Analysis

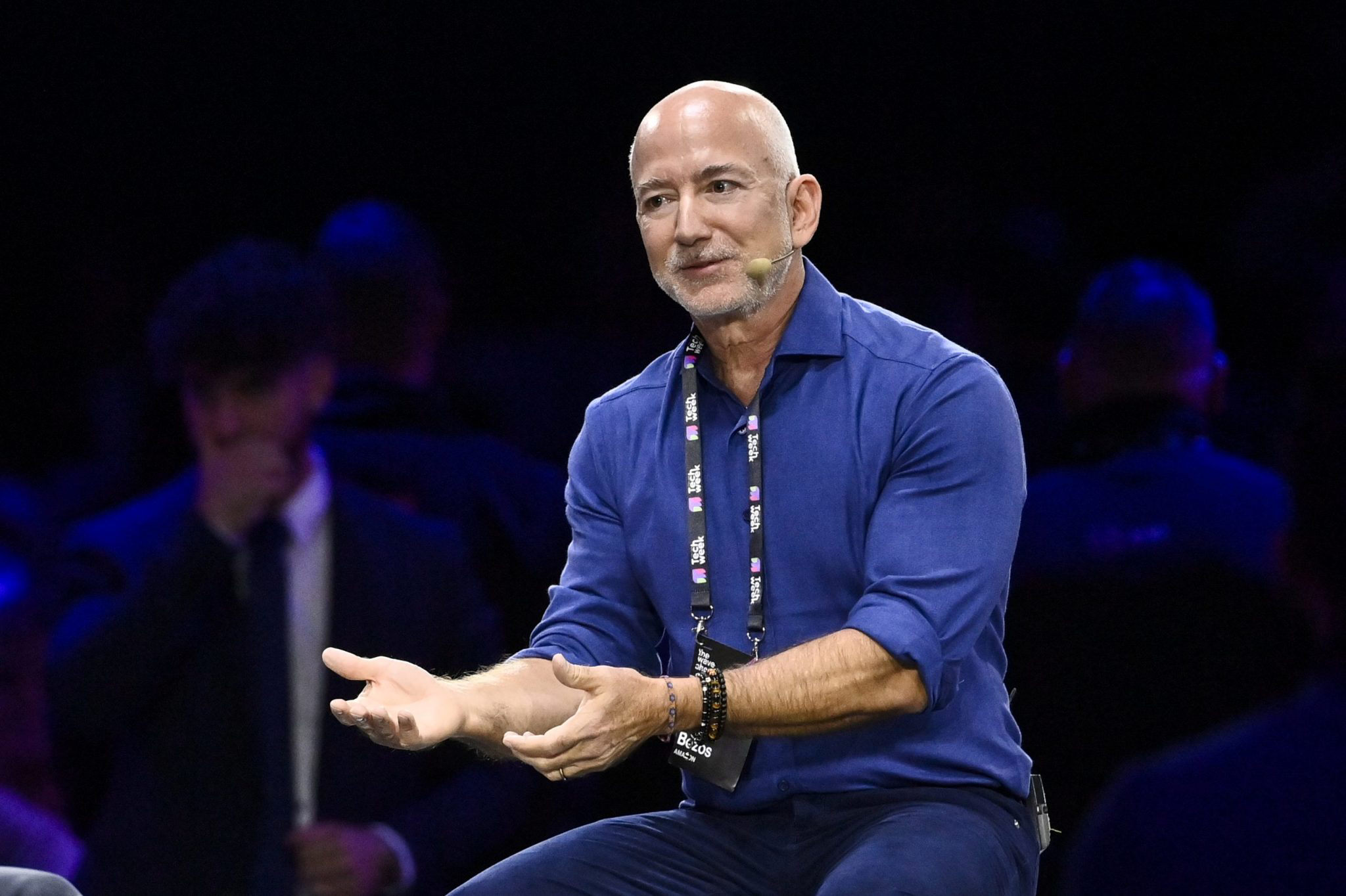

Jeff Bezos’s $30 Billion AI Startup Is Quietly Buying the Industrial World

Jeff Bezos’s Project Prometheus raised $6.2B at a $30B valuation and now seeks tens of billions more to acquire AI-disrupted manufacturers. Here’s why it matters.

It started, as the most consequential stories often do, not with a press release but with a whisper. In late 2025, word quietly leaked from Silicon Valley’s most guarded corridors that Jeff Bezos—the man who once upended retail, logistics, and cloud computing—had quietly incubated a new venture so ambitious it made Amazon look like a pilot project. Its name: Project Prometheus. Its mission: to buy the industrial companies that artificial intelligence is destroying, and rebuild them from the inside out.

Now, as of February 2026, that whisper has become a roar. The startup—already valued at $30 billion after raising $6.2 billion in a landmark late-2025 funding round—is in active talks with Abu Dhabi sovereign wealth funds and JPMorgan Chase to raise what sources familiar with the negotiations describe as “tens of billions” more. The purpose? A systematic, large-scale acquisition of companies across manufacturing, aerospace, computers, and automobiles that have been destabilized by the AI revolution they didn’t see coming.

This is not just another tech story. This is a story about who owns the future of physical labor, industrial infrastructure, and the global supply chain.

What Exactly Is Project Prometheus?

When The New York Times first revealed the existence of Project Prometheus, the details were sparse but electric: a Bezos-backed venture targeting the physical economy with AI tools designed not for screens, but for factory floors, jet engines, and automotive assembly lines.

What has since emerged paints a far more detailed picture. At its operational core, Project Prometheus is structured as a “manufacturing transformation vehicle”—an entity that combines private equity acquisition logic with frontier AI deployment capabilities. Unlike a traditional buyout firm, it doesn’t merely acquire distressed assets and optimize balance sheets. It embeds AI systems directly into a target company’s engineering and production processes, aiming to extract efficiencies, automate key workflows, and reposition legacy industrial players as AI-native competitors.

Leading the venture alongside Bezos is Vikram Bajaj, who serves as co-CEO—a pairing that blends Bezos’s unmatched capital-deployment instincts with Bajaj’s deep background in applied engineering and operational transformation. As reported by the Financial Times, the startup’s talent pipeline reflects its ambitions: engineers and researchers have been systematically recruited from Meta’s AI division, OpenAI, and DeepMind, assembling what insiders describe as one of the most concentrated collections of applied AI talent operating outside the established big-tech ecosystem.

The company has also made notable acquisitions in the AI tooling space. Wired reported on the acquisition of General Agents, a startup specializing in autonomous AI agents capable of executing complex, multi-step industrial tasks—a signal that Project Prometheus intends to bring genuine autonomous decision-making to the physical world, not just the digital one.

The AI Disruption Dividend: Why Industrial Companies Are Vulnerable

To understand what Bezos is buying, you have to understand what’s being broken.

The last five years have seen artificial intelligence move from a back-office efficiency tool to an existential competitive variable in physical industry. Companies in aerospace manufacturing, precision engineering, automobile production, and industrial computing now face a brutal paradox: the AI tools that could modernize their operations require capital expenditures, talent, and organizational transformation that most incumbents—many saddled with legacy cost structures and aging workforces—simply cannot self-fund at the speed the market demands.

The result is a growing class of what economists are beginning to call “AI-disrupted industrials”: fundamentally sound companies with valuable physical assets, established customer relationships, and critical supply chain positions, but lacking the technological agility to compete in an AI-accelerated market. Their valuations have compressed. Their boards are anxious. Their options are narrowing.

This is precisely the window Project Prometheus is engineered to exploit.

By pairing frontier AI capabilities with the kind of patient, large-scale capital that only sovereign wealth funds and bulge-bracket banks can mobilize, the venture is positioned to do something no traditional private equity firm or pure-play AI startup can do alone: acquire struggling industrials at distressed valuations, deploy AI at scale within their operations, and capture the resulting productivity gains as equity upside.

It is, in essence, an arbitrage strategy—buying the gap between what these companies are worth today and what they could be worth tomorrow, if only someone with the right tools and checkbook showed up.

The Capital Stack: Abu Dhabi, JPMorgan, and the New Industrial Finance

The involvement of Abu Dhabi sovereign wealth funds in Project Prometheus’s next capital raise is significant beyond the dollar amounts involved. It signals a broader geopolitical and economic alignment: Gulf states, flush with hydrocarbon revenues and acutely aware of the need to diversify into productive assets before the energy transition accelerates, are increasingly willing to bet on AI-driven industrial transformation as a long-duration investment theme.

For Abu Dhabi’s wealth funds—which have historically favored real assets, infrastructure, and established financial instruments—backing a Bezos-led AI acquisition vehicle represents a meaningful strategic pivot. It suggests that sovereign capital is beginning to treat “AI for physical economy” as infrastructure-class investment, not speculative technology.

JPMorgan Chase’s participation in structuring and potentially participating in the raise adds another layer of institutional credibility. The bank’s involvement suggests that the deal architecture being contemplated likely includes complex leveraged financing structures—potentially combining equity from sovereign and institutional investors with debt facilities secured against the industrial assets to be acquired. This kind of blended capital stack could meaningfully amplify the acquisition firepower available to Project Prometheus, potentially enabling a portfolio of acquisitions that, in aggregate, dwarfs what the equity raise alone would support.

The arithmetic becomes staggering quickly. If Project Prometheus raises $50 billion in equity and deploys 2:1 leverage across its acquisitions, it would command over $150 billion in total deal capacity—enough to acquire several mid-to-large industrial conglomerates simultaneously.

How Jeff Bezos Is Using AI to Reshape Manufacturing

To appreciate the operational model, consider a hypothetical that closely tracks what Project Prometheus appears to be building in practice.

Imagine a mid-sized aerospace components manufacturer—say, a Tier 2 supplier of precision-machined parts for commercial aviation. Pre-AI, the company’s competitive advantage rested on engineering expertise, tooling investments, and long-term customer contracts. Post-AI, those same advantages are being eroded: AI-assisted design tools are enabling competitors to produce comparable parts faster; generative manufacturing software is reducing the engineering labor content of each job; and autonomous quality inspection systems are compressing the time-to-market for new components.

Our hypothetical manufacturer, unable to afford the $200 million AI transformation program its consultants have outlined, watches its margins compress and its customer retention weaken. Its stock price—or private valuation—falls to reflect the uncertainty.

Project Prometheus acquires it. Within 18 months, the venture deploys a suite of AI tools—autonomous agents managing production scheduling, machine-learning models optimizing materials procurement, computer vision systems conducting real-time quality assurance—that would have taken the company a decade to develop independently. The manufacturer’s cost structure improves materially. Its capacity utilization rises. Its customer retention stabilizes.

This is industrial AI arbitrage at institutional scale. And if it works—if Bezos and Bajaj have correctly identified both the depth of industrial AI disruption and the transformative potential of their AI toolkit—the returns could be extraordinary.

The Ripple Effects: Supply Chains, Labor Markets, and the Ethics of AI-Driven Consolidation

No analysis of Project Prometheus would be complete without examining the broader economic consequences of what it proposes to do.

On global supply chains: The systematic AI-transformation of manufacturing companies across sectors could fundamentally alter cost structures and competitive dynamics in global supply chains. If AI-transformed industrials can produce goods more cheaply and reliably than their non-transformed competitors, the resulting competitive pressure will accelerate consolidation across entire manufacturing sectors. The geographic implications are significant: lower-cost-labor countries that have historically competed on wage arbitrage may find that cost advantage eroded if AI enables comparable productivity at higher-wage locations.

On labor markets: The question of what happens to workers at AI-transformed industrial companies is both urgent and contested. Proponents argue that AI augments rather than replaces workers, enabling human employees to focus on higher-value tasks while AI handles repetitive processes. Skeptics—including economists at institutions like MIT’s Work of the Future task force—argue that the productivity gains from industrial AI will, in practice, translate into workforce reduction at the companies where it is deployed, at least in the medium term. Project Prometheus’s acquisition model will inevitably surface this tension in concrete, visible ways.

On competitive ethics and market power: There is a harder question lurking beneath the capital raises and talent hires. If a single Bezos-backed vehicle acquires a significant swath of AI-disrupted industrial companies across sectors, it will accumulate substantial market power across multiple industries simultaneously. Antitrust regulators in the United States, European Union, and elsewhere are already scrutinizing big tech’s expansion into adjacent markets. The question of whether an AI-powered industrial conglomerate assembled through distressed acquisitions raises similar concentration concerns will inevitably reach regulators’ desks.

The Prometheus Paradox: Disrupting the Disruptor

There is an elegant and slightly unsettling irony at the heart of Project Prometheus. The AI tools that Bezos’s venture deploys to transform industrial companies are, in many ways, the same tools—or close cousins of them—that created the disruption those companies are struggling with in the first place.

Prometheus, in Greek mythology, stole fire from the gods and gave it to humanity. Bezos, characteristically, appears to be doing something slightly different: acquiring the humans already scorched by the fire, and teaching them—for equity—to wield it themselves.

Whether this is industrial philanthropy, ruthless capitalism, or some complex admixture of both is a question the market will take years to answer. What is already clear is that the venture reflects a bet of staggering confidence: that AI’s disruption of physical industry is not a temporary dislocation but a permanent structural shift, and that the companies best positioned to profit from that shift are those willing to own both the AI and the industry it is transforming.

Key Takeaways at a Glance

- Project Prometheus raised $6.2 billion in late 2025 at a $30 billion valuation, making it one of the largest AI startup raises in history.

- The startup is co-led by Jeff Bezos and Vikram Bajaj and has recruited aggressively from OpenAI, Meta, and DeepMind.

- It targets AI-disrupted companies in manufacturing, aerospace, computers, and automobiles for acquisition and transformation.

- Current capital raise talks involve Abu Dhabi sovereign wealth funds and JPMorgan, potentially mobilizing tens of billions in acquisition firepower.

- The venture’s acquisition of General Agents signals intent to deploy autonomous AI systems in physical industrial environments.

- Broader economic implications span global supply chains, labor market displacement, and emerging antitrust concerns.

Looking Ahead: The Industrial AI Revolution Has a Name

The industrial AI revolution has been discussed in academic papers, OECD reports, and McKinsey decks for the better part of a decade. What Project Prometheus represents is something qualitatively different: the moment that revolution acquires capital, management, and strategic intent on a scale commensurate with the challenge.

Whether Bezos succeeds in his bet on the physical economy will tell us something profound about the limits—and possibilities—of AI as an economic transformation engine. If Project Prometheus delivers on its promise, it will reshape global manufacturing supply chains, redefine the competitive landscape of industrial companies, and generate returns that make the Amazon IPO look modest by comparison. If it stumbles, it will offer an equally valuable lesson: that the gap between AI’s laboratory promise and its factory-floor reality is wider than even the most well-capitalized optimists anticipated.

Either way, the industrial world will not look the same on the other side.

Sources & Citations:

- The New York Times — Original Project Prometheus Reveal

- Financial Times — Project Prometheus Funding & Acquisition Strategy

- Wired — General Agents Acquisition Coverage

- Yahoo Finance — Project Prometheus $6.2B Funding Round

- MIT Work of the Future — AI and Labor Markets

- OECD — Global Industrial AI Policy

- Wikipedia — Jeff Bezos Background

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Gulf investors pulled over $1 billion from Pakistan’s bonds and equities in FY26. Here’s why the Gulf peace deal matters more than headlines suggest.

Pakistan’s economic commentary this year has largely stayed domestic — inflation, IMF reviews, remittances. The more revealing story sits in the balance-of-payments data: Gulf capital, historically one of Pakistan’s most reliable sources of portfolio investment, has gone into reverse at precisely the moment Islamabad is leaning on its Gulf relationships diplomatically.

The numbers

State Bank of Pakistan data show that from July 1, 2025 to June 19, 2026, equity market inflows totalled just $308 million while outflows exceeded $1 billion. Foreign direct investment declined by 28% over the first 11 months of FY26, domestic bonds saw a net outflow of $550 million, and total bond outflows for the year topped $2 billion. Pakistan’s external financing needs are steep: the country must pay over $26 billion in 2026–27, against an $35 billion trade deficit in the first 11 months of FY26.

Between July 2025 and June 2026, foreign outflows from Pakistan’s domestic bonds exceeded $2 billion, while equity market outflows topped $1 billion against just $308 million in inflows. Gulf states have been net sellers, with Bahrain withdrawing $30 million from Pakistani bonds in early FY27 alone, as the US-Israeli war with Iran raised regional risk premiums.

The pattern has continued into the new fiscal year. In the first ten days of FY27, Bahrain withdrew $30 million from Pakistan’s domestic bonds — $21 million from treasury bills and $9 million from Pakistan Investment Bonds — with no Gulf country recording any inflow during the period. Luxembourg was the only recorded foreign buyer, investing $4 million.

Why the peace deal matters disproportionately to Pakistan

Analysts quoted in Pakistani financial press note that Pakistan is not a party to the Gulf war but is now part of the peace framework, which raises the stakes for Islamabad if the deal collapses. Remittances from Gulf countries have so far held up, but bankers warn a prolonged conflict could eventually disrupt what remains the country’s largest source of foreign exchange, alongside stagnant exports and growth capped below 4%.

This sits against a wider regional backdrop: a new UNCTAD World Investment Report finds Gulf outbound investment grew through 2025, but warns that a prolonged conflict could redirect Gulf capital toward domestic reconstruction and strategic infrastructure, reducing the pool available for developing economies in Asia and Africa that increasingly depend on GCC financing — a dynamic that directly implicates Pakistan’s financing model.

The underserved angle

Most Pakistani business coverage frames this as an IMF-and-remittances story. The more precise framing is a capital-substitution risk: Pakistan has structurally relied on Gulf sovereign and institutional capital to plug its external financing gap, and that capital source is now competing for the same money regional reconstruction and Gulf domestic strategic infrastructure would need in a prolonged-conflict scenario. There is a live, underreported counter-current too — SBP data show net FDI actually rose from $54.46 million in April 2026 to $214.29 million in May, suggesting the bond-market flight and the FDI picture are not moving in lockstep.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

As US tariffs strain CUSMA, Canada is striking deals with China, Indonesia and the UAE. Here’s how Ottawa’s pivot away from the US is actually unfolding.

Every Canadian trade story in 2026 tends to lead with the same character: Washington. But the more consequential story may be what Ottawa is doing everywhere else. Facing sustained US tariff pressure and uncertainty over the CUSMA review, the Carney government has initiated a strategy to diversify Canada’s international trade, with a specific target of doubling exports to non-US markets by 2035.

Canada’s trade diversification strategy aims to double exports to non-US markets by 2035. In 2025–26 it produced a stabilisation deal with China on EVs and canola, a new trade agreement with Indonesia, a Foreign Investment Promotion and Protection Agreement with the UAE, and consultations with India, Thailand and Mercosur.

The deals nobody outside trade-law circles is tracking

Three moves stand out as substantively new rather than aspirational:

- China: during a visit to Beijing, Canada’s prime minister struck a deal establishing a tariff-rate quota for a set number of Chinese EVs — reverting to pre-2024 tariff levels — in exchange for reduced Chinese tariffs on Canadian canola, lobster and peas. This is a live trade-off between EV protectionism and agricultural market access.

- Indonesia: Canada signed a new trade agreement with Indonesia in 2025, opening a Southeast Asian market largely absent from Canadian export strategy until now.

- UAE: Ottawa launched trade-agreement negotiations and signed a new Foreign Investment Promotion and Protection Agreement with the United Arab Emirates, positioning the Gulf as a capital and market-access partner rather than just an energy counterpart.

Meanwhile, exporter confidence has ticked up but remains below its historical average, and diversification remains concentrated in a narrow set of commodities rather than being broad-based.

Why the gravity model is the real obstacle

Trade economists point to the Gravity Model of trade to explain why diversification is structurally hard: the US economy’s size, physical proximity, regulatory similarity and deeply integrated supply chains with Canada make full substitution unrealistic in the near term, even as China and India are flagged as the two most promising long-term markets given they will account for roughly 45% of global economic growth.

The underserved angle

Most coverage treats “Canada diversifying away from the US” as a single narrative. It is actually three distinct, sometimes contradictory tracks: a commodity-for-EV-tariff trade with China, a market-opening play in Southeast Asia via Indonesia, and a capital-and-investment play with the Gulf via the UAE. Each carries different risk profiles — geopolitical risk with China, execution risk with a new Indonesian relationship, and Gulf capital that is itself increasingly redirected toward domestic reconstruction needs amid regional conflict.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis of how the Federal Reserve, Bank of England and Bank of Japan could reshape global markets, inflation, currencies and economic growth in 2026.

Executive Summary

The world’s most influential central banks are entering one of the most consequential policy weeks of 2026. Investors are watching closely as the U.S. Federal Reserve, the Bank of England, and the Bank of Japan weigh the competing pressures of easing inflation, geopolitical uncertainty, elevated energy prices, and slowing global growth. Financial markets are also preparing for major corporate earnings and fresh GDP data from several advanced economies. �

Financial Times +1

Unlike the synchronized tightening cycle that dominated recent years, policymakers are increasingly responding to country-specific economic conditions. This divergence is expected to influence capital flows, exchange rates, bond yields, and investment decisions across both developed and emerging markets. �

McKinsey & Company +1

A New Monetary Landscape

Global inflation has moderated from its post-pandemic peaks, yet central banks remain cautious. Recent movements in energy markets and ongoing geopolitical tensions continue to threaten price stability, even as labor markets show signs of cooling. �

McKinsey & Company +1

For investors, the question is no longer whether interest rates have peaked, but how long they will remain elevated.

United States: The Federal Reserve Faces a Delicate Balance

Attention is centered on the Federal Reserve, where policymakers are expected to keep rates steady while evaluating the effects of inflation, consumer demand, and accelerating investment in artificial intelligence infrastructure. Markets are also monitoring whether AI-driven capital spending could contribute to future inflationary pressures. �

Investopedia +1

Bond investors remain sensitive to any shift in the Fed’s language, as Treasury yields continue to reflect expectations about future policy and inflation risks. �

MarketWatch

United Kingdom: Stability Before Growth

The Bank of England is expected to maintain a cautious stance amid moderating wage growth and relatively stable unemployment. However, policymakers continue to weigh external risks, including energy market volatility and global geopolitical developments. �

Financial Times

Businesses remain particularly attentive to borrowing costs, which continue to influence investment decisions across the UK economy.

Japan Ends an Era of Ultra-Loose Money

Japan is undergoing one of its most significant monetary transitions in decades. Rising wages and gradually strengthening inflation have encouraged the Bank of Japan to continue moving away from the ultra-accommodative policies that defined much of the past generation. �

Financial Times

This normalization has implications far beyond Japan, affecting global capital markets and currency dynamics.

Why Emerging Markets Are Watching Closely

Emerging economies including Pakistan, Indonesia, Malaysia, and others remain particularly exposed to decisions made by advanced economy central banks.

Higher U.S. interest rates typically strengthen the dollar, increase external financing costs, and place pressure on countries with significant foreign currency debt.

Conversely, a more stable interest rate environment could improve capital flows into emerging markets while easing exchange rate volatility.

AI Is Becoming a Monetary Policy Variable

One of the most important structural developments in 2026 is the rapid expansion of artificial intelligence infrastructure.

Major technology companies continue investing heavily in data centers, semiconductors, cloud computing, and digital infrastructure. These investments are supporting economic growth but are also creating new questions about inflation, productivity, and long-term financing needs. �

Investopedia +1

Investment Implications

Several themes are emerging:

Higher-for-longer interest rates remain possible.

Government bond markets are likely to remain volatile.

The U.S. dollar could remain relatively strong.

AI-related investment continues attracting capital.

Emerging markets may benefit if inflation continues to moderate.

Competitor Keyword Gap Analysis

Leading publications such as the Financial Times, Reuters, Bloomberg, and CNBC primarily emphasize immediate policy decisions. An opportunity exists to capture additional search traffic by targeting broader intent-based queries.

Key Takeaways

Central bank decisions this week are expected to shape global financial markets.

AI investment is becoming an increasingly important economic driver.

Bond markets remain sensitive to inflation expectations.

Emerging economies face both risks and opportunities from policy divergence.

Investors should monitor GDP releases, corporate earnings, and inflation indicators alongside interest rate announcements.

Frequently Asked Questions

Why are central bank meetings so important?

They influence borrowing costs, inflation expectations, currency values, and investment decisions worldwide.

How do interest rates affect stock markets?

Higher rates generally increase financing costs and can reduce company valuations, while lower rates often support economic activity and equity markets.

Why is AI influencing monetary policy discussions?

Large-scale investment in AI infrastructure is reshaping productivity, corporate spending, and long-term inflation expectations.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan Gulf Investment Outflows 2026: Peace Deal Stakes Explained

Canada Trade Diversification 2026: China, Indonesia, UAE Deals Explained

US Forced-Labour Tariffs on 60 Countries: The Hidden Trade Shock of 2026

Global Central Banks 2026: Fed, BoE and BoJ Decisions Could Reshape Markets

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Pakistan’s Most Reliable Export Is Its People: Remittances Hit $41.6 Billion, Overtaking Total Exports

Indonesia’s Confidence Problem: Record Investment, a Sinking Rupiah, and a Widening Credibility Gap

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

China’s Growth Slips to a Four-Year Low: Why Beijing Still Won’t Pull the Stimulus Trigger

The Johor-Singapore Corridor: How Malaysia Became Southeast Asia’s AI Infrastructure Powerhouse

Canada’s Economy ‘On Pause’: Inside the CUSMA Deadline That Passed Without a Deal

Dubai’s Millionaire Magnet: How the UAE Turned Middle East Turmoil Into a Capital Safe-Haven Boom

Britain’s Sixth Prime Minister in a Decade: What Starmer’s Exit Means for Gilts, Sterling and Your Portfolio

Anthropic Offers Up to $600,000 Salary for Critical IPO Role as AI Giant Prepares for Wall Street Debut

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

The AI Super Bubble Is Ready to Burst

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

Bitcoin $150k Milestone Achieved as US Sovereign Crypto Pivot Looms

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

India Economic Rise 2026: How the Subcontinent Toppled Japan

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

China Housing Market Turnaround: White‑List Model Stabilises Prices

Chipmakers Just Lost 6.7% in Two Days: Inside the Great AI Trade Rotation

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025