Analysis

The Permanent Scars of the 2026 Strait of Hormuz Crisis

Ten million barrels a day offline. Qatar’s LNG trains in ruins. Brent past $120. The ceasefire changes the headlines — it does not change the damage. The Middle East energy order as we knew it is not disrupted. It is broken.

There is a peculiar ritual that follows every great energy shock: within days of the first price spike, the soothing voices of market analysts and government spokespeople emerge to reassure us that supply disruption is temporary, strategic reserves are ample, and the world’s oil machine will self-correct. The ritual is underway again. But this time — after forty-three days of the largest supply disruption in the history of the global oil market, as the International Energy Agency has described it — those soothing voices are reciting from a script the facts no longer support. The 2026 Strait of Hormuz crisis is not a disruption to be managed. It is a structural wound.

The arithmetic alone is staggering. Since Iran’s Revolutionary Guards declared the strait “not allowed” to commercial shipping on February 28, 2026 — hours after the United States launched Operation Epic Fury — tanker traffic through the waterway has collapsed by more than 90 percent. Roughly 10 million barrels per day of oil production have been effectively taken off world markets. That is more oil than Germany, France, the United Kingdom, and Italy consume combined. Add the simultaneous shutdown of Qatar’s LNG exports — the world’s largest — and you have an energy rupture that dwarfs the 1973 Yom Kippur embargo, the 1979 Iranian Revolution, and the 1990 Gulf War disruption, rolled into one.

Crisis at a Glance — Key Metrics (as of 12 April 2026)

| Metric | Figure |

|---|---|

| Gulf oil production effectively offline | ~10 mb/d |

| Brent crude peak | $120+ per barrel |

| Qatar LNG capacity destroyed | 17% — 3–5 year repair timeline |

| QatarEnergy estimated annual lost revenue | $20 billion |

| Asian LNG spot price spike post-Ras Laffan strike | +140% |

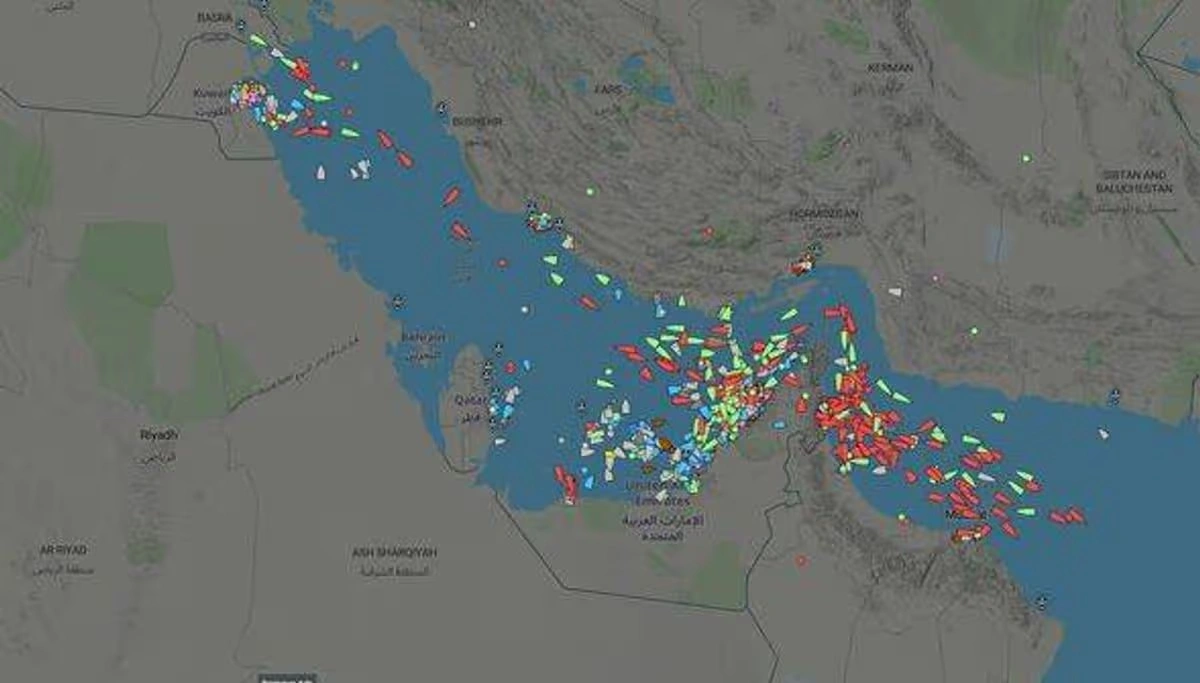

| Loaded tankers trapped in the Persian Gulf (9 Apr) | 230 vessels |

Yet numbers, however eye-watering, fail to capture the true nature of what has happened. The war has not merely interrupted flows through a choke point. It has physically destroyed irreplaceable infrastructure, accelerated a geopolitical realignment years in the making, and imposed costs — financial, strategic, and reputational — that the Gulf’s great petrostate empires will be paying for the better part of a decade. A fragile two-week ceasefire agreed on April 8 has not reopened the strait. By April 9, ADNOC CEO Sultan Al Jaber was blunt: “The Strait of Hormuz is not open. Access is being restricted, conditioned and controlled.” Two hundred and thirty laden tankers sat anchored inside the Gulf, waiting for a passage that, as of this writing, remains subject to Iranian veto.

The Physical Damage: Bombed Trains, Broken Compressors, Years of Repair

Start with the concrete and the steel — because in energy infrastructure, the physical damage is where the multi-year consequences begin. On March 18, Iranian missiles struck Ras Laffan Industrial City, the sprawling 200-square-kilometre complex eighty kilometres northeast of Doha that is, without exaggeration, the most important natural gas export hub on earth. QatarEnergy subsequently confirmed that two of its fourteen LNG production trains — the giant refrigeration units that liquefy gas for export — and one of its two gas-to-liquids (GTL) facilities were destroyed. According to Bloomberg, two of the plant’s 14 production trains were damaged, with repairs expected to take years.

QatarEnergy CEO Saad al-Kaabi was precise in his damage assessment: the attack wiped out capacity producing 12.8 million tonnes per year of LNG — 17 percent of Qatar’s total export capacity. Repairs will take three to five years. The reason is not a lack of money or will. It is physics and procurement. QatarEnergy requires replacement gas turbines to power the refrigeration compressors of the destroyed trains. Only three manufacturers worldwide produce the required equipment, and current order books put delivery timelines at two to four years. You cannot Amazon-Prime a gas turbine. The South site at Ras Laffan, which took the direct hits, has dropped from 36 million tonnes per annum capacity to 24 mtpa — a permanent loss that no ceasefire can rapidly undo.

“These are not repairs that can be made in a week or two. These are repairs that are going to take probably years to replace, and, by virtue of that, there is going to be a sizable impact.”

— Energy Economist, University of Colorado Denver, via Scientific American, March 2026

The damage beyond Qatar is less headline-grabbing but cumulatively severe. Kpler’s vessel-tracking analysis confirms that insurance withdrawal — not physical blockade alone — effectively shuttered the strait from day one of the conflict. By early March, insurance premiums for vessels transiting the passage had risen four to six times over the prior week. Iraq and Kuwait began curtailing oil well production by early March as onshore storage filled to capacity with crude that had nowhere to go. The collective oil output of Kuwait, Iraq, Saudi Arabia, and the UAE had dropped by a reported 6.7 million barrels per day by March 10, and by at least 10 million barrels per day by March 12. Saudi Arabia’s Ras Tanura refinery, one of the world’s largest at 550,000 barrels per day, was among Iranian targets. Iran also struck facilities in Kuwait, UAE, and threatened further strikes on the Jubail Petrochemical complex and UAE’s Al Hosn gasfield.

The infrastructure repair bill, when it is eventually totalled, will run well into the tens of billions of dollars across the Gulf. The direct $20 billion annual revenue loss from Ras Laffan alone — over a three-to-five-year repair horizon — implies a present-value destruction of somewhere between $40 billion and $70 billion in Qatari energy wealth, before secondary effects on planned expansions such as the North Field East project are accounted for.

The Hormuz Stranglehold: A 20% Global Oil Shock That the Pipelines Cannot Fix

One of the persistent myths of pre-war energy security planning was that Gulf producers had meaningful bypass routes. Saudi Arabia’s East-West Pipeline can carry crude to Yanbu on the Red Sea; the UAE’s Habshan-Fujairah pipeline offers an outlet to the Gulf of Oman. In theory, these could absorb some Hormuz disruption. In practice, as the Congressional Research Service noted in its March 2026 analysis, combined available capacity across both pipelines amounts to roughly 2.6 million barrels per day — a fraction of the 20 million barrels that normally transit the strait daily. Saudi Arabia did crank the East-West pipeline to its 7 million bpd capacity limit by end of March, according to Al Jazeera, pumping more oil through it than ever before. But there is no pipeline for LNG. Gas molecules trapped inside the Gulf have nowhere to go.

The scale of the supply shock — 20 percent of global seaborne oil trade suddenly offline — is without modern precedent. The 1973 embargo removed roughly 7 percent of global supply. The 1979 Iranian Revolution cut about 4 percent. Even combined, they did not approach what the 2026 Hormuz closure has achieved. Federal Reserve Bank of Dallas economists writing in March 2026 are unequivocal: “A complete cessation of oil exports from the Gulf region amounts to removing close to 20 percent of global oil supplies from the market.” Their models warn that a quarter-long closure would impose significant output losses on the global economy, weighted most heavily on Asia, which receives roughly 80 percent of Gulf crude exports.

The Asian Dilemma

China sourced roughly a third of its oil imports through Hormuz. Japan, as of February 2026, sourced 94.2 percent of its crude from the Middle East. India’s refineries pivoted rapidly to Russian crude — deepening a strategic dependency that will not easily reverse when the war ends. South Korea has emergency reserves estimated to last over a year. The Philippines, importing 98 percent of its oil from the Middle East, declared a state of national energy emergency on March 24. As Bloomberg’s analysis documents, fuel shortages spread from Thailand to Pakistan within weeks, while European traders warned of diesel scarcity if the strait remained closed.

Beyond Oil: The Invisible Damage — Fertilizer, Helium, and Food

This crisis has taught an uncomfortable lesson: the Strait of Hormuz is not merely an oil pipeline. It is a supply artery for the global agricultural system. Up to 30 percent of internationally traded fertilizers — primarily urea and ammonia — normally transit the strait. The Gulf region accounts for 30–35 percent of global urea exports and 20–30 percent of ammonia exports. Disruption to fertilizer supply during the Northern Hemisphere spring planting season could suppress corn yields in the United States, the world’s primary corn producer — with downstream effects rippling through beef, poultry, and dairy prices into 2027. Global fertilizer prices are estimated to average 15–20 percent higher in the first half of 2026 if the crisis continues.

Add to that helium — critical for MRI machines, semiconductor manufacturing, and scientific research — of which the Gulf is a major supplier. The crisis has constrained global helium supply, disrupting industries with few substitute suppliers. Sulfur — of which Gulf countries supply roughly 45 percent globally — faces similar choking, with knock-on effects on copper mining and acid production. The 2026 Hormuz crisis is not an energy crisis. It is a civilizational supply chain emergency whose secondary consequences will take years to fully surface.

“Every day the Strait remains restricted, the consequences compound. Supply is delayed, markets tighten, prices rise. The impact is felt beyond energy markets, in economies, industries and households worldwide.”

— Sultan Ahmed Al Jaber, CEO, ADNOC, via CNBC, 9 April 2026

The Structural Wound: Why This Is Not the 1970s — It Is Worse

Historical analogies are seductive in a crisis. Market veterans reflexively reach for 1973 and 1979, the canonical oil shocks. But the 2026 crisis differs from its predecessors in three ways that make it structurally more damaging.

First, physical destruction. The 1973 embargo was a political act — a tap turned off. The tap was always intact and could be turned back on. Ras Laffan’s destroyed LNG trains cannot be turned back on. The Pearl GTL facility — one of the world’s most complex energy installations — will require years of engineering work and two-to-four years of lead time just on gas turbine procurement. This is infrastructure damage, not a pricing dispute. The gap between “disruption” and “destruction” is measured in years, not quarters.

Second, the simultaneous closure of multiple commodity streams. The 1973 shock was an oil shock. The 2026 crisis is an oil shock, a gas shock, a fertilizer shock, a helium shock, and a food security shock — simultaneously, through a single choke point. The systemic interdependencies are categorically more complex, and the feedback loops — oil prices feeding into food prices feeding into inflation feeding into central bank tightening feeding into recession risk — operate faster in the digitally connected, just-in-time supply chain world of 2026 than they did in 1973.

Third, the Gulf Cooperation Council’s economic model has suffered a credibility rupture. Analysts describe a “systemic collapse of the GCC economic model” — the implicit contract in which Gulf states provided the world with uninterrupted energy flows in exchange for security guarantees and geopolitical accommodation. That contract has been violated. Not by choice, but by geography and the logic of warfare. Foreign investors who once treated Gulf energy infrastructure as the world’s most bankable physical asset are reassessing. Capital that was financing the Gulf’s Vision 2030-style economic diversification programmes will seek safer harbours, at precisely the moment when diversification was finally beginning to bear fruit.

