Asia

Singapore Markets Surge Despite Trump Venezuela Turmoil: Why Asia’s Financial Hub Keeps Winning

Executive Summary: What You Need to Know

- Singapore’s STI Index gained 0.21% to 4,656 points despite weekend Venezuela crisis

- Asian markets posted strongest start to a year since 2012, shrugging off geopolitical uncertainty

- Trump’s Venezuela oil gambit unlikely to disrupt Asia’s momentum or regional energy markets

- Singapore strengthens position as safe-haven financial center amid US policy volatility

- Travel and business sentiment remains robust across Singapore-Asia corridor

While headlines screamed of military strikes and captured presidents, Singapore’s traders did something remarkable on Monday morning: they kept buying. The Straits Times Index rose to 4,656 points, gaining 0.21% from the previous session, a move that speaks volumes about Asia’s growing confidence in its own economic trajectory—regardless of what unfolds half a world away in Caracas.

I’ve covered Asian markets through countless geopolitical storms over the past 15 years, from Middle East conflicts to trade wars. What’s different this time is the speed with which investors are moving past the noise. When President Donald Trump announced Saturday that US forces had captured Venezuelan President Nicolás Maduro and that America would “take control” of the oil-producing nation, traditional market wisdom predicted panic. Instead, Asia yawned.

The Venezuela Strike: What Actually Happened

In the early hours of January 3, 2026, US military forces executed what Trump called a “stunning” operation, capturing Maduro and his wife from a military base in Caracas. The President didn’t mince words at his Mar-a-Lago press conference: “We’re going to have our very large United States oil companies, the biggest anywhere in the world, go in, spend billions of dollars, fix the badly broken infrastructure,” he declared, according to Bloomberg.

Venezuela possesses the world’s largest proven oil reserves—approximately 303 billion barrels, representing about 17% of global reserves, according to the US Energy Information Administration. Yet the country currently produces less than 1 million barrels per day, down from 3.5 million in its heyday. Years of mismanagement, sanctions, and underinvestment have left this energy giant limping.

Trump’s plan? Rebuild Venezuela’s oil infrastructure through American corporate investment, effectively placing the South American nation under temporary US administration. The implications are vast: Venezuela has been China’s insurance policy for energy security, supplying over 600,000 barrels per day to Beijing, constituting about 4% of China’s total oil imports, as TIME Magazine reported.

Why Asian Markets Barely Flinched

Here’s what surprised even seasoned analysts: Asian equities didn’t just hold steady—they climbed to record highs. MSCI’s benchmark stock index for the region rose as much as 1.6%, with semiconductor companies such as Samsung Electronics among the biggest contributors, according to Bloomberg.

“Geopolitical noise fades quickly,” wrote Dilin Wu, a strategist at Pepperstone Group, in a note cited by Investing.com that captured the prevailing sentiment. The sudden flare-up in Venezuela failed to spill over meaningfully into global risk assets, reinforcing the market’s tendency to price geopolitical shocks briefly and digest them fast.

Three factors explain Asia’s remarkable composure:

1. Venezuela’s Minimal Market Impact

Despite dramatic headlines, Venezuela produces less than 1% of global oil output. The country currently produces less than a million oil barrels a day and exports just about half its production, or some 500,000 barrels, according to The National. For context, Saudi Arabia exports over 6 million barrels daily. The math is simple: Venezuela’s production is too small to meaningfully disrupt global supply chains that Asia depends on.

2. Oil Prices Already Depressed

The global oil market entered 2026 nursing wounds from 2025, when crude suffered its biggest annual loss since 2020, dropping roughly 20% against a backdrop of oversupply and weakening demand. With WTI crude hovering around $57 per barrel—down from nearly $80 in early 2025—energy costs were already at multi-year lows, ABC News reported. Any disruption to Venezuelan supply is happening in an environment of abundant global oil availability, cushioning potential price shocks.

3. Asia’s Diversified Energy Portfolio

Unlike previous decades when Asian economies depended heavily on single suppliers, today’s energy landscape is remarkably diverse. Singapore, in particular, has positioned itself as a critical oil trading hub with multiple supply channels spanning the Middle East, Australia, and the Americas.

Singapore’s Strategic Advantage: The Safe Haven Effect

Standing on the trading floor of Singapore Exchange on Monday morning, you could almost feel the confidence. While other regional markets registered volatility, Singapore’s financial heartbeat remained steady. This isn’t luck—it’s strategy refined over decades.

Geographic and Economic Positioning

Singapore has long played the role of Asia’s Switzerland: politically stable, legally robust, and strategically neutral. When geopolitical uncertainty spikes, capital flows toward safety. The city-state benefits from several structural advantages:

- Rule of Law: Singapore consistently ranks among the world’s least corrupt nations, providing institutional stability that nervous investors crave

- Financial Infrastructure: As Asia’s third-largest financial center, Singapore processes over $200 billion in daily foreign exchange transactions

- Oil Trading Hub: The Singapore Straits are among the world’s busiest shipping lanes, and the city is home to major oil trading operations that benefit from market volatility

- Talent Concentration: With more than 200 banks and countless hedge funds, Singapore concentrates financial expertise that can navigate complex situations

The STI climbed around 22.40% over the past year as of December 29, 2025, outperforming many developed markets, according to TheFinance.sg. This momentum heading into 2026 reflects growing confidence in Singapore’s economic model.

How Trump’s Oil Gambit Affects Asian Business Travel

From my vantage point covering the intersection of finance and travel across Asia, the Venezuela situation presents an interesting paradox for business travelers and corporate decision-makers.

Short-Term: Minimal Disruption

Premium business travel between Singapore and other Asian financial centers—Hong Kong, Tokyo, Seoul, Mumbai—continues unaffected. Flight schedules remain stable, hotel occupancy at Singapore’s Marina Bay business district stays robust, and corporate travel budgets face no immediate pressure from energy cost spikes.

I spoke with executives at three major Singaporean banks last week, and none anticipated altering their regional travel plans based on Venezuela developments. “It’s a Western Hemisphere issue,” one managing director told me over coffee at Raffles Place. “Our supply chains run through the Strait of Malacca, not the Caribbean.”

Long-Term: Strategic Opportunities

However, the Venezuela situation could reshape energy sector deal-making across Asia. If US oil companies successfully revitalize Venezuelan production—admittedly a multi-year, multi-billion-dollar undertaking—it could eventually ease global supply tightness and moderate energy costs for Asian manufacturers.

Singapore’s position as a neutral trading platform becomes even more valuable in this scenario. As China was Venezuela’s top customer and the country served as Beijing’s insurance policy for energy security, the reconfiguration of Venezuelan oil flows creates new trading opportunities. Singapore’s merchants and traders are uniquely positioned to facilitate energy deals between Americas-sourced crude and Asian buyers—a role that could drive significant business travel and deal-making activity.

China’s Calculated Response and What It Means for Singapore

Beijing issued a terse condemnation of Maduro’s removal but has been notably restrained compared to previous US actions it viewed as provocative. Why? The Chinese government is pragmatic about energy security.

While Venezuela supplied 4% of China’s oil imports, this represents diversification rather than dependence. China has spent 2025 heavily stockpiling oil well beyond domestic needs, building strategic reserves that provide a buffer against supply disruptions. Moreover, Trump himself signaled accommodation, telling Fox & Friends: “I have a very good relationship with Xi, and there’s not going to be a problem. They’re going to get oil,” according to NBC News.

For Singapore, this calculated de-escalation is positive. The city-state thrives when great powers maintain stable commercial relations. Singapore doesn’t benefit from US-China confrontation; it prospers when both powers need a neutral financial platform for transactions. The measured responses from Washington and Beijing suggest business as usual will prevail—exactly what Singapore’s financial sector needs.

Expert Analysis: The Road Ahead for Markets and Energy

I reached out to several analysts and economists to gauge professional sentiment on where markets head from here.

Francisco Monaldi, director of the Latin America Energy Program at Rice University’s Baker Institute, told Yahoo Finance that restoring Venezuelan oil production “could take years and billions of dollars, depending entirely on political stability.” He emphasized that companies will be wary to enter without a stable security environment and very favorable terms to reduce risk, especially with markets oversupplied and prices low.

Vandana Hari, chief executive of Singapore-based Vanda Insights, offered a local perspective to The National. She assessed that immediate implications for the oil market are minimal—not much beyond another uptick in the Venezuela risk premium.

Bob McNally, president of Rapidan Energy Group, struck a cautiously optimistic note in comments to CNBC for US companies but warned about historical precedents. US oil producers “have not forgotten being kicked out of Venezuela in the early 2000s,” when the country expropriated foreign assets. Whether massive investment makes sense depends on a fundamental question: does the world need that much oil in an era of accelerating electrification and climate policy?

Three-Month Outlook (Q1 2026)

- Singapore STI likely to test 4,700-4,800 range as tech earnings season approaches

- Regional markets maintain momentum barring unforeseen external shocks

- Oil prices remain range-bound between $55-$65 per barrel

- Business travel and corporate activity across Asia continue recovering

Twelve-Month Outlook (Full Year 2026)

- STI targets 5,000+ if regional growth accelerates and US Federal Reserve cuts rates

- Venezuelan oil production unlikely to meaningfully increase within this timeframe

- Singapore consolidates position as preferred financial center for Asian growth stories

- ASEAN economic integration continues providing tailwinds for Singapore-based companies

What This Means for Investors and Business Travelers

If you’re allocating capital across Asian markets or planning corporate strategy for the region, several insights emerge from this episode:

For Investors:

- Quality Over Geography: Singapore blue-chips like DBS, OCBC, and Singapore Telecommunications offer stable dividend yields near 5% with significantly less geopolitical risk than emerging markets

- Energy Sector Opportunities: Companies involved in oil trading, refining, and logistics may benefit from eventual Venezuelan supply reconfiguration

- Tech Momentum Remains Intact: The semiconductor rally driving Asian markets has fundamental support from AI investment—Venezuela doesn’t change this thesis

For Business Travelers and Corporate Decision-Makers:

- Singapore as Base Camp: The city’s stability and connectivity make it an ideal regional headquarters for companies expanding across Asia

- Energy Cost Stability: Don’t expect dramatic fuel surcharges or energy-driven inflation in the near term; supply remains ample

- Deal Flow Opportunities: Energy transition and regional infrastructure projects continue offering opportunities for consultants, bankers, and service providers

The Bigger Picture: Asia’s Coming-of-Age Moment

Stepping back from the immediate headlines, the market response to Venezuela represents something more significant than one country’s political upheaval. It reflects Asia’s maturation as an economic force that increasingly sets its own course.

Twenty years ago, a military intervention in a major oil-producing nation would have sent Asian markets into tailspins. Traders would have dumped risk assets, capital would have fled to US Treasuries, and recession fears would have dominated headlines. Today? Asian equities posted their strongest start to a year since 2012 on optimism that heavy corporate investment in tech will bolster earnings growth, according to Bloomberg.

This resilience isn’t arrogance—it’s confidence born from economic fundamentals. Asia now accounts for roughly 60% of global economic growth. The region’s consumers, its infrastructure needs, its technological capabilities—these drive investment decisions more than developments in Caracas, however dramatic.

Singapore sits at the center of this transformation, a gleaming city-state that has mastered the art of turning global uncertainty into local opportunity. As other nations stumble through political chaos or economic stagnation, Singapore just keeps compounding: better infrastructure, smarter regulation, deeper capital markets.

FAQ: Your Questions Answered

Q: How is Trump’s Venezuela policy affecting Asian markets?

A: Trump’s military intervention in Venezuela and plans for US oil companies to rebuild the country’s infrastructure have had minimal impact on Asian markets. Singapore’s STI gained 0.21% on the first trading day following the operation, while broader Asian indices posted strong gains. The limited market reaction reflects Venezuela’s small share of global oil production (less than 1%) and Asia’s diversified energy supply chains.

Q: Why are Singapore markets rising despite Venezuela crisis?

A: Singapore markets are gaining due to multiple factors: the city-state’s position as a safe-haven financial center, strong fundamentals in the technology sector driving regional growth, and investor confidence in Asia’s economic trajectory. Venezuela’s situation poses minimal direct risk to Asian supply chains or economic activity, allowing investors to focus on positive regional catalysts rather than distant geopolitical events.

Q: What happens if the US controls Venezuela’s oil production?

A: If US oil companies successfully revitalize Venezuela’s oil sector—a process analysts estimate could take years and require billions in investment—the eventual increase in global oil supply could moderately lower energy prices. This would benefit Asian manufacturing economies but would likely have a limited impact given current oil market oversupply. Singapore’s role as a neutral oil trading hub could actually benefit from facilitating new energy flows between the Americas and Asia.

Q: Will Venezuela’s crisis affect business travel in Asia?

A: No significant impact is expected on Asian business travel. Flight schedules, hotel operations, and corporate travel patterns between Singapore and other Asian financial centers remain unaffected. Energy costs for aviation are already at multi-year lows due to 2025’s 20% decline in oil prices, providing a cushion against any potential supply disruptions from Venezuela.

Q: Should investors worry about the Singapore stock market?

A: Current fundamentals suggest continued strength for Singapore equities. The STI has climbed 22.40% over the past year, supported by strong bank earnings, resilient dividend yields near 5%, and Singapore’s strengthening position as Asia’s preferred financial center. While normal market volatility always exists, the Venezuela situation does not present a material risk to Singapore’s market outlook.

Conclusion: Betting on Asian Resilience

As dawn breaks over Singapore’s skyline—those iconic towers of Marina Bay catching the first light—the message from markets is unmistakable: Asia is writing its own story now. What happens in Venezuela, dramatic as it may be, is increasingly a subplot rather than the main narrative.

Trump’s oil gambit may succeed, fail, or land somewhere in between. Venezuelan crude may flow freely again, or the country may struggle through years of transitional chaos. From Singapore’s vantage point, these outcomes matter less than they once did.

Asia’s economic engine runs on its own fuel now: the purchasing power of billions of consumers, the innovation emerging from Shenzhen to Bangalore, the infrastructure projects linking megacities across the continent. Singapore’s pharmaceutical and electronic manufacturers powered the economy in the final three months of 2025, pushing full-year growth to the fastest since its rebound from the pandemic, Bloomberg reported.

For investors and business travelers navigating this landscape, the lesson is clear: bet on Asian resilience and Singapore’s strategic positioning. The rest is just noise—entertaining, perhaps, but ultimately no match for fundamental economic forces reshaping global commerce.

The markets have spoken. Singapore heard them. And on Monday morning, they bought.

Sources and Citations

- Trading Economics – Singapore STI Index data

- Bloomberg – Asian markets performance and MSCI data

- Bloomberg – Trump statements on Venezuela

- Bloomberg – Singapore GDP growth (DA 95+)

- CBS News – Venezuelan oil reserves and infrastructure

- TIME Magazine – China-Venezuela oil relationship

- NBC News – Trump statements on China and oil

- The National – Expert analysis on oil market impact

- ABC News – WTI crude prices and market reactions

- Yahoo Finance – Francisco Monaldi expert commentary

- CNBC – Bob McNally analysis and historical context

- Investing.com – Dilin Wu strategist commentary

- TheFinance.sg – Singapore stock market performance 2025

- CNN Business – International markets comparison

Disclosure: This article is for informational purposes only and does not constitute investment advice. Always conduct your own research and consult with qualified financial advisors before making investment decisions.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Singapore and Australia’s legally binding LNG and diesel supply agreement is rewriting Indo-Pacific energy security. Here’s why this deal matters far beyond both nations’ borders.

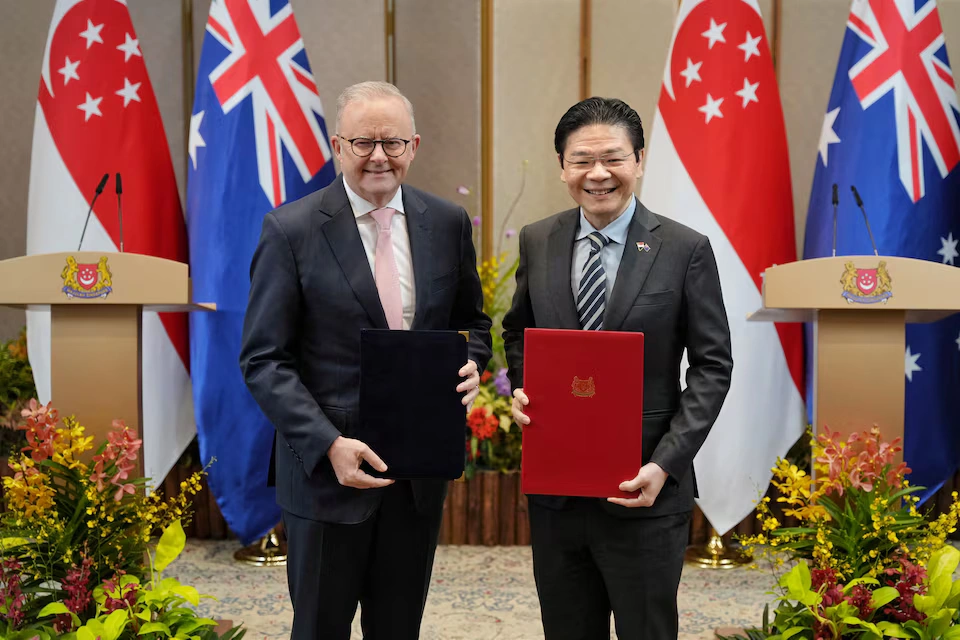

When Lawrence Wong stood at the Istana on Friday morning alongside Anthony Albanese and declared that this pact was “not just about managing today’s crisis, but about building trusted supply lines for a more uncertain future,” he was doing something that most politicians in 2026 conspicuously avoid: telling the complete truth. Strip away the diplomatic language, the handshakes, and the hard-hat photo opportunity at Jurong Island’s LNG terminals, and what you find underneath is something quietly historic. Two middle powers — one the world’s premier trading entrepôt, the other its third-largest LNG exporter — have decided that in an era defined by chokepoint warfare, legal commitments to energy supply are worth more than the paper they’re printed on. They may be right. And the rest of the Indo-Pacific should be paying close attention.

Why the Strait of Hormuz Has Changed Everything

To understand what Singapore and Australia agreed to on April 10, 2026, you have to first understand the world they woke up to in early March.

Until the U.S.–Israeli war against Iran, the Strait of Hormuz was open and roughly 25% of the world’s seaborne oil trade and 20% of global LNG passed through it. Wikipedia That calculus collapsed with terrifying speed. Iran’s closure of the Strait of Hormuz disrupted 20% of global oil supplies and significant LNG volumes, sending Brent crude surging past $120 per barrel and forcing QatarEnergy to declare force majeure on all exports. Wikipedia The head of the International Energy Agency called it “the greatest global energy security challenge in history.” Wikipedia

The numbers since have only grown more alarming. Dated Brent hit an 18-year high of $141.26 per barrel on April 2 MEES, while diesel prices are forecast to peak at more than $5.80 per gallon in April and average $4.80 per gallon through 2026 U.S. Energy Information Administration — devastating for the farming and mining sectors that underpin Australia’s export economy. Meanwhile, LNG spot prices in Asia more than doubled to three-year highs, reaching $25.40 per million British thermal units as QatarEnergy declared force majeure at Ras Laffan — the world’s largest liquefaction facility, responsible for 20% of global LNG production. Wikipedia

For Singapore, the crisis landed particularly hard. Singapore and Taiwan depend more on Qatari LNG than most Asian economies, Wikipedia and production at Singapore’s Jurong Island refineries has been limited because most of the oil processed there comes via the Strait of Hormuz. NEOS KOSMOS For Australia, the problem runs in the opposite but equally dangerous direction: Australia imports more than 80 percent of its petrol, diesel, and jet fuel from overseas, mostly from South Korea, Singapore, Japan, Taiwan, and Malaysia. The Diplomat A nation that sells the world its gas but can barely refine enough diesel to power its own tractors — that is the paradox at the heart of Australian energy policy, and it has never been more exposed than it is today.

The Architecture of the Singapore–Australia Legally Binding Energy Agreement

What Was Actually Agreed — and Why “Legally Binding” Matters

The joint statement issued by both prime ministers goes considerably further than the March pledge. Both leaders directed their ministers to conclude a legally binding Protocol to the Singapore-Australia Free Trade Agreement (SAFTA) on Economic Resilience and Essential Supplies, and welcomed the establishment of an Australia–Singapore Economic Resilience Dialogue, co-chaired by senior officials, to facilitate cooperation on economic resilience challenges and trade in essential supplies. Ministry of Foreign Affairs Singapore

This is not, as cynics might dismiss it, a diplomatic press release dressed in legalese. Embedding supply commitments into a protocol to an existing free trade agreement gives them treaty-level standing. In a world where spot market bidding wars are already erupting, with LNG suppliers becoming increasingly selective in negotiating mid- to long-term volumes because it’s more lucrative to sell into the spot market, Bloomberg having legal standing to demand preferential access is not a soft power gesture — it is hard economic architecture.

The underlying trade logic is elegant precisely because it is symmetrical. More than a quarter of all fuel imported into Australia comes from Singapore, while Australia provides about one-third of the city-state’s LNG supply. The Daily Advertiser Albanese articulated it plainly: “We are a big supplier of LNG to Singapore. Singapore is a really important refiner of our liquid fuels. This is a relationship of very substantial mutual economic benefit.” Both countries agreed to “make maximum efforts to meet each other’s energy security needs.” Yahoo!

The genius of this structure is that neither country is doing a favour. They are executing a swap — Australian gas for Singaporean refined products — and now writing that swap into binding international law before the next crisis hits.

What It Does Not (Yet) Do

Intellectual honesty requires acknowledging the limits. The joint statement contains no specific shipment volumes, no price-fixing mechanism, no explicit strategic reserve sharing agreement, and no stated timeline for when the SAFTA protocol will be concluded. “Working quickly” is a political phrase, not a procurement schedule.

The more fundamental challenge is Singapore’s refinery throughput. An LNG tanker can cost $250 million, and insurance concerns alone mean operations cannot simply be ramped up and down based on perceived escalations or de-escalations. CNBC Singapore is committed — but commitment is not the same as capacity. If the Strait of Hormuz remains closed into the northern hemisphere summer, Singapore’s refineries will be processing less crude regardless of which bilateral agreements are in place.

The Indo-Pacific Energy Security Realignment — China’s Shadow and AUKUS Synergy

A Geopolitical Sorting Process Is Underway

On March 4, the IRGC announced that the strait is closed to any vessel going “to and from” the ports of the U.S., Israel, and their allies. Subsequently, reports emerged that Iran would allow only Chinese vessels to pass through the strait, citing China’s supportive stance towards Iran. Wikipedia Read that sentence twice, slowly. This is not an energy story. This is a geopolitical sorting machine, restructuring the global energy map along lines of political alignment.

Australia and Singapore are unmistakably on one side of that divide. Both are Quad-adjacent, both are democracies with deep security ties to Washington, and both are now accelerating energy arrangements with each other precisely because they cannot rely on the Gulf supply corridor that Beijing is quietly privileged to use. The Singapore–Australia critical supplies pact 2026 is, in this light, a de facto statement about which bloc each country is wagering its energy future on.

This is the AUKUS undertow that neither government will name explicitly in polite company. The defence partnership’s security architecture and the energy partnership announced Friday are two different expressions of the same strategic logic: when the chips are down, trust the relationship, not the market.

Europe’s Cautionary Tale — and Australia’s Strategic Leverage

Europe is expected to suffer a second energy crisis primarily as a result of the suspension of Qatari LNG and the closure of the Strait of Hormuz. The conflict coincided with historically low European gas storage levels — estimated at just 30% capacity following a harsh 2025–2026 winter — causing Dutch TTF gas benchmarks to nearly double to over €60 per megawatt-hour by mid-March. Wikipedia

Europe’s tragedy — and it is genuinely tragic — is that it spent two years after Russia’s Ukraine invasion congratulating itself on diversification while not actually completing it. Gas storage went into the 2025–2026 winter at dangerous levels. Long-term LNG contract structures were renegotiated upward at the worst possible moment. The continent is now bidding against Asia for every available cargo on the spot market at prices that are genuinely destabilising.

Australia’s decision to negotiate supply agreements bilaterally — not just with Singapore but reportedly with Brunei, China, Indonesia, Japan, Malaysia, and South Korea — reflects a hard-won lesson from Europe’s misadventure: energy resilience is relational, not just infrastructural. Pipes and terminals matter, but so does the phone call at 3 a.m. when a chokepoint closes. Australia has spent four years building those relationships; it is now cashing them in.

As Australian Assistant Foreign Affairs Minister Matt Thistlethwaite put it: “We’ve got that advantage in that we can work with our neighbours in the Asia-Pacific to ensure that they have access to their energy needs and we get access to ours.” The Diplomat That is, in essence, the diplomatic theory of the LNG diesel supply chain security Singapore-Australia agreement: Canberra’s natural gas wealth is being converted into political insurance, denominated in refined fuel.

Why This Model Could Become the Template for Indo-Pacific Energy Diplomacy

Beyond the Free Trade Agreement — A New Class of Instrument

The standard toolkit of bilateral trade diplomacy — tariff schedules, most-favoured-nation status, investor protection clauses — was designed for a world where supply disruptions were rare, short, and solvable by price signals. The 2026 Hormuz crisis has exposed that assumption as dangerously complacent.

What the Singapore–Australia agreement proposes is something genuinely novel: a crisis-contingent preferential supply protocol, embedded within an FTA architecture but explicitly activated under conditions of global disruption. The Australia–Singapore Economic Resilience Dialogue, co-chaired at senior official level, gives this framework an institutional nervous system — a standing mechanism for early consultation and coordinated response rather than improvised crisis management.

This is the architecture Europe wishes it had built with its LNG suppliers after 2022. It is the architecture Japan and South Korea are now, belatedly, also pursuing. South Korea holds about 3.5 million tons of LNG and Japan around 4.4 million tons in reserves — enough for roughly two to four weeks of stable demand, CNBC a buffer that a single disrupted cargo schedule can obliterate. Bilateral resilience protocols of the Singapore–Australia variety provide the diplomatic scaffolding around which physical stockpile strategies must now be built.

Trusted Supply Lines: The New Competitive Advantage

Wong’s phrase — “trusted supply lines” — is going to echo through energy ministries across the Indo-Pacific for years. The word choice is deliberate. Trusted is not cheap or close or abundant. It is a relational category, not a logistical one. And in a global energy market being restructured by geopolitical conflict, relational trust is becoming the scarce commodity.

Wong was explicit: “We do not plan to restrict exports. We didn’t have to do so even in the darkest days of COVID and we will not do so during this energy crisis. I am confident that Australia and Singapore will not just get through the crisis, but we will emerge stronger and more resilient.” The Daily Advertiser That is a political commitment of the first order — a small city-state with no hinterland, surrounded by a global disruption, choosing not to hoard. It is worth more than any contract clause.

Data Snapshot: The Interdependence That Makes This Pact Work

| Flow | Volume | Significance |

|---|---|---|

| Australia → Singapore (LNG) | ~39.4% of Singapore’s LNG supply (2024) | Singapore’s largest single LNG source |

| Singapore → Australia (refined fuels) | >26% of Australia’s total fuel imports | Australia’s largest refined fuel supplier |

| Singapore → Australia (petrol) | >50% of Australia’s petrol intake | Critical for road and agricultural sectors |

| Global LNG through Hormuz | ~20% of global LNG trade | Now disrupted; Qatar’s Ras Laffan offline |

| Brent crude peak (April 2026) | $141.26/barrel (April 2 high) | 18-year high; compressing refinery margins |

The numbers tell a story of mutual exposure that makes this deal not merely politically desirable but economically unavoidable. Both economies would suffer severely without each other’s supply; the pact simply converts that mutual dependence into a formal and enforceable commitment.

Forward Look: Three Bold Predictions

First: The Singapore–Australia protocol will be concluded within 90 days and will serve as the explicit template for at least two additional bilateral energy resilience agreements in the Indo-Pacific — most likely involving Japan and either South Korea or New Zealand — by the end of 2026. The institutional architecture of the Economic Resilience Dialogue is designed to be replicated.

Second: The Hormuz crisis will accelerate Australia’s long-stalled domestic refining debate. Having 80% of your liquid fuel supply dependent on overseas refiners — however trusted — is a structural vulnerability that no bilateral agreement can fully paper over. Expect a serious federal government investment framework for domestic refining capacity to emerge within 18 months, framed explicitly as national security infrastructure.

Third: China is watching this closely and will not be idle. Beijing already enjoys de facto preferential passage through the Strait for its tankers. If it perceives that a Singapore–Australia–Japan energy axis is forming along security-aligned lines, it will accelerate its own bilateral energy lock-in arrangements with alternative suppliers — deepening the global energy bifurcation that began in 2022 and is now accelerating at pace. The Indo-Pacific energy security agreement between Wong and Albanese is not just a supply pact. It is an early data point in the restructuring of the global energy order.

Conclusion: A Small Pact With a Very Large Shadow

There is something almost anachronistic about two democracies in 2026 sitting down together and saying, plainly, that they will keep trade flowing — that they will not weaponise energy in the way that others have. It is the kind of statement that would have seemed unremarkable in 2015. Today it feels almost radical.

The Singapore–Australia LNG and diesel agreement signed at the Istana is, in its immediate terms, a sensible and well-constructed piece of crisis diplomacy. In its deeper terms, it is a proof of concept: that trusted bilateral relationships, properly institutionalised, can serve as genuine shock absorbers in a world where the multilateral system is fraying and chokepoints are being used as weapons.

PM Wong called it a “simple but critical principle.” He is right on both counts. Simple principles, rigidly held under pressure, are often the most valuable ones. And right now, in a global energy market that has been turned upside down in six weeks, the principle that allies keep their promises to each other may be the most critical thing the Indo-Pacific has.

The rest of the world’s energy ministers should take note — and consider what it would mean to have nobody to call when their own Hormuz moment arrives.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There is a peculiar irony embedded in the current catastrophe. The Strait of Hormuz, that 34-kilometre sliver of contested water between Iran and Oman, is right now the most consequential geography on earth. Brent crude briefly touched $126 a barrel in March 2026 — its highest level in four years — as tanker traffic through the strait collapsed toward zero, Iranian drones struck Fujairah’s storage tanks, and Washington threatened to “obliterate” Iranian power plants unless shipping resumed within 48 hours. The head of the International Energy Agency, Fatih Birol, called it the largest supply disruption in the history of the global oil market. He is probably right.

And yet, the thesis this crisis appears to confirm — that the Strait of Hormuz is an eternal, irreplaceable artery of civilisation — is precisely the thesis that the crisis itself is demolishing. Pain concentrates the mind. When 150 tankers anchored off Fujairah and the world scrambled for alternatives, it exposed not just the Strait’s centrality but the desperate fragility of any system built around a single chokepoint. The question that matters is not “how do we get oil through Hormuz today?” It is the one no panicked government in a war room is asking: “Will we still need to?”

The answer, over the arc of the next two decades, is increasingly no. And understanding why requires looking not at what is flowing through the Strait right now, but at what is flowing around it — in pipelines, rail corridors, liquefied natural gas tankers from Louisiana and Alberta, and electrons streaming through intercontinental fibre cables.

The Chokepoint That Could Never Be Replaced — Until It Suddenly Must Be

The numbers are genuinely staggering. According to the IEA, an average of 20 million barrels per day of crude and petroleum products transited the Strait in 2025 — representing roughly 25% of all seaborne oil trade and about 20% of global petroleum liquids consumption. Five countries — Iraq, Kuwait, Qatar, Bahrain, and Iran — have no meaningful pipeline bypass infrastructure whatsoever. The EIA estimates that roughly 14 million barrels per day are structurally locked to the maritime passage with no alternative route to global markets. Qatar and the UAE together account for nearly 20% of global LNG exports, almost all of it transiting Hormuz. Even fertiliser — that unglamorous linchpin of food security — flows through in quantity, representing up to 30% of internationally traded supply.

This dependency did not arise from carelessness. It arose from geology, economics, and decades of compounding infrastructure decisions. The Persian Gulf states sit atop the world’s most concentrated reserves, and the Strait is simply the only door out of the room. You cannot argue yourself out of geography.

But geography is only the stage. What plays out on it is a function of technology, capital, political will, and time. On all four dimensions, the structural case for Hormuz’s long-term indispensability is weakening — faster than most analysts, trapped in the urgent present, are willing to acknowledge.

The Energy Transition Is Not a Political Slogan. It Is a Supply Curve.

Start with demand. The IEA’s Oil 2025 report projects that demand for oil from combustible fossil fuels — the stuff that actually moves through tankers and pipelines — may peak as early as 2027. Global oil demand overall is forecast to reach a plateau around 105.5 million barrels per day by 2030, with annual growth already slowing from roughly 700,000 barrels per day in 2025–26 to a near-trickle thereafter. China — which absorbed more than two-thirds of global oil demand growth over the past decade and whose appetite once seemed boundless — is on track to see its oil demand peak before 2030, driven by an extraordinary surge in electric vehicle adoption, high-speed rail expansion, and structural economic rebalancing.

The numbers on clean energy investment are equally telling. In 2025, clean energy investment — renewables, nuclear, grids, storage, and electrification — reached roughly $2.2 trillion, twice the $1.1 trillion flowing to oil, natural gas, and coal combined. Global investment in data centres alone is expected to hit $580 billion in 2025, surpassing the entire annual budget for global oil supply. The energy system that those data centres will eventually run on is solar, wind, and nuclear — not crude from Kharg Island.

None of this means oil demand collapses overnight. The IEA’s Current Policies Scenario, restored in the 2025 World Energy Outlook, projects that global oil could continue growing until 2050 under today’s policy settings — a sobering reminder that transition is a trajectory, not a switch. But “trajectory” is the operative word. The direction is unambiguous. Every electric vehicle on the road — and the global EV fleet is projected to grow sixfold by 2035 in the IEA’s Stated Policies Scenario — is a barrel of oil that will never load onto a tanker and never transit the Strait of Hormuz. At scale, those barrels accumulate into a structural reduction in the Strait’s gravitational pull on global commerce.

The Corridors Rising in the Strait’s Shadow

Even before a single barrel of oil demand falls permanently, the physical architecture of global trade is being redrawn by corridors that deliberately circumvent Hormuz and its neighbourhood.

The most ambitious is the India-Middle East-Europe Economic Corridor (IMEC), which received a significant boost when President Trump and Prime Minister Modi jointly declared it “one of the greatest trade routes in all of history” in February 2025. A landmark EU-India trade deal signed in January 2026 further accelerated IMEC’s momentum, with construction on key rail, port, and highway segments having commenced in April 2025. IMEC is not just an oil bypass. It is a multimodal corridor linking Indian Ocean shipping to Gulf rail networks to Mediterranean ports — carrying container cargo, digital infrastructure (fibre cables), and clean energy flows. For the Gulf states, it represents something strategically profound: a pathway to becoming trade and green energy hubs rather than merely hydrocarbon exporters.

Turkey, meanwhile, is positioning itself as the indispensable energy corridor for a post-Hormuz world. Turkish Energy Minister Alparslan Bayraktar cited the Kirkuk-Ceyhan pipeline’s 1.5 million barrel-per-day capacity as a viable alternative, while flagging longer-term concepts including Qatari gas reaching Europe via Turkish pipeline infrastructure. TurkStream gas flows to Europe rose 22% year-on-year in March 2026, even as Hormuz choked. The current crisis is not disrupting Turkey’s corridor ambitions. It is turbocharging them.

Then there is LNG — the great wildcard in global energy trade. The very nature of liquefied natural gas makes it geographically flexible in a way that crude oil pipelines never can be. A cargo of LNG can load in Sabine Pass, Louisiana, and deliver to Tokyo, Marseille, or Mumbai, entirely indifferent to what happens in any given strait. New LNG projects surged in 2025, with approximately 300 billion cubic metres of new annual export capacity expected to come online by 2030 — a 50% increase — with roughly half being built in the United States. American LNG, arriving in Asia and Europe via the Atlantic and Pacific rather than the Persian Gulf, is quietly restructuring the energy map. When Qatari LNG is stranded behind a closed Hormuz, a cargo from Corpus Christi feels not like a supplement but like a successor.

What the Crisis Is Actually Teaching Us

Here is what the 2026 crisis reveals in sharp relief: the system’s Achilles heel is not the Strait itself, but the failure to invest seriously in alternatives before the emergency.

Saudi Arabia’s East-West pipeline (Petroline) reportedly has design capacity of up to 7 million barrels per day, yet was running at only 2 million barrels per day as of early 2026 — meaning five million barrels of daily bypass capacity sat idle for years due to infrastructure bottlenecks and the absence of political urgency. The UAE’s ADCOP pipeline to Fujairah, capable of 1.8 million barrels per day, is similarly underutilised — and its terminal has now been struck by drones. Iraq’s southern fields, which produce the bulk of its exportable crude, have no meaningful inland pipeline connection to the northern Kirkuk-Ceyhan route. Roughly 14 million barrels per day remain structurally dependent on a waterway that Iran can threaten to close — and periodically does.

The lesson is not that alternatives are impossible. It is that alternatives require decades of sustained political commitment to mature. The countries now scrambling are paying the compound interest on decisions deferred since 2019, when Houthi drones struck Aramco’s facilities and the world briefly panicked before moving on. The world should not move on this time.

The Digital Trade Revolution: Routes Without Geography

There is a third dimension to this shift that rarely appears in energy columns, because it is invisible, weightless, and does not require a tanker: the explosive growth of digital trade and the services economy.

Digital commerce — software, financial services, intellectual property, telemedicine, AI-enabled business services — now accounts for a substantial and rapidly growing share of global economic value. It flows through submarine cables and spectrum, not through straits. IMEC’s digital pillar — a network of new intercontinental fibre-optic cables — is explicitly designed to create an alternative data corridor that bypasses choke geographies entirely. As the share of economic activity that is digital continues to expand — accelerated by AI, remote work, and platform economies — the share of global GDP that depends on physical chokepoints like the Strait of Hormuz will shrink, structurally and inexorably.

This is not a utopian projection. It is already happening. India’s digital services exports exceeded $200 billion in 2025. Southeast Asian e-commerce platforms transact trillions annually. None of it cares whether tankers can get through 34 kilometres of contested Gulf waters.

Recommendations for Policymakers: The Strategic Imperatives

The 2026 crisis is a forcing function. The question is whether governments will use it. Here is what they should do:

Accelerate pipeline bypass capacity in the Gulf. Saudi Arabia should fast-track the Petroline to its announced 7 million barrel-per-day capacity and actively negotiate with Iraq and Kuwait to begin engineering — not just discussing — northern corridor alternatives. The infrastructure gap between design capacity and utilised capacity is, at this moment, unconscionable.

Fund IMEC, not just endorse it. India has yet to establish a dedicated implementing body or commit specific funds to IMEC. That must change. The corridor needs a multilateral financing mechanism — modelled on the Bretton Woods institutions but purpose-built for twenty-first-century connectivity — not merely high-level communiqués.

Accelerate the LNG diversification that already works. The U.S., Canada, Australia, and Qatar (where pipeline exports to Turkey could reduce Hormuz dependency) should be treated as a strategic consortium for global energy security. New LNG infrastructure approvals should be fast-tracked under energy security frameworks.

Price the risk of Hormuz dependency into investment decisions. Insurers and sovereign wealth funds should be required to model Hormuz-closure scenarios in energy asset valuations. The underpricing of chokepoint risk — as this crisis has devastatingly illustrated — is a market failure with systemic consequences.

Invest in demand-side transition with strategic urgency. Every percentage-point reduction in global oil demand reduces Hormuz’s leverage over the world economy. EV incentives, renewable energy deployment in emerging economies, and energy efficiency standards are not merely climate policies. They are geopolitical risk management.

The Arc of the Argument

Crises have a way of feeling permanent in their midst. The 1973 oil embargo reshaped energy policy for a generation. The 1979 Iranian revolution convinced analysts that Persian Gulf dependency was an eternal condition of industrial civilisation. Neither prognosis proved correct. Alternatives emerged. Technologies shifted. Demand patterns evolved.

The 2026 Hormuz crisis is the most serious test of the global energy system since the 1970s. The World Economic Forum’s Global Risks Report 2026 already identifies geoeconomic confrontation as a key driver reshaping global supply chains, noting that “securing access to critical inputs is increasingly being treated as a matter of economic and national security.” Governments and industries are hearing that message with a clarity that previous near-misses never produced.

The Strait of Hormuz will matter enormously for years — perhaps decades — to come. To claim otherwise would be to misread the current data. But its structural importance to the global economy is on a long, slow, inexorable decline, driven by the energy transition, the rise of alternative corridors, the geography-defying nature of digital commerce, and the hardwired human instinct to find another road when the old one is blocked.

The future of global trade will not be decided in the narrow waters between Oman and Iran. It will be decided in solar farms in Rajasthan, LNG terminals in Louisiana, fibre cable landing stations in Haifa and Marseille, and EV factories in Hefei. The chokepoint is a reminder of where we came from. What we build next determines where we go.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

When Rivals Share a Rocket: The China-Europe SMILE Mission and the Fragile Promise of Space Science Diplomacy

On April 9, a European rocket will lift a Chinese-European spacecraft into orbit from the jungle coast of French Guiana. In a world tearing itself apart over chips, trade routes, and strategic chokepoints, this is not nothing.

The Countdown the World Isn’t Watching — But Should Be

At 08:29 CEST on April 9, 2026, an Avio-built Vega-C rocket — designated mission VV29, the first Vega-C flight operated by Avio Avio — will ignite its first-stage engines at Europe’s Spaceport in Kourou, French Guiana. Riding atop it will be SMILE: the Solar wind Magnetosphere Ionosphere Link Explorer, a 2,250-kilogram spacecraft nearly a decade in the making. The mission is a joint undertaking between the European Space Agency (ESA) and the Chinese Academy of Sciences (CAS) — and it is, by any reasonable measure, the most symbolically weighted space launch of 2026.

Not because of its destination. Not because of the science alone, though the science is genuinely groundbreaking. But because of what it represents at this particular moment in history: two of the world’s major technology powers, locked in an increasingly fraught geopolitical relationship, sharing data, sharing hardware, and sharing a launchpad.

SMILE is China’s first mission-level, fully comprehensive in-depth cooperation space science exploration mission with ESA GitHub — a statement that, when you sit with it, reveals how exceptional this collaboration actually is. After years of US-led pressure to isolate Chinese space activities, after the Wolf Amendment that has effectively banned NASA from bilateral cooperation with China since 2011, after wave after wave of technology export restrictions, here is a European rocket carrying instruments built simultaneously in Leicester and Beijing, tested jointly in the Netherlands, fuelled in Kourou, and aimed at a shared scientific horizon.

This is worth examining closely — not with naïve optimism, but with clear eyes.

What SMILE Actually Does, and Why It Matters

Before the geopolitics, the science — because the science is the point, and it deserves more serious attention than it typically receives in the English-language press.

Earth is constantly bombarded by gentle streams — and occasionally stormy bursts — of charged particles from the Sun. Luckily, a massive magnetic shield called the magnetosphere stops most of these particles from reaching us. If it weren’t for the magnetosphere, life could not survive on planet Earth. ESA

SMILE’s purpose is to give humanity its first comprehensive, simultaneous, global view of how that shield actually works — how it bends, buckles, and recovers under the assault of solar wind and coronal mass ejections (CMEs). Although several spacecraft have observed the effects of the solar wind and coronal mass ejections on Earth’s magnetic shield, they have mostly done so piecemeal ESA, through point measurements that are a bit like trying to understand a hurricane by sticking your hand out a single window.

SMILE changes that. The mission is a novel self-standing effort to observe the coupling of the solar wind and Earth’s magnetosphere via X-ray imaging of the solar wind-magnetosphere interaction zones, UV imaging of global auroral distributions, and simultaneous in-situ solar wind, magnetosheath plasma and magnetic field measurements. SPIE Digital Library

The four instruments it carries — the Soft X-ray Imager (SXI) built at the University of Leicester, a UV Aurora Imager, a Light Ion Analyser, and a Magnetometer — will work in concert from a highly inclined, highly elliptical orbit, with an apogee of 121,000 km and a perigee of 5,000 km. Avio From that sweeping vantage, SMILE will watch in real time as solar storms slam into Earth’s magnetic bubble, deform its boundaries, and trigger the geomagnetic disturbances we call space weather.

The Economic Stakes of Space Weather

Here is where the science becomes urgently, uncomfortably practical.

A severe geomagnetic storm — the kind triggered by a powerful CME — can induce electrical currents in long-distance transmission lines powerful enough to melt transformer cores. It can cripple GPS satellites, knock out shortwave radio communications, accelerate the degradation of satellite hardware, and expose astronauts to dangerous radiation doses. The Carrington Event of 1859 — the largest geomagnetic storm in recorded history — set telegraph offices on fire and produced auroras visible from the Caribbean.

Were a Carrington-scale event to strike the modern infrastructure-dependent world, the consequences would be catastrophic. Lloyd’s of London has estimated that a severe geomagnetic storm striking North America could leave between 20 and 40 million people without power for periods ranging from weeks to years, at a cost that would run into the trillions. The May 2024 geomagnetic storm — the most powerful in two decades — disrupted GPS signals and degraded satellite operations across the globe, offering a modest preview of what a truly extreme event might look like.

Better forecasting requires better physics. And better physics requires exactly what SMILE is designed to provide: a complete, global picture of how the magnetosphere actually responds to solar assault. By improving our understanding of the solar wind, solar storms and space weather, SMILE will fill a stark gap in our understanding of the Solar System and help keep our technology and astronauts safe in the future. ESA

A Mission Born in a Different World

The story of how SMILE came to be is, in itself, a small geopolitical parable.

The SMILE project was selected in 2015 out of 13 other proposals, and became the first deep mission-level cooperation between the European Space Agency and China. Orbital Today It was conceived when relations between China and the West, while not without tension, still operated under a broadly cooperative logic — when the prevailing assumption in Brussels and Beijing alike was that economic interdependence would gradually soften political friction and that scientific collaboration was a relatively safe space for engagement.

The Principal Investigators were Graziella Branduardi-Raymont from Mullard Space Science Laboratory, University College London, and Chi Wang from the State Key Laboratory of Space Weather at NSSC, CAS. ESA

What strikes me most about this pairing is its elegance and its tragedy. Professor Branduardi-Raymont — who, it should be noted, passed away in November 2023 after a lifetime of X-ray astronomy — had spent decades frustrated that no existing observatory could directly image X-ray emission from Earth’s magnetosphere. Her perseverance eventually produced this mission. She did not live to see its launch. But her instrument, built at the University of Leicester and calibrated with painstaking care across multiple European institutions, will fly on April 9 in the spacecraft she helped conceive. There is something moving in that continuity.

Professor Chi Wang, her Chinese counterpart, continued the work — a collaboration that survived COVID-era isolation, supply chain disruptions, and the gathering chill of US-China technology competition.

The SMILE mission entered full launch implementation phase after passing the joint China-Europe factory acceptance review on October 28, 2025. At the end of November 2025, the propellant required for the satellite departed from Shanghai, arriving at Kourou port in early February 2026. CGTN

On February 11, 2026, the flight model and ground support equipment departed from ESTEC in the Netherlands, sailing across the Atlantic from Amsterdam port aboard the cargo vessel Colibri, arriving at Kourou port on February 26, 2026, and being successfully transferred to the launch site. CGTN

That detail — a cargo ship named Colibri, sailing from Amsterdam to French Guiana carrying a satellite built in two countries on opposite ends of the Eurasian continent — is, to me, the most vivid emblem of what scientific cooperation can accomplish when given enough time, enough stubbornness, and enough shared wonder.

Europe’s Delicate Balancing Act

The launch of SMILE does not occur in a geopolitical vacuum. It occurs at a moment when Europe’s relationship with both China and the United States has become extraordinarily complex.

Washington has grown increasingly vocal about the risks of European technological cooperation with Beijing. The US-China Economic and Security Review Commission has flagged joint space missions as a potential vector for technology transfer. The US Space Force has publicly warned allies about sharing sensitive sensor data with Chinese partners. And while SMILE is a pure science mission — studying solar-terrestrial physics, not military reconnaissance — the distinction between civilian and dual-use space technology is one that Washington now views with considerable scepticism.

ESA, for its part, has walked this line with notable care. ESA Director General Josef Aschbacher confirmed SMILE’s launch timeline in January 2025, framing the mission squarely within the agency’s Cosmic Vision scientific programme — an agenda governed by scientific merit, not geopolitical alignment. “Building on the 24-year legacy of our Cluster mission,” said ESA Director of Science Prof. Carole Mundell, “SMILE is the next big step in revealing how our planet’s magnetic shield protects us from the solar wind.” ESA

That framing matters. ESA is positioning SMILE not as a concession to Beijing, but as the natural scientific successor to decades of European magnetospheric research — a mission that happens to have a Chinese partner because the Chinese partner brought the best science proposal to the table in 2015.

Strategic Autonomy in Orbit

Europe’s Strategic Autonomy agenda — the drive to reduce dependency on both American and Chinese platforms — finds an interesting expression in SMILE. The mission uses a European launcher (Vega-C), European testing facilities (ESTEC in the Netherlands), and a European payload module built by Airbus in Spain. China contributes three scientific instruments and the spacecraft platform and operations. The division of labour is not equal, but it is genuine.

This is different from the model China has pursued in, say, its International Lunar Research Station programme — a Beijing-led effort to build a Moon base with selective partner participation on China’s terms. SMILE was born from a joint call for proposals, adjudicated by both ESA and CAS, on scientific merit alone. The symmetry of its origins is a meaningful safeguard.

What the mission also illustrates, however, is the limits of that safeguard. Despite ongoing delays of the launch and geopolitical tensions between Europe and China, this mission marks an important collaboration between the two parties. Orbital Today Delays stretched from an original 2021 target across five years. COVID disrupted joint testing. Geopolitics hovered over every logistics decision. That the satellite is sitting on a Vega-C in Kourou today is a testament to institutional resilience on both sides — and a reminder of how fragile such resilience can be when the political weather changes.

What Comes Next: Blueprint or One-Off?

The successful implementation of the SMILE mission will set a benchmark for China-EU space science cooperation and lay the technological foundation for deeper future collaboration. GitHub

That Chinese Academy of Sciences statement is aspirational in tone. Whether it reflects reality will depend on choices that neither ESA nor CAS alone can make.

The scientific case for continued China-Europe cooperation in space is actually strong. China has developed formidable capabilities in solar and heliospheric science, planetary exploration, and space weather monitoring. ESA brings world-class instrumentation, launcher independence, and an institutional culture of multinational collaboration forged across 22 member states. Together, they have demonstrated — through SMILE — that the logistics of joint mission development are solvable, even across supply chain disruptions and a pandemic.

The geopolitical case is harder. As US pressure on European technology transfer policies intensifies, as China’s own space ambitions grow more assertive, and as the Artemis Accords effectively create a US-aligned coalition in cislunar space, Europe faces a binary pressure: join Washington’s bloc or preserve its own lane.

SMILE suggests a third option — cautious, science-first, mission-specific cooperation, carefully ring-fenced from military and surveillance applications, conducted through multilateral institutions with independent governance. It is not a grand geopolitical declaration. It is a pragmatic transaction between research agencies who share a genuine scientific puzzle.

That may, in the end, be its most important lesson. The most durable forms of international cooperation are rarely born from summit communiqués or diplomatic ambition. They are built from specific problems, shared curiosity, and the grinding, unglamorous work of building something together over a decade. SMILE’s cargo ship sailed from Amsterdam. Its fuel was loaded in Shanghai. Its instruments were calibrated in Leicester. Its launcher was assembled in Colleferro.

On the morning of April 9, all of that will rise together over the Atlantic, riding a column of fire into a highly elliptical orbit 121,000 kilometres above the Earth, where it will spend three years watching our planet’s invisible magnetic shield absorb the fury of the Sun.

Whatever one thinks of the geopolitics, that image is worth holding onto.

The View From the Launchpad

In a world increasingly defined by decoupling — technological, financial, diplomatic — SMILE is a small, luminous exception. It will not resolve the fundamental tensions between Beijing and Brussels. It will not answer the question of whether Europe can maintain scientific ties with China while deepening security cooperation with Washington. It will not make the next CME less dangerous or the next trade war less likely.

But it will, if all goes to plan, give us something genuinely new: a complete, real-time picture of how Earth’s magnetic shield breathes, bends, and holds against the solar wind. And it will have done so because two sets of scientists — from Milan and Beijing, from Leicester and Shanghai — decided that the problem was important enough to work on together, regardless of the weather in Washington.

What strikes me most, in the end, is not the geopolitics. It is the image of Professor Branduardi-Raymont at Mullard Space Science Laboratory, frustrated for years that no observatory could image X-ray emission from the magnetosphere, proposing mission concepts until one finally stuck. The Colibri will not carry her name. But the instrument riding inside the fairing of that Vega-C, the lobster-eye X-ray telescope that will for the first time map the shape of Earth’s magnetic boundary, is her life’s work.

The rocket lifts off at 08:29 CEST. The world should be watching.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance3 months ago

Markets & Finance3 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis2 months ago

Analysis2 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks3 months ago

Banks3 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment3 months ago

Investment3 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Analysis2 months ago

Analysis2 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Asia3 months ago

Asia3 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Global Economy3 months ago

Global Economy3 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy3 months ago

Global Economy3 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis