Human Resourcs

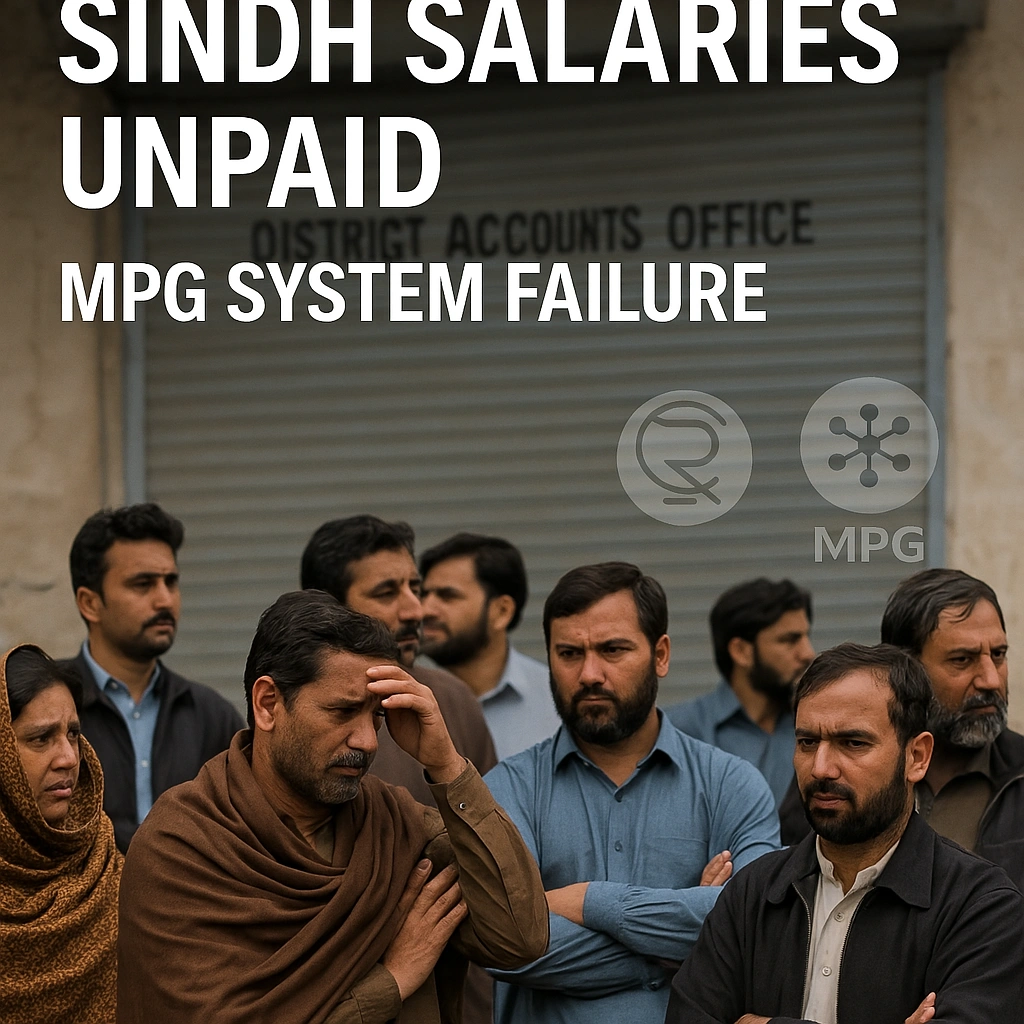

Sindh’s Payroll Crisis: How a Digital Payment System Collapse Left Thousands of Government Employees Without January Salaries

Sindh government employees remain unpaid as MPG payment system fails past January 25th deadline. Exclusive investigation into Pakistan’s digital payment infrastructure breakdown and its human cost.

“The 25th Has Come and Gone—But Salaries Haven’t“

For Muhammad Rasheed, a grade-17 officer in Sindh’s education department, January 28th marks the third day of uncertainty. The 25th—traditionally the day when government salaries illuminate bank accounts across Pakistan—passed without the familiar notification ping. His children’s school fees are overdue. His wife postponed a medical appointment. And like thousands of civil servants across Sindh province, he’s caught in the crossfire of what experts are calling Pakistan’s most significant digital payment system failure in recent memory.

The culprit? The Micro Payment Gateway (MPG), a digital disbursement platform that was supposed to modernize how Sindh pays its 400,000-plus government employees. Instead, it has created a humanitarian and administrative crisis that exposes the fragility of Pakistan’s rush toward digitalization without adequate safeguards.

According to sources within the Accountant General (AG) Sindh office who spoke on condition of anonymity, the system experienced “catastrophic failures” in processing the January 2026 payroll, leaving employees—from junior clerks to senior administrators—in financial limbo. This isn’t merely a technical glitch; it’s a case study in how premature digital transformation can collapse under its own weight.

Understanding the MPG Debacle: What Went Wrong?

The Promise of Digital Transformation

Pakistan’s State Bank of Pakistan (SBP) has been aggressively promoting digital payment infrastructure, including the Raast instant payment system, as part of its National Financial Inclusion Strategy. The MPG was envisioned as Sindh’s answer to efficient, transparent salary disbursement—eliminating intermediaries, reducing corruption, and ensuring timely payments.

The Washington Post recently highlighted Pakistan’s digital ambitions in its Asia economic coverage, noting that “emerging markets face unique challenges in digital payment adoption“—a prescient observation given Sindh’s current predicament.

The Reality: A System Unraveling

Multiple technical failures have compounded since late 2025:

District-Level Breakdowns

- Badin District: Complete payroll processing failure affecting 8,000+ employees

- Dadu District: Partial disbursements with unexplained deductions

- Ghotki District: System rejecting employee bank account validations

Sources indicate the MPG’s integration with the Controller General of Accounts Pakistan (CGA) database encountered synchronization errors, particularly affecting employees receiving the Salaries through MPG .

“The system wasn’t stress-tested for scale,” explains Dr. Ayesha Malik, a digital governance expert at Lahore University of Management Sciences. “When you’re processing 400,000 salaries simultaneously, any latency in API calls or database queries creates cascading failures.”

The Federal-Provincial Divide

The crisis highlights a disturbing disparity. Federal government employees in Islamabad received January salaries on schedule through the tried-and-tested systems managed by the Controller General of Accounts. Punjab province, which piloted a hybrid digital-manual approach, reported 99% on-time disbursement according to data tracked by governance monitoring organizations.

Sindh stands alone in its comprehensive failure—a province that accounts for approximately 22% of Pakistan’s GDP but now cannot pay its own workforce.

The Human Toll: Beyond Statistics and Systems

Stories From the Frontlines

Khadija Bibi, Grade 9 Clerk, Health Department, Hyderabad: “I couldn’t pay my electricity bill. When I went to the school to explain why I couldn’t pay my daughter’s fees, I felt humiliated. They know I’m a government employee. They think I’m making excuses.”

Rashid Ahmed, Grade 16 Officer, Irrigation Department, Sukkur: “We took out high-interest private loans just to buy groceries. The irony? I work in a department that manages water resources for millions, but I can’t manage my own household expenses.”

These aren’t isolated incidents. According to preliminary surveys by civil servant unions, approximately 68% of affected employees have resorted to informal borrowing, often at predatory interest rates exceeding 15% monthly.

The Economist’s recent analysis of emerging market labor dynamics noted that “government employment in South Asia functions as both economic stimulus and social safety net”—making salary delays not just administrative failures but potential triggers for broader economic disruption.

Pension Paralysis

The crisis extends beyond active employees. Thousands of retirees dependent on monthly pensions face similar uncertainty. For many elderly recipients without alternative income sources, this represents an existential threat.

“My father served 35 years in the judiciary,” shares Maryam Khan, daughter of a retired civil judge. “His pension hasn’t come through. He has diabetes medication to buy. This is how we treat our retired public servants?”

Administrative Autopsy: Who’s Accountable?

The Blame Cascade

AG Sindh Office: Claims the State Bank of Pakistan infrastructure experienced “unexpected downtime” during critical processing windows.

State Bank of Pakistan: Points to incomplete data submission from provincial authorities and “non-standard file formats” that violated integration protocols.

Provincial Finance Department: Suggests the Controller General of Accounts delayed authorization for January disbursements due to “budgetary reconciliation issues.”

This circular blame game reveals a fundamental problem: no single entity owns the end-to-end payment process. The MPG system exists in a bureaucratic no-man’s-land where technical failures become administrative hot potatoes.

The Reversion Rumors

Multiple sources confirm that senior Sindh government officials have discussed reverting to manual salary disbursement processes—essentially abandoning the MPG experiment. However, this creates its own complications:

- Data Migration Challenges: Employee records have been partially migrated to the digital system

- Timeline Concerns: Manual processing for 400,000+ employees could take 3-4 business days

- Political Optics: Admitting digital transformation failure before upcoming elections

Financial Times’ coverage of government technology implementations in developing economies warns that “premature abandonment of digital systems after initial failures can create worse long-term outcomes than temporary persistence with fixes”—a dilemma Sindh now faces.

Key Takeaways

- 400,000+ Sindh government employees haven’t received January 2026 salaries due to MPG system failure or Deliberate apathy of Accounts Offices .

- District-level breakdowns in Badin, Dadu,Kashmore and Ghotki compound the crisis

- Federal and Punjab governments disbursed salaries on time, highlighting Sindh’s unique failure

- 68% of affected employees have resorted to high-interest informal borrowing

- Reversion to manual systems being considered but faces logistical and political obstacles

- Broader implications for Pakistan’s digital transformation credibility and economic stability

Comparative Analysis: Lessons From Other Provinces

Punjab’s Hybrid Success

Punjab province implemented a gradual digital transition:

- Pilot program with 10,000 employees (6 months)

- Parallel manual and digital processing (12 months)

- Full digital transition only after 98% success rate achieved

Result? Zero salary delays in the past 18 months.

Federal Government’s Conservative Approach

The federal establishment maintains legacy systems with incremental digital enhancements—prioritizing reliability over innovation. While less efficient, this approach has delivered 100% on-time salary disbursement for 47 consecutive months.

Forbes recently profiled successful government digital transformations in Asia-Pacific, emphasizing that “speed of implementation matters far less than thoroughness of testing and redundancy planning”—wisdom Sindh appears to have ignored.

Broader Implications: Pakistan’s Digital Governance Crossroads

The Credibility Crisis

This failure undermines Pakistan’s broader digital transformation initiatives:

- Raast Payment System Adoption: Banks report declining merchant confidence in government-backed digital platforms

- Tax Digitalization: Concerns about FBR’s planned e-filing mandate

- E-Governance Projects: Provincial governments reconsidering aggressive digital timelines

“One high-profile failure creates systemic skepticism,” notes Farhan Mahmood, a Karachi-based technology governance consultant. “It takes years to rebuild trust in digital government systems.”

The Economic Ripple Effect

When 400,000+ government employees lack purchasing power:

- Local Commerce Disruption: Retailers in government employment hubs (Karachi, Hyderabad, Sukkur) report 30-40% sales declines

- Informal Lending Surge: Private money lenders report unprecedented demand

- Household Debt Accumulation: Long-term financial vulnerability for civil servant families

The Washington Post’s economics desk has documented how public sector salary disruptions in developing economies create “multiplier effects that reduce GDP by 0.3-0.5% quarterly”—a potential scenario for Sindh if delays persist.

The Path Forward: Five Critical Interventions

1. Emergency Manual Disbursement

Activate legacy systems immediately for critical-need employees (grades 1-11, pensioners, medical emergencies) while debugging MPG infrastructure.

2. Independent Technical Audit

Engage international payment system auditors (similar to those used by State Bank of Pakistan for Raast system validation) to identify root causes and recommend fixes.

3. Transparent Communication Protocol

Establish daily public updates on resolution progress—reducing anxiety and rumor circulation among affected employees.

4. Compensatory Measures

Consider:

- Interest-free advance salary loans through government banks

- Automatic reversal of late payment penalties for employee bills

- Hardship grants for lowest-grade employees

5. Accountability Framework

Commission a formal inquiry with public hearings—not for political theater, but genuine systemic learning. The Economist’s governance research emphasizes that “administrative failures require institutional accountability, not individual scapegoating” to prevent recurrence.

Conclusion: A Cautionary Tale for Digital Governance

The Sindh MPG payment system failure represents more than delayed salaries—it’s a referendum on how governments approach digital transformation in resource-constrained environments. The rush to appear technologically progressive, without adequate testing, redundancy planning, and stakeholder preparation, has created precisely the crisis digitalization was meant to prevent.

For Muhammad Rasheed and hundreds of thousands like him, the promise of efficiency has yielded only uncertainty. For Pakistan’s digital governance ambitions, this is a watershed moment: either a catalyst for genuine reform, or the beginning of a retreat to comfortable but inefficient status quo.

The next 72 hours will determine which path employees go for rights . Still no updates for salaries

As Financial Times noted in its recent analysis of emerging market governance challenges: “Technology is only as good as the systems that implement it, and the people who depend on it.” Sindh’s 400,000 government employees are now the unwilling test subjects of that axiom.

The question remains: Will anyone be held accountable before the February salary cycle begins?

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The memo landed on a Thursday afternoon, and for anyone who has followed OpenAI’s evolution from scrappy non-profit to near-trillion-dollar enterprise machine, the subtext was louder than the text. Fidji Simo — the former Meta and Instacart executive who had become the company’s most visible commercial face — announced to her team that she would be taking medical leave to manage a neuroimmune condition. In the same breath, she disclosed that Brad Lightcap, the quietly indispensable COO who had run OpenAI’s operational machinery since the GPT-3 era, was moving out of his role and into something called “special projects.” And that the company’s chief marketing officer, Kate Rouch, was stepping down — not to a rival, but to fight cancer.

Three senior executives, three simultaneous transitions, all announced in a single internal memo. On the surface, it reads like a company under strain. Look closer, and it reads like something more deliberate, more consequential — and far more revealing about where OpenAI actually intends to go.

The Lightcap Move: Elevation or Exile?

The first question anyone asks about a COO being moved to “special projects” is whether this is a promotion or a parking lot. In most corporate contexts, the phrase is C-suite shorthand for managed exits. At OpenAI in April 2026, it is almost certainly neither.

According to a memo viewed by Bloomberg, Lightcap will now lead special projects and report directly to CEO Sam Altman, with one of his primary mandates being to oversee OpenAI’s push to sell software to businesses through a joint venture with private equity firms. Bloomberg That joint venture — internally referred to as DeployCo — is no sideshow. OpenAI is in advanced talks with TPG, Advent International, Bain Capital, and Brookfield Asset Management to form a vehicle with a pre-money valuation of roughly $10 billion, through which PE investors would commit approximately $4 billion and receive equity stakes, along with influence over how OpenAI’s technology is deployed across their portfolio companies. Yahoo Finance

Put plainly: Lightcap is not being sidelined. He is being handed what may be the single most strategically important commercial initiative in OpenAI’s history. The COO title, which implied running the whole operational machine, has been traded for something narrower and arguably higher-stakes — the task of turning OpenAI’s enterprise ambitions into a durable revenue stream before the IPO window opens.

Lightcap had served as OpenAI’s go-to executive for complex deals and investments, and had been a visible face of the company’s commercial ambitions, speaking publicly about hardware plans and brokering enterprise deals across the industry. OfficeChai Those skills translate directly. Structuring preferred equity instruments with sovereign-scale PE firms, negotiating board seats, aligning incentive structures across TPG, Bain, and Brookfield — this is a relationship-heavy, structurally intricate mandate that requires someone who understands both the technology and the term sheet.

The COO role, meanwhile, passes operationally into the hands of Denise Dresser. Dresser is a seasoned enterprise executive with decades of experience including several senior positions at Salesforce, and most recently served as CEO of Slack. OfficeChai Her appointment as Chief Revenue Officer earlier this year already signaled that OpenAI was getting serious about enterprise distribution at scale. Now, with Lightcap’s commercial duties folded into her remit, Dresser becomes the most powerful commercial executive in the company below Altman himself.

The Enterprise Imperative — and Why It’s Urgent

To understand why Lightcap’s new assignment matters, you need to understand OpenAI’s revenue arithmetic. Enterprise now makes up more than 40% of OpenAI’s total revenue and is on track to reach parity with consumer revenue by the end of 2026, with GPT-5.4 driving record engagement across agentic workflows. OpenAI That sounds impressive until you consider the comparative dynamics. Among U.S. businesses tracked by Ramp Economics Lab, Anthropic’s share of combined OpenAI-plus-Anthropic enterprise spend has grown from roughly 10% at the start of 2025 to over 65% by February 2026. OpenAI’s enterprise LLM API share has fallen from 50% in 2023 to 25% by mid-2025. TECHi®

The numbers are startling. OpenAI has the bigger brand, the larger user base, and the higher valuation. But in the market that matters most to institutional investors evaluating an IPO — high-value, sticky, recurring enterprise contracts — it has been losing ground to a younger rival. As Morningstar analysis has noted, OpenAI has never publicly disclosed its enterprise customer retention rate, a conspicuous omission for a company approaching a trillion-dollar valuation. Morningstar

The private equity joint venture is a direct response to this problem. A single PE partnership can unlock AI deployments across entire industry sectors simultaneously — a scale that consulting-led integrations cannot match. OpenAI’s enterprise business generates $10 billion of its $25 billion in total annualized revenue; channeling AI tools directly into portfolio companies controlled by PE partners would create a new enterprise AI distribution strategy beyond traditional software sales channels. WinBuzzer

In this context, handing Lightcap the DeployCo mandate is not a demotion. It is a precision deployment — sending your most experienced deal-maker to close the most important deal-making project in the company’s commercial evolution.

Fidji Simo’s Absence, and What It Reveals

The Simo news is harder to separate from human concern. Fidji Simo, CEO of AGI development, will take medical leave for several weeks to navigate a neuroimmune condition. As she noted in her memo, the timing is maddening given that OpenAI has an exciting roadmap ahead. National Today Her candor — the frank acknowledgment that her body “is not cooperating” — is the kind of leadership transparency that is still rare in Silicon Valley’s performative culture, and it deserves recognition as such.

But her absence also removes the executive who had, in the space of barely a year, become the principal architect of OpenAI’s application-layer strategy. Simo had been central to moves including acquiring Statsig for $1.1 billion, buying tech podcast TBPN as a narrative infrastructure play, launching the OpenAI Jobs platform, and publicly championing the company’s application-layer strategy. OfficeChai While she is away, co-founder Greg Brockman will step in to handle product management. NewsBytes

Brockman’s return to operational product responsibility is itself significant. The co-founder who stepped back from day-to-day duties to take a leave of his own in 2024 is now being called back into the arena, which underscores both OpenAI’s depth of bench concern and, more charitably, the genuine camaraderie that defines its founding generation. It also places an unusual degree of product authority back with someone whose instincts are research-first — a potential counter-current to the enterprise-revenue urgency the rest of the restructuring signals.

The Kate Rouch Question: Talent, Health, and the Human Cost of Hypergrowth

If Lightcap’s transition is a strategic calculation and Simo’s absence is a medical reality, Kate Rouch’s departure sits at the painful intersection of both. The chief marketing officer is stepping down to focus on her cancer recovery, with plans to return in a different, more limited role when her health allows. In the interim, the company is searching for a new CMO. TechCrunch

There is no analytical frame that makes this feel anything other than what it is — a human being dealing with something far more serious than quarterly targets, and a company that, whatever its strategic intentions, is navigating extraordinary personal circumstances among its leadership ranks. Three senior executives facing serious health challenges simultaneously is not a pattern you expect to see in a single memo, and it would be inappropriate to reduce it to a governance risk calculation.

And yet, for investors evaluating OpenAI’s trajectory toward a public listing, the concentration of institutional knowledge at the senior level — and the fragility that implies — is a legitimate consideration. OpenAI has built an extraordinary organization, but it has done so at a pace and intensity that extracts real costs from the people inside it. The question of whether hypergrowth culture is sustainable is not abstract when you are reading about simultaneous health crises in the C-suite.

What This Means for the IPO Narrative

On March 31, 2026, OpenAI closed a funding round totaling $122 billion in committed capital at a post-money valuation of $852 billion, anchored by Amazon ($50 billion), NVIDIA ($30 billion), and other strategic investors. Nerdleveltech A Q4 2026 IPO is widely expected, and the executive restructuring announced this week must be read against that backdrop.

For an IPO to succeed at a valuation approaching or exceeding $1 trillion, OpenAI needs to demonstrate two things that public investors demand above all else: predictable, recurring enterprise revenue, and a governance structure that inspires confidence. The current week’s events simultaneously advance one objective and complicate the other.

On the revenue side, placing Lightcap on the PE joint venture and Dresser on commercial operations is exactly the right structure. Both OpenAI and Anthropic are aggressively courting private equity firms because they control enterprise companies and influence how businesses budget for software and AI — a race growing more urgent as both companies prepare to go public as soon as this year. Yahoo Finance Lightcap’s focused mandate, freed from the operational overhead of a COO role, gives him the bandwidth to close the DeployCo negotiation properly.

On governance, the picture is messier. Three simultaneous leadership transitions — one strategic, two health-related — will attract scrutiny from institutional investors who prize continuity in the months before an S-1 filing. The company’s statement that it is “well-positioned to keep executing with continuity and momentum” Yahoo Finance is the right message, but reassurances require underlying architecture. The burden now falls on Dresser, Brockman, and Altman to demonstrate that OpenAI’s flywheel keeps spinning without missing a revolution.

The Deeper Signal: From Startup to Scaled Enterprise

Step back from the individual moves and a coherent portrait emerges. OpenAI is no longer a startup that accidentally became a cultural phenomenon. It is becoming — with considerable growing pains — a scaled enterprise technology company, and the leadership restructuring reflects that maturation.

The classic startup COO is a generalist: part chief of staff, part dealmaker, part operational firefighter. As companies scale, that role almost always bifurcates. The operational machinery gets a dedicated leader with process-discipline instincts (Dresser, who built Slack’s enterprise go-to-market at scale). The deal-making and strategic partnership functions migrate to someone who can work at a higher level of complexity and ambiguity (Lightcap, now reporting directly to Altman). This bifurcation is not unusual — it is, in fact, the textbook trajectory of every company that has successfully navigated the transition from breakout growth to institutional durability.

What makes OpenAI’s version distinctive is the altitude at which it is happening. The PE joint venture Lightcap is overseeing is not a side arrangement — it is a $10 billion structural bet on a new distribution model for enterprise AI at a moment when the competitive window is closing. Once an AI system is embedded into internal workflows, switching providers becomes costly and time-consuming; early partnerships can define long-term market share. SquaredTech Lightcap’s role is to ensure that OpenAI wins that embedding race before Anthropic does.

Meanwhile, Dresser brings to the revenue function exactly the muscle memory that OpenAI needs: she ran enterprise at Salesforce and then rebuilt Slack’s commercial operations at a moment when the company needed to prove it could grow beyond viral adoption into boardroom-level contracts. The parallels to OpenAI’s current moment are striking. ChatGPT’s consumer virality is not in question. What remains unproven — to skeptical institutional investors, to enterprise buyers, and to rival AI companies gaining ground — is whether OpenAI can convert that consumer footprint into enterprise contracts with the kind of net revenue retention that justifies a trillion-dollar valuation.

What This Means: A Forward-Looking Assessment

For policymakers: The accelerating concentration of AI distribution power through private equity networks deserves regulatory attention. When TPG, Bain, and Brookfield control how AI is deployed across hundreds of portfolio companies spanning financial services, healthcare, and logistics, the implications for competition policy, data governance, and labor markets are substantial. This is not a hypothetical — it is an arrangement being structured right now.

For enterprise technology buyers: The restructuring is, in net terms, good news. Dresser’s commercial acumen and Lightcap’s deal-making focus suggest OpenAI is getting more serious about enterprise SLAs, integration support, and the kind of long-term account management that large organizations actually require. The era of enterprise AI as a self-serve API product is giving way to something that looks more like traditional enterprise software — with all the commercial discipline and relationship investment that entails.

For investors: The executive transitions complicate, but do not invalidate, the IPO thesis. OpenAI is generating $2 billion in revenue per month and is still burning significant cash; the push toward enterprise profitability is not optional, it is existential. CNBC Lightcap’s DeployCo mandate is the most direct mechanism for closing that gap. If the PE joint venture closes as structured and delivers on its distribution promise, the enterprise revenue trajectory could meaningfully improve the margin story ahead of an S-1 filing.

For the AI industry: The talent and health pressures visible in this single memo — across Simo, Rouch, and implicitly in the organizational strain that produces such simultaneous transitions — are a signal worth taking seriously. The AI industry’s intensity is not sustainable at current velocities for all of the people inside it. The companies that figure out how to pursue frontier AI development while maintaining the human durability of their leadership will outlast those that do not.

Brad Lightcap’s transition, in the end, is not the story of an executive being sidelined. It is the story of a company deploying its most trusted commercial architect on its most consequential commercial mission, at the exact moment when the outcome will determine whether OpenAI’s extraordinary private-market story becomes a publicly accountable one. The structural logic is sound. The human arithmetic is harder. And for an AI company that has spent years promising to be beneficial for humanity, learning to be sustainable for the humans inside it may be the more immediate test.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Banks

The Rupture at HDFC Bank: How a Power Struggle Between Chairman and CEO Unraveled India’s Most Valued Franchise

Atanu Chakraborty’s abrupt resignation as HDFC Bank Chairman exposes a deep power struggle with CEO Sashidhar Jagdishan. We analyze the leadership clash, governance fallout, and what it means for India’s banking giant.

In the rarefied world of Indian banking, HDFC Bank has long been the exception—a private-sector behemoth so meticulously governed and consistently profitable that it was often spoken of in the same reverent tones as JPMorgan Chase or HSBC in their prime. That aura of invincibility cracked on March 18, 2026, when Atanu Chakraborty, the bank’s non-executive chairman, submitted a resignation letter that sent a tremor through Dalal Street .

His parting words were as brief as they were devastating: “Certain happenings and practices within the bank, that I have observed over the last two years, are not in congruence with my personal values and ethics” . In a sector where stability is currency, such a cryptic public rupture between the chairman and the management is virtually unprecedented.

Over the following days, a more complex picture emerged—not of fraud or regulatory malfeasance, but of a deep-seated power struggle between Chakraborty and Managing Director & CEO Sashidhar Jagdishan. According to sources cited by the Financial Times, the clash involved divergent views on strategy, the future of key subsidiaries, and ultimately, the question of whether Jagdishan deserved a second term .

As the dust settles, investors, regulators, and corporate India are grappling with a singular question: Was this a necessary cleansing of governance norms, or a destructive personality conflict that has exposed the fragility of India’s most valuable banking franchise?

The Abrupt Exit: A Timeline of Turmoil

The timeline of events reveals a boardroom in disarray, struggling to contain reputational damage.

- March 17, 2026: Atanu Chakraborty sends his resignation letter to H.K. Bhanwala, chairman of the Governance, Nomination and Remuneration Committee. Citing ethical misalignment, he steps down immediately .

- March 18, 2026: The news breaks. HDFC Bank’s stock plunges as much as 8.7% in early trade—its steepest intra-day fall in over two years—erasing over ₹1 lakh crore in market capitalization at the peak of the panic .

- March 19, 2026: The Reserve Bank of India (RBI) moves swiftly to reassure the system, stating that HDFC Bank remains a “Domestic Systemically Important Bank (D-SIB)” with “no material concerns on record as regards its conduct or governance.” It approves Keki Mistry, a veteran of the HDFC group, as interim chairman .

- March 23, 2026: The board, seeking to get ahead of the narrative, appoints domestic and international law firms to conduct a formal review of the contents of Chakraborty’s resignation letter .

- March 26, 2026: The Financial Times reports that the resignation was the culmination of a long-running power struggle over strategy and Jagdishan’s reappointment. Global brokerage Jefferies removes HDFC Bank from its key portfolios, replacing it with HSBC, citing governance concerns .

Anatomy of a Rift: Strategy, Personality, and Power

While Keki Mistry, the interim chairman, publicly dismissed the idea of a “power struggle,” the details leaking from Mumbai’s financial circles suggest a relationship that had soured irreparably . The friction between Chakraborty, a career bureaucrat with a hands-on style, and Jagdishan, a low-profile insider who rose through the ranks, was apparent on multiple fronts.

The CEO Reappointment

The most immediate trigger appears to have been the renewal of Sashidhar Jagdishan’s tenure. According to sources quoted by the Financial Times, Chakraborty was not in favor of extending Jagdishan’s term, while a majority of the board supported the CEO’s continuation . A senior banking executive in Mumbai told FT that the chairman had “taken a clear stand against renewing Jagdishan’s term,” making the disagreement the primary catalyst for the fallout .

The HDB Financial Services Flashpoint

The tensions were not sudden. They had been building for years, crystallizing around the future of HDB Financial Services, the bank’s key non-banking subsidiary. In 2024, Jagdishan supported selling a minority stake to Japan’s Mitsubishi UFJ Financial Group. Chakraborty opposed the move. The deal collapsed, and the business was taken public instead . It was a clear defeat for the CEO’s strategic vision, orchestrated by the chairman—a dynamic that would have strained any working relationship.

Leadership Styles: The Bureaucrat vs. The Operator

Perhaps the most intractable difference was one of style. Chakraborty, a retired IAS officer and former Economic Affairs Secretary, is accustomed to wielding authority. Sources told CNBC-TV18 that the friction stemmed from Chakraborty’s functioning in an “executive style” despite holding a non-executive role . He reportedly involved himself in day-to-day decisions, including promotions and staff interactions, encroaching on territory that Jagdishan and his management team considered their own .

Jagdishan, in contrast, rose through the ranks of HDFC Bank over a quarter-century. He succeeded the legendary Aditya Puri, who led the bank for over 26 years. One shareholder noted that Jagdishan’s “understated” leadership style took time for senior executives to adjust to, lacking the imposing authority of his predecessor . The result was a boardroom where the chairman was perceived as overly assertive, and the CEO struggled to assert his operational control.

Governance at a Crossroads: India vs. Global Standards

The episode has reignited a crucial debate about governance norms in India’s banking sector. In the United States, a departure of this nature—involving ethical qualms from a director—would trigger a mandatory SEC filing (Form 8-K) detailing the nature of the disagreement. In the UK, the FCA expects immediate and precise market updates .

In India, the regulatory framework allowed for a degree of ambiguity that the market punished severely. Moneylife noted in its analysis that “confidence can evaporate faster than capital,” emphasizing that the RBI’s prompt reassurance was necessary to prevent a potential run on deposits in the age of UPI and instant transfers . The 2023 collapse of Silicon Valley Bank showed how quickly social media can accelerate a bank run; a similar dynamic could have unfolded for HDFC Bank had the central bank not intervened decisively .

The RBI’s quick approval of Keki Mistry and its public statement of support were designed to draw a line under the episode. However, the fact that the board had to hire external law firms to investigate the contents of a chairman’s resignation letter—a document the board presumably saw before it was made public—points to a breakdown in internal communication.

Market Reaction and Institutional Consequences

For institutional investors, governance risk is now a premium that must be priced into HDFC Bank’s valuation. The stock, which had already been under pressure due to post-merger integration challenges with HDFC Ltd, has declined about 14% in the past month .

The most telling blow came from Jefferies. The global brokerage exited its holdings in HDFC Bank, removing it from its Asia ex-Japan and global long-only equity portfolios, replacing it with HSBC . This decision, made without a specific explanation, signals that for some international investors, the reputational stain may take time to wash out.

Analysts are now split. Some, like JPMorgan’s Anuj Singla, warn that while no specific misconduct has been alleged, the “perception could weigh on investor sentiment and increase governance risk premium on the stock” . Others argue that the sell-off is overdone, noting that the bank’s fundamentals remain intact. As of late March, HDFC Bank was trading at approximately 1.7–1.8 times price-to-book, a discount to its historical averages but reflective of the broader macro headwinds and this specific governance hiccup .

Conclusion: A Test of Resilience

Atanu Chakraborty’s resignation is more than a boardroom drama; it is a stress test for HDFC Bank’s institutional resilience. The bank has survived—and thrived—through leadership transitions before. But the manner of this exit exposed the fragility of the relationship between the board and the executive suite.

For Sashidhar Jagdishan, the path forward is now clearer—and lonelier. With Chakraborty’s departure, the board has effectively endorsed his leadership. Yet, the scrutiny from the RBI and SEBI, as well as the watchful eyes of global investors, will be intense. The bank has appointed external law firms to review the matter, a move that suggests a desire for transparency, but also one that opens the door to further disclosures .

In the end, the HDFC Bank episode serves as a reminder that in banking, trust is built over decades and can be shaken in minutes. Whether this moment becomes a footnote in the bank’s illustrious history or a turning point will depend on how quickly the institution can demonstrate that its governance is as robust as its balance sheet.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The February 2026 jobs report delivered the starkest labor market warning in months: nonfarm payrolls fell by 92,000 — far worse than any forecast — as federal workforce cuts, a major healthcare strike, and mounting AI-driven layoffs converged into a single, bruising data point.

The American jobs machine didn’t just stall in February. It reversed. The U.S. Bureau of Labor Statistics reported Friday that nonfarm payrolls dropped by 92,000 last month — a miss so severe it nearly doubled the worst estimates on Wall Street, which had penciled in a modest gain of 50,000 to 59,000. The unemployment rate climbed to 4.4%, up from 4.3% in January, marking the highest reading since late 2024.

The February 2026 jobs report doesn’t arrive in a vacuum. It lands at a moment of compounding economic pressures: a Federal Reserve frozen in a “wait-and-see” posture, geopolitical oil shocks from a new Middle East conflict, tariff uncertainty reshaping corporate hiring plans, and a relentless wave of AI-driven workforce restructuring. The convergence of all these forces — punctuated by what one economist called “a perfect storm of temporary drags” — produced a headline number that markets could not dismiss.

Equity futures reacted with immediate alarm. The S&P 500 fell 0.8% and the Nasdaq dropped 1.0% in the minutes after the 8:30 a.m. ET release. The 10-year Treasury yield retreated four basis points to 4.11% as investors rushed into safe-haven bonds, while gold rose 1% and silver 2%. WTI crude oil surged 6.2% to $86 per barrel, adding another layer of stagflationary pressure that complicates the Fed’s already knotted path.

What the February 2026 Nonfarm Payrolls Data Actually Shows

The headline figure — a loss of 92,000 jobs — is striking enough. But the full picture from the BLS Employment Situation report is considerably darker once the revisions are accounted for.

December 2025 was revised downward by a stunning 65,000 jobs, swinging from a reported gain of 48,000 to a loss of 17,000 — the first outright contraction in months. January 2026 was nudged down by 4,000, from 130,000 to 126,000. In total, the two-month revision erased 69,000 jobs from prior estimates. The three-month average payroll gain now stands at approximately 6,000 — essentially statistical noise. The six-month average has turned negative for the fourth time in five months.

“After lackluster job gains in 2025, the labor market is coming to a standstill,” said Jeffrey Roach, chief economist at LPL Financial. “I don’t expect the Fed to act sooner than June, but if the labor market deteriorates faster than expected, officials could cut rates on April 29.”

Sector Breakdown: Where the Jobs Disappeared

| Sector | February Change | Context |

|---|---|---|

| Health Care | –28,000 | Kaiser Permanente strike (31,000+ workers) |

| Manufacturing | –12,000 | Missed estimate of +3,000 |

| Information | –11,000 | AI-driven restructuring, 12-month trend |

| Transportation & Warehousing | –11,000 | Demand softening |

| Federal Government | –10,000 | Down 330,000 (–11%) since Oct. 2024 peak |

| Local Government | –1,000 | Partially offset by state gains |

| Social Assistance | +9,000 | Individual and family services (+12,000) |

The health care sector’s reversal is perhaps the most analytically significant. For much of 2025 and early 2026, health care was the single pillar keeping the headline payroll numbers out of outright contraction territory. In January it added 77,000 jobs. In February it shed 28,000 — a 105,000-job swing — primarily because a strike at Kaiser Permanente kept more than 30,000 nurses and healthcare professionals in California and Hawaii off the payroll during the BLS survey reference week. The labor action ended February 23, meaning the jobs will likely reappear in the March data, but the strike’s timing could not have been worse for February’s optics.

Federal government employment, meanwhile, continues its historic contraction. Federal government employment is down 330,000 jobs, or 11%, from its October 2024 peak Fox Business, a decline driven by the Trump administration’s aggressive reduction-in-force campaign. President Trump’s efforts to pare federal payrolls has seen a slide of 330,000 jobs since October 2024, a few months before Trump took office. CNBC

Manufacturing’s 12,000-job loss underscores the squeeze that elevated borrowing costs and trade-policy uncertainty are placing on goods-producing industries. Transportation and warehousing losses of 11,000 suggest logistics networks are already adjusting to softer demand expectations. The information sector’s 11,000-job decline continues a 12-month trend in which the sector has averaged losses of 5,000 per month — a structural signal, not a cyclical one, as artificial intelligence reshapes the contours of knowledge-work employment.

The Wage Paradox: Hot Pay, Cold Hiring

In an economy where the headline is undeniably weak, one data point stands out as paradoxically stubborn: wages.

Average hourly earnings increased 0.4% for the month and 3.8% from a year ago, both 0.1 percentage point above forecast. CNBC That combination — deteriorating employment alongside above-expectation wage growth — is precisely the stagflationary profile that gives the Federal Reserve its greatest headache. The Fed cannot simply cut rates to rescue the labor market if doing so risks reigniting the price pressures it has spent three years fighting.

The wage story is also deeply unequal. While higher-income wage growth rose to 4.2% year-over-year in February, lower- and middle-income wage growth slowed to 0.6% and 1.2% respectively — the largest gap since the beginning of available data. Bank of America Institute An economy where the well-paid are getting paid more while everyone else sees real-wage stagnation is not a healthy one, regardless of what the aggregate number says.

The household survey — which provides the unemployment rate and tends to be more sensitive to true labor-market stress — painted an even grimmer portrait. That portion of the report indicated a drop of 185,000 in those reporting at work and a rise of 203,000 in the unemployment level. CNBC The broader U-6 measure of underemployment, which includes discouraged workers and those involuntarily working part-time, came in at 7.9%, down 0.2 percentage points from January — a modest offset to the headline deterioration.

The Federal Reserve’s Dilemma

What the Jobs Report Means for Rate Cuts

Following the payrolls report, traders pulled forward expectations for the next cut to July and priced in a greater chance of two cuts before the end of the year, according to the CME Group’s FedWatch gauge of futures market pricing. CNBC

The Federal Reserve has been navigating a uniquely treacherous policy landscape. After cutting the federal funds rate to its current range of 3.50%–3.75%, it paused its easing cycle in early 2026 as inflation remained sticky above the 2% target and layoffs — despite slowing hiring — failed to produce the labor-market slack needed to justify further accommodation.

Fed Governor Christopher Waller said earlier in the morning that a weak jobs report could impact policy. “If we get a bad number, January’s revised down to some really low number… the question is, why are you just sitting on your hands?” Waller said on Bloomberg News. CNBC Waller has been among the minority of FOMC members pressing for near-term cuts. Friday’s data gave him considerably more ammunition.

San Francisco Fed President Mary Daly offered a characteristic note of caution. “I think it just tells us that the hopes that the labor market was steadying, maybe that was too much,” Daly told CNBC. “We also have inflation printing above target and oil prices rising. How long they last, we don’t know, but both of our goals are in our risks now.” CNBC

That dual-mandate tension — maximum employment under pressure, price stability still elusive — defines the central bank’s predicament heading into its next meeting.

Atlanta Fed GDPNow: A Warning Already Flashing

The jobs report doesn’t arrive as a surprise to those tracking the Atlanta Fed’s real-time growth model. The GDPNow model estimate for real GDP growth in the first quarter of 2026 was 3.0% on March 2 Federal Reserve Bank of Atlanta — a figure that already reflected softening in personal consumption and private investment. Critically, that pre-report estimate has not yet incorporated February’s job losses; Friday’s data will almost certainly pull the Q1 nowcast lower.

GDPNow had recently dropped to as low as –2.8% earlier in the current tracking period before recovering Charles Schwab, suggesting the model’s directional trajectory was already pointing toward deceleration even before the payroll shock. Whether the updated estimate breaks below zero again will be closely watched as a leading indicator of recession risk.

Is This a Recession Signal? A Closer Look

Temporary Shocks vs. Structural Deterioration

The intellectual debate emerging from Friday’s report centers on one critical distinction: how much of the 92,000-job loss is temporary, and how much is the economy genuinely breaking down?

The case for temporary distortion is real. Jefferies economist Thomas Simons called the result “a perfect storm of temporary drags coming together following an above-trend print in January.” CNBC The Kaiser Permanente strike alone subtracted roughly 28,000 to 31,000 jobs from the headline. Severe winter weather further depressed activity in construction and outdoor industries during the survey week. Both factors should partially reverse in March.

But the case for structural concern is equally compelling. “Looking through the weather-impacted sectors and the strike, which ended on February 23, this is still a poor jobs number,” Simons added. CNBC Strip out the healthcare strike and winter-weather effects and the underlying number is still deeply soft. Manufacturing lost 12,000 jobs without a weather excuse. Federal employment continues its unprecedented contraction. And the information sector’s ongoing slide reflects not a seasonal disruption but a multi-year rearchitecting of how corporations use labor in an age of generative AI.

“Still, the pace of job gains over the last few months is still dramatically slower than it was in 2024 and much of 2025 — this is going to make it harder for the Fed to sell the labor market stabilization narrative that’s been used to justify patience on further rate cuts. Add higher oil prices given conflict in the Middle East and renewed tariff uncertainty to the convoluted jobs market story, and you have a tricky, stagflationary mix of risks in the backdrop for the Fed,” Fox Business said one Ausenbaugh of J.P. Morgan.

What Happens Next: A Scenario Framework

Scenario A — Temporary Bounce-Back (Base Case): The Kaiser strike’s resolution and a weather reversal produce a March payroll rebound of 100,000–150,000. The Fed stays on hold through June, inflation data cools, and markets stabilize. Probability: ~45%.

Scenario B — Protracted Weakness (Risk Case): Federal workforce contraction deepens, manufacturing continues shedding jobs, and the three-month average payroll trend falls below zero outright. The Fed cuts rates in June or earlier. Recession risk climbs above 35%. Probability: ~35%.

Scenario C — Stagflationary Spiral (Tail Risk): Wage growth remains above 3.5%, oil sustains above $85, and tariff escalation drives goods-price inflation back above 3%. The Fed is paralyzed, unable to cut despite labor market deterioration. Dollar strengthens. Equity markets re-price earnings estimates lower. Probability: ~20%.

Global Ripple Effects

How the February 2026 US Jobs Report Moves the World

A weakening US labor market is not a domestic story. It travels — through capital flows, trade volumes, currency markets, and commodity demand — to every corner of the global economy.

Europe: The euro-area economy, which has been cautiously recovering from the energy crisis of 2023–2024, now faces the prospect of a softer US import demand picture just as its own manufacturing sector had begun to stabilize. The European Central Bank, which has already cut rates further than the Fed, finds its policy divergence potentially narrowing. A weaker dollar would provide some export-competitiveness relief to European firms, but it would also reduce the purchasing power of European consumers of dollar-denominated commodities like oil — of which Friday’s $86 WTI price is already a concern.

China and Emerging Markets: Beijing, which has been engineering its own modest stimulus program to stabilize growth at around 4.5%, will watch the US labor deterioration with some ambivalence. A slowing American consumer is a headwind for Chinese export sectors, particularly electronics, consumer goods, and industrial equipment. For dollar-denominated debt holders in emerging markets, however, any shift toward a weaker dollar — if the Fed is eventually forced to cut — would provide meaningful relief on debt-servicing costs.

Travel and Hospitality: The leisure and hospitality sector saw no notable job gains in February, continuing a pattern of stagnation in an industry still recalibrating from post-pandemic normalization. Expedia Group and other travel industry bellwethers will be monitoring whether consumer spending resilience — which has so far been concentrated among upper-income earners — can sustain international travel demand even as lower- and middle-income households face real-wage erosion. The risk is a bifurcated travel economy: business-class cabins full while economy-seat bookings slow.

The Bigger Picture: A Labor Market in Structural Transition

Zoom out far enough and February’s number is less a sudden rupture than the clearest confirmation yet of a trend that has been building for 18 months. Total nonfarm employment growth for 2025 was revised down to +181,000 from +584,000, implying average monthly job gains of just 15,000 — well below the previously reported 49,000. TRADING ECONOMICS An economy adding 15,000 jobs per month on average is not expanding its workforce in any meaningful sense; it is essentially flatlining.

Three structural forces are doing the work that cyclical headwinds once did:

Federal workforce reduction is real, large, and accelerating. A loss of 330,000 federal jobs since October 2024 is not a rounding error — it is a deliberate political restructuring of the size of the American state, with multiplier effects on contractors, lobbyists, lawyers, consultants, and the entire ecosystem of the Washington metropolitan area and beyond.

AI-driven labor displacement is moving from theoretical to measurable. The information sector’s 12-month average loss of 5,000 jobs per month reflects an industry actively substituting machine intelligence for human workers. Jack Dorsey’s announcement that Block would cut 40% of its payroll due to AI — cited in pre-report previews — was emblematic of a boardroom trend spreading well beyond Silicon Valley.

Healthcare dependency has masked the underlying weakness for too long. “One of the things that is very interesting-slash-potentially problematic is that we have almost all the growth happening in this health care and social assistance sector,” CNBC said Laura Ullrich of the Federal Reserve Bank of Richmond. When the single sector sustaining your jobs headline goes on strike, the vulnerability of the entire superstructure is suddenly visible.

Key Data Summary

| Indicator | February 2026 | January 2026 | Consensus Estimate |

|---|---|---|---|

| Nonfarm Payrolls | –92,000 | +126,000 (rev.) | +50,000–59,000 |

| Unemployment Rate | 4.4% | 4.3% | 4.3% |

| Avg. Hourly Earnings (MoM) | +0.4% | +0.4% | +0.3% |

| Avg. Hourly Earnings (YoY) | +3.8% | +3.7% | +3.7% |

| U-6 Underemployment | 7.9% | 8.1% | — |

| Dec. 2025 Revision | –17,000 | Prior: +48,000 | — |

| 10-Year Treasury Yield | 4.11% | ~4.15% | — |

| S&P 500 Futures | –0.8% | — | — |

The Bottom Line

February’s employment report is not a definitive verdict on the American economy. One month of data — distorted by a strike and abnormal weather — does not make a recession. But it does something arguably more important: it forces a serious reckoning with the possibility that the “stable but slow” labor market narrative that policymakers have been selling since mid-2025 was always more fragile than it appeared.

The Federal Reserve is now caught in a policy bind that will define the next six months of market psychology. Cut too soon and you risk re-igniting inflation in an economy where wages are still growing at 3.8%. Cut too late and you risk allowing a soft landing to become a hard one. The Fed’s March meeting was always going to be consequential. After Friday morning, it is indispensable.

The March jobs report — due April 3 — will be the next critical data point. If the healthcare bounce-back materializes and weather-related distortions reverse, the February number may be remembered as a noisy outlier. If it doesn’t, the conversation shifts from “when does the Fed cut?” to “can the Fed cut fast enough?”

For the full BLS Employment Situation data tables, visit bls.gov. For Atlanta Fed GDPNow real-time Q1 2026 tracking, see atlantafed.org.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance3 months ago

Markets & Finance3 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis2 months ago

Analysis2 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks3 months ago

Banks3 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment3 months ago

Investment3 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Analysis2 months ago

Analysis2 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Asia3 months ago

Asia3 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Global Economy3 months ago

Global Economy3 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy3 months ago

Global Economy3 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis