Analysis

AI and Accountancy: Evolution or Elimination? Here’s What the Data Tells Us

Will AI replace accountants? Explore what 2026 data on AI in accounting reveals about job growth, productivity gains, skill shifts, and the future of the profession globally.

Whenever a new wave of technology emerges, the same question follows: Will this replace jobs? With artificial intelligence (AI), that question feels more urgent. AI can scan thousands of transactions in seconds. It can detect patterns humans might miss. Understandably, people are asking whether accountants, especially junior ones, will become obsolete. From the lens of the Institute of Singapore Chartered Accountants (ISCA), that is not where the profession is heading.

But ISCA is not alone in that assessment. A growing body of research — from MIT, Stanford, and the world’s largest professional services firms — suggests that AI in accounting is not a termination notice. It is, in many respects, an upgrade. The more important question isn’t whether AI will eliminate accountants. It’s whether accountants who embrace AI will outcompete those who don’t.

That distinction matters enormously, and the data makes it clearer than ever.

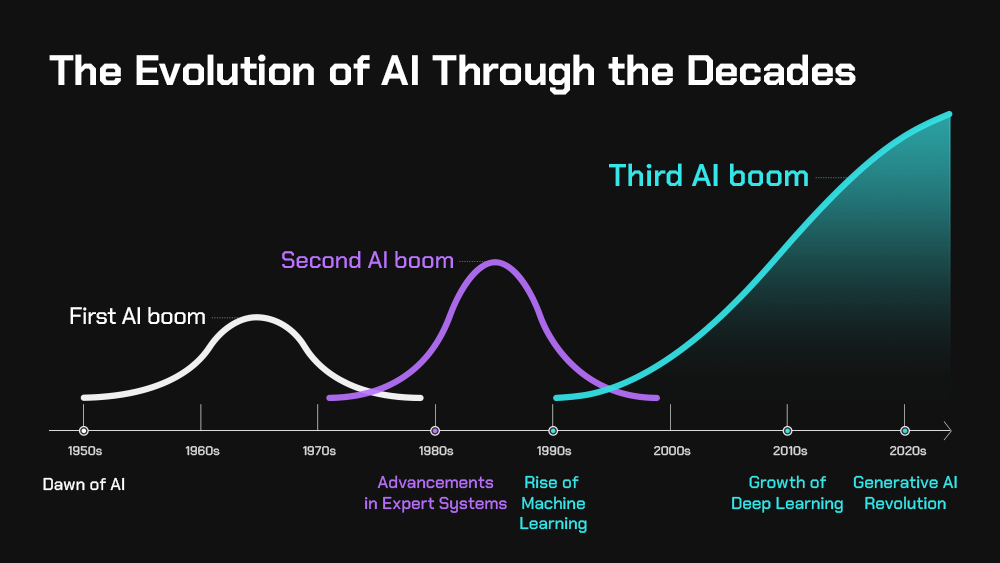

How AI in Accounting Is Already Reshaping Productivity

Before we assess the human cost, we must first understand the scale of AI’s operational impact. The numbers are striking.

The global AI accounting market was valued at approximately $10.87 billion as of recent estimates by DualEntry, with projections placing that figure significantly higher through the end of this decade. AI-powered tools are now embedded in audit workflows, tax compliance engines, accounts payable automation, and real-time financial forecasting. What once required a team of analysts for three days can now be completed in hours — sometimes minutes.

Stanford Graduate School of Business research on AI-assisted professional workflows found productivity gains of roughly 12% in financial reporting accuracy and speed when AI tools were deployed alongside skilled professionals. This is not about replacing human judgment; it is about amplifying it. The model that emerges from this data is collaborative, not competitive.

Deloitte’s most recent AI report reveals that worker access to AI tools has increased by 50% in a single year, marking a tectonic shift in how firms onboard, train, and deploy talent. Tasks that were once the bread and butter of entry-level accountants — reconciliations, data entry, variance analysis — are being automated at scale. But this is not inherently a loss. As Deloitte’s research notes, automation of routine tasks frees higher-order cognitive capacity for advisory work, risk analysis, and strategic counsel — functions where human accountants remain irreplaceable.

AI Impact on Accounting Jobs: Reshaping, Not Replacing

Here is where the nuance becomes critical — and where much of the public discourse gets it wrong.

The United States Bureau of Labor Statistics (BLS), as cited by Careery.pro, projects 5% job growth for accountants and auditors through 2034, which sits comfortably at the average growth rate for all occupations. That is not the trajectory of a dying profession. That is the trajectory of a profession in transformation.

Consider what that transformation looks like at ground level:

- Routine compliance tasks (data entry, invoice matching, basic reconciliations) — increasingly automated

- Tax preparation for standard cases — largely handled by AI platforms with minimal human intervention

- Audit sampling and anomaly detection — AI outperforms human-only review in both speed and pattern recognition

- Advisory services, forensic accounting, M&A due diligence, ESG reporting — growing in complexity and demand

- AI governance and compliance oversight — an entirely new category of roles that did not exist five years ago

Gartner’s research on finance function transformation supports this picture, projecting that by the late 2020s, finance departments will dedicate a larger share of resources to insight generation and strategic planning than to transactional processing. AI handles the transaction layer. Humans own the insight layer.

The AI impact on accounting jobs, in other words, is not mass unemployment. It is mass redeployment — upward, toward more complex and more valued work.

Wages, Inequality, and the Premium on AI Fluency

Not all accountants will benefit equally. The data on wage dynamics carries an important warning.

