Tariffs

Trump’s Greenland Gambit: How Tariffs on Eight European Allies Could Reshape the Transatlantic Alliance

On the frigid evening of January 17, 2026, President Donald Trump lobbed what may prove to be the most audacious—and potentially destructive—ultimatum of his second term across the Atlantic. Via his preferred digital megaphone, Truth Social, Trump announced sweeping tariffs targeting eight of America’s closest European allies: Denmark, Norway, Sweden, France, Germany, the United Kingdom, the Netherlands, and Finland. The levy, set at 10% on all imported goods beginning February 1 and escalating to 25% from June 1, comes with a singular, extraordinary condition: the “Complete and Total purchase of Greenland” by the United States.

The declaration sent tremors through diplomatic channels, financial markets, and NATO headquarters alike. Within hours, European capitals responded with a mixture of bewilderment, outrage, and steely resolve. Danish Prime Minister Mette Frederiksen, who had previously dismissed Trump’s Greenland overtures as “absurd,” condemned the tariff threat as “economic blackmail” that violates fundamental principles of international law and alliance solidarity. German Chancellor’s office termed the move “incomprehensible,” while French officials warned of swift EU-wide countermeasures.

This is not merely another chapter in Trump’s unpredictable trade policy playbook. It represents a fundamental reassessment of America’s relationship with its oldest democratic partners—one that prioritizes Arctic ambitions and resource nationalism over seven decades of transatlantic cooperation. The question facing European leaders and global observers is stark: Is this a negotiating tactic from a president known for brinkmanship, or does it signal a permanent fracturing of the Western alliance at precisely the moment when unity matters most?

The Island That Haunts Trump’s Strategic Imagination

Trump’s fixation on Greenland is neither new nor entirely irrational, even if his methods appear extraordinary. The world’s largest island has occupied a peculiar space in American strategic thinking since 1946, when President Harry Truman offered Denmark $100 million for outright purchase—a proposal politely declined. During the Cold War, the United States established Thule Air Base in northwest Greenland, which remains a critical early-warning station for ballistic missile detection and satellite surveillance, now upgraded to monitor threats from Russia and China.

Trump first publicly floated the purchase idea in August 2019, initially reported as a jest before the then-president confirmed serious interest. The proposal met swift rejection from both Denmark and Greenland’s autonomous government, prompting Trump to cancel a scheduled state visit to Copenhagen in a diplomatic snub that reverberated for months. At the time, analysts dismissed the episode as characteristic Trump bluster—a distraction from domestic troubles or perhaps genuine curiosity about an unconventional deal.

Yet the intervening years have transformed Greenland from a geopolitical curiosity into a strategic imperative in Washington’s eyes. The Arctic is warming twice as fast as the global average, opening previously ice-locked sea routes and revealing vast mineral wealth beneath Greenland’s melting ice sheets. Geological surveys suggest the island harbors significant deposits of rare earth elements—including neodymium, praseodymium, and dysprosium—critical for electric vehicles, wind turbines, advanced weaponry, and semiconductors. China currently controls roughly 70% of global rare earth production and 90% of processing capacity, creating what Pentagon strategists view as an unacceptable vulnerability in supply chains for both commercial technology and defense systems.

Russia’s 2022 invasion of Ukraine and subsequent militarization of its Arctic territories has further elevated Greenland’s importance. Moscow has reopened Soviet-era bases along its northern coastline, deployed advanced anti-access/area denial systems, and conducted frequent bomber patrols near North American airspace. China, despite being a “near-Arctic” nation by its own creative geography, has declared itself a “Polar Silk Road” power, investing in Icelandic infrastructure and conducting research expeditions that European intelligence agencies suspect serve dual civilian-military purposes.

For Trump and his advisers, Greenland represents the ultimate “art of the deal”—a territorial acquisition that would simultaneously secure critical minerals, establish American dominance in the Arctic, and cement a legacy comparable to the Louisiana Purchase or Alaska acquisition. The fact that such a deal contradicts modern international norms regarding self-determination and sovereignty appears, in this calculation, a manageable obstacle rather than a disqualifying one.

The Tariff Ultimatum: Mechanics and Targeted Impact

The tariffs Trump announced represent a significant escalation in both scope and justification. Unlike his first-term steel and aluminum levies, ostensibly grounded in Section 232 national security provisions, or his China tariffs under Section 301, these measures reportedly invoke the International Emergency Economic Powers Act (IEEPA)—an assertion of presidential authority typically reserved for sanctions against hostile nations like Iran or North Korea, as legal experts have noted with alarm.

The eight targeted nations collectively represent America’s third-largest trade relationship, with bilateral goods trade totaling approximately $680 billion annually. The economic pain would be unevenly distributed but universally felt:

Denmark, though a modest trading partner with roughly $15 billion in annual bilateral trade, faces disproportionate leverage given its sovereignty over Greenland. Danish pharmaceutical giants like Novo Nordisk—which supplies approximately 50% of the world’s insulin and has invested billions in US manufacturing—could see profit margins compressed and supply chains disrupted. The country’s wind energy sector, led by Vestas and Ørsted, exports significant turbine components to American renewable projects that could face cost increases precisely when the US seeks to expand green energy capacity.

Germany, America’s largest European trading partner with $267 billion in bilateral trade, confronts the most severe economic exposure. The automotive sector—BMW, Mercedes-Benz, and Volkswagen together exported over $24 billion worth of vehicles to the US in 2025—would face punishing costs that could render German cars uncompetitive against American, Japanese, and Korean alternatives. German machinery, chemicals, and precision instruments, which underpin countless American manufacturing processes, would ripple through industrial supply chains with inflationary consequences for US businesses and consumers.

The United Kingdom, still navigating post-Brexit trade relationships, sees roughly $132 billion in annual goods and services trade with America potentially jeopardized. While services trade might initially escape tariffs, financial institutions, consulting firms, and creative industries fear retaliatory measures or secondary impacts. British Aerospace, with deep integration into US defense projects including the F-35 fighter program, faces potential disruption despite ostensible national security carve-outs.

France, the Netherlands, Sweden, Norway, and Finland each face sector-specific vulnerabilities: French aerospace and luxury goods, Dutch chemicals and refined petroleum, Swedish automobiles and telecommunications equipment, Norwegian seafood and aluminum, and Finnish paper products and technology exports all enter the crosshairs. Collectively, these represent not just bilateral relationships but intricate European supply chains that feed American consumers and manufacturers.

The escalation timeline—from 10% to 25%—appears designed to maximize pressure while offering a narrow window for capitulation. A 10% tariff might be absorbed through currency adjustments or marginal price increases; a 25% levy would fundamentally alter trade flows, forcing companies to relocate production, seek alternative markets, or accept devastating market share losses.

Europe’s Response: Unity, Defiance, and Legal Recourse

European reaction has been swift, coordinated, and unambiguous. Within 24 hours of Trump’s announcement, European Commission President Ursula von der Leyen convened an emergency meeting of EU trade ministers, emerging with a preliminary retaliatory package targeting $75 billion in American exports—from Kentucky bourbon and Harley-Davidson motorcycles to California almonds and Florida orange juice, mirroring the effective pressure tactics employed during Trump’s first-term steel tariffs.

Critically, the European response extends beyond mere economic retaliation. Legal experts within the EU have begun preparing a complaint to the World Trade Organization, arguing that IEEPA invocation for territorial acquisition constitutes an abuse of emergency powers and violates foundational WTO principles. While WTO dispute resolution typically proceeds slowly—often requiring years for final rulings—the symbolic importance of challenging American legal rationale cannot be overstated. It frames the conflict not as a legitimate trade dispute but as an arbitrary exercise of power that threatens the multilateral trading system itself.

NATO allies face a particularly acute dilemma. The alliance, already strained by burden-sharing debates and divergent threat perceptions regarding Russia and China, now confronts a fundamental question: Can collective defense coexist with economic coercion among members? Several European defense ministers have privately expressed concern that Trump’s tariff threats undermine the alliance’s credibility at precisely the moment when Russian aggression demands unity. NATO Secretary General Mark Rutte, in carefully calibrated remarks, emphasized that “economic disputes must not weaken our shared security commitments,” a plea that acknowledges deep anxiety about alliance cohesion.

Perhaps most significantly, Greenland itself has asserted its voice in ways that complicate Trump’s narrative. Múte Bourup Egede, Greenland’s Premier, issued a statement reiterating that “Greenland is not for sale and will never be for sale,” while emphasizing the island’s ongoing path toward full independence from Denmark. Greenland’s 57,000 inhabitants, predominantly Indigenous Inuit, have increasingly demanded autonomy over their resource development and foreign relations—a self-determination claim that makes external purchase proposals both legally dubious and morally fraught. Greenlandic officials have suggested openness to expanded US investment and security cooperation, but firmly within frameworks respecting sovereignty rather than territorial transfer.

Economic Consequences: Beyond the Spreadsheet

Trade wars, as economists wearily remind policymakers, rarely produce clear winners. The immediate impact of Trump’s Greenland tariffs would be quantifiable: the Peterson Institute for International Economics estimates that a full 25% tariff regime could reduce US GDP growth by 0.3-0.5 percentage points while increasing consumer prices by $850-1,200 per household annually through higher costs for vehicles, pharmaceuticals, machinery, and consumer goods.

European economies would suffer comparably, with Germany potentially seeing GDP contraction of 0.4% and manufacturing job losses concentrated in export-dependent regions. Smaller Nordic economies, heavily reliant on US markets for specialized exports, could face sharper downturns. The Netherlands, a critical logistics hub for European-American trade, would experience cascading effects through Rotterdam’s ports and distribution networks.

Yet the deeper consequences extend beyond quarterly earnings reports. Global supply chains, painstakingly constructed over decades to optimize efficiency and resilience, would face abrupt reconfiguration. American pharmaceutical companies relying on Danish active ingredients or German precision equipment would scramble for alternative suppliers—often at higher cost and lower quality. European manufacturers would accelerate efforts to diversify away from American markets, potentially strengthening trade ties with China, India, and Southeast Asia in ways that diminish long-term US influence.

Financial markets, initially wobbling on tariff announcement day with the S&P 500 dropping 1.8%, face sustained uncertainty. Currency volatility—particularly euro-dollar fluctuations—could destabilize international transactions and complicate central bank monetary policy. Investment flows, already cautious amid geopolitical tensions, might retreat further from transatlantic ventures, starving promising technologies and industries of capital.

The rare earth dimension adds peculiar irony to Trump’s strategy. While Greenland theoretically harbors valuable deposits, actual extraction would require decades of infrastructure development, environmental assessments, and community consultation—hardly a near-term solution to Chinese dominance. Meanwhile, alienating European allies who are themselves seeking to diversify rare earth supply chains squanders opportunities for coordinated Western resource strategies that might genuinely challenge Beijing’s monopoly.

The Geopolitical Chessboard: Arctic Ambitions and Alliance Erosion

Beneath the tariff theatre lies a substantive geopolitical question: What does American leadership mean in the 21st century? Trump’s Greenland gambit reflects a worldview increasingly common among American nationalists—that alliances are transactional arrangements to be leveraged for discrete national advantages rather than collective security frameworks requiring mutual sacrifice and long-term commitment.

This philosophy stands in stark contrast to the architecture that has defined Western security since 1949. NATO’s Article 5 mutual defense guarantee assumes that an attack on one member constitutes an attack on all—a principle tested after 9/11 when European allies invoked the clause on America’s behalf, deploying forces to Afghanistan for two decades. The EU-US partnership on sanctions against Russia, technology export controls on China, and climate cooperation similarly presumes shared interests transcending narrow economic calculation.

Trump’s willingness to economically coerce NATO allies fundamentally challenges this framework. If the United States will threaten Denmark—a loyal ally hosting critical defense infrastructure and deploying forces to US-led missions from Iraq to Mali—over territorial ambitions, what restraints apply to American pressure on any partner? The message to European capitals is clear: alignment with Washington offers no protection from Washington’s demands.

The Arctic dimension complicates matters further. All eight nations targeted by Trump’s tariffs are Arctic Council members, engaged in scientific cooperation and environmental governance in the far north. Norway and Finland share Arctic borders with Russia; Sweden recently joined NATO explicitly to enhance Arctic security; Denmark (via Greenland) and the United States are the region’s dominant territorial powers. Effective Arctic strategy—whether addressing Russian militarization, Chinese economic penetration, or climate change impacts—requires precisely the coordinated approach that Trump’s unilateralism undermines.

Russia and China observe these fissures with undisguised satisfaction. Moscow’s propaganda apparatus has gleefully highlighted Western disunity, while Chinese state media frames Trump’s tactics as evidence of American imperial decline and unreliability. Beijing, simultaneously facing its own tariff battles with Washington, sees opportunity to position itself as a more stable economic partner for European nations seeking alternatives to American volatility. The strategic competition that ostensibly motivates Trump’s Greenland interest may actually be advanced by the very methods he employs to pursue it.

Precedents, Parallels, and the Question of Feasibility

Historical parallels to Trump’s approach are scarce and sobering. The United States has acquired territory through purchase—Louisiana from France in 1803, Alaska from Russia in 1867, the Virgin Islands from Denmark in 1917—but always through willing seller-buyer transactions, often driven by the seller’s financial desperation or strategic realignment. Modern international law, codified in the UN Charter and subsequent frameworks, explicitly rejects territorial transfer without the consent of governed populations.

The Virgin Islands precedent, interestingly involving Denmark, occurred during World War I when Copenhagen faced potential German occupation and desperately needed funds. The $25 million transaction (equivalent to roughly $600 million today) came after decades of Danish-American negotiations, formal ratification by both governments, and—crucially—no meaningful consultation with the islands’ inhabitants, reflecting colonial-era norms now universally rejected.

Greenland’s situation differs fundamentally. The island enjoys substantial autonomy under Denmark’s constitutional framework, with local government controlling most domestic affairs while Copenhagen manages foreign relations and defense. Greenland has pursued gradual independence, achieving self-governance in 1979 and expanded autonomy in 2009, with full sovereignty theoretically achievable through referendum. Any transfer of sovereignty—whether to full independence or hypothetically to another nation—would require Greenlandic consent through democratic processes that current polling suggests would overwhelmingly reject American purchase.

The tariff mechanism itself carries ominous precedent from Trump’s first term. Steel and aluminum tariffs imposed in 2018 under Section 232 national security justifications triggered retaliatory cycles that harmed American farmers, manufacturers, and consumers while achieving minimal strategic benefit. The Phase One trade deal with China, celebrated by Trump as a historic victory, saw Beijing fall short of purchase commitments while American concessions on Huawei and technology transfer went substantially unreciprocated. Subsequent economic analyses suggested that American consumers and businesses bore the primary cost of Trump’s trade wars through higher prices and disrupted supply chains.

Legal experts question whether IEEPA, designed for sanctions against hostile actors threatening US national interests, can legitimately justify tariffs aimed at coercing friendly democracies into property sales. Constitutional scholars note that while presidents enjoy broad trade authorities, using them for purposes unrelated to trade policy or genuine national emergencies potentially exceeds statutory authorization and invites judicial challenge. The prospect of courts intervening in foreign policy remains uncertain, but the legal architecture appears shakier than Trump’s confident pronouncements suggest.

Scenarios and Futures: Where Does This End?

As European and American officials absorb the initial shock, several potential pathways emerge, each carrying distinct implications for transatlantic relations and global order.

Scenario One: Strategic Capitulation and Creative Dealmaking. Perhaps least likely but most aligned with Trump’s apparent hopes, Denmark and Greenland could interpret the tariff threat as sufficiently severe to explore unprecedented arrangements. Rather than outright sale, imaginative diplomacy might yield a 99-year lease model (similar to Hong Kong’s pre-1997 status), expanded US basing rights, joint resource development agreements, or substantial American infrastructure investment in exchange for privileged access to minerals and strategic facilities. This outcome would require Greenlandic leadership to view American partnership as preferable to continued Danish association and incipient independence—a calculation that current political sentiment does not support but economic realities and Chinese pressure might eventually encourage.

Scenario Two: Managed De-escalation Through Face-Saving Compromise. More plausibly, intense diplomatic engagement over the coming weeks could produce a formula allowing Trump to claim victory while European allies avoid economic catastrophe. Enhanced US-Greenland bilateral cooperation, formalized through treaties or executive agreements, might address legitimate American security and resource concerns without sovereignty transfer. Denmark could facilitate expanded American military presence or rare earth development partnerships, framed as alliance strengthening rather than territorial concession. Trump could declare that improved Arctic access and resource agreements satisfy US interests, suspending tariffs while preserving rhetorical claims about Greenland’s importance. This path requires European willingness to reward American coercion with substantive concessions—a precedent with troubling implications but potentially preferable to economic warfare.

Scenario Three: Mutual Escalation and Transatlantic Rupture. The darkest timeline sees neither side blinking as February 1 approaches. American tariffs take effect at 10%, triggering immediate EU countermeasures targeting politically sensitive US exports and states. Financial markets deteriorate amid uncertainty; businesses accelerate supply chain reconfiguration; political rhetoric hardens on both sides. The June 1 escalation to 25% produces genuine economic pain—job losses in German automotive regions, pharmaceutical shortages in American markets, inflationary pressures complicating monetary policy. NATO faces existential questions about its viability when economic and security interests diverge so sharply. US-European cooperation on China, Russia, climate, and technology fractures as mutual recrimination overwhelms shared interests. This scenario, while catastrophic, cannot be dismissed given Trump’s demonstrated willingness to sustain confrontation and European determination not to reward extortion.

Scenario Four: Domestic American Constraint. An often overlooked possibility involves American political and economic actors constraining Trump’s ambitions. US businesses dependent on European imports—pharmaceutical companies, auto manufacturers, technology firms—would lobby intensively for tariff reversal or exemption. Congressional Republicans, facing midterm elections in 2026 and constituent pressure from affected industries, might threaten legislation curtailing presidential tariff authorities or blocking IEEPA invocation for non-emergency purposes. Federal courts could issue injunctions questioning the legal basis for tariffs, forcing administration lawyers into prolonged litigation. While Trump demonstrated during his first term a capacity to resist such pressures, the economic stakes here are substantially higher, potentially mobilizing more formidable domestic opposition.

What This Reveals About American Power and Its Limits

Beyond the immediate diplomatic crisis and economic calculations lies a more fundamental question about the nature of American power in the 2020s. Trump’s Greenland gambit embodies a particular vision of strength—one rooted in unilateral action, economic leverage, and transactional relationships rather than alliance management, institutional frameworks, and long-term strategic patience.

This approach contains internal contradictions that European observers have noted with a mixture of concern and strategic calculation. The United States seeks to counter Chinese influence in critical mineral supply chains and Arctic regions, yet does so by alienating the very partners whose cooperation would be essential for any successful containment strategy. America demands loyalty and burden-sharing from NATO allies while demonstrating that loyalty provides no immunity from Washington’s economic coercion. The administration champions sovereignty and self-determination in contexts like Taiwan or Ukraine while dismissing those same principles when applied to Greenland.

These contradictions do not necessarily doom Trump’s approach—inconsistency has rarely constrained effective exercise of power—but they do reveal limits. American economic leverage over Europe remains substantial but not absolute; the EU collectively represents a $17 trillion economy with capacity to absorb short-term pain while diversifying partnerships. Military alliances cannot be sustained indefinitely through intimidation alone; at some threshold, partners conclude that autonomy and alternative arrangements serve their interests better than subordination to an unreliable hegemon.

The Greenland episode may ultimately be remembered less for its specific outcome—whether Trump secures mineral agreements, basing rights, actual territory, or nothing at all—than for what it clarifies about early 21st-century geopolitics. We inhabit an era where even the closest democratic partnerships face strain from nationalism, resource competition, and divergent threat perceptions. The post-1945 liberal international order, built on American leadership and institutional cooperation, confronts challenges from without (authoritarian powers) and within (democratic leaders questioning multilateralism’s value).

Trump’s tariff ultimatum forces allies to answer uncomfortable questions: What price are Europeans willing to pay for transatlantic partnership? Can NATO survive fundamental economic disputes among members? How do middle powers navigate a world where the superpower they’ve relied upon for protection increasingly treats them as adversaries in resource competition?

Conclusion: The Weight of an Island in a Fragmenting World

Greenland, an island of 57,000 souls, spectacular fjords, and melting ice sheets, never asked to become the flashpoint for transatlantic crisis. Its strategic importance is real—the Arctic is indeed warming, minerals are genuinely critical, and great power competition increasingly focuses on polar regions. But the manner in which Trump has chosen to pursue American interests transforms a potential opportunity for cooperative Western strategy into a loyalty test that may fracture the alliances such strategy requires.

As February 1 approaches and European capitals weigh their responses to Trump’s Greenland tariffs, the world watches a stress test of the Western alliance’s resilience. The immediate question—whether Denmark will negotiate, Trump will relent, or economic warfare will escalate—matters enormously for trade flows, market stability, and political careers. But the deeper inquiry concerns whether democracies can sustain cooperation in an age of resource nationalism, where even longtime partners view each other’s assets as potential acquisitions and deploy economic coercion against friends with the same ruthlessness once reserved for adversaries.

History suggests that great powers overestimate their leverage and underestimate their partners’ capacity for independent action. Rome discovered this as client kingdoms rebelled; Britain learned it as colonies demanded independence; the Soviet Union realized it as satellites broke away. Whether the United States is embarking on a similar trajectory—transforming allies into adversaries through arrogance and overreach—remains uncertain.

What is clear is that Trump’s Greenland gambit represents something more consequential than another unpredictable presidential pronouncement. It is a wager on the nature of power itself: whether strength derives from the capacity to compel or the wisdom to cooperate, whether interests are best served through intimidation or partnership, whether the future belongs to those who dominate or those who build coalitions capable of addressing shared challenges.

The answer will shape not just Greenland’s fate or transatlantic trade, but the structure of international order for decades to come. An island in the Arctic has become a mirror reflecting the fractures in the Western alliance—and perhaps the fault lines along which our geopolitical era will ultimately break.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The US administration has launched an investigation into 60 countries — including the European Union — to determine whether they are permitting imports of goods produced with forced labor, setting the stage for new tariffs ranging from 10% to 12.5% and reopening a trade fight many assumed was settled, according to Deloitte’s Weekly Global Economic Update.

From Historic Tariffs to Legal Setbacks to a New Workaround

The administration spent much of 2025 attempting to construct a new global trading regime built around historically high tariffs and the constant threat of additional duties. That effort hit turbulence in 2026 when court decisions challenged the legality of certain tariff actions. Rather than retreat, the administration has pivoted to a forced-labor investigation as an alternative legal basis for imposing new duties — a maneuver that effectively route around the same legal constraints that felled its earlier tariff architecture, according to Deloitte’s tracking of the policy shift.

TD Economics notes the new Section 301 tariffs, covering the 60 countries under investigation, are set to take effect in late July 2026, replacing temporary Section 122 tariffs that had themselves replaced earlier IEEPA-based tariffs back in February — a rapid succession of legal justifications that underscores how central tariff policy remains to the administration’s trade strategy despite repeated judicial pushback, according to TD’s Canadian Quarterly Economic Forecast.

The EU Is Back on the List

Perhaps the most consequential detail is the inclusion of the European Union among the 60 countries under investigation, despite the US and EU having reached a trade agreement the previous year that was subsequently ratified by the European Parliament. The renewed scrutiny threatens to reopen a trade relationship both sides had treated as stabilized, introducing fresh uncertainty for European exporters already navigating elevated energy costs tied to the Middle East conflict.

The Broader Tariff Landscape Businesses Are Now Operating In

TD Economics estimates that despite the legal churn, the overall effective US tariff rate is likely to hold steady around 10% once the new Section 301 measures take effect — meaning that for most businesses, “peak uncertainty” over the shape of US trade policy is now behind them even if the specific legal mechanism keeps changing. Canadian exports, by comparison, face a lower roughly 6% average effective tariff rate given extensive CUSMA-compliance exemptions, according to RBC’s tariff impact analysis.

Knock-On Effects Across Asia and North America

The tariff churn has already reshaped global trade flows. RBC Economics notes that global trade patterns have reoriented dramatically to route around higher-tariff regions such as China, even as global trade volumes overall continued to rise through 2025 and the US trade deficit widened slightly despite the tariff push, according to RBC’s year-one tariff retrospective. For Asian exporters, exposure to the US market varies widely — from around 30% of exports for Vietnam to roughly 15% for China — meaning the forced-labor investigation’s ultimate impact will fall unevenly depending on each economy’s US trade concentration.

What Comes Next

With the investigation’s findings expected to determine tariff levels within the 10%-12.5% range for affected countries, businesses across the EU, and potentially exporters in Asia and Latin America caught up in the 60-country review, face a fresh compliance burden: documenting labor-sourcing practices deep into their supply chains to avoid punitive duties, even in sectors with no direct history of forced-labor allegations.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Having lost its most powerful tariff tool in the Supreme Court, the Trump administration has found a new one — and it comes with a moral argument attached.

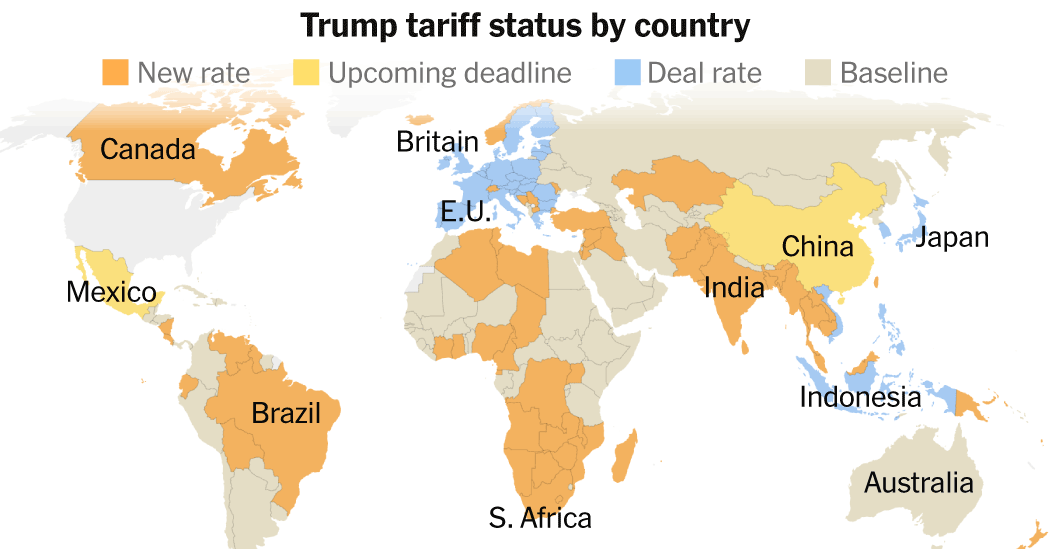

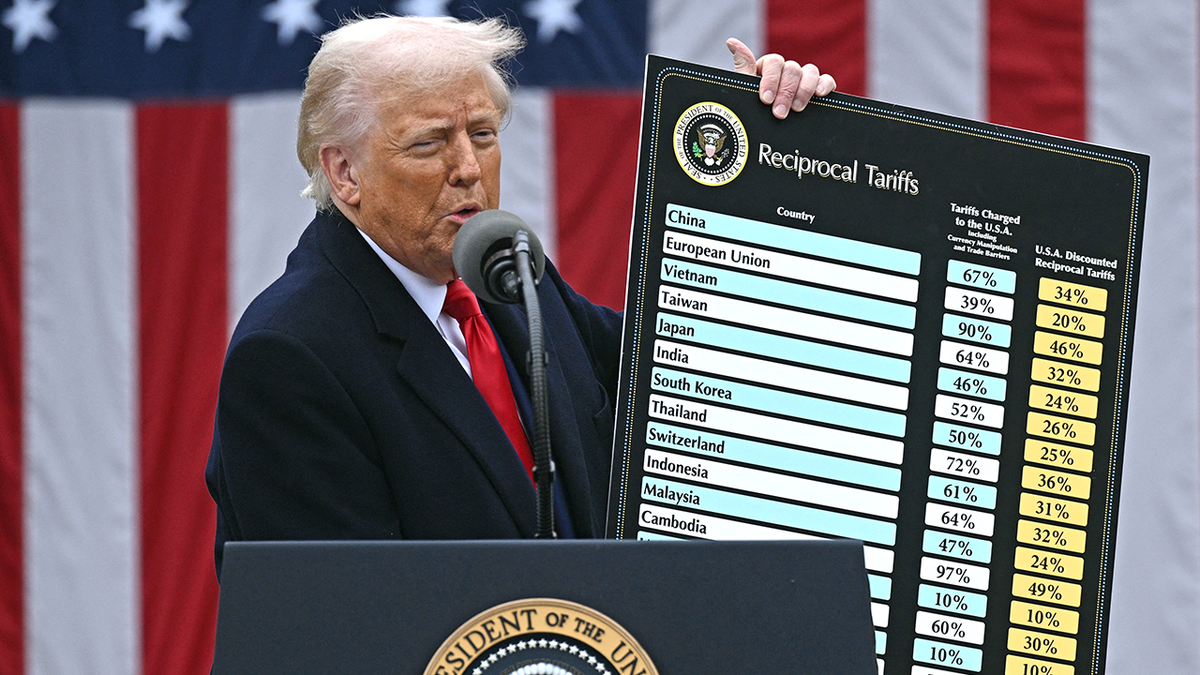

On June 2, 2026, the Office of the United States Trade Representative concluded 60 simultaneous Section 301 investigations, finding that each of the targeted economies had failed to impose or effectively enforce a prohibition on the importation of goods produced with forced labour. The proposed remedy: additional tariffs of 10% to 12.5% on all imports from those economies, covering 99.4% of total US imports by origin. The scope is unprecedented. It sweeps in China, the European Union, Japan, India, Vietnam, Australia, South Korea, and 52 other trading partners in a single action.

The Legal Architecture Post-Supreme Court

The context matters. In February 2026, the US Supreme Court struck down most of President Trump’s “Liberation Day” emergency tariffs, ruling that they exceeded the executive’s authority under the International Emergency Economic Powers Act (IEEPA). That decision dismantled the headline tariff architecture the administration had built over 2025. Rather than abandon the strategy, the Trump administration pivoted to legal frameworks with stronger statutory grounding. Section 301 of the Trade Act of 1974 authorises the president to impose levies to counter foreign trade practices that are “unreasonable or discriminatory and burden or restrict U.S. commerce” — a standard that the USTR has now applied to forced labour enforcement failures.

The investigations were formally initiated on March 12, 2026, with public hearings drawing testimony from nearly 60 witnesses and 500 written comments over April and May. The USTR’s findings drew a direct causal link between inadequate forced labour enforcement and competitive harm to US companies and workers.

The Rate Architecture

The proposed tariff structure creates two tiers. Economies that have adopted full or partial forced labour import prohibitions — notably Canada, Mexico, and a handful of others — would face 10% additional duties. The remaining 45 economies, including China, India, Japan, Vietnam, Australia, and New Zealand, would face 12.5% additional duties. A separate textile mechanism would allow a capped volume of apparel and textile imports from certain economies at a reduced rate. Electronics and AI-related products are widely expected to carry significant exemptions, according to the Economist Intelligence Unit.

The public comment period closes July 6, 2026, with hearings beginning July 7. The duties are not yet in effect — but for companies sourcing from any of the 60 targeted economies, the window to map exposure and file comments is rapidly closing.

Trading Partners Push Back

Responses from affected governments were swift and uniformly dismissive of the USTR’s reasoning. Beijing‘s commerce ministry spokesperson stated flatly that “there is no so-called forced labor in China,” and that Washington and Beijing should “meet each other halfway.” China’s foreign ministry called the accusations politically motivated.

The European Union is in a particularly complex position. Brussels signed a broad bilateral trade agreement with Washington in 2025, which the European Parliament ratified. The proposed new tariffs — which the EU called “unjustified” — would come on top of the existing 15% tariff framework from that deal. The USTR’s own report acknowledged that the EU’s anti-forced-labour regulation only entered into force in December 2027 and lacks certain enforcement elements — giving the administration its statutory foothold. The chair of the European Parliament’s trade committee described the determination as “utterly absurd” given the 2024 EU forced labour import ban law.

France‘s government questioned whether the investigation reflected genuine concerns, with officials suggesting a tariff measure was “sought first, and only then is a suitable legal justification found.”

The Supply Chain Reality for Multinationals

For global supply chain managers, the practical implications are immediate regardless of the final duty levels. The Clark Hill law firm’s trade practice advised clients to map exposure against the 60 targeted economies by HTS code, model the 10% and 12.5% rate scenarios, and test exclusion eligibility before assuming coverage — noting that even partial exposure in electronics supply chains could run to billions in added costs at scale.

Nick Marro of the Economist Intelligence Unit told CNBC that he expects the Trump administration to “unleash further investigations and tariff announcements in preparation for renewed rounds of trade talks,” characterising the Section 301 action as part of a broader pattern of building leverage ahead of bilateral negotiations. The July 24 expiration of the separate 10% baseline tariff imposed under Section 122 adds another inflection point to the calendar.

For the global trading system, the implication is clear: the US high-tariff era is not over; it has simply found a new statutory vehicle.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Trump’s 2026 tariffs represent the largest US tax increase as a share of GDP since 1993, costing households $1,500 on average. Here’s how the trade war is reshaping global supply chains, prices, and growth.

The tariff regime assembled by the Trump administration since 2025 now constitutes the largest U.S. tax increase as a share of GDP since 1993—a fact that took more than a year to fully register in household budgets, but whose full weight is being felt with increasing force in the middle months of 2026.

The average American household will pay an estimated $1,500 more in 2026 as a direct consequence of elevated import duties, according to Tax Foundation analysis—up from roughly $1,000 in 2025. The costs are not distributed evenly. Lower-income households, which spend a higher proportion of their income on goods (particularly apparel, electronics, and food), absorb a larger relative burden.

A Legal Architecture Under Pressure

The tariff program has faced serious legal challenges. On February 20, 2026, the Supreme Court ruled that the President cannot use the International Economic Emergency Powers Act—IEEPA—to impose tariffs. The decision stripped the administration of the legal vehicle it had used to impose much of its most aggressive tariff architecture.

But the administration adapted rather than retreated. In the same week as the ruling, President Trump signed an executive order imposing a 10% tariff on all countries under Section 122—a different statutory authority tied to balance-of-payments deficits—covering approximately $1.2 trillion worth of imports. The administration also initiated multiple Section 301 investigations into 60 countries on March 11, examining whether those nations allow imports of products made by forced labor. The list includes the European Union, positioning both parties for a potential renewal of the transatlantic trade conflict that a deal in 2025 had temporarily paused.

On pharmaceuticals, the administration signaled that tariffs on imported drugs could rise toward 200% by mid- to late-2026—a figure that would represent an extraordinary disruption to global pharmaceutical supply chains, though J.P. Morgan analysts noted that inventory builds and domestic manufacturing announcements by large biopharma companies should limit near-term exposure for major producers.

The China Equilibrium

U.S.-China trade relations have settled into an uneasy equilibrium. Following the June 11, 2025 trade deal announcement that left in place 20% fentanyl-related tariffs and 10% reciprocal tariffs for a combined 30%, and a subsequent series of extensions and escalations that included a 100% tariff imposed in November 2025, the two countries entered 2026 with a tense but functional trading relationship.

Chinese exporters responded to U.S. tariffs not by collapsing but by redirecting. China’s semiconductor exports surged 110% year-over-year in May 2026. That strength reflects both genuine demand from AI-related industries globally and a deliberate Chinese strategy of deepening trade relationships with Southeast Asia, the Gulf, and Europe to reduce dependence on U.S. market access.

The economic cost of U.S. tariffs on China, per J.P. Morgan Global Research, was to reduce Chinese GDP growth by roughly 0.6 percentage points through the combined effect of export drag and weaker domestic investment. But China’s export machine proved more resilient than many forecasters expected, partly because third countries absorbed Chinese goods that could not reach the U.S. market directly.

Inflation Is the Tariff’s Most Persistent Legacy

The clearest economic consequence of the tariff regime is its contribution to inflation. Businesses faced with import tariffs have three choices: absorb the cost and compress margins; pass it to consumers in higher prices; or reshore production in the U.S. at significantly higher labor costs. All three options carry economic costs, and in practice most companies have pursued a combination.

Atlanta Fed President Raphael Bostic noted in research published late 2025 that U.S. firms expected tariffs to account for 40% of their total unit cost growth in 2025 and 2026. That contribution to inflation is structural rather than transitory—unlike oil prices, which can fall as conflict dynamics ease, tariff-driven cost increases remain embedded in supply chain economics until the tariffs themselves are removed or the supply chains are restructured.

The Council on Foreign Relations analysis of tariff-Treasury interactions found that tariff uncertainty—independent of the tariffs themselves—was raising the risk premium in U.S. Treasury markets: “An eventual court ruling against the administration’s reliance on IEEPA could significantly alter the implementation path,” J.P. Morgan’s Nora Szentivanyi noted, adding that even without IEEPA, alternative statutory pathways would keep elevated tariffs in place.

Where the Trade War Goes Next

The Section 301 investigations launched in March against 60 countries—including EU members—signal that the tariff posture is not an emergency measure being wound down but a permanent feature of U.S. trade policy. Many market participants expect that Treasury will need to increase issuance of longer-term bonds starting in Q4 2026 partly to ensure liquidity along the yield curve—with tariff revenue being one of the contested variables in fiscal planning.

For U.S. businesses, the clearest strategic message from the tariff regime’s staying power is that supply chain localization is no longer a nice-to-have contingency plan. It is a competitive necessity in an environment where trade routes can change with a single executive order and where the legal found

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan Gulf Investment Outflows 2026: Peace Deal Stakes Explained

Canada Trade Diversification 2026: China, Indonesia, UAE Deals Explained

US Forced-Labour Tariffs on 60 Countries: The Hidden Trade Shock of 2026

Global Central Banks 2026: Fed, BoE and BoJ Decisions Could Reshape Markets

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Pakistan’s Most Reliable Export Is Its People: Remittances Hit $41.6 Billion, Overtaking Total Exports

Indonesia’s Confidence Problem: Record Investment, a Sinking Rupiah, and a Widening Credibility Gap

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

China’s Growth Slips to a Four-Year Low: Why Beijing Still Won’t Pull the Stimulus Trigger

The Johor-Singapore Corridor: How Malaysia Became Southeast Asia’s AI Infrastructure Powerhouse

Canada’s Economy ‘On Pause’: Inside the CUSMA Deadline That Passed Without a Deal

Dubai’s Millionaire Magnet: How the UAE Turned Middle East Turmoil Into a Capital Safe-Haven Boom

Britain’s Sixth Prime Minister in a Decade: What Starmer’s Exit Means for Gilts, Sterling and Your Portfolio

Anthropic Offers Up to $600,000 Salary for Critical IPO Role as AI Giant Prepares for Wall Street Debut

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

The AI Super Bubble Is Ready to Burst

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Bitcoin $150k Milestone Achieved as US Sovereign Crypto Pivot Looms

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

India Economic Rise 2026: How the Subcontinent Toppled Japan

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

China Housing Market Turnaround: White‑List Model Stabilises Prices

Chipmakers Just Lost 6.7% in Two Days: Inside the Great AI Trade Rotation

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025