Oil Markets

Pakistan and India Most Vulnerable from Oil Shock as Strait of Hormuz Tensions Escalate

In a cramped flat in Karachi’s Lyari district, Fatima Siddiqui runs the calculations she hoped she would never have to make again. The LPG cylinder that kept her family’s stove burning through winter now costs 40 percent more than it did a fortnight ago. Across the border in Mumbai, autorickshaw driver Rajan Patil stares at a fuel pump showing prices he last saw in 2022. Neither of them has ever heard of Operation Epic Fury. Both of them are paying for it.

Oil prices surged past $100 a barrel on Sunday, March 9 — the first time crude has traded in triple digits since Russia’s invasion of Ukraine — after Brent jumped more than 30 percent, at one point topping $119, as the US and Israeli war on Iran entered its second week. Al Jazeera International benchmark Brent crude futures traded 11.6 percent higher at $103.47 per barrel on Monday morning, while US West Texas Intermediate futures were last seen 12.2 percent higher at $101.97, putting oil on track for one of its biggest single-day jumps on record. CNBC

The trigger is as structural as it is sudden. On February 28, 2026, the United States and Israel initiated coordinated airstrikes on Iran under Operation Epic Fury, targeting military facilities, nuclear sites, and leadership, resulting in the death of Supreme Leader Ali Khamenei. Wikipedia Iran’s retaliation was immediate and surgical: tanker traffic through the Strait of Hormuz dropped to four vessels on Sunday, March 1, compared with an average of 24 per day since January. Euronews For the world’s most critical energy chokepoint — the narrow passage connecting the Persian Gulf to the Arabian Sea — that is the equivalent of cardiac arrest.

For Pakistan and India, it is something closer to a pre-existing condition suddenly, violently exposed.

Why the Strait of Hormuz Is the Aorta of South Asian Energy

The geography of South Asia’s energy dependency is stark. Almost half of India’s crude oil imports and about 60 percent of its natural gas supplies move through the Strait of Hormuz. Seatrade Maritime Qatar and the United Arab Emirates account for 99 percent of Pakistan’s LNG imports and 53 percent of India’s, according to Kpler data. CNBC No other major economy outside the Gulf itself carries that kind of concentrated exposure to a single 21-mile-wide chokepoint.

The majority of the crude oil shipped through the Strait of Hormuz goes to Asia, with China, India, Japan, and South Korea accounting for nearly 70 percent of shipments, according to the US Energy Information Administration. NPR But the strategic buffer that separates China — with its substantial onshore storage — from India and Pakistan is decisive. India’s limited crude oil reserves of about 100 million barrels are sufficient for only 40 to 45 days of consumption, leaving the country particularly vulnerable to supply disruptions through the Strait of Hormuz, the Asian Development Bank warned on Friday. Business Standard Pakistan has no meaningful strategic petroleum reserve at all.

The prognosis from analysts is blunt. BMI (Fitch Solutions) identifies Pakistan and India as the most vulnerable among emerging markets, as energy importers with relatively high exposure to the Strait of Hormuz, while Egypt and Turkey are singled out for secondary exposure due to high energy import bills, fragile external positions, large energy subsidies, and unanchored inflation. Business Recorder

The Supply Shock: Unprecedented, and Worsening

Energy market veterans are reaching for superlatives they rarely deploy. Claudio Galimberti, chief economist at Rystad Energy, compares the effective halt of oil flows through the Strait of Hormuz to blocking the aorta in a circulatory system, adding that “we have not seen anything like this in pretty much the history of the Strait of Hormuz.” NPR

The anatomy of the disruption has several compounding layers. QatarEnergy halted activity at the world’s largest liquefied natural gas export facility after it was targeted in an Iranian drone attack, while tanker traffic through the Strait of Hormuz — which handles around a quarter of global seaborne oil trade and a fifth of LNG supply — has come to a near standstill. Bloomberg Iraq and Kuwait have already begun to shut in production, with analysts warning that the UAE and Saudi Arabia may also be vulnerable if the Strait of Hormuz remains closed for a sustained period. CNBC

Goldman Sachs, which had forecast a second-quarter Brent average of $76 per barrel as recently as Wednesday, now warns of a far darker scenario. The bank estimates that traders demand about $14 more per barrel than before the conflict to compensate for increased risks, roughly corresponding to the effect of a full four-week halt in flows through the Strait of Hormuz with spare pipeline capacity used as a partial offset. If flows are halted for five weeks, prices could reach $100 per barrel — a threshold already breached. Goldman Sachs

Saul Kavonic, a senior energy analyst, captures the systemic danger with particular clarity: cutting off 15 to 20 percent of the world’s oil supply not only slows down every economy globally but also introduces an inflation impulse — and inflation plus slowing growth is stagflation, which constitutes an economic disaster. Business Recorder

Pakistan: Structurally Fragile, Acutely Exposed

Pakistan enters this crisis with no margin. An IMF bailout program, a current account that was only just stabilizing, and energy subsidies already consuming a destabilizing share of the federal budget — the Hormuz shock arrives at the worst possible moment.

Petrol prices in Pakistan rose by Rs55 per litre in March 2026, triggering long queues at filling stations, increased transport costs, and widespread public frustration. Modern Diplomacy The government’s official line — that the increase is an inevitable consequence of global oil volatility — is accurate as far as it goes. What it understates is the structural dimension: Pakistan’s near-total LNG dependence on Qatar and the UAE, combined with the absence of meaningful storage infrastructure, leaves the country exposed not just to price spikes but to physical shortfalls.

Pakistan has limited storage and procurement flexibility, meaning disruption would likely trigger fast power-sector demand destruction rather than aggressive spot bidding, according to Go Katayama, principal insight analyst at Kpler. CNBC In practical terms, that means rolling blackouts in a country where electricity shortfalls are already politically explosive.

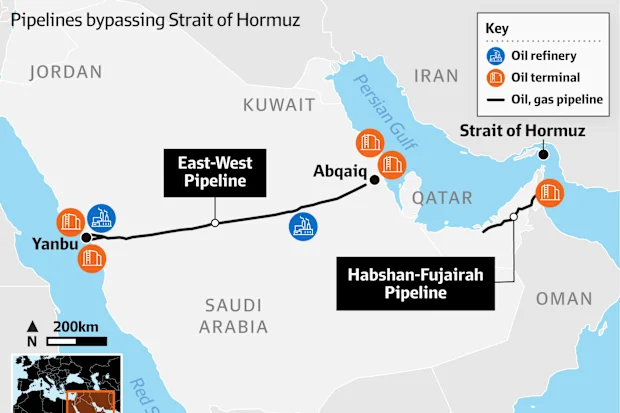

On March 4, Pakistan officially requested that Saudi Arabia reroute oil supplies through Yanbu’s Red Sea port, with Riyadh providing assurances and arranging at least one crude shipment to bypass the closed strait. Wikipedia The arrangement provides temporary relief. It cannot substitute for the volume, reliability, or price levels to which Pakistan’s energy system is calibrated.

The Pakistani rupee, already among the most depreciated major currencies of the past three years, faces renewed downward pressure. Every $10 increase in oil prices widens Pakistan’s current account deficit by an estimated 0.4 to 0.6 percent of GDP — an economy that cannot absorb that hit without either rationing foreign exchange or accelerating monetary loosening that further stokes inflation already running above 20 percent in food categories.

India: Scale Amplifies Vulnerability

India’s exposure is structural rather than acute — but at Indian scale, structural vulnerability produces acute consequences.

With nearly 90 percent of India’s crude oil requirement met through imports, any disruption in global energy supply — particularly through the Strait of Hormuz — poses a direct risk to macroeconomic stability, according to SBI Research. Business Today Moody’s warned that costly energy imports would weaken the rupee, raise inflation, worsen the current account balance, and complicate monetary policy as well as fiscal management if they lead to expanded subsidies to offset the economic shock. Business Standard

The fiscal arithmetic is unforgiving. India’s Union Budget for 2026–27 was constructed on oil averaging $68 to $70 per barrel. At $103, every rupee of subsidy relief the government extends to consumers — and political pressure to do so is intense, with state elections pending — translates directly into fiscal slippage. Every rupee of subsidy withheld translates into retail fuel price increases of ₹5 to ₹15 per litre on current trajectory estimates.

India has already ordered refiners to maximise production of cooking fuel as imports from the Middle East decline, while gas-intensive industries, particularly fertiliser manufacturers, may face pressure if LNG supplies remain tight. Business Standard The fertiliser link is particularly consequential: disrupted LNG supply constrains domestic fertiliser production just as Rabi crop planting cycles approach, threatening both agricultural output and rural inflation.

The Indian rupee’s recent relative stability — it had appreciated marginally against the dollar in early 2026 — faces a sharp test. India’s oil imports are priced in dollars, so a weaker rupee means the same barrel of oil costs more in local currency, driving inflation through the transport, manufacturing, and agriculture chains simultaneously. Wordzz

The Comparison Table: Pakistan vs India vs GCC

| Indicator | Pakistan | India | GCC Average |

|---|---|---|---|

| Oil import dependency | ~85% imported | ~90% imported | Net exporter |

| LNG sourced from Gulf | ~99% | ~53% | Exporter |

| Strategic petroleum reserve | Effectively none | 40–45 days | Substantial |

| Current account position | Fragile surplus | ~1.5% deficit | Surplus |

| Fiscal space for subsidies | Very limited | Constrained | Ample |

| Currency resilience | Low | Moderate | High |

| Exposure rating (BMI/Fitch) | Most vulnerable | Most vulnerable | Adverse but manageable |

Tourism, Logistics, and the Invisible Multiplier

The economic damage radiating from the Strait of Hormuz crisis extends well beyond oil prices. The waterway is not merely an energy corridor — it is a central artery of the global logistics system, and its disruption is reshaping aviation, hospitality, and freight networks with consequences that will outlast any ceasefire.

Cruise ships reduced activity in the Persian Gulf and stopped using the strait, stranding 15,000 passengers on six major cruise ships. Wikipedia The Gulf aviation hub model — built on Dubai and Abu Dhabi serving as transfer points between Asia and Europe — is under immediate pressure as war-risk insurance surcharges inflate operating costs and itinerary rerouting adds hours and fuel burns to long-haul routes.

For Pakistan and India, the tourism dimension cuts both ways. The Gulf diaspora — some 7 million Pakistanis and 8 million Indians working in the Gulf Cooperation Council states — represents a critical source of remittances. Any sustained economic disruption to Gulf economies, whether through reduced oil revenues or conflict-related instability, threatens remittance flows that collectively account for 7 to 8 percent of Pakistan’s GDP and a meaningful share of India’s foreign exchange receipts. BMI’s baseline scenario is that the conflict in Iran will be large but short-lived, though there is a clear risk of a prolonged war. Among emerging markets, the economic impact will be most pronounced in the GCC, reflecting the shock’s adverse effects on trade, logistics, tourism, and investment. Business Recorder The knock-on to South Asian remittance economies would be severe.

The Forward Scenarios: Baseline and Downside

Baseline (BMI/Goldman Sachs): The conflict remains intense but contained, with the Strait of Hormuz beginning to partially reopen within three to four weeks as US naval escorts provide a corridor. Goldman Sachs estimates that a four-week full halt in Hormuz flows would push Brent to around $85 to $90 per barrel, with prices moderating as Strategic Petroleum Reserve releases from the G7 — which finance ministers discussed on Monday — provide partial offset. Goldman Sachs Under this scenario, Pakistan faces six to eight months of elevated inflation and currency pressure but avoids balance-of-payments crisis. India absorbs a current account widening of approximately 0.8 to 1.2 percent of GDP.

Downside (Prolonged Disruption): If the disruption in the Strait of Hormuz persists for another one to two weeks beyond current levels, prices could move toward $130 to $150 per barrel, according to senior market analysts. Business Recorder Under this scenario, Pakistan would almost certainly require an emergency IMF facility enhancement; India would face stagflationary pressure combining slowing growth with food and fuel inflation above 8 percent. The rupee and Pakistani rupee would both face disorderly adjustment risk.

The tail risk is darker still. If infrastructure is seriously damaged in oil-rich countries along the Gulf, it could take much longer for production to normalize even after missile strikes stop, and a full closure of the Strait of Hormuz would leave OPEC barrels in the region as effectively stranded assets in an extended war scenario. NPR

Policy Responses: What Islamabad and New Delhi Are Doing

Pakistan’s immediate moves:

- Emergency request to Saudi Arabia to reroute crude shipments via the Red Sea corridor through Yanbu port

- Engagement with the State Bank of Pakistan to manage rupee liquidity and cap speculative dollar demand

- Preliminary discussions with the IMF on contingency facility options if the crisis extends beyond six weeks

India’s immediate moves:

- Directive to state refiners to maximize domestic fuel production capacity

- Reopening of discussions on Russian crude procurement from floating storage in Asian waters

- Review of strategic petroleum reserve release protocols in coordination with the IEA

Both governments face the same fundamental dilemma: subsidise to protect consumers and blow up fiscal balances, or pass through prices and risk political instability. There is no clean answer when the originating shock is geopolitical and beyond domestic control.

Investor and Traveller Takeaways

For investors with exposure to South Asian equities and credit: the Pakistani rupee and Indian rupee face asymmetric downside risk in a prolonged disruption scenario. Pakistani sovereign spreads, already elevated, will widen further on any indication of IMF program slippage. Indian equities’ energy-sector composition and the fiscal arithmetic of subsidy policy make consumer staples and financial sector names most vulnerable to earnings revisions.

For travellers and the travel industry: Gulf aviation hubs face operational disruption and insurance cost inflation that will flow through to ticket prices across Asia-Europe routes within days. Bangladesh is experiencing severe strain, with the government bringing forward Eid holidays, ordering universities to close temporarily to reduce electricity demand, and imposing limits on fuel sales amid panic buying. Business Standard Regional tourism recovery, which had only just returned to pre-pandemic levels across South and Southeast Asia, faces a significant setback.

The Strait of Hormuz has been threatened before. It has never actually closed — until now. What the markets are pricing, and what Fatima Siddiqui and Rajan Patil are already living, is the realisation that 50 years of energy-security wargaming has finally become a news headline. The models suggested Pakistan and India would be most vulnerable. The models were right.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan’s petrol price hit Rs. 316.15 per litre by mid-July 2026 as global crude climbed toward $89 a barrel following disruption in the Strait of Hormuz. The IMF has held Pakistan’s FY2026 growth forecast at 3.5%, warning that a wider Middle East conflict could trigger further price volatility — squeezing a government already bound by strict Extended Fund Facility (EFF) spending limits.

The story underneath the pump-price headlines

Pakistani business media has covered the weekly petrol price revisions extensively. What’s been under-examined is the macro trap those revisions represent: Islamabad is caught between political pressure to subsidise fuel and an IMF programme that leaves almost no room to do so — a bind that has already produced one failed negotiation this year.

The numbers driving the squeeze

The IMF’s July update to its World Economic Outlook kept Pakistan’s growth forecast unchanged at 3.5% for the new fiscal year, even as it flagged the risk of renewed Middle East conflict fuelling further price volatility. The Fund’s average petroleum spot price index is now projected at $89 a barrel — 9% above its earlier reference forecast — after crude jumped roughly $8 a barrel within two trading days once the US withdrew Iran’s oil-export waivers and struck Iranian targets (Express Tribune).

That pass-through has been immediate at the pump. Petrol in Pakistan rose to Rs. 316.15 per litre and diesel to Rs. 354.35 per litre by July 18, with the Oil and Gas Regulatory Authority (OGRA) shifting from fortnightly to weekly price reviews to keep pace with global crude swings (PetrolPrice.com.pk; MashriqTV).

Why Islamabad can’t simply subsidise its way out

Pakistan remains under strict IMF supervision through its Extended Fund Facility, which sharply limits the government’s room to cushion consumers from global price shocks. Economist Kaiser Bengali, former adviser for planning and development to the Sindh chief minister, has described the arrangement bluntly: a single $1 billion IMF tranche — trivial by global fiscal standards — can be the difference between stability and crisis for Pakistan’s external accounts (Al Jazeera).

The government has already been burned attempting to work around this constraint. Earlier this year it sought IMF approval for higher fuel subsidies and was rebuffed, a negotiating misstep analysts have criticised as poorly handled given how little fiscal slack the programme allows (Al Jazeera).

The FY26-27 budget math

Pakistan’s FY2026-27 budget is explicitly framed as a pivot from “stabilization to growth” under the IMF programme, targeting 4% GDP growth, 8.2% inflation and a 3.6% fiscal deficit. But sector analysts at the Pakistan & Gulf Economist note the entire framework is contingent on oil prices behaving: if crude continues climbing, the fiscal deficit will widen, pressuring government borrowing and forcing tighter monetary policy in response (Pakistan & Gulf Economist). Separate estimates put the FY26 consolidated fiscal deficit in the 4.0-4.5% of GDP range — already above the IMF’s 4.0% target before accounting for the latest oil shock (Dawn).

The political cost

The squeeze has visible street-level consequences. Rickshaw drivers in Lahore staged protests against rising fuel costs during the earlier phase of the US-Iran conflict, a preview of the public frustration that further price hikes risk reigniting (Al Jazeera). With inflation forecast by the IMF to climb globally from 4.1% in 2025 to 4.7% in 2026 before easing to 3.9% in 2027, Pakistan’s own disinflation trend — which had been improving since early 2024 — now risks stalling in step with the wider global pattern (Express Tribune).

The one offsetting factor

Not every signal points downward. The IMF noted that part of the reduction in oil flows through Hormuz has been offset globally by inventory drawdowns, which has kept the overall price increase more muted than a pure supply-shock model would predict (Express Tribune). And Pakistan’s rupee has shown relative stability against the US dollar through 2026, which — if sustained — would partially cushion import costs regardless of what happens to global crude (PetrolPrice.com.pk).

The bottom line

Pakistan’s economic trajectory for FY27 now depends on a variable no domestic policymaker controls: how long the Strait of Hormuz disruption persists. With IMF conditionality removing the traditional subsidy lever and the rupee’s stability doing much of the defensive work, Islamabad’s fiscal room for manoeuvre this cycle is as narrow as it has been at any point in the current EFF programme.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Gulf oil producers are fast-tracking at least seven new or expanded pipelines — from Iraq’s Kirkuk-Baniyas line through Syria to the UAE’s second Fujairah link — to move up to 14 million barrels a day around the Strait of Hormuz by 2028, after renewed Iranian tanker attacks halved Iraqi output and pushed Brent crude above $84 a barrel.

For decades, the Strait of Hormuz has been the single most consequential 33 kilometres of water in the global economy — the channel through which roughly a fifth of the world’s oil has passed on its way from the Gulf to refineries in Rotterdam, Singapore and Karachi. That geography is now being actively engineered away.

Why this is the story competitors are missing

Most coverage of the Hormuz crisis has focused narrowly on tanker attacks and day-to-day Brent price swings. The bigger, under-reported story is structural: a permanent reshaping of Middle East export infrastructure that will outlast the current conflict and change how nine-market economies — from Pakistan to Singapore to the UK — plan their energy security for the next decade.

What triggered the scramble

Iran’s attacks on commercial vessels this month forced a sharp slowdown in Hormuz shipping, prompting two days of US strikes on Iranian military targets and reinforcing what shipbrokers describe as a “stop-start” pattern of disruption likely to persist (AGBI). The damage to Iraq has been severe: OPEC’s second-largest producer saw output fall from roughly 4.2 million barrels per day in February to about 1.9 million bpd by June, since Baghdad depends almost entirely on its southern Basra terminals with few pipeline alternatives (CNBC).

Brent crude climbed to around $84 a barrel, up from $76 before the latest escalation, according to reporting from Abu Dhabi (The National). Analysts at Goldman Sachs warn prices could push toward $100 or higher if disruptions persist (Carra Globe).

The pipeline build-out, country by country

Iraq–Syria: Washington is backing efforts to revive the Kirkuk-to-Baniyas pipeline to Syria’s Mediterranean coast, dormant since it was damaged during the 2003 US invasion. US energy officials signed a formal agreement in Washington, with Chevron among the companies exploring involvement in construction (Marketplace; Bloomberg). Even fully restored, the line would carry only around 2 million bpd — a fraction of the roughly 20 million bpd that normally transits Hormuz when fully open, but a meaningful hedge nonetheless.

Iraq–Jordan: Baghdad and Amman have revived a 2013-era plan for a pipeline linking Basra to the Jordanian port of Aqaba, discussed at a trilateral meeting involving US special envoy Tom Barrack (The National).

UAE: Abu Dhabi is doubling the capacity of its pipeline to the Port of Fujairah on the Gulf of Oman, which sits outside the strait entirely.

Saudi Arabia: Riyadh is weighing an expansion of its East-West pipeline to the Red Sea port of Yanbu by as much as 2 million bpd.

Taken together, Goldman Sachs analysts estimate the region’s Hormuz-bypass pipeline capacity could exceed 14 million bpd by the end of 2028 — more than 60% of the Gulf states’ pre-war export volume of roughly 23 million bpd (CNBC).

The catch: pipelines aren’t a shield

Analysts caution the infrastructure build-out will not eliminate Iran’s leverage. New pipelines remain just as exposed to the low-cost, asymmetric drone and missile attacks that have already targeted tankers inside the strait, according to shipping analysts quoted by CNBC. Lloyd’s List editor-in-chief Richard Meade notes the disruption has exposed the absence of any durable, long-term framework for managing the strait itself (AGBI).

The nine-market ripple effect

Pakistan is arguably the most exposed of the nine markets in this analysis outside the Gulf itself. Islamabad formally requested Saudi Arabia supply oil via the Red Sea Yanbu route in March, as Karachi refineries scrambled for alternatives to Hormuz-transiting cargo (Carra Globe). Pakistani pump prices have been revised weekly rather than fortnightly to keep pace with volatility, with petrol hitting Rs. 316.15 per litre by mid-July (PetrolPrice.com.pk).

The UAE and Dubai face the sharpest logistics squeeze on the container-shipping side: Jebel Ali, the world’s ninth-largest port and the primary transshipment hub for the Middle East, East Africa and South Asia, is experiencing mounting congestion as vessels reroute around the Cape of Good Hope, adding 10–14 days and materially higher fuel costs to Asia-Europe voyages (Carra Globe).

Singapore, as Asia’s dominant refining and bunkering hub, sits on the receiving end of both higher freight costs and longer transit times for Gulf crude — a dynamic compounding the cost pressures already facing the city-state’s trade-dependent economy.

The UK, as a net oil importer since North Sea output decline, is exposed through global benchmark pricing rather than direct route disruption, but Brent — priced internationally — flows straight into UK pump and industrial energy costs regardless of which pipeline barrels ultimately take.

The bottom line

This is no longer simply a story about tanker attacks — it is the early architecture of a post-Hormuz energy order that Gulf states, Washington and Asian importers alike are building in real time, barrel by barrel, pipeline by pipeline. For businesses and policymakers across the nine markets covered here, the operative question by 2027 will not be whether Hormuz reopens fully, but how much of the world’s oil no longer needs it to.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

The Hidden Cost of the Hormuz Standoff: Why “Sea Gunk” Is the Shipping Industry’s Next Billion-Dollar Problem

Tankers stranded in the Persian Gulf during the US-Iran conflict have sat idle long enough for warm-water barnacles, algae and marine growth to colonize their hulls, a phenomenon known as biofouling. This is now forcing costly dry-dock cleaning, slowing vessel speeds, raising fuel burn and pushing up war-risk insurance premiums — a knock-on cost of the conflict that has received far less attention than headline oil prices.

An Underreported Consequence of the Standoff

Most coverage of the US-Iran conflict has focused on oil prices and the risk of a full closure of the Strait of Hormuz, through which roughly a fifth of the world’s seaborne crude normally passes. Less visible is a slower-moving, equally costly problem: ships that have been anchored or rerouted for weeks are now dealing with heavy hull fouling. Specialist “bottom cleaner” crews are being dispatched to scrape off marine growth that has attached itself to tankers stranded in the warm waters of the Persian Gulf, according to reporting on the scale of the buildup facing vessels caught in the standoff (CNN Business).

Biofouling is not a cosmetic issue. A fouled hull increases drag, which raises fuel consumption by as much as 20–40% depending on severity, according to maritime engineering estimates cited across shipping-industry literature. For an industry already absorbing higher war-risk premiums, the added fuel and dry-docking costs compound an already expensive standoff.

Where the Standoff Stands Now

By early July, daily oil flows through the Strait had recovered to more than 10 million barrels a day, with Saudi and UAE crude exports running at roughly 90% of pre-war levels, according to a review of shipping data by UK Finance. That recovery has helped push Brent crude down roughly 40% from its April peak. But the fact that flows are recovering doesn’t erase the weeks of disruption already priced into contracts, insurance renewals and vessel maintenance schedules.

Bank of England Governor Andrew Bailey has flagged this lag effect directly, noting that even as spot oil prices fall, “the higher energy prices of the past four months mean there’s already some inflationary pressure in the pipeline” for consumer economies (Hanbury Wealth Economic Review).

Why This Matters Beyond Shipping

The biofouling problem is a useful proxy for a broader truth about the Hormuz conflict: its costs are not confined to the headline price of a barrel of oil. They show up in:

- Insurance markets — War-risk premiums for Gulf transits have risen sharply and are only slowly normalizing as underwriters reassess vessel-specific risk.

- Fuel and emissions costs — Fouled hulls burn more bunker fuel, an expense that ultimately filters into freight rates and consumer goods prices.

- Dry-dock capacity — A surge in demand for emergency hull cleaning is straining specialist marine services capacity in Gulf ports.

- Second-round inflation — Central banks in energy-importing economies, including the UK, have explicitly built these lagged supply-chain effects into their inflation forecasts for the second half of 2026 (Bank of England, June 2026 Monetary Policy Summary).

The Bigger Picture for Trade-Dependent Economies

Economies with heavy exposure to Gulf shipping lanes — the UK, Singapore, and the broader Gulf states themselves — are watching this unwind carefully. Singapore’s own trade ministry has explicitly cited the conflict as a downside risk to its 2026 growth forecast even as second-quarter GDP beat expectations (CNBC). Dubai, meanwhile, has continued to post resilient non-oil growth, insulated somewhat by economic diversification away from hydrocarbons (Gulf Business).

For freight forwarders, insurers and importers, the lesson of the biofouling episode is that Gulf conflict risk doesn’t disappear the moment a ceasefire is announced — it lingers in maintenance backlogs, insurance renewal cycles and fuel cost pass-through for months afterward.

Key Takeaways

- Prolonged vessel idling in the Persian Gulf has created a costly biofouling problem now requiring emergency hull-cleaning operations.

- Oil flows through Hormuz have largely recovered, but the inflationary “pipeline effect” of the disruption is still working through import-dependent economies.

- Central banks, including the Bank of England, have explicitly incorporated lagged energy-shock effects into their 2026 inflation forecasts.

- Trade hubs like Singapore and Dubai are tracking the conflict’s tail risks even as headline growth figures remain strong.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan Gulf Investment Outflows 2026: Peace Deal Stakes Explained

Canada Trade Diversification 2026: China, Indonesia, UAE Deals Explained

US Forced-Labour Tariffs on 60 Countries: The Hidden Trade Shock of 2026

Global Central Banks 2026: Fed, BoE and BoJ Decisions Could Reshape Markets

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Pakistan’s Most Reliable Export Is Its People: Remittances Hit $41.6 Billion, Overtaking Total Exports

Indonesia’s Confidence Problem: Record Investment, a Sinking Rupiah, and a Widening Credibility Gap

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

China’s Growth Slips to a Four-Year Low: Why Beijing Still Won’t Pull the Stimulus Trigger

The Johor-Singapore Corridor: How Malaysia Became Southeast Asia’s AI Infrastructure Powerhouse

Canada’s Economy ‘On Pause’: Inside the CUSMA Deadline That Passed Without a Deal

Dubai’s Millionaire Magnet: How the UAE Turned Middle East Turmoil Into a Capital Safe-Haven Boom

Britain’s Sixth Prime Minister in a Decade: What Starmer’s Exit Means for Gilts, Sterling and Your Portfolio

Anthropic Offers Up to $600,000 Salary for Critical IPO Role as AI Giant Prepares for Wall Street Debut

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

The AI Super Bubble Is Ready to Burst

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

Bitcoin $150k Milestone Achieved as US Sovereign Crypto Pivot Looms

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

India Economic Rise 2026: How the Subcontinent Toppled Japan

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

China Housing Market Turnaround: White‑List Model Stabilises Prices

Chipmakers Just Lost 6.7% in Two Days: Inside the Great AI Trade Rotation

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025