Opinion

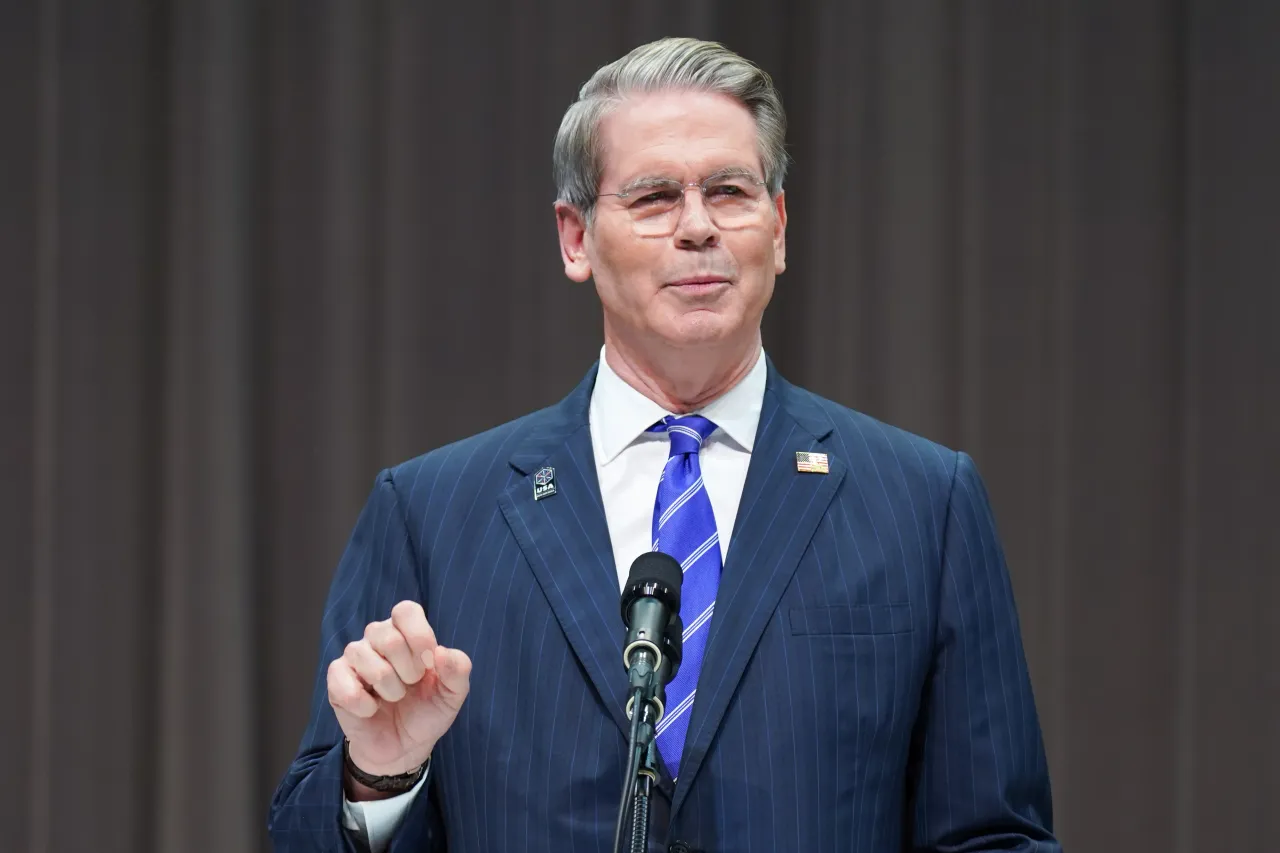

Scott Bessent’s Fed Overhaul: How the Bank of England Blueprint Is Reshaping U.S. Central Bank Independence Under Trump

There is something deliciously ironic about the man who helped break the Bank of England now contemplating whether its institutional model could fix the Federal Reserve. Scott Bessent—U.S. Treasury Secretary, former Chief Investment Officer at Soros Fund Management, and a key architect of the 1992 “Black Wednesday” trade that forced sterling out of Europe’s Exchange Rate Mechanism—sat down in early March 2026 in the ornate Cash Room of the Treasury Building with interviewer Wilfred Frost of Sky News’ The Master Investor Podcast. The resulting conversation was interrupted, dramatically, by a White House aide informing the secretary that President Trump wanted him “right away” in the Situation Room. Iran. Oil at $120. The straits closing. Bessent departed and returned an hour later—and then calmly resumed discussing the structural architecture of American monetary institutions.

That juxtaposition—geopolitical fire on one side, institutional plumbing debates on the other—captures the peculiar moment the U.S. central banking system inhabits in 2026. Donald Trump has waged the most sustained assault on Federal Reserve independence since the Nixon era. Jerome Powell’s term as chair expires in May. Kevin Warsh has been nominated as successor. A Justice Department probe of the Fed’s building renovation costs has been widely interpreted as a political pretext to bend the institution’s will on interest rates. And through it all, Bessent has positioned himself as the most consequential—and arguably most complex—voice in the debate: a self-described guardian of market integrity who has simultaneously pushed, probed, and occasionally defended the Fed’s structural independence.

His measured comparison of the Federal Reserve and the Bank of England, delivered to Frost in that mid-March session, may prove to be among the most consequential policy signals of 2026. Understated in delivery, it was nonetheless rich with implication.

A Tale of Two Central Banks: What Bessent Actually Said

When Frost asked Bessent—a long-time Anglophile who spent formative professional years in London—whether he preferred the Bank of England’s operating model to that of the Federal Reserve, the Treasury Secretary was characteristically precise in his evasion-that-isn’t-quite-evasion.

“The Federal Reserve and the Bank of England are very different institutions,” Bessent said. “The Federal Reserve is a larger, more decentralized organization with multiple regional Federal Reserve Banks and Board of Governors members, but only a subset of these members have voting rights.”

He did not declare a preference. But the framing was deliberate. In Washington, what a senior official chooses to compare is often as revealing as what he endorses outright. Bessent’s willingness to surface the BoE model—its unified structure, its clearer Treasury-Bank coordination on financial stability, its post-1997 inflation-targeting mandate—as a reference point signals an intellectual appetite for institutional reform that goes beyond the usual rhetoric about “resetting” financial regulation.

The broader interview, which spanned Bessent’s macro investing philosophy, the economics of the Iran conflict, and his decision to decline the Fed chairmanship himself, painted a portrait of a Treasury Secretary who thinks about monetary architecture in frameworks shaped by three decades of global macro experience. He described his role as “guardian of the bond market”—a phrase that, when read against the BoE comparison, suggests he sees Treasury and the central bank as co-managers of a shared sovereign credit enterprise, rather than entirely separate sovereigns.

The Bank of England Framework: What It Would Mean in Practice

The Bank of England was granted operational independence in May 1997, when Chancellor Gordon Brown—in a move that stunned markets—transferred day-to-day monetary policy decisions to the Bank’s new Monetary Policy Committee. But the architecture that emerged was not independence in the American mode. It was coordinated independence: the Bank sets interest rates, but the inflation target itself is set by HM Treasury. The Chancellor writes the Bank Governor an annual letter specifying the target. Financial stability responsibilities are shared through the Financial Policy Committee, in which the Treasury is formally represented.

This is precisely the kind of structure that market analysts have begun examining in the context of the Bessent-Warsh era at the Treasury and Fed respectively. A Bloomberg Economics newsletter in February 2026, authored by senior economics editor Chris Anstey, explicitly explored whether Warsh at the Fed and Bessent at Treasury might “remodel” the central bank’s role along lines closer to the Treasury-Bank of England relationship. The BoE model offers three features that are increasingly discussed in Washington circles:

- A government-set inflation target with central bank operational freedom to meet it. Under such an arrangement, the Fed would retain rate-setting autonomy but the 2% inflation target—currently self-imposed—would be formally codified in legislation or established by Treasury directive, making the mandate more politically accountable.

- Integrated financial stability governance. The BoE’s Financial Policy Committee includes both Bank and Treasury officials in a formal coordination structure. Bessent, who has repeatedly argued that Treasury should “drive financial regulatory policy” and criticized what he calls “regulation by reflex” at the Fed, has already moved in this direction through his aggressive engagement with the Fed’s capital reform agenda and his remarks at the Federal Reserve Capital Conference.

