Opinion

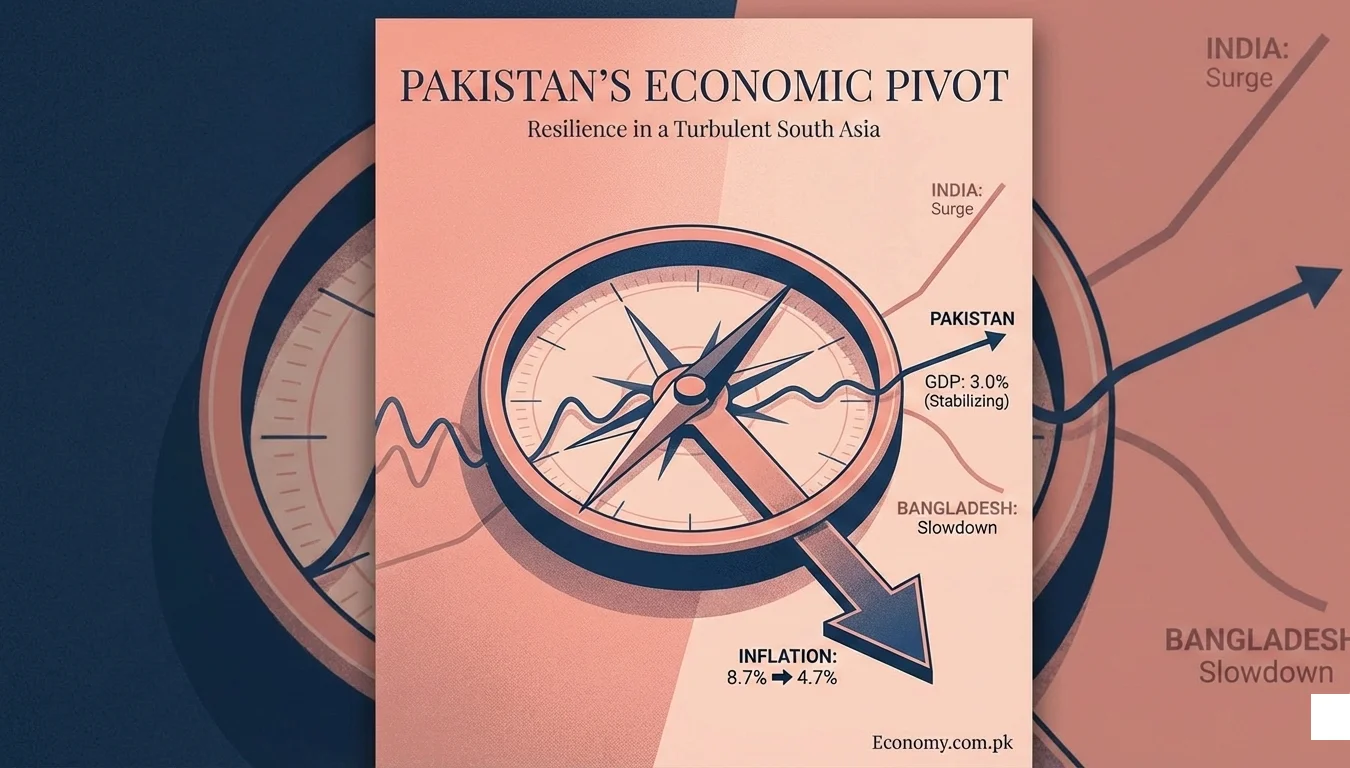

Pakistan’s Economic Pivot: Finding Resilience in a Turbulent South Asia

The narrative surrounding South Asia’s economy has long been dominated by singular giants, but the tides are shifting. For years, the headlines have focused solely on high-speed growth or deepening crises. However, the latest data released by the Asian Development Bank (ADB) in its December 2025 Asian Development Outlook (ADO) paints a far more nuanced picture—one of divergence, realignment, and for Pakistan, a critical moment of stabilization.

While the region as a whole is projected to grow at a robust 6.5% in 2025, the internal dynamics are changing. As India continues its consumption-led surge and Bangladesh faces unexpected headwinds, Pakistan is quietly executing a pivot. The numbers suggest that despite political noise and the lingering scars of climate disasters, the Pakistani economy is showing signs of genuine resilience, offering a unique, albeit cautious, investment case for the fiscal year 2025-26.

The Pakistani Pivot: What the Numbers Really Mean

For investors and policymakers fatigued by volatility, the ADB’s latest upgrade is a breath of fresh air. The bank has revised Pakistan’s GDP growth forecast for FY2025 up to 3.0%, a significant improvement from the earlier estimate of 2.7%. This trajectory is expected to hold steady, with a sustained 3.0% forecast for FY2026.

At first glance, 3% might not seem like a headline-grabbing figure compared to historical highs. However, in the context of stabilization, it is monumental. It represents a floor—a foundational level of activity that proves the economy has absorbed the worst of the shocks.

Resilience in Action

The most telling data point, arguably, is not the annual forecast but the quarterly performance. Despite severe flood disruptions that threatened to derail agricultural output, Pakistan’s economy clocked a surprising 5.7% growth in Q4 FY2025. This figure is a testament to the adaptability of Pakistan’s private sector and the hard-won resilience of its agricultural base.

The Inflation Relief

Perhaps the most critical indicator for the common man and the business community is the dramatic cooling of prices. The ADB report highlights a sharp decline in inflation, averaging 4.7% in the first four months of FY2026 (July–October). This is a massive reprieve compared to the suffocating 8.7% recorded during the same period last year.

For the Pakistan Economic Outlook 2025, this drop in inflation is the game-changer. It signals that monetary tightening has worked, supply chains are normalizing, and the central bank may soon have the room to pivot toward pro-growth policies, potentially lowering borrowing costs for the private sector.

The Regional Race: A Comparative Analysis

To understand Pakistan’s position, we must look at the neighborhood. The South Asia Economic Trends revealed in the ADO report show three distinct economic stories unfolding simultaneously.

India: The Consumption Engine

India remains the regional outlier in terms of sheer velocity. The ADB has upgraded India’s growth forecast to 7.2% for 2025, driven largely by robust domestic consumption. India is currently in an expansion phase, leveraging its massive internal market to buffer against global slowdowns. For Pakistan, India serves as a benchmark for what is possible when political stability meets consistent policy frameworks.

Bangladesh: The Unexpected Slowdown

The sharper contrast, however, lies to the east. Bangladesh, often touted as the “miracle” economy, is facing significant friction. The ADB has cut Bangladesh’s growth forecast to 4.7% (down from 5.1%). This deceleration is attributed to export weakness—particularly in the readymade garment sector—and rising political uncertainty.

“Stabilization is not the destination; it is merely the platform. A 3% growth rate keeps the lights on, but it does not employ the millions of youth entering the workforce.“

Pakistan vs India Economy comparisons are common, but the comparison with Bangladesh is currently more relevant. As Bangladesh struggles with export dips and structural adjustments, Pakistan has an opportunity to regain lost ground. The narrative that Pakistan is the “sick man” of South Asia is being challenged by data that shows Pakistan stabilizing while competitors stumble.

Opinion: Turning Stabilization into Acceleration

As the Lead Editor of Economy.com.pk, I view these numbers with “cautious optimism.” Stabilization is not the destination; it is merely the platform. A 3% growth rate keeps the lights on, but it does not employ the millions of youth entering the workforce annually.

To turn this ADB GDP Forecast for Pakistan into a sustained trajectory of 5-6% growth, three things must happen:

- Capitalize on Regional Weakness: With Bangladesh’s export engine sputtering, Pakistan’s textile and manufacturing sectors must aggressively court international buyers looking to diversify supply chains. The stabilization of the Rupee and lower inflation provide the perfect window for this.

- Climate-Proofing is Economic Policy: The 5.7% growth in Q4 FY2025 occurred despite floods. Imagine the potential if our infrastructure was resilient. Investment in climate-smart agriculture is no longer a “green” luxury; it is a hard economic necessity.

- Political Continuity: The data shows that the economy responds to stability. The current recovery is fragile. Any return to chaotic populism could spook the very investors now taking a second look at Pakistani assets.

Conclusion

The data from the Asian Development Bank confirms what analysts on the ground have suspected: the storm is passing. While India sprints and Bangladesh catches its breath, Pakistan is standing firm.

With GDP growth revised upward to 3.0%, inflation nearly halved to 4.7%, and a private sector showing remarkable grit in Q4, the indicators for FY2026 are flashing green. The road ahead requires discipline, but for the first time in years, the economic map of South Asia shows Pakistan not as a crisis point, but as a recovering contender.

**

Disclaimer: This analysis is based on the latest Asian Development Outlook (ADO) data. Investors are advised to conduct their own due diligence.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The machines are already choosing who dies. The question is whether humanity will choose to stop them.

In the early weeks of Israel’s military campaign in Gaza, a targeting system called Lavender quietly changed the nature of modern warfare. The Israeli army marked tens of thousands of Gazans as suspects for assassination using an AI targeting system with limited human oversight and a permissive policy for civilian casualties. +972 Magazine Israeli intelligence officials acknowledged an error rate of around 10 percent — but simply priced it in, deeming 15 to 20 civilian deaths acceptable for every junior militant the algorithm identified, and over 100 for commanders. CIVICUS LENS The machine, according to one Israeli intelligence officer cited in the original +972 Magazine investigation, “did it coldly.”

This is not a hypothetical future threat. This is 2026. And this is why global AI regulation under the United Nations — a binding, enforceable, internationally backed governance platform — is no longer a matter of philosophical debate. It is the defining policy emergency of our era.

Why the Global AI Regulation UN Framework Is the Most Urgent Issue of 2026

When historians eventually write the account of humanity’s encounter with artificial intelligence, they will mark 2026 as the year the world stood at the threshold and hesitated. UN Secretary-General António Guterres affirmed in early February 2026: “AI is moving at the speed of light. No country can see the full picture alone. We need shared understandings to build effective guardrails, unlock innovation for the common good, and foster cooperation.” United Nations Foundation

That statement, measured and diplomatic in tone, barely captures the urgency on the ground. From the rubble of Gaza to the drone corridors above eastern Ukraine, algorithmic warfare has become normalized with terrifying speed. The Future of Life Institute now tracks approximately 200 autonomous weapons systems deployed across Ukraine, the Middle East, and Africa Globaleducationnews — the majority operating in legal and regulatory voids that no international treaty has yet filled.

Meanwhile, the governance architecture intended to respond to this moment remains fragile and fragmented. Just seven countries — all from the developed world — are parties to all current significant global AI governance initiatives, according to the UN. World Economic Forum A full 118 member states have no meaningful seat at the table where the rules of AI are being written. This is not merely inequitable; it is dangerous. The technologies being deployed against human populations are outrunning the institutions designed to constrain them.

The Lethal Reality: AI Warfare and Human Safety in the Middle East

The Gaza conflict has provided the world its most documented and disturbing window into what AI warfare looks like when accountability is stripped away. Israel’s AI tools include the Gospel, which automatically reviews surveillance data to recommend bombing targets, and Lavender, an AI-powered database that listed tens of thousands of Palestinian men linked by algorithm to Hamas or Palestinian Islamic Jihad. Wikipedia Critics across the spectrum of international law have argued that the use of these systems blurs accountability and results in disproportionate violence in violation of international humanitarian law.

Evidence recorded in the classified Israeli military database in May 2025 revealed that only 17% of the 53,000 Palestinians killed in Gaza were combatants — implying that 83% were civilians. Action on Armed Violence That figure, if accurate, represents one of the highest civilian death rates in modern recorded warfare, and it emerges directly from the logic of algorithmic targeting: speed over deliberation, efficiency over ethics, statistical probability over the irreducible humanity of each individual life.

Many operators trusted Lavender so much that they approved its targets without checking them SETA — a collapse of human oversight so complete that it renders the phrase “human-in-the-loop” meaningless in practice. UN Secretary-General Guterres stated that he was “deeply troubled” by reports of AI use in Gaza, warning that the practice puts civilians at risk and fundamentally blurs accountability.

This is not an isolated case study. Contemporary conflicts — from Gaza, Sudan and Ukraine — have become “testing grounds” for the military use of new technologies. United Nations Slovenia’s President Nataša Pirc Musar, addressing the UN Security Council, put it with stark clarity: “Algorithms, armed drones and robots created by humans have no conscience. We cannot appeal to their mercy.”

The Accountability Void: Who Is Responsible When an Algorithm Kills?

The legal and moral vacuum at the center of AI warfare is not accidental — it is structural. Although autonomous weapons systems are making life-or-death decisions in conflicts without human intervention, no specific treaty regulates these new weapons. TRENDS Research & Advisory The foundational principles of international humanitarian law — distinction between combatants and civilians, proportionality, and precaution — were designed for human actors capable of judgment, hesitation, and moral reckoning. They were not designed for systems that process kill decisions in milliseconds.

Both international humanitarian law and international criminal law emphasize that serious violations must be punished to fulfil their purpose of deterrence. A “criminal responsibility gap” caused by AI would mean impunity for war crimes committed with the aid of advanced technology. Action on Armed Violence This is the nightmare scenario that legal scholars from Human Rights Watch to the International Committee of the Red Cross now warn about openly: not only that AI enables atrocities, but that it systematically destroys the chain of accountability that makes justice possible after them.

A 2019 Turkish Bayraktar drone strike in Libya created precisely this precedent: UN investigators could not determine whether the operator, manufacturer, or foreign advisors bore ultimate responsibility. TRENDS Research & Advisory That ambiguity, multiplied by the speed and scale of contemporary AI systems, represents an existential challenge to the international legal order.

The question “who is responsible when an algorithm kills?” cannot be answered under the current framework. And that is precisely why the current framework must be replaced.

The UN’s New Architecture: Promising, But Dangerously Insufficient

There are genuine signs that the international community understands what is at stake. The Global Dialogue on AI Governance will provide an inclusive platform within the United Nations for states and stakeholders to discuss the critical issues concerning AI facing humanity, with the Scientific Panel on AI serving as a bridge between cutting-edge AI research and policymaking — presenting annual reports at sessions in Geneva in July 2026 and New York in 2027. United Nations

The CCW Group of Experts’ rolling text from November 2024 outlines potential regulatory measures for lethal autonomous weapons systems, including ensuring they are predictable, reliable, and explainable; maintaining human oversight in morally significant decisions; restricting target types and operational scope; and enabling human operators to deactivate systems after activation. ASIL

Yet the gulf between these principles and enforceable reality remains vast. In November 2025, the UN General Assembly’s First Committee passed a historic resolution calling to negotiate a legally enforceable LAWS agreement by 2026 — 156 nations supported it overwhelmingly. Only five nations strictly rejected the resolution, notably the United States and Russia. Usanas Foundation Their resistance sends a signal that is impossible to misread: the two largest military AI developers on earth are actively resisting the international constraints that the rest of the world is demanding.

By the end of 2026, the Global Dialogue will likely have made AI governance global in form but geopolitical in substance — a first test of whether international cooperation can meaningfully shape the future of AI or merely coexist alongside competing national strategies. Atlantic Council That assessment, from the Atlantic Council’s January 2026 analysis, should be understood as a warning, not a prediction to be accepted passively.

The Case for an IAEA-Style UN AI Governance Body

The most compelling model for meaningful global AI regulation under the UN has been circulating in serious policy circles for several years, and in February 2026 it gained its most prominent corporate advocate. At the international AI Impact Summit 2026 in New Delhi, OpenAI CEO Sam Altman called for a radical new format for global regulation of artificial intelligence — modeled after the International Atomic Energy Agency — arguing that “democratizing AI is the only fair and safe way forward, because centralizing technology in one company or country can have disastrous consequences.” Logos-pres

The IAEA analogy is instructive precisely because it addresses the core failure of current approaches: the absence of verification, inspection, and enforcement. An IAEA-like agency for AI could develop industry-wide safety standards and monitor stakeholders to assess whether those standards are being met — similar to how the IAEA monitors the distribution and use of uranium, conducting inspections to help ensure that non-nuclear weapon states don’t develop nuclear weapons. Lawfare

This proposal has been echoed and refined by researchers published in Nature, who draw a direct parallel: the IAEA’s standardized safety standards-setting approach and emergency response system offer valuable lessons for establishing AI safety regulations, with standardized safety standards providing a fundamental framework to ensure the stability and transparency of AI systems. Nature

Skeptics argue, with some justification, that achieving this level of cooperation in the current geopolitical climate is extraordinarily difficult. But consider the alternative. The 2026 deadline is increasingly seen as the “finish line” for global diplomacy; if a treaty is not reached, the speed of innovation in military AI driven by the very powers currently blocking the UN’s progress will likely make any future regulation obsolete before the ink is even dry. Usanas Foundation We are, in the language of arms control analysts, in the “pre-proliferation window” — the last viable moment before these systems become as ubiquitous and ungovernable as small arms.

EU AI Act Enforcement and the Patchwork Problem

The European Union has moved further than any other jurisdiction toward binding regulation. By 2026, the EU AI Act is partially in force, with obligations for general-purpose AI and prohibited AI practices already applying, and high-risk AI systems facing requirements for pre-deployment assessments, extensive documentation, post-market monitoring, and incident reporting. OneTrust This is meaningful progress. It is also deeply insufficient as a global solution.

According to Gartner, by 2030, fragmented AI regulation will quadruple and extend to 75% of the world’s economies — but organizations that have deployed AI governance platforms are currently 3.4 times more likely to achieve high effectiveness in AI governance than those that do not. Gartner That statistic reveals both the potential of structured governance and the cost of its absence.

The EU’s rules, however rigorous, apply within EU member states and to companies seeking EU market access. They do not reach the drone manufacturers of Turkey, the autonomous targeting systems of Israel, the Replicator program of the United States Pentagon, or the algorithmic weapons being developed at pace in Beijing. The International AI Safety Report 2026 notes that reliable pre-deployment safety testing has become harder to conduct, and it has become more common for models to distinguish between test settings and real-world deployment — meaning dangerous capabilities could go undetected before deployment. Internationalaisafetyreport In a military context, undetected dangerous capabilities do not result in regulatory fines. They result in mass civilian casualties.

Comprehensive global AI regulation under the United Nations must transcend this patchwork. The model cannot be voluntary principles and national strategies stitched together by hope. It must be treaty-based, inspection-backed, and enforceable — with particular urgency around military applications.

The Policy Architecture the World Needs

The outline of what a viable global AI regulation UN platform would require is not, in fact, mysterious. The intellectual groundwork has been laid. What is missing is political will, specifically from the three states — the United States, Russia, and China — whose cooperation is structurally indispensable.

A credible architecture would include, at minimum:

- A binding treaty on lethal autonomous weapons systems, prohibiting systems that cannot be used in compliance with international humanitarian law and mandating meaningful human oversight for all others. The UN Secretary-General has maintained since 2018 that lethal autonomous weapons systems are politically unacceptable and morally repugnant, reiterating in his New Agenda for Peace the call to conclude a legally binding instrument by 2026. UNODA

- An Independent International AI Agency modeled on the IAEA, with authority to develop safety standards, conduct inspections of frontier AI systems, and verify compliance — particularly for dual-use applications with military potential.

- Universal inclusion of the Global South, whose populations bear a disproportionate share of the consequences of algorithmic warfare and AI-enabled surveillance, yet remain largely absent from the forums where the rules are being written. Many countries of the Global South are notably absent from the UN’s experts group on autonomous weapons, despite the inevitable future global impact of these systems once they become cheap and accessible. Arms Control Association

- A standing accountability mechanism for AI-related violations of international humanitarian law, closing the “responsibility gap” that currently allows commanders to deflect culpability onto algorithms.

- Real-time AI risk monitoring and reporting, with annual assessments presented to the UN General Assembly — building on the model of the Independent International Scientific Panel on AI already authorized for its first report in Geneva in July 2026.

None of this is technically impossible. The scientific consensus exists. The legal frameworks are available. The moral case is overwhelming.

Conclusion: Global AI Regulation UN 2026 — The Last Clear Moment

The Greek Prime Minister, speaking at the UN Security Council’s open debate on AI, made a comparison that deserves to reverberate through every foreign ministry and defense establishment on earth: the world must rise to govern AI “as it once did for nuclear weapons and peacekeeping.” He warned that “malign actors are racing ahead in developing military AI capabilities” and urged the Council to rise to the occasion. United Nations

Humanity’s fate, as the UN Secretary-General has said plainly, cannot be left to an algorithm. But neither can it be left to voluntary declarations, aspirational principles, and annual dialogues that produce no binding obligation. The deadly deployment of AI in active conflicts has already raised existential concerns for human safety that cannot be wished away by appeals to innovation or national security prerogative.

The architecture for a genuine global AI regulation UN platform exists in skeletal form. The Geneva Dialogue, the Scientific Panel, the LAWS treaty negotiations — these are the bones of something that could actually work. What they require now is not more deliberation. They require the political courage of the world’s most powerful states to subordinate short-term strategic advantage to the longer-term survival of the rules-based international order — and, more fundamentally, to the survival of human dignity in the age of the algorithm.

The pre-proliferation window is closing. 2026 is not a deadline to be managed. It is a moral threshold to be met.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Iran conflict has turned frontier AI models into contested weapons of state — and the financial and human fallout is only beginning to register.

In the first eleven days of the U.S.-Israeli offensive against Iran, which began on February 28, 2026, American and Israeli forces executed roughly 5,500 strikes on Iranian targets. That is an operational tempo that would have required months in any previous conflict — made possible, in significant part, by artificial intelligence. In the first eleven days of the conflict, America achieved an astonishing 5,500 strikes, using AI on a large-scale battlefield for the first time at this scale. The National The same week those bombs fell, a legal and commercial crisis erupted in Silicon Valley with consequences that will define the AI industry for years. Both events are part of the same story.

We are living through the moment when AI ceased being a future-war thought experiment and became an operational reality — embedded in targeting pipelines, shaping intelligence assessments, and now at the center of a constitutional showdown between a frontier AI company and the United States government. Alfred Nobel, who invented dynamite and then spent the remainder of his life in tortured ambivalence about it, would have recognized the pattern immediately.

The Kill Chain, Accelerated

The joint U.S. and Israeli offensive on Iran revealed how algorithm-based targeting and data-driven intelligence are reforming the mechanics of warfare. In the first twelve hours alone, U.S. and Israeli forces reportedly carried out nearly 900 strikes on Iranian targets — an operational tempo that would have taken days or even weeks in earlier conflicts. Interesting Engineering

At the technological center of this acceleration sits a system most Americans have never heard of: Project Maven. Anthropic’s Claude has become a crucial component of Palantir’s Maven intelligence analysis program, which was also used in the U.S. operation to capture Venezuelan President Nicolás Maduro. Claude is used to help military analysts sort through intelligence and does not directly provide targeting advice, according to a person with knowledge of Anthropic’s work with the Defense Department. NBC News This is a distinction with genuine moral weight — between decision-support and decision-making — but one that is becoming harder to sustain at the speed at which modern targeting now operates.

Critics warn that this trend could compress decision timelines to levels where human judgment is marginalized, ushering in an era of warfare conducted at what has been described as “faster than the speed of thought.” This shortening interval raises fears that human experts may end up merely approving recommendations generated by algorithms. In an environment dictated by speed and automation, the space for hesitation, dissent, or moral restraint may be shrinking just as quickly. Interesting Engineering

The U.S. military’s posture has been notably sanguine about these concerns. Admiral Brad Cooper, head of U.S. Central Command, confirmed that AI is helping soldiers process troves of data, stressing that humans make final targeting decisions — but critics note the gap between that principle and verifiable practice remains wide. Al Jazeera

The Financial Architecture of AI Warfare

The economic dimensions of this transformation are substantial and largely unreported in their full complexity. Understanding them requires holding three separate financial narratives simultaneously.

The direct contract market is the most visible layer. Over the past year, the U.S. Department of Defense signed agreements worth up to $200 million each with several major AI companies, including Anthropic, OpenAI, and Google. CNBC These are not trivial sums in isolation, but they represent the seed capital of a much larger transformation. The military AI market is projected to reach $28.67 billion by 2030, as the speed of military decision-making begins to surpass human cognitive capacity. Emirates 24|7

The collateral economic disruption is less discussed but potentially far larger. On March 1, Iranian drone strikes took out three Amazon Web Services facilities in the Middle East — two in the UAE and one in Bahrain — in what appear to be the first publicly confirmed military attacks on a hyperscale cloud provider. The strikes devastated cloud availability across the region, affecting banks, online payment platforms, and ride-hailing services, with some effects felt by AWS users worldwide. The Motley Fool The IRGC cited the data centers’ support for U.S. military and intelligence networks as justification. This represents a strategic escalation that no risk-management framework in the technology sector adequately anticipated: cloud infrastructure as a legitimate military target.

The reputational and legal costs of AI’s battlefield role may ultimately dwarf both. Anthropic’s court filings stated that the Pentagon’s supply-chain designation could cut the company’s 2026 revenue by several billion dollars and harm its reputation with enterprise clients. A single partner with a multi-million-dollar contract has already switched from Claude to a competing system, eliminating a potential revenue pipeline worth more than $100 million. Negotiations with financial institutions worth approximately $180 million combined have also been disrupted. Itp

The Anthropic-Pentagon Fracture: A Defining Test

The dispute between Anthropic and the U.S. Department of Defense is not merely a contract negotiation gone wrong. It is the first high-profile case in which a frontier AI company drew a public ethical line — and then watched the government attempt to destroy it for doing so.

The sequence of events is now well-documented. The administration’s decisions capped an acrimonious dispute over whether Anthropic could prohibit its tools from being used in mass surveillance of American citizens or to power autonomous weapon systems, as part of a military contract worth up to $200 million. Anthropic said it had tried in good faith to reach an agreement, making clear it supported all lawful uses of AI for national security aside from two narrow exceptions. NPR

When Anthropic held its position, the response was unprecedented in the annals of U.S. technology policy. Defense Secretary Pete Hegseth declared Anthropic a supply chain risk in a statement so broad that it can only be seen as a power play aimed at destroying the company. Shortly thereafter, OpenAI announced it had reached its own deal with the Pentagon, claiming it had secured all the safety terms that Anthropic sought, plus additional guardrails. Council on Foreign Relations

In an extraordinary move, the Pentagon designated Anthropic a supply chain risk — a label historically only applied to foreign adversaries. The designation would require defense vendors and contractors to certify that they don’t use the company’s models in their work with the Pentagon. CNBC That this was applied to a U.S.-headquartered company, founded by former employees of a U.S. nonprofit, and valued at $380 billion, represents a remarkable inversion of the logic the designation was designed to serve.

Meanwhile, Washington was attacking an American frontier AI leader while Chinese labs were on a tear. In the past month alone, five major Chinese models dropped: Alibaba’s Qwen 3.5, Zhipu AI’s GLM-5, MiniMax’s M2.5, ByteDance’s Doubao 2.0, and Moonshot’s Kimi K2.5. Council on Foreign Relations The geopolitical irony is not subtle: in punishing a safety-focused American AI company, the administration may have handed Beijing its most useful competitive gift of the year.

The Human Cost: Social Ramifications No Algorithm Can Compute

Against the financial ledger, the humanitarian accounting is staggering and still incomplete.

The Iranian Red Crescent Society reported that the U.S.-Israeli bombardment campaign damaged nearly 20,000 civilian buildings and 77 healthcare facilities. Strikes also hit oil depots, several street markets, sports venues, schools, and a water desalination plant, according to Iranian officials. Al Jazeera

The case that has attracted the most scrutiny is the bombing of the Shajareh Tayyebeh elementary school in Minab, southern Iran. A strike on the school in the early hours of February 28 killed more than 170 people, most of them children. More than 120 Democratic members of Congress wrote to Defense Secretary Hegseth demanding answers, citing preliminary findings that outdated intelligence may have been to blame for selecting the target. NBC News

The potential connection to AI decision-support systems is explored with forensic precision by experts at the Bulletin of the Atomic Scientists. One analysis notes that the mistargeting could have stemmed from an AI system with access to old intelligence — satellite data that predated the conversion of an IRGC compound into an active school — and that such temporal reasoning failures are a known weakness of large language models. Even with humans nominally “in the loop,” people frequently defer to algorithmic outputs without careful independent examination. Bulletin of the Atomic Scientists

The social fallout extends well beyond individual atrocities. Israel’s Lavender AI-powered database, used to analyze surveillance data and identify potential targets in Gaza, was wrong at least 10 percent of the time, resulting in thousands of civilian casualties. A recent study found that AI models from OpenAI, Anthropic, and Google opted to use nuclear weapons in simulated war games in 95 percent of cases. Rest of World The simulation result does not predict real-world behavior, but it reveals how strategic reasoning models can default toward extreme outcomes under pressure — a finding that ought to unsettle anyone who imagines that algorithmic warfare is inherently more precise than the human kind.

The corrosion of accountability is perhaps the most insidious long-term social effect. “There is no evidence that AI lowers civilian deaths or wrongful targeting decisions — and it may be that the opposite is true,” says Craig Jones, a political geographer at Newcastle University who researches military targeting. Nature Yet the speed and opacity of AI-assisted operations makes it exponentially harder to assign responsibility when things go wrong. Algorithms do not face courts-martial.

Governance: The International Gap

Rapid technological development is outpacing slow international discussions. Academics and legal experts meeting in Geneva in March 2026 to discuss lethal autonomous weapons systems found themselves studying a technology already being used at scale in active conflicts. Nature The gap between the pace of deployment and the pace of governance has never been wider.

The Middle East and North Africa are arguably the most conflict-ridden and militarized regions in the world, with four out of eleven “extreme conflicts” identified in 2024 by the Armed Conflict Location and Event Data organization occurring there. The region has become a testing ground for AI warfare whose lessons — and whose errors — will shape every future conflict. War on the Rocks

The legal framework governing AI in warfare remains, generously described, aspirational. The U.S. military’s stated commitment to keeping “humans in the loop” is a principle that has no internationally binding enforcement mechanism, no agreed definition of what meaningful human control actually entails, and no independent auditing process. One expert observed that the biggest danger with AI is when humans treat it as an all-purpose solution rather than something that can speed up specific processes — and that this habit of over-reliance is particularly lethal in a military context. The National

AI as the New Dynamite: Nobel’s Unresolved Legacy

When Alfred Nobel invented dynamite in 1867, he believed — genuinely — that a weapon so devastatingly efficient would make war unthinkably costly and therefore rare. He was catastrophically wrong. The Franco-Prussian War, the First World War, and the entire industrial-era atrocity that followed proved that more powerful weapons do not deter wars; they escalate them, and they increase civilian mortality relative to combatant casualties.

The parallel to AI is not decorative. The argument for AI in warfare — that algorithmic precision reduces collateral damage, that faster targeting shortens conflicts, that autonomous systems absorb military risk that would otherwise fall on human soldiers — is structurally identical to Nobel’s argument for dynamite. It is the rationalization of a dual-use technology by those with an interest in its proliferation.

Drone technology in the Middle East has already shifted from manual control toward full autonomy, with “kamikaze” drones utilizing computer vision to strike targets independently if communications are severed. As AI becomes more integrated into militaries, the advancements will become even more pronounced with “unpredictable, risky, and lethal consequences,” according to Steve Feldstein, a senior fellow at the Carnegie Endowment for International Peace. Rest of World

The Anthropic dispute, whatever its ultimate legal resolution, has surfaced a question that Silicon Valley has been able to defer until now: can a technology company that builds frontier AI models — systems capable of synthesizing intelligence, generating targeting assessments, and running strategic simulations — genuinely control how those systems are used once deployed by a state? As OpenAI’s own FAQ acknowledged when asked what would happen if the government violated its contract terms: “As with any contract, we could terminate it.” The entire edifice of AI safety in warfare, for now, rests on the contractual leverage of companies that have already agreed to participate. Council on Foreign Relations

Nobel at least had the decency to endow prizes. The AI industry is still working out what it owes.

Policy Recommendations

A minimally adequate governance framework for AI in warfare would need to accomplish several things. Independent verification of “human in the loop” claims — not merely the assertion of it — is the essential starting point. Mandatory after-action reporting on AI involvement in any strike that results in civilian casualties would create accountability where none currently exists. International agreement on a baseline error-rate threshold — above which AI targeting systems may not be used without additional human review — would translate abstract humanitarian law into operational reality.

The technology companies themselves bear responsibility that no contract clause can fully discharge. Researchers from OpenAI, Google DeepMind, and other labs submitted a court filing supporting Anthropic’s position, arguing that restrictions on domestic surveillance and autonomous weapons are reasonable until stronger legal safeguards are established. ColombiaOne That the most capable AI builders in the world believe their own technology is not yet reliable enough for autonomous lethal use is information that should be at the center of every policy debate — not buried in court filings.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

On November 19, 2023, Houthi militants seized a Bahamian-flagged cargo ship in the Red Sea. That single act of piracy — framed as solidarity with Gaza — triggered the most consequential maritime disruption to global trade since the 2021 Ever Given blockage. Two and a half years later, the Strait of Bab el-Mandeb remains a war zone in all but name, the Suez Canal handles barely a fraction of its former traffic, and the economies of eighteen nations stretching from Sri Lanka to the Philippines are absorbing cascading shocks they did not generate and cannot fully control. This is the story of how a distant conflict has become a near-present economic emergency across ASEAN and SAARC — and what it means for growth, inflation, remittances, and supply chains through 2028.

The Red Sea in Numbers: A Chokepoint Under Siege

The statistics are staggering. According to UNCTAD’s 2025 Maritime Trade Review, tonnage through the Suez Canal stood 70 percent below 2023 levels as recently as May 2025 UNCTAD, and the trajectory of recovery remains deeply uncertain. Container shipping has been devastated: traffic through the canal collapsed by roughly 75 percent during 2024 compared with 2023 averages, with no meaningful recovery through mid-2025 — data from July 2025 showing no recovery in container vessel transit through the canal, and Houthi attacks as recently as August 2025 making recovery unlikely soon Project44. The Suez Canal’s share of global maritime traffic has slipped from roughly 12 percent to below 9 percent — a structural shift that may not fully reverse even if hostilities cease.

The rerouting of vessels around Africa’s Cape of Good Hope adds 10–14 days to Asia–Europe voyages, pushing total transit times to 40–50 days. Freight rates between Shanghai and Rotterdam surged fivefold in 2024 Yqn. Rates between Shanghai and Rotterdam remained significantly higher than before the attacks began — up 80 percent relative to pre-crisis levels as of 2025. Coface UNCTAD notes that ship ton-miles hit a record annual rise of 6 percent in 2024, nearly three times faster than underlying trade volume growth. By May 2025, the Strait of Hormuz — through which 11 percent of global trade and a third of seaborne oil pass — also faced disruption risks. UNCTAD

The Asian Development Bank’s July 2025 Outlook modelled three Middle East scenarios. In its most severe case — a protracted conflict with Strait of Hormuz disruption — oil prices could surge $55 per barrel for four consecutive quarters. Asian Development Bank The Strait of Hormuz, through which roughly one-third of all seaborne oil and over one-fifth of global LNG supply passes (the latter primarily from Qatar), is a chokepoint of existential importance to every oil-importing nation from Dhaka to Manila.

The Oil Shock Transmission: How Energy Costs Hit 18 Economies

For most of 2025, Brent crude had traded in the $60–$74/barrel range, offering breathing room to energy-hungry emerging economies. That calculus shifted dramatically in early 2026. With fresh military action involving the United States and Israel targeting Iran, Brent broke above $100/bbl — roughly 70 percent above its 2025 average of $68/bbl — according to OCBC Group Research. European gas (TTF) simultaneously pushed past €50/MWh. OCBC

MUFG Research sensitivity modelling shows that every $10/barrel increase in oil prices worsens Asia’s current account balance by 0.2–0.9 percent of GDP. Thailand is the region’s most exposed economy (current account impact: -0.9% of GDP per $10/bbl), followed by Singapore (-0.7%), South Korea (-0.6%), and the Philippines. Inflationary effects are equally asymmetric: a $10/bbl oil price rise pushes annual headline CPI up by 0.6–0.8 percentage points in Thailand, 0.5–0.7pp in India and the Philippines, and 0.4–0.6pp across Malaysia, Indonesia, and Vietnam. MUFG Research Countries with fuel subsidies — notably Indonesia and Malaysia — absorb part of the pass-through fiscally, but at escalating cost to their budgets.

ASEAN: The Differentiated Exposure

ASEAN nations face wildly varying degrees of vulnerability. The Philippines sources 96 percent of its oil from the Gulf, Vietnam and Thailand approximately 87 percent and 74 percent respectively, while Singapore is more than 70 percent dependent on Middle Eastern crude — with 45 percent of its LNG imports arriving from Qatar alone. The Diplomat

The ADB’s April 2025 Outlook cut Singapore’s 2025 growth forecast to 2.6 percent (from 4.4% in 2024), citing weaker exports driven by global trade uncertainties and weaker external demand. Asian Development Bank The IMF revised ASEAN-5 aggregate growth down further to 4.1 percent in July 2025, versus earlier forecasts of 4.6 percent, with trade-dependent Vietnam (revised to 5.2% in 2025), Thailand (2.8%), and Cambodia most acutely affected. Krungsri

SAARC: The Remittance Fault Line

For the eight SAARC economies, the crisis is doubly coercive: higher energy import bills on one side, threatened remittance flows on the other.

India illustrates the tension most sharply. The country consumes approximately 5.3–5.5 million barrels per day while producing barely 0.6 million domestically, making it nearly 85 percent import-dependent. Petroleum imports already account for 25–30 percent of India’s total import bill, and every $10 oil price increase adds $12–15 billion to the annual cost. IANS News Historically, such episodes have triggered rupee depreciations exceeding 10 percent.

The remittance dimension is equally alarming. India received a record $137 billion in remittances in 2024, retaining its position as the world’s largest recipient. United Nations The 9-million-strong Indian diaspora in Gulf countries contributes nearly 38 percent of India’s total remittance inflows — roughly $51.4 billion from the GCC alone, based on FY2025 inflows of $135.4 billion. These workers are concentrated in oil services, construction, hospitality and retail: precisely the sectors most vulnerable to Gulf economic disruption. Oxford Economics estimates a sustained shock “would worsen India’s external position and could put some pressure on the rupee.” CNBC

Pakistan: Caught in the Crossfire

Pakistan’s total petroleum import bill reached approximately $10.7 billion in FY25, with crude petroleum imports of over $5.7 billion sourced predominantly from Saudi Arabia and the UAE. Its trade deficit has widened to approximately $25 billion during July–February FY26. Domestic fuel prices have already risen by approximately Rs55 ($0.20) per litre, reflecting the war-risk premium embedded in global crude markets. Profit by Pakistan Today

The remittance channel is equally fragile. Pakistan received $34.6 billion in remittances in 2024 — accounting for 9.4 percent of GDP — with Saudi Arabia alone contributing $7.4 billion (25 percent of the total), and the UAE contributing $5.5 billion (18.7 percent). Displacement Tracking Matrix An Insight Securities research note from March 2026 warns that geopolitical tensions involving the US, Israel, and Iran “have taken a hit on the security and stability perception” of Gulf economies, with the effect on Pakistani remittances expected to materialise with a lag. About 55 percent of Pakistan’s remittance inflows come from the Middle East, making the country particularly vulnerable. Arab News PK

For Pakistani exporters, shipping diversions around the Cape of Good Hope are extending transit times to Europe by 15–20 days, while freight rates on key routes could rise by up to 300 percent under war-risk classification. Profit by Pakistan Today

Bangladesh and Sri Lanka: Garments, Tea, and the Weight of Distance

Bangladesh’s vulnerability is concentrated in one devastating statistic: more than 65 percent of its garment exports — representing roughly $47 billion of an approximately $55 billion annual export economy — pass through or proximate to the Red Sea corridor. LinkedIn When Maersk confirmed on March 3, 2026, that it had suspended all new bookings between the Indian subcontinent and the Upper Gulf — covering the UAE, Bahrain, Qatar, Iraq, Kuwait, and Saudi Arabia — it confirmed that the escalating Iran crisis was no longer merely raising risk premiums; it was severing commercial flows entirely. The Daily Star

The garment sector cannot absorb air freight as a substitute: the BGMEA president notes that air freight costs have increased between 25–40 percent for some European buyers due to the Red Sea crisis, and some buyers are renegotiating contracts or diverting orders. The Daily Star As one garment vice president told Nikkei Asia, air freight costs 10–12 times more than sea transport — an instant route to negative margins. Bangladesh cannot afford order diversion at scale.

Sri Lanka’s exposure cuts across multiple arteries simultaneously. With over 1.5 million Sri Lankans (nearly 7 percent of the population) employed in the Gulf region, and the island recording a record $8 billion in remittances in 2025, any large-scale evacuation or Gulf economic contraction would shatter the fiscal stability the government has only recently achieved. Sri Lanka’s tea exports to Iran, Iraq, and the UAE — where the Iranian rial’s collapse has triggered a freeze in new orders — threaten the livelihoods of smallholder farmers across the southern highlands. EconomyNext

The Hormuz Wildcard: A Scenario That Could Rewrite Everything

Much of the analysis above rests on a scenario in which the Strait of Hormuz remains open. Should it be disrupted — even temporarily — the macroeconomic calculus transforms. Approximately 20 percent of global oil consumption transits the Strait daily, along with over one-fifth of the world’s LNG supply. Alternative land pipelines — Saudi Arabia’s East-West Pipeline and the UAE’s Abu Dhabi Crude Oil Pipeline to Fujairah — can offer some help, but their capacity represents barely one quarter of normal Hormuz throughput. MUFG Research

Under the ADB’s most severe scenario — a $55/barrel sustained oil shock — the impact on current account balances across ASEAN and South Asia would be severe. Current account deficits for the Philippines and India could widen above 4.5 percent and 2 percent of GDP respectively if oil prices were to rise above $90/bbl on a sustained basis. MUFG Research Pakistan, with minimal fiscal buffers, would face renewed currency crisis. India’s annual import bill would expand by roughly $82 billion relative to 2025 averages — approximately equal to its entire defence budget.

Silver Linings and Second-Order Winners

Crises reshape competitive landscapes. Vietnam’s electronics and apparel sector recorded export turnover of $4.45 billion in July 2025 — an 8.2 percent increase over June and 21 percent higher than the same month last year — driven partly by supply chain shifts away from China. Asian Development Bank Malaysia and Indonesia, as partial net energy exporters, benefit from elevated crude prices on the revenue side. Singapore, with a FY2025 fiscal surplus of 1.9 percent of GDP, has the deepest fiscal reserves in ASEAN to deploy energy transition support without macroeconomic destabilisation. OCBC

Thailand has launched planning work on its $28 billion Landbridge project — deep-sea ports at Ranong and Chumphon connected by highway and rail — as a potential alternative corridor to the Strait of Malacca. India is accelerating infrastructure at Chabahar Port, a corridor that bypasses Pakistani territory and opens Central Asian trade routes. The “friend-shoring” dynamic identified by the IMF is also accelerating: as Western supply chains reconfigure away from single-region dependence, ASEAN economies — particularly Vietnam and Indonesia — stand to attract manufacturing diversion from China that partially offsets the Middle East trade cost shock. Krungsri

China’s Shadow: The Geopolitical Dimension

No analysis of the Middle East’s economic impact on ASEAN and SAARC is complete without acknowledging Beijing’s role. China, which imports roughly 75 percent of its crude from the Middle East and Africa, has more at stake in Hormuz stability than almost any other economy. Yet Beijing has maintained studied neutrality, positioning itself as potential peacebroker while expanding bilateral energy security arrangements with Gulf states.

Meanwhile, China’s Belt and Road Initiative (BRI) port infrastructure — Gwadar in Pakistan, Hambantota in Sri Lanka, Kyaukpyu in Myanmar — is emerging as a hedging option for economies seeking to reduce Red Sea exposure. The IMF’s Regional Economic Outlook warns that geoeconomic fragmentation — the splitting of global trade into rival blocs — carries a potential output cost, with a persistent spike in global uncertainty producing GDP losses of 2.5 percent after two years in the MENA and adjacent regions, with the impacts more pronounced than elsewhere due to vulnerabilities including higher public debt and weaker institutions. International Monetary Fund

Outlook 2026–2028: GDP Drag Estimates and Divergent Trajectories

Baseline projections remain broadly positive for the region, underpinned by demographic dividends and resilient domestic demand. The World Bank’s October 2025 MENAAP Update projects regional growth reaching 2.8 percent in 2025 and 3.3 percent in 2026. World Bank The IMF’s October 2025 Regional Outlook projects Pakistan’s growth increasing to 3.6 percent in 2026, supported by reform implementation and improving financial conditions. International Monetary Fund ADB’s September 2025 forecasts show Indonesia at 4.9%, Philippines at 5.6%, and Malaysia at 4.3% for 2025. Asian Development Bank

But the scenario distribution has widened materially. In a contained-conflict baseline (oil averaging $75–85/bbl), the GDP drag for oil-importing SAARC economies is estimated at 0.3–0.7 percentage points annually through 2027 — painful but manageable. In a protracted Hormuz-disruption scenario, modelled GDP losses escalate to 1.5–3.0 percentage points for the most energy-dependent economies: Sri Lanka, Philippines, Bangladesh, and Pakistan. Currency pressures in that scenario could trigger sovereign debt rating downgrades for Pakistan (still under IMF programme) and Sri Lanka (still restructuring external debt).

Policy Recommendations for ASEAN and SAARC Governments

The foregoing analysis suggests a multi-track policy agenda structured across three time horizons:

Immediate (0–6 months)

- Strategic petroleum reserves: Economies with fewer than 30 days of import cover — Bangladesh, Sri Lanka, Pakistan, Philippines — should accelerate bilateral arrangements with GCC suppliers for deferred-payment oil stocking.

- Freight & insurance backstops: State-owned development banks in India, Indonesia, and Malaysia should establish temporary freight insurance facilities for SME exporters unable to access war-risk cover at commercial rates.

- Fiscal fuel-price buffers: Governments should resist immediate full pass-through of oil price increases to consumers in 2026 — the inflationary second-round effects of premature deregulation risk destabilising monetary policy just as disinflation was being consolidated.

Medium-Term (6–24 months)

- Trade corridor diversification: ASEAN and SAARC should jointly accelerate operationalisation of the India-Middle East-Europe Economic Corridor (IMEC) and Chabahar-Central Asia links to reduce exclusive dependence on the Suez/Red Sea routing for European-bound exports.

- Renewable energy acceleration: Each percentage point of fossil fuel imports replaced by domestic solar, wind, or nuclear capacity is a permanent reduction in geopolitical exposure. ADB Green Climate Fund allocations should be explicitly linked to energy import substitution targets.

- Remittance formalisation: Bangladesh, Pakistan, and Sri Lanka should extend incentive schemes to maximise remittance capture through official banking channels, maximising their foreign-exchange multiplier effect.

Long-Term (2–5 years)

- “Asia Premium” hedge architecture: A regional crude futures market, potentially anchored in Singapore, could provide more effective price discovery and hedging access to smaller economies that currently pay a structural premium above Brent.

- Supply chain friend-shoring with selectivity: ASEAN’s competitive advantage is best served by remaining in the middle of the US-China geopolitical competition rather than choosing sides definitively, attracting Western supply-chain investment without triggering Chinese economic retaliation through rare earth or intermediate input export controls.

- Multilateral maritime security: ASEAN and SAARC together represent a significant share of the global trade disruption cost. A formal joint diplomatic initiative requesting a UN-mandated naval security corridor for commercial shipping through the Red Sea and Gulf would add multilateral legitimacy to what is currently a US-led Western operation.

Conclusion: The Geography of Exposure

The Middle East conflict has delivered a masterclass in the hidden geography of economic exposure. Countries that share no border with Israel, Hamas, or Iran — countries that have issued no military guarantee and sent no troops — are nonetheless absorbing the full force of an energy price shock, a logistics cost spiral, and a remittance fragility that was structurally built into their growth models over decades.

Even if hostilities ceased tomorrow, the Red Sea crisis — now stretching into its third year as of 2026 — has tested the limits of global logistics. With Red Sea transits down up to 90 percent and Cape of Good Hope routing now the industry standard, companies face 10–14 extra days in transit, higher inventory costs, and sustained freight premiums of 25–35 percent. DocShipper The ceasefire declared in October 2025 barely shifted the dial. Shipping insurers remain risk-averse; carriers have rebuilt vessel schedules around the longer route.

What the crisis has done is clarify something that globalisation’s practitioners long preferred to obscure: deep economic integration produces deep interdependence, and deep interdependence produces deep vulnerability. The eighteen economies of ASEAN and SAARC are not passive bystanders in a conflict 4,000 miles away. They are, in the most material and measurable sense, participants in its economic consequences. The policy leaders who understand that soonest — and build the resilience architecture accordingly — will determine which countries emerge from the coming years stronger, and which emerge diminished.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance2 months ago

Markets & Finance2 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis1 month ago

Analysis1 month agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks2 months ago

Banks2 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment2 months ago

Investment2 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Asia2 months ago

Asia2 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Analysis4 weeks ago

Analysis4 weeks agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Global Economy3 months ago

Global Economy3 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy3 months ago

Global Economy3 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

Pingback: Pakistan's Strategic Economic Position in South Asia - The Economy