China Economy

China’s Economy Is Now Dangerously Dependent on One Thing: Exports

China’s economy has held up better than many expected through 2026’s geopolitical turbulence, with growth for the second quarter tracking toward roughly 4.5% year-on-year, according to a median forecast of analysts surveyed by AFP — a step down from 5% in the prior quarter but still within the government’s 4.5–5% annual target. The headline resilience, however, is masking a structural shift that has received far less attention than it deserves: China’s growth engine has become almost entirely dependent on one lever, exports, at exactly the moment that lever faces the most geopolitical uncertainty in years.

The Domestic Engine Has Effectively Stalled

The data on China’s internal economy is stark. Retail sales fell for the first time in three years in May, despite the government pumping billions of yuan into special bonds supporting consumer trade-in subsidy programmes since 2024. Fixed-asset investment has also slumped. Rabobank’s Teeuwe Mevissen summarised the underlying problem bluntly: with no signal that the real estate crisis is ending, a recovery in consumption is hard to envision — a crisis now in its fifth consecutive year, with once-reliable home prices stagnating and dissuading buyers from treating property as a store of wealth.

The World Bank’s own July 2026 update confirms the property drag is structural rather than cyclical, projecting growth to slow to 4.4% in 2026 and 4.3% in 2027 as the property sector continues adjusting to genuinely lower housing demand. The Bank’s specific policy recommendation — strengthening the social safety net by raising benefit levels and extending coverage to informal workers — is a tacit admission that Chinese households are saving defensively rather than spending, precisely because they lack the social insurance that would let them draw down savings with confidence.

Exports Are Doing All the Work

What’s compensating for this domestic weakness is a genuinely resilient export sector. Goldman Sachs Research projects China’s current account surplus will rise to 4.2% of GDP in 2026, up from 3.6% in 2025 — a materially more bullish call than the Bloomberg consensus of 2.5%. The team’s reasoning rests on three pillars: rapid export expansion to emerging-market economies, limited ability among trade partners to erect meaningful new barriers given China’s dominance in critical supply chains, and falling export prices making Chinese goods increasingly price-competitive globally, even as dollar-denominated export price inflation is expected to turn positive in 2026, rising to 0.7% from -2.7% the prior year.

China’s service-sector trade tells the same story from a different angle: services trade expanded 6% year-on-year in the first five months of 2026, with knowledge-intensive service exports jumping 12.2%, reaching a combined 3.1 trillion yuan in total trade value — evidence that China’s export resilience isn’t confined to manufactured goods but extends into higher-value digital and intellectual-property-linked services as well.

The Labour Market Is the Weak Link Nobody’s Pricing

Perhaps the most underreported risk sits in China’s job market. Goldman Sachs’ own wage tracker shows year-over-year growth in urban nominal wages slowing to just 3.8% in the third quarter of 2025 — the weakest hiring environment in a decade outside of the Covid lockdown period, based on a composite of PMI employment sub-indexes. High-tech manufacturing, the sector generating China’s export strength, is simply not labour-intensive enough to absorb the workers displaced from the shrinking property and construction sector. That mismatch is a structural, not cyclical, constraint on any consumption-led rebalancing.

Why the Export Dependency Is a Genuine Vulnerability

The risk in over-relying on exports is not abstract. UBS’s own 2026-27 outlook flags uncertainties related to US trade and technology policy as a direct risk to the baseline forecast, noting that a burst of the global AI investment bubble could hit China’s tech-export momentum just as hard as a fresh round of tariff escalation. China’s own “new economy” sectors — estimated to already contribute roughly a quarter of GDP growth from 2020-24 — are precisely the export-exposed, high-tech segments most vulnerable to a shift in US policy or a correction in global AI capital expenditure.

The Bottom Line

China’s 2026 growth numbers look stable on the surface, but the composition has shifted meaningfully toward a single external lever — exports — at a moment when trade friction, an AI capex cycle that some analysts already worry is overextended, and a structurally weak domestic labour market all point toward the same conclusion: China’s rebalancing toward consumption, a stated priority since at least the 15th Five-Year Plan, remains more aspiration than reality. Investors and trading partners — including Pakistan, whose textile exports compete directly with Chinese manufacturing in some segments — should watch export data more closely than GDP headlines for the real signal on China’s trajectory.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

For years, the phrase “no-limits partnership” defined how Beijing and Moscow described their relationship. It’s still the phrase both governments use publicly. But look closely at what’s actually happening in the energy trade underpinning that partnership, and a very different picture emerges — one where China holds nearly all the leverage, and Russia is discovering that a lifeline can also function as a leash.

The Summit That Produced Declarations, Not Deals

The most recent Xi-Putin summit, which concluded on May 20, 2026, generated the usual round of cooperation announcements across economy, trade, education, science, and technology. But beneath the diplomatic choreography, the meeting failed to deliver the one outcome Russia actually needed: a finalized pricing agreement for the Power of Siberia 2 pipeline (OilPrice.com).

That pipeline matters enormously to Moscow. Russia’s pipeline gas exports to the European Union collapsed from roughly 157 billion cubic meters before the 2022 invasion of Ukraine to just 18 bcm in 2025, dragging Russia’s gas-related tax revenue down 7%. Power of Siberia 2 would add 50 bcm of annual capacity and could roughly double Russia’s share of China’s total gas consumption, from about 10% to 20%. Without that eastward redirection, Russia’s massive Yamal gas reserves — once feeding Europe — risk becoming stranded assets with nowhere to go (Insight EU Monitoring).

Why China Isn’t in a Hurry

Here’s the detail that gets lost in most “Russia-China axis” coverage: China doesn’t actually need this pipeline urgently, and its behavior reflects that. When Gazprom announced a 30-year memorandum on the project in September 2025, Beijing didn’t issue any matching statement. China’s own 15th Five-Year Plan, approved in March 2026, mentions only “advancing preparatory work” — deliberately non-committal language for a project Russia has been publicly promoting for years (Insight EU Monitoring).

The pricing standoff illustrates the imbalance clearly. Putin has insisted gas flowing through the pipeline should use a market-based pricing formula similar to what Russia once charged Europe. Gazprom reportedly made what one source close to the company called a “very competitive offer.” Chinese counterparts still haven’t shown willingness to move forward. Meanwhile, as Russian Foreign Minister Lavrov was in Beijing promoting the pipeline, China’s Vice Premier Ding Xuexiang was simultaneously in Turkmenistan signing deals to expand gas cooperation with China’s second-largest pipeline gas supplier — a live demonstration that Beijing is actively diversifying away from dependence on any single supplier, Russia included (Insight EU Monitoring).

Even the project’s own timeline undercuts any sense of urgency: the head of research at China National Petroleum Corporation has noted that projects of this scale require eight to ten years to build, and Gazprom itself doesn’t expect the pipeline to reach even half capacity before 2034-2035, assuming deliveries start after 2031 (Insight EU Monitoring).

The Trade Numbers Tell an Uncomfortable Story for Moscow

Bilateral trade between China and Russia soared 55% between 2021 and 2025, comfortably surpassing the two countries’ shared $200 billion target set back in 2019. But 2025 marked the first annual decline since the pandemic year of 2020, with trade falling 7% to $227.6 billion (The Moscow Times).

Economically, the asymmetry is stark. China’s economy is nearly eight times larger than Russia’s on a nominal GDP basis, and Russia represents just 4% of China’s total international trade — while China accounts for the overwhelming majority of Russia’s trade relationships (OilPrice.com). That imbalance shows up directly in Russia’s war-fighting capacity: Russia now imports more than 90% of its sanctioned technology from China, up 10 percentage points from 2025. Some of that includes high-end Chinese components that Ukrainian forces have physically extracted from intercepted Russian Kinzhal missile warheads, while Chinese microchips reportedly provide processing power for Iskander ballistic missile and Lancet loitering munition targeting systems (OilPrice.com).

A Temporary Rebound, Not a Reversal

There has been a recent uptick worth noting: Russian oil exports to China surged 22% and oil products rose 9% in early 2026, partly a byproduct of the Iran-linked conflict disrupting Middle East energy flows through the Strait of Hormuz, pushing buyers toward Russian crude that doesn’t depend on that chokepoint (The Moscow Times). Chinese exports to Russia also strengthened, helped by lower Russian interest rates and a stronger ruble reviving consumer demand — car exports nearly doubled, while telecom and computer exports both rose 21%.

But Moscow-based analysts are cautioning against reading too much into this bounce. Economist Andrei Gnidchenko of the CMAKP research center expects trade growth to slow through the second half of 2026 as China builds up energy reserves and economic activity in both countries remains subdued, projecting total 2026 trade will land just 5-10% above 2025 levels — essentially flat versus 2024 (The Moscow Times). And because energy accounts for nearly all of what Russia sells to China, Moscow has little else to offer once oil and gas demand plateaus — Russian oil shipments to China were already slowing to an average 2.2 million barrels per day by April, still above year-ago levels but below Q1 2026’s pace, while pipeline gas exports are already running at maximum existing infrastructure capacity.

The Bigger Picture: China Buys Discounted Oil Precisely Because It Can

China’s discount on Russian crude peaked at roughly 18% in 2022 before easing to around 5%, then rising again in late 2025 following new US sanctions targeting buyers. Between April 2022 and February 2026, China’s average discount stood at 7.7%, saving Beijing an estimated $18.3 billion over that period (Merics China-Russia Dashboard). That’s not a partnership priced between equals — it’s a buyer’s market where China sets the terms because Russia has nowhere else to sell.

What This Means for Global Markets and Investors

For energy traders, the practical takeaway is that Russian crude flows to China will likely keep growing in volume terms but shrink in strategic leverage, since China’s diversification into Central Asian gas (via Turkmenistan) and its patient negotiating posture on Power of Siberia 2 signal it isn’t willing to let Moscow dictate pricing terms. For geopolitical risk analysts, the widening asymmetry suggests China is positioning itself to treat the Russian Far East as a sphere of economic influence rather than a genuine strategic equal — a dynamic that could accelerate if Russia’s war-driven isolation from Western markets continues.

For businesses assessing sanctions exposure, the growing volume of dual-use Chinese components inside Russian weapons systems is likely to keep secondary-sanctions risk elevated for Chinese financial institutions and industrial firms doing cross-border business — a trend that expanded significantly throughout 2025 and shows no sign of reversing.

The Bottom Line

The “no-limits” framing was always more useful as propaganda than as an accurate description of the relationship’s power dynamics. China gets cheap, reliable energy and expanding influence across Russia’s Far East. Russia gets a lifeline that grows thinner and more conditional with every passing quarter. Unless the trajectory of the war in Ukraine or Russia’s broader economic fortunes shifts dramatically, that imbalance is set to deepen — and the Power of Siberia 2 stalemate is the clearest evidence yet of who is actually setting the terms.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

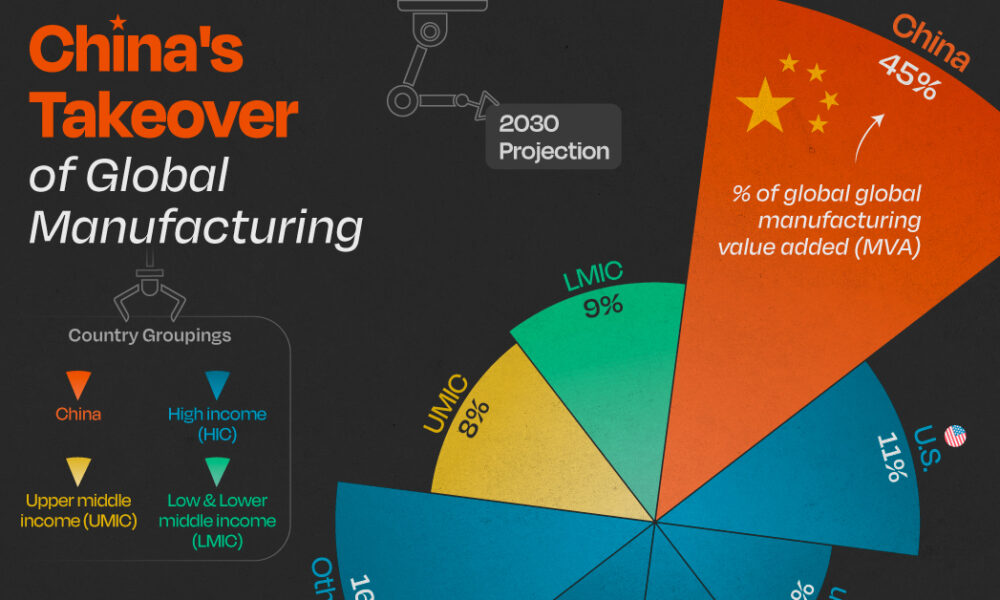

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The US Treasury Department has moved aggressively against a sanctions-evasion network linking Russia and China, exposing a secret payment channel used to facilitate cross-border transactions for sensitive exports and designating a Kyrgyz Republic-based financial institution accused of helping Moscow evade restrictions, according to the US Treasury’s official press release.

Inside the Evasion Network

The scheme relied on so-called “ruble clearing platforms” that facilitate non-cash mutual settlement for payments tied to sanctioned goods. US-designated Russian financial institutions including Sberbank, Alfa-Bank, Sovcombank, T-Bank, and Bank Tochka were reportedly participants. Treasury identified Russia-based and China-based trading companies acting as counterparties in the network, while also designating Keremet Bank, which Treasury says was purchased specifically to create a new sanctions-evasion hub for Russian import payments and export receipts. Treasury simultaneously re-designated nearly 100 entities under Executive Order 13662, reinforcing risk exposure for any foreign party continuing to work with Russia’s military-industrial base.

China’s Banks Start Saying No

The pressure appears to be working, at least partially. Russian banking sources describe a dramatic slowdown in cross-border payment flows, not only with China but also with Central Asian intermediaries such as Kyrgyzstan and Uzbekistan. A Moscow-based banker quoted by CEPA described the situation bluntly, noting that money has largely stopped flowing and only a narrow set of intermediary countries remain viable, according to CEPA’s analysis of the sanctions squeeze. Chinese banks have reportedly begun refusing payments from Russia and rejecting transactions where Russian names appear anywhere in supporting paperwork — a shift CEPA attributes to a US threat late last year to impose secondary sanctions on Chinese banks, cutting them off from dollar access.

The Scale of China’s Role

China has become indispensable to Russia’s wartime economy. Bilateral trade between the two countries hit a record $237 billion in 2023, up nearly 70% since 2021, and China has supplied more than 90% of Russia’s semiconductor imports since the invasion of Ukraine began, more than half of which were Western-branded or produced, according to CSIS’s research on sanctions and Russia’s economic transformation. China’s imports from Russia rose 60% between 2021 and 2024, according to a Congressional Research Service report.

The Crypto Workaround — And Its Limits

As traditional banking channels tighten, Russian banks are being pushed toward cryptocurrency settlement, though CEPA reports Chinese counterparties treat crypto transactions with Russia as fast but increasingly costly, further raising the effective price of Russian imports. The sanctioned Russian exchange Garantex has been under US sanctions since April 2022, and few jurisdictions remain willing to accept Russian crypto transfers, though Russian bankers reportedly expect the UAE to emerge as a more permissive hub for such flows.

The EU’s Parallel Track

The squeeze is not solely an American project. The European Council voted on June 18–19, 2026, to extend EU economic sanctions against Russia for a further twelve months, through July 2027, while calling for swift adoption of a 21st sanctions package targeting Russia’s shadow fleet, energy revenues, and banking system, according to the Council of the EU’s official statement. For global banks and multinational corporates, the compounding effect of US and EU enforcement means compliance risk tied to any residual Russia exposure — even indirect exposure routed through Chinese or Central Asian intermediaries — is rising sharply heading into the second half of 2026.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Yuan Now Settles 67% of Russian Oil Payments — Quiet De-Dollarization in Action

China’s Economy Is Now Dangerously Dependent on One Thing: Exports

Malaysia’s Growth Forecast Just Jumped to 4.9% — The JS-SEZ Master Plan Is Why

$23 Trillion Just Descended on Singapore — What the Capital Reallocation Really Signals

Canada’s Two-Track Economic Play: New Bridge, Tighter Russia Sanctions

UK Business Confidence Hits a 4-Year Low — The Insolvency Wave Nobody’s Pricing In

Stablecoins Now Exceed the FX Reserves of 95 Countries — What That Means for You

PSX’s 18% Rally: Genuine Bull Market or Rate-Cut Mirage?

Pakistan’s Growth Paradox: GDP Up, FDI Down — The Untold FY26 Story

Gold Crashed From $5,600 to $4,300 — Here’s What It Means for Reserves

Malaysia’s flagship finance event, Unlocking Capital for Sustainability (UCFS) 2026

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

AI Capex Bubble 2026: The Hidden $662B Debt Nobody Reports

Gold Overtakes US Treasuries in Reserves: What It Means

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Japan’s Property Sector Looks Strong. So Why Are Investors Going Abroad?

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025