- A more unified, less federalist structure. The BoE has no equivalent of the U.S. system’s twelve semi-autonomous regional reserve banks, each with its own president and policy voice. Bessent’s proposal for residency requirements for regional Fed presidents—suggesting that local bank heads should actually represent their regions—represents an oblique challenge to the national talent-search model that has produced a technically homogeneous but geographically detached leadership class at the regional banks.

The Historical Irony: The Man Who Broke the BoE

Any honest account of Bessent’s BoE affinity requires acknowledgment of the extraordinary biographical irony at its core. As detailed in Sebastian Mallaby’s authoritative history of hedge fund investing, More Money Than God, Bessent was a young portfolio manager at Soros’s Quantum Fund in September 1992 when the firm launched its legendary assault on the British pound. His research into the vulnerability of Britain’s variable-rate mortgage market to interest rate increases helped convince Stanley Druckenmiller—Soros’s chief strategist—to put on what became a billion-dollar short position against sterling. On the day of the climax, it was Bessent calling for the position to be pressed harder.

The pound crashed out of the Exchange Rate Mechanism. The Bank of England burned through billions in reserves trying to defend an untenable peg. It was a defining moment for the institution’s post-independence reform—and, indirectly, for the credibility argument that central banks should not be subordinated to politically-imposed exchange rate commitments. In a sense, Bessent helped create the conditions for the BoE’s 1997 reform by exposing the limits of the old model.

Three decades later, that same intellectual arc—skepticism of rigid institutional commitments, respect for market reality, appreciation for the need of clear mandates over ambiguous ones—appears to inform his thinking about the Fed. “Unlike most of my predecessors,” he told the Financial Times in October 2025, “I maintain a healthy skepticism toward elite institutions and elite viewpoints… But I have a healthy reverence for the market.” The Black Wednesday trade was, at its core, an argument that reality will eventually overwhelm institutional pride. Bessent appears to believe the same logic applies to the Fed’s current structural ambiguities.

Trump’s Escalating Assault: Where Bessent Fits

To understand what makes Bessent’s BoE musings consequential rather than merely academic, one must understand the full texture of the pressure the Trump administration has applied to the Federal Reserve since 2025.

The assault has been multi-frontal and escalating. Trump publicly demanded the Fed cut its benchmark rate to as low as 1 percent in July 2025. He visited the Fed’s headquarters in Washington in an unusual personal inspection of cost overruns in its building renovation—a move widely read as an attempt to manufacture grounds for removing Powell. Governor Lisa Cook was subjected to an attempted dismissal, ultimately challenged in court. Stephen Miran, Trump’s own Council of Economic Advisers chair, was installed as a Fed governor while remaining affiliated with the administration—a conflict of interest that drew sharp criticism from economists. And in January 2026, the Justice Department threatened the Fed itself with criminal proceedings over Powell’s congressional testimony about the renovation project. Powell responded with unusual sharpness: he called the probe a “pretext” to undermine monetary independence, and vowed to continue doing “the job the Senate confirmed me to do.”

Republican cracks followed almost immediately. Senator Thom Tillis of North Carolina, a Banking Committee member, declared that “if there were any remaining doubt whether advisers within the Trump Administration are actively pushing to end the independence of the Federal Reserve, there should now be none.” Representative French Hill, chairman of the House Financial Services Committee, called the investigation an “unnecessary distraction.”

Into this maelstrom, Bessent has navigated with the precision of a macro trader managing risk on multiple books simultaneously. He challenged Trump’s “revenge probe” of Powell, reportedly opposing the DOJ move on both legal and economic grounds. He has previously described Fed independence as a “jewel box that has got to be preserved.” Yet he has also consistently pushed for structural reforms that would—incrementally and deniably—tilt the balance of influence toward Treasury. The residency requirement proposal for regional bank presidents. The push for a “fundamental reset” of financial regulation. The meeting with Bank of England Governor Andrew Bailey in April 2025, after which the Treasury noted Bessent was “pleased to discuss his remarks from earlier in the week”—a formulation that deliberately linked the bilateral meeting to a broader policy signal.

Whether this constitutes a sincere reform agenda, a sophisticated diplomatic shield between Trump and full institutional destruction, or some combination of both is a question that defines Bessent’s peculiar role in one of the most consequential institutional debates of the decade.

Kevin Warsh and the Architecture of Change

The nomination of Kevin Warsh as Powell’s successor adds another layer of complexity to the BoE comparison. Warsh, a former Fed governor and veteran of the 2008 crisis response, has long argued that the Fed has accumulated too many responsibilities and that its balance sheet policy has strayed from its core monetary mandate. He has advocated for a narrower, more accountable central bank—a vision that has clear family resemblances to the post-1997 BoE model.

If Warsh and Bessent share an intellectual framework—operational independence for rate-setting, greater Treasury-Fed coordination on financial stability and macro-prudential regulation, clearer mandate accountability—the result could be a genuine institutional reorganization that achieves many of the BoE’s structural features without requiring congressional legislation. Much of the architecture could be achieved through changes to Treasury-Fed coordination agreements, adjustments to the Fed’s self-imposed communication frameworks, and the gradual reshaping of the FOMC’s composition through appointments.

Markets appear to have absorbed this possibility with relative equanimity. Upon Warsh’s nomination announcement, financial markets were steady—a signal, analysts noted, that investors viewed him as credible even if they anticipated a more accommodating rate posture. Mohamed El-Erian of Queens’ College Cambridge observed in a January 2026 Project Syndicate essay that the Trump-Powell feud had “raised fears of a grim future of unanchored inflation expectations, macroeconomic instability, and heightened financial volatility”—but concluded that internal and external checks were likely “sufficiently robust to prevent a major accident.”

The Risks: Why the BoE Model Is Not a Simple Blueprint

It would be intellectually dishonest to present the Bank of England framework as an uncomplicated upgrade for the United States. Several structural differences make a direct transplant enormously complex—and potentially dangerous.

Scale and complexity. The Fed is not simply a larger version of the BoE. It manages monetary policy for the world’s reserve currency, oversees a banking system of incomparably greater global systemic importance, and functions as the global lender of last resort in crises. The BoE operates within the European regulatory ecosystem (notwithstanding Brexit) and manages a much smaller sovereign debt market. Coordinating Treasury-Fed relations at the scale of the U.S. dollar system involves risks of fiscal dominance—the historical tendency, as seen in pre-1951 America and in multiple emerging market economies, for treasury departments to subordinate monetary policy to their own financing needs.

The 1951 Accord’s shadow. The Treasury-Federal Reserve Accord of 1951, which ended Treasury’s wartime control over Fed interest rates, is the foundational document of modern Fed independence. Any formal Treasury-Fed coordination mechanism risks, at the margin, reversing the logic of that accord. The Council on Foreign Relations has explicitly noted that “the Fed did not secure true operational independence from the federal government until the 1951 Accord, which allowed it to set monetary policy without concern for the long-term borrowing costs of the U.S. government.” Bessent, as a student of economic history, understands this tension acutely.

Dollar dominance and credibility externalities. The dollar’s reserve currency status depends, in part, on global confidence in the Fed’s independence from political pressure. Even perceived coordination between Treasury and the Fed on rate-setting—let alone formal institutional mechanisms—could trigger a reassessment by sovereign wealth funds, central bank reserve managers, and international investors of U.S. Treasury paper as the ultimate safe asset. Bessent himself has described this moment as “extraordinary for U.S. dollar dominance”—a framing that suggests he understands the fragility of that dominance and the asymmetric risks of appearing to compromise it.

The inflation target question. If the inflation target were to be formally transferred to Treasury—as in the BoE model—a future administration hostile to price stability could, in theory, simply adjust the target upward. The self-imposed 2% target at the Fed, whatever its ambiguities, cannot be changed unilaterally by the executive branch. A legislated or Treasury-directed target could be.

Forward Scenarios: Three Possible Outcomes

As Powell’s May exit approaches and Warsh prepares for what could be a contentious confirmation, three broad institutional trajectories present themselves.

Scenario 1: Managed Convergence. Warsh and Bessent establish informal Treasury-Fed coordination mechanisms that functionally resemble BoE-style fiscal-monetary alignment without formal institutional change. The Fed retains its legal independence, but Bessent’s Treasury plays a more active role in financial regulatory policy, the inflation target becomes more explicitly codified, and the FOMC communication framework is simplified. Markets adjust incrementally. Dollar credibility is maintained. This is the outcome Bessent appears to be engineering.

Scenario 2: Institutional Erosion. Trump’s political pressure intensifies after Warsh’s arrival, driving a majority of the FOMC—reshaped through strategic appointments—toward persistent accommodation of fiscal policy. Long-term Treasury yields rise as investors reprice U.S. sovereign credit risk. The dollar weakens. Global central banks accelerate reserve diversification. El-Erian’s “grim future” scenario is not averted, merely delayed.

Scenario 3: Reform and Renewal. A genuine legislative overhaul—modeled explicitly on the 1997 BoE settlement, but adapted for U.S. scale—establishes clearer mandate accountability, a reformed financial stability committee structure, and a streamlined FOMC. Controversial but coherent, this outcome is the most intellectually defensible but politically the least probable in the current polarized environment.

The Bond Market as the Final Arbiter

Bessent told Wilfred Frost that his defining framework—the one that has guided both his investing career and his tenure at Treasury—is that “the crowd is right 85% or 90% of the time. It’s really when things turn, or when you could imagine a different outcome than the consensus, that’s when you can really make a lot of money.” In 1992, he imagined a different state of the world for the pound. The bond market confirmed the trade.

The bond market is now running its own analysis on the Fed-Treasury question. Daily Treasury trading volumes of approximately $1 trillion—a figure Bessent himself cited at the November 2025 Treasury Market Conference—mean that any credible signal of fiscal dominance would be priced swiftly and punishingly. Bessent knows this better than perhaps any Treasury Secretary in history. He made his fortune understanding how institutional commitments collapse under market pressure. Now he is the institution.

That is, in the end, the deepest irony of the BoE comparison. The man who broke one central bank through superior market analysis is now trying to reform another through institutional architecture. The question for global investors, policymakers, and the international monetary system is whether those two skillsets—speculative precision and institutional design—can coexist in one Treasury Secretary navigating the most politically turbulent period for U.S. monetary institutions since the Second World War.

The bond market will have an opinion. It always does.

Expert Takeaways for International Investors and Policymakers

- Watch the Warsh confirmation hearings closely for signals on whether he endorses any formal Treasury-Fed coordination mechanisms. Language around “accountability,” “mandate clarity,” or “financial stability governance” will be more important than his positions on near-term rates.

- The BoE comparison is a signal, not a blueprint. Bessent is unlikely to push for a formal legislative restructuring. The more probable outcome is incremental administrative convergence—enough to reshape practice without triggering constitutional or market crises.

- Dollar-denominated assets carry a new institutional risk premium. The sustained assault on Fed independence—regardless of its ultimate outcome—has introduced a structural uncertainty into U.S. monetary credibility that sovereign investors will have to price for at least the remainder of Trump’s second term.

- The 1951 Accord is the key historical precedent. Any future Treasury-Fed coordination framework that echoes pre-Accord arrangements should be treated as a materially negative signal for long-duration U.S. Treasuries and the dollar’s reserve currency status.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The shipment arrived at Changi before dawn — sixteen pallets of PAMP Suisse bars, crated and heat-sealed in Zurich, routed through a cargo carrier that had quietly rerouted its flight path to avoid airspace over the Persian Gulf. By the time the sun came up over Singapore’s eastern shoreline, the bars were already being logged into The Reserve’s inventory system, disappearing into one of fifteen high-security gold vaults assembled from 350 tonnes of composite steel. No fanfare. No press release. Just another morning in what is becoming, by almost every available metric, the world’s most consequential new epicentre for physical gold demand.

What is unfolding in Singapore in the first quarter of 2026 is not a story that fits neatly into the familiar grammar of commodity cycles. This is not the panicked hoarding of 2008 or the pandemic-era scramble of 2020. It is something more deliberate, more structural — and, remarkably, more demographically diverse than anything the city-state’s gold industry has seen in living memory. The queues at Orchard Road jewellers, the cranes rising above Changi South, the twenty-four-year-olds photographing serial numbers on one-kilogram bars with their phones — together, they tell a story about how geopolitical rupture reshapes financial behaviour, and why Singapore, for reasons that are as much architectural as accidental, sits at the centre of it.

How the Middle East Crisis Ignited Singapore’s Gold Demand Surge

To understand the Changi shipment, you have to understand what happened 4,000 kilometres to the west.

Gold prices surged again in early March 2026, breaching US$5,300 per ounce following United States and Israeli strikes on Iran, before settling near US$5,050 amid broader volatility linked to oil prices and inflation expectations. worldgoldpricepro The strikes effectively scrambled global risk calculations overnight. Equity indices from Tokyo to Frankfurt registered sharp losses. Insurance premiums on cargo passing through the Gulf of Oman spiked to levels not seen since the tanker wars of the 1980s. And in Singapore, dealers’ phones began ringing before the smoke had cleared.

The price trajectory tells its own story. Gold reached a record US$5,589.38 per ounce on January 28 before retreating, then rebounded above US$5,300 in early March following the US and Israeli strikes on Iran, amid broader volatility linked to oil prices and inflation expectations. Gata In the weeks that followed, that volatility — far from deterring buyers — became an accelerant. Every dip below the psychologically significant US$5,000 level triggered what dealers describe as “dip-buying waves” that emptied display cases within hours.

The current gold rally is distinguished by record central bank buying since 2022, with purchases more than twice their 2015–19 average. Central banks’ share of total demand rose to nearly 25 percent in 2024, compared with 12 percent in 2015–19. World Bank What is new in early 2026 is that this institutional floor — already historically elevated — is now being augmented from below by a retail surge of remarkable breadth and intensity. The World Gold Council’s most recent demand outlook flags continued central bank buying of approximately 850 tonnes through 2026. But it is the retail dimension, particularly in Southeast Asia, that analysts say is catching the market structurally off-guard.

Singapore’s Gold Demand Hits Historic Levels: The Data Behind the Rush

The numbers coming out of Singapore’s bullion ecosystem in the first quarter of 2026 are, by any historical standard, extraordinary.

Silver Bullion founder Gregor Gregersen said sales of gold and silver bullion surged about 350 per cent year-on-year in the 12 months to March 1, driven largely by heavy buying during price dips after a late-January correction. Gata That figure — a near-fourfold increase over a twelve-month period — would be remarkable in any market. In one that deals in physical precious metals, where supply chains depend on Swiss refineries, LBMA-certified carriers, and bonded logistics corridors that can take days to navigate, it is close to unprecedented.

At pawnshop operator ValueMax, managing director Yeah Lee Ching reported a “noticeable increase” in gold purchases, particularly for LBMA bars and 916 jewellery. The company, which posted revenue of S$425 million, plans to significantly expand its inventory of PAMP Suisse bars. worldgoldpricepro The detail about PAMP Suisse — a Geneva-headquartered refinery whose gold bars are among the most liquid and universally recognised bullion instruments in the world — matters. These are not buyers purchasing gold chains as ornaments or gifts. They are making portfolio allocations, with the same calculus that guides any serious financial decision.

David Mitchell, founder and managing director of Indigo Precious Metals, reported that his Bukit Pasoh Road outlet has seen demand more than double in 2026 compared with the same period last year. worldgoldpricepro He has also seen the supply side straining under the pressure. According to industry insiders, demand has outpaced supply, partly due to constraints in refining capacity and logistics in key hubs such as Switzerland, the UK, and Hong Kong. Malay Mail The paradox is acute: the greatest surge of physical gold demand in a generation is arriving at precisely the moment when the global system for producing, hallmarking, and delivering refined bullion is most constrained.

The escalating Middle East conflict created unexpected supply chain constraints. Airspace closures disrupted traditional logistics routes, particularly affecting gold imports from the United Arab Emirates to key consuming markets, creating a paradoxical situation where supply constraints narrowed rather than widened price discounts. World Bank In practical terms, that means premiums are rising. Buyers prepared to pay above spot are being rewarded with faster delivery. Those seeking standard pricing are waiting.

Singapore’s New Gold Vaults: Inside the Infrastructure Bet at Changi South

The most durable evidence that something structurally significant is happening in Singapore’s gold market lies not at retail counters but in the construction activity near the eastern end of the island.

Encased in sleek onyx, The Reserve soars some 32 metres above Singapore’s Changi Airport. The six-storey warehouse is designed to hold 10,000 tonnes of silver — more than a third of global annual supply — and 500 tonnes of gold, equivalent to about half of what central banks purchased in 2023. Bloomberg Completed in 2024 by Silver Bullion after its previous facility ran out of space, The Reserve is the kind of infrastructure statement that speaks louder than any marketing campaign. Fifteen individual high-security gold vaults were assembled from 350 tonnes of composite steel UL-class 2 vault panels, giving an estimated 500-tonne storage capacity for gold and other valuables. The Northern Miner

But even this monument to bullion ambition is being expanded. Silver Bullion is expanding storage capacity to 2,500 tonnes with 22 new vaults at its secure facility in Changi South, anticipating revenues of around S$2.5 billion for 2026 split evenly between gold and silver. worldgoldpricepro A S$2.5 billion revenue projection for a single Singapore-based precious metals company would have seemed fantastical five years ago. Today, given the rate at which inventory is moving, dealers describe it as conservative.

The strategic logic behind Singapore’s vault-building goes beyond current demand. “London took 200 years to build the infrastructure to become the centre of the world gold market,” said Albert Cheng, chief executive of the Singapore Bullion Market Association. “We have lots of work to do, but it won’t take us that long.” Silver Bullion Singapore’s advantage over London — and increasingly over Zurich and Dubai — is not merely geographic. It is jurisdictional. In consultation with key stakeholders including bullion banks and the Singapore Bullion Market Association, Singapore removed the Goods and Services Tax on Investment Precious Metals in October 2012, recognising that IPM are essentially financial assets, much like stocks, bonds, and other financial instruments that are typically GST-exempt. World Gold Council

Combined with Singapore’s permanent absence of capital gains tax and a regulatory framework whose stability is calibrated over decades rather than election cycles, this creates a storage and trading environment that global wealth managers find uniquely hospitable. Prior to the GST exemption, only 2% of world gold demand flowed through Singapore; the government aimed to increase that to between 10% and 15%. World Gold Council The events of early 2026 suggest that target may be within reach ahead of schedule.

Why Young Singaporeans Are Buying Gold Bars: The Demographic Revolution

The most consequential dimension of Singapore’s 2026 gold rush may be the one hardest to capture in a spreadsheet: the age of the people buying.

Alongside middle-aged customers, a growing number of younger investors in their 20s and 30s are entering the market, viewing gold as a long-term investment asset. Malay Mail This cohort is not buying gold the way their parents did — 916 jewellery selected for a wedding gift, to be locked in a drawer and forgotten. They are approaching it as a rational, data-driven portfolio allocation, comparing gold’s performance against Singapore REITs, US equities, and cryptocurrency across five-year rolling windows, and finding the metal increasingly persuasive.

What is driving this gold buying trend among younger Singaporeans is a confluence of anxieties that are distinctly of this era. They have watched two episodes of equity market carnage in a single decade. They have seen cryptocurrency oscillate between revolutionary asset class and spectacular fraud. They have observed, in real time, how quickly property liquidity evaporates when credit tightens. Gold, by contrast, is boring — and in 2026, boring is exactly what a significant slice of Singapore’s under-35 professional class is looking for.

In the first quarter of 2025, Singapore’s bullion sales reached a record 2.5 tonnes of gold bars and coins sold, a 35% increase compared to the previous year, and the highest quarterly demand since 2010. World Gold Council The Q1 2026 figures, when they are published, are expected to dwarf that record. Dealers describe a pattern in which younger buyers — many of them digital-native, fluent in live spot prices and LBMA certification requirements before they ever set foot in a dealership — are approaching their first gold purchase with more preparation than most first-home buyers bring to a property viewing.

Jewellery retailers are also seeing changes in customer behaviour, with more customers trading in older pieces purchased at lower prices for new designs or multiple items, reflecting both profit-taking and shifting preferences. worldgoldpricepro Angelina Lau of SK Jewellery Group has noted the evolution: the transaction is no longer purely sentimental. It is financial reasoning dressed in gold filigree.

Singapore vs. Hong Kong: The Race to Become Asia’s Gold Safe Haven

Singapore’s emergence as the region’s pre-eminent gold storage hub has not gone uncontested. The competition for the title of Asia’s gold safe haven is intensifying on multiple fronts.

Hong Kong plans to expand gold storage capacity to more than 2,000 tonnes in three years, up from its current 200 tonnes, and has launched renminbi-denominated contracts, mounting an explicit challenge to Singapore’s vault supremacy. Silver Bullion The proximity to mainland China — the world’s largest gold consumer and producer — gives Hong Kong a structural advantage that Singapore cannot replicate. “On the vaulting side, we are ahead in Singapore; on trading, I would say Hong Kong is ahead,” said Gregor Gregersen. “Both hubs have realised that the world is changing and they need to revisit their role when it comes to gold.” The Reserve

But Singapore holds advantages that are not easily dislodged. Political neutrality — the city is not perceived as being within either the Washington or Beijing sphere — is increasingly valued by the private wealth flows that drive high-value bullion storage decisions. “Vis-à-vis Dubai, we are a more credible financial center; vis-à-vis Hong Kong, we are seen as not part of China and therefore more neutral,” World Gold Council a government official noted in policy commentary that now reads as almost prophetically accurate. In a world fragmenting along geopolitical fault lines, neutrality is itself a premium product.

Switzerland remains the historical benchmark, but the LBMA’s own research has documented Singapore’s deliberate and systematic effort to build LBMA-equivalent frameworks over the past decade. Swiss refiner Metalor established regional operations in Singapore in 2013, the year after the GST exemption came into force. Major logistics firms — Brink’s, Malca-Amit, Loomis — have embedded significant Singapore operations. JPMorgan and UBS both offer bullion services from the city. The ecosystem that London took two centuries to build, Singapore has been attempting to construct in two decades.

The Broader Economic Calculus: Inflation, Interest Rates, and the Erosion of Paper Certainty

The surge in Singapore gold demand sits within a wider macro environment that is, for gold, almost perversely favourable.

Gold prices surged to record highs amid rising geopolitical tensions and strong investor demand supported by central bank purchases. Precious metals are projected to remain elevated into 2026, according to the World Bank’s Commodity Markets Outlook. News Directory 3 The traditional relationship between rising interest rates and weaker gold — higher yields make non-yielding bullion relatively less attractive — has broken down in 2026 in a way that is forcing even gold sceptics to revisit their models. The inflation being priced into the market is not the textbook demand-pull variety that central banks can cool with a sequence of rate hikes. It is geopolitically sourced, energy-driven, and supply-side in character — precisely the form that monetary policy is least equipped to address.

HSBC analysts emphasised that gold’s traditional safe-haven characteristics do not insulate it from significant price fluctuations. ANZ Bank issued guidance projecting gold would reach $5,800 per ounce during the second quarter of 2026. World Bank J.P. Morgan has published a year-end target of US$6,300. Even assuming significant volatility around those projections, the directional consensus among major institutional analysts is striking in its alignment: gold has further to run, and the structural drivers — central bank diversification away from dollar assets, geopolitical fragmentation, demographic shifts in investor preference — are not resolved by a ceasefire.

According to Bloomberg’s precious metals research desk, Singapore’s storage facilities are filling faster than at any point since the city formally positioned itself as a bullion hub. That rate of fill is not driven purely by crisis buyers. It reflects a long-term allocation decision being made, simultaneously, by sovereign wealth funds, family offices, retail investors, and twenty-six-year-olds who have been quietly reading the World Gold Council’s research on their lunch breaks.

Risks and Realities: What Could Reverse Singapore’s Gold Boom

Honest analysis demands a reckoning with the downside scenarios, and they are not trivial.

“We have seen more buyers than sellers over the past year, but more sellers are now entering the market, which is typical after strong price movements,” noted David Mitchell of Indigo Precious Metals. worldgoldpricepro The pattern he describes — later entrants buying near the top as earlier investors take profits — has preceded corrections in every previous gold cycle. At over US$5,000 per ounce, gold is priced for a world in which the Middle East crisis is both sustained and escalatory. Any credible diplomatic movement toward de-escalation would likely trigger a sharp correction, leaving buyers who entered at current levels nursing paper losses.

There is also the structural question of whether Singapore’s vault ambitions are outrunning the liquidity that would make them self-sustaining. “What really matters in this industry is building up liquidity,” said Gregersen. Both hubs have realised that the world is changing and they need to revisit their role when it comes to gold. Silver Bullion Storage capacity without trading depth is a warehouse, not a market. Singapore has the former in abundance; the latter remains a work in progress.

And yet — even applying the most conservative stress tests to the scenario — the case for Singapore as the defining Asian node in global gold infrastructure grows stronger with each passing quarter of the current crisis. The city has spent fourteen years building the regulatory, logistical, and fiscal architecture for exactly this moment. The demand has arrived.

The Unmistakable Signal: Singapore’s Gold Story Is Only Beginning

There is a particular kind of intelligence that operates in commodity markets — not the frenzied intelligence of a trading floor, but the slow, patient intelligence of capital seeking sanctuary over decades. It moves in response to tectonic forces: the fragmentation of great-power relationships, the erosion of confidence in paper systems, the generational transfer of wealth to cohorts who carry different memories and different instincts.

What Singapore’s gold rush of early 2026 represents, viewed through that longer lens, is not a crisis trade. It is a structural repositioning — of capital, of infrastructure, and of investor psychology — that the crisis has accelerated but not invented. The cranes above Changi South would have risen eventually. The young Singaporeans queuing at ValueMax would have found their way to bullion eventually. The Middle East has simply compressed the timeline.

The metal that outlasted the Roman Empire, the Ottoman Empire, and Bretton Woods is finding a new generation of custodians. They are arriving at the counter with spreadsheets on their phones and specific questions about LBMA certification. They are building vaults visible from the landing approach at one of the world’s busiest airports. They are, in their very deliberateness, making the most bullish possible argument for gold’s enduring relevance — not because the world is ending, but because they have decided, with clear eyes and careful calculation, that they would rather own some of it.

That calculation, repeated several hundred thousand times across the city-state and the broader region it serves, is what a gold rush looks like when it is driven not by panic, but by conviction.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The central bank that spent two years engineering the perfect soft landing is now watching the runway catch fire.

Speaking at the ECB Watchers Conference in Frankfurt on Wednesday, European Central Bank President Christine Lagarde delivered the most explicit hawkish signal Frankfurt has fired in nearly four years: “We are prepared, if appropriate, to make changes to our policy at any meeting.” The Irish Times Six short words. Enormous implications.

The timing is not accidental. Soaring energy costs brought on by the conflict in the Middle East are stoking fears of another inflation spike like the one four years ago, with Bundesbank chief Joachim Nagel and others signalling borrowing costs may need to be lifted as soon as April if the price outlook sours further. The Irish Times Lagarde’s carefully chosen phrase — “at any meeting” — is central-bank language for: we are not waiting for a scheduled window; the next move could come at any of the eight annual gatherings on our calendar. Markets heard her clearly.

The immediate market reaction confirmed it. ECB-dated OIS now price 16 basis points of hikes through April — up from 14.5bp before the sources update hit the wires — while Bloomberg reported the possibility of a rate hike in April, and Reuters sources suggested April was too early but June increasingly viable. Marketnews The euro, which had been softening all week amid risk-aversion, traded at 1.1457 against the greenback — down from 1.1778 before U.S.-Israeli attacks on Iran began — making imports, including energy, more expensive for buyers in the eurozone. Morningstar European equities absorbed a fresh leg lower, and German Bund yields climbed as traders repriced the front end.

This is not the Christine Lagarde who, just weeks ago, was serenely describing Frankfurt’s policy stance as being in a “good place.” That phrase — her mantra through six consecutive hold decisions — has now been retired, deliberately. “We are starting from a good base, so I’m not saying we are in a good place — we are both well-positioned and well-equipped to deal with the development of a major shock that is unfolding,” CNBC she told reporters after the March 19 Governing Council decision. The language shift is not cosmetic. In the theology of ECB communications, “good place” was a dovish comfort signal; its removal is an act of institutional vigilance.

The Iran Shock: Why the ECB’s Inflation Calculus Collapsed Overnight

To understand how dramatically the picture shifted, consider the ECB’s own projections. At the December 2025 meeting, staff projected headline inflation averaging 1.9% in 2026, 1.8% in 2027, and 2.0% in 2028 — a Goldilocks path that seemed to confirm the ECB could sit comfortably at its neutral 2% deposit rate indefinitely. European Central Bank That serenity lasted exactly eleven weeks.

U.S.-Israeli attacks on Iran began in late February 2026 Global Banking and Finance, and by the time the Governing Council convened on March 19, the energy landscape had been redrawn. Brent crude closed at $90 per barrel on the technical cut-off date of March 11 — yet by the meeting itself, it was trading in a range of $112–$115, having touched $119 during the session. The Irish Times Natural gas prices followed a similar trajectory. The ECB’s own updated staff projections incorporated this shock, and the numbers are stark.

The ECB’s latest staff projections show inflation averaging 2.6% in 2026, before easing to 2.0% in 2027 and 2.1% in 2028 Euronews — a revision of more than half a percentage point for this year alone, driven entirely by energy. But the baseline is already obsolete. In a more adverse scenario — involving stronger and longer-lasting disruptions to oil and gas supply through the Strait of Hormuz — inflation could rise to 3.5% in 2026. In a severe scenario, where energy prices remain elevated for longer, headline inflation could reach as high as 4.4% in 2026. Euronews

To put that last number in context: eurozone inflation has not touched 4% since the tail-end of the post-Ukraine energy crisis. The ECB would be back in emergency territory before summer.

Growth, meanwhile, has been revised sharply lower. The ECB expects GDP growth of just 0.9% in 2026, 1.3% in 2027, and 1.4% in 2028 TRADING ECONOMICS — essentially stagnation-adjacent for the current year. The stagflationary cocktail that haunted the 2022–2023 cycle is back on the table.

‘Monitor Closely’: Decoding the ECB’s Institutional Vocabulary

Inside the ECB, language carries the weight of precedent. Officials and seasoned ECB-watchers know that certain phrases function as coded escalation signals — a vocabulary that stretches back decades and is never used carelessly.

The fact that the well-known phrase “monitor closely” has returned to ECB communications is a clear signal that the central bank has shifted to a higher alert. In the past, the term “monitor closely” had always been a sign of high alertness — the time it was used was during the short-lived banking tensions in March 2023 and before in 2022. In the distant past, “monitor closely” was followed by “vigilance” in the run-up to rate hikes. ING THINK

That sequencing matters enormously. The 2022 cycle — when the ECB spent months saying it was “monitoring” inflation before eventually being forced into the most aggressive tightening campaign in its history — is the institutional ghost Frankfurt is desperate not to repeat. “In those four years, we have learned,” Lagarde said, noting that interest rates are now higher, inflation lower, and the labour market less overheated than four years ago, when the economy was re-emerging from the COVID-19 pandemic. “I think we also understand better the mechanism of the pass-through into indirect and second-round effects.” Global Banking and Finance

That self-aware acknowledgment of the 2022 policy mistake is the most important sentence Lagarde has delivered in years. It signals that the ECB’s reaction function has fundamentally changed: the central bank will not let second-round effects embed before it acts. “We will not act before we have sufficient information on the size and persistence of the shock and its propagation,” she said at the ECB Watchers Conference. “But we will not be paralysed by hesitation: our commitment to delivering 2% inflation over the medium term is unconditional.” The Irish Times

What Markets Are Pricing: Hike Paths, Bond Yields, and the April Trigger

The market reaction to the ECB’s hawkish pivot has been swift and instructive. Traders are pricing in two or three rate hikes by December, even as most economists still see no change, betting that the ECB would not tolerate another war-fuelled spike in inflation after being stung by Russia’s 2022 invasion of Ukraine. Global Banking and Finance

The April 29–30 meeting is now in live play. ECB policymakers would be ready to raise interest rates as soon as their next meeting should fallout from the war in Iran push inflation too far above target, according to people familiar with the situation. While nothing has been decided yet and a later date may be more appropriate, factors including signs of second-round effects could trigger such a move at the April 29–30 gathering. Bloomberg

The oil price threshold matters. A rate rise at the April meeting would require an even bigger surge in energy prices, with one of the sources mentioning a $200 per barrel oil price as a potential trigger. Benchmark Brent crude touched $119 per barrel on March 19. The ECB itself said that a “severe” scenario under which crude peaks at almost $150 per barrel by June would likely require “tighter monetary policy.” Global Banking and Finance

Economists at Barclays said the ECB would raise rates in a scenario where Brent crude settled at around $100 a barrel — compared to $113 at the time of the meeting — and natural gas at 70 euros. RTÉ With spot prices already comfortably above that threshold, the bar to a June hike, at minimum, is looking increasingly low.

Key Takeaways:

- ECB deposit rate remains at 2.0% (sixth consecutive hold), main refinancing rate at 2.15%

- Lagarde replaced “good place” language with “well-positioned and well-equipped” — a significant hawkish shift

- Baseline 2026 inflation: 2.6%; severe scenario: 4.4%

- Brent crude at ~$112–119/bbl at March 19 meeting vs. March 11 cut-off assumption of $81/bbl

- Markets pricing 16bp of hikes through April; 2–3 hikes by December

- EUR/USD at approximately 1.1457, weaker post-war, amplifying imported inflation

- April 29–30 ECB meeting is the next live decision point

The Stagflation Trap: Growth Risks and the Dual Mandate Squeeze

Here lies the ECB’s cruellest dilemma. The same oil shock that threatens to push inflation higher is simultaneously crushing the growth outlook. GDP growth has been revised down to just 0.9% for 2026 — barely above stagnation — as the war weighs on real incomes, business confidence, and consumption. Euronews An economy growing at sub-1% is not one that screams “raise rates.”

And yet Lagarde has made clear that the ECB will not be paralysed by this tension. The key variable is second-round effects — the mechanism by which an initial energy shock bleeds into wages, services prices, and long-run inflation expectations. “If persistent, higher energy prices may lead to a broader increase in inflation through indirect and second-round effects — a situation which requires close monitoring,” Lagarde said. Euronews

“The experience of the 2022 energy crisis, and consumers’ expectations still scarred from that episode, could make the ECB quicker to hike if energy pressures are sustained,” HSBC economist Fabio Balboni noted. Morningstar Crucially, Isabel Schnabel, a prominent anti-inflation hawk among ECB policymakers, has also warned about the “scars” that episode left on households and businesses — though she notes an important difference: monetary and fiscal policies are not loose this time, which should help limit inflationary pressures. RTÉ

In a scenario where the war in the Middle East and soaring energy prices remain limited in time, the ECB will talk like a hawk but not walk like a hawk. However, if energy prices stay high or higher for longer and find their way into other parts of the eurozone economy, the central bank apparently wouldn’t shy away from rate hikes. ING THINK

That is the critical fork in the road. Duration, not magnitude, is the decisive variable. A spike that resolves in eight weeks is one problem. A sustained disruption lasting into Q3 2026 — with supply chains rerouted, shipping costs elevated, and wage negotiators armed with fresh grievances — is something else entirely.

Global Spillovers: The Fed, the BOE, and Emerging Market Currencies

Frankfurt is not facing this shock in isolation. The Federal Reserve kept rates unchanged, as expected, and its Summary of Economic Projections showed policymakers still expect to deliver one rate cut in 2026 and another one in 2027. Officials revised inflation higher, with PCE inflation now expected at 2.7% at the end of 2026 versus 2.4% in December, while growth was revised to 2.4% versus 2.3% previously. FXStreet

The Bank of England, meanwhile, voted unanimously to keep its benchmark interest rate on hold at 3.75%. Before the war in Iran erupted in late February, the BOE had been expected to cut its key interest rate. CNBC That rate-cut cycle is now indefinitely suspended.

Central banks in the United States, Canada, Japan, Britain, Sweden, and Switzerland delivered broadly similar messages — a global synchronised pause, with a hawkish tilt. Global Banking and Finance The synchronicity matters: when multiple major central banks simultaneously signal willingness to tighten, the knock-on effects for emerging market economies that borrowed in dollars and euros — from Turkey to Indonesia to South Africa — can be severe, as capital flows back towards developed-market yields.

For the euro area, the weaker EUR/USD compounds the inflation problem directly. Energy is priced in dollars. A euro that buys fewer dollars means European households pay more for every barrel of crude and cubic metre of gas, regardless of what happens to spot commodity prices. The currency channel is, in effect, a built-in amplifier on the energy shock — and it is currently working against Frankfurt.

What Investors and Businesses Should Watch

What Investors Should Watch:

- April 30 ECB Decision: The next meeting is the true test. Monitor Brent crude pricing in the two weeks preceding — if it holds above $100/bbl, a hike becomes a live possibility. If it retreats toward $85, the ECB is likely to hold and reassess in June.

- Second-Round Effect Indicators: Watch the ECB’s Wage Tracker (updated monthly), eurozone services inflation, and industrial selling price surveys. These are Lagarde’s own stated tripwires.

- Inflation Expectations: The 5y5y EUR inflation swap — the market’s long-run inflation gauge — is the ECB’s preferred thermometer for anchoring risks. Any sustained move above 2.5% would be an emergency signal for Frankfurt.

- Hormuz Developments: Geopolitical developments in the Strait of Hormuz remain the dominant macro variable for the next 6–8 weeks, overriding all conventional economic indicators.

- EUR/USD: A further decline in the euro amplifies the imported inflation channel, potentially pulling the ECB’s trigger sooner. Watch 1.12 as a line in the sand.

Eurozone Growth at Risk: The Political Economy of Austerity Under Fire

There is a painful irony in the current configuration. Germany, the eurozone’s fiscal anchor, is finally loosening its legendary Schuldenbremse — the constitutional debt brake — to fund defence and infrastructure spending, a stimulus long demanded by Brussels. That fiscal expansion, however welcome in the short run, arrives precisely as the energy shock threatens to reignite inflation.

Investors are already bracing for higher government borrowing in response to the Iran crisis — a shift that comes on top of Germany’s plans to sell more debt to ramp up military and infrastructure spending. That could further fuel inflation and has already pushed up bond market borrowing costs before any ECB action. Global Banking and Finance

The result is a doubly challenging environment for southern European sovereigns — Italy, Spain, Portugal — whose financing costs are sensitive to both ECB policy rates and market risk premia. Should the ECB raise rates in June, peripheral bond spreads will widen, potentially triggering the very financial fragmentation that Frankfurt’s Transmission Protection Instrument (TPI) was designed to prevent.

Growth in the eurozone could drop by 0.2% in 2026 if the impact of the conflict persists, according to the UK-based National Institute of Economic and Social Research. Morningstar Against an already-revised baseline of 0.9%, that would push the eurozone to the verge of contraction. The ECB’s communications department will have to perform extraordinary feats of policy narrative management to explain rate hikes amid near-recession conditions — if that moment arrives.

The Verdict: Hawkish Pivot, Conditional Tightening, and the Long Game

Step back from the daily noise, and the strategic picture that emerges from Frankfurt is coherent, if uncomfortable. The ECB has made a deliberate choice to move from passive accommodation to active vigilance — not a tightening, but a pre-positioning. All in all, a rate hike is not yet on the table, but today’s meeting clearly marks a hawkish pivot. ING THINK

Lagarde’s “at any meeting” formulation is the monetary policy equivalent of a chess player picking up a piece and placing their hand on it, without yet committing to a square. The signal is intentional: the ECB has options, the ECB is watching, and the ECB will not repeat 2022’s mistake of labelling a sustained shock “transitory.”

“This hawkish tilt supports our view that the ECB is more likely to raise rates rather than lower them this year, with cuts now seemingly out of the question,” noted Roman Ziruk, senior market analyst at Ebury. The Irish Times

The next six weeks — running up to the April 29–30 Governing Council — will determine whether this is a credible hawkish posture or the opening act of an actual tightening cycle. The variables are brutally simple: oil prices, wage data, and the trajectory of a war that no economist’s model fully anticipated. If Lagarde sounds like a hawk today, it is because history — painful, recent, institutional memory — has taught her that waiting costs dearly.

In Frankfurt, the fireside chat is over. The fire is outside.

There is something quietly extraordinary about watching Christine Lagarde retire the phrase “good place” after using it as a near-liturgical mantra through six consecutive hold decisions. Central bank language is a form of institutional trust management — every repeated phrase becomes a commitment, and every abandoned phrase becomes a statement about the world having changed.

The phrase “at any meeting” is doing significant work here. It is not “we are considering raising rates.” It is not “the next meeting is live.” It is a blanket statement of optionality: we could act in April, June, July, September — wherever the data takes us. This is textbook forward guidance deployed in reverse — rather than anchoring expectations of inaction, Lagarde is deliberately leaving them unanchored, forcing markets to price a broader distribution of outcomes.

The deeper question — and the one that keeps ECB-watchers up at night — is whether the central bank has internalized the right lesson from 2022. That crisis showed the catastrophic cost of wishful thinking: the ECB’s initial “transitory” framing delayed tightening by crucial months, allowing inflation expectations to drift and ultimately requiring emergency-speed rate hikes that hurt growth. The self-awareness Lagarde displayed this week, noting “in those four years, we have learned,” is encouraging. But institutional memory is most reliable when it is written into frameworks and processes, not just recited from podiums.

What this moment also reveals is the irreversibility of the geopolitical dimension in central banking. For three decades post-Cold War, energy markets were treated as a background variable — occasionally disruptive, never structural. 2022 changed that. The Iran shock of 2026 confirms it. Central banks are now, unavoidably, geopolitical actors — making monetary decisions whose outcomes depend on military developments they cannot observe, predict, or control. Christine Lagarde did not train for that role at Sciences Po. But she is, with increasing command, learning to inhabit it.

People Also Ask: Related Questions

- Will the ECB raise interest rates at the April 2026 meeting? ECB sources reported by Bloomberg and Reuters suggest a hike is possible at April 29–30, contingent on sustained energy price elevation and emerging second-round inflation effects. Markets are pricing 16bp of hikes through April.

- What did Lagarde say at the ECB Watchers Conference on March 25, 2026? Lagarde said the ECB “will not be paralysed by hesitation” and is “prepared, if appropriate, to make changes to our policy at any meeting” — the clearest hawkish signal since the Iran war began.

- How does the Iran war affect eurozone inflation and ECB rates? The conflict has pushed Brent crude above $115/bbl, causing the ECB to revise its 2026 inflation forecast from 1.9% to 2.6%. A severe scenario with sustained energy disruptions could push inflation to 4.4% in 2026, which the ECB has said would require tighter monetary policy.

- What is the current ECB interest rate in 2026? As of March 19, 2026, the ECB deposit facility rate is 2.0%, the main refinancing rate is 2.15%, and the marginal lending rate is 2.4%. All three are unchanged for the sixth consecutive meeting.

- How is EUR/USD responding to ECB hawkish signals and the Iran war? EUR/USD has weakened from around 1.1778 pre-war to approximately 1.1457, reflecting combined risk-aversion and dollar strength. A weaker euro amplifies imported energy inflation, potentially accelerating the ECB’s decision to raise rates.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Merck’s $6 Billion Cancer Power Move: The Terns Pharma Deal That Rewrites Pharma’s Post-Keytruda Playbook

Merck nears a $6bn all-cash acquisition of Terns Pharma and its CML drug TERN-701. Here’s the full strategic picture—what it means for patients, investors, and Big Pharma’s 2026 M&A wave.

The ink isn’t dry. The deal isn’t signed. But the logic behind Merck’s reported $6 billion pursuit of Terns Pharmaceuticals is already one of the clearest strategic narratives in modern pharma — a $30 billion time bomb called Keytruda, and the urgent search for what comes after.

Merck is nearing a roughly $6 billion all-cash deal to acquire Terns Pharmaceuticals, the Financial Times reported on Tuesday, citing people familiar with the matter. MarketScreener Talks between the two companies are at an advanced stage, and a deal could be reached within days. MarketScreener The target: a Foster City, California clinical-stage company whose lead drug is quietly generating the most excitement in blood cancer treatment since a Novartis blockbuster redrew the CML landscape a generation ago.

For Merck, this is not merely another acquisition. It is an act of strategic triage — and perhaps the most scientifically precise bet the Kenilworth giant has placed since it licensed pembrolizumab from Schering-Plough in 2009 and renamed it Keytruda.

Why Keytruda’s Patent Cliff Is the Most Watched Clock in Global Pharma

To understand why Merck is willing to pay a premium for a drug that has never been approved — and has barely cleared Phase 1 — you must first understand the existential arithmetic of the world’s best-selling medicine.

Keytruda is slated for a loss of exclusivity in 2028, and a growing pipeline of biosimilars is already lining up to take a shot at the drug’s massive market. Fierce Pharma The cancer therapy brought the company $29.5 billion last year C&EN, representing nearly half of Merck’s total revenue. CEO Robert Davis sees about $70 billion in commercial opportunities by the mid-2030s and has described the current pipeline as one of the “deepest and broadest” Merck has ever had. Stocktwits

That confidence, however, must be earned — deal by deal, trial by trial. Merck has predicted Keytruda will collect $35 billion in peak annual sales in 2028, the same year the drug will face an expected patent cliff. Fierce Pharma After that, biosimilar entrants from Samsung Bioepis, Amgen, and Indian manufacturers are expected to erode revenues precipitously. The company needs successors, and it needs them now.

The response has been an M&A blitz of rare intensity. Merck has accelerated dealmaking in recent months, snapping up Verona Pharma for $10 billion and Cidara Therapeutics for $9.2 billion last year Investing.com, adding a first-in-class COPD therapy and a long-acting flu antiviral, respectively. Merck has been building up its late-stage drug pipeline since 2021 and has signed several deals to broaden its portfolio. U.S. News & World Report February brought yet another structural bet: Merck split its core pharmaceutical business in two — one housing its oncology portfolio and the other including all non-cancer medicines Fierce Pharma — a move analysts interpreted as pre-positioning for either a spin-off, a focused acquisition strategy, or both.

The Terns deal, if confirmed, is the latest and sharpest arrow in that quiver.

TERN-701: The Drug That Has CML Specialists Talking in Superlatives

Chronic myeloid leukemia is not a common cancer. Roughly 8,900 new cases are diagnosed in the United States each year. But it is a high-value market — heavily treated with expensive precision medicines — and Terns has built its entire identity around the conviction that the next generation of CML therapy remains conspicuously unfinished.

Terns’ lead cancer drug candidate is TERN-701, which is in development for the treatment of relapsed/refractory CML under the Phase 1 CARDINAL trial. RTTNews The drug’s mechanism is where the science gets genuinely interesting: TERN-701 is active at the myristate pocket of BCR-ABL1, providing it with 10,000 times greater selectivity than active-site tyrosine kinase inhibitors. Onclive

That molecular precision matters enormously in a disease defined by acquired resistance. The current standard of care for later-line CML, Novartis’s asciminib (Scemblix), was itself an allosteric BCR-ABL inhibitor that redrew treatment algorithms when it won approval — but resistance mutations and tolerability issues mean a significant portion of patients still cycle through therapies without achieving durable molecular response. Early study results suggest that TERN-701 could be a successor to Novartis’s blockbuster Scemblix. Statnews

The CARDINAL trial data, presented at the American Society of Hematology annual meeting in December 2025, was what turned heads. At the recommended Phase 2 dose of at least 320 mg once daily, the overall 24-week major molecular response rate was 80% among efficacy-evaluable patients with more than 24 weeks of follow-up. Onclive For patients maintaining MMR, the rate held at 100%. Ternspharma

The safety profile is equally notable. The majority of treatment-emergent adverse effects were low grade, with no apparent dose relationship. Rates of cytopenias were generally low, with less than 10% Grade 3 thrombocytopenia and neutropenia. Onclive No dose-limiting toxicities were observed up to the maximum dose of 500mg QD. Ternspharma

For heavily pre-treated patients — many of whom had previously received asciminib, ponatinib, and investigational next-generation therapies — these numbers are not merely encouraging. They are, by the standards of relapsed/refractory CML, remarkable. “Best-in-disease potential” is the phrase Terns itself has used, and the clinical data does not obviously contradict that claim.

The Valuation Calculus: What Does $6 Billion Actually Buy?

The all-cash deal is expected to value Terns at a premium to its market capitalization of about $5.3 billion. Investing.com That premium, while meaningful, is modest by the standards of 2025–2026 oncology M&A — a sector where bidding wars routinely push acquirers to 60–80% above last close.

Why the relative restraint? Several factors shape the math.

TERN-701 remains in Phase 1. There is no approved product, no commercial infrastructure, and no Phase 3 data. Pivotal trial results — the evidence that would trigger blockbuster valuations and genuine upside scenarios — are still at least two to three years away. For a drug targeting a relatively rare indication, the peak revenue ceiling, while lucrative, is bounded. Analysts covering the CML market typically model mature annual sales for a best-in-class next-generation allosteric inhibitor in the $2–4 billion range globally, depending on label breadth and first-line expansion.

At $6 billion all-cash, Merck is effectively paying two to three times peak sales estimates upfront — aggressive, but not irrational when the acquirer is running a multi-decade oncology platform and values de-risked, validated science over raw market speculation.

The deal also reflects Terns’ strategic leverage. Terns had cash runway into 2028 focused on advancing the CML program internally and partnering metabolic assets Ternspharma — meaning the company was not under existential financial pressure to sell. That negotiating position, combined with competitive interest from other potential suitors, likely shaped the final price.

The Broader Strategic Picture: Merck’s New Oncology Architecture

The Terns acquisition, viewed in isolation, reads as a sensible pipeline bolt-on. Viewed in the context of Merck’s full strategic reshaping, it takes on a different quality — the latest piece in what is becoming one of the most ambitious pharma rebuilding exercises since the post-Lipitor era.

Consider the deal sequencing. Merck’s $11.5 billion deal for Acceleron Pharmaceuticals added the pulmonary arterial hypertension therapy Winrevair; the Verona Pharma acquisition brought Ohtuvayre, a first-in-class COPD treatment; and the Cidara deal added CD388, a long-acting antiviral against all flu strains. Invezz Each transaction has shared a common logic: early enough in commercial life to offer genuine upside, but far enough along in clinical development to substantially de-risk.

TERN-701 fits that template — though the clinical-stage risk is somewhat higher than in those prior deals. What elevates the strategic rationale is the oncology division context. As part of the restructuring, Merck’s human-health business will be split into two — one housing its oncology portfolio and the other including all of its non-cancer medicines. U.S. News & World Report Citi analysts said the split would help to more clearly distinguish Merck’s mature oncology portfolio from its newer, acquisition-driven assets. U.S. News & World Report

Adding a potentially best-in-class CML asset directly strengthens the new oncology unit’s pipeline depth — a consideration that matters not only commercially, but also in how investors and potential partners value the separated entity. If Merck eventually pursues a spin-off or strategic transaction involving the oncology division, a richer pipeline commands a materially higher multiple.

There is also the question of platform. BCR-ABL inhibition in CML has historically served as a scientific and regulatory template for targeted therapies in adjacent hematological malignancies. If TERN-701’s allosteric mechanism proves transferable — to blast phase CML, to Philadelphia chromosome-positive ALL, or to other BCR-ABL-driven contexts — the addressable market expands substantially beyond the initial rare indication.

What It Means for Patients: Access, Pricing, and the CML Treatment Gap

Abstract strategy and valuation calculus exist in tension with a more human question: what does this deal mean for the roughly 30,000 Americans — and hundreds of thousands globally — currently living with CML?

On balance, consolidation under a well-capitalized major pharma is likely to accelerate the path to approval. Merck’s regulatory infrastructure, commercial relationships, and Phase 3 execution capability represent genuine accelerants for a drug that Terns, as a clinical-stage company, would have struggled to advance at comparable speed. The CARDINAL trial needs to expand into a full pivotal program; a major pharma’s resources materially compress that timeline.

The pricing question is less comfortable. Tyrosine kinase inhibitors for CML are already among the most expensive chronic disease therapies in the U.S. market. Novartis’s asciminib lists at over $200,000 annually. Should TERN-701 achieve approval — and the Phase 1 data suggests it is on track to try — it will enter a market where Merck will be under both commercial pressure to recoup its $6 billion investment and political pressure to justify the cost of a rare disease therapy.

The international access picture is sharper still. Keytruda may face “price setting” from the Inflation Reduction Act in 2026 C&EN, and the broader U.S.-China oncology R&D race is intensifying as Chinese biotechs, many partnered with or competing directly against Western majors, rapidly advance their own BCR-ABL and kinase inhibitor portfolios. A Merck-owned TERN-701 will need a global commercialization strategy that balances pricing sustainability in the U.S. against access in markets where affordability remains the defining constraint.

The 2026 M&A Wave: Terns as Precedent, Not Outlier

Industry-watchers have spent the past 18 months watching the pharma M&A pipeline with unusual intensity, and the Terns deal — if it closes — will not be the last deal of this kind in 2026. The conditions for a sustained acquisition wave remain firmly in place.

Patent cliffs are not unique to Merck. AstraZeneca, Bristol-Myers Squibb, and Pfizer all face meaningful revenue transitions in the latter half of the decade. Interest rates, while elevated versus the zero-rate era, remain manageable for investment-grade acquirers with strong cash generation. Biotech valuations, while partially recovered from the 2022–2023 trough, have not returned to the frothy heights that previously priced out strategic acquirers. That creates a window — perhaps 18 to 36 months — in which well-capitalized majors can acquire genuine clinical-stage innovation at multiples that may look cheap in retrospect.

The calculus changes if clinical-stage failures mount, or if the regulatory environment shifts adversely for rare oncology indications. But for now, the structural incentives point toward more deals, not fewer. Merck CEO Robert Davis said as much in February: “Our belief in our ability to have substantial growth once we get closer to the [loss of exclusivity] is as high as it’s ever been. And we’re not done.” Fierce Pharma

The Terns deal, at $6 billion, is arguably modest by the ambitions of that statement — a targeted bet on a validated mechanism in a well-understood disease, dressed in the clinical data that Big Pharma acquirers find most legible. What comes next in Merck’s dealmaking could be considerably larger.

Forward Scenarios: Three Possible Outcomes for TERN-701

Scenario 1 — Accelerated Approval Pathway: If TERN-701’s Phase 1 data is persuasive enough for Breakthrough Therapy Designation (which Terns has not yet obtained), Merck could potentially pursue an accelerated approval pathway using MMR as a surrogate endpoint — a strategy previously used for asciminib. A 2028–2029 approval timeline is not implausible. In this scenario, the deal looks like sharp value creation.

Scenario 2 — Pivotal Trial Success, Standard Path: The more likely route involves a full Phase 3 randomized controlled trial, standard FDA review, and approval in the early 2030s. In this scenario, TERN-701 becomes a useful but not transformative contributor to Merck’s oncology revenue — meaningful for patients, positive but not game-changing for Merck’s post-Keytruda financials.

Scenario 3 — First-Line Expansion: The real prize — the scenario that would vindicate the $6 billion price tag in full — is if TERN-701 demonstrates superiority or equivalence to standard-of-care in earlier lines of CML therapy. A first- or second-line label would multiply the addressable patient population by an order of magnitude, transforming a rare disease asset into a genuine oncology pillar.

The Bottom Line

The Merck–Terns deal is not, by the standards of 2025–2026 Big Pharma dealmaking, extraordinary in size. What makes it significant is its specificity. Merck is not buying a diversified biotech platform or hedging its bets across a sprawling pipeline. It is making a concentrated, scientifically defensible wager on one drug, one mechanism, and one disease — a bet that a next-generation allosteric BCR-ABL inhibitor with 80% major molecular response rates in heavily pre-treated patients represents exactly the kind of targeted, data-driven oncology innovation that commands a premium in any market cycle.

Whether TERN-701 ultimately delivers on its early clinical promise remains genuinely uncertain. Phase 1 data, however spectacular, does not guarantee Phase 3 success. Regulatory hurdles, competitive pressure from asciminib and emerging Chinese generics, and the perennial challenges of rare disease commercialization will all shape the eventual story.

But for the patients cycling through failed CML therapies — people who have exhausted three, four, even six prior tyrosine kinase inhibitors — the prospect of a new mechanism with a favorable safety profile and compelling molecular response rates is not a valuation abstraction. It is the news they have been waiting for.

Merck is betting $6 billion on the proposition that those patients deserve a better option. That, at its core, is the deal.

Key Deal Facts at a Glance

- Deal Value: ~$6 billion, all-cash

- Target: Terns Pharmaceuticals (NASDAQ: TERN), Foster City, CA

- Lead Asset: TERN-701 — oral, allosteric BCR-ABL inhibitor for relapsed/refractory CML

- Clinical Stage: Phase 1 CARDINAL trial (dose expansion ongoing)

- Key Clinical Data: 80% MMR rate at ≥320mg dose, 0 dose-limiting toxicities

- Terns Market Cap Pre-Deal: ~$5.3 billion

- Merck’s M&A Spend Since 2024: $25+ billion (Verona Pharma, Cidara, Terns)

- Keytruda Annual Revenue: ~$30 billion; LOE expected 2028

- Deal Status: Advanced negotiations; expected to close within days

Sources: Financial Times, Reuters, Fierce Pharma, Terns Pharmaceuticals IR, ASH 2025 oral presentation (Blood, 2025;146:901), OncLive, Seeking Alpha, STAT News

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance3 months ago

Markets & Finance3 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis2 months ago

Analysis2 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks2 months ago

Banks2 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment2 months ago

Investment2 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Asia3 months ago

Asia3 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Analysis1 month ago

Analysis1 month agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Global Economy3 months ago

Global Economy3 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy3 months ago

Global Economy3 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis