Analysis

The Hidden Cost of the Hormuz Standoff: Why “Sea Gunk” Is the Shipping Industry’s Next Billion-Dollar Problem

Tankers stranded in the Persian Gulf during the US-Iran conflict have sat idle long enough for warm-water barnacles, algae and marine growth to colonize their hulls, a phenomenon known as biofouling. This is now forcing costly dry-dock cleaning, slowing vessel speeds, raising fuel burn and pushing up war-risk insurance premiums — a knock-on cost of the conflict that has received far less attention than headline oil prices.

An Underreported Consequence of the Standoff

Most coverage of the US-Iran conflict has focused on oil prices and the risk of a full closure of the Strait of Hormuz, through which roughly a fifth of the world’s seaborne crude normally passes. Less visible is a slower-moving, equally costly problem: ships that have been anchored or rerouted for weeks are now dealing with heavy hull fouling. Specialist “bottom cleaner” crews are being dispatched to scrape off marine growth that has attached itself to tankers stranded in the warm waters of the Persian Gulf, according to reporting on the scale of the buildup facing vessels caught in the standoff (CNN Business).

Biofouling is not a cosmetic issue. A fouled hull increases drag, which raises fuel consumption by as much as 20–40% depending on severity, according to maritime engineering estimates cited across shipping-industry literature. For an industry already absorbing higher war-risk premiums, the added fuel and dry-docking costs compound an already expensive standoff.

Where the Standoff Stands Now

By early July, daily oil flows through the Strait had recovered to more than 10 million barrels a day, with Saudi and UAE crude exports running at roughly 90% of pre-war levels, according to a review of shipping data by UK Finance. That recovery has helped push Brent crude down roughly 40% from its April peak. But the fact that flows are recovering doesn’t erase the weeks of disruption already priced into contracts, insurance renewals and vessel maintenance schedules.

Bank of England Governor Andrew Bailey has flagged this lag effect directly, noting that even as spot oil prices fall, “the higher energy prices of the past four months mean there’s already some inflationary pressure in the pipeline” for consumer economies (Hanbury Wealth Economic Review).

Why This Matters Beyond Shipping

The biofouling problem is a useful proxy for a broader truth about the Hormuz conflict: its costs are not confined to the headline price of a barrel of oil. They show up in:

- Insurance markets — War-risk premiums for Gulf transits have risen sharply and are only slowly normalizing as underwriters reassess vessel-specific risk.

- Fuel and emissions costs — Fouled hulls burn more bunker fuel, an expense that ultimately filters into freight rates and consumer goods prices.

- Dry-dock capacity — A surge in demand for emergency hull cleaning is straining specialist marine services capacity in Gulf ports.

- Second-round inflation — Central banks in energy-importing economies, including the UK, have explicitly built these lagged supply-chain effects into their inflation forecasts for the second half of 2026 (Bank of England, June 2026 Monetary Policy Summary).

The Bigger Picture for Trade-Dependent Economies

Economies with heavy exposure to Gulf shipping lanes — the UK, Singapore, and the broader Gulf states themselves — are watching this unwind carefully. Singapore’s own trade ministry has explicitly cited the conflict as a downside risk to its 2026 growth forecast even as second-quarter GDP beat expectations (CNBC). Dubai, meanwhile, has continued to post resilient non-oil growth, insulated somewhat by economic diversification away from hydrocarbons (Gulf Business).

For freight forwarders, insurers and importers, the lesson of the biofouling episode is that Gulf conflict risk doesn’t disappear the moment a ceasefire is announced — it lingers in maintenance backlogs, insurance renewal cycles and fuel cost pass-through for months afterward.

Key Takeaways

- Prolonged vessel idling in the Persian Gulf has created a costly biofouling problem now requiring emergency hull-cleaning operations.

- Oil flows through Hormuz have largely recovered, but the inflationary “pipeline effect” of the disruption is still working through import-dependent economies.

- Central banks, including the Bank of England, have explicitly incorporated lagged energy-shock effects into their 2026 inflation forecasts.

- Trade hubs like Singapore and Dubai are tracking the conflict’s tail risks even as headline growth figures remain strong.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

The UK’s Second-Round Problem: Why the Bank of England Is Bracing for Inflation to Rise, Not Fall

UK inflation fell to 2.8% by May 2026, but the Bank of England expects it to climb back to roughly 3.5–3.8% by year-end as the delayed effects of the Middle East energy shock work through supply chains. The Monetary Policy Committee held Bank Rate at 3.75% in June, with two of nine members voting for an immediate hike — a rare hawkish dissent that signals how finely balanced UK policy has become.

A Rare Split Vote

At its June meeting, the Bank of England’s Monetary Policy Committee voted 7–2 to hold Bank Rate at 3.75%, with two members preferring an immediate quarter-point increase to 4% (Bank of England). The committee noted that while global energy prices have fallen since its previous meeting, they remain above pre-conflict levels and “have continued to be volatile.”

That volatility is the crux of the UK’s problem. Unlike a straightforward demand-driven inflation cycle, this one is propagated through what the Bank calls “second-round effects” — the way an initial energy price spike filters into transport costs, food prices, and ultimately wage-setting expectations, even after the original shock partially reverses.

The Numbers Behind the Warning

- UK GDP grew 0.6% in Q1 2026, with output 0.9% higher year-on-year, according to Office for National Statistics data reviewed by Hanbury Wealth.

- CPI inflation registered 2.8% in May 2026, matching April’s reading, but the Bank’s own Monetary Policy Report flagged this as likely to be the low point for the year (Parliament’s Economic Indicators briefing).

- The British Chambers of Commerce now expects inflation to reach 3.8% by the end of 2026 and forecasts UK growth of just 0.9% this year, citing the direct impact of the Iran conflict and elevated energy costs (BCC).

- The composite Purchasing Managers’ Index slipped to 49.4 in the mid-June flash reading, its lowest level in 14 months and below the 50-point threshold that separates expansion from contraction (Hanbury Wealth).

Taken together, these figures describe a textbook stagflationary bind: growth is softening at the same time inflation is expected to reaccelerate, leaving the Bank of England little room to cut rates to support activity without risking a fresh round of price pressure.

Bailey’s Own Words

Bank of England Governor Andrew Bailey has been unusually direct about the lag between falling oil prices and consumer inflation. Speaking after the June MPC meeting, he noted that recent oil price declines were “encouraging,” but cautioned that months of elevated energy costs mean “there’s already some inflationary pressure in the pipeline,” regardless of where prices go from here (Hanbury Wealth).

The UK’s energy price cap adjustment for the July–September quarter, combined with the removal of the Renewables Obligation subsidy from household bills, is expected to add roughly a third of a percentage point to CPI inflation in the same window, according to the House of Commons Library (Commons Library briefing).

Why the UK Is More Exposed Than Other G7 Economies

The UK’s vulnerability comes down to structure: it is a net energy importer, meaning wholesale gas and oil price swings pass through to consumers and businesses more directly than in economies with larger domestic production. This is part of why the Bank of England modeled three separate scenarios for the UK economy in its April 2026 report, ranging from a relatively contained energy shock to a more prolonged and severe one, depending on how the Hormuz situation evolves (Bank of England, June minutes).

Key Takeaways

- The Bank of England held rates at 3.75% in June, but a two-member hawkish dissent shows how close the committee is to reversing course on cuts.

- Inflation is expected to climb from 2.8% toward 3.5–3.8% by year-end as delayed energy costs filter through the economy.

- The UK’s status as a net energy importer makes it structurally more exposed to Gulf conflict spillover than economies with larger domestic energy production.

- A weakening PMI alongside rising inflation forecasts point toward a stagflationary environment through the second half of 2026.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

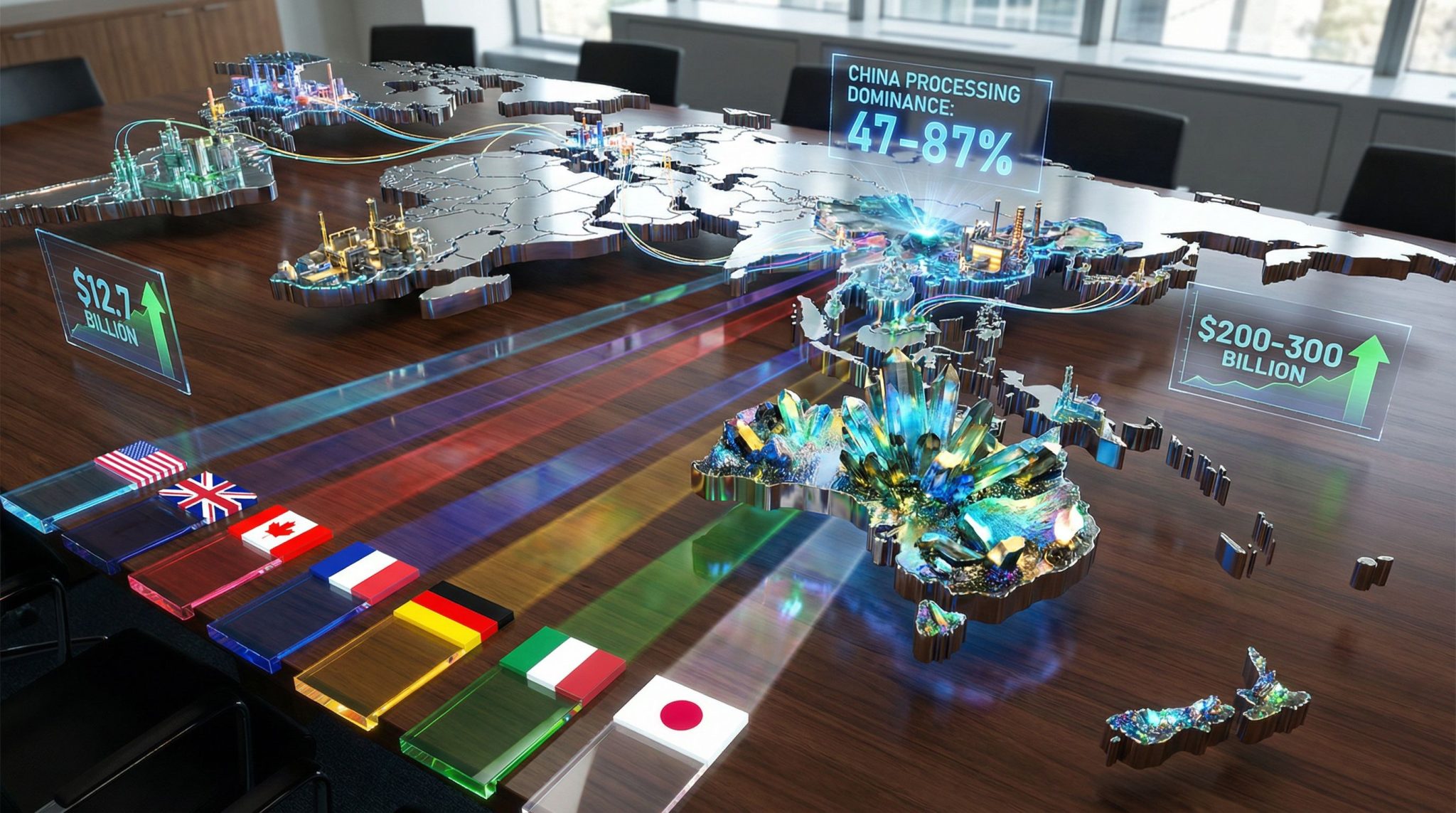

The New Resource Geopolitics: How G7 Critical Minerals Strategy Is Forcing ASEAN Into a Careful Balancing Act

As the United States and its G7 partners race to build critical minerals supply chains outside China’s control, ASEAN economies — sitting on some of the world’s largest reserves of nickel, tin and rare earth-adjacent minerals — are increasingly practicing a strategy of deliberate hedging: courting Western investment in processing and manufacturing capacity while avoiding formal alignment against China, their largest trading partner and dominant regional investor.

Why This Has Become Urgent

China’s near-total dominance of global rare earth processing — controlling roughly 90% of capacity, according to industry analysis — has turned critical minerals into one of the sharpest instruments of economic statecraft in the current cycle (see our companion coverage). Beijing’s escalating export controls on yttrium, scandium and other elements essential to AI chip manufacturing have made clear to Washington and its allies that dependence on a single-country supply chain for these inputs is a structural vulnerability, not a temporary inconvenience.

Researchers at the Center for Strategic and International Studies have warned explicitly that the pattern of escalating export controls between the US and China risks triggering “an export control and economic statecraft arms race that could severely undermine global security and economic prosperity” (Cryptopolitan).

Where ASEAN Fits

Southeast Asia holds a genuinely pivotal position in this contest, but its individual economies are responding in structurally different ways:

- Indonesia has leaned into resource nationalism, banning raw nickel ore exports to force domestic processing investment — a strategy that has driven record foreign investment but risks entrenching a narrow, commodity-dependent industrial base if it fails to move into higher-value battery manufacturing (see our companion coverage).

- Malaysia has instead captured the manufacturing layer of the battery and electronics supply chain, positioning itself as ASEAN’s leading battery exporter while AMRO credits “robust electronics exports and AI-related investment” for cushioning growth against broader “geoeconomic fracturing” (see our companion coverage).

- Singapore continues to function as the region’s financial and logistics anchor, benefiting from rerouted shipping traffic during the Hormuz conflict while its manufacturing sector rides the same AI-driven semiconductor supercycle reshaping demand for the critical minerals underlying chip production (see our companion coverage).

The Regional Coordination Angle

Rather than each country negotiating individually with Washington or Beijing, ASEAN members have been building horizontal coordination mechanisms. Indonesia and the Philippines have proposed a nickel supply chain corridor explicitly framed around regional integration, with the Philippine Chamber of Commerce and Industry’s president describing the goal as ensuring “ASEAN is strongest when it acts as one unit” (Tribune.net.ph). Separately, Malaysia’s Selangor state has deepened bilateral cooperation with Indonesia’s West Java Province across manufacturing, infrastructure and Islamic finance, reflecting a broader pattern of intra-ASEAN economic deepening running in parallel with — rather than as a substitute for — engagement with both Washington and Beijing (ACN Newswire via Barchart).

Why Neither Superpower Can Simply Bypass ASEAN

For Washington, ASEAN’s mineral reserves and manufacturing capacity represent one of the few credible near-term paths to diversifying critical minerals and electronics supply chains away from China — a strategic priority underscored by the UAE’s own recent upgrade in US technology export access (see our companion coverage), part of a broader pattern of Washington deepening ties with trusted partners outside China’s orbit. For Beijing, ASEAN remains both an enormous export market and, increasingly, a manufacturing base for goods designed to route around US tariffs and export restrictions — making continued economic engagement equally indispensable.

This dual dependency is precisely what gives ASEAN economies room to hedge rather than choose. It also means the region’s trade and investment data over the next several years will likely be read closely by policymakers in Washington, Beijing, Brussels and Tokyo as a real-time indicator of how the broader US-China economic rivalry is actually being resolved on the ground, rather than in policy statements.

Key Takeaways

- China’s dominance of rare earth processing has made critical minerals a central front in US-China economic rivalry, with ASEAN’s mineral reserves newly strategically significant.

- Indonesia, Malaysia and Singapore are pursuing distinct national strategies — resource nationalism, manufacturing capture, and financial/logistics hubbing, respectively — rather than a unified regional approach.

- ASEAN nations are building horizontal coordination mechanisms, like the proposed Indonesia-Philippines nickel corridor, to strengthen collective bargaining power.

- Both the US and China have deep enough economic stakes in ASEAN that the region can credibly hedge between them rather than being forced to align with either bloc.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Uber’s pursuit of Delivery Hero has finally crossed the finish line, and the structure of the winning bid says as much about the state of global food-delivery competition as the headline price itself.

The Deal Terms

Uber will acquire Frankfurt-listed Delivery Hero in a deal valued at €41.50, or $47.59, per share, with Dutch technology investor Prosus offloading its near-17 percent stake in Delivery Hero to Uber as part of the transaction. The improved offer follows a rejected earlier approach: one of Delivery Hero’s major shareholders had turned down a €38-per-share offer from Uber back in May, forcing Uber to sweeten terms by roughly 9 percent to get the deal across the line.

The transaction’s second component is arguably more strategically important than the headline acquisition. Delivery Hero will simultaneously sell its businesses across 14 markets to SSW Partners in a deal worth $1.4 billion, specifically covering territories where Delivery Hero’s operations would otherwise overlap directly with Uber’s existing footprint post-acquisition — a structure clearly designed to pre-empt antitrust objections in those markets.

Why the Divestiture Structure Matters

Regulators across Europe and Asia have grown increasingly wary of food-delivery consolidation given the sector’s history of just two or three dominant platforms per market. By carving out the 14 overlapping markets into a separate sale to SSW Partners before regulatory review even begins, Uber and Delivery Hero appear to be attempting to neutralise the most obvious competition concerns pre-emptively — a playbook increasingly common in large tech-platform M&A globally.

Market Reaction

The market’s initial reaction was muted rather than euphoric: Delivery Hero shares fell about 1 percent on the news, suggesting investors had already priced in a deal at or near these terms following months of on-and-off negotiations, or harboured lingering doubts about regulatory approval timelines given the multi-market divestiture complexity involved.

The Broader M&A Backdrop

The Uber-Delivery Hero transaction lands amid a broader resurgence in large-scale industrial and technology M&A. On the same trading day, Swiss engineering group ABB agreed to acquire UK-listed industrial flow-control specialist Rotork for £4.1 billion, or $5.6 billion — ABB’s biggest-ever acquisition, sending Rotork shares soaring 66.7 percent in morning trading (a deal covered in greater depth in our companion piece on the UK industrial M&A wave). The concurrent timing of two multi-billion-dollar cross-border deals suggests dealmakers are treating current valuations and financing conditions as a window worth acting on before the Fed’s tightening bias, discussed elsewhere in this series, potentially raises the cost of acquisition financing further.

What It Means for Consumers and Competitors

For consumers across Uber’s and Delivery Hero’s combined markets, the immediate practical question is pricing power: fewer major platforms per market historically correlates with reduced promotional intensity and, eventually, higher delivery fees, even as the SSW Partners carve-out is designed to preserve at least nominal competition in the 14 most overlap-sensitive territories. Competing platforms — from DoorDash in the US to regional players across Southeast Asia — will be watching regulatory reception to this deal closely as a signal for how much further consolidation authorities are willing to tolerate in a sector still recovering from pandemic-era overexpansion.

Featured Snippet

How much is Uber paying for Delivery Hero? Uber’s takeover of Delivery Hero values the company at €41.50 ($47.59) per share, an increase from a previously rejected €38 offer. As part of the deal, Delivery Hero will sell its operations in 14 overlapping markets to SSW Partners for $1.4 billion.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The UK’s Second-Round Problem: Why the Bank of England Is Bracing for Inflation to Rise, Not Fall

The Fed’s Quiet Doctrine Shift: Why a Dovish Central Bank Is Suddenly Hearing Calls for Rate Hikes

The Hidden Cost of the Hormuz Standoff: Why “Sea Gunk” Is the Shipping Industry’s Next Billion-Dollar Problem

The New Resource Geopolitics: How G7 Critical Minerals Strategy Is Forcing ASEAN Into a Careful Balancing Act

Uber’s $47.59-a-Share Delivery Hero Deal: Inside the Consolidation Wave

Johor-Singapore Economic Zone: Inside the $19 Billion Investment Boom

Indonesia’s Rupiah Balancing Act: Growth Surges as Singapore Capital Pours In

Malaysia GDP Forecast Raised to 4.9% as $23 Trillion Descends on Singapore

The Bank of England Just Modelled an AI Crash — Here’s What It Found

Pakistan Economy 2026: IMF Growth Warning vs. a Booming KSE-100

Russia’s Oil Sanctions Paradox: Why Revenue Is Rising, Not Falling

China GDP Growth Misses Target: What’s Behind the 4.3% Slowdown

The Strait of Hormuz Shock Nobody Has Priced In Yet

Fed Rate Hikes 2026: Why Kevin Warsh Is Reversing the Cut Cycle

Top 7 Banking Stocks for Investment in PSX: Pakistan’s Lenders Are Still Printing Money

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

JPMorgan Cuts Anthropic AI Access in Hong Kong

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Why China’s Demand Stimulus Still Isn’t Working

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

India Economic Rise 2026: How the Subcontinent Toppled Japan

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025