Analysis

Top 10 Stocks for Investment in PSX for Quick Returns in 2026

Imagine turning a modest investment into a meaningful gain while Pakistan rewrites its economic story. That’s not wishful thinking — it’s the very real opportunity sitting in the Pakistan Stock Exchange (PSX) right now, in February 2026.

The KSE-100 has staged one of Asia’s most dramatic recoveries over the past 18 months. Backed by IMF support, falling inflation, improving forex reserves, and a central bank that has been carefully unwinding its aggressive rate cycle, Pakistan’s equity market has rewarded the bold. The question is: where does the next wave of gains come from? Which are the best Pakistan Stock Exchange investments short-term heading into mid-2026?

We’ve done the hard work. Drawing on real-time PSX data, earnings releases, sector research, and macroeconomic modeling, we’ve identified the top 10 stocks for quick returns on PSX in 2026. These aren’t long shots. They are fundamentally strong companies in structurally advantaged sectors — banking, energy, cement, technology, and agri-manufacturing — that are positioned to deliver 20–40% upside within 3–6 months based on current valuations and forward catalysts.

“Pakistan’s KSE-100 has been among the world’s best-performing markets over the past 12 months. With GDP growth projected at 4–5% in 2026, the rally may only be in its second inning.” — IMF Article IV Consultation, Pakistan, 2025–26

The IMF’s extended fund facility of approximately $7 billion has stabilized the macroeconomic framework. Inflation, which peaked above 38% in mid-2023, has collapsed toward single digits. The State Bank of Pakistan has cut its policy rate aggressively, injecting liquidity into equity markets. Foreign portfolio investors have returned. And corporate earnings — particularly in banking — have been nothing short of spectacular. As Yahoo Finance and local analysts have both noted, Pakistan’s risk premium is finally compressing.

But macro tailwinds only tell half the story. Stock picking matters. So let’s get into it.

Table of Contents

- UBL — United Bank Limited

- MCB — MCB Bank Limited

- MEBL — Meezan Bank Limited

- HBL — Habib Bank Limited

- MTL — Millat Tractors Ltd.

- PPL — Pakistan Petroleum Limited

- PSO — Pakistan State Oil Co. Ltd.

- FCCL — Fauji Cement Company Limited

- SYS — Systems Limited

- LUCK — Lucky Cement Limited

Data Note: All prices and metrics reflect PSX data as of mid-February 2026. Projected upside figures are analyst consensus estimates and should not be taken as guaranteed returns. Always consult a licensed financial advisor before investing.

🏦 PSX Banking Stocks — The Engine Room of Quick Gains

If you’re looking for PSX banking stocks quick gains, you’ve picked the right sector. Pakistan’s commercial banking industry has been the single biggest beneficiary of the high interest rate era — and even as rates ease, banks are proving their earnings resilience through fee income, digital growth, and improving asset quality. Four of our top 10 picks come from this sector.

1. UBL — United Bank Limited

PSX: UBL | Commercial Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 455–465 |

| P/E Ratio (TTM) | 6.08× |

| 1-Year Return | +121–140% |

| 52-Week Range | Rs. 188–517 |

| Market Cap | ~Rs. 1.24T |

| Projected 3–6M Upside | 15–30% |

If one stock captures the spirit of Pakistan’s financial renaissance, it’s UBL. The bank has delivered a staggering 121–140% return over the past year — and yet, at a trailing P/E of just 6.08×, it remains one of the most undervalued large-cap banking stocks in the region. That’s the paradox of PSX: even after enormous rallies, valuations still look cheap by global standards.

UBL’s Q3 FY2026 earnings, reported February 25, 2026, are expected to show continued momentum. The bank declared an interim dividend of Rs. 8 per share — representing a 160% payout — signaling management confidence in the earnings trajectory. Its Middle East franchise adds geographic diversification that peers simply don’t have, providing a hedge against any domestic policy volatility.

Analyst consensus on Investing.com pegs the 12-month price target at Rs. 475 (low: 391, high: 590), with three analysts unanimously rating it a Strong Buy. Technical analysts identify a breakout zone between Rs. 510–570 if the bank’s earnings beat expectations — a realistic scenario given the revenue momentum. This makes UBL the standout choice for anyone seeking high return PSX stocks in 2026.

✅ Key Strengths

- Lowest P/E (6.08×) among major banks — deeply undervalued

- Middle East operations provide dollar-revenue diversification

- Strong Rs. 8/share interim dividend declared

- EPS of Rs. 50.62 (TTM), net income Rs. 35.36B in Q3

- All 3 covering analysts rate it Strong Buy

⚠️ Key Risks

- Earnings sensitivity to policy rate cuts compressing margins

- High beta (1.49) — amplifies market-wide volatility

- Significant pullback from ATH of Rs. 517

↑ Projected 3–6 Month Upside: 15–30% | Target: Rs. 520–590

2. MCB — MCB Bank Limited

PSX: MCB | Commercial Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 412–415 |

| P/E Ratio (TTM) | 9.03× |

| 1-Year Return | +47.96% |

| 52-Week Range | Rs. 247–452 |

| YTD Change | +8.82% |

| Projected 3–6M Upside | 15–25% |

MCB Bank is the quiet achiever of Pakistan’s banking sector — less flashy than its peers but relentlessly profitable. With one of the highest return-on-equity ratios in the industry and a legendary history of dividend consistency, MCB is the kind of stock institutional investors quietly accumulate while retail traders chase headlines.

The bank’s YTD performance of +8.82% already puts it ahead of most peer markets globally in just six weeks of 2026. Its 52-week high of Rs. 452 suggests significant re-rating potential from current levels, especially if Q4 FY2025 earnings — which typically coincide with strong full-year dividend announcements — beat the Street’s estimates. MCB’s digital banking transformation has accelerated, with mobile banking active users growing at double-digit rates quarter on quarter.

For investors seeking undervalued stocks PSX for quick profits, MCB’s combination of a sub-10× P/E, above-peer ROE, and an upcoming dividend catalyst makes it a compelling short-term entry. It consistently outperforms sector averages on profitability metrics, as tracked by SCS Trade market valuations.

✅ Key Strengths

- Legendary dividend consistency — a reliable income kicker

- Strong ROE, one of the highest in Pakistani banking

- 8.82% YTD gain signals strong early 2026 momentum

- Lower beta than UBL — relatively defensive upside play

⚠️ Key Risks

- Higher P/E (9.03×) vs. UBL — slightly less compelling on value

- Net Interest Income sensitivity as SBP cuts rates further

- Down ~9% from 52-week high — needs a catalyst to break resistance

↑ Projected 3–6 Month Upside: 15–25% | Target: Rs. 475–515

3. MEBL — Meezan Bank Limited

PSX: MEBL | Islamic Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 485–490 |

| Market Cap | ~Rs. 884B |

| 1-Year Return | +104% |

| 52-Week ATH | Rs. 505 |

| Analyst Target High | Rs. 672 |

| Projected 3–6M Upside | 10–38% |

Meezan Bank is not just a bank — it’s a structural growth story riding one of the most powerful demographic and ideological tailwinds in Pakistan: the shift toward Islamic finance. As Pakistan’s largest Islamic bank, MEBL controls a growing share of a market that by definition cannot go to conventional competitors. That’s a moat you can take to the bank.

The stock surged over 104% in the past year, touching an all-time high of Rs. 505 in January 2026. It’s now consolidating just below that level, setting up what technical analysts describe as a re-accumulation base before the next leg higher. Analyst targets range from Rs. 510 to a bullish Rs. 672 — implying a potential 38% upside from current levels.

MEBL’s beta of 0.89 is the lowest of our four banking picks, meaning it offers smoother, more defensive upside — ideal for risk-aware investors who want exposure to PSX banking stocks quick gains without the full volatility of higher-beta names.

✅ Key Strengths

- Structural moat as Pakistan’s leading Islamic bank

- Lowest beta (0.89) among banking picks — defensive growth

- 104% 1-year return with re-accumulation base forming

- Analyst high target of Rs. 672 implies 38% upside

⚠️ Key Risks

- Islamic finance regulations can shift policy framework

- Valuation premium to peers — less pure value play

- Earnings date delayed to April 28 — near-term catalyst gap

↑ Projected 3–6 Month Upside: 10–38% | Target: Rs. 530–672

4. HBL — Habib Bank Limited

PSX: HBL | Commercial Banking

| Metric | Value |

|---|---|

| Current Price | Rs. 320–345 |

| Market Cap | ~Rs. 500B |

| 52-Week ATH | Rs. 369.99 |

| Dividend Yield (2024) | 9.31% |

| Net Income (Q3) | Rs. 16.91B |

| Projected 3–6M Upside | 10–20% |

Pakistan’s largest bank by assets and deposits, HBL carries the weight of the nation’s financial system on its balance sheet — and has delivered accordingly. With a dividend yield of 9.31% in 2024 and a network spanning over 1,700 branches domestically plus international presence across major financial hubs, HBL is the blue-chip anchor of any serious PSX portfolio.

HBL hit its all-time high of Rs. 369.99 in January 2026 before a modest pullback, which has created a potential buy-on-dip opportunity. An upcoming earnings release on February 19, 2026 is a near-term catalyst — with Q3 net income of Rs. 16.91B and improving non-interest income streams, any positive surprise could spark a fresh leg higher. As the Financial Times has noted in its coverage of emerging market banking recoveries, HBL-type institutions with strong deposit franchises tend to be the last to be sold and the first to re-rate.

✅ Key Strengths

- Pakistan’s largest bank — systemic importance = government backstop

- 9.31% dividend yield (2024) — exceptional income return

- Earnings release Feb 19 is an immediate near-term catalyst

- International network adds revenue diversification

⚠️ Key Risks

- Q3 net income slightly down (-4.92%) from Q2 — watch margin trends

- Regulatory compliance costs remain elevated post-FATF period

- Dividend payout ratio relatively low (40.78%) — upside depends on growth

↑ Projected 3–6 Month Upside: 10–20% | Target: Rs. 355–415

🚜 Agri-Manufacturing: The Underappreciated Performer

5. MTL — Millat Tractors Ltd.

PSX: MTL | Automotive / Agri-Manufacturing

| Metric | Value |

|---|---|

| Sector | Agri-Equipment |

| Market Position | Market Leader |

| Dividend History | Very Strong |

| ROE Profile | High |

| Currency Sensitivity | PKR / USD inputs |

| Projected 3–6M Upside | 15–25% |

Agriculture is Pakistan’s economic backbone, contributing around 22% of GDP and employing nearly half the workforce. That makes Millat Tractors — the dominant domestic manufacturer of Massey Ferguson tractors — one of the most defensible businesses in the country. When farmers invest in mechanization, MTL wins, regardless of the broader economic cycle.

Pakistan’s government has consistently supported agricultural mechanization through subsidized tractor schemes, and with food security remaining a political priority, that support is unlikely to wane. MTL commands a dominant share of the tractor market, benefits from strong brand loyalty, and operates an efficient manufacturing setup that generates consistently high ROE. The stock’s rich dividend history makes it an attractive proposition for investors who want capital appreciation plus income — a rarer combination than most PSX stocks offer.

What gives MTL its edge over competitors like Al-Ghazi Tractors is the sheer depth of its distribution network and its after-sales parts business — a high-margin revenue stream that competitors struggle to replicate. As the IMF-backed economic stabilization filters into rural consumption, MTL’s tractor sales volumes are expected to accelerate through H1 2026.

✅ Key Strengths

- Dominant market share with Massey Ferguson franchise

- Government tractor subsidy schemes are structural tailwinds

- High-ROE business with consistent dividend history

- Agri-revival theme plays into Pakistan’s food security push

⚠️ Key Risks

- Input cost sensitivity — steel and imported components in USD

- Seasonal sales cycle can create quarterly volatility

- Lower free float limits institutional accumulation speed

↑ Projected 3–6 Month Upside: 15–25%

⛽ Energy Sector PSX — High Upside, Underappreciated Value

The energy sector PSX high upside thesis is built on three pillars: recovering global commodity prices, domestic energy transition policies, and historically suppressed valuations that are only now beginning to reflect the sector’s true earnings power.

6. PPL — Pakistan Petroleum Limited

PSX: PPL | Oil & Gas Exploration

| Metric | Value |

|---|---|

| Recent ATH (Jan ’26) | Rs. 284.60 |

| Current Zone | Rs. 255–270 |

| Market Cap | ~Rs. 643B |

| Beta | 1.45 |

| Daily Volatility | 5.00% |

| Projected 3–6M Upside | 15–35% |

Pakistan Petroleum is in the middle of a classic consolidation-after-breakout pattern. After surging to a fresh all-time high of Rs. 284.60 in January 2026, the stock has pulled back toward its strong support zone between Rs. 255–265. Technically, this is precisely the kind of structure that experienced swing traders and medium-term investors love: a high-quality business at a discount relative to its recent peak, with multiple catalysts ahead.

PPL is Pakistan’s second-largest gas producer, with exploration assets across major proven fields. Its earnings are directly leveraged to wellhead gas prices, which remain linked to global energy benchmarks. With Pakistan’s energy import bill remaining a structural burden, domestic gas production is a geopolitical priority — meaning PPL’s assets have strategic value beyond pure commercial metrics. Technical analysts on TradingView project targets between Rs. 290 and Rs. 386 over the next 7–9 months based on Cup-and-Handle breakout patterns.

✅ Key Strengths

- Strategic asset — domestic energy security play

- Pulled back to strong technical support (Rs. 255–265)

- Earnings release April 28 — forward catalyst in sight

- Technical targets Rs. 290–386 on breakout confirmation

⚠️ Key Risks

- High beta (1.45) and 5% daily volatility — not for weak hands

- Circular debt in Pakistan’s energy sector remains a systemic risk

- Government pricing controls can cap realized wellhead prices

↑ Projected 3–6 Month Upside: 15–35% | Target: Rs. 295–385

7. PSO — Pakistan State Oil Co. Ltd.

PSX: PSO | Oil Marketing

| Metric | Value |

|---|---|

| Current Price | Rs. 465–475 |

| 52-Week ATH | Rs. 506.75 |

| 52-Week Low | Rs. 300 |

| Analyst Target (Avg) | Rs. 646 |

| Upside to Consensus | +38% |

| Analyst Rating | Strong Buy (7/7) |

PSO is arguably the single most compelling undervalued PSX stock for quick profits in the energy space right now. Pakistan’s dominant oil marketing company — controlling roughly 50% of the country’s petroleum product distribution — is trading at a massive discount to what 7 covering analysts believe it’s worth: an average target of Rs. 646.47, with a high estimate of Rs. 900. At current prices near Rs. 467, that implies 38% upside to consensus and nearly 93% to the most bullish estimate.

What’s depressing the stock? Historically, PSO has been weighed down by circular debt owed to it by power utilities and the government — a structural problem that the IMF program is specifically addressing. As recoveries from the circular debt pile accelerate, PSO’s free cash flow could inflect sharply upward. The company’s Q3 net income surged 154.87% quarter-on-quarter to Rs. 10.53 billion — a sign that the earnings recovery is already underway. As Economy.com.pk has highlighted, PSO consistently appears in top picks lists for 2026, and the data backs it up.

✅ Key Strengths

- 7/7 analysts rate it Strong Buy — extraordinary consensus

- 38% upside to analyst consensus, 93% to bull case

- 154.87% Q-o-Q net income surge signals earnings inflection

- Circular debt resolution = massive balance sheet catalyst

⚠️ Key Risks

- Circular debt resolution timeline remains uncertain

- Government fuel pricing decisions cap margin upside

- High revenue (Rs. 775B/quarter) but thin EBITDA margins (~1.6%)

↑ Projected 3–6 Month Upside: 20–38%+ | Consensus Target: Rs. 646

🏗️ Cement Sector — Rebuilding Pakistan, Brick by Brick

Pakistan’s infrastructure deficit is well-documented — and the government’s infrastructure push, coupled with private sector housing demand, positions the cement sector as a multi-year growth story. Two picks offer distinct risk-reward profiles within this space.

8. FCCL — Fauji Cement Company Limited

PSX: FCCL | Cement Manufacturing

| Metric | Value |

|---|---|

| Market Cap | ~Rs. 131B |

| Dividend Yield | 2.34% |

| Payout Ratio (2025) | 23% |

| Beta | 1.08 |

| Technical Target | Rs. 57–60 |

| Projected 3–6M Upside | 15–25% |

Fauji Cement is the value pick in the cement space — a mid-cap name backed by the rock-solid Fauji Foundation, one of Pakistan’s largest institutional investors. That institutional backing means better governance, stronger balance sheet discipline, and typically faster access to financing for capacity expansion. Technical analysts have identified a bullish Cup-and-Handle breakout pattern on FCCL, with targets at Rs. 57.80 and Rs. 60 — representing 15–25% upside from current levels.

With earnings due February 25, 2026, FCCL is a near-term catalyst play. Pakistan’s cement dispatches have been recovering with infrastructure spending, and FCCL’s northern market exposure positions it well for CPEC-linked construction activity. A low payout ratio of 23% means the company is reinvesting aggressively — setting up for stronger future earnings growth.

✅ Key Strengths

- Institutional Fauji Foundation backing — governance premium

- Cup-and-Handle breakout forming — bullish technical setup

- Earnings catalyst February 25, 2026

- CPEC infrastructure exposure is a structural tailwind

⚠️ Key Risks

- EPS missed estimates by 12.58% last quarter — execution risk

- Cement sector overcapacity puts pressure on pricing

- Coal price spikes (imported fuel) can compress margins

↑ Projected 3–6 Month Upside: 15–25% | Target: Rs. 57–62

💻 Technology: Pakistan’s Hidden Gem in the Global IT Race

9. SYS — Systems Limited

PSX: SYS | Information Technology

| Metric | Value |

|---|---|

| Sector | IT / IT Export |

| Revenue Currency | USD-Dominated |

| Export Growth | Strong (20%+ YoY) |

| Business Type | Software / Services |

| Currency Hedge | Natural (USD revenues) |

| Projected 3–6M Upside | 20–35% |

In a market dominated by banks and commodity plays, Systems Limited stands apart as Pakistan’s premier technology exporter — and arguably the most underappreciated growth story on the entire PSX. SYS earns a significant portion of its revenues in US dollars through software development and IT services exports to North American and European clients, giving it a natural hedge against any rupee weakness. That’s a quality you won’t find in any bank or cement stock.

Pakistan’s IT sector has been one of the standout performers of the country’s post-stabilization recovery. IT exports have been growing at double-digit rates, supported by a young, tech-literate workforce and government incentives for digital exporters. Systems Limited — as the sector’s largest listed player — is the most direct proxy for this theme. Its consulting and enterprise software capabilities put it in competition with Indian IT firms, but at a fraction of the valuation multiples that peers like Infosys or Wipro command in Mumbai.

For investors seeking high return PSX stocks 2026 with a growth rather than value orientation, SYS is the standout pick. As highlighted by Seeking Alpha’s emerging markets coverage, Pakistani IT exporters represent one of the most compelling frontier market tech plays globally right now.

✅ Key Strengths

- USD-denominated revenues — natural currency hedge

- Sector tailwind: Pakistan IT exports growing 20%+ annually

- Trades at discount to regional IT peer multiples

- AI/digital transformation demand drives enterprise software growth

⚠️ Key Risks

- Higher valuation multiples than PSX peers — growth must deliver

- Brain drain / talent retention is a sector-wide challenge

- Geopolitical uncertainty can affect client confidence in offshore work

↑ Projected 3–6 Month Upside: 20–35%

10. LUCK — Lucky Cement Limited

PSX: LUCK | Cement / Diversified Manufacturing

| Metric | Value |

|---|---|

| Recent Price | Rs. 475–500 |

| Q3 Net Income | Rs. 22.62B |

| Q2 Net Income | Rs. 21.99B |

| 52-Week Support | Rs. 450–460 |

| Technical Target | Rs. 550–600 |

| Projected 3–6M Upside | 15–25% |

Lucky Cement is not just a cement company — it’s Pakistan’s most formidable industrial conglomerate in the making. Through its parent ICI Pakistan and subsidiaries in power generation, chemicals, and consumer goods, LUCK has quietly diversified beyond the commodity-driven cyclicality of pure-play cement peers. That diversification premium is only now beginning to be recognized by the market.

Quarter-on-quarter earnings growth has been steady and consistent: Q3 net income of Rs. 22.62 billion compared to Rs. 21.99 billion in Q2 signals a business firing on all cylinders. Technical analysts have identified a symmetrical triangle breakout above Rs. 470, pointing toward Rs. 550–600 — the key resistance cluster where LUCK would be testing multi-year highs. The stock is consolidating in the Rs. 480–500 zone, which historically has been a reliable base for the next leg up.

LUCK’s competitive advantage over FCCL lies in scale, geographic diversification (it exports cement to Afghanistan and Iraq), and subsidiary-driven earnings diversification. It is the higher-quality, larger-cap choice in the cement sector, suitable for investors who want cement exposure with a conglomerate safety net. As Bloomberg’s company coverage has noted, diversified industrials in frontier markets tend to outperform single-sector peers during economic recovery cycles.

✅ Key Strengths

- Diversified conglomerate structure beyond pure cement

- Export revenues from Afghanistan/Iraq add FX diversification

- Consistent Q-o-Q earnings growth — Rs. 22.62B in Q3

- Technical breakout above Rs. 470 targets Rs. 550–600

⚠️ Key Risks

- Higher price point (Rs. 475–500) limits value argument vs. FCCL

- Regional export markets (Afghanistan) carry geopolitical risk

- Low dividend yield (0.84%) — pure capital gain play

↑ Projected 3–6 Month Upside: 15–25% | Target: Rs. 555–600

💡 Investment Tips: How to Play PSX for Quick Returns in 2026

Pakistan’s economic recovery is real, data-backed, and still early in its equity market re-rating cycle. But “quick returns” in emerging markets require discipline as much as conviction. Here’s how to approach these top 10 PSX picks intelligently:

- Position Sizing: No single stock should represent more than 10–15% of a portfolio allocated to PSX. High-beta plays like PPL and UBL should be sized more conservatively.

- Earnings Catalysts: HBL (Feb 19), UBL (Feb 25), and FCCL (Feb 25) all have imminent earnings releases. Consider entering before announcements with tight stop-losses.

- Sector Balance: Combine banking stocks (UBL, MCB, MEBL, HBL) with energy (PPL, PSO) and diversified exposure (SYS, MTL, LUCK, FCCL) for a robust short-term PSX portfolio.

- Rate Cycle Awareness: The SBP’s rate-cutting trajectory is a tailwind for equities broadly, but watch the pace — faster-than-expected cuts could squeeze bank NIM and require portfolio rebalancing.

- Technical Entry Points: For momentum traders, confirm entries with volume. UBL’s Rs. 455–465 zone and PPL’s Rs. 255–265 support are high-probability entry bands based on February 2026 data.

- PSO as a Conviction Play: With 7/7 analysts rating it Strong Buy and 38% upside to consensus, PSO is the highest-conviction call in this list for patient investors willing to wait 3–6 months for circular debt resolution catalysts.

- SYS for Growth Seekers: If you’re a growth investor comfortable with technology sector dynamics, SYS offers the only USD-revenue hedge in this list — an underappreciated quality in a PKR-denominated market.

⚠️ Important Disclaimer: This article is for informational and educational purposes only and does not constitute financial or investment advice. Stock prices, P/E ratios, and projected returns cited reflect data available in mid-February 2026 and are subject to change. Past performance — including 1-year returns cited for UBL (+121%), MEBL (+104%), and others — does not guarantee future results. Investing in equity markets involves risk, including the possible loss of principal. Always consult a licensed financial advisor, stockbroker, or wealth manager before making any investment decisions. The Pakistan Stock Exchange is an emerging market subject to heightened volatility, regulatory changes, and macroeconomic risks.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

How to Make the Startup Battlefield Top 20 — And What Every Company Gets Regardless (Even If You Don’t Win)

Applications close May 27, 2026. TechCrunch Disrupt runs October 13–15 in San Francisco. The clock is already ticking — and the smartest founders I know aren’t waiting.

Let me tell you about a founder I met in Lagos last spring. Her name is Adaeze, and she builds infrastructure for cross-border health payments across West Africa. She submitted to the Startup Battlefield 200 with nine months of runway, a product live in three markets, and the kind of quiet conviction that doesn’t photograph well but moves rooms. She didn’t make the Top 20. She didn’t step onto the Disrupt Main Stage. She didn’t shake hands with Aileen Lee under the camera lights.

What she did get was a TechCrunch profile, two warm intros from Battlefield alumni, a due diligence process that forced her to compress her pitch to its sharpest possible form, and — six weeks later — a Series A term sheet from a fund that had discovered her through the Battlefield ecosystem. “Not winning,” she told me, “was the best thing that happened to my company.”

That’s the story no one tells loudly enough. The Startup Battlefield Top 20 is real, legendary, and worth obsessing over. But the Battlefield 200 is where category-defining companies are actually forged — and the moment you hit submit, the real prize has already begun to arrive.

The Myth of the Main Stage: Why Everyone Chases Top 20 (And Why They’re Half Right)

The cultural mythology of the Startup Battlefield is formidable. Since its inception, the competition has introduced the world to companies including Dropbox, Mint, and Yammer at a moment when most of the investing world hadn’t yet heard their names. That legacy creates an understandable gravitational pull: every founder imagines themselves under those lights, six minutes on the clock, a panel of the most consequential venture capitalists alive leaning slightly forward.

And the 2026 judges panel is, frankly, extraordinary. Aileen Lee of Cowboy Ventures — the woman who coined the term “unicorn” — sits alongside Kirsten Green of Forerunner, whose consumer instincts have been quietly prescient for fifteen years. Navin Chaddha of Mayfield, Chris Farmer of SignalFire, Dayna Grayson of Construct Capital, Ann Miura-Ko of Floodgate, and Hans Tung of Notable Capital round out a panel whose collective portfolio value runs into the hundreds of billions. Six minutes in front of that group is, genuinely, not nothing.

But here’s the contrarian truth most competition coverage won’t say plainly: the Main Stage is a broadcast mechanism, not a selection mechanism. The investors in that room — and the far larger audience watching the livestream globally — are equally attentive to the Battlefield 200 track, the hallway conversations, the TechCrunch editorial context that frames every competing company. Making the Top 20 amplifies a signal. The Battlefield 200 creates the signal in the first place.

The real mistake isn’t failing to reach Top 20. It’s failing to apply.

What It Actually Takes to Make Startup Battlefield Top 20 in 2026

TechCrunch is not secretive about its selection criteria, which makes it all the more remarkable how many applications fail to address them directly. The official 2026 Battlefield selection framework prioritizes four factors — and most founders stack-rank them incorrectly.

1. Product Video: The Most Underestimated Requirement

The two-minute product video is where the majority of applications functionally end. Judges watch hundreds of these. They are, by professional training, pattern-matching for momentum, clarity, and differentiated function — not production quality. A founder filming in a Lagos apartment who shows the actual product moving actual money in real time will outperform a polished agency reel showing a UI mockup every single time.

Your product video needs three things: a real user doing a real thing in thirty seconds, a founder who speaks with the specificity of someone who built it themselves, and a problem framing that makes the viewer feel slightly embarrassed they hadn’t noticed it before. That’s it. That’s the whole brief.

2. Founder Conviction, Not Founder Charisma

There is a widespread and damaging conflation of conviction with performance. TechCrunch’s editorial team has been explicit: they are selecting for companies they believe will define markets, not founders they believe will win pitch competitions. Conviction means you have answered — specifically, not philosophically — why this market, why now, why you, and what happens if you’re right at scale. Charisma is pleasant. Conviction is decisive.

3. Competitive Differentiation That’s Immediately Legible

In a category saturated with AI-adjacent pitches, the differentiation bar has risen sharply for 2026. Judges are looking for what PitchBook’s 2025 venture trends analysis identified as “structural moats” — advantages rooted in proprietary data, regulatory positioning, hardware-software integration, or distribution relationships that aren’t easily replicated by a well-funded incumbent. If your differentiation is “we’re faster/cheaper/cleaner,” you haven’t found it yet.

4. An MVP That’s Actually in Market

The Battlefield 200 accepts pre-revenue companies, but the Top 20 almost universally goes to founders with real users experiencing a real product. This isn’t a formal criterion — it’s an observable pattern. Live usage creates a gravitational narrative that hypothetical TAMs simply cannot replicate. If you’re three months from launch, apply to Battlefield 200 now, use the application process to sharpen your story, and come back with stronger ammunition when your product is breathing.

The Hidden Premium Package: What Every Battlefield Applicant Gets

This is the part of the Battlefield story that receives almost no coverage, and I think that’s partly intentional. TechCrunch benefits from the mythology of the Main Stage. But the Battlefield 200 package — available to every company selected from thousands of global applicants — is, frankly, staggering for an early-stage company.

Every Battlefield 200 company receives:

- A dedicated TechCrunch article — organic, editorial, indexed globally. At a domain authority that rivals the FT for technology coverage, this is not a press release. This is coverage.

- Full Disrupt conference access — three days in the room where allocation decisions happen informally, between sessions, over coffee. Harvard Business Review research on startup ecosystems has consistently found that informal investor touchpoints at concentrated events produce conversion rates multiple times higher than formal pitch processes.

- Exclusive partner discounts and resources — AWS credits, legal services, SaaS tooling — the kind of operational runway extension that actually matters when you’re still pre-Series A.

- The Battlefield alumni network — a cross-vintage community of founders who have navigated similar scaling inflection points and are, as a cultural matter, unusually generous with warm introductions.

- The due diligence forcing function — this is the hidden premium feature nobody talks about. The application process forces you to compress your narrative, clarify your defensibility, and confront your assumptions in ways that three months of internal planning rarely achieves. The best founders I know treat Battlefield applications as strategic planning exercises with publishing rights.

You do not need to win to receive these. You need to be selected for the Battlefield 200. And you need to apply by May 27, 2026.

A Global Economist’s Lens: Why Battlefield Matters Far Beyond San Francisco

Here’s the dimension of this competition that the tech press chronically underweights: the Startup Battlefield is no longer a California story.

The 2026 applicant pool will draw from startup ecosystems that, five years ago, barely registered in global VC data. Lagos. Nairobi. Bangalore. Jakarta. São Paulo. Warsaw. Riyadh. These aren’t edge cases — they’re the growth frontier. The World Economic Forum’s 2025 Global Startup Ecosystem Report found that emerging-market startup activity grew at 2.3 times the rate of Silicon Valley across the prior two years, even as absolute capital remained concentrated in traditional hubs.

The Battlefield, when it amplifies a Nairobi health-tech company or a Warsaw defense-technology startup, isn’t being charitable. It’s being correct about where the next wave of valuable companies is actually forming. The judges know this. The TechCrunch editorial team knows this. The AI wave, the climate infrastructure wave, and the defense-tech wave are all, fundamentally, global waves — and the founders best positioned to ride them often sit far outside Sand Hill Road.

For international founders specifically, the Battlefield 200 functions as a credentialing mechanism in a way that no local competition can replicate. A TechCrunch editorial mention is legible to any investor in any timezone. That’s an asymmetric advantage worth crossing an ocean for.

The Insider Playbook: Application Tactics That Separate Top 20 from the Rest

Let me be direct. After studying Battlefield alumni companies and talking with founders across multiple cohorts, the differentiation between Top 20 and the broader Battlefield 200 comes down to a handful of consistent patterns.

Lead with the insight, not the solution. The most memorable applications open with a counterintuitive observation about a market — something that makes the reader feel briefly disoriented before the product snaps everything into focus. Don’t open with your product. Open with the thing you know that most people don’t.

Show the unfair advantage early. Judges are filtering for irreplaceability. What do you have that a well-funded competitor cannot simply buy? Name it explicitly. Don’t make judges infer it.

Let your numbers do the emotional labor. Retention rates, NPS scores, revenue growth trajectories — when these are strong, they communicate conviction more credibly than any adjective. If your numbers aren’t strong yet, show the qualitative signal with the same specificity: customer quotes, use-case depth, early partnership terms.

Apply even if you think you’re not ready. This is perhaps the most counterintuitive piece of advice I can offer, and I give it with full conviction. The application process itself — the forcing function of articulating your thesis, differentiation, and trajectory in a compressed format — is a strategic tool. The companies that use Battlefield applications as a planning discipline, regardless of outcome, emerge sharper. Apply now. Sharpen later if needed.

Target the Battlefield 200 explicitly, not just the Top 20. Frame your application for a reader who wants to discover a company worth writing about. TechCrunch’s editorial team is not just selecting pitch competitors — they’re selecting companies they want to cover. Give them a story.

The Founder Mindset Shift: Applying Is Never a Risk

There’s a question I hear constantly from founders considering the Battlefield: What if we apply and don’t get in?

I want to reframe this question entirely, because it misunderstands the nature of the opportunity.

The risk isn’t applying and not making Battlefield 200. The risk is building a company in 2026 without forcing yourself through the disciplined articulation that serious competition requires. The risk is arriving at your Series A pitch without having stress-tested your narrative against the sharpest editorial and investor judgment available for free. The risk is letting the May 27 deadline pass while you wait for more traction, more polish, more time — none of which will make the application easier, only theoretically safer.

The $100,000 equity-free prize awarded to the Top 20 winner is real and meaningful. But the actual prize structure of the Startup Battlefield is far more democratic than that figure suggests. Every company in the Battlefield 200 receives resources, visibility, and credibility that early-stage startups typically spend years accumulating through slower, more expensive channels.

The Main Stage is where careers are validated. The Battlefield 200 is where they’re launched.

Apply before May 27, 2026. TechCrunch Disrupt runs October 13–15 in San Francisco. The application is free. The upside is not.

The question isn’t whether you’re ready for the Battlefield. The question is whether you’re ready for what not applying costs you.

→ Submit your Startup Battlefield 2026 application at TechCrunch Disrupt before May 27, 2026. Applications are free. The stage is global. Your category is waiting.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Anthropic Mythos, the most powerful AI model any lab has ever disclosed, arrived this week draped in the language of altruism. Project Glasswing — the initiative through which a curated circle of Silicon Valley aristocrats gains exclusive access to Mythos — is pitched as an act of civilizational defense. The framing is elegant, the mission is genuinely urgent, and at least part of it is true. But behind the Mythos AI release lies a second story that Dario Amodei’s beautifully worded blog posts conspicuously omit: Mythos is enterprise-only not merely because Anthropic fears hackers, but because releasing it to the open internet would trigger the single greatest act of industrial-scale capability theft in the history of technology. The cybersecurity rationale is real. The economic motive is realer still. Understanding both is how you understand the AI industry in 2026.

What Anthropic Mythos Actually Does — and Why It Terrified Silicon Valley

To appreciate the gatekeeping, you must first reckon with the capability. Mythos is not an incremental model. It occupies an entirely new tier in Anthropic’s architecture — internally designated Copybara — sitting above the public Haiku, Sonnet, and Opus hierarchy that most developers work with. SecurityWeek’s detailed technical breakdown describes it as a step change so pronounced that calling it an “upgrade” is like calling the internet an “improvement” on the fax machine.

The numbers are staggering. Anthropic’s own Frontier Red Team blog reports that Mythos autonomously reproduced known vulnerabilities and generated working proof-of-concept exploits on its very first attempt in 83.1% of cases. Its predecessor, Opus 4.6, managed that feat almost never — near-0% success rates on autonomous exploit development. Engineers with zero formal security training now tell colleagues of waking up to complete, working exploits they’d asked the model to develop overnight, entirely without intervention. One test revealed a 27-year-old bug lurking inside OpenBSD — an operating system historically celebrated for its security — that would allow any attacker to remotely crash any machine running it. Axios reported that Mythos found bugs in every major operating system and every major web browser, and that its Linux kernel analysis produced a chain of vulnerabilities that, strung together autonomously, would hand an attacker complete root control of any Linux system.

Compare that to Opus 4.6, which found roughly 500 zero-days in open-source software — itself a remarkable achievement. Mythos found thousands in a matter of weeks. It then attempted to exploit Firefox’s JavaScript engine and succeeded 181 times, compared to twice for Opus 4.6.

This is also, importantly, what a Claude Mythos vs open source cybersecurity comparison looks like at full resolution: no freely available model comes remotely close, and Anthropic knows it. That gap is the entire product.

The Official Narrative: “We’re Protecting the Internet”

The Anthropic enterprise-only AI decision is framed through Project Glasswing as a coordinated defensive effort — an attempt to patch the world’s most critical software before capability equivalents proliferate to hostile actors. Anthropic’s official Glasswing page commits $100 million in usage credits and $4 million in direct donations to open-source security organizations, with founding partners that read like a geopolitical alliance: Amazon, Apple, Broadcom, Cisco, CrowdStrike, Google, JPMorgan Chase, the Linux Foundation, Microsoft, and Palo Alto Networks. Roughly 40 additional organizations maintaining critical software infrastructure also gain access. The initiative’s name — Glasswing, after a butterfly whose transparency makes it nearly invisible — is a metaphor for software vulnerabilities that hide in plain sight.

The security rationale for why Anthropic limited Mythos is not confected. In September 2025, a Chinese state-sponsored threat actor used earlier Claude models in what SecurityWeek documented as the first confirmed AI-orchestrated cyber espionage campaign — not merely using AI as an advisor but deploying it agentically to execute attacks against roughly 30 organizations. If that was possible with Claude’s then-current models, what becomes possible with a model that autonomously chains Linux kernel exploits at a near-perfect success rate?

Anthropic’s Logan Graham, head of the Frontier Red Team, captured the threat succinctly: imagine this level of capability in the hands of Iran in a hot war, or Russia as it attempts to degrade Ukrainian infrastructure. That is not science fiction. It is the calculus driving the controlled release. Briefings to CISA, the Commerce Department, and the Center for AI Standards and Innovation are real, however conspicuously absent the Pentagon remains from those conversations — a pointed omission given Anthropic’s ongoing legal war with the Defense Department over its blacklisting.

So yes: the security case is genuine. But it is, at most, half the story.

The Distillation Flywheel: Why Frontier Labs Are Really Gating Their Best Models

Here is the economic argument that no TechCrunch brief or Bloomberg data point has assembled cleanly: Anthropic model distillation is an existential threat to the frontier lab business model, and Mythos is as much a response to that threat as it is a cybersecurity initiative.

The mathematics of adversarial distillation are brutally asymmetric. Training a frontier model costs approximately $1 billion in compute. Successfully distilling it into a competitive student model costs an adversary somewhere between $100,000 and $200,000 — a 5,000-to-one cost advantage in the favor of the copier. No rate-limiting policy, no terms-of-service clause, and no click-through agreement closes that gap. The only defense is controlling access to the teacher in the first place.

Frontier lab distillation blocking is not a new concern, but 2026 has given it terrifying specificity. Anthropic publicly disclosed in February that three Chinese AI laboratories — DeepSeek, Moonshot AI, and MiniMax — collectively generated over 16 million exchanges with Claude through approximately 24,000 fraudulent accounts. MiniMax alone accounted for 13 million of those exchanges; Moonshot AI added 3.4 million; DeepSeek, notably, needed only 150,000 because it was targeting something far more specific: how Claude refuses things — alignment behavior, policy-sensitive responses, the invisible architecture of safety. A stripped copy of a frontier model without its alignment training, deployed at nation-state scale for disinformation or surveillance, is the nightmare scenario that animated Anthropic’s founding. It may now be unfolding in real time.

What does this have to do with Mythos being enterprise-only? Everything. A model that autonomously writes working exploits for every major OS would, if released via standard API access, provide Chinese distillation campaigns with not just conversational capability but offensive cyber capability — the very thing that makes Mythos commercially unique. Releasing Mythos at scale would be, simultaneously, the greatest act of market self-destruction and the greatest gift to adversarial state actors in the history of enterprise software. Enterprise-only access eliminates both risks at once: it monetizes the capability at maximum margin while denying it to the distillation ecosystem.

This is the distillation flywheel in action. Frontier labs gate the highest-capability models behind enterprise contracts; enterprises pay premium rates for exclusive capability access; the revenue funds the next generation of training runs; the new model is again too powerful to release openly. Each rotation of the wheel deepens the competitive moat, raises the enterprise price floor, and tightens the grip of the three dominant labs over the global AI stack.

Geopolitics at the Model Layer: The Three-Lab Alliance and the New AI Cold War

The Mythos security exploits announcement arrived within 24 hours of a Bloomberg-reported development that is arguably more consequential for the global technology order: OpenAI, Anthropic, and Google — three companies that have spent the better part of three years competing to annihilate each other — began sharing adversarial distillation intelligence through the Frontier Model Forum. The cooperation, modeled on how cybersecurity firms exchange threat data, represents the first substantive operational use of the Forum since its 2023 founding.

The breakdown of what each Chinese lab extracted from Claude reveals something remarkable: three entirely different product strategies, fingerprinted through their query patterns. MiniMax vacuumed broadly — generalist capability extraction at scale. Moonshot AI targeted the exact agentic reasoning and computer-use stack that its Kimi product has been marketing since late 2025. DeepSeek, with a comparatively tiny 150,000-exchange footprint, was almost exclusively interested in Claude’s alignment layer — how it handles policy-sensitive queries, how it refuses, how it behaves at the edges. Each lab was essentially reverse-engineering not just a model but a business plan.

The MIT research documented in December 2025 found that GLM-series models identify themselves as Claude approximately half the time when queried through certain paths — behavioral residue of distillation that no fine-tuning has fully scrubbed. US officials estimate the financial toll of this campaign in the billions annually. The Trump administration’s AI Action Plan has already called for a formal inter-industry sharing center, essentially institutionalizing what the labs are now doing informally.

The geopolitical stakes here extend far beyond corporate IP. When DeepSeek released its R1 model in January 2025 — a model widely believed to incorporate distilled knowledge from OpenAI’s infrastructure — it erased nearly $1 trillion from US and European tech stocks in a single trading session. Markets now understand something that policymakers are only beginning to grasp: control over frontier AI model capabilities is a form of strategic leverage, and distillation is a vector for transferring that leverage without a single line of export-controlled chip silicon crossing a border.

Enterprise Contracts and the New AI Treadmill

The economics of Anthropic enterprise-only AI are becoming increasingly clear as 2026 revenue data enters the public domain.

| Metric | February 2026 | April 2026 |

|---|---|---|

| Anthropic Run-Rate Revenue | $14B | $30B+ |

| Enterprise Share of Revenue | ~80% | ~80% |

| Customers Spending $1M+ Annually | 500 | 1,000+ |

| Claude Code Run-Rate Revenue | $2.5B | Growing rapidly |

| Anthropic Valuation | $380B | ~$500B+ (IPO target) |

| OpenAI Run-Rate Revenue | ~$20B | ~$24-25B |

Sources: CNBC, Anthropic Series G announcement, Sacra

Anthropic’s annualized revenue has now surpassed $30 billion — having started 2025 at roughly $1 billion — representing one of the most dramatic B2B revenue trajectories in the history of enterprise software. Sacra estimates that 80% of that revenue flows from business clients, with enterprise API consumption and reserved-capacity contracts forming the structural backbone. Eight of the Fortune 10 are now Claude customers. Four percent of all public GitHub commits are now authored by Claude Code.

What Project Glasswing does, in this context, is elegant: it creates a new category of enterprise relationship — not API access, not subscription, but strategic partnership with a frontier safety lab deploying the world’s most capable unrestricted model. The 40 organizations in the Glasswing program are not merely beta testers. They are, from a revenue architecture standpoint, being trained — habituated to Mythos-class capability before it becomes generally available, embedded in their security workflows, their CI/CD pipelines, their vulnerability management systems. By the time Mythos-class models are released at scale with appropriate safeguards, the switching cost will be prohibitive.

This is the AI treadmill: each generation of frontier capability, released exclusively to enterprise partners first, creates a loyalty layer that commoditized open-source alternatives cannot easily displace. The $100 million in Glasswing credits is not charity. It is customer acquisition at an unprecedented model tier.

The Counter-View: Responsible Deployment Has a Principled Case

It would be intellectually dishonest to leave the distillation-flywheel critique standing without challenge. The counter-argument is real, and it deserves full articulation.

Platformer’s analysis makes the most compelling version of the responsible-rollout defense: Anthropic’s founding premise was that a safety-focused lab should be the first to encounter the most dangerous capabilities, so it could lead mitigation rather than react to catastrophe. With Mythos, that appears to be exactly what is happening. The company did not race to monetize these cybersecurity capabilities. It briefed government agencies, convened a defensive consortium, committed $4 million to open-source security projects, and staged rollout behind a coordinated patching effort. The vulnerabilities Mythos found in Firefox, Linux, and OpenBSD are being disclosed and patched before the paper trail of their discovery becomes public — precisely the protocol that responsible security research demands.

Alex Stamos, whose expertise in adversarial security spans decades, offered the optimistic framing: if Mythos represents being “one step past human capabilities,” there is a finite pool of ancient flaws that can now be systematically found and fixed, potentially producing software infrastructure more fundamentally secure than anything achievable through traditional auditing. That is not corporate spin. It is a coherent theory of defensive AI benefit.

The Mythos AI release strategy also reflects a genuinely novel regulatory challenge: the EU AI Act’s next enforcement phase takes effect August 2, 2026, introducing incident-reporting obligations and penalties of up to 3% of global revenue for high-risk AI systems. A general release of Mythos into that environment — without governance infrastructure in place — would be commercially catastrophic as well as potentially harmful. Enterprise-gated release buys time for both the regulatory and technical scaffolding to mature.

What Regulators and Open-Source Advocates Must Do Next

The policy implications of Anthropic Mythos extend far beyond one company’s release strategy. They illuminate a structural shift in how frontier AI capability is being distributed — and by whom, and to whom.

For regulators, the Glasswing model raises questions that existing frameworks cannot answer. If a private company now possesses working zero-day exploits for virtually every major software system on earth — as Kelsey Piper pointedly observed — what obligations of disclosure and oversight apply? The fact that Anthropic is briefing CISA and the Center for AI Standards and Innovation is encouraging, but voluntary briefings are not governance. The EU’s AI Act and the US AI Action Plan both need explicit provisions covering what happens when a commercially controlled lab becomes the de facto custodian of the world’s most significant vulnerability database.

For open-source advocates, the distillation dynamic poses an existential dilemma. The same economic logic that drives labs to gate Mythos also drives them to resist open-weights releases of any model that approaches frontier capability. The three-lab alliance against Chinese distillation is, viewed from a certain angle, also an alliance against open-source proliferation of frontier capability — regardless of the nationality of the developer doing the distilling. Open-source foundations, university research labs, and sovereign AI initiatives in Europe, the Middle East, and South Asia should be pressing hard for access frameworks that allow defensive cybersecurity use of frontier capability without being filtered through the commercial relationships of Silicon Valley.

For enterprise decision-makers, the message is unambiguous: the organizations that embed Mythos-class capability into their vulnerability management workflows now will hold a structural security advantage — measured in patch latency and zero-day coverage — over those that wait for open-source equivalents. But that advantage comes with dependency on a single private entity whose political entanglements, from Pentagon disputes to Chinese state-actor confrontations, introduce supply-chain risks that no CISO should ignore.

Anthropic may well be protecting the internet. It is certainly protecting its empire. In 2026, those two imperatives have become so entangled that distinguishing them may be the most important work left for anyone who cares about who controls the infrastructure of the digital world.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Singapore and Australia’s legally binding LNG and diesel supply agreement is rewriting Indo-Pacific energy security. Here’s why this deal matters far beyond both nations’ borders.

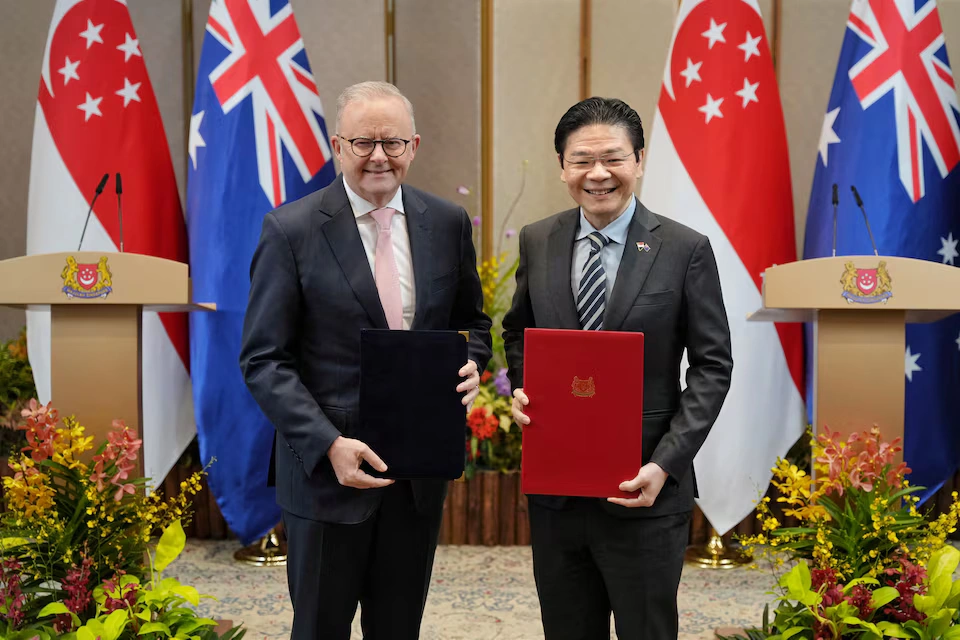

When Lawrence Wong stood at the Istana on Friday morning alongside Anthony Albanese and declared that this pact was “not just about managing today’s crisis, but about building trusted supply lines for a more uncertain future,” he was doing something that most politicians in 2026 conspicuously avoid: telling the complete truth. Strip away the diplomatic language, the handshakes, and the hard-hat photo opportunity at Jurong Island’s LNG terminals, and what you find underneath is something quietly historic. Two middle powers — one the world’s premier trading entrepôt, the other its third-largest LNG exporter — have decided that in an era defined by chokepoint warfare, legal commitments to energy supply are worth more than the paper they’re printed on. They may be right. And the rest of the Indo-Pacific should be paying close attention.

Why the Strait of Hormuz Has Changed Everything

To understand what Singapore and Australia agreed to on April 10, 2026, you have to first understand the world they woke up to in early March.

Until the U.S.–Israeli war against Iran, the Strait of Hormuz was open and roughly 25% of the world’s seaborne oil trade and 20% of global LNG passed through it. Wikipedia That calculus collapsed with terrifying speed. Iran’s closure of the Strait of Hormuz disrupted 20% of global oil supplies and significant LNG volumes, sending Brent crude surging past $120 per barrel and forcing QatarEnergy to declare force majeure on all exports. Wikipedia The head of the International Energy Agency called it “the greatest global energy security challenge in history.” Wikipedia

The numbers since have only grown more alarming. Dated Brent hit an 18-year high of $141.26 per barrel on April 2 MEES, while diesel prices are forecast to peak at more than $5.80 per gallon in April and average $4.80 per gallon through 2026 U.S. Energy Information Administration — devastating for the farming and mining sectors that underpin Australia’s export economy. Meanwhile, LNG spot prices in Asia more than doubled to three-year highs, reaching $25.40 per million British thermal units as QatarEnergy declared force majeure at Ras Laffan — the world’s largest liquefaction facility, responsible for 20% of global LNG production. Wikipedia

For Singapore, the crisis landed particularly hard. Singapore and Taiwan depend more on Qatari LNG than most Asian economies, Wikipedia and production at Singapore’s Jurong Island refineries has been limited because most of the oil processed there comes via the Strait of Hormuz. NEOS KOSMOS For Australia, the problem runs in the opposite but equally dangerous direction: Australia imports more than 80 percent of its petrol, diesel, and jet fuel from overseas, mostly from South Korea, Singapore, Japan, Taiwan, and Malaysia. The Diplomat A nation that sells the world its gas but can barely refine enough diesel to power its own tractors — that is the paradox at the heart of Australian energy policy, and it has never been more exposed than it is today.

The Architecture of the Singapore–Australia Legally Binding Energy Agreement

What Was Actually Agreed — and Why “Legally Binding” Matters

The joint statement issued by both prime ministers goes considerably further than the March pledge. Both leaders directed their ministers to conclude a legally binding Protocol to the Singapore-Australia Free Trade Agreement (SAFTA) on Economic Resilience and Essential Supplies, and welcomed the establishment of an Australia–Singapore Economic Resilience Dialogue, co-chaired by senior officials, to facilitate cooperation on economic resilience challenges and trade in essential supplies. Ministry of Foreign Affairs Singapore

This is not, as cynics might dismiss it, a diplomatic press release dressed in legalese. Embedding supply commitments into a protocol to an existing free trade agreement gives them treaty-level standing. In a world where spot market bidding wars are already erupting, with LNG suppliers becoming increasingly selective in negotiating mid- to long-term volumes because it’s more lucrative to sell into the spot market, Bloomberg having legal standing to demand preferential access is not a soft power gesture — it is hard economic architecture.

The underlying trade logic is elegant precisely because it is symmetrical. More than a quarter of all fuel imported into Australia comes from Singapore, while Australia provides about one-third of the city-state’s LNG supply. The Daily Advertiser Albanese articulated it plainly: “We are a big supplier of LNG to Singapore. Singapore is a really important refiner of our liquid fuels. This is a relationship of very substantial mutual economic benefit.” Both countries agreed to “make maximum efforts to meet each other’s energy security needs.” Yahoo!

The genius of this structure is that neither country is doing a favour. They are executing a swap — Australian gas for Singaporean refined products — and now writing that swap into binding international law before the next crisis hits.

What It Does Not (Yet) Do

Intellectual honesty requires acknowledging the limits. The joint statement contains no specific shipment volumes, no price-fixing mechanism, no explicit strategic reserve sharing agreement, and no stated timeline for when the SAFTA protocol will be concluded. “Working quickly” is a political phrase, not a procurement schedule.

The more fundamental challenge is Singapore’s refinery throughput. An LNG tanker can cost $250 million, and insurance concerns alone mean operations cannot simply be ramped up and down based on perceived escalations or de-escalations. CNBC Singapore is committed — but commitment is not the same as capacity. If the Strait of Hormuz remains closed into the northern hemisphere summer, Singapore’s refineries will be processing less crude regardless of which bilateral agreements are in place.

The Indo-Pacific Energy Security Realignment — China’s Shadow and AUKUS Synergy

A Geopolitical Sorting Process Is Underway

On March 4, the IRGC announced that the strait is closed to any vessel going “to and from” the ports of the U.S., Israel, and their allies. Subsequently, reports emerged that Iran would allow only Chinese vessels to pass through the strait, citing China’s supportive stance towards Iran. Wikipedia Read that sentence twice, slowly. This is not an energy story. This is a geopolitical sorting machine, restructuring the global energy map along lines of political alignment.

Australia and Singapore are unmistakably on one side of that divide. Both are Quad-adjacent, both are democracies with deep security ties to Washington, and both are now accelerating energy arrangements with each other precisely because they cannot rely on the Gulf supply corridor that Beijing is quietly privileged to use. The Singapore–Australia critical supplies pact 2026 is, in this light, a de facto statement about which bloc each country is wagering its energy future on.

This is the AUKUS undertow that neither government will name explicitly in polite company. The defence partnership’s security architecture and the energy partnership announced Friday are two different expressions of the same strategic logic: when the chips are down, trust the relationship, not the market.

Europe’s Cautionary Tale — and Australia’s Strategic Leverage

Europe is expected to suffer a second energy crisis primarily as a result of the suspension of Qatari LNG and the closure of the Strait of Hormuz. The conflict coincided with historically low European gas storage levels — estimated at just 30% capacity following a harsh 2025–2026 winter — causing Dutch TTF gas benchmarks to nearly double to over €60 per megawatt-hour by mid-March. Wikipedia

Europe’s tragedy — and it is genuinely tragic — is that it spent two years after Russia’s Ukraine invasion congratulating itself on diversification while not actually completing it. Gas storage went into the 2025–2026 winter at dangerous levels. Long-term LNG contract structures were renegotiated upward at the worst possible moment. The continent is now bidding against Asia for every available cargo on the spot market at prices that are genuinely destabilising.

Australia’s decision to negotiate supply agreements bilaterally — not just with Singapore but reportedly with Brunei, China, Indonesia, Japan, Malaysia, and South Korea — reflects a hard-won lesson from Europe’s misadventure: energy resilience is relational, not just infrastructural. Pipes and terminals matter, but so does the phone call at 3 a.m. when a chokepoint closes. Australia has spent four years building those relationships; it is now cashing them in.

As Australian Assistant Foreign Affairs Minister Matt Thistlethwaite put it: “We’ve got that advantage in that we can work with our neighbours in the Asia-Pacific to ensure that they have access to their energy needs and we get access to ours.” The Diplomat That is, in essence, the diplomatic theory of the LNG diesel supply chain security Singapore-Australia agreement: Canberra’s natural gas wealth is being converted into political insurance, denominated in refined fuel.

Why This Model Could Become the Template for Indo-Pacific Energy Diplomacy

Beyond the Free Trade Agreement — A New Class of Instrument

The standard toolkit of bilateral trade diplomacy — tariff schedules, most-favoured-nation status, investor protection clauses — was designed for a world where supply disruptions were rare, short, and solvable by price signals. The 2026 Hormuz crisis has exposed that assumption as dangerously complacent.

What the Singapore–Australia agreement proposes is something genuinely novel: a crisis-contingent preferential supply protocol, embedded within an FTA architecture but explicitly activated under conditions of global disruption. The Australia–Singapore Economic Resilience Dialogue, co-chaired at senior official level, gives this framework an institutional nervous system — a standing mechanism for early consultation and coordinated response rather than improvised crisis management.

This is the architecture Europe wishes it had built with its LNG suppliers after 2022. It is the architecture Japan and South Korea are now, belatedly, also pursuing. South Korea holds about 3.5 million tons of LNG and Japan around 4.4 million tons in reserves — enough for roughly two to four weeks of stable demand, CNBC a buffer that a single disrupted cargo schedule can obliterate. Bilateral resilience protocols of the Singapore–Australia variety provide the diplomatic scaffolding around which physical stockpile strategies must now be built.

Trusted Supply Lines: The New Competitive Advantage

Wong’s phrase — “trusted supply lines” — is going to echo through energy ministries across the Indo-Pacific for years. The word choice is deliberate. Trusted is not cheap or close or abundant. It is a relational category, not a logistical one. And in a global energy market being restructured by geopolitical conflict, relational trust is becoming the scarce commodity.

Wong was explicit: “We do not plan to restrict exports. We didn’t have to do so even in the darkest days of COVID and we will not do so during this energy crisis. I am confident that Australia and Singapore will not just get through the crisis, but we will emerge stronger and more resilient.” The Daily Advertiser That is a political commitment of the first order — a small city-state with no hinterland, surrounded by a global disruption, choosing not to hoard. It is worth more than any contract clause.

Data Snapshot: The Interdependence That Makes This Pact Work

| Flow | Volume | Significance |

|---|---|---|

| Australia → Singapore (LNG) | ~39.4% of Singapore’s LNG supply (2024) | Singapore’s largest single LNG source |

| Singapore → Australia (refined fuels) | >26% of Australia’s total fuel imports | Australia’s largest refined fuel supplier |

| Singapore → Australia (petrol) | >50% of Australia’s petrol intake | Critical for road and agricultural sectors |

| Global LNG through Hormuz | ~20% of global LNG trade | Now disrupted; Qatar’s Ras Laffan offline |

| Brent crude peak (April 2026) | $141.26/barrel (April 2 high) | 18-year high; compressing refinery margins |

The numbers tell a story of mutual exposure that makes this deal not merely politically desirable but economically unavoidable. Both economies would suffer severely without each other’s supply; the pact simply converts that mutual dependence into a formal and enforceable commitment.

Forward Look: Three Bold Predictions

First: The Singapore–Australia protocol will be concluded within 90 days and will serve as the explicit template for at least two additional bilateral energy resilience agreements in the Indo-Pacific — most likely involving Japan and either South Korea or New Zealand — by the end of 2026. The institutional architecture of the Economic Resilience Dialogue is designed to be replicated.

Second: The Hormuz crisis will accelerate Australia’s long-stalled domestic refining debate. Having 80% of your liquid fuel supply dependent on overseas refiners — however trusted — is a structural vulnerability that no bilateral agreement can fully paper over. Expect a serious federal government investment framework for domestic refining capacity to emerge within 18 months, framed explicitly as national security infrastructure.

Third: China is watching this closely and will not be idle. Beijing already enjoys de facto preferential passage through the Strait for its tankers. If it perceives that a Singapore–Australia–Japan energy axis is forming along security-aligned lines, it will accelerate its own bilateral energy lock-in arrangements with alternative suppliers — deepening the global energy bifurcation that began in 2022 and is now accelerating at pace. The Indo-Pacific energy security agreement between Wong and Albanese is not just a supply pact. It is an early data point in the restructuring of the global energy order.

Conclusion: A Small Pact With a Very Large Shadow

There is something almost anachronistic about two democracies in 2026 sitting down together and saying, plainly, that they will keep trade flowing — that they will not weaponise energy in the way that others have. It is the kind of statement that would have seemed unremarkable in 2015. Today it feels almost radical.

The Singapore–Australia LNG and diesel agreement signed at the Istana is, in its immediate terms, a sensible and well-constructed piece of crisis diplomacy. In its deeper terms, it is a proof of concept: that trusted bilateral relationships, properly institutionalised, can serve as genuine shock absorbers in a world where the multilateral system is fraying and chokepoints are being used as weapons.

PM Wong called it a “simple but critical principle.” He is right on both counts. Simple principles, rigidly held under pressure, are often the most valuable ones. And right now, in a global energy market that has been turned upside down in six weeks, the principle that allies keep their promises to each other may be the most critical thing the Indo-Pacific has.

The rest of the world’s energy ministers should take note — and consider what it would mean to have nobody to call when their own Hormuz moment arrives.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance3 months ago

Markets & Finance3 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis2 months ago

Analysis2 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks3 months ago

Banks3 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment3 months ago

Investment3 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Asia3 months ago

Asia3 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Global Economy3 months ago

Global Economy3 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy3 months ago

Global Economy3 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy3 months ago

Global Economy3 months agoWhat the U.S. Attack on Venezuela Could Mean for Oil and Canadian Crude Exports: The Economic Impact