100 million addressing this disparity in vulnerable nations, while the Systematic Observations Financing Facility provides long-term financing for basic surface-based observational data. The 2022 “Early Warnings for All” initiative, spearheaded by UN Secretary-General António Guterres, aims to provide protection for everyone on Earth by 2027. Yet achieving this target requires accelerating current implementation rates while confronting the political and economic barriers that have historically constrained weather infrastructure investment.

Mozambique illustrates both the potential and the challenges. Cyclone Idai in March 2019 killed over 600 people and caused $3 billion in damages, exposing critical gaps in early warning capabilities. Supported by a $265 million World Bank Disaster Risk Management and Resilience Program, Mozambique developed a comprehensive early warning system using cutting-edge technology. When Cyclone Freddy made landfall in 2023, the improved system demonstrated the life-saving power of preparedness. Yet sustaining these capabilities requires ongoing investment that competes with myriad other development priorities in resource-constrained nations.

Fragile and conflict-affected states face compounded challenges. In Haiti, years of political instability, gang violence, and weak institutions have severely impeded early warning system development despite the country’s acute vulnerability to hurricanes, floods, and earthquakes. In Afghanistan, the World Bank and WMO have pioneered using 3D printing technology to locally produce materials for weather station construction, equipped with solar power to operate in areas with limited electricity access. These innovations demonstrate that technical solutions exist even in extremely difficult contexts, yet they require sustained international support and functional governance structures to operate reliably.

The 2025 Breaking Point: Funding Crises and Political Turbulence

The first half of 2025 represented a watershed for weather infrastructure politics. Climate Central reported that costs associated with catastrophic weather events totaled $101.4 billion—the costliest six-month period on record. The fourteen extreme weather events crossing the billion-dollar threshold included six tornado outbreaks across the Midwest, four severe storms on the East Coast, two severe storms and a hailstorm in Texas, and the Los Angeles wildfires.

Yet as disaster costs soared, weather infrastructure funding faced unprecedented political attacks. The Trump administration’s budget proposals sought to eliminate NOAA’s research arm, cut weather satellite programs, and reduce overall NOAA spending by hundreds of millions below congressional appropriations. While Congress largely rejected these cuts in bipartisan votes—providing $634 million for NOAA’s Office of Oceanic and Atmospheric Research versus the administration’s proposed zero funding—bureaucratic obstruction persisted.

New layers of federal review within the Department of Commerce and Office of Management and Budget delayed critical grant cycles. Secretary of Commerce Howard Lutnick’s requirement for personal sign-off on grants exceeding $100,000 created bottlenecks affecting routine operations. The Integrated Ocean Observing System faced the prospect of funding gaps at the peak of hurricane season. Regional climate centers serving 21 states went dark in April 2025 when contract approvals stalled, eliminating crucial drought monitoring and historical climate data services farmers and researchers depend upon.

The political turbulence extended beyond federal agencies. State-level responses varied dramatically. Arizona created a Workplace Heat Safety Task Force following its 2024 Extreme Heat Preparedness Plan. Connecticut formed a Severe Weather Mitigation and Resiliency Advisory Council and passed legislation requiring communities to account for disaster risks in local planning. Rhode Island enacted the Resilient Rhody Infrastructure Fund for local climate resilience projects. Vermont released its inaugural Resilience Implementation Strategy, though implementing the full strategy would cost approximately $270 million in one-time funds and $95 million annually—sums that remain politically contentious.

Meanwhile, some positive developments emerged internationally. The Severe Weather Forecasting Programme expanded coverage to Central America and early 2025 to Southeastern Asia-Oceania. The Space for Early Warning in Africa project launched as part of the Africa-EU Space Partnership Programme to enhance continental capability for Earth observation services. The Global Observatory for Early Warning Systems Investments, a collaborative platform led by UNDRR and WMO with nine international financial institutions, began consolidating project-level data using a shared classification system.

Yet these initiatives, while valuable, operate against headwinds. The first half of 2025 demonstrated that FEMA’s disaster budget model—relying on historic data rather than future risk predictions—left the agency chronically underfunded. Just eight days into fiscal year 2025, FEMA had spent half its annual disaster budget. This reactive approach means critical relief arrives slower for disaster victims while sending ever-growing bills to taxpayers after the fact, rather than investing proactively in prevention and early warning systems that reduce both human suffering and fiscal costs.

Climate Change: The Accelerating Imperative

The political and economic challenges surrounding weather infrastructure occur against the backdrop of accelerating climate change, which fundamentally alters the risk calculus. Under a 1.5°C warming scenario, average annualized losses could reach 2.4% of GDP. Yet current emissions trajectories point toward higher warming levels, with correspondingly greater impacts.

Extreme weather events are becoming more frequent, more intense, and more costly. The 2024 Atlantic hurricane season saw 27 confirmed billion-dollar weather and climate disaster events in the United States—an average of one every two weeks. This represents not merely bad luck but a structural shift in atmospheric physics as greenhouse gases trap more heat energy, warm ocean surfaces fuel stronger storms, and atmospheric water vapor content increases by approximately 7% per degree Celsius of warming.

These changes stress existing early warning systems in multiple ways. Historical baselines for extreme weather become less reliable as predictors of future events. Compound disasters—where multiple hazards strike simultaneously or in rapid succession, as Bangladesh experienced in 2024 with Cyclone Remal followed by flash floods in the Haor Region, riverine floods in the Jamuna Basin, and devastating flash floods in Chattogram affecting 18 million people—challenge response systems designed for single hazards.

Weather station networks calibrated for historical climate patterns may require recalibration and densification. Radar systems must track more intense precipitation events. Satellite systems need enhanced resolution to capture rapid intensification of tropical cyclones. Flood forecasting models require updates to account for changing hydrological patterns. All of these technical necessities demand sustained investment precisely when political will appears most fragile.

The paradox is acute: climate change simultaneously increases the value of early warning systems and makes sustained funding more politically difficult. As disaster costs mount, emergency response consumes budget capacity that could otherwise support preventive infrastructure. Political polarization around climate science creates headwinds for meteorological agencies perceived as documenting climate change. The temptation to cut “invisible” preventive systems intensifies as immediate disaster response demands escalate.

Yet the alternative—continuing to underfund weather infrastructure while climate risks intensify—represents a catastrophically false economy. Every dollar not invested in early warning systems today translates into multiple dollars in disaster losses tomorrow, along with preventable deaths and suffering.

Toward a Sustainable Political Economy of Weather Infrastructure

Breaking the cycle of underinvestment requires confronting several interconnected challenges. First, the public goods problem demands innovative financing mechanisms that can mobilize sustained resources despite free-rider incentives. The CREWS initiative and SOFF demonstrate that multilateral funding pools can address gaps in vulnerable countries, yet they operate on scales insufficient for global needs.

One promising approach involves hybrid public-private models. The World Economic Forum’s 2025 white paper “Catalysing Business Engagement in Early Warning Systems” calls on governments to incentivize business participation and make meteorological data as accessible as possible. Private sector actors ranging from agriculture to insurance to transportation depend on accurate weather information; mechanisms that capture some of this economic value could supplement public funding.

However, commoditization of weather data creates risks. If basic observational data becomes proprietary rather than freely shared, the global exchange system coordinated by WMO could fragment, reducing forecast accuracy worldwide. The challenge lies in designing systems where private sector contributions supplement rather than substitute for public investment, while preserving the open data sharing that underpins effective early warning systems.

Second, political constituencies for preventive infrastructure need strengthening. Disaster survivors provide powerful testimony, but successful early warning systems operate invisibly—their victories are disasters that don’t occur, deaths that don’t happen, economic losses that don’t materialize. Building political support requires consistently communicating these avoided harms and highlighting the asymmetric returns on investment.

Bangladesh offers instructive lessons. The dramatic mortality reductions from cyclones created political champions for continued investment in the Cyclone Preparedness Programme. When lives saved number in the hundreds of thousands, the political case for sustained funding becomes compelling. Replicating this dynamic in countries without such stark before-and-after contrasts requires proactive documentation of early warning system performance and aggressive communication of cost-benefit evidence.

Third, institutional design matters profoundly. The recent turbulence at U.S. federal agencies demonstrates how weather infrastructure depends on bureaucratic stability and professional autonomy. When grant approvals require cabinet-level sign-offs, when career scientists face political purges, when research programs face repeated elimination attempts, the capacity to maintain sophisticated early warning systems degrades regardless of nominal funding levels.

Countries that have successfully sustained meteorological capacity over decades typically embed these functions in technocratic institutions with stable budgets and clear mandates. The European Centre for Medium-Range Weather Forecasts operates as an independent intergovernmental organization with member state contributions insulated from annual political battles. Similar models could enhance resilience of national meteorological services to political turbulence.

Fourth, integration with broader climate adaptation strategies creates synergies. Early warning systems deliver immediate disaster risk reduction benefits while simultaneously supporting longer-term adaptation planning. Meteorological data informs decisions about infrastructure siting, agricultural practices, water resource management, and coastal zone development. Framing weather infrastructure as essential adaptation infrastructure rather than discretionary spending shifts political calculations.

Finally, international cooperation requires sustained cultivation. Climate and weather cross borders; no country can achieve adequate forecasting capacity in isolation. The WMO’s Global Basic Observing Network addresses geographical inconsistencies in internationally exchanged data, but depends on voluntary compliance with observational standards and data sharing protocols. As climate impacts intensify and disasters multiply, maintaining cooperative frameworks against nationalist or mercantilist pressures represents a critical diplomatic priority.

The False Economy of Underinvestment

In January 2026, as this analysis goes to press, the political future of weather infrastructure remains contested. Congressional appropriators have largely rejected the most draconian proposed cuts to NOAA and NASA Earth science programs, yet bureaucratic obstruction continues. Regional climate centers remain shuttered. Ocean buoy networks face aging equipment and inadequate maintenance budgets. International funding for early warning systems in vulnerable countries remains orders of magnitude below identified needs.

This persistent underinvestment represents a textbook false economy—one where penny-wise, pound-foolish decisions prioritize immediate budget pressures over vastly larger long-term costs. The economic evidence is unambiguous: every dollar invested in early warning systems generates four to thirty-six dollars in benefits. The humanitarian case is even more compelling: adequate early warning systems reduce disaster mortality by a factor of six.

Yet knowing what we should do and mustering the political will to do it remain frustratingly disconnected. The challenge is not technical—we possess the meteorological science, the satellite technology, the computational capacity, and the organizational know-how to build and maintain effective early warning systems globally. The challenge is political: mobilizing sustained investment in public goods that generate diffuse benefits, operate invisibly when successful, and require long-term thinking in political systems optimized for short-term calculations.

The experience of Bangladesh demonstrates that dramatic progress is possible when political will aligns with sustained investment. The country’s transformation from suffering 500,000 cyclone deaths in 1970 to minimizing casualties from comparable storms today stands as one of the great disaster risk reduction achievements of the modern era. Replicating this success globally requires recognizing that weather infrastructure represents not a luxury expenditure but essential public infrastructure—as fundamental as roads, electrical grids, or water systems.

As climate change intensifies and disaster costs mount, the question is not whether to invest in early warning systems but whether we do so proactively or continue learning expensive lessons with each preventable catastrophe. The first half of 2025, with its record-breaking $101.4 billion in disaster costs, illustrates the fiscal and human consequences of inadequate investment. The contrast between Bangladesh’s effective cyclone response and California’s devastating wildfires highlights how infrastructure choices determine outcomes.

The political economy of weather stations ultimately reflects deeper questions about collective action, public goods provision, and societal time horizons. In an era of climate disruption, our ability to answer these questions well—to build and sustain the meteorological infrastructure that turns atmospheric chaos into actionable intelligence—will help determine which communities thrive and which face preventable disasters. The technology exists; the economic case is proven; the humanitarian imperative is clear. What remains uncertain is whether political systems can rise to meet a challenge where the costs of failure compound with each passing year.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

In a sleek laboratory at the University of Science and Technology of China in Hefei, researchers huddle around the Jiuzhang photonic quantum computer, a machine that can complete certain computational tasks in 200 seconds that would take classical supercomputers an estimated half-billion years. Just down the corridor, graduate students test components for next-generation electric vehicle batteries, their work funded by partnerships with BYD and Contemporary Amperex Technology. This scene, replicated across dozens of Chinese research institutions, captures a profound transformation: China’s evolution from the world’s factory floor to an innovation powerhouse where academic research increasingly determines economic competitiveness.

The numbers tell a remarkable story. In 2025, China’s research and development spending reached 2.8 percent of GDP, surpassing the average level of OECD countries for the first time, according to the National Bureau of Statistics. This milestone represents more than statistical achievement—it signals a fundamental reorientation of the world’s second-largest economy toward knowledge-intensive growth. With R&D expenditure rising 8.9 percent year-on-year to exceed 3.6 trillion yuan in 2024, China now stands as the world’s second-largest R&D investor, trailing only the United States but gaining ground rapidly.

Yet China’s research-driven transformation extends far beyond headline spending figures. The country has systematically built an innovation ecosystem where universities, research institutes, and industry collaborate with unprecedented intensity. The results manifest across multiple dimensions: Chinese institutions now dominate the Nature Index rankings, with nine of the world’s top ten academic institutions coming from China, while patent applications reached 1.8 million in 2024, accounting for nearly half of the global total. In strategic sectors from artificial intelligence to quantum computing, electric vehicles to biotechnology, academic research increasingly provides the foundation for commercial breakthroughs that reshape global markets.

This article examines ten distinct ways that China’s academic and research institutions fuel economic expansion. Drawing on the latest data from 2025-2026, it analyzes how university-industry partnerships, talent pipelines, patent commercialization, and regional innovation clusters collectively drive China’s transition toward innovation-led growth. The analysis also acknowledges persistent challenges—inefficiencies in spending allocation, geopolitical tensions constraining international collaboration, and questions about research quality versus quantity—that complicate assessments of China’s research performance. Understanding these dynamics matters not only for evaluating China’s economic trajectory but for anticipating shifts in global technological leadership and competitive advantage.

1. Building a World-Class Talent Pipeline Through Elite Universities

China’s research-driven economic growth begins with human capital cultivation at elite universities that have rapidly ascended global rankings. Tsinghua University and Peking University, China’s flagship institutions, consistently rank among the world’s top 20 universities and produce thousands of STEM graduates annually who populate both domestic industries and international research labs. The University of Science and Technology of China now ranks as the top university in China and second globally in the Nature Index with a total paper count of 2,585, demonstrating research output that rivals Harvard.

This talent pipeline operates at unprecedented scale. China produces more than four million STEM graduates annually, creating the world’s largest pool of technically trained workers. These graduates don’t merely fill existing positions—they drive innovation across emerging sectors. At Zhejiang University, dubbed the “mother of little dragons” because so many founders of top startups, including DeepSeek and Unitree, came from its programs, students transition seamlessly from academic research to entrepreneurship, often with university support providing subsidized infrastructure, mentorship, and capital.

The quality of this talent pool has improved alongside its expansion. Chinese universities have invested heavily in attracting top faculty, including returnee scholars from Western institutions and international researchers. The “Thousand Talents Program” and similar initiatives, despite generating geopolitical controversy, successfully recruited experienced researchers who elevated China’s academic capabilities. These faculty members not only conduct research but train the next generation, creating multiplier effects that compound over time.

Beyond individual institutions, China has developed tiered excellence through initiatives like Project 985 and the Double First-Class Construction project, which concentrate resources at top universities while raising standards across the system. This hierarchical approach allows specialization: while Tsinghua excels in engineering, Peking University leads in humanities and social sciences, and USTC dominates in physics and quantum research. Such specialization enables Chinese universities to compete globally across multiple disciplines simultaneously, rather than concentrating strengths in limited areas.

2. Dominating Global Patent Filings and Intellectual Property Creation

China’s intellectual property generation has reached extraordinary levels, fundamentally altering global innovation dynamics. The country’s patent filing surge reflects not merely bureaucratic productivity but increasingly sophisticated research capabilities that translate into commercial applications. In 2024, China maintained its position as the global leader with 1.8 million patent applications, a figure that dwarfs the 501,831 applications filed in the United States and represents nearly half the global total.

These patents span critical technological domains. Computer technology, electrical machinery, and digital communications lead filing activity, sectors where China seeks competitive advantage and where patents can protect lucrative markets. Huawei Technologies alone filed 6,600 Patent Cooperation Treaty applications in 2024, making it the world’s most prolific corporate filer and demonstrating how Chinese firms use IP strategy to secure market position. Contemporary Amperex Technology, the battery manufacturer, ranked fifth globally with nearly 2,000 applications, illustrating patent activity in sectors like electric vehicles where China has already achieved market dominance.

The quality question surrounding Chinese patents deserves nuanced assessment. Critics correctly note that quantity doesn’t equal quality, and that some Chinese patent filings have historically aimed to meet bureaucratic targets rather than protect genuine innovations. The Chinese government has acknowledged this concern, reducing subsidies that encouraged low-quality filings and implementing stricter quality checks, meaning that while the total number is still impressive, there is a clear focus on ensuring patents are meaningful. Recent data suggests improvement: Chinese patent citations have increased, foreign filings (an indicator of commercial value) have grown, and Chinese-origin patents increasingly appear in high-value litigation globally.

Patent commercialization presents another dimension of economic impact. Chinese universities and research institutes have established technology transfer offices that actively license patents to industry. Tsinghua University operates dedicated tech transfer infrastructure designed to ensure that research outcomes result in products and services that benefit the public, transforming innovations from concept to real-world application. This commercialization creates direct economic value through licensing revenues while generating spillover effects as patented technologies diffuse through supply chains.

3. Forging Deep University-Industry Partnerships and Tech Transfer Hubs

The integration of academic research with industrial application has become a hallmark of China’s innovation system, creating feedback loops where industry funding supports university research that generates commercially relevant findings. This model differs from Western arms-length relationships, instead featuring close collaboration that accelerates technology transfer. Major tech firms maintain extensive research partnerships with leading universities, jointly funding labs, co-supervising graduate students, and sharing research facilities.

The Tsinghua Berkeley Shenzhen Institute exemplifies this model, bringing together U.S. expertise and technological capabilities developed by U.S. professors with Chinese commercialization infrastructure. While such partnerships have generated security concerns in Washington, they demonstrate how Chinese institutions leverage global knowledge networks while building domestic capabilities. Similar institutes linking Chinese universities with international partners have proliferated, particularly in fields like artificial intelligence, semiconductor design, and renewable energy.

Regional tech transfer hubs amplify these partnerships. The China International Technology Transfer Center, established by the Ministry of Science and Technology, promotes technology transfer between universities, research centers, and industry while facilitating international collaboration. These platforms reduce transaction costs associated with moving research from lab to market, providing matchmaking services, incubation support, and commercialization expertise that individual universities might lack.