Human Resourcs

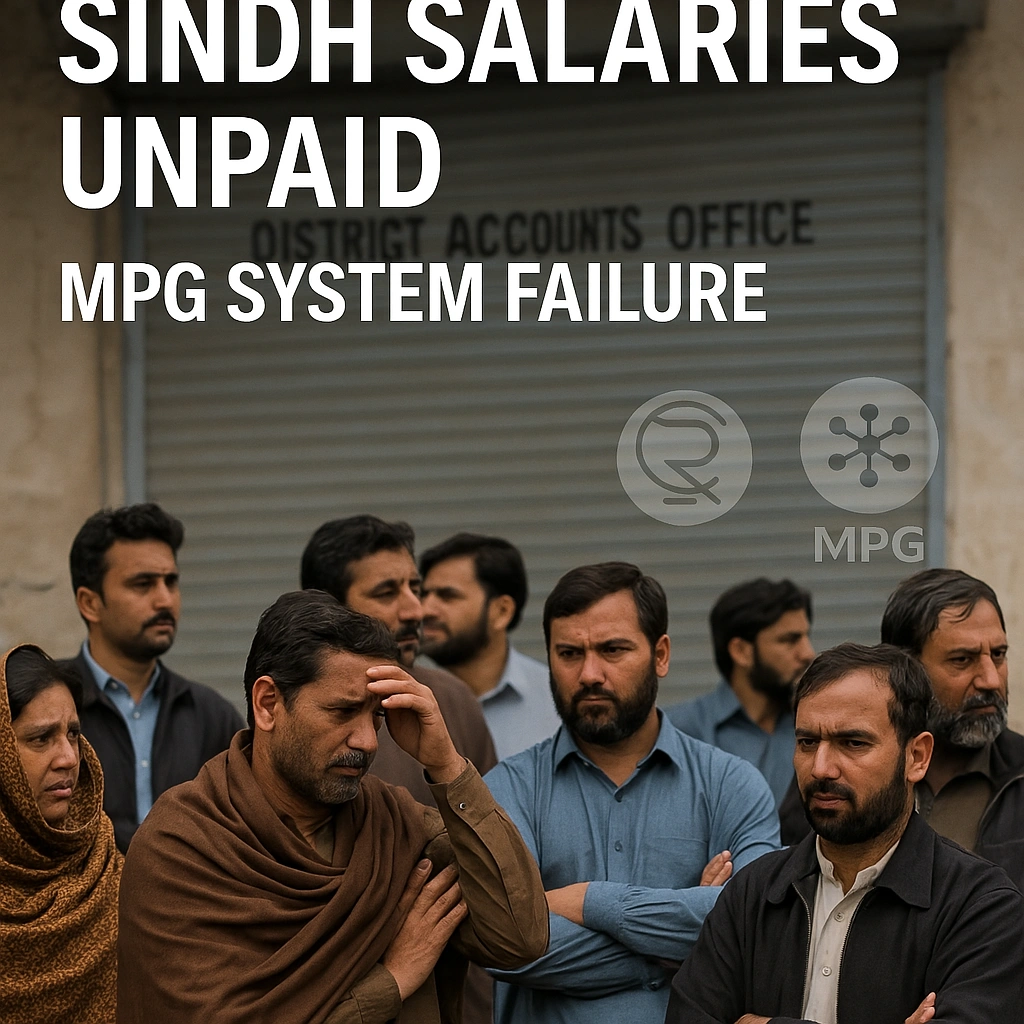

Sindh’s Payroll Crisis: How a Digital Payment System Collapse Left Thousands of Government Employees Without January Salaries

Sindh government employees remain unpaid as MPG payment system fails past January 25th deadline. Exclusive investigation into Pakistan’s digital payment infrastructure breakdown and its human cost.

“The 25th Has Come and Gone—But Salaries Haven’t“

For Muhammad Rasheed, a grade-17 officer in Sindh’s education department, January 28th marks the third day of uncertainty. The 25th—traditionally the day when government salaries illuminate bank accounts across Pakistan—passed without the familiar notification ping. His children’s school fees are overdue. His wife postponed a medical appointment. And like thousands of civil servants across Sindh province, he’s caught in the crossfire of what experts are calling Pakistan’s most significant digital payment system failure in recent memory.

The culprit? The Micro Payment Gateway (MPG), a digital disbursement platform that was supposed to modernize how Sindh pays its 400,000-plus government employees. Instead, it has created a humanitarian and administrative crisis that exposes the fragility of Pakistan’s rush toward digitalization without adequate safeguards.

According to sources within the Accountant General (AG) Sindh office who spoke on condition of anonymity, the system experienced “catastrophic failures” in processing the January 2026 payroll, leaving employees—from junior clerks to senior administrators—in financial limbo. This isn’t merely a technical glitch; it’s a case study in how premature digital transformation can collapse under its own weight.

Understanding the MPG Debacle: What Went Wrong?

The Promise of Digital Transformation

Pakistan’s State Bank of Pakistan (SBP) has been aggressively promoting digital payment infrastructure, including the Raast instant payment system, as part of its National Financial Inclusion Strategy. The MPG was envisioned as Sindh’s answer to efficient, transparent salary disbursement—eliminating intermediaries, reducing corruption, and ensuring timely payments.

The Washington Post recently highlighted Pakistan’s digital ambitions in its Asia economic coverage, noting that “emerging markets face unique challenges in digital payment adoption“—a prescient observation given Sindh’s current predicament.

The Reality: A System Unraveling

Multiple technical failures have compounded since late 2025:

District-Level Breakdowns

- Badin District: Complete payroll processing failure affecting 8,000+ employees

- Dadu District: Partial disbursements with unexplained deductions

- Ghotki District: System rejecting employee bank account validations

Sources indicate the MPG’s integration with the Controller General of Accounts Pakistan (CGA) database encountered synchronization errors, particularly affecting employees receiving the Salaries through MPG .

“The system wasn’t stress-tested for scale,” explains Dr. Ayesha Malik, a digital governance expert at Lahore University of Management Sciences. “When you’re processing 400,000 salaries simultaneously, any latency in API calls or database queries creates cascading failures.”

The Federal-Provincial Divide

The crisis highlights a disturbing disparity. Federal government employees in Islamabad received January salaries on schedule through the tried-and-tested systems managed by the Controller General of Accounts. Punjab province, which piloted a hybrid digital-manual approach, reported 99% on-time disbursement according to data tracked by governance monitoring organizations.

Sindh stands alone in its comprehensive failure—a province that accounts for approximately 22% of Pakistan’s GDP but now cannot pay its own workforce.

The Human Toll: Beyond Statistics and Systems

Stories From the Frontlines

Khadija Bibi, Grade 9 Clerk, Health Department, Hyderabad: “I couldn’t pay my electricity bill. When I went to the school to explain why I couldn’t pay my daughter’s fees, I felt humiliated. They know I’m a government employee. They think I’m making excuses.”

Rashid Ahmed, Grade 16 Officer, Irrigation Department, Sukkur: “We took out high-interest private loans just to buy groceries. The irony? I work in a department that manages water resources for millions, but I can’t manage my own household expenses.”

These aren’t isolated incidents. According to preliminary surveys by civil servant unions, approximately 68% of affected employees have resorted to informal borrowing, often at predatory interest rates exceeding 15% monthly.

The Economist’s recent analysis of emerging market labor dynamics noted that “government employment in South Asia functions as both economic stimulus and social safety net”—making salary delays not just administrative failures but potential triggers for broader economic disruption.

Pension Paralysis

The crisis extends beyond active employees. Thousands of retirees dependent on monthly pensions face similar uncertainty. For many elderly recipients without alternative income sources, this represents an existential threat.

“My father served 35 years in the judiciary,” shares Maryam Khan, daughter of a retired civil judge. “His pension hasn’t come through. He has diabetes medication to buy. This is how we treat our retired public servants?”

Administrative Autopsy: Who’s Accountable?

The Blame Cascade

AG Sindh Office: Claims the State Bank of Pakistan infrastructure experienced “unexpected downtime” during critical processing windows.

State Bank of Pakistan: Points to incomplete data submission from provincial authorities and “non-standard file formats” that violated integration protocols.

Provincial Finance Department: Suggests the Controller General of Accounts delayed authorization for January disbursements due to “budgetary reconciliation issues.”

This circular blame game reveals a fundamental problem: no single entity owns the end-to-end payment process. The MPG system exists in a bureaucratic no-man’s-land where technical failures become administrative hot potatoes.

The Reversion Rumors

Multiple sources confirm that senior Sindh government officials have discussed reverting to manual salary disbursement processes—essentially abandoning the MPG experiment. However, this creates its own complications:

- Data Migration Challenges: Employee records have been partially migrated to the digital system

- Timeline Concerns: Manual processing for 400,000+ employees could take 3-4 business days

- Political Optics: Admitting digital transformation failure before upcoming elections

Financial Times’ coverage of government technology implementations in developing economies warns that “premature abandonment of digital systems after initial failures can create worse long-term outcomes than temporary persistence with fixes”—a dilemma Sindh now faces.

Key Takeaways

- 400,000+ Sindh government employees haven’t received January 2026 salaries due to MPG system failure or Deliberate apathy of Accounts Offices .

- District-level breakdowns in Badin, Dadu,Kashmore and Ghotki compound the crisis

- Federal and Punjab governments disbursed salaries on time, highlighting Sindh’s unique failure

- 68% of affected employees have resorted to high-interest informal borrowing

- Reversion to manual systems being considered but faces logistical and political obstacles

- Broader implications for Pakistan’s digital transformation credibility and economic stability

Comparative Analysis: Lessons From Other Provinces

Punjab’s Hybrid Success

Punjab province implemented a gradual digital transition:

- Pilot program with 10,000 employees (6 months)

- Parallel manual and digital processing (12 months)

- Full digital transition only after 98% success rate achieved

Result? Zero salary delays in the past 18 months.

Federal Government’s Conservative Approach

The federal establishment maintains legacy systems with incremental digital enhancements—prioritizing reliability over innovation. While less efficient, this approach has delivered 100% on-time salary disbursement for 47 consecutive months.

Forbes recently profiled successful government digital transformations in Asia-Pacific, emphasizing that “speed of implementation matters far less than thoroughness of testing and redundancy planning”—wisdom Sindh appears to have ignored.

Broader Implications: Pakistan’s Digital Governance Crossroads

The Credibility Crisis

This failure undermines Pakistan’s broader digital transformation initiatives:

- Raast Payment System Adoption: Banks report declining merchant confidence in government-backed digital platforms

- Tax Digitalization: Concerns about FBR’s planned e-filing mandate

- E-Governance Projects: Provincial governments reconsidering aggressive digital timelines

“One high-profile failure creates systemic skepticism,” notes Farhan Mahmood, a Karachi-based technology governance consultant. “It takes years to rebuild trust in digital government systems.”

The Economic Ripple Effect

When 400,000+ government employees lack purchasing power:

- Local Commerce Disruption: Retailers in government employment hubs (Karachi, Hyderabad, Sukkur) report 30-40% sales declines

- Informal Lending Surge: Private money lenders report unprecedented demand

- Household Debt Accumulation: Long-term financial vulnerability for civil servant families

The Washington Post’s economics desk has documented how public sector salary disruptions in developing economies create “multiplier effects that reduce GDP by 0.3-0.5% quarterly”—a potential scenario for Sindh if delays persist.

The Path Forward: Five Critical Interventions

1. Emergency Manual Disbursement

Activate legacy systems immediately for critical-need employees (grades 1-11, pensioners, medical emergencies) while debugging MPG infrastructure.

2. Independent Technical Audit

Engage international payment system auditors (similar to those used by State Bank of Pakistan for Raast system validation) to identify root causes and recommend fixes.

3. Transparent Communication Protocol

Establish daily public updates on resolution progress—reducing anxiety and rumor circulation among affected employees.

4. Compensatory Measures

Consider:

- Interest-free advance salary loans through government banks

- Automatic reversal of late payment penalties for employee bills

- Hardship grants for lowest-grade employees

5. Accountability Framework

Commission a formal inquiry with public hearings—not for political theater, but genuine systemic learning. The Economist’s governance research emphasizes that “administrative failures require institutional accountability, not individual scapegoating” to prevent recurrence.

Conclusion: A Cautionary Tale for Digital Governance

The Sindh MPG payment system failure represents more than delayed salaries—it’s a referendum on how governments approach digital transformation in resource-constrained environments. The rush to appear technologically progressive, without adequate testing, redundancy planning, and stakeholder preparation, has created precisely the crisis digitalization was meant to prevent.

For Muhammad Rasheed and hundreds of thousands like him, the promise of efficiency has yielded only uncertainty. For Pakistan’s digital governance ambitions, this is a watershed moment: either a catalyst for genuine reform, or the beginning of a retreat to comfortable but inefficient status quo.

The next 72 hours will determine which path employees go for rights . Still no updates for salaries

As Financial Times noted in its recent analysis of emerging market governance challenges: “Technology is only as good as the systems that implement it, and the people who depend on it.” Sindh’s 400,000 government employees are now the unwilling test subjects of that axiom.

The question remains: Will anyone be held accountable before the February salary cycle begins?

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Human Resourcs

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

The US labor force participation rate has fallen to its lowest level in 50 years outside of the Covid-19 pandemic period, a decline that is reshaping how economists read every other US labor market indicator, according to CNBC’s ongoing coverage of the trend.

Why a Falling Unemployment Rate Can Be Misleading

A shrinking labor force participation rate means fewer working-age Americans are actively employed or looking for work — a dynamic that can mechanically push the headline unemployment rate lower even when underlying labor-market health is deteriorating, since people who stop searching for jobs are no longer counted as unemployed. That distinction matters enormously for how policymakers, including the Federal Reserve under new chair Kevin Warsh, interpret incoming jobs data at a moment when the central bank has explicitly moved away from forward guidance and toward a purely data-driven policy stance.

The AI Overlay on an Already Complex Picture

The participation decline is unfolding against the backdrop of intensifying debate over AI’s labor-market impact. A National Bureau of Economic Research study published in February 2026 found that despite widespread adoption, 90% of firms reported no measurable impact of AI on workplace productivity or employment levels, a finding that has been widely cited by critics of the AI investment boom as evidence that current valuations have outrun genuine productivity gains, according to Wikipedia’s tracking of the AI bubble debate. That gap between AI investment intensity and measured labor-market effects complicates the task of isolating how much of the participation decline, if any, is attributable to automation versus other structural and demographic factors.

A Global Pattern of Labor Market Caution

The US is not alone in exhibiting unusual labor-market dynamics. Canada’s labor market has settled into what Indeed Canada economist Brendon Bernard describes as a “low-hire, low-fire” pattern, where weak hiring and weak layoffs combine to keep the unemployment rate stable even as underlying momentum stays soft, according to Yahoo Finance Canada’s economist survey. The UK has shown a similar caution pattern, with businesses reporting weakened operating conditions and falling revenue expectations even as headline employment figures remain comparatively stable, according to CPA’s coverage of the Institute of Directors’ June sentiment survey.

The Grid and Heat Stress Layer

Compounding the labor-market picture, an extreme heat wave is straining power grids across the eastern United States heading into the July 4 holiday travel period, with the largest US power grid operator, PJM, escalating emergency actions to avoid blackouts, according to CNBC’s reporting on the grid strain. The combination of extreme weather events and elevated electricity demand tied partly to AI data-center growth adds a further layer of complexity for businesses managing both workforce planning and operational continuity through the summer months.

What Economists Are Watching Next

With the Federal Reserve no longer providing forward guidance on its policy path, incoming labor-market data — including the closely watched participation rate — will carry outsized weight in shaping market expectations for the remainder of 2026. Economists caution that a genuinely healthy labor market requires participation, hiring, and wage growth to move together; a scenario in which unemployment appears low purely because discouraged workers have exited the labor force altogether would represent a materially weaker underlying picture than the headline rate suggests, with direct implications for consumer spending forecasts across the US retail, housing, and services sectors heading into the back half of 2026.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The US economy added just 57,000 jobs in June, roughly half the number economists had forecast, and Wall Street’s reaction was almost perfectly inverted from what the headline number would suggest. The Dow Jones Industrial Average surged nearly 600 points to a record close of 52,900.07, even as the weak print signaled a cooling labor market, because investors read it as evidence the Federal Reserve has less reason to keep policy tight, according to Google Finance’s market wrap.

A Fed Chair Asking Markets to Watch the Data, Not Him

The rally happened against a specific backdrop: Federal Reserve Chairman Kevin Warsh has been urging Wall Street to look to incoming economic data to map the path for interest rates rather than to the central bank for forward guidance, a shift in communication style noted by Yahoo Finance. That framing matters because it puts the weak jobs report, rather than any Fed statement, in the driver’s seat for rate expectations heading into the July 30 policy decision.

Warsh had separately told the market that inflation risks have come down substantially, comments that had already lifted sentiment earlier in the week, per Bloomberg’s coverage of the prior session. The combination of easing inflation rhetoric and a soft jobs number gives the Fed cover to hold rates steady, or even consider cuts, without appearing to react to political pressure or market demands.

A Market Split Down the Middle

The reaction split sharply by sector. The S&P 500 was essentially flat, while the tech-heavy Nasdaq Composite fell 0.8%, dragged down by a second consecutive day of semiconductor selling that saw the VanEck Semiconductor ETF drop 4.5%, according to CNBC’s live markets desk. Tesla shares sank as much as 7.3% despite reporting second-quarter delivery and production levels that beat Wall Street expectations, a reminder that in the current environment, even strong operating results are being overshadowed by broader positioning shifts out of AI-adjacent names.

Meanwhile, defensive and rate-sensitive sectors caught a bid. The Communication Services Select Sector SPDR gained 2.4% and the Financials Select Sector SPDR added 2.2%, according to Zacks’ daily market summary, a rotation pattern consistent with investors repositioning toward sectors that benefit from lower borrowing costs and away from the crowded AI trade that has dominated 2026 returns so far.

Oil, Gold, and the Lingering Iran War Effect

The jobs report landed alongside an easing of a separate inflation risk. WTI crude futures fell nearly 2% to just above $68 a barrel, down almost 20% over the prior two weeks, as markets priced in signs that indirect talks between the US and Iran were progressing positively, according to Schwab’s market open report. That decline matters directly for the Fed’s calculus: falling energy prices reduce one of the clearest channels through which the Iran conflict has been pushing inflation higher across the global economy since the Strait of Hormuz disruption began in late February.

At the same time, gold rose after the cooler-than-expected jobs data, and Bitcoin climbed more than 2% to surpass $61,000, buoyed by renewed accumulation from long-term holders and institutional buyers, Google Finance’s market summary noted. The simultaneous rally in equities, gold, and crypto is an unusual combination that reflects a market betting on looser monetary policy across every asset class at once, even as the underlying economic signal, a half-strength jobs report, is not obviously bullish news.

What the July 30 Decision Now Hinges On

Markets enter the July 30 Federal Open Market Committee meeting with a genuinely two-sided setup. On one hand, a labor market adding jobs at half the expected pace historically justifies rate cuts. On the other, the Iran-driven energy shock has already pushed inflation forecasts higher across nearly every advanced economy this year, and Warsh’s own commentary suggests the Fed wants to avoid being seen as reactive to a single data point. The Federal Open Market Committee minutes due July 8 will offer the clearest signal yet of how divided the committee is on this question, with markets closed Friday, July 3, for the Independence Day holiday, resuming trading Monday.

For now, the record Dow close alongside a weak jobs report captures a market more focused on the Fed’s next move than on the underlying health of hiring. That combination, cooling employment growth paired with equity records, is precisely the kind of divergence that tends to persist until a policy decision forces a reconciliation between the two signals.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

US male labor force participation has fallen to 69.5%—from 86.4% in 1950. New research finds the cause starts in childhood. Here’s what this crisis means for GDP, wages, and US competitiveness.The male labor force participation rate in the United States fell to 69.5% in May 2026—the latest reading in a generational decline that economists have struggled for decades to fully explain and policymakers have largely failed to address.

The number is stark in historical perspective. The male participation rate peaked at 86.4% in 1950. It had already slipped to 76% by May 2006. It now stands nearly seven percentage points lower than it did twenty years ago, and the research suggests the forces driving it are not cyclical but structural—embedded in the childhood experiences of men who grew up watching the labor market fail the males around them.

The New Research: Childhood Shapes Lifetime Expectations

A paper published by University of Connecticut economists Remy Levin and Daniela Vidart in June 2026 advances what may be the most empirically rigorous explanation yet offered for the male participation decline. Their finding: men’s beliefs about the benefits of working are shaped significantly by the labor market conditions they observed during childhood—particularly the wages and employment rates of men in their immediate environment.

When boys grow up surrounded by men who face weak wages and chronic unemployment, they form pessimistic expectations about their own prospects. Those expectations, Levin and Vidart found, become self-fulfilling: men with pessimistic priors are less likely to seek employment, invest in skills, or remain attached to the labor force when discouraged.

“Our findings suggest that experience effects can turn short-run declines in labor demand into long-run declines in labor supply,” they wrote. Their model found that generational childhood exposure to poor male labor market outcomes explained nearly all of the participation dynamics—not macroeconomic conditions in real time, but the lagged echo of conditions that shaped expectations years or decades earlier.

This has a sobering implication: the communities hardest hit by deindustrialization in the 1980s and 1990s are now producing the next generation of non-participants. The experience effect propagates across cohorts. It cannot be solved by a single strong jobs report.

The Theories That Preceded This One

The new research lands in a field dense with competing explanations, each capturing part of the picture. When the housing bubble popped and triggered the Great Recession, the sudden collapse of construction employment—a heavily male sector—pulled hundreds of thousands of men out of the labor force at a moment of acute vulnerability. Many did not return.

The San Francisco Fed identified two channels at work in prior research: men being pulled out of the workforce by caregiving and educational enrollment, and pushed out by disability and skill mismatch. Meredith Whitney, who predicted the Great Financial Crisis, pointed to a “crisis of the American male” rooted in young single men living at home and disengaging from both employment and civic life. The introduction of more sophisticated video games has been cited by economists as a partial substitute for work, particularly among men in their twenties.

Each theory has supporting evidence. None is complete on its own. The University of Connecticut paper’s contribution is to provide a unified mechanism—childhood experience shaping adult expectations—that can account for the persistence and geographic concentration of the decline.

The Economic Cost

The GDP cost of chronically low male participation is difficult to overstate. Labor force participation is one of the two components of labor supply (the other being hours worked). When men leave the workforce permanently, the economy loses not just their current output but the compounding returns on the human capital they would have accumulated over careers.

Researchers estimate the participation gap—the difference between current male participation and what it would be if it had held at 2000 levels—represents millions of missing workers. At an average productivity contribution aligned with current wages, the annual output cost runs into the hundreds of billions of dollars. This is not a cyclical drag that disappears with the next expansion. It is structural loss that compounds each year.

The distribution of that loss is not uniform. States and communities that experienced the heaviest deindustrialization have the lowest male participation rates. Those communities also tend to have lower educational attainment, higher rates of opioid addiction, and weaker social infrastructure. The labor market crisis and the social crisis reinforce each other.

What Follows

If the Levin-Vidart finding is correct, the policy implications are uncomfortable. Short-term demand management—stimulus, job training, even wage subsidies—does not address the expectation formation mechanism that the paper identifies. What changes childhood experience of the labor market is decades of sustained improvement in wages and employment for working-class men, coupled with community-level investment in visible male economic success.

That is a long time horizon for a political system that operates on two- and four-year cycles. The more immediate policy levers—expanding apprenticeship programs, reforming occupational licensing that makes it harder to enter trade careers, addressing the child support enforcement systems that can make formal employment economically punishing for non-custodial fathers—exist but require sustained commitment.

Consumer sentiment at a near-historic low of 48.9% in late June 2026 reflects, in part, the lived experience of the communities where male participation has declined most sharply. An economy where the richest 20% are the primary engines of consumer spending—and where that spending is itself dependent on elevated asset prices that could correct—is structurally fragile in ways that the employment rate headline does not capture.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Pakistan’s Most Reliable Export Is Its People: Remittances Hit $41.6 Billion, Overtaking Total Exports

Indonesia’s Confidence Problem: Record Investment, a Sinking Rupiah, and a Widening Credibility Gap

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

China’s Growth Slips to a Four-Year Low: Why Beijing Still Won’t Pull the Stimulus Trigger

The Johor-Singapore Corridor: How Malaysia Became Southeast Asia’s AI Infrastructure Powerhouse

Canada’s Economy ‘On Pause’: Inside the CUSMA Deadline That Passed Without a Deal

Dubai’s Millionaire Magnet: How the UAE Turned Middle East Turmoil Into a Capital Safe-Haven Boom

Britain’s Sixth Prime Minister in a Decade: What Starmer’s Exit Means for Gilts, Sterling and Your Portfolio

Anthropic Offers Up to $600,000 Salary for Critical IPO Role as AI Giant Prepares for Wall Street Debut

EU Readies Crisis Team for Potential China Rare Earths Stand-Off as Supply Chain Risks Mount

Singapore Weighs Hedge Fund Tax Cuts to Counter Hong Kong’s Growing Financial Challenge

Facebook and Instagram Experience Global Outage

Inside the $1 Billion Tap-to-Pay Fraud Rings Targeting Banks and Retailers

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

The AI Super Bubble Is Ready to Burst

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

India Economic Rise 2026: How the Subcontinent Toppled Japan

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

Bitcoin $150k Milestone Achieved as US Sovereign Crypto Pivot Looms

Chipmakers Just Lost 6.7% in Two Days: Inside the Great AI Trade Rotation

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025