International Trade

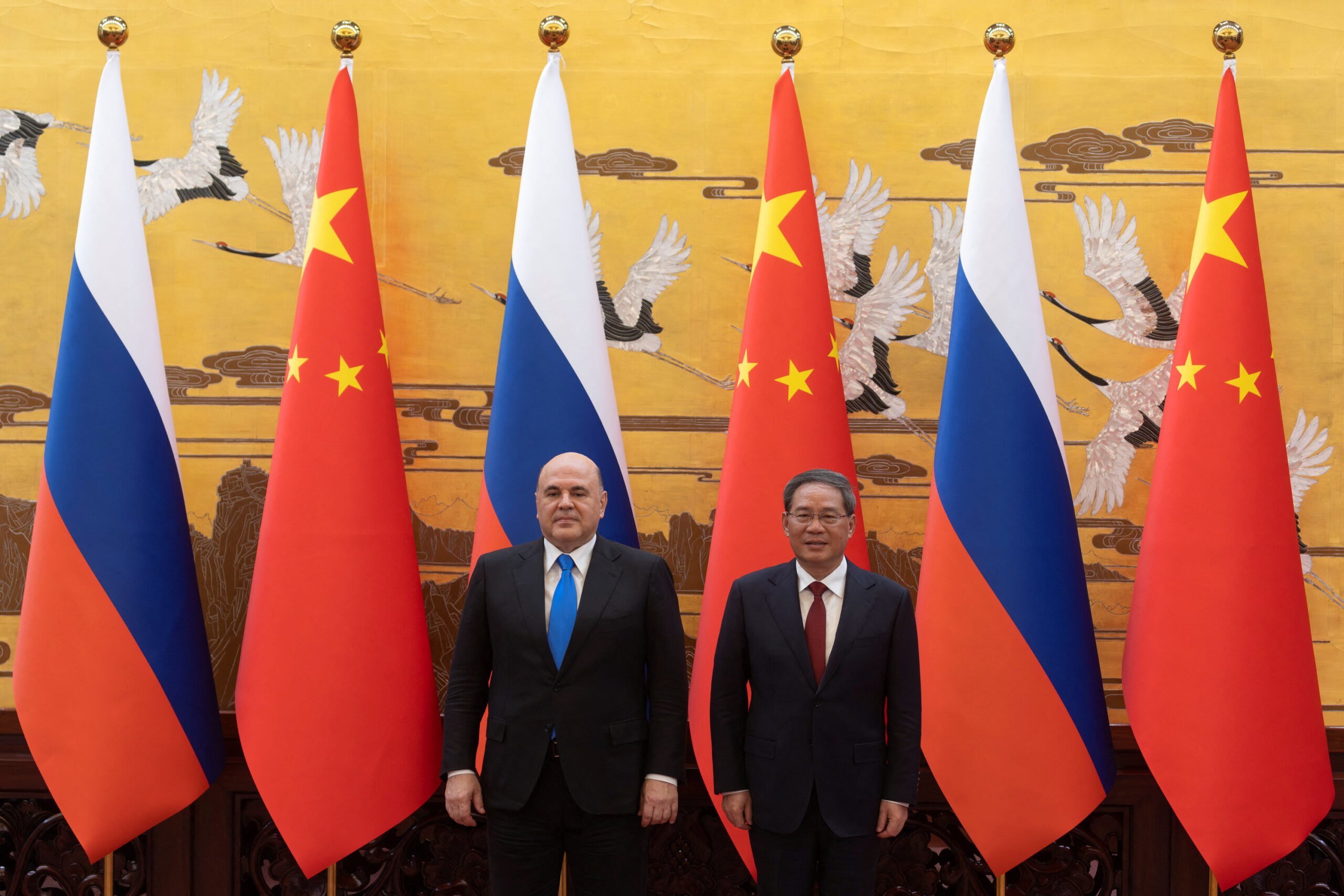

China-Russia Trade: Signs of Decline Despite 2026 Agreements

Despite Vladimir Putin’s May 2026 Beijing visit and more than 20 new cooperation agreements signed with Xi Jinping, analysts say China-Russia trade is approaching the limits of what the relationship can economically deliver, with bilateral trade actually declining in 2025 for the first time since the pandemic.

The Numbers Behind the Political Theater

Bilateral trade grew 55% between 2021 and 2025, comfortably surpassing the two countries’ shared $200 billion target set in 2019 — but trade actually fell 7% to $227.6 billion in 2025, marking the first annual decline since the pandemic year of 2020, according to The Moscow Times. Economist Andrei Gnidchenko of Moscow-based analytical center CMAKP said trade growth is likely to slow further in the second half of 2026 as China builds up its own energy reserves and economic activity in both countries remains subdued, estimating full-year trade will land only 5%–10% above 2025 levels — roughly flat with 2024.

Q1 2026 customs data tells a more nuanced story: trade turnover exceeded $61 billion in the first three months, up 14.8% year-on-year, with Russian imports of Chinese goods growing 22% to $27.7 billion and Russian exports to China — dominated by energy — rising 9% to $33.6 billion, according to European Business Magazine.

The May 2026 Beijing Summit

On May 16–17, 2026, Xi and Putin signed two joint statements in Beijing — one deepening their “comprehensive strategic partnership of coordination for a new era” and another renewing the Treaty of Good-Neighborliness and Friendly Cooperation — alongside more than 20 bilateral agreements spanning energy, trade, technology, and media, according to analysis from Indoneo. Both sides also reaffirmed support for India’s BRICS chairmanship in 2026 and pledged deeper cooperation within the BRICS Economic Partnership Strategy framework, per the official joint statement.

Carnegie Russia Eurasia Center director Alexander Gabuev has characterized the summit as evidence Moscow has effectively accepted a junior role in the relationship, trading growing economic dependence on Beijing for diplomatic cover and continued economic survival amid Western sanctions and confrontation, according to Indoneo’s analysis.

Where the Friction Is Emerging

Behind the diplomatic choreography, real frictions are growing over energy pricing, banking channels, and Russian customs duties on Chinese vehicles, according to reporting from Insight EU Monitoring. The long-discussed Power of Siberia 2 pipeline remains unresolved more than a year after Gazprom’s original memorandum, with China’s own 2026-2030 Five-Year Plan committing only to “advance preparatory work” rather than a firm construction timeline. China has also signaled through its energy diversification strategy — expanding solar, wind, and alternative suppliers — that it is no longer as dependent on Russian energy as it was in 2022, giving Beijing more leverage to negotiate lower prices.

What It Means for Global Markets

For Western policymakers, the persistence of the China-Russia trade relationship — even amid signs of cooling — remains the clearest evidence that four years of sanctions pressure has not fractured the alignment, according to Indoneo. But the slowing growth rate suggests the relationship may be maturing into a more transactional, price-sensitive phase rather than continuing its post-2022 boom trajectory — a dynamic that will shape everything from global energy flows to the yuan’s role in bilateral settlement.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Indonesia posted its first trade deficit in six years as imports soared and June inflation rose to 3.34% year-on-year. While most coverage attributes this to rising imports generally, the more specific and underreported cause is a policy collision: a new mandatory B50 biodiesel program raising domestic fuel costs just as a temporary coal export suspension cut into one of Indonesia’s most reliable trade-surplus generators.

The headline number, and the policy story behind it

Indonesia logged its first trade deficit in six years as imports surged, according to Nikkei Asia’s tracking of the country’s trade data, with Southeast Asia’s largest economy now weighed down by a higher energy import bill (Nikkei Asia). June inflation climbed to 3.34% year-on-year (Indonesia Investments).

What’s been under-explained is why this happened now, specifically. Two domestic energy-policy moves collided in the same window:

First, the B50 mandate. The Indonesian government officially began mandating a 50%-palm-oil-blend biodiesel program (B50) on July 1, 2026, replacing the previous B40 standard. A three-month adjustment period was granted to fuel companies to transition operations and deplete existing B40 stock before full implementation in October (Monitorday). While the mandate is aimed at reducing Indonesia’s reliance on imported diesel over the medium term, the transition period itself has created near-term cost and supply friction.

Second, a coal export suspension. The government temporarily suspended some coal exports specifically to address rolling blackouts, redirecting supply toward the domestic grid rather than international buyers (Nikkei Asia). Notably, some miners reportedly preferred paying fines over selling into the lower-priced domestic market, according to industry observers tracking the policy’s enforcement — a sign of how costly the suspension has been for exporters used to global pricing (Nikkei Asia). Coal has historically been one of Indonesia’s most consistent trade-surplus contributors; suspending exports even temporarily removes a meaningful offset just as import costs are climbing.

The manufacturing and consumer backdrop

This isn’t happening in isolation. Manufacturing activity was largely in contraction during Q2 2026, consumer confidence has been declining, and retail sales are showing weakness — all compounding the deficit’s effects on near-term growth momentum (Indonesia Investments). Bank Indonesia’s higher benchmark interest rate environment, currently at 5.75%, is also weighing on activity while pushing up government bond yields.

The government’s response, and what it signals

Indonesia’s Coordinating Ministry for Economic Affairs has outlined a four-step response aimed at preserving the government’s 5.4% growth target for 2026, including maintaining purchasing power through transportation discounts, exempting import duties on LPG for petrochemicals, plastic raw materials and aircraft spare parts, among other targeted stimulus measures (Indonesia Investments). The government has also rolled out an additional IDR 26.34 trillion economic stimulus package for the second half of the year (Business Indonesia).

Why global lenders still aren’t alarmed

Despite the deficit, the IMF maintained its Indonesia growth projection at 5.0% for 2026 in its July 2026 World Economic Outlook update, comfortably above the 3.0% global average forecast, while urging Indonesia to hold firm on its 3%-of-GDP budget deficit ceiling and pursue tax administration reform to strengthen revenue collection (Indonesia Investments). Indonesia’s sovereign wealth fund, the Indonesia Investment Authority, has also mobilized roughly IDR 74.5 trillion (about USD 4.7 billion) in investments with global partners over its first five years, retaining investment-grade ratings from Fitch and a governance score above the global sovereign wealth fund average (Business Indonesia).

What businesses should watch

The trade deficit is likely to be transitional rather than structural — but only if the B50 adjustment period completes smoothly by October and the coal export suspension is genuinely temporary. Businesses with energy-cost exposure in Indonesia should model both a base case (deficit narrows as biodiesel transition completes) and a downside case (coal suspension extends, energy import costs stay elevated into Q4).

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

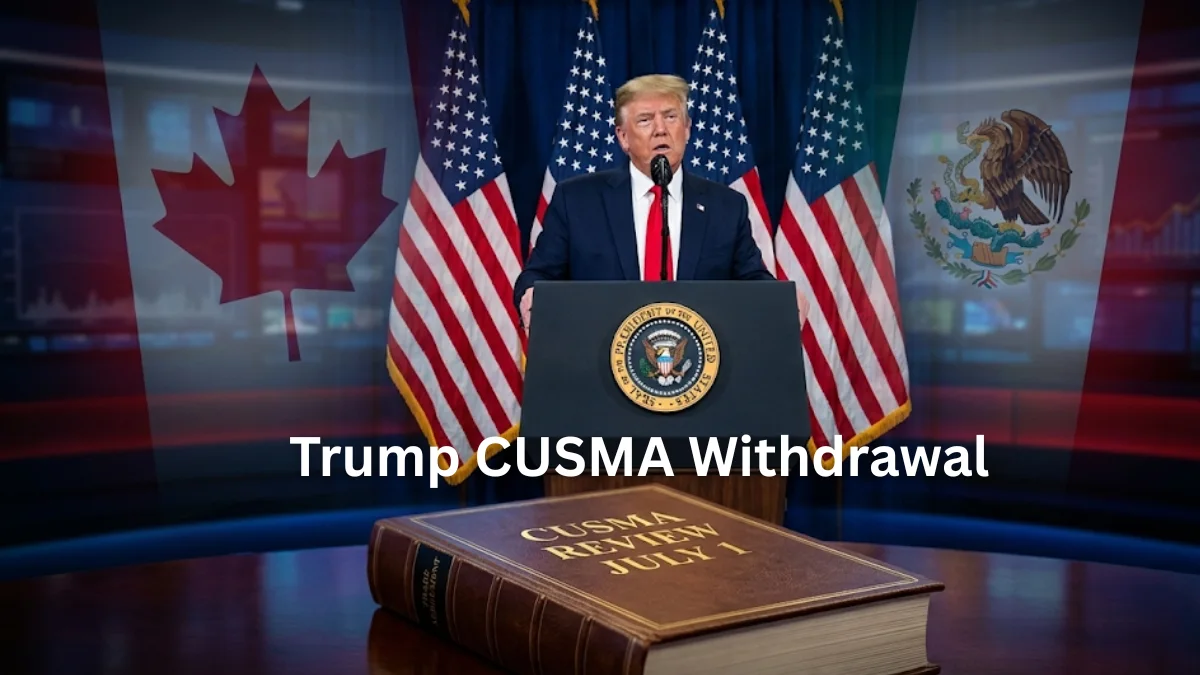

The mandatory CUSMA review deadline passed on July 1, 2026 without a new agreement. Rather than triggering an immediate shock, it defaulted to a rolling annual-review process that could extend uncertainty until 2036 — and economists say that open-ended uncertainty, not the tariffs currently in place, is the bigger structural drag on Canadian business investment.

The story most coverage missed

Headlines framed the July 1 CUSMA deadline as a binary event: deal or no deal. What actually happened is more consequential and far less clean. The Canada-United States-Mexico Agreement review had three possible outcomes — a 16-year renewal (which Canada and Mexico pushed for), a 10-year extension with annual reviews, or a full replacement framework. None of those happened cleanly. Instead, the process rolled into annual reviews with tariffs still in place, meaning the “cloud of uncertainty” that has depressed business investment for the past five consecutive quarters doesn’t lift — it just resets on a yearly clock, according to TD Economics (TD Bank).

That distinction matters enormously for how Canadian businesses plan capital spending. A known 16-year horizon lets a manufacturer plan a decade of investment. An annual review process means every major capital decision now carries a built-in one-year uncertainty discount, indefinitely, until 2036 (The Hub).

The numbers behind the “not quite a recession” narrative

Canada’s economy met the technical definition of recession — two consecutive quarterly GDP declines spanning late 2025 into early 2026 — but most economists, including Bank of Canada Governor Tiff Macklem, have pushed back on the recession label, noting the weakness is concentrated in specific tariff-exposed sectors like steel, aluminum and lumber rather than being broad-based (BNN Bloomberg).

The sectoral divergence is stark. Canada’s exports to the U.S. fell roughly 10% over the past year, and the U.S. share of Canadian exports dropped to 71.7% — its lowest level since the early 1980s (The Hub). Yet at the same time, real GDP expanded 0.5% in April alone — the strongest monthly growth since July 2025 — driven overwhelmingly by energy production, with Western Canadian Select crude trading more than 30% above its start-of-year level (BNN Bloomberg).

Energy is masking a manufacturing problem

This is the underreported tension in Canada’s 2026 economic story: energy — boosted paradoxically by the same Middle East conflict driving up costs elsewhere — is carrying headline GDP numbers even as tariff-exposed manufacturing continues to bleed. Auto-sector output remains below pre-tariff levels, and Ontario communities dependent on factory employment face what analysts call the “big question” of whether manufacturing can recover before the annual-review cycle grinds on for another decade (BNN Bloomberg).

What comes next

The Bank of Canada projects GDP will finish 2026 roughly 1.5% below its pre-tariff trajectory, with about half of that shortfall attributed to reduced potential output rather than a temporary shock (The Hub). Deloitte Canada forecasts growth of just 0.7% for 2026, rebounding to 2% in 2027 once — and if — trade clarity finally arrives (BNN Bloomberg).

For Canadian businesses, the practical takeaway is that “waiting for CUSMA clarity” is no longer a strategy with a defined end date. Firms in tariff-exposed sectors should plan for a multi-year uncertainty regime rather than a near-term resolution — while businesses tied to energy, construction, and non-U.S. export markets are likely to keep outperforming.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Indonesia’s balance of trade turned negative for the first time in six years, with skyrocketing oil prices pushing up import costs while weak global demand simultaneously suppressed exports (The Jakarta Post). That headline alone would normally dominate a news cycle. But it’s actually the second-most important economic story unfolding in Indonesia right now — and understanding why requires looking past the trade numbers to what’s happening with the rupiah and the country’s manufacturing base simultaneously.

The Currency Squeeze

The rupiah has been under sustained pressure, trading near Rp 18,000 per US dollar as weak manufacturing data and concerns over Indonesia’s foreign exchange reserves weighed on sentiment (Jakarta Globe). Bank Indonesia has responded with aggressive rate hikes specifically aimed at defending the currency — a defensive posture that international ratings agency Fitch has characterized as underscoring the central bank’s resolve amid policy uncertainty and investor concern (Jakarta Globe).

That’s an important signal in itself: when a central bank is hiking rates primarily to defend a currency rather than to cool domestic demand, it usually means the currency pressure is coming from external or structural sources that domestic monetary policy can only partially offset.

The Manufacturing Collapse Hiding Behind the Trade Headline

Here’s the detail that deserves far more attention than it’s getting: Indonesia’s manufacturing sector suffered its sharpest contraction in a year, with the S&P Global Indonesia Manufacturing PMI plunging to 46.9 in June from 50.0 in May — the exact threshold separating expansion from contraction. New orders dried up while factory-gate prices rose at their fastest pace in nearly 13 years (The Jakarta Post).

That combination — collapsing new orders alongside accelerating input costs — is a genuinely difficult one for policymakers to address, because it doesn’t respond cleanly to either rate hikes (which would further squeeze weak demand) or rate cuts (which would worsen currency pressure and imported inflation). It’s the kind of stagflationary bind that tends to get buried under trade-deficit headlines but actually poses the harder policy problem.

Rising Inflation From an Unexpected Source

Indonesia’s June inflation accelerated to 3.34%, driven higher by rising non-subsidized fuel prices and airfares that pushed up transport costs specifically (Jakarta Globe). Gasoline alone was the largest single contributor to transportation inflation, adding 0.21 percentage points, with airfare and engine lubricants following close behind (The Jakarta Post).

This matters because it shows Indonesia’s inflation is currently import- and energy-driven rather than demand-driven — reinforcing why Bank Indonesia keeps the door open for further rate hikes even as domestic manufacturing and household purchasing power weaken simultaneously.

Danantara: The Sovereign Wealth Fund Under Scrutiny

Running parallel to the trade and currency story is a governance controversy around Danantara, Indonesia’s consolidated sovereign wealth vehicle. Finance Minister Purbaya has had to publicly defend Danantara’s “Patriot Bond” program, rejecting money laundering allegations after a civil society coalition formally appealed to the Financial Action Task Force (FATF) requesting an investigation into changes to Indonesia’s financial law (Jakarta Globe).

Separately, Indonesia’s existing sovereign wealth fund, INA (Indonesia Investment Authority), reported it has mobilized $4.7 billion in investments and secured $25 billion in additional commitments since its 2021 launch, with its new chief executive stating no immediate plans to issue debt because the fund holds sufficient capital despite recent market volatility affecting parts of its portfolio (The Jakarta Post). Danantara’s first consolidated financial report has been described by independent economists as a positive step toward transparency, though they stress timely disclosure and stronger governance remain essential going forward (Jakarta Globe).

For international investors, the FATF appeal specifically is worth monitoring closely — a formal international financial-crime watchdog inquiry, even if it ultimately clears the fund, introduces a reputational and compliance overhang that can affect how comfortable large institutional investors feel deploying capital alongside Danantara-linked vehicles in the near term.

Indonesia’s Answer: A New International Financial Hub

In the middle of this currency and governance turbulence, Indonesia is simultaneously moving forward with plans to launch a new international financial hub explicitly designed to attract global investors into government bonds and development projects, structured with a common-law framework modeled on Singapore’s approach rather than Indonesia’s existing civil-law system (Jakarta Globe).

That’s a notable structural bet — building a legally distinct enclave specifically to offer foreign investors the kind of contract predictability and dispute-resolution familiarity that Singapore has used to become Southeast Asia’s dominant financial centre. Whether it succeeds will depend heavily on execution details that remain largely unannounced.

The Coal Export Standoff: A Microcosm of the Bigger Tension

A smaller but telling story illustrates the friction between Indonesia’s export ambitions and domestic energy needs: the government temporarily suspended some coal exports to address rolling blackouts, but miners have shown they’re willing to export coal and simply pay resulting fines rather than sell into the domestic market at lower mandated prices (Nikkei Asia). That’s a clear signal that global coal prices currently offer a big enough premium over domestic obligations that financial penalties aren’t an effective deterrent — a policy design problem regulators will likely need to revisit.

What Foreign Investors Are Actually Doing Right Now

Despite all of this turbulence, foreign investors have poured $9 billion into Indonesian securities this year, with higher interest rates specifically boosting market confidence in fixed-income instruments (Jakarta Globe). That’s a genuinely important counter-signal to the doom-and-gloom trade deficit headlines — it suggests sophisticated capital is treating Indonesia’s higher-rate environment as a yield opportunity rather than purely a risk signal, even as the rupiah struggles.

What to Watch Next

The practical signals worth tracking over the coming months: whether Bank Indonesia’s rate path stabilizes or requires further hikes if June’s inflation trend persists; whether the June PMI contraction proves to be a one-month blip or the start of a sustained manufacturing downturn; how the FATF inquiry into Danantara’s Patriot Bond program resolves; and whether concrete details emerge on the new common-law international financial hub, which could meaningfully change Indonesia’s positioning as a capital markets destination if executed well.

The Bottom Line

Indonesia’s first trade deficit in six years is a real and legitimate warning sign, but it’s arguably the most visible symptom of a more complex underlying story: a currency under structural pressure, a manufacturing sector contracting for the first time in a year, energy-driven inflation squeezing households, and a sovereign wealth governance question still working through international scrutiny — all happening while foreign capital continues flowing into Indonesian bonds and the government bets on a Singapore-style financial hub to secure the country’s next growth chapter. Investors and businesses tracking only the trade balance headline are missing most of the actual story.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

CUSMA Review Deadline: Economic Impacts on Canada

Bank of England Rate Decision Amid Energy Crisis

China-Russia Trade: Signs of Decline Despite 2026 Agreements

US Charges in Nvidia Export Control Scheme

Johor-Singapore Special Economic Zone Progress Update

Pakistan Economy 2026: GDP Grows 3.7% as IMF Completes EFF Review Amid Middle East Risk

Gold Price Forecast 2026: Fed’s July 29 Decision and Record Central Bank Buying Explained

Global Stock Market Selloff 2026: Stagflation Fears Return as Iran Conflict Reignites

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Russia Oil Revenue 2026: How the Hormuz Crisis Is Undermining Western Sanctions

Apple vs OpenAI Lawsuit: The Economic Story Behind the Headline

Pakistan’s KSE-100 Surged 44% in FY26 — But Its Foundation Is Fragile

Indonesia’s First Trade Deficit in 6 Years: The B50 and Coal Connection

Russia’s Shadow Fleet Insurance Economy: How Sanctions Really Work in 2026

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Top 7 Banking Stocks for Investment in PSX: Pakistan’s Lenders Are Still Printing Money

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

India Economic Rise 2026: How the Subcontinent Toppled Japan

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Why China’s Demand Stimulus Still Isn’t Working

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025