PwC’s 2025 Global AI Jobs Barometer found that industries with higher AI exposure are experiencing wage growth approximately two times faster than sectors with low AI exposure. For accountants, the implication is stark: professionals who develop AI fluency command a growing wage premium, while those who resist upskilling risk being left behind — not by AI directly, but by AI-proficient peers.

This creates a bifurcation within the profession. On one end: accountants who use AI as a force multiplier, taking on higher-complexity work, billing more hours at higher rates, and expanding their advisory scope. On the other: accountants who remain anchored to task-based roles that AI can increasingly replicate at a fraction of the cost.

The signal for professionals is unambiguous. AI fluency is no longer a differentiator. In the context of AI in accountancy in 2026, it is quickly becoming table stakes.

Thomson Reuters’ Institute research on the future of professional services echoes this clearly: firms that invest in AI tools alongside human capital development are seeing measurably better client outcomes, stronger retention, and faster revenue growth than those that deploy AI without an accompanying talent strategy. Technology alone is not the answer. Technology combined with skilled human judgment is.

A Global Lens: Singapore, Asia, and the ISCA Perspective

The conversation around AI in accounting is not uniform across geographies. Different regulatory environments, economic structures, and labor markets produce different outcomes — and some of the most instructive cases are emerging from Asia.

Singapore offers a particularly compelling study. ISCA, which represents the country’s chartered accounting profession, has been among the more forward-thinking bodies globally when it comes to AI adoption frameworks. In a landmark study on AI readiness, ISCA found that 85% of accounting professionals expressed willingness to adopt AI tools in their workflows — a figure that reflects both the pragmatism of Singapore’s professional culture and the effectiveness of ISCA’s ongoing education and advocacy programs.

This contrasts with more hesitant adoption curves in parts of Europe and North America, where regulatory ambiguity around AI in audit and compliance has slowed institutional uptake. Singapore’s Accounting and Corporate Regulatory Authority (ACRA) has worked in tandem with ISCA to create a structured but enabling environment for AI deployment in financial services — a model that other jurisdictions are beginning to study carefully.

In the broader Asia-Pacific context, the MIT Sloan Management Review has highlighted that Asian markets are experiencing faster AI adoption in finance functions partly because of newer digital infrastructure and a younger workforce with higher baseline digital fluency. China, South Korea, and Singapore are all investing heavily in AI-driven audit and tax technology, creating competitive pressure on Western accounting firms to accelerate their own integration strategies.

For accounting professionals in the region, this is an opportunity. The firms and individuals that move earliest and most strategically will define what AI reshaping accounting roles looks like in practice — building the playbooks that the rest of the world will eventually follow.

The Future of Accounting with AI: New Roles, New Skills, New Demands

What, concretely, does the future of accounting with AI look like? Several emerging roles are already moving from concept to job posting.

AI Compliance Officers sit at the intersection of accounting expertise and AI governance. As regulators in the EU, US, and Southeast Asia begin requiring auditable AI decision trails for financial systems, firms need professionals who understand both the technical logic of AI models and the compliance implications of their outputs. This is fundamentally an accounting role — but one that demands literacy in data science and machine learning fundamentals.

Forensic AI Auditors are being deployed to assess whether AI systems used in financial reporting are producing accurate, unbiased, and regulatorily compliant outputs. Traditional forensic accounting skills — pattern recognition, investigative rigor, understanding of fraud typologies — translate well. But new capabilities in model interpretability and algorithmic bias detection are increasingly required alongside them.

Sustainability and ESG Reporting Strategists are in surging demand as public companies face tightening mandatory disclosure requirements across multiple jurisdictions. AI can process enormous volumes of supply chain, emissions, and social impact data — but the synthesis, stakeholder communication, and assurance of that data requires seasoned professional judgment that no model can yet replicate.

Chief AI Finance Officers (CAFOs) — a title beginning to appear in technology-forward organizations — blend traditional CFO responsibilities with deep fluency in AI strategy, data architecture, and automation governance. These roles command premium compensation and are likely to multiply rapidly through the rest of the decade.

The skills needed to thrive in these roles are not radically foreign to accountants. Critical thinking, professional skepticism, regulatory knowledge, and communication are already foundational. What changes is the technological overlay: data literacy, prompt engineering, understanding of machine learning outputs, and the ability to evaluate AI-generated analyses with the same rigor previously applied to human-generated ones.

The Bottom Line: Evolution Is Not Optional

The data, viewed in aggregate, tells a coherent and ultimately optimistic story — but one with a clear condition attached.

AI in accounting is not an elimination event. It is an evolution imperative.

Will AI replace accountants? The evidence says no — but it will absolutely replace accountants who fail to evolve. The profession will not shrink; it will shift. The accountants who will struggle are not those facing AI directly. They are those who underestimate AI’s scope, delay adaptation, and cede ground to peers who are moving faster.

The 5% BLS job growth projection, the 85% ISCA adoption willingness rate, the 2x wage premium for AI-exposed industries — these are not contradictory data points. They form a consistent picture of a profession that is growing in value precisely because its most capable practitioners are using AI to do more, better, faster.

ISCA frames this correctly: the destination is not obsolescence. It is elevation. The accountant of 2030 will not be competing with AI. They will be wielding it — as a diagnostic tool, a compliance engine, a risk detector, and a strategic advisor’s most powerful instrument.

For professionals in the field, the call to action is not complicated. Upskill now. Engage with AI tools at the practice level, not merely in theory. Seek out certifications in data analytics and AI governance. Participate in professional bodies — like ISCA — that are building the frameworks and networks to help members navigate this transition with confidence.

The wave is already here. The question is not whether it will change the profession. It already has. The question now is who will ride it — and who will be left standing on the shore.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Supreme Court’s landmark ruling on Trump’s “Liberation Day” tariffs has reshuffled the deck in Washington’s trade relationships with Beijing and New Delhi — but neither side is playing its hand just yet.

On the morning of February 20, 2026, President Donald Trump was in a closed-door White House meeting with state governors when a trade adviser slipped him a handwritten note. “So it’s a loss, then?” Trump reportedly said aloud. Within hours, the Supreme Court’s 6-3 ruling in Learning Resources, Inc. v. Trump had detonated across global trading floors from Mumbai to Shanghai — and the reverberations have yet to subside.

The court’s verdict, delivered by Chief Justice John Roberts and joined by an unusual coalition of conservative and liberal justices, was unambiguous: the International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose tariffs. Gone, at a stroke, were the sweeping “Liberation Day” levies — duties that had ranged as high as 145% on Chinese goods and 26% on Indian exports in their peak form. As reported by the Tax Foundation, more than $160 billion in duties had been collected under the now-illegal framework, and the tariffs had been projected to generate $1.4 trillion over the next decade.

Trump moved fast, signing an executive order hours later imposing a temporary 10% global tariff under Section 122 of the Trade Act of 1974 — a rarely invoked provision that limits duties to 150 days without congressional approval. By Saturday, he had ratcheted the announced rate up to 15%. The whiplash, as one Citigroup economist noted, implied “little change in the effective tariff rate or inflation forecasts in the near term.” But the strategic calculus for Asia’s two largest economies shifted dramatically nonetheless.

The Tariff Landscape Before and After: What Actually Changed

To understand the opportunity — and the risk — for China and India, it helps to map the actual numerical terrain.

| Country | Peak IEEPA Tariff Rate | Current Effective Rate (Post-Ruling) | Net Change |

|---|---|---|---|

| China | ~35–50% (combined) | ~20–25% (Section 301 + 10% baseline) | -6.9 pp* |

| India | ~26% | ~15–18% (new baseline + deal terms) | -8 to -11 pp |

| Vietnam | ~46% | ~19% (deal rate preserved) | -27 pp |

| EU | ~20% | ~15% | -5 pp |

*Per Maybank IBG Research analysis

Bloomberg Economics calculated that Trump’s proposed 15% global rate would produce an average effective tariff of around 12% — the lowest since “Liberation Day” tariffs were released in April 2025. China, India, and Brazil emerged, in the words of the analysis, as “the biggest winners from the Supreme Court’s decision.”

Yet winning in absolute tariff terms is not the same as winning strategically. The picture is considerably more complicated.

China: A Tactical Windfall, Not a Strategic Reprieve

For Beijing, the ruling arrives at a diplomatically sensitive moment. Trump is scheduled to visit China from March 31 to April 2, 2026, for what will be the highest-stakes trade summit since his first term. The Supreme Court decision has altered the pre-meeting power dynamics in ways that Chinese negotiators will carefully — and quietly — exploit.

As the Council on Foreign Relations noted, the ruling “narrows unilateral presidential trade powers, constrains improvisational coercion, and shifts the terrain of U.S.-China competition away from executive brinkmanship to institutional process.” Trump enters Beijing with one fewer unilateral lever — and Chinese negotiators know it.

China’s public response has been characteristically calibrated. Beijing’s Commerce Ministry declared it was conducting a “comprehensive assessment” of the ruling’s impact, calling on Washington to “cancel its unilateral tariff measures on its trading partners” and warning that “there are no winners in a trade war.” That language — restrained, multilateralist, positioning China as the aggrieved rule-follower — is deliberate. Beijing is framing the ruling as validation of its long-standing critique that US trade policy violates both international norms and, as it turns out, US domestic law.

The arithmetic backs the posture. Crucially, the 10% flat tariff is meaningfully lower than the pre-ruling rate for Chinese goods. Analysts at one major bank noted that “the effective tariff rate will fall this year and that the world post-SCOTUS will see lower tariffs than the pre-SCOTUS world.” For Chinese exporters who had been dealing with cumulative duties far exceeding 30%, a 10–20% effective rate — before Section 301 levies on specific goods — represents real relief.

But the relief is partial and fragile. As The Associated Press reported, Section 301 of the 1974 Trade Act remains fully intact, and US Trade Representative Jamieson Greer announced Friday that the administration was “launching a series of 301 investigations” following its Supreme Court loss. Those “sticky tariffs,” as one trade lawyer put it, have been in place for eight years across two administrations, targeting Chinese technology, electric vehicles, and advanced manufacturing. The ruling did not touch them.

China’s countermeasures strategy is also evolving. With the reciprocal and fentanyl-related IEEPA tariffs on China suspended — they had reached a combined 24% — Beijing indicated a willingness to adjust its own retaliatory posture, signaling readiness for “candid consultations” before Trump’s arrival. That is diplomatic language for: we are willing to negotiate, but we hold more cards than we did last week.

India: Strategic Pause, or Strategic Hesitation?

India’s response has been more visibly disruptive. New Delhi became the first country to take a concrete step in response to the ruling, postponing its trade delegation’s planned trip to Washington to “finalise the legal text” of an interim trade deal that Trump had announced earlier in February. No new date has been set.

The deferral is understandable. India had negotiated a framework that pegged its tariff rate at 18% — a meaningful reduction from the previous 26% under IEEPA, and a result secured after considerable diplomatic effort by Prime Minister Narendra Modi’s government. Then, in a matter of days, the baseline for every country dropped to 10–15%, effectively eroding the competitive advantage India had worked to secure.

The situation is further complicated by the Trump administration’s decision, just four days after the Supreme Court ruling, to impose a 125.87% preliminary countervailing duty on solar cell imports from India under a separate trade investigation. As India Briefing reported, the targeted measure underscores how the ruling addresses emergency tariff authority, but leaves sectoral tools fully operative. For New Delhi, the tariff environment remains as volatile as ever.

Moody’s noted that “the Supreme Court’s intervention restricts Washington’s ability to deploy country-specific tariffs as a negotiation tool,” a constraint that “could reduce US leverage in bilateral trade talks.” That cuts both ways for India. Washington has less coercive power; but India also has less urgency to sign deals quickly.

India is also, quietly, revisiting its stance on Chinese investment. Reports indicate New Delhi is reviewing “Press Note 3,” the 2020 policy that placed strict scrutiny on foreign direct investment from countries sharing land borders — principally China. A tiered approval framework may emerge, reflecting India’s pragmatic recognition that it needs capital and technology inflows even as it manages strategic competition with Beijing.

The Geopolitical Chessboard: What Numbers Cannot Capture

Headline tariff rates are, as experienced trade negotiators know, only one variable in a far more complex equation. Energy security, technology supply chains, domestic political constituencies, and investment commitments all shape negotiations in ways that percentage points cannot fully represent.

For China, the structural competition with the US in semiconductors, artificial intelligence, and green technology remains fundamentally unchanged. The CFR’s Zongyuan Zoe Liu observed that “the structural factors driving U.S.-China strategic rivalry — technological competition, industrial policy clashes, and security tensions — remain unchanged.” What the ruling provides China is a modest tactical advantage: the moral authority of having been vindicated by America’s own highest court, and a negotiating room in which Trump arrives slightly disarmed.

For India, the geopolitical calculus is particularly delicate. New Delhi has spent years cultivating a “strategic autonomy” posture — deepening ties with Washington through initiatives like the Quad while maintaining its historical equidistance from great-power blocs. The tariff reshuffle tests that balance. A rushed deal with the US that locks India into trade commitments could constrain its flexibility with other partners. A prolonged delay, meanwhile, risks inviting retaliatory Section 301 investigations.

Fortune reported that Trump has warned countries they could face something “far worse” if they attempt to renegotiate existing deals — a reminder that the Section 122 tariff authority, though temporary (it expires in approximately 150 days, around mid-July), could be supplemented by Sections 232 and 301, which carry no such time limit.

The uncertainty, as Moody’s chief economist Mark Zandi told CNBC, has already begun to affect business behavior. “Businesses don’t know what’s going to happen next. They’re going to invest less, they’re going to hire less, they’re going to be less aggressive in their expansions.” That chilling effect applies equally to supply chain decisions across Asia.

The Road Ahead: Three Scenarios

Scenario 1 — Managed De-escalation. Trump’s China visit in late March produces a framework agreement. China adjusts its countermeasures, the US agrees to hold Section 301 rates steady (rather than expanding them), and a 90-day diplomatic truce takes hold. India finalizes its interim deal at a rate near or below 15%. Both countries gain breathing room. Probability: Moderate, contingent on domestic political conditions in Washington.

Scenario 2 — Procedural Escalation. The US uses Section 301 investigations to reconstruct country-specific pressure on China, and Section 232 national security reviews to target Indian steel, pharmaceuticals, and solar exports. The “new 10%” baseline becomes a floor, not a ceiling. India’s interim deal collapses. China digs in ahead of a midterm-election-minded Trump. Probability: Elevated, given the USTR’s stated intention to launch new investigations.

Scenario 3 — Legislative Reset. Congress, under pressure from businesses seeking tariff refunds and legal certainty, passes framework legislation granting the president conditional tariff authority with statutory guardrails. Both China and India face a more institutionally anchored — and therefore more predictable, if not necessarily lower — tariff regime. Timeline: 12–18 months at minimum.

Conclusion: The Numbers Are Not the Story

The Supreme Court’s February 20 ruling is less the end of America’s tariff wars than the end of their most arbitrary phase. As AP reported, the ruling means Trump “can’t conjure up new import taxes on a whim anymore” — but it does not mean tariff confrontation is over.

For Beijing, the ruling is a tactical gift deployed at a strategically opportune moment. For New Delhi, it is an unwelcome complication to a negotiation already dense with sectoral trade-offs and domestic sensitivities. Neither capital is rushing to the table. Both are recalculating.

What is clear is that the era of IEEPA-powered shock tariffs — unilateral, unlimited, and legally contested — has ended. What replaces it will be slower, more institutionally embedded, and therefore harder for trading partners to navigate through simple concession. That is a subtler kind of pressure, but it is pressure nonetheless.

Researchers and policymakers tracking the US-China-India trade triangle should watch three indicators closely over the coming weeks: the outcome of the Trump-Xi summit, whether India’s rescheduled trade delegation reaches Washington before Section 122 authority expires in mid-July, and the pace of new Section 301 investigation filings. The numbers on a tariff schedule are, in the end, just the opening bid. The real negotiation has barely begun.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Børge Brende WEF Resignation Epstein: How One Scandal Broke an Institution Already on Its Knees

The departure of the World Economic Forum’s CEO over Jeffrey Epstein ties is more than a personal scandal — it is an institutional reckoning with elite impunity at Davos.

There is a particular kind of silence that descends on institutions when their carefully constructed image of moral authority finally collapses. On February 26, 2026, that silence fell over the headquarters of the World Economic Forum in Cologny, Switzerland — a sleek stone-and-glass building overlooking Lake Geneva that has come to symbolize the lofty ambitions, and equally lofty contradictions, of the global elite. Børge Brende, president and CEO of the WEF, announced he was stepping down after the organization launched an independent investigation into his relationship with the late sex offender Jeffrey Epstein. CNN He had been in the role for eight and a half years. He leaves it diminished, and so, many argue, does the institution he led.

The timing is brutal. Just five weeks earlier, Brende had stood on the Davos stage interviewing US President Donald Trump following his address to global leaders. CNN The Forum had declared its 2026 annual meeting a triumph. And then the files arrived.

The Resignation: What the Epstein Files Revealed

Documents in the Epstein files showed Brende arranging to meet the financier at his home in New York for dinner in 2018 and 2019. The second of those meetings was planned just weeks before Epstein’s arrest on federal sex trafficking charges. Bloomberg He died in jail in August 2019, his network of wealthy and influential contacts frozen in amber by circumstance — until the US Department of Justice began releasing millions of pages of documents in late 2025 under the Epstein Files Transparency Act.

The WEF launched an independent review earlier this month when it emerged that Brende had attended three business dinners with Epstein in 2018 and 2019, as well as communicated with him via emails and text messages. At least one of the dinners took place at Epstein’s New York home, according to the emails. CNN What made the correspondence particularly damaging was its warmth. The Financial Times reported that Brende wrote to Epstein: “thx for a very interesting dinner … You’re a brilliant host,” and in another message said, “Missing you Sir.” Breitbart

In an earlier statement after the WEF launched its probe, Brende said he had been “completely unaware of Epstein’s past and criminal activities” and would not have communicated or attended dinners with him had he known. “I recognize that I could have conducted a more thorough investigation into Epstein’s history, and I regret not doing so,” he said. CNN That admission — careful, measured, calibrated to minimize — could not withstand the accumulating weight of scrutiny.

The contradiction at the heart of Brende’s defence deserves examination. By 2018, Epstein’s 2008 conviction for procuring a minor for prostitution was a matter of public record. The former Norwegian foreign minister — a man whose entire professional life was built on due diligence, diplomatic intelligence, and geopolitical risk assessment — claims he did not investigate Epstein’s background. He had, in fact, denied ever having met Epstein as recently as November 2025, before the document release forced him to acknowledge the contacts. Wikipedia This reversal, combined with the tonal intimacy of the emails, generated precisely the kind of “distraction” that would ultimately cost him his position.

In a joint statement, WEF co-chairs André Hoffmann and Larry Fink said the independent review had concluded, with findings that “there were no additional concerns beyond what had been previously disclosed.” Al Jazeera Brende’s resignation statement, notably, made no mention of Epstein, with Brende saying only that “now is the right moment for the Forum to continue its important work without distractions.” Axios Alois Zwinggi will take over as interim president and chief executive with immediate effect, with the WEF Board of Trustees supervising the leadership transition and beginning the process of identifying a permanent successor. wionews

WEF CEO Quits Jeffrey Epstein Ties: A Growing Casualty List

Brende’s departure is the latest in what has become a rolling institutional crisis in the corridors of global power. The list of executives whose careers have been derailed by the Epstein files includes Hyatt Hotels executive chairman Tom Pritzker, top Goldman Sachs lawyer Kathy Ruemmler, and Sultan Ahmed bin Sulayem, CEO of DP World. CNN Brad Karp, chair of top corporate law firm Paul, Weiss, resigned after his emails with Epstein were revealed. Casey Wasserman, the Hollywood talent agent who chairs the LA28 Olympic committee, said he would sell his agency after his Epstein ties were disclosed. Axios

What distinguishes this wave from earlier Epstein fallout — such as the 2021 departures of Apollo Global Management CEO Leon Black and Barclays CEO Jes Staley — is its velocity and geographical breadth. The DOJ’s release of over three million documents has created a kind of accountability avalanche that no elite management communications team was prepared for. The files do not merely name individuals; they document the texture of relationships, the tone of correspondence, the specificity of social arrangements. In that texture, reputations dissolve.

Norway’s Epstein Shadow: Jagland, Brende and a Pattern of Proximity

For Norway, a country that has long positioned itself as a global moral beacon — home to the Nobel Peace Prize, a leader in development aid, a proponent of multilateral governance — the Epstein files have been a particular kind of reckoning.

Thorbjørn Jagland, former Norwegian prime minister and former secretary-general of the Council of Europe, has been charged with “aggravated corruption” following a police probe into his Epstein ties. Terje Rød-Larsen and his wife Mona Juul, both diplomats, have also been charged. Al Jazeera These are not peripheral figures in Norwegian public life. They are among the country’s most senior statesmen, individuals who spent careers representing humanitarian values on the international stage.

The pattern invites uncomfortable analysis. Norway’s small, tightly networked political elite — educated at the same institutions, rotating through the same multilateral organizations, attending the same Davos dinners — may have been structurally predisposed to encounter Epstein’s curated world of access and influence brokerage. Epstein did not merely collect the powerful; he collected people who collected the powerful. Norwegian diplomats and multilateral organization heads were precisely the kind of connective tissue he sought. That Brende and Jagland should both appear in the files, in different capacities, is less a coincidence than a reflection of how Epstein understood and exploited the architecture of global influence.

The WEF’s Institutional Reckoning: From Schwab to Brende

Klaus Schwab’s abrupt departure from the World Economic Forum, the influential organization he founded and led for more than half a century, had already complicated carefully laid plans to persuade Christine Lagarde to assume the helm in a seamless transition. Bloomberg Schwab resigned from the post of chairman at the end of April 2025 in the wake of an external investigation into allegations of possible misconduct, which he denies. Swissinfo In the aftermath, Larry Fink and André Hoffmann were appointed interim co-chairs of the Board of Trustees. Wikipedia

The Brende crisis arrives, therefore, not as an isolated shock but as the second major leadership implosion inside twelve months at an organization that has, for over five decades, styled itself as a forum for responsible global leadership. Davos has always attracted criticism — for its carbon-intensive private jets, its exclusive membership fees, its air of patrician consensus-building insulated from democratic accountability. But until recently, that criticism was largely tolerated as the price of convening power. Two consecutive leadership scandals have changed the calculus. The WEF was also reportedly under Swiss investigation in February 2026 over whether it had broken the law by paying Brende around 19 million NOK in salary — 3 million more than the previous year — with questions arising over whether such remuneration to managers of a tax-exempt non-profit foundation could constitute illicit enrichment. Wikipedia

These are no longer questions about optics. They are questions about governance.

Epstein Scandal Davos 2026: Economic and Reputational Fallout

For international economists and governance researchers, the question is not simply whether Børge Brende had inappropriate ties to a convicted sex offender. The deeper question is structural: what does it mean for an organization whose core value proposition is convening power when that power becomes associated, even tangentially, with the Epstein network?

The WEF’s revenue model depends on roughly 1,000 member companies — typically multinationals with annual turnovers exceeding $5 billion — paying substantial membership fees for access to the annual Davos gathering and year-round platform benefits. Participation is not merely transactional; it is reputational. CEOs attend Davos partly because other CEOs attend Davos. That reflexive logic of prestige is durable, but not infinitely so. Two consecutive scandals involving the organization’s most senior figures, combined with the broader Epstein fallout now touching multiple Davos-adjacent networks, introduce a reputational friction that some corporate governance officers and compliance teams will find professionally untenable to ignore.

There are also structural questions about the WEF’s convening model in the current geopolitical climate. The January 2026 Davos meeting was notable partly because Donald Trump’s presence and tariff-focused address served, in the words of one analyst, as a direct challenge to the globalist consensus the WEF has long championed. The departure of Schwab, who created that consensus over 55 years, followed by the departure of his designated operational heir under Epstein-related pressure, leaves the Forum without a defining intellectual anchor at precisely the moment when the political philosophy it represents is under its most sustained global challenge since the 1990s.

Alois Zwinggi Interim WEF CEO: What Comes Next?

Alois Zwinggi, a managing director of the WEF, has been appointed interim president and chief executive while the board manages the leadership transition. Christine Lagarde, ECB President, has widely been seen as a potential future chair following the departure of WEF founder Klaus Schwab. euronews However, within the Swiss organization, Lagarde has begun to be viewed as “Klaus’s candidate,” a label that has started working against her, with some around the organization becoming wary of any perception of an overly close connection to the previous leadership. BankingNews

The search for permanent leadership, therefore, remains genuinely open — and genuinely fraught. The new WEF president will need to achieve several incompatible things simultaneously: demonstrate a clean break from the Schwab and Brende eras while preserving the institutional relationships those eras cultivated; rebuild confidence among corporate members growing wary of reputational entanglement; and provide an intellectual vision capable of justifying Davos’s continued relevance in an era of economic nationalism, democratic populism, and deep public suspicion of multilateral elite institutions.

That is not an impossible brief. But it is a daunting one. And the organization’s recent track record in identifying, vetting, and retaining leadership has not been encouraging.

A Forum at the Crossroads

The story of Børge Brende’s resignation over Epstein ties is ultimately a story about institutional trust in the age of radical transparency. The Epstein files did not create the relationships they exposed; they merely illuminated them. In a previous era, three business dinners with a disgraced financier, however ill-judged, might have remained a private embarrassment managed through careful distance and quiet acknowledgment. In 2026, with three million documents digitally searchable and a global media ecosystem attuned to the cadence of elite accountability, there is no such discretion available.

The World Economic Forum will survive this. Institutions with the WEF’s structural advantages — established relationships, financial reserves, a half-century of convening infrastructure — do not simply dissolve because their leaders err. But the organization that emerges from this period of twin crises will need to do more than change its faces. It will need to change its self-conception: from a summit of the world’s most powerful people managing global challenges on behalf of everyone else, to something more modest, more accountable, and more genuinely connected to the populations whose futures it claims to shape.

That transformation, if it comes at all, will be far harder than replacing a president and CEO.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Yen to Decide if Japan’s ‘Iron Lady’ is Steely or Rusty: Takaichi’s Path to Economic Revival and Global Influence in 2026

Sanae Takaichi economic policy 2026 is now the most consequential story in Asian geopolitics. Japan’s first female prime minister has a landslide mandate, a supermajority in parliament, and a to-do list that would humble most heads of state. But the real verdict on her premiership will not be delivered by pollsters or pundits — it will be rendered, quietly and ruthlessly, by the foreign-exchange market. At roughly ¥156 to the dollar as of late February 2026, the yen is part barometer, part referendum. If Takaichi can coax it stronger, she will have earned her iron. If it wilts further, the rust will show.

A Landslide Built on Frustration — and Expectation

On February 8, 2026, Sanae Takaichi did what no woman had done in Japan’s 76 years of post-war parliamentary democracy: she won a commanding general election and walked into the Kantei as prime minister. The Liberal Democratic Party’s victory was not merely symbolic. With a two-thirds supermajority in the Lower House, the LDP now controls the legislative machinery of the world’s fourth-largest economy with a completeness that Takaichi’s predecessors — a procession of short-lived leaders who averaged barely fourteen months in office across the last decade — could only dream of.

The election result represented a decisive break from Japan’s revolving-door politics. Since Shinzo Abe’s resignation in 2020, Japan has cycled through five prime ministers in five years, each one eroding investor confidence and diplomatic continuity. Takaichi’s victory, analysts at the Brookings Institution noted, was powered by voter exhaustion with instability as much as by enthusiasm for her agenda — a distinction that matters enormously for how durable her mandate will prove.

Her agenda is ambitious by any measure. She has pledged to tame inflation, boost household incomes that have stagnated in real terms for the better part of three decades, and — most fraught of all — strengthen a yen that has become a source of national anxiety.

Takaichi’s Economic Mandate: Taming Inflation and the Yen

Japan’s consumer price index, stripped of fresh food, is running at approximately 2.5% — a number that sounds modest by the standards of recent Western experience but represents a generational shock in a country that lived with deflation for much of the 1990s and 2000s. For ordinary Japanese households, the bite is real: energy costs, imported food prices, and service-sector wages have all risen in ways that nominal pay increases have not fully offset.

Takaichi has framed her economic agenda around three interlocking priorities. First, price stability — not by returning to deflation, but by anchoring inflation in a zone that feels like prosperity rather than punishment. Second, income growth, with a particular emphasis on small and medium-sized enterprises, which employ roughly 70% of Japan’s private-sector workforce. Third, and most geopolitically charged: a stronger yen.

The yen’s current weakness — hovering near ¥156 per dollar as of late February 2026 — is the compound product of years of ultra-loose monetary policy, dovish appointments to the Bank of Japan’s policy board, and persistent hesitation about rate hikes in an economy still scarred by deflationary memory. The irony is acute: Takaichi herself has historically been associated with the “Abenomics” school of aggressive monetary easing. Her pivot toward yen strength represents either a genuine ideological evolution or a calculated response to political headwinds — and the markets are watching closely to determine which.

| Indicator | Current Value (Feb 2026) | Target / Direction |

|---|---|---|

| USD/JPY Exchange Rate | ~¥156 | Strengthen toward ¥140–145 |

| Core CPI (ex. fresh food) | ~2.5% YoY | Stabilize near 2.0% |

| BOJ Policy Rate | 0.5% | Cautious, gradual tightening |

| LDP Lower House Seats | ~310 (two-thirds+) | Supermajority retained |

| Avg. PM Tenure (2020–2025) | ~14 months | Extend to Abe-length horizon |

Bloomberg’s USD/JPY analysis has flagged that yen depreciation in the range of ¥150–160 creates a self-reinforcing problem: it inflates import costs, which feeds the very CPI pressure Takaichi wants to suppress, which in turn demands BOJ action that her own dovish board appointments have complicated. Breaking this loop will require either a coherent signals strategy with the BOJ or a willingness to replace key officials — a politically costly move she has so far resisted.

Reuters currency strategists have modeled scenarios in which a credible fiscal consolidation signal from Tokyo, combined with even a modest BOJ rate path, could bring USD/JPY back toward ¥145 by year-end. That would represent a 7% yen appreciation — meaningful for households but not catastrophic for Japan’s export machine, which has partly adapted to weaker-yen conditions over the past three years.

Japan Yen Strength Under Takaichi: The Policy Toolkit

The challenge of yen management is that it sits at the intersection of monetary, fiscal, and diplomatic policy in ways that resist simple levers. Takaichi’s government has several tools available — and each carries trade-offs.

On the monetary side, the new prime minister must navigate her own history. The Economist’s profile of her conservative agenda notes that she spent much of the last decade advocating for the continuation of Abenomics-style quantitative easing. Reversing course now — or even appearing to — risks accusations of opportunism. Yet the arithmetic of yen weakness is unforgiving. A sustained rate differential between the US Federal Reserve (still holding rates in a 4.25–4.50% corridor) and the BOJ makes carry-trade pressure on the yen almost structural.

On the fiscal side, Takaichi has proposed a stimulus package that blends short-term income support with longer-term investment in semiconductors, green energy, and artificial intelligence — sectors where Japan’s industrial base has competitive depth but chronic underinvestment. Forbes’s analysis of her economic stimulus blueprint suggests the package could inject ¥30–40 trillion over three years, a scale that would rival Abe’s initial Abenomics bazooka. Done right, this could attract foreign capital and support the yen. Done sloppily — with bond issuance outpacing growth returns — it could accelerate the currency’s decline.

The wildcard is the BOJ itself. Takaichi’s recent appointments to the policy board were read by markets as dovish signals, contributing to the yen’s softening in late January 2026. Walking that back without triggering a bond-market sell-off is the central technical challenge of her economic team.

Takaichi vs. Abe Legacy: Foreign Policy Boost from Electoral Strength

In foreign affairs, electoral supermajorities translate into diplomatic credibility in ways that are easy to underestimate. When Shinzo Abe governed from 2012 to 2020 — the longest tenure of any postwar Japanese prime minister — his stability became a strategic asset. Foreign leaders knew he would still be in office in two years. Treaties got signed. Defense upgrades got funded. The Quad — the informal security grouping of the US, Japan, India, and Australia — found its practical architecture during his tenure.

Takaichi has been explicit about emulating that model. She has framed her electoral mandate as a foundation for long-horizon diplomacy: deepening the US alliance, anchoring relationships across Southeast Asia through expanded Official Development Assistance, and advancing Japan’s strategic partnership with India — a relationship with particular resonance given both countries’ desire to hedge against Chinese economic and military assertiveness.

The contrast with the revolving-door years is stark. Between 2020 and 2025, Japan’s foreign counterparts had to recalibrate relationships with five different prime ministers. Diplomatic continuity is not merely an aesthetic preference; it affects the willingness of partners to make binding commitments, share intelligence, and coordinate on multilateral frameworks from trade to climate.

BBC’s coverage of the February 8 election emphasized that her win was received warmly in Washington and Delhi, with early indications of accelerated bilateral defence and technology talks. Whether that goodwill translates into durable institutional architecture — the test of Abe’s legacy — remains to be seen.

Challenges Ahead: Discipline in a Supermajority

Supermajorities are not pure gifts. They carry their own pathologies. A governing coalition with two-thirds of the lower house faces the perennial temptation to overreach — to pursue constitutional revision, defence spending expansion, and structural reform simultaneously, spreading political capital thin and provoking the backlash that has historically dogged the LDP’s more ambitious moments.

Japan economy outlook 2026 among independent economists is cautiously optimistic but conditioned on three risks. First, demographic drag: Japan’s working-age population continues to shrink, limiting the growth ceiling regardless of policy quality. Second, energy vulnerability: with roughly 90% of energy still imported, yen weakness translates directly into household energy costs — a politically explosive channel for any PM who has promised to boost living standards. Third, China exposure: Japan’s supply chains remain deeply integrated with Chinese manufacturing, even as its security posture pivots away from Beijing.

Takaichi’s government will also face the scrutiny that comes with strength. In opposition-thin parliaments, accountability tends to migrate from the floor of the Diet to the media, civil society, and — crucially — financial markets. The Wall Street Journal’s recent analysis of Japan’s fiscal position warned that the new administration’s stimulus ambitions could widen the deficit at precisely the moment when global bond markets are reassessing sovereign credit risk across developed economies.

Yen Impact on Japan Inflation 2026: The Feedback Loop

The relationship between yen impact on Japan inflation 2026 is not merely academic — it is the lived experience of every Japanese consumer who has watched grocery bills climb faster than wages. A yen at ¥156 to the dollar means that every imported barrel of oil, every tonne of wheat, every semiconductor fab component costs roughly 30% more in local-currency terms than it did five years ago.

For Takaichi, this creates a political clock. Her approval ratings — strong now, buoyed by the election — will erode if households feel no relief by mid-2026. The government has proposed targeted subsidies on energy and food staples as a bridge measure, but economists across the spectrum have noted that subsidies without currency stabilisation are a fiscal leak: money flows out through the subsidy channel even as import costs continue rising through the exchange-rate channel.

The BOJ’s next quarterly review, expected in April 2026, will be watched as an early test of whether Takaichi’s government can credibly signal a tighter monetary path without spooking bond markets or triggering a sharp yen overshoot in the other direction. Getting this sequencing right is less art than watchmaking — precision timing, in conditions of significant uncertainty.

Japan’s First Female Prime Minister Foreign Affairs: The Historical Weight

It would be reductive to view Takaichi’s historic significance purely through the lens of the economic numbers. Japan’s first female prime minister carries symbolic weight in a nation where the World Economic Forum’s gender gap index ranks political representation among the lowest in the G7. Her tenure — however it ends — will alter the reference class for what Japanese political leadership can look like.

That said, Takaichi herself has consistently resisted being defined by gender. Her policy instincts are hawkish on defence, conservative on social questions, and market-oriented on economics — a combination that places her in Abe’s ideological tradition rather than a progressive feminist one. The historical irony is not lost on observers: Japan’s glass ceiling in politics was broken not by a centrist reformer but by a hardline nationalist with a record of visiting the Yasukuni Shrine.

This complexity will matter in foreign policy. Relations with South Korea and China — perennially complicated by historical memory — will require careful navigation from a prime minister whose nationalist credentials are well-documented. CSIS analysts have suggested that her strong electoral position could, counterintuitively, give her the political capital to make pragmatic overtures to Seoul and Beijing that weaker predecessors could not risk.

Japan Economy Outlook 2026: Steely or Rusty?

The metaphor embedded in Takaichi’s “Iron Lady” epithet — a comparison she has neither sought nor explicitly repudiated — implies a binary: strength or corrosion. Reality, of course, is more granular.

The case for steeliness is real. She has a supermajority. She has a stable mandate in a system notorious for instability. She has a credible international profile and an ideological tradition with a proven track record of market confidence. And she has, at least rhetorically, identified the right problems: inflation that erodes household welfare, a currency that amplifies every external shock, and an income structure that has left ordinary Japanese workers behind for too long.

The case for rust is equally real. The yen’s weakness is partly her own government’s doing — a product of BOJ appointments that sent dovish signals. Her stimulus agenda carries fiscal risks in a country already carrying a debt-to-GDP ratio above 260%. Her historical association with Abenomics makes credible monetary tightening a harder sell, politically and intellectually.

The yen, ultimately, will arbitrate between these two interpretations. A currency that strengthens by year-end will vindicate her economic framework and give her the diplomatic runway to emulate Abe’s longevity. A currency that drifts toward ¥165 or beyond will tell a different story — one of a leader whose political strength outran her policy coherence.

As Japan navigates 2026, watch the yen as the ultimate barometer. It will move before the polls do, signal before the speeches do, and judge with the cold precision that only markets can muster. Takaichi has the mandate. The question is whether she has the sequencing — and whether Japan’s long-suffering households will give her the time to find out. Bookmark the USD/JPY ticker; it will tell you more about her premiership than any press conference.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance2 months ago

Markets & Finance2 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis3 weeks ago

Analysis3 weeks agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Investment2 months ago

Investment2 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Banks1 month ago

Banks1 month agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Asia2 months ago

Asia2 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Global Economy2 months ago

Global Economy2 months agoWhat the U.S. Attack on Venezuela Could Mean for Oil and Canadian Crude Exports: The Economic Impact

-

Global Economy2 months ago

Global Economy2 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy2 months ago

Global Economy2 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis