AI

The Bank of England Just Modelled an AI Crash — Here’s What It Found

Central banks rarely name specific asset bubbles in official reports. The Bank of England’s July 2026 Financial Stability Report comes close, devoting substantial analysis to what happens if the AI-driven equity rally that has powered global markets for two years abruptly unwinds.

A Scenario, Not a Prediction — But a Detailed One

Bank staff explicitly modelled the impact on the UK economy of a potential global correction in AI valuations, running the scenario through both equity markets and, more significantly, sovereign debt dynamics. The Bank’s own assessment is measured: an equity shock in isolation would be unlikely to present a direct risk to UK financial stability on its own.

The caveat is where the real story lives. The report warns that a reassessment of AI-related companies’ prospects could trigger a fall in equity prices that gets amplified by high concentration, correlated momentum-driven positions and elevated use of leverage — the same structural fragilities that have historically turned ordinary corrections into disorderly ones.

Why Gilt Markets Are Suddenly Part of the AI Story

The more novel finding concerns sovereign debt. In the Bank’s hypothetical scenario, debt-to-GDP ratios rise as a corrective aftershock, but the report notes that in its analysis both the US Treasury market and the UK gilt market continued to function well — with an explicit warning that had those markets come under pressure instead, the financial stability consequences could have been considerably worse.

That’s a notable acknowledgment that AI equity valuations and sovereign bond market resilience are no longer separate conversations. The Bank’s broader Financial Policy Committee analysis observes that the pace of AI-related investment is unprecedented historically, with AI companies increasingly turning to the financial system — particularly debt financing — to fund infrastructure buildouts, a trend that has accelerated corporate credit issuance across global markets.

Is the Bank of England worried about an AI bubble?

Yes. The Bank’s July 2026 Financial Stability Report modelled a global AI valuation correction, warning that concentrated, leveraged equity positions could amplify a sell-off, though it found UK gilt and US Treasury markets held up well under the hypothetical scenario tested.

The Leverage Problem Underneath the Rally

The report is candid about how narrow the rally has become. Equity price gains have been driven in significant part by a concentrated set of AI-related companies, with valuations on some metrics now stretched even as continuing positive earnings news has supported prices since the Bank’s December report. The FPC also flags a substantial increase in the use of leverage tied to these positions — precisely the mechanism that turns a valuation reset into a liquidity event.

On the credit side, the Bank notes that vulnerabilities in risky asset valuations, sovereign debt markets and risky credit — including private credit — remain, with some having become more pronounced since the previous report, as energy-driven cost increases and globally higher interest rates add pressure on corporate borrowers.

The Policy Response

Rather than attempting to deflate the AI rally directly — not a central bank’s job — the Bank is focused on shock absorption. It points to reforms already announced for money market funds across the UK and Europe, and changes under exploration to bolster resilience in the gilt repo market specifically, as the tools most likely to prevent an AI-driven equity correction from cascading into a broader liquidity crisis.

Why This Matters Beyond the UK

The Bank’s framing — that the UK and euro area are less directly reliant on the AI-financing ecosystem than the US, but not insulated from its unwind — is a useful lens for investors across every market covered in this series. A disorderly correction centred on US AI infrastructure debt would transmit through global risk appetite, currency markets and credit spreads well before it reached UK-specific balance sheets, making this less a domestic UK story than a global one told through a UK institutional lens.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Fed Chair Kevin Warsh’s AI Rate Bet 2026: Inside the FOMC Split on Productivity vs Inflation

Federal Reserve Chairman Kevin Warsh, sworn in on May 22, 2026, used his first appearance at the European Central Bank’s Sintra forum to tie the future of US interest-rate policy explicitly to a single question: whether the artificial intelligence capital-expenditure wave will eventually translate into real productivity gains (24/7 Wall St.). “We’re all in the price stability business,” Warsh told the forum, adding that officials had grown more open-minded about AI’s disinflationary potential even as current prices remain too high (CNBC).

The Data Behind Warsh’s Bet

The numbers Warsh is watching are stark: Q1 2026 private investment surged 7.9% while consumer spending crawled at just 0.5%, meaning corporate capital expenditure — not household demand — is now the dominant engine of US GDP growth. Domestic nonfinancial corporate profits hit $2.97 trillion in the first quarter, with the information sector alone contributing $352.5 billion, up from $265 billion two years earlier (24/7 Wall St.).

A Genuine Split on the FOMC

Not everyone on the Federal Open Market Committee shares Warsh’s optimism. New York Fed President John Williams has cited AI-related spending as a persistent source of demand that could eventually force the central bank toward rate hikes rather than cuts — the opposite conclusion from Warsh’s own framing (Moneywise). Minutes from the June meeting, Warsh’s first as chair, showed heightened committee-wide awareness of inflation risk tied both to the Iran war’s disruption of oil shipping and to lingering tariffs.

The $700 Billion Number That Complicates the Story

Quartz’s analysis frames the tension precisely: Warsh arrived in the role with a case for lower rates built on an AI productivity story, only to confront a roughly $700 billion AI spending blitz from hyperscalers that is, for now, showing up overwhelmingly on the demand side of the economy rather than the supply side he is banking on (Quartz). Markets are already pricing in the possibility of one rate hike by October — a scenario few analysts anticipated when Warsh took office pledging a fresh, less-predictive approach to Fed communication.

Inflation Has Not Cooperated

Personal Consumption Expenditures inflation hit 4.1% in May, with core inflation at 3.4%, prompting some analysts to describe Warsh’s tenure as marking a “hawkish turn” that has caught investors off guard after years of expectations for near-term easing (Intellectia). The federal funds rate has been held at 3.50–3.75% for four consecutive meetings spanning both the Powell and Warsh chairmanships.

Why This Matters Well Beyond Wall Street

Warsh’s framing — that AI represents “the first or second inning” of a productivity revolution comparable to the internet’s creation of entirely new job categories — is not merely rhetorical. If the Fed holds or cuts rates based on an AI productivity bet that fails to materialise on schedule, the resulting policy error would ripple through every economy whose currency, borrowing costs and capital flows are benchmarked against the dollar, from the Bank of England’s own rate path to emerging-market central banks in Pakistan and Indonesia currently managing their own inflation dynamics.

The Next Test

The FOMC’s July 28–29 meeting is, per multiple analysts, the pivotal near-term data point — the first real signal of whether Warsh’s productivity bet or Williams’s demand-side inflation concern is shaping actual policy rather than just public messaging.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

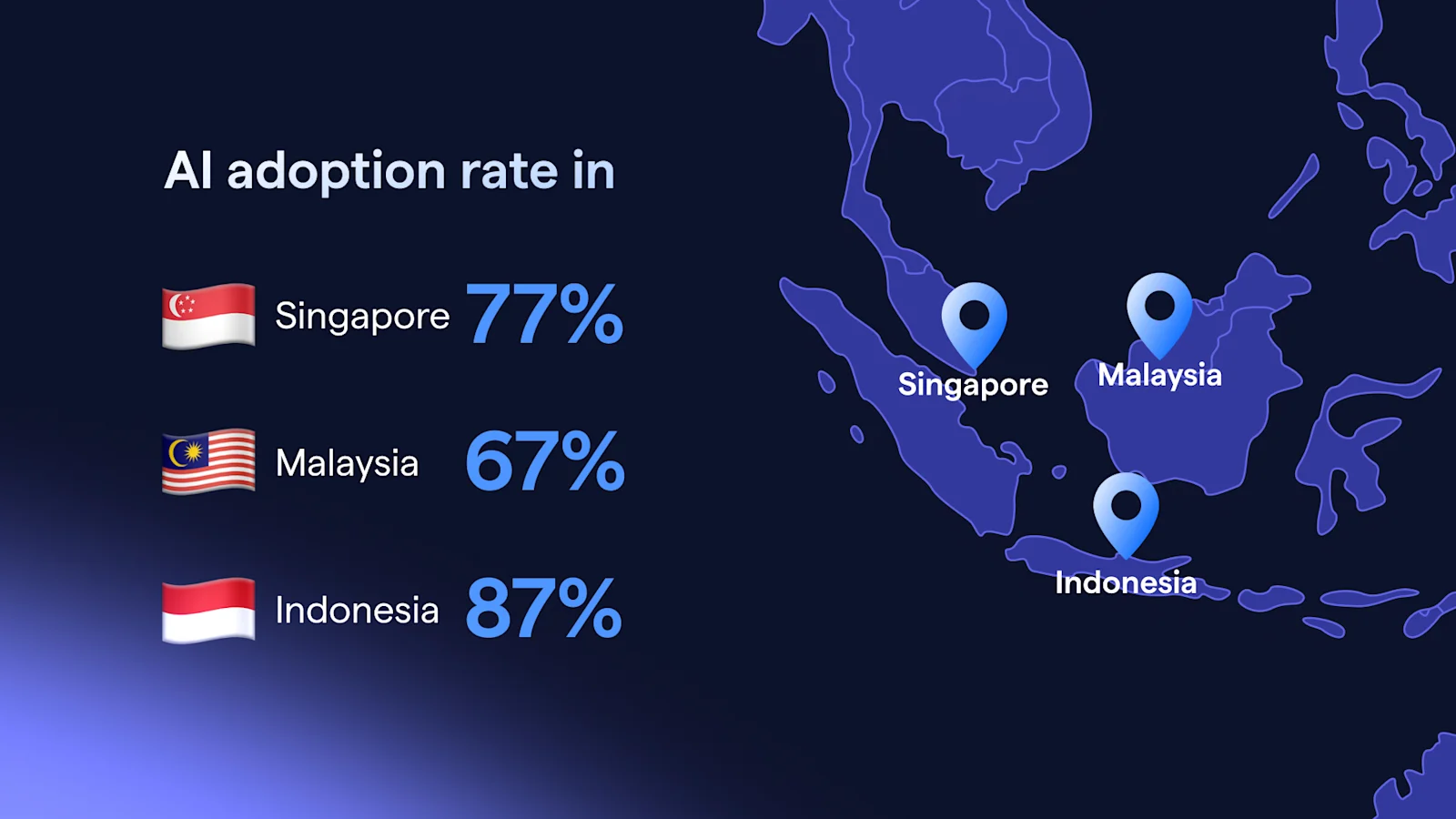

Malaysia Singapore AI Boom 2026: Inside the Sovereign AI Policy Shift Behind the Growth Numbers

Research houses have repeatedly upgraded Malaysia’s 2026 growth forecast through the summer, with Maybank Investment Bank raising its estimate to 4.9% from 4.4%, citing resilient domestic demand, robust exports and the global AI-driven technology upcycle even after the bank had cut its outlook in May over Strait of Hormuz concerns (Xinhua). HSBC Private Bank separately held its 4.5% forecast, pointing to Malaysia’s position as a net oil exporter and its emerging role leading the region’s data-centre market as key buffers against global instability (The Rakyat Post).

The Semiconductor Pipeline Story Everyone Is Covering

Maybank’s chief executive Michael Oh-Lau told the bank’s Invest ASEAN conference in Singapore that energy transition, supply-chain reconfiguration and AI-led digital transformation dominated this year’s agenda, as $23 trillion in assets under management descended on the summit (BigGo Finance). Malaysia’s semiconductor testing and assembly infrastructure is feeding directly into the regional AI trade, according to HSBC’s Desmond Kuang, while Singapore’s manufacturing sector accelerated to 12.2% growth in Q2, driven by electronics and precision engineering tied to AI-related semiconductor demand (Vietnam Plus).

The Angle Competitors Are Missing: Governance, Not Just GDP

What most business coverage has not connected is a parallel policy shift documented by trade-law specialists at MLex: both Malaysia and Singapore are quietly redefining what “sovereign AI” means for smaller economies. Rather than pursuing full technological self-sufficiency, both governments are combining targeted domestic capability with governance frameworks, trusted partnerships and selective investment — a middle path distinct from the US-China AI arms race (MLex). The defining question, per MLex’s analysis, is not how much governments should own, but what they need to control.

Singapore’s Growth Deceleration Is a Warning Sign, Not Just a Data Point

Singapore’s economy grew 5.7% year-on-year in Q2, decelerating from the prior quarter despite the near-doubling of electronics exports, suggesting AI-related demand alone cannot fully insulate a trade-dependent economy from Middle East volatility (Free Malaysia Today). Prime Minister Lawrence Wong warned in June that the economy had not yet felt the full impact of the conflict, a caution that stands in tension with the more bullish AI-investment narrative dominating research-house forecasts.

The AMRO Warning Beneath the Optimism

The ASEAN+3 Macroeconomic Research Office’s annual consultation flagged a sharper-than-expected cooling of the global AI cycle as Malaysia’s principal downside risk — one capable of dampening electronics and data-centre demand and triggering broader financial market volatility, alongside renewed tariff frictions and tighter technology controls (AMRO). That is a meaningfully different risk framing than the “AI boom insulates Southeast Asia” narrative currently dominating headlines.

What This Means for Investors and Policymakers

The structural story is real: Malaysia and Singapore have entrenched positions in global semiconductor and AI infrastructure value chains, and institutional capital is responding accordingly. But the sustainability of that story now rests on governance choices around sovereign AI policy as much as on the capex cycle itself — a dimension largely absent from mainstream financial coverage of the region.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Singapore’s Q2 2026 GDP print beat expectations. Every headline led with that. Almost none led with the fact that growth is decelerating quarter over quarter — and that the country’s own prime minister has warned the worst may still be ahead.

The number that beat forecasts, and the trend it’s hiding

Singapore’s economy grew 5.7% year-on-year in the second quarter of 2026, according to advance estimates from the Ministry of Trade and Industry (MTI), beating the median forecast of 5.5% in a Bloomberg survey, per Free Malaysia Today. But that headline “beat” obscures the trend: it’s a deceleration from a revised 6.3% in the January-March quarter.

The explanation is straightforward but underreported: continued geopolitical tension in the Middle East is tempering the export boost that Singapore had been getting from the AI-driven electronics boom. Electronics exports nearly doubled in May year-on-year, but renewed Middle East conflict has clouded the broader outlook for trade and investment, per the same report. In effect, Singapore is running two offsetting stories simultaneously — an AI supercycle tailwind and a geopolitical-disruption headwind — and the net GDP number is the residual of both, not a clean read on either.

The prime minister’s own warning

Prime Minister Lawrence Wong warned last month that Singapore has “yet to feel the full economic impact of the Iran war,” according to the same Free Malaysia Today report. That’s a notably candid admission from a sitting head of government about downside risk still working through the system — and it’s a warning that deserves more coverage than the beat-the-forecast headline it accompanied.

Separately, Joey Choy’s July 2026 markets newsletter notes that Singapore’s Economic Strategy Review Final Report has proposed more detailed measures for long-term competitiveness, while MTI has maintained its full-year 2026 GDP growth forecast at “2.0 to 4.0 percent” — a range that implies officials expect meaningful deceleration in the back half of the year even after a strong first half.

The policy decision to watch

The Monetary Authority of Singapore (MAS) will decide on its policy settings no later than July 31, 2026, with economists largely forecasting a hold given benign inflation data for May, per Free Malaysia Today. That decision will be a genuine test of the deceleration thesis: a hold despite slowing sequential growth would signal MAS sees the slowdown as temporary and geopolitically driven rather than structural; any dovish signal would suggest more concern about underlying momentum than the headline Q2 number implies.

Why this matters for the region

Singapore functions as a bellwether for Southeast Asian trade and AI-linked electronics demand more broadly. Its currency-basket monetary policy (rather than a simple interest-rate target) makes MAS decisions a read on the trade-weighted outlook for the whole region, not just the city-state itself. The deceleration story here connects directly to what’s happening in Malaysia, where Maybank has upgraded its 2026 GDP forecast partly on the same AI-driven tech upcycle — meaning the region’s growth narrative and its risks are more intertwined than country-by-country headlines suggest.

For businesses and investors with exposure to Southeast Asian supply chains, the signal to track isn’t the Q2 beat — it’s whether Q3 growth continues decelerating toward the bottom of MTI’s 2.0–4.0% full-year range, which would confirm the Iran-war drag Wong flagged is materializing rather than dissipating.

FAQ

What was Singapore’s GDP growth in Q2 2026? 5.7% year-on-year, beating the 5.5% median forecast, but down from a revised 6.3% in Q1 2026.

Why is Singapore’s growth slowing despite an AI export boom? Geopolitical tension from the Middle East conflict is offsetting gains from AI-driven electronics exports, which nearly doubled in May 2026 year-on-year.

When does the Monetary Authority of Singapore make its next policy decision? No later than July 31, 2026; economists largely expect a hold given benign May inflation data.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Uber’s $47.59-a-Share Delivery Hero Deal: Inside the Consolidation Wave

Johor-Singapore Economic Zone: Inside the $19 Billion Investment Boom

Indonesia’s Rupiah Balancing Act: Growth Surges as Singapore Capital Pours In

Malaysia GDP Forecast Raised to 4.9% as $23 Trillion Descends on Singapore

The Bank of England Just Modelled an AI Crash — Here’s What It Found

Pakistan Economy 2026: IMF Growth Warning vs. a Booming KSE-100

Russia’s Oil Sanctions Paradox: Why Revenue Is Rising, Not Falling

China GDP Growth Misses Target: What’s Behind the 4.3% Slowdown

The Strait of Hormuz Shock Nobody Has Priced In Yet

Fed Rate Hikes 2026: Why Kevin Warsh Is Reversing the Cut Cycle

Gold Price 2026: How Central Banks Made Gold Bigger Than US Treasuries in Reserves

Fed Chair Kevin Warsh’s AI Rate Bet 2026: Inside the FOMC Split on Productivity vs Inflation

Dubai Real Estate 2026: Inside the $5.1 Billion Ultra-Prime Boom and the Cooling Mid-Market

Bank of Canada 2026: Why the 0.7% Growth Cut Hides a Deeper Tariff-Adaptation Story

Top 7 Banking Stocks for Investment in PSX: Pakistan’s Lenders Are Still Printing Money

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

JPMorgan Cuts Anthropic AI Access in Hong Kong

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Why China’s Demand Stimulus Still Isn’t Working

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

India Economic Rise 2026: How the Subcontinent Toppled Japan

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025