Analysis

The Resilient Periphery: What the Singapore-New Zealand Supply Pact Means for Global Trade

In the grand theater of global geopolitics, it is easy to fixate exclusively on the tectonic friction between superpowers. We monitor the escalating US-China tech rivalries, parse the rhetoric of calibrated economic coercion, and watch with bated breath as vital maritime arteries choke under geopolitical strain. The ongoing maritime disruptions in the Strait of Hormuz, which have sent cascading shockwaves through global energy routes and downstream petrochemical derivatives, are a stark reminder of our collective fragility.

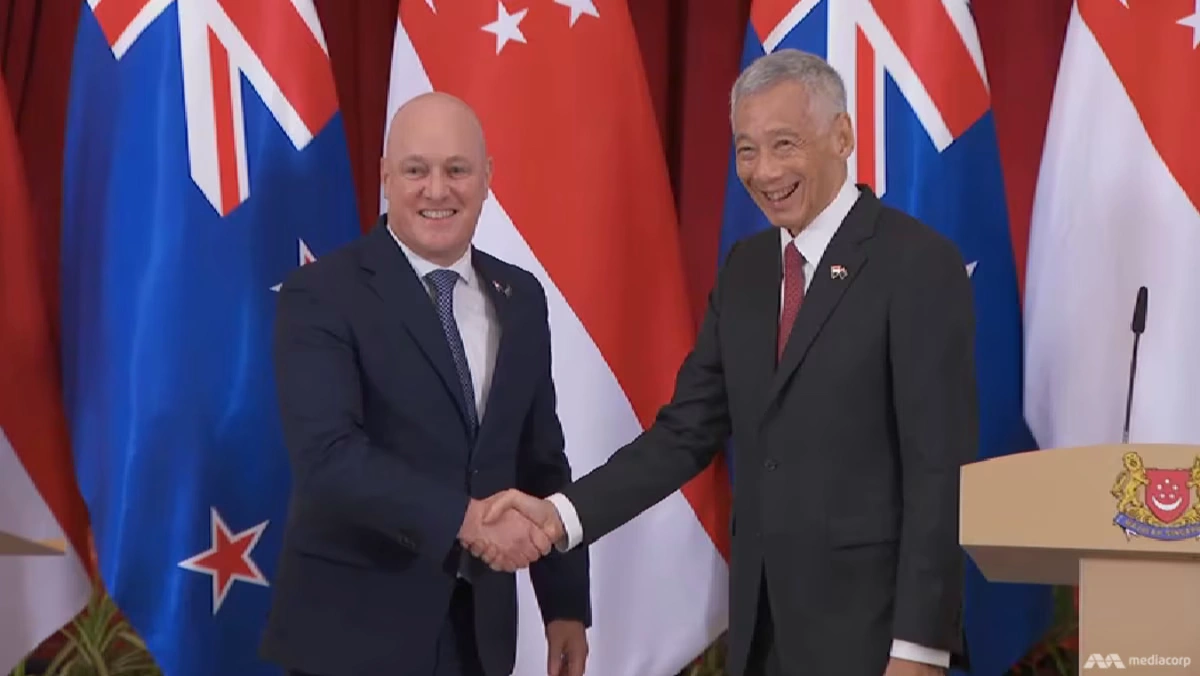

Yet, while the world’s heavyweights engage in a costly zero-sum game of tariffs and technological containment, a far quieter, vastly more pragmatic revolution is taking place on the periphery. On May 4, 2026, within the air-conditioned calm of a Singapore leadership forum, Singapore Prime Minister Lawrence Wong and New Zealand Prime Minister Christopher Luxon signed a document that, in my view, represents the future of global commerce.

The Agreement on Trade in Essential Supplies (AOTES) is the world’s first legally binding bilateral supply chain resilience pact. In an era defined by weaponized interdependence—where countries routinely hoard vaccines, ban semiconductor exports, and weaponize grain shipments—this agreement is a radical act of mutual trust. It offers a blueprint for how open, trade-dependent economies can pivot from the vulnerabilities of “just-in-time” supply chains to the security of trusted, “just-in-case” networks.

The Anatomy of the AOTES: Institutionalizing Trust

To appreciate the gravity of the AOTES, we must first understand the default reflex of the modern nation-state during a crisis: protectionism. When global supply chains buckle, the immediate political impulse is to shutter borders and halt exports to satisfy domestic anxieties. We saw this during the darkest days of the COVID-19 pandemic, and we are witnessing it again as global food and fuel prices oscillate wildly due to Middle Eastern conflicts.

The AOTES essentially outlaws this panic-induced protectionism between Singapore and New Zealand. As detailed by Singapore’s Ministry of Trade and Industry (MTI), both governments have legally committed not to impose unnecessary export restrictions on a predefined list of critical goods. This is not a vague memorandum of understanding; it is a binding framework integrated into their existing Closer Economic Partnership (ANZSCEP). The list of protected goods is comprehensive, encompassing food, fuel, healthcare products, chemicals, and construction materials.

“We will keep essential goods flowing… We will not shut each other out,” Prime Minister Wong stated with characteristic pragmatism during the signing. “In difficult times, every country will be tempted to look inward. But when that happens, supply chains break down and everyone ends up worse off.”

It takes profound confidence to codify such a promise. If a severe global fuel shortage occurs, Singapore’s domestic populace will undoubtedly demand that local refineries prioritize local pumps. By signing the AOTES, Singapore is tying its own hands to ensure New Zealand is not left stranded. Conversely, New Zealand is guaranteeing that, should a regional crisis sever international food networks, its agricultural bounty will continue to sustain Singaporeans. This is not mere diplomacy; it is the institutionalization of survival.

The Beautiful Symmetry of Food and Fuel

The Singapore-New Zealand relationship is uniquely positioned for this kind of pact because of a striking macroeconomic symmetry. They are two highly developed, profoundly open economies situated at opposite ends of the Indo-Pacific, each possessing exactly what the other lacks.

Consider the energy-agriculture nexus. As Prime Minister Luxon highlighted during the inaugural Annual Leaders’ Meeting, roughly one-third of New Zealand’s fuel is refined in Singapore. The diesel that flows from the refineries of Jurong Island directly underpins the vast farming and freight logistics networks across the New Zealand archipelago. Without Singaporean fuel, New Zealand’s agricultural engine grinds to a halt.

Conversely, Singapore imports over 90 percent of its nutritional needs. The city-state is a financial and technological powerhouse but remains existentially vulnerable to global food shocks. New Zealand, a global heavyweight in agricultural exports, serves as a vital guarantor of Singapore’s food security. Under AOTES, the New Zealand food that Singapore requires to feed its population is harvested and transported using the very diesel Singapore refined and shipped southward.

This reciprocal machinery is the antithesis of the broad, vulnerable, multi-node supply chains that defined globalization in the 2010s. It signals a shift away from efficiency at all costs, moving toward dedicated bilateral corridors that prioritize resilience. If the closure of the Strait of Hormuz limits flows to the broader region, as Prime Minister Wong starkly warned, this Singapore-New Zealand artery is designed to bypass the global arterial blockage.

Small States, Big Ideas: Navigating Geopolitical Fragmentation

The broader significance of the May 4 signing cannot be understood without looking at the Comprehensive Strategic Partnership (CSP) elevated between the two nations in October 2025. The CSP upgraded ties across six pillars, including defense, climate change, and science and technology, essentially aligning the strategic posture of two middle powers operating in an increasingly multipolar and fractured Indo-Pacific.

Both nations are acutely aware of the dangers posed by superpower decoupling. For Washington and Beijing, the restructuring of global trade is viewed through the lens of national security and strategic dominance. For Wellington and Singapore, maintaining open trade lines is quite literally a matter of economic life and death. They do not have the luxury of vast domestic markets or endless natural resources to fall back on if the global trading system collapses into fragmented, protectionist blocs.

Therefore, they have historically punched above their weight in setting global trade rules. It is worth recalling that New Zealand and Singapore, along with Chile and Brunei, were the original architects of the P4 agreement in 2005. That small, seemingly niche pact eventually snowballed into the Trans-Pacific Partnership, and ultimately the CPTPP—one of the world’s most significant trade blocs.

Similarly, they pioneered the Digital Economy Partnership Agreement (DEPA) alongside Chile, setting early global rules for digital trade, cross-border data flows, and AI governance. With the AOTES, they are running the same playbook. They are establishing a high-standard, proof-of-concept framework for supply chain resilience with the explicit hope that it will attract like-minded nations.

As PM Luxon noted in his remarks, they are open to inviting other countries that can “meet the standard” and are prepared to “have each other’s backs.” In a global economy desperate for stability, this plurilateral potential is immensely valuable. It offers a blueprint for middle powers—from Canada to South Korea to Australia—to build an overlapping web of resilient trade corridors that are immune to superpower whims or regional conflicts.

The Next Frontier: AI Deployment and the Green Transition

While the AOTES addresses the immediate, physical requirements of national survival—calories and kilowatts—the deepening Singapore-New Zealand partnership is equally focused on the defining economic transformations of our era: artificial intelligence and the green economy.

In the realm of AI, both nations wisely recognize their structural limitations. Neither Singapore nor New Zealand will win the capital-intensive arms race to build the next trillion-parameter foundational model; that arena is firmly dominated by the US-China tech rivalries and Silicon Valley monoliths. However, the true economic value of the next decade will not solely reside in creating the models, but in the speed and ingenuity of their deployment.

At the Singapore-New Zealand Leadership Forum, PM Wong emphasized synergies for deploying AI in practical, economy-boosting sectors. By establishing joint frameworks for AI governance, healthcare diagnostics, advanced manufacturing, and maritime logistics, these two nations can serve as agile regulatory sandboxes. They can attract capital from global enterprises seeking stable, forward-looking jurisdictions to test and scale AI applications without the regulatory whiplash seen in larger blocs.

Parallel to this digital collaboration is an urgent push toward the green economy. Both nations face distinct challenges in achieving net-zero emissions. Singapore is land-scarce and alternative-energy disadvantaged, relying heavily on imported natural gas. New Zealand, while blessed with renewable hydropower and geothermal energy, grapples with massive agricultural emissions.

Through the elevated CSP, the two are pooling intellectual and financial capital to address these hurdles. There is significant potential for cross-pollination between their sovereign wealth funds and institutional investors—such as Temasek Holdings and the NZ Super Fund—to scale sustainable finance, develop robust carbon markets, and accelerate the commercialization of green hydrogen and sustainable aviation fuels (SAF). It is no coincidence that the CEOs of Singapore Airlines and Air New Zealand are fostering closer ties; decarbonizing long-haul aviation is an existential requirement for both geographically isolated nations.

The Realist’s Caveat: Testing the Ties

Despite the undeniable strategic elegance of the AOTES and the broader partnership, a rigorous analysis must acknowledge the implementation risks. Treaties, no matter how ironclad the legal vernacular, are only as strong as the political will sustaining them during a true crisis.

What happens if a severe geopolitical shock fundamentally severs maritime routes through the South China Sea or the Strait of Malacca, rather than just the Middle East? While the political commitment to supply one another remains, the physical logistics of moving diesel from Jurong Island to Auckland, or dairy from Waikato to Pasir Panjang, could become prohibitively dangerous or expensive. The AOTES establishes a framework for consultations and information sharing during disruptions, but it cannot magically conjure cargo ships out of thin air or guarantee their safe passage through contested waters.

Furthermore, defining what constitutes an “unnecessary” export restriction leaves a sliver of ambiguity that could be exploited under intense domestic political pressure. If domestic fuel reserves in Singapore drop to critical, emergency-service-only levels, political leaders will face an excruciating choice between international legal commitments and domestic stability.

Scaling the AOTES to include other nations also presents a diplomatic hurdle. Bilateral trust between two deeply aligned, non-threatening, complementary economies is relatively easy to foster. Expanding this to a plurilateral agreement involving larger economies with competing domestic industries will require navigating fierce lobbying and protectionist instincts.

A Blueprint for Resilient Globalization

Despite these caveats, the signing of the Agreement on Trade in Essential Supplies on May 4 is a milestone worth celebrating. It is a necessary rebuke to the prevailing narrative of global decoupling.

For the past five years, the global economic discourse has been dominated by fear: fear of dependency, fear of technological espionage, fear of supply shocks. The default policy response from major capitals has been to build higher walls, subsidize domestic industries, and retreat into economic nationalism.

Singapore and New Zealand are offering an alternative. They are proving that the antidote to fragile globalization is not isolationism, but resilient globalization. By codifying mutual reliance, integrating their technological and green ambitions, and refusing to succumb to the sirens of protectionism, they have charted a course through the geopolitical storm.

In an era where large powers are increasingly defining themselves by who they choose to exclude, this partnership between two forward-looking middle powers reminds us of the enduring, stabilizing power of choosing to include. It is a small-state masterclass with profoundly big implications, and the rest of the world would do well to take notes.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Dubai is in the middle of building what is intended to become the world’s largest airport by capacity — a Dh128 billion ($34.8 billion) expansion of Al Maktoum International Airport at Dubai World Central (DWC), according to Gulf News. When complete, the facility will feature five parallel runways, roughly 400 gates, and the capacity to handle up to 260 million passengers a year — nearly three times the current capacity of Dubai International Airport (DXB), already the world’s second-busiest airport for international traffic, per analysis from K Estates.

Where the project actually stands in 2026

Construction crews have already excavated more than 45 million cubic metres of earth and completed the airport’s second runway, according to MyBayut’s DWC guide. The first phase — a central passenger terminal and four concourses designed to handle 150 million passengers annually — is targeted for completion around 2032, per Khaleej Times. Dubai is set to allocate AED 55 billion worth of expansion contracts by the end of 2026 alone, underscoring the pace at which the project is being financed and built.

The scale of ambition extends beyond aviation infrastructure. DWC is being planned as a self-contained “airport city,” incorporating business, cultural, and residential districts across Dubai South, roughly 35 kilometres from Dubai Marina, according to the same Khaleej Times reporting. All operations currently based at DXB — including Emirates’ long-haul network — are expected to eventually transfer to the new hub.

Part of a much bigger regional aviation build-out

Al Maktoum’s expansion is the largest single project within a broader regional wave of investment: airports across the Middle East, Africa, and South Asia are expected to spend a combined $183 billion on capacity, connectivity, and passenger-experience upgrades, with the UAE and Saudi Arabia leading the push, according to Gulf News. Within the UAE alone, expansion plans extend beyond Dubai to Sharjah and Ras Al Khaimah, with a shared emphasis on AI-enabled operations, IoT systems, and energy-efficient terminal design.

What it means for the region’s real estate and travel markets

The airport build-out is already reshaping property markets nearby. Transactions in Dubai South exceeded AED 15 billion ($4.1 billion) in just the first five months of 2025 — nearly matching the entire AED 16.1 billion recorded across all of 2024 — with analysts forecasting further price appreciation as the airport nears completion, according to K Estates. For travellers and airlines, the eventual payoff is a dramatic increase in regional connectivity capacity at a time when global air travel demand — and airfares — have both been climbing steadily through 2026.

Key takeaways

- Al Maktoum International Airport’s expansion carries a price tag of roughly $34.8 billion (Dh128 billion) and is intended to make it the world’s largest airport by 2050.

- Full build-out capacity: five runways, ~400 gates, up to 260 million passengers annually and 12 million tonnes of cargo.

- Phase one, targeted for around 2032, alone will handle 150 million passengers a year.

- The project has already reshaped Dubai South real estate, with transactions surpassing AED 15 billion in the first five months of 2025.

- It is the anchor project within a broader $183 billion regional airport investment wave across the Middle East, Africa, and South Asia.

FAQ

When will Al Maktoum International Airport be the world’s largest? Full completion is projected around 2050, though the first major phase is targeted for roughly 2032.

How many passengers will Al Maktoum Airport handle? Up to 260 million passengers annually at full capacity, with the first completed phase alone handling 150 million.

Will Emirates move its operations to the new airport? Yes — all Dubai International Airport operations, including Emirates’ long-haul network, are expected to eventually transfer to Al Maktoum International.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Thursday, August 6, 2026, is not an ordinary session for SpaceX shareholders. It is the day the company’s first post-IPO lockup period expires, freeing up to roughly 911.5 million insider-held shares — worth close to $123 billion at recent prices — for potential sale on the open market, according to The Motley Fool. To put that in perspective: SpaceX’s entire public float has stood below 280 million shares since its record-breaking June 12 IPO, meaning the unlock could roughly triple the number of tradable shares in a single day.

This is the story competitor outlets are covering as a single-day news event. Few are explaining why the structure of SpaceX’s lockup makes this particular date so unusual — or what it signals about how the company priced risk into its unprecedented listing.

Why this lockup is different from a typical IPO unlock

Most companies use a single 180-day lockup. SpaceX instead built a staggered, performance-linked release schedule tied to its earnings calendar. Insiders became eligible to sell an initial 20% tranche on the second full trading day after the company’s first quarterly earnings report as a public company — which landed on August 4, pushing the unlock date to August 6, per The Motley Fool’s original lockup breakdown.

A bonus 10% tranche would have unlocked early had SPCX traded at least 30% above its $135 IPO price for five of the ten sessions before earnings. That threshold — above $175 — was never reached; the stock has instead spent recent weeks trading near or below its offer price, having fallen more than 40% from the post-IPO high of $225.64 it touched four days after listing, according to StartupHub.ai.

Further pressure is scheduled, not speculative. Additional 7% employee tranches are due around August 21 and September 10, and analysts at 22V Research estimate insiders could collectively be free to sell as much as 44% of total shares by early September — an roughly ninefold increase in the tradable float from where it stood at listing, per Yahoo Finance.

The fundamentals behind the slide

The unlock is landing on a stock that was already under pressure for reasons beyond supply mechanics. SpaceX reported a $4.9 billion net loss for 2025 and lost a further $4.28 billion in the first quarter of 2026, a burn rate that has cooled post-IPO enthusiasm even among investors who back the long-term Starship and Starlink thesis, according to analysis from DayTradingToolkit. Despite posting stronger-than-expected earnings this week, SPCX shares tumbled roughly 14% as the market looked past the results and priced in the incoming supply, based on Bloomberg’s markets desk.

What history suggests happens next

Lockup expirations do not automatically trigger crashes — the actual price impact depends on how much of the newly eligible stock insiders choose to sell, and at what price they’re willing to part with it. Some analysts argue the reaction could be a useful signal in itself: if SPCX absorbs this wave of supply without breaking to fresh lows, that would suggest the market has already priced in the dilution risk, a view echoed by commentary from The Motley Fool’s investing desk. Others counsel patience, arguing the stock’s valuation looks stretched even before accounting for the added float.

For investors weighing an entry point, the practical takeaway is that August 6 is the first of several tests, not the last. The rolling 7% employee releases in late August and September mean supply pressure is likely to recur through the fourth quarter, with the float expected to expand roughly sixfold by late September and to around a third of total shares by Halloween, according to earlier lockup modelling reported by Investing.com.

Key takeaways

- SpaceX’s first lockup expiration frees up to 911.5 million shares (~$123 billion) for potential sale starting August 6, 2026.

- The bonus early-unlock trigger — a 30% share-price premium to the $135 IPO price — was not met, so this is the baseline release, not an accelerated one.

- SPCX has fallen over 40% from its post-IPO peak and briefly traded below its offer price.

- Further 7% tranches are scheduled for late August and mid-September, meaning supply-driven volatility is likely to continue into Q4 2026.

- The stock’s slide reflects both the lockup mechanics and underlying losses of roughly $4.28 billion in Q1 2026 alone.

FAQ

When does SpaceX’s stock lockup expire? The first tranche expired August 6, 2026, two trading days after SpaceX’s first quarterly earnings report as a public company. Additional tranches are scheduled through December 8, 2026.

How many SpaceX shares could be sold? Up to approximately 911.5 million shares — about 20% of eligible insider holdings — became sellable on August 6, against a public float that had been below 280 million shares.

Why did SpaceX stock fall despite strong earnings? Investors appear to be pricing in the incoming supply from the lockup expiration rather than reacting purely to quarterly results, alongside continued losses tied to Starship development costs.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China’s global hunt for billions in unpaid taxes is rewriting the rules for its wealthy citizens.

Just after the Lunar New Year in 2026, a Shenzhen-based family office manager began fielding a new, unwelcome kind of call from his clients. Chinese tax authorities were asking them to settle liabilities on overseas capital gains—some dating back to 2017, others as far as 2000. He had no explanation for the arbitrary five-year window, only the stark reality of a new era: the era of Beijing’s global tax hunt.

Within weeks, the picture became clearer and more alarming for the country’s ultra-wealthy. Banks in mainland China had received instructions to freeze the accounts of wealthy depositors until they could prove taxes on foreign assets, trusts, and investments had been paid. As one banker put it, speaking to the Financial Times under the condition of anonymity: “These wealthy individuals now immediately need to pay penalties and taxes in cash to reactivate their accounts.” The policy response is unambiguous: the People’s Republic has launched a campaign to recover what it believes to be hundreds of billions of dollars in unpaid taxes.

It is, by any measure, a foundational shift in China’s fiscal policy, prompted by a grinding budget deficit and a genuine overhaul of its tax system to align more closely with the United States’ model of global taxation.

The Crunch and the Crackdown

The reason for the campaign’s urgency is a stark one: Beijing is running out of money. The traditional engines of state revenue have seized. Total government land sales, once a core source of funding for local governments, have collapsed from a peak of 8.7 trillion yuan ($1.3 trillion) in 2021 to just 4.15 trillion yuan after the spectacular unwinding of the property market .

This is not a short-term liquidity crisis. It is a structural fiscal realignment. Since the pandemic, overall budget revenue in China has largely stagnated, falling by 1.7% to 21.6 trillion yuan ($3.2 trillion) in 2025 . With the property sector no longer the reliable cash cow it once was, the state has been forced to look elsewhere, and it has set its sights on the billions of dollars in wealth held offshore by its citizens. The State Taxation Administration and the Ministry of Finance confirmed the new measures, formalising a pursuit that was already well underway .

This is the hard data behind the crackdown: a fiscal imperative. It signals that the government is willing to reach decades back into the past—some accounts are being scrutinised as far back as the year 2000—to plug the hole in the present.

The Core Development: A Data-Driven Manhunt

What makes this campaign different from previous sporadic efforts is its technological sophistication and its sheer scope. The hunt is not merely targeted; it is systematic and data-driven.

Chinese authorities are leveraging the full force of modern financial surveillance, utilising data obtained through the OECD’s Common Reporting Standard (CRS), which China has been an active participant in since 2018. As tax lawyer Ye Yongqing of Anli Partners noted, regulators are steadily strengthening the supervision of cross-border capital flows and foreign exchange transactions, narrowing the scope for wealthy Chinese to transfer assets offshore .

Private bankers and wealth managers are already seeing the impact. Singapore-based bankers who manage assets for Chinese families have confirmed that new rules on foreign trusts have “shocked” their clients . Last month, China introduced comprehensive tax rules on assets transferred to foreign trusts, closing a long-standing loophole. Under the new regime, income generated by overseas trusts will be taxed at 20% across multiple stages.

The specific assets under scrutiny are varied, including real estate, stocks, precious metals, and even cryptocurrencies . Financial institutions are being asked to verify whether income from these assets has been declared to Beijing. The retroactive nature of the campaign—in some cases extending more than 25 years—has been confirmed by multiple officials, bankers, and advisors .

Why are banks freezing accounts?

Chinese banks have been instructed to cooperate with tax authorities by freezing the accounts of wealthy depositors until they settle tax liabilities on their overseas assets. This includes gains from foreign stocks, real estate, trusts, and insurance policies. The freeze is only lifted when the individual pays the outstanding tax and penalties in cash, creating powerful leverage for the state to enforce compliance quickly.

An American Model, A Chinese Reality

The structural ambition of this campaign reaches well beyond a one-off tax grab. It represents a deliberate strategy to move China’s tax system closer to the US model.

Just as the US Internal Revenue Service taxes American citizens on their worldwide income regardless of where they reside, China is beginning to adopt a similar territorial approach. This is a significant escalation. For years, wealthy Chinese individuals have used offshore trusts and other complex structures to defer or eliminate tax liabilities on foreign earnings. These structures were often established during the heyday of Hong Kong IPOs, providing a “perfect income tax shield,” according to a Singapore-based banker . The new rules aim to dismantle those shields.

The implications are profound. When the taxman begins to treat offshore gains the same as domestic profits, the calculus of wealth management for high-net-worth individuals changes entirely. As Ye Yongqing noted, this “reduces the scope for wealthy Chinese to transfer their assets abroad or structure their tax affairs through offshore vehicles” .

Victor Shih, a professor of political economy at the University of California, San Diego, summed up the driving force simply: “The motive behind the new campaign is clearly fiscal” . That fiscal necessity is now reshaping the legal architecture of Chinese wealth.

The Second-Order Effects: Compliance and Capital Flight

Downstream consequences of this policy are already rippling through the economy and across borders.

For those in the cross-border trade business, the squeeze is tangible. Zhejiang-based exporter Henry Huang told the South China Morning Post that the heightened scrutiny of unreported overseas income is “taking a real bite out of profits,” forcing him to rethink cross-border operations with little room to pass on costs to price-sensitive US and European customers .

Chinese authorities are also ramping up the legal and psychological pressure. The public security ministry’s “Fox Hunt” campaign, which focuses on extraditing economic fugitives, has already captured over 880 overseas suspects, demonstrating a hardened stance on economic crime .

Yet the most significant risk might be a self-inflicted wound. There is a growing concern that such an aggressive enforcement posture, while potentially lucrative, could accelerate the very capital flight it is designed to reverse. If the wealthy feel they are being pursued relentlessly and facing punitive fines, they may seek to move not just their cash but their entire operations to jurisdictions they perceive as safer.

A Dissenting View: The Cost of Compliance

Of course, the narrative is not without its critics. Some experts warn that the crackdown could have unintended consequences that outweigh the potential revenue gains. The shift in policy, while designed to boost state coffers, might create an exodus of talent and capital.

Furthermore, the operational challenges for tax authorities are immense. While big data and the CRS give them a new level of visibility, they are still largely in the dark about the total quantum of overseas assets. A Bloomberg report from January noted that “even in Beijing’s tightly controlled society, the crackdown is proving spotty,” with local authorities largely unaware of the amount of wealth stashed abroad .

The risk is that a “one-size-fits-all” approach could drive the most mobile taxpayers away. A banker in Singapore managing Chinese wealth observed that many trust owners now face “one-off tax liabilities” and may be forced to sell assets to cover the bills . The campaign may ultimately shrink the tax base it is trying to capture, a classic Laffer Curve dilemma applied to capital.

The “global tax hunt” is, at its heart, a story of transformation. It illustrates a China trying to build a modern welfare state without the traditional safety net of property speculation. The era of the tax-free offshore account for Chinese citizens is ending, not with a whimper but with a series of account freezes and data-driven audits. The policy represents a historic pivot, a move to international norms that at once strengthens Beijing’s fiscal position and challenges the global mobility of its wealthiest citizens. The state’s appetite for its own citizens’ foreign wealth has only just begun, and it is ravenous.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Singapore GDP Q2 2026: 5.7% Growth Driven by AI-Linked Semiconductor Exports

Al Maktoum International Airport 2026: Dubai’s $35B Plan for the World’s Largest Airport

Pakistan Economy 2026: Why GDP Growth Isn’t Reaching Ordinary Households

Strait of Hormuz Deal 2026: Iran-Oman Talks, Oil Price Impact & What Happens Next

SpaceX Stock Lockup Expiration Explained: Why $123B in Shares Could Hit the Market

The Taxman Cometh from Beijing

Pakistan IMF Program 2026: Inside the Push Toward an Interest-Free Economy

Russia Oil Revenue 2026: How Sanctions on Rosneft and Lukoil Are Draining the War Chest

Canada US Trade War 2026: Inside Carney’s Push to Cut Ties With Trump’s Tariffs

Rachel Reeves’s £25 Billion Problem: What the Autumn Budget Gap Means for Britain

Inside the Fed’s Most Divided Vote in Years: Why Warsh Held the Line on Rates

Pakistan Passed Its Third IMF Review

The Fed Is Fractured — And a New Chair Just Made It Louder, Not Quieter

The UK Economy in 2026 Is Neither Recession Nor Recovery :Stagflaton

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gold Price Forecast 2026: Fed’s July 29 Decision and Record Central Bank Buying Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

China Politburo July 2026: Stimulus Signals Explained

Pakistan Economy 2026: GDP Grows 3.7% as IMF Completes EFF Review Amid Middle East Risk

Apple vs OpenAI Lawsuit: The Economic Story Behind the Headline

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

The Yuan Now Settles 67% of Russian Oil Payments — Quiet De-Dollarization in Action

AI Capex Bubble 2026: The Hidden $662B Debt Nobody Reports

Global Stock Market Selloff 2026: Stagflation Fears Return as Iran Conflict Reignites

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis6 months ago

Analysis6 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis6 months ago

Analysis6 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks7 months ago

Banks7 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025