Startups

Pakistan’s Startup Revival: How Hybrid Financing Drove a $74 Million Surge in 2025

After years of contraction, a strategic pivot to debt-equity blends signals maturation—not just survival—in one of South Asia’s most resilient tech ecosystems

In early April 2025, Omer bin Ahsan faced a familiar dilemma. The founder of Haball, a Karachi-based fintech enabling shariah-compliant supply chain financing, had spent months courting investors for a pre-Series A round. Traditional venture capital appetite remained tepid—Pakistan startup funding 2025 had opened with a dismal $196,000 across three disclosed deals in Q1, marking the ecosystem’s lowest quarterly performance in years. Yet Ahsan’s company had processed over $3 billion in payments since inception, serving nearly 8,000 small and medium enterprises across sectors from retail to aerospace. The fundamentals were solid. What Pakistan lacked wasn’t viable startups—it was capital willing to deploy at scale.

By late April, Haball announced a $52 million raise, comprising $5 million in equity from Zayn VC and a strategic $47 million financing component from Meezan Bank, Pakistan’s largest Islamic financial institution. The structure was a watershed: not pure venture equity, but a hybrid blend of ownership and debt, calibrated to minimize dilution while leveraging established banking infrastructure. It was also emblematic of a broader shift reshaping Pakistan’s startup landscape—one driven less by Silicon Valley playbooks and more by local pragmatism forged through years of macroeconomic turbulence.

When the year closed, Invest2Innovate’s full-year report revealed that Pakistani startups raised over $74 million across 16 deals in 2025, a 121% increase from $33.5 million in 2024. The headline figure, however, concealed the more profound transformation: $66.04 million came through hybrid financing models blending debt, quasi-equity, and structured instruments, while just $8.18 million represented pure equity. It was the clearest signal yet that Pakistan’s startup ecosystem, battered by three years of funding drought and global venture capital winter, had evolved a distinctly localized survival—and growth—mechanism.

The Numbers in Context: Recovery, Not Rebound

To understand Pakistan startup funding 2025, one must first grasp where the ecosystem stood. Between 2021 and 2023, Pakistani startups rode a wave of global liquidity, raising $347 million and $331 million in 2021 and 2022 respectively, according to Data Darbar, a Karachi-based research firm tracking venture activity since 2015. Then came the correction. Funding collapsed 77% to $75.6 million in 2023 amid Federal Reserve rate hikes and a global venture pullback, then tumbled further to $42.5 million in 2024—a nadir unseen since the ecosystem’s nascent years.

The 2025 recovery to $74 million, while encouraging, remained well below pre-2023 peaks. Yet the composition mattered more than the quantum. Data Darbar, in a parallel year-end analysis, reported that pure equity funding reached $36.6 million across 10 disclosed rounds—a 63% increase from 2024’s $22.5 million. The discrepancy between Invest2Innovate’s $74 million total and Data Darbar’s $36.6 million equity-only figure reflects differing methodologies: Invest2Innovate counts all capital deployed, including debt-like instruments, whereas Data Darbar isolates traditional venture equity.

Both narratives are true. Pakistani startups raised more total capital in 2025, but the structure of that capital had fundamentally changed. Consider the quarterly trajectory:

- Q1 2025: $196,000 disclosed (3 deals). A paralytic start as investors awaited IMF program clarity.

- Q2 2025: $58 million, dominated by Haball’s $52 million hybrid round.

- Q3 2025: $15.2 million across six deals, featuring BusCaro’s $2 million hybrid deal and Trukkr’s $10 million mixed equity-debt raise.

- Q4 2025: Modest, sub-$1 million disclosed volumes, but critical for structural shifts—KalPay secured shariah-compliant structured debt from Accelerate Prosperity, while agritech Agrilift and creator economy platform Echooo AI both raised debt financing.

The average disclosed equity deal size climbed to approximately $3.7 million, up from previous years, signaling that investors—when they did commit—deployed more concentrated capital into fewer, higher-conviction bets. This is the hallmark of market maturation: selectivity over spray-and-pray.

Key Deals and Winners: The 2025 Titans

Haball: The Hybrid Pioneer

Haball’s $52 million raise was the defining transaction of 2025. The fintech, founded in 2017, provides digital invoicing, payment collection, tax compliance, and working capital to SMEs—functions critical in a market where less than 5% of small businesses access traditional bank financing. By structuring its round as $5 million in equity plus $47 million in strategic financing from Meezan Bank, Haball achieved two objectives: securing growth capital without excessive dilution, and validating hybrid models as viable for scaling B2B fintechs in emerging markets.

The company plans to enter Saudi Arabia’s $9 billion supply chain finance market in 2025, with further Gulf Cooperation Council (GCC) expansion eyed for 2026. As CEO Omer bin Ahsan noted, “We’re responding to clear market demand for shariah-compliant SME-focused digital financial services”—a thesis resonating not just in Pakistan but across MENA’s Islamic finance corridors.

MedIQ: Female-Founded, GCC-Bound

In April, Dr. Saira Siddique’s MedIQ raised $6 million in a Series A led by Qatar’s Rasmal Ventures and Saudi Arabia’s Joa Capital. The healthtech, born from Siddique’s personal experience navigating Pakistan’s fragmented healthcare system while recovering from paralysis, offers a digitally integrated hybrid ecosystem—telehealth, e-pharmacy, AI-powered facility digitization, and insurance backend automation.

MedIQ’s trajectory underscores a critical trend: Pakistani startups pivoting to GCC markets not as Plan B, but as core strategy. With over 10 million customers served in Pakistan and EBITDA-positive operations, MedIQ exemplifies the product-market fit achievable when founders solve genuine, large-scale inefficiencies. The raise also marked a milestone for gender diversity—female-led startups captured $8.8 million (24%) of 2025’s total equity funding, per Data Darbar, a notable improvement in a historically male-dominated ecosystem.

Mobility, Fintech, and the Long Tail

Beyond mega-rounds, 2025 saw seed-stage activity across diverse verticals:

- BusCaro (mobility): $2 million hybrid deal, female-founded, addressing intercity transport inefficiencies.

- Metric (fintech): $1.3 million seed for infrastructure finance enablement.

- ScholarBee (edtech): $350,000 convertible note, targeting affordable learning platforms.

- Qist Bazaar (fintech BNPL): Rs55 million (~$196,000) disclosed portion of a larger Series A from Bank Alfalah.

- Shadiyana (wedding-tech): $800,000 pre-seed, tapping Pakistan’s multi-billion-dollar wedding industry.

- Myco.io (Web3): $1.5 million, reflecting nascent but persistent interest in decentralized tech.

These transactions, while modest individually, signaled ecosystem resilience. Founders were fundraising—just under radically different assumptions than 2021’s exuberance.

The Hybrid Financing Revolution: Necessity Becomes Strategy

Why did Pakistan startup funding 2025 pivot so decisively to hybrid models? The answer lies in supply-demand asymmetries and risk-adjusted returns.

On the supply side, traditional venture capital remained scarce. Global VC funding reached $512.6 billion in 2025, up 30.8% year-over-year, but concentration was extreme: AI captured 46.4% of Q3 2025 global VC, with mega-rounds ($500M+) to Anthropic, xAI, and others dominating deployment. Emerging markets outside India and select MENA hubs saw limited allocations. Pakistan, with its history of political volatility and currency risk, struggled to compete for the shrinking pool of “generalist” VC dollars.

On the demand side, Pakistani startups needed capital, but on terms preserving founder control. After witnessing down rounds and fire-sale exits across the region during 2022-2024’s contraction, founders sought structures minimizing dilution. Debt or quasi-debt instruments—repayable at fixed schedules with or without convertible features—offered that optionality.

Enter hybrid financing: structures blending equity stakes with revenue-based financing, shariah-compliant murabaha (cost-plus) arrangements, supply chain receivables financing, or convertible notes with conservative caps. Haball’s model epitomizes this: Zayn VC took equity exposure, betting on upside, while Meezan Bank deployed a $47 million financing facility tied to Haball’s transaction volumes—essentially supply chain capital leveraging Haball’s platform as intermediary.

For investors like Meezan Bank, the appeal is clear: lower risk than pure equity, secured by tangible cash flows, and aligned with Islamic banking mandates prohibiting interest (riba) yet permitting profit-sharing and asset-backed financing. For startups, it’s growth capital without governance concessions. For the ecosystem, it’s a localization of financing norms—adapting global venture structures to Pakistan’s financial and regulatory realities.

Sector Spotlight: Where the Money Flowed

Fintech: Still the Heavyweight

Fintech dominated Pakistani startups funding 2025, accounting for the largest share of both disclosed equity and hybrid capital. Beyond Haball and Metric, the sector includes Qist Bazaar (BNPL), KalPay (shariah-compliant payments), and established players like Bazaar Technologies, which acquired rival Keenu in late 2025, signaling consolidation.

Pakistan’s fintech appeal is structural: Islamic banking assets reached Rs9,689 billion ($34.54 billion) by mid-2024, representing 18.8% of banking sector assets, with the State Bank targeting 30% by 2028. Digital payments via Raast, Pakistan’s instant payment system, surged, and SME financing gaps remained vast. Fintechs offering compliance-friendly, digitally native solutions tapped into multi-billion-dollar addressable markets.

Healthtech: The Female Founder Vanguard

Healthtech emerged as the second most-funded sector, led by MedIQ’s $6 million and complemented by seed rounds for diagnostics and preventive health startups. Pakistan’s healthcare system—fragmented, cash-based, and inaccessible to rural populations—presents massive digitization opportunities. Telemedicine uptake accelerated post-pandemic, and corporate health insurance mandates are slowly expanding coverage.

Notably, female founders have disproportionately shaped healthtech: MedIQ (Dr. Saira Siddique), Sehat Kahani (Drs. Sara Saeed Khurram and Iffat Zafar Aga, which raised $2.7 million in 2023), and emerging players like Ailaaj and Marham. Women comprise 74% of MedIQ’s user base, per Arab News interviews—a demographic underserved by traditional clinic models requiring male accompaniment or lengthy travel in conservative regions.

Edtech, Mobility, and Climate: Early-Stage Activity

Edtech startups like ScholarBee secured convertible notes, targeting affordable skill development for Pakistan’s youth bulge (over 60% of the population under 30). Mobility players like BusCaro and Trukkr raised hybrid rounds to address intercity transport and logistics inefficiencies. Climate-linked ventures—Agrilift (agritech) and energy platforms—attracted debt financing from impact-focused vehicles like Accelerate Prosperity, reflecting growing alignment between climate resilience mandates (Pakistan is among the world’s most climate-vulnerable nations) and venture deployment.

Web3 and IoT saw niche activity (Myco.io, undisclosed IoT deals), indicating experimentation persists despite limited exits and regulatory ambiguity.

Global and Macroeconomic Backdrop: Pakistan’s Stabilization Gambit

Pakistan startup funding 2025 unfolded against a volatile but ultimately stabilizing macroeconomic canvas. The country entered 2025 under its 25th IMF program since 1950—a 37-month Extended Fund Facility (EFF) approved in August 2024, coupled with a 28-month Resilience and Sustainability Facility (RSF) targeting climate vulnerabilities.

By year-end, the IMF’s second EFF review in December 2025 confirmed progress: Pakistan achieved a primary fiscal surplus of 1.3% of GDP in FY25, inflation fell from 26% in 2024 to 4.7% over the year’s first ten months, and gross foreign reserves climbed from $9.4 billion (August 2024) to $14.5 billion by year-end—projected to reach $21 billion in 2026. The State Bank of Pakistan cut policy rates by 1,100 basis points since June 2025, easing borrowing costs.

These improvements mattered. Investor confidence, globally, correlates with macroeconomic stability and reserve adequacy. Pakistan’s first current account surplus in 14 years, achieved in FY25, signaled reduced external vulnerabilities. Yet GDP growth remained tepid—2.7% in FY25, projected 3.2% for FY26—barely outpacing population growth. For startups, the message was mixed: stability had returned, but explosive growth remained distant.

Comparatively, India’s startup ecosystem raised $3.1 billion in Q1 2025 alone, dwarfing Pakistan’s full-year $36.6 million equity tally. Pakistan’s total VC funding since 2015—approximately $1.037 billion across 368 deals, per Invest2Innovate—pales against India’s $161 billion deployed since 2014. The gap is structural: India’s scale, deeper capital markets, and diaspora networks create self-reinforcing flywheel effects Pakistan lacks.

Yet within emerging markets, context matters. Southeast Asia saw VC funding drop 42% YoY to $1.71 billion in H1 2025, while Africa’s $676 million (up 56%) remained concentrated in Nigeria, Kenya, and Egypt. Pakistan’s $74 million, while modest, outperformed its own recent trough—and the hybrid financing pivot offers a replicable playbook for markets where traditional VC flows remain constrained.

Challenges Ahead: The Structural Headwinds

Despite 2025’s recovery, Pakistan’s startup ecosystem confronts formidable obstacles:

Limited Domestic Capital

Institutional venture capital remains nascent. Gobi Partners’ Techxila Fund II ($50 million, announced Q4 2024) and Sarmayacar’s Climaventures Fund ($40 million target, $15 million anchor from UN’s Green Climate Fund) represent progress, but Pakistan lacks the density of local VC firms—family offices, pension funds, and corporate venture arms—that India, Indonesia, or even Kenya enjoy. Without robust domestic LP pools, international investors’ risk perceptions dominate, and Pakistan’s geopolitical optics (terrorism concerns, political instability) deter allocations.

Regulatory and Infrastructure Gaps

Startups cite slow regulatory approvals, opaque tax frameworks, and energy/internet outages as persistent friction. The IMF’s 2025 Governance and Corruption Diagnostic estimated Pakistan loses 5-6.5% of GDP annually to “elite capture”—policy distortions favoring entrenched interests. For startups, this manifests as uneven playing fields: established businesses leverage connections for subsidies or licenses, while digital-first ventures navigate bureaucratic mazes.

The State Bank of Pakistan has made strides—Raast adoption, licensing frameworks for digital invoicing (Haball was the first fintech to receive such a license from the Federal Board of Revenue)—but broader structural reforms lag. State-owned enterprise (SOE) losses hemorrhage fiscal resources that could otherwise fund innovation, and privatization efforts (e.g., Pakistan International Airlines) proceed glacially.

Talent Retention and Brain Drain

Pakistan produces over 15,000 IT graduates annually, yet emigration rates are high. Gulf markets, Europe, and North America offer salaries multiples higher than local startups can afford. Top founders increasingly “de-risk” by incorporating in Dubai or Delaware, maintaining development teams in Pakistan but moving corporate entities offshore—a pragmatic but double-edged strategy that limits ecosystem depth.

Exit Drought

Pakistan has recorded zero venture-backed IPOs since Careem’s 2019 acquisition by Uber (a $3.1 billion exit, though Careem was Dubai-domiciled). Without consistent exits—IPOs, strategic acquisitions, or secondary sales—early investors cannot realize returns, limiting LP appetite to reinvest. The absence of a Nasdaq-style tech exchange or active M&A market (few multinational acquirers operate locally at scale) perpetuates this cycle.

Future Outlook: Toward 2026 and Beyond

What does Pakistan startup funding 2025’s hybrid pivot augur for the ecosystem’s next phase?

Optimistic Case: The hybrid model becomes a sustainable competitive advantage. If Haball successfully scales across GCC, MedIQ replicates Pakistan learnings in Saudi Arabia, and debt-equity blends prove scalable for B2B SaaS, logistics, and agritech verticals, Pakistan could carve a niche as a “hybrid capital lab” for emerging markets. Islamic finance alignment is non-trivial: GCC investors managing trillions in shariah-compliant assets seek deployment opportunities, and Pakistani startups fluent in murabaha, tawarruq, and wakalah structures have first-mover advantages.

Further, macroeconomic stability—if sustained—creates virtuous cycles. Lower inflation and interest rates reduce cost of capital, IMF program credibility attracts development finance institutions (DFIs) and multilateral capital, and sectoral growth (IT exports surpassed $3.2 billion in FY25, per government data) generates wealth reinvestable locally.

Cautious Case: 2025’s recovery is a dead-cat bounce. If global VC remains concentrated in AI and developed markets, Pakistani startups continue battling for scraps. Hybrid financing, while pragmatic, may limit upside—debt requires repayment, constraining burn rates and growth velocity. Founders opting for conservative capital structures might achieve profitability but miss transformative scale. Meanwhile, India’s ecosystem compounds advantages, Gulf markets attract Pakistani founders directly, and the domestic market’s 240.5 million people remains fragmented by low digital penetration and purchasing power.

The likeliest path lies between extremes. Pakistan’s startup ecosystem in 2025 demonstrated resilience, adaptability, and strategic pragmatism. It won’t replicate India’s scale or Silicon Valley’s density, but it could build sustainable, profitable tech businesses solving real problems for Pakistan’s SMEs, diaspora, and underserved populations—and increasingly, for GCC markets seeking culturally aligned solutions.

Key signposts for 2026 include:

- Fund Formation: Will local LPs (family offices, corporates) launch more $20-50 million seed/early-stage vehicles? Climaventures and Techxila II are starts, but scale matters.

- Exits: Any M&A activity (e.g., Bazaar-Keenu)? Secondary sales via platforms like Forge/EquityZen?

- Government Policy: Will the new administration (post-2024 elections) deliver on promised tax incentives, streamlined approvals, or tech-zone infrastructure?

- GCC Traction: Do Haball, MedIQ, and others convert Saudi/UAE market entry into revenue scale validating cross-border models?

Azfar Hussain, Project Director at National Incubation Center Karachi, captured the moment succinctly: “2025 marked a period of correction and maturity. Capital became more selective, filtering out hype-driven ventures while strengthening founders focused on solving real-world problems. Growth in 2026 will increasingly favor founders who invest in governance, product depth, and regional scalability rather than pursuing rapid expansion or vanity metrics.”

Conclusion: A Pivot, Not a Peak

The story of Pakistan startup funding 2025 is not one of triumphant return to 2021’s heady days. It is, instead, a narrative of adaptation—founders and investors recalibrating expectations, structures, and strategies in response to prolonged capital scarcity and macroeconomic volatility. The pivot to hybrid financing, far from signaling weakness, reflects ecosystem maturation: recognition that sustainable growth, not blitzscaling on cheap capital, suits Pakistan’s current conditions.

When Omer bin Ahsan closed Haball’s $52 million round in April, or Dr. Saira Siddique secured MedIQ’s $6 million in May, they weren’t just fundraising—they were validating new templates. Templates where debt and equity coexist, where Islamic finance principles align with venture returns, where regional expansion to GCC markets complements domestic consolidation, and where profitability timelines matter as much as user acquisition curves.

For Pakistan’s digital economy—still nascent, still fragile, still shadowed by structural challenges—2025’s $74 million across hybrid and equity instruments represents neither arrival nor defeat. It is progress, incremental but real, toward an ecosystem that may never match India’s scale but could nonetheless produce resilient, profitable businesses improving millions of lives. In venture capital, as in geopolitics, survival itself can be a victory. Pakistan’s startups, battered by funding winters and macro headwinds, survived 2025—and in doing so, they sowed seeds for the next phase of growth.

The question is no longer whether Pakistan can build a startup ecosystem. It already has one. The question is whether it can sustain, deepen, and scale what 2025’s hybrid financing surge began.

This analysis synthesizes data from Invest2Innovate, Data Darbar, IMF reports, KPMG Venture Pulse, MAGNiTT, and reporting by Business Recorder, The Express Tribune, Arab News, Financial Times, and other premium sources. All figures current as of January 2026.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Despite the tragedy and turbulence of the Iran conflict, history offers a bracing truth: markets are ruthlessly efficient at discounting temporary shocks. The Straits Times Index, and Asian equities broadly, are built for this moment.

| Indicator | Value | Change |

|---|---|---|

| IMF Global Growth Forecast 2026 | 3.1% | ↓ from 3.3% |

| Brent Crude Peak | $91/bbl | ↑ 18% since tensions |

| STI Level (May 2026) | ~4,850 | Near multi-year highs |

| STI Bull Target (UOB) | 6,500 | 12-month horizon |

Let us begin with the human cost, because market commentary that skips straight to price targets is a form of moral amnesia. The Iran conflict has brought suffering to real people — displacement, economic disruption across the Persian Gulf, elevated anxiety from Oman to Osaka. Any serious analysis must hold that truth in one hand, even while the other reaches for data. The two are not incompatible. Cold-eyed economic realism is not indifference; it is the discipline that separates good policy from panic.

With that said, here is what the historical record tells us with remarkable consistency: wars in the Middle East — even catastrophic ones — do not derail global economic expansions for long. They create violent, temporary dislocations. They reset risk premiums. They punish the complacent. And then, almost invariably, the world adapts, energy markets recalibrate, and equities resume their march upward. The investors who understand this mechanism — and hold their nerve — tend to capture the recovery that the frightened leave on the table.

For Singapore’s Straits Times Index, currently trading near multi-year highs in the 4,700–4,900 range and targeted as high as 6,500 by several institutional desks, the question is not whether this conflict will cause pain. It already has. The question is whether that pain is structural or episodic. History votes decisively for the latter.

The Anatomy of a Market Shock: Three Phases That Always Repeat

Students of geopolitical market history — and I would argue every serious investor should be one — will recognise a recurring three-act structure to how financial markets process armed conflict. It is not a perfect template, but it rhymes with enough consistency to be operationally useful.

Phase 1 — Saber-Rattling Volatility

Diplomatic breakdown, troop movements, and sanctions announcements drive risk-off positioning. Oil spikes on supply-risk premiums. Equities sell off on worst-case headline risks. VIX elevates. This phase is driven by fear of what might happen, not what is happening.

Phase 2 — Worst-Case Pricing

Initial fighting breaks out. Markets price catastrophic scenarios — Strait of Hormuz closure, regional conflagration, supply chain collapse. Sentiment bottoms. This is typically the moment of maximum pessimism, and paradoxically, often the best entry point for investors with long enough horizons to wait out the noise.

Phase 3 — Scope Realisation & Rally

As the conflict’s actual scope becomes clear — limited, contained, manageable — markets rapidly unwind worst-case scenarios. Oil recedes. Equities rally sharply. Underlying growth fundamentals reassert dominance. Recoveries often overshoot the initial drop in the opposite direction.

We are currently navigating the seam between Phase 2 and Phase 3. And that is precisely why the strategic conversation matters most right now.

History’s Unambiguous Verdict on Wars and Markets

The Iraq War of 2003 is the most instructive modern parallel. The Financial Times documented extensively how Brent crude surged through $35 per barrel on invasion fears — a level that felt alarming at the time — only to retreat as coalition forces achieved rapid initial objectives. The S&P 500, which had fallen into correction territory in the weeks before the invasion, bottomed almost precisely on the day ground operations began. Within six months, it had recovered all losses and continued rallying into 2004.

Gulf War I — 1990–91

Iraq’s Kuwait invasion sent Brent to $46/bbl. The S&P 500 fell 20%. Within six months of conflict resolution, U.S. equities had fully recovered and were posting new highs.

9/11 — 2001

NYSE closed for four sessions — the longest halt since 1933. On reopening, the Dow fell 7.1% in a single session. Full recovery came within 31 trading days. Long-run effects were structural and security-related, not cyclical.

Iraq War — 2003

The S&P 500 bottomed on invasion day, March 20. Global equities rose 35%+ over the following twelve months despite the conflict’s protracted nature.

Israel–Gaza Escalation — October 2023

Initial shock sent oil up 9% and regional indices down 4–6%. Within three weeks, most indices had fully retraced. Global growth continued at 3.2% for 2023 per IMF final estimates.

The pattern is not coincidence. It reflects a structural truth about modern globalised economies: they are vastly more diversified, adaptive, and shock-absorbent than any single geopolitical event. As The Economist noted in its landmark analysis of conflict economics, the elasticity of global supply chains — forged through decades of just-in-time logistics and now hardened by post-pandemic diversification — means that the transmission mechanism between Middle East conflict and global recession is far weaker than public discourse assumes.

The Iran Conflict in 2026: Real Disruption, Manageable Scope

The current Iran conflict has, as conflicts do, produced genuine economic dislocation. The IMF’s April 2026 World Economic Outlook revised global growth down to approximately 3.1% from an earlier projection of 3.3% — a meaningful but far from catastrophic reduction. The Fund cited elevated energy prices and heightened uncertainty as the primary transmission channels, with Gulf Cooperation Council economies bearing a disproportionate share of direct impact.

Brent crude touched $91 per barrel at the conflict’s early peak, driven primarily by risk premiums around Strait of Hormuz transit rather than actual supply disruption. The Strait carries approximately 21 million barrels per day — roughly 21% of global petroleum liquids — making it the world’s most critical maritime chokepoint. Partial disruptions, even temporary ones, command an immediate price response. But the market’s pricing of full closure proved, as it almost always does, to be excessive.

“The oil price shock is real. The permanent impairment of global growth is not. These two statements are compatible, and confusing one for the other is the most expensive mistake an investor can make in a crisis.”

Several structural factors limit the long-term damage. First, the International Energy Agency has confirmed that OECD Strategic Petroleum Reserves hold sufficient capacity to offset meaningful supply disruptions for extended periods — the U.S. SPR alone represents roughly 350 million barrels. Second, alternative transit routes via Saudi Arabia’s East-West Pipeline and Oman’s Habshan–Fujairah link, while costlier, remain operational. Third, and critically, the conflict has not — as of this writing — disrupted Iranian crude exports to the degree that many worst-case scenarios projected, partly because key buyers in Asia have maintained pragmatic purchase arrangements through intermediary channels.

For the broader global economy, the energy shock functions like a tax on consumption — painful, regressive, and inflationary at the margin, but not the kind of systemic demand destruction that precipitates recession. World Bank commodity market data suggests that for every $10/bbl sustained increase in crude, global GDP loses approximately 0.15–0.2 percentage points over 12 months. Even at current elevated levels, the arithmetic does not add up to a global contraction.

Why the Straits Times Index Is Built for This Moment

Singapore occupies a peculiar position in the global energy economy — one that makes it both more exposed to energy disruptions and, paradoxically, more resilient to them than almost any other major financial hub. The city-state is the world’s third-largest oil trading centre, home to refining capacity across Jurong Island, and a critical node in Asian LNG distribution. One might expect this to make Singapore equities particularly vulnerable to energy shocks.

In practice, the opposite is often true. Singapore’s banks — DBS, OCBC, and UOB, which collectively dominate STI weighting — earn substantial trade finance revenues from precisely the kinds of commodity flows that intensify during supply disruptions. Higher oil prices, sustained even temporarily, boost the margins on letters of credit, commodity-backed lending, and treasury operations that form the backbone of Singapore banking profitability. Bloomberg Intelligence estimates that for every 10% sustained increase in oil and commodity prices, Singapore bank earnings face a net positive effect of approximately 2–3% through trade finance and treasury channels, more than offsetting any credit quality deterioration in exposed sectors.

STI 2026 — Institutional Price Targets

| Scenario | Target |

|---|---|

| Current Level (May 2026) | ~4,850 |

| Base Case | 5,000 |

| Bull Case | 5,500 |

| UOB Extended Target | 6,500 |

The STI’s composition also offers a natural hedge against the specific risk profile of this conflict. Financial services represent over 40% of index weight; real estate investment trusts a further 12–15%. These sectors are driven primarily by interest rate cycles, domestic economic activity, and regional capital flows — not oil prices. The technology and industrial components, while not immune to global growth headwinds, are tied to the secular AI infrastructure build-out across Southeast Asia, a demand driver that operates on a five-to-ten year horizon, not a quarterly one.

JPMorgan’s Asia equity strategy team and UOB’s research division have both maintained constructive 12-month targets for the STI in the 5,000–6,500 range, citing earnings momentum at Singapore’s major banks — DBS posted record profits in its most recent quarterly result — alongside an attractive valuation discount to regional peers at roughly 11–12x forward earnings. The Straits Times has reported sustained foreign institutional inflows into Singapore equities even as the conflict-driven risk-off move briefly pushed indices lower, suggesting that sophisticated international capital is already separating signal from noise.

Asia’s Structural Resilience: The Longer Arc

Zoom out from the daily price moves, and the picture for Asian equities in 2026 looks structurally compelling in ways that no single geopolitical event can easily undo. The region is mid-cycle in one of the most significant economic transitions of the past generation: the shift from export-led manufacturing dependency toward domestic consumption, services-led growth, and technological capability.

India’s economy, as Reuters reported drawing on IMF data, is tracking approximately 6.5% real GDP growth for 2026 — a pace that makes it the world’s fastest-growing major economy and increasingly a gravitational centre for regional capital flows. ASEAN collectively is forecast by the World Bank East Asia Pacific team to grow at 4.7–5.0%, anchored by Indonesia’s domestic consumption story and Vietnam’s continued manufacturing ascendancy. These are not small-ticket geographies; together they represent a consumer market of over two billion people at various stages of an income transition that wars in distant theatres do not easily interrupt.

The AI infrastructure wave deserves particular attention, because it represents something genuinely new in the global growth calculus. Hyperscaler capital expenditure — from Microsoft, Google, Amazon, and their Asian equivalents in Alibaba, SoftBank, and a resurgent Samsung — is flowing into regional data centres, semiconductor supply chains, and connectivity infrastructure at a pace that structural economists haven’t seen since the original internet buildout of the late 1990s. Singapore is a primary beneficiary of this investment cycle, capturing hyperscaler facility investments that generate construction activity, utility demand, and high-value employment. This is not cyclical demand. It doesn’t care about oil prices in the Persian Gulf.

Energy Diversification: Asia’s Long-Term Hedge

Perhaps the most underappreciated structural shift limiting the long-term damage of Middle East conflicts to Asian growth is the region’s accelerating energy diversification. IEA World Energy Outlook data shows that Asia-Pacific renewable energy capacity additions in 2025 exceeded fossil fuel additions for the first time in history. China added more solar capacity in a single year than the entire installed base of the United Kingdom. India’s renewable auction pipeline runs through 2030 with government-backed certainty.

This is not to suggest that Asian economies have weaned themselves off Persian Gulf oil — they have not, and won’t for years. But the marginal sensitivity of Asian growth to oil supply disruptions is measurably declining with each passing year. The elasticity that made the 1973 OPEC embargo or the 1979 Iranian Revolution so economically devastating — when oil represented a far larger share of industrial cost structures — is simply not present in the same magnitude today. Electric vehicles, efficiency improvements, and fuel substitution mean that a $91 barrel in 2026 carries roughly 60–65% of the economic punch that the same real-price level carried in 1990.

The Bull Case, Stated Plainly

Let me be direct about what the evidence suggests, shorn of false modesty or performative hedging. The Iran conflict has created a temporary and likely partially reversible oil shock. It has shaved perhaps 0.2 percentage points from 2026 global growth — meaningful at the margin, not transformative in its consequence. It has caused equity markets, including Singapore’s, to experience exactly the kind of short-term volatility that long-horizon investors should view as opportunity rather than threat.

The STI, sitting near 4,850 with institutional targets ranging from 5,000 to 6,500, is backed by earnings momentum in its largest constituents, attractive relative valuations, sustained foreign inflows, and Singapore’s structural position as the premier financial and trade hub of Southeast Asia — a region that is, by any credible measure, the most dynamic growth theatre in the global economy over the next decade.

The three-phase market reaction framework has, historically, resolved in Phase 3 rallies that often exceed the initial Phase 1–2 drawdowns. The Gulf War I resolution produced a 25% S&P rally within six months. The Iraq War produced 35% global equity gains over twelve months. The Israel-Gaza shock of October 2023 reversed within three weeks. Each instance differed in its specifics; all of them rhymed in their resolution. There is no obvious reason why 2026 should be the exception to a pattern that reflects deep structural truths about how modern market economies process and absorb geopolitical shocks.

The Caveats That Honest Analysis Demands

None of this is to suggest complacency. Several scenarios could meaningfully extend the disruption beyond what history’s template predicts. A full Strait of Hormuz closure sustained beyond six weeks would test SPR capacity and force genuine demand destruction. Iranian missile strikes on Saudi Arabian production infrastructure — as occurred briefly in the Abqaiq attack of 2019 — would be a different order of shock altogether. A broadening of the conflict to involve Hezbollah on a full-war footing, with implications for Israeli and Lebanese economic activity, would expand the affected geography significantly.

Investors in Singapore and Asia more broadly should maintain scenario discipline: size positions to weather a Phase 2 extension, hedge energy exposures where cost-effective, and resist the temptation to over-extrapolate short-term commodity moves into long-duration equity valuations. The VIX is not a perpetual state. Neither is a $91 oil price, which implies market expectations of sustained supply tightness that historical precedent suggests are almost always too pessimistic.

Central bank policy adds another layer of complexity. The U.S. Federal Reserve, already navigating a delicate path between residual inflation and softening labour markets, faces renewed upward pressure from energy costs. Fed communications in recent weeks have carefully preserved optionality on rate cuts, which means the anticipated monetary tailwind for risk assets may arrive later than pre-conflict pricing implied. This is a headwind, not a structural impediment.

Conclusion: Resilience Is Not Optimism, It Is History

There is a tendency, in moments of geopolitical stress, to mistake the intensity of news flow for the magnitude of economic consequence. These are not the same thing. The Iran conflict is, by any human measure, a serious and tragic event. By the measure of global economic history, it is an episodic shock to a system that has repeatedly demonstrated its capacity to absorb, adapt, and resume growth.

The Straits Times Index, rooted in the earnings power of world-class financial institutions and the structural growth of Southeast Asia’s most important commercial hub, does not need geopolitical calm to compound value over time. It needs the structural tailwinds — regional growth, AI investment, trade finance expansion, tourism recovery — to continue. They are continuing.

History does not repeat. But it rhymes with sufficient regularity that investors who study it carefully tend to act at precisely the moments when others are paralysed by fear. Phase 3 is coming. It always does. The only question worth asking, right now, is whether you intend to be positioned for it.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Greg Abel’s Patient Baton: How Discipline—Not Drama—Will Define Berkshire Hathaway’s Next Century

Greg Abel’s first annual meeting as Berkshire Hathaway CEO delivered a clear signal: patience and disciplined capital allocation will define the post-Buffett era. With a record $397.4 billion cash pile and operating earnings up 18%, here’s what investors need to understand.

The Morning After a Legend Leaves the Stage

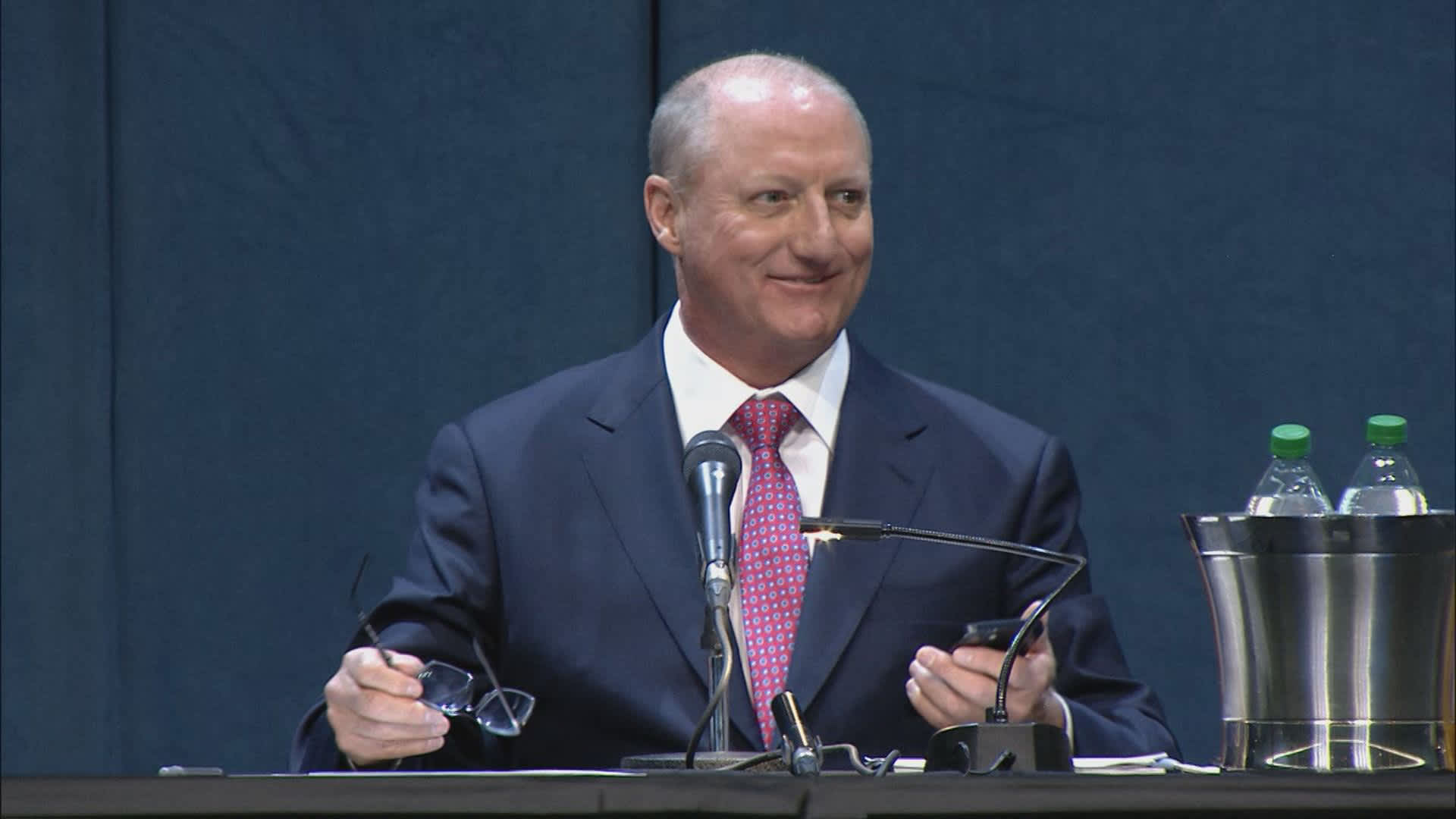

When someone really special steps down, it gets really quiet. On May 2, 2026, at the CHI Health Center in Omaha, Nebraska, the people who own parts of Berkshire Hathaway got together for their yearly meeting. This was the first time in 60 years that Warren Buffett wasn’t in charge of the meeting. The big room was only half full, which was really different from the 40,000 people who used to come every year. And the simple, wise sayings that Warren Buffett used to share with everyone were mostly gone.

It felt like something was missing, like the air in the room wasn’t the same without him. The meeting was still important, but it wasn’t the same without the person who had been leading it for so long. People were probably thinking about how things would change now that Warren Buffett wasn’t in charge. The quiet in the room was like a sign that something big had happened, and everyone was waiting to see what would come next. Instead of flashy announcements, the CEO focused on in-depth business talks, key performance numbers, and a well-structured approach. As the sole leader of the sixth-largest company in the world, he gave his first public presentation and said exactly what long-term investors wanted to hear. He showed that he is a careful and disciplined CEO, which is what the company needed at this time. This approach was a breath of fresh air for investors who are in it for the long haul.

“One of our greatest strengths at Berkshire is patience and being disciplined at allocating our capital. We’re not anxious to deploy capital into subpar opportunities.” — Greg Abel, Berkshire Hathaway CEO, Omaha, May 2, 2026

Greg Abel, 63, the Canadian-born engineer-turned-conglomerate-executive who spent more than 25 years earning Buffett’s trust, stood before shareholders and said something profoundly unfashionable in an era of algorithmic trading, AI hype cycles, and relentless activist pressure: we are not in a hurry.

That restraint is not timidity. It is strategy. And understanding why it may be the most sophisticated capital allocation posture available to a $1 trillion enterprise in today’s market environment is the central task of this analysis.

Abel’s First Letter: Stewardship, Not Showmanship

Before the Omaha meeting, Abel authored his first annual shareholder letter as CEO—a document that financial analysts, value investors, and institutional allocators parsed with the intensity usually reserved for Federal Reserve minutes. The letter’s opening paragraph set the tone with elegant simplicity: “Your capital is commingled with ours, but it does not belong to us. Our role is stewardship.”

That single sentence—eight words distilled from decades of Buffett doctrine—tells you nearly everything about how Abel intends to run Berkshire. He is not positioning himself as a disruptor. He is positioning himself as a custodian.

The letter repeatedly invoked net operating cash flow as the true compass for evaluating Berkshire’s varied businesses, comparing current performance against five-year averages rather than quarterly analyst estimates. Abel committed to assessing value carefully, acting patiently, and holding for the long term—”preferably forever.” He reiterated the fortress balance sheet as a non-negotiable asset, writing that Berkshire’s liquidity ensures the company “can act decisively when opportunities appear and remain resilient during difficult periods.”

This is the language of a man who has read the entire Buffett canon, internalized it, and is now authoring the next chapter in the same idiom—without copying the syntax.

The $397 Billion Question: Patience or Paralysis?

The most provocative number hovering over the 2026 annual meeting was not an earnings figure but a bank balance. Berkshire’s cash, Treasury bills, and short-term securities reached a record $397.4 billion at the end of Q1 2026, up from $373 billion at year-end 2025—itself a record inherited from Buffett’s 13-consecutive-quarter streak as a net seller of equities.

For context, $397 billion is roughly the GDP of Malaysia. It exceeds the market capitalization of most S&P 500 companies. It is not a liquidity buffer. It is a strategic arsenal.

Critics will frame this as elephantine inertia—a conglomerate so large it can no longer find elephants large enough to hunt. That framing mistakes constraint for character. Berkshire is not sitting on cash because it cannot decide what to buy. It is sitting on cash because, as both Abel and Buffett made clear on Saturday, the prices being asked for most assets do not reflect the returns Berkshire requires.

Buffett, now 95 and attending as chairman emeritus, said it plainly in a sideline interview with CNBC’s Becky Quick: “It isn’t our ideal environment in terms of deploying cash for Berkshire,” citing elevated market valuations as the central obstacle. He noted that prices for “an awful lot of things will look awfully silly,” channeling the same sensibility he expressed in his famous 1999 Fortune essay warning against extrapolating a decade of equity returns into the next.

Abel echoed the sentiment from the stage with characteristic operational precision: “It doesn’t mean you need to deploy all your capital and spend all your money.” He acknowledged that Berkshire had identified several firms with interesting management and operations but wasn’t interested in paying current valuations to own them. This is not indecision—it is the Ted Williams strike zone philosophy applied to corporate finance. Wait for your pitch.

The brilliance of that posture becomes clearer when you consider the alternative. A CEO who felt compelled to spend $400 billion to demonstrate decisiveness would almost certainly overpay, diluting decades of compounding in the process. The history of corporate M&A is a graveyard of such urgency.

Operating Results: The Unglamorous Engine Keeps Humming

While the cash pile attracts the headlines, the underlying engine of Berkshire’s operating businesses continues to generate returns that most conglomerates can only envy. Q1 2026 operating earnings came in at $11.35 billion, up nearly 18% year-over-year—a number that reflects the durable cash generation of Berkshire’s 60-plus operating subsidiaries rather than the volatility of mark-to-market investment gains.

Net income attributable to shareholders more than doubled, rising to $10.1 billion from $4.6 billion in Q1 2025, as the value of Berkshire’s equity portfolio—still anchored by Apple, American Express, Coca-Cola, and Moody’s—appreciated sharply.

The insurance segment, long the golden goose of Berkshire’s float-driven model, delivered an underwriting profit of $1.7 billion, up from $1.34 billion in the same period last year. Ajit Jain, the legendary insurance chief who joined Abel onstage in Omaha, reinforced the discipline-over-volume philosophy: insurance premiums are only written when they can be done profitably, on terms that make sense for the long haul. When the market softens and competitors chase volume at inadequate rates, Berkshire pulls back—even if the resulting numbers look temporarily rough.

BNSF railroad and Berkshire Hathaway Energy both showed improved operating results, with Abel spending considerable time on his energy businesses’ pivotal role in the AI infrastructure buildout. His observation that hyperscalers and data centers “have to bear the full cost” of the energy they consume was both a policy statement and a revenue signal: Berkshire’s utility assets are positioned to be among the key beneficiaries of the data center boom, provided the regulatory and cost frameworks are structured fairly.

Continuity vs. Evolution: What Actually Changes Under Abel?

The meeting carried the branding “The Legacy Continues”—a phrase that could read as reassurance or as obligation, depending on your disposition. For investors trying to map Abel’s tenure against Buffett’s, three meaningful differences are worth tracking closely.

Communication style. Buffett translated capitalism into parable. Abel translates it into operations. Where Buffett might invoke Ben Franklin, Abel will cite net operating cash flow and five-year averages. This is not a deficiency—it is a different skill set. Abel spent decades as the hands-on operator of Berkshire Hathaway Energy, running a complex regulated utility empire across multiple jurisdictions. He thinks in infrastructure, not allegory. Shareholders who were drawn to Omaha for Buffett’s wit will need to recalibrate; those drawn for financial substance will find Abel’s style more directly useful.

Collaborative leadership. Abel notably shared the stage with his top lieutenants—a departure from the Buffett-Munger bilateral that defined the meeting’s format for decades. CEOs of Dairy Queen, See’s Candies, Brooks Running, and Jazwares were given time to address shareholders. NetJets CEO Adam Johnson, who now oversees 32 retail and service businesses, was prominently featured. This distributed model signals something important: Abel is building an institutional structure, not a cult of personality. When the latter is inevitable (as it was with Buffett), it is also irreplaceable. When the former is constructed deliberately, it endures.

Technology posture. Buffett famously avoided technology investments for most of his career, then made an extraordinarily well-timed bet on Apple. Abel is carving out a more nuanced stance. He told shareholders that Berkshire “isn’t going to do AI for the sake of AI,” but acknowledged that AI presents both significant opportunities (particularly through the energy infrastructure that powers data centers) and existential risks—including the cybersecurity vulnerabilities illustrated, somewhat surreally, when the first shareholder question of the day arrived via a deepfake of Buffett himself.

The Cultural Moat: Berkshire’s True Durable Advantage

Perhaps the most underappreciated element of Berkshire’s post-Buffett positioning is the cultural architecture that Buffett spent 60 years constructing. Dan Sheridan, CEO of Brooks Running, captured it well from the floor of the exhibit hall: “I think this is a very deeply rooted culture that Warren has created, and I believe the transition to Greg is going to be rooted in those values that Warren has for 60 years instituted and will continue.”

That culture operates on several levels simultaneously. At the subsidiary level, Berkshire’s radical decentralization—CEOs run their businesses with minimal headquarters interference, maximizing accountability and entrepreneurial energy—has survived multiple management transitions at the operating company level without degradation. At the capital allocation level, the aversion to what Abel called the “ABCs”—arrogance, bureaucracy, and complacency—functions as an immune system against the empire-building tendencies that have destroyed shareholder value at comparable conglomerates.

Critically, the float model—insurance premiums invested in equities and bonds before claims are paid—remains structurally intact and irreplaceable. No competitor can simply choose to replicate it. It took Buffett and Jain decades to build GEICO and General Re and the reinsurance operations into the capital generation machines they are today. This is the moat that other moats flow from, and Abel understands it at the granular operational level that the job requires.

The Japan Chapter: Patient Capital’s Finest Recent Chapter

One of Buffett’s most celebrated late-career decisions—accumulating roughly $20 billion in stakes across five major Japanese trading houses (Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo)—remains a template for how Berkshire approaches patient capital deployment at scale. Those positions, initiated quietly in 2019 and revealed on Buffett’s 90th birthday, have since generated substantial gains as the trading companies reported record profits, increased dividends, and bought back shares aggressively.

The Japan investments embody the Berkshire thesis in concentrated form: identify businesses with durable economics trading at irrational discounts, accumulate quietly, hold without the pressure to demonstrate activity, and let compounding do the heavy lifting. Abel has signaled that Berkshire’s relationship with its Japanese partners will continue and deepen. More broadly, the Japan playbook offers a template for how $397 billion in dry powder might eventually be deployed—not in a single transformative acquisition, but in patient accumulation of concentrated positions in undervalued, cash-generative businesses, wherever global dislocations create them.

Key Investor Takeaways

For investors assessing Berkshire in the post-Buffett era, several signals deserve close attention:

- The buyback signal. Berkshire repurchased $234.2 million in stock during Q1 2026—modest but meaningful, its first buyback activity since May 2024. The resumption suggests Abel views current prices as at or below intrinsic value, a useful calibration data point. The average Class A repurchase price of $729,701 and Class B price of ~$486.92 establish implicit floor valuations.

- The valuation discipline signal. Abel explicitly told shareholders that Berkshire has identified companies with excellent management and operations but won’t pay current prices. This is Berkshire’s version of a disciplined capital deployment framework: the opportunity set exists, but the entry prices do not yet justify action.

- The insurance discipline signal. Jain’s comments about pulling back in competitive market conditions—even at the cost of volume—confirm that Berkshire’s insurance profitability is structural, not cyclical. The $1.7 billion underwriting profit in a quarter when peers were facing elevated catastrophe losses is not accidental.

- The AI infrastructure signal. Abel’s emphasis on Berkshire’s energy businesses as essential infrastructure for the data center boom represents the most actionable near-term growth vector for a company of Berkshire’s scale. Unlike direct AI investments, utilities provide regulated, predictable returns with AI-driven tailwinds—precisely the kind of investment profile Berkshire has always preferred.

The Elephant in the Room: Scale as Berkshire’s Primary Challenge

Any honest analysis of Berkshire’s post-Buffett prospects must grapple with the constraint that Abel himself will never quite name directly: size. At roughly $1 trillion in market capitalization and $397 billion in available capital, Berkshire has effectively outgrown the universe of investments that can move the needle. A $10 billion acquisition that would transform a mid-cap company is almost irrelevant to Berkshire’s per-share value. Only acquisitions in the $50 billion–$150 billion range register meaningfully—and at current valuations, such acquisitions are nearly impossible to execute at returns Berkshire would accept.

This is the fundamental tension of the Abel era, and it has no clean resolution. The most likely outcome is a gradual shift toward more international exposure (building on the Japan template), larger bolt-on acquisitions within existing verticals like energy and industrials where Abel has the deepest expertise, and continued share repurchases when prices are attractive.

What the scale constraint definitively rules out is the kind of transformative bet—a General Re in 1998, a Burlington Northern in 2009—that Buffett made at critical junctures to reshape Berkshire’s future. Those opportunities required not just capital but a market dislocation severe enough to offer Berkshire-sized targets at Berkshire-acceptable prices. They are rare, and when they appear, Abel will need to act with the conviction of someone who has never previously managed an investment portfolio at the public company level. That is a legitimate and unresolved question.

Why Patience Remains a Superpower

Buffett, in his sideline CNBC interview, made an observation that cuts to the heart of why Berkshire’s cash patience is a genuine competitive advantage rather than institutional inertia: “We’ve never had more people in a gambling mood than now.”

The evidence is abundant. Retail options volumes at record highs. Meme stocks cycling in and out of speculative manias. Cryptocurrency valuations that defy discounted cash flow analysis. AI-adjacent companies trading at revenue multiples that price in decades of flawless execution. In this environment, a company with $397 billion in dry powder and the institutional culture to resist deployment pressure is not being passive—it is accumulating an option on the next dislocation.

Those dislocations come. They always do. In 2008, Berkshire deployed capital into Goldman Sachs and General Electric at terms available only to lenders of last resort. In 2020, Berkshire was slower to deploy than the historical record would suggest it should have been—a fact Buffett himself acknowledged—but the Japanese trading house accumulation that began in 2019 proved masterful timing in retrospect. The lesson is not that Berkshire is infallible. It is that a company with permanent capital, a fortress balance sheet, and the patience to wait for its pitch will consistently outperform over the full cycle, even if it lags in the middle innings of a bull market.

Berkshire’s Class B shares have underperformed the S&P 500 by 12.4% since Abel was named CEO—a datapoint that bears watching but almost certainly reflects the transition anxiety of a shareholder base recalibrating to a new face rather than any deterioration in the underlying business. For long-term investors, this is exactly the kind of sentiment-driven dislocation that Berkshire’s own investment framework would identify as an opportunity.

Conclusion: The Long Game Is the Only Game Berkshire Plays

Greg Abel is not Warren Buffett. He will never be Warren Buffett. And the sooner investors stop expecting him to be, the sooner they will be able to see what he actually is: a disciplined, operationally sophisticated, culturally literate steward of one of the greatest capital allocation machines ever assembled.

His first shareholder letter established the terms of engagement with clarity and humility. His first annual meeting—delivered without the safety net of Buffett’s presence on stage—demonstrated that he can hold the room, manage the Q&A, honor the legacy, and chart a forward course, all simultaneously. Warren Buffett himself, watching from the audience, told the crowd that Abel is “very, very smart about businesses” and expressed satisfaction with the timing and execution of the transition.

The fundamental premises of Berkshire’s model—permanent capital, decentralized operations, float-funded investing, cultural alignment, and an absolute refusal to deploy capital into subpar opportunities—remain intact under Abel’s stewardship. The $397 billion in cash is not a problem to be solved. It is a testament to sixty years of disciplined refusal to be rushed. In an investment landscape increasingly defined by the tyranny of the quarterly calendar, that refusal is rarer and more valuable than ever.

Patience, as Abel put it in Omaha, is one of Berkshire’s greatest strengths. The market will spend the next several quarters deciding whether to believe him. The long-term record suggests it probably should.

Key Takeaways at a Glance

- Berkshire’s Q1 2026 cash pile hit a record $397.4 billion, up from $373 billion at year-end 2025

- Operating earnings rose 18% year-over-year to $11.35 billion in Q1 2026

- Abel’s core message: patience in capital allocation is a strength, not a failure to act

- Abel explicitly confirmed Berkshire has identified good companies but won’t pay today’s elevated prices

- Insurance underwriting profit of $1.7 billion confirms the structural strength of the float model

- The first share buybacks since May 2024 ($234.2 million) signal Abel’s view on intrinsic value

- The culture of decentralization, anti-bureaucracy, and long-term holding is explicitly preserved

- Energy/utility infrastructure is positioned as Berkshire’s primary near-term AI-era growth vector

- Buffett publicly praised Abel as “very, very smart about businesses”

Frequently Asked Questions

Q: Who is Greg Abel and why is he running Berkshire Hathaway? Greg Abel, 63, is a Canadian-born executive who spent more than 25 years at Berkshire Hathaway, primarily as the head of Berkshire Hathaway Energy. He was publicly identified as Buffett’s successor in 2021 and became CEO on January 1, 2026, after Buffett announced his retirement at the 2025 annual meeting. Buffett remains chairman emeritus.

Q: Why is Berkshire Hathaway not deploying its $397 billion cash pile? Abel has stated clearly that Berkshire will not deploy capital into “subpar opportunities”—meaning companies whose current market prices do not offer the return profile Berkshire requires for long-term compounding. With equity markets trading at historically elevated valuations, the opportunity cost of patience is low while the risk of overpaying is high. Buffett separately noted that the current environment is “not ideal” for deploying Berkshire’s cash.

Q: How did Berkshire perform in Q1 2026 under Greg Abel? Berkshire reported operating earnings of $11.35 billion in Q1 2026, up nearly 18% from the prior year. Net income more than doubled to $10.1 billion. The insurance segment reported a $1.7 billion underwriting profit, up from $1.34 billion. The cash pile grew to a record $397.4 billion from $373 billion at year-end 2025.

Q: Is Greg Abel’s investment style different from Warren Buffett’s? Abel communicates in operational specifics rather than Buffett’s parables, but the underlying investment philosophy—patience, discipline, long holding periods, cultural alignment, refusal to overpay—is explicitly preserved. Abel has also signaled a more systematic approach to leadership, sharing the stage with subsidiary CEOs and building an institutional rather than personality-driven culture.

Q: What is Berkshire Hathaway’s approach to artificial intelligence under Greg Abel? Abel stated that Berkshire will not “do AI for the sake of AI.” The conglomerate’s most direct AI exposure comes through Berkshire Hathaway Energy, whose utility assets power data centers. Abel argued that hyperscalers must bear the full cost of the energy they consume, positioning Berkshire’s utilities as infrastructure beneficiaries of the AI buildout. He also flagged cybersecurity as a significant risk being actively managed, particularly within the insurance businesses.

Q: Should long-term investors hold Berkshire Hathaway stock under Greg Abel? This is a financial decision that depends on individual circumstances, and readers should consult a financial advisor. Analytically, Berkshire’s Class B shares have underperformed the S&P 500 by approximately 12.4% since Abel was named CEO—likely reflecting transition anxiety rather than fundamental deterioration. The underlying business continues to generate record operating earnings and a growing cash reserve, and Abel has demonstrated cultural continuity with the Buffett playbook. Investors with long time horizons who value capital preservation and disciplined compounding have hi

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

KKR’s $10 Billion Exit Gamble: What the Potential Sale of Its Ex-Unilever Spreads Empire Reveals

Eight years after the largest European leveraged buyout of 2017, KKR is back at the table — this time on the sell side. The question is whether the market is ready to pay up for a business straddling one of consumer goods’ most contested fault lines.

Walk into any well-stocked supermarket in Amsterdam, Lagos, or São Paulo and you will find it — a cheerful yellow tub, modest in size but outsized in ambition. Flora, the plant-based spread that has graced European breakfast tables for six decades, is today the flagship of Flora Food Group, a Dutch food conglomerate that also owns Blue Band, Becel, Country Crock, I Can’t Believe It’s Not Butter!, and Violife — and, critically, the entire strategic wager that Kohlberg Kravis Roberts placed on the long-term viability of plant-based fats when it carved out Unilever’s spreads division in 2018.

That wager is now approaching its verdict. Bloomberg reported on 30 April 2026 that KKR is actively exploring a sale of Flora Food Group for as much as $10 billion, with sell-side advisers working through potential buyer meetings. It is a figure that sounds impressive until you trace the deal’s full arc — and then it begins to look rather more complicated.

The story of how a margarine portfolio became a $10 billion negotiation is, at its core, a story about private equity’s enduring faith in categories that the wider market has given up on, the fickle nature of consumer health trends, and what happens when a highly leveraged buyout runs headlong into an era of rising dairy butter, retreating plant-based enthusiasm, and stubbornly high borrowing costs. It is also, frankly, a stress test of whether KKR — one of the world’s most sophisticated dealmakers — can deliver a return that justifies the wait.

Sprexit: How KKR Came to Own the World’s Largest Margarine Empire

To understand where Flora Food Group stands today, it is necessary to revisit the catalysing crisis that brought it into existence as a standalone entity. In February 2017, Kraft Heinz launched an unsolicited $143 billion takeover bid for Unilever — a brazen move that shocked the consumer goods establishment and sent Unilever’s chief executive, Paul Polman, scrambling for a defensive narrative. The bid was rebuffed within days, but its lasting effect was to commit Unilever to a more ruthless posture on portfolio rationalisation.

The spreads business — margarine, plant-based blends, cooking fats — was an obvious candidate for disposal. In the five years leading to 2014, global margarine sales had fallen roughly 6% while butter sales climbed 7%. The category carried robust margins but declining volumes, an awkward combination in an age when activist investors demanded growth, not mere profitability. In April 2017, Unilever formally put the division up for sale, sparking a bidding war that drew Apollo, CVC, Bain Capital, and Clayton, Dubilier & Rice before KKR prevailed at €6.825 billion ($8.04 billion) — the biggest leveraged buyout in Europe that year.

The business was renamed Upfield, and KKR’s thesis was clear: strip out corporate overhead from a business that had been slowly suffocating inside Unilever’s vast machine, pivot aggressively toward plant-based positioning, leverage the portfolio’s extraordinary global reach — present in roughly 100 countries — and exit within five to seven years at a healthy premium. It was a template that private equity had successfully applied to other Unilever orphans: HUL’s flavours unit, Coty’s beauty brands, Alberto-Culver. Why not margarine?

“Private equity’s love affair with declining categories is built on a simple insight: mature businesses can generate tremendous cash, if only you are willing to manage them without corporate sentimentality.”

KKR’s Stewardship: The Good, the Complicated, and the Debt Pile

KKR did deliver genuine operational discipline. Upfield shed excess manufacturing capacity, consolidated back-office functions, and pushed aggressively into plant-based innovation — purchasing Violife, the Greek plant-based cheese brand, in 2020 and investing €50 million in a new research and development campus. The rebranding to Flora Food Group in September 2024 was itself a signal: an effort to align the portfolio’s identity with its plant-based ambitions and shed the Upfield name, which had never quite achieved commercial resonance beyond the trade press.

The financial results tell a story of resilience, if not quite triumph. Flora Food Group’s 2024 Annual Report disclosed €3.1 billion in net sales, with 96% of product volumes meeting core nutrition benchmarks. By 2025, the company’s investor page cited approximately €3.0 billion in net sales — a slight decline year on year, and a figure that, while not catastrophic, suggests the business is managing volumes rather than growing them. For a leveraged buyout carrying the kind of debt load Upfield accumulated, that distinction matters enormously.

And here lies the central complication. According to Reorg Research, Flora Food Group’s reported leverage ratio stood at 6.9x net debt to EBITDA as of September 2023 — elevated even by leveraged buyout standards, and a direct consequence of the structure that financed the original €6.8 billion acquisition. In July 2023, the company was compelled to extend the maturity of term loan tranches totalling over €3 billion across three currencies to January 2028, buying time but also advertising to the market that the original exit runway had narrowed.

This debt burden is why Bloomberg reported in February 2025 that KKR was likely to hold the business until at least 2026 — not out of lingering affection for margarine, but because a sale at the time would not have cleared the debt cleanly enough to return meaningful equity to KKR’s funds. The ADQ talks of 2024, which collapsed over price disagreements with the Abu Dhabi sovereign wealth fund, were a missed opportunity that has since complicated the exit narrative.

Flora Food Group — Key Financials at a Glance (April 2026)

| Metric | Value |

|---|---|

| Net Sales 2024 | €3.1 billion |

| Net Sales 2025 | ~€3.0 billion |

| Target Valuation | ~$10 billion |

| EBITDA (marketed) | €800M–€900M |

| Leverage (Sept 2023) | 6.9x net debt/EBITDA |

| Countries of Operation | ~100 |

| Employees | ~4,600 |

| M&A Advisers | Citi, Goldman Sachs |

The Butter Counter-Revolution: Market Dynamics That Complicate the Story

KKR bought into spreads at precisely the moment when the broader culture appeared to be pivoting against them — and then doubled down on plant-based at precisely the moment when that pivot showed signs of plateauing. Both moves were defensible at the time; both are now being tested.

Dairy’s Quiet Comeback

The rehabilitation of butter — once demonised as a cardiovascular villain — has been one of consumer goods’ most striking reversals of the past decade. Driven by the rise of full-fat, clean-label, ketogenic, and ancestral dietary philosophies, butter has recovered not just cultural cachet but commercial mass. The global butter market was valued at $43.83 billion in 2025 and is projected to grow at a compound annual rate of 4.34% to reach $63.49 billion by 2034 — a rate that comfortably outpaces most plant-based spread forecasts. In the United States, the shift toward grass-fed, organic, and artisanal butter has eroded the margarine aisle in a way that no marketing campaign has convincingly reversed.

This is not merely a fashionable food trend. It reflects a genuine paradigm shift in nutritional thinking: saturated fats, once the enemy, have been partly rehabilitated by a body of research questioning the oversimplified fat-heart disease hypothesis. Consumers who once reached for “I Can’t Believe It’s Not Butter!” because they believed it was healthier are now, with similar conviction, reaching for Kerrygold or Président. The irony — and strategic challenge — for Flora Food Group is that several of its most storied brands built their identity on exactly this anti-dairy, pro-margarine messaging that has now fallen out of favour.

The Plant-Based Plateau

The plant-based food category, which experienced its evangelical peak around 2019–2021, has since entered a more sobering phase. Data from SPINS compiled by the Good Food Institute shows that in 2025, total US retail plant-based food dollar sales declined 2% and unit volumes also fell 2%. While the overall retail market still totalled $7.9 billion — double its 2017 size — the trajectory has clearly flattened, and the declines in premium categories have been steeper than the headlines suggest. Taste gaps, price premiums versus conventional equivalents, and a broader consumer pullback on discretionary spending have all compounded.

Flora Food Group’s flagship product range spans this contested territory. Its plant-based butters and spreads remain category leaders, and it has invested genuinely in reformulation and sustainability packaging — Mintel noted in late 2025 that Flora Food Group launched what it described as the world’s first plastic-free recyclable tub for plant butters. But innovation in packaging does not address the more fundamental tension: the consumer who most fervently wants plant-based butter is also the consumer most likely to make her own nut butter or seek out artisan alternatives. The mass-market grocery shopper, who is Flora’s bread and butter (so to speak), remains stubbornly ambivalent.

Volume Compression and Pricing Power

The post-pandemic inflation cycle placed heavy input cost pressure on fat-based products — vegetable oils, palm oil, sunflower oil — before the commodity cycle partially reversed. Flora Food Group navigated this environment through pricing actions, but pricing in a commodity-adjacent category has limits. When a business reports approximately €3.0 billion in net sales in 2025 versus €3.1 billion in 2024, the question of whether the modest decline reflects volume pressure, price normalisation, or deliberate strategic SKU rationalisation becomes critical to valuation. For prospective buyers underwriting a $10 billion enterprise value, the answer to that question matters enormously.

Can KKR Double Its Money on Margarine? The Valuation Puzzle

At $10 billion, KKR would be booking a nominal gain of approximately $2 billion, or roughly 25%, over its original $8 billion acquisition cost — before accounting for the costs of eight years of debt service on a heavily leveraged structure. In real terms, adjusting for the time value of money, this would represent a distinctly mediocre return on one of the largest consumer staples buyouts in history.

The mathematics depend critically on how one frames the EBITDA multiple. According to Reorg Research, the business is being marketed off EBITDA of between €800 million and €900 million depending on adjustments — a range that implies an enterprise value multiple of roughly 10 to 11 times EBITDA at the $10 billion headline price (accounting for current EUR/USD exchange dynamics). That is not an unreasonable multiple for a branded consumer staples business with genuine global distribution depth and category leadership in plant-based fats. Comparable acquisitions in the European consumer staples universe have traded at 9 to 13 times EBITDA in recent years, depending on growth profile and leverage.

Bull case for $10bn: A strategic buyer — a sovereign wealth fund, a major Asian food conglomerate, or a CPG giant seeking instant scale in plant-based — could justify paying a 10–11x EBITDA multiple for a business with genuinely irreplaceable global distribution across 100 countries, a portfolio of household-name brands, and what remains the world’s largest plant-based consumer packaged goods platform.

Bear case: The leverage overhang, the declining revenue trajectory, and the structural headwinds in core geographies could compress the achievable multiple to 8–9x — implying a significantly lower clearing price, and one that would require much more creative structuring to make the numbers work for KKR’s fund economics.

The ADQ precedent: The failed 2024 sale to Abu Dhabi’s ADQ at roughly the same $10 billion headline suggests that the price gap between seller expectations and buyer willingness has not materially closed. KKR’s decision to hold for another year to tackle the debt pile may have improved the credit story, but it has not transformed the strategic narrative.

The question — can KKR double its money on margarine? — turns out to have a sobering answer: almost certainly not, at least not on an equity-return basis. What KKR can hope for is a clean exit that returns capital to its 2018-vintage funds, clears the debt, and allows it to characterise the investment as a value-preservation story in a difficult macro environment. For a firm of KKR’s stature and track record, that framing is available. It simply is not the triumph the original thesis promised.

“The deal that was once the largest leveraged buyout in Europe may ultimately be remembered less for its returns than for the market education it provided about the limits of plant-based premiumisation in a mainstream grocery context.”

The PE Exit Environment: Why 2026 Is Both Better and More Complicated

Private equity’s exit machine, which seized up dramatically when interest rates rose sharply in 2022–2023, has been slowly unjamming. Sponsor-to-sponsor deals have picked up, strategic acquirers are returning to the table, and several large IPO windows opened in late 2025. But the consumer staples segment remains challenging: growth profiles are thin, commodity exposure creates earnings volatility, and public market investors — burned by the de-ratings of 2022 — remain sceptical of high-multiple consumer deals.

For KKR, the 2028 debt maturity creates a structural deadline that is not fully negotiable. A sale in 2026 would provide a comfortable runway; a failed sale in 2026 reopens the IPO and minority-stake options that KKR had previously considered. The appointment of Citi and Goldman Sachs as sell-side advisers signals that this process is real, not exploratory — the bankers’ fireplace chats with potential buyers are underway, and the buyer universe will likely include Middle Eastern sovereign funds, Asian strategic players (Japan’s Kewpie, India’s Tata Consumer, or similar), and potentially a consortium structure that lets multiple buyers share the risk of a $10 billion bet on fats.

What This Tells Us About Private Equity in Slow-Growth Consumer Categories

The Flora Food Group saga is instructive well beyond the specifics of margarine and plant-based spreads. It illustrates the particular tensions that arise when private equity buys a structurally challenged category and attempts to re-narrative it as a growth story through brand reorientation and sustainability positioning.