Recovery Timeline: What Partial Ceasefire Actually Means

| Timeframe | Expected Milestone | Key Risk |

|---|---|---|

| May–June 2026 | Ras Laffan North site potentially restarts 12 operable LNG trains (Wood Mackenzie); 14 stranded LNG cargoes exit the Gulf | Fragile ceasefire collapses; Iran re-restricts passage |

| Aug–Sep 2026 | Ras Laffan South site earliest possible partial restart; tanker flows normalize if strait fully opens | Turbine procurement bottleneck; insurance market slow to re-normalise |

| 2027–2028 | Gulf oil production ramps back toward pre-war levels; stranded North Field East expansion resumes | Investor confidence gap; delayed capex decisions across region |

| 2029–2031 | Two destroyed LNG trains at Ras Laffan fully repaired and online (CEO estimate: 3–5 years from strike) | Gas turbine delivery delays; structural demand shift to US LNG may be permanent |

Wood Mackenzie’s assessment is sobering: even with a ceasefire, QatarEnergy cannot fully restart all twelve operable trains before late August at the earliest, assuming a May resumption — and that assumes security conditions permit it. “The ceasefire means it may be possible for the 14 trapped laden LNG cargoes in the Gulf to exit the Strait of Hormuz,” said Wood Mackenzie’s Tom Marzec-Manser. “But for there to be a real structural change in supply, the Ras Laffan site in Qatar would need to restart its 12 operable trains. It is unclear if QatarEnergy would consider doing this during a ceasefire.”

Winners, Losers, and the Accelerated Energy Transition

Winners

- US LNG exporters — structural demand shift from Qatar LNG by European and Asian buyers

- American shale producers — Brent above $100 makes marginal barrels highly profitable

- Russia — India and China deepening crude import dependency amid Gulf disruption

- Renewable energy developers — war accelerates energy diversification mandates globally

- Norwegian gas exporters — European pipeline gas alternatives gain premium

- Australian LNG — new long-term contracts from Asia locked in at elevated prices

Losers

- Qatar — $20B annual revenue loss, North Field expansion delayed, sovereign reputation damage

- Kuwait and Iraq — prolonged well shut-ins cause reservoir damage; fiscal crises deepen

- Asian LNG importers — Japan, South Korea, China facing multi-year supply tightness

- European industry — energy-intensive manufacturing faces existential competitiveness crisis

- Global food systems — fertilizer shock cascades into 2027 harvests

- Emerging markets — fuel import bills spike; currency crises in Philippines, Bangladesh, Pakistan

The most consequential long-run winner may be the energy transition itself — though not in any comfortable sense. As one executive interviewed by Bloomberg put it bluntly: “The main message is that we’re going to get the energy transition forced on us in a very painful way.” Forced transitions are rarely efficient ones. Governments scrambling to reactivate coal plants and speed-build LNG regasification terminals are making choices that will lock in infrastructure for thirty years. The crisis has simultaneously made fossil fuel investment look more profitable in the short term — producers will not rush to bet on multi-year projects given volatility risk — and made diversification away from Middle Eastern supply a strategic imperative. The result, paradoxically, may be more investment in both shale and renewables simultaneously, further compressing the role of Gulf producers in the global energy mix over the next decade.

Policy Implications: What Must Come Next

The 2026 Hormuz crisis has exposed the hollowness of decades of energy security planning. The assumption that strategic petroleum reserves — built for 90-day disruptions — could manage a complete cessation of Gulf supply was always a comforting fiction. The IEA’s emergency stock release mechanisms were designed for disruptions, not destructions. The fertilizer sector, as the Wikipedia crisis chronicle notes, lacks any internationally coordinated strategic reserves whatsoever, making supply disruptions there almost entirely unmanageable through existing tools.

- Establish international fertilizer strategic reserves — modelled on IEA oil emergency sharing agreements. The agricultural cascades from 2026 will arrive in 2027 and 2028; governments that act now can blunt the worst of them.

- Accelerate LNG import infrastructure in Europe and Asia — floating storage and regasification units can be deployed in 18–24 months. The lesson of 2026 is that no single supplier — not Qatar, not Russia — should command more than 20 percent of any country’s gas supply.

- Renegotiate the architecture of Gulf energy security guarantees — the implicit US-Gulf compact that underpinned the post-1945 energy order has cracked. New frameworks must involve China and India, as the world’s largest Gulf oil importers, in the burden-sharing of strait security.

- Design a Hormuz bypass financing mechanism — Saudi Arabia’s East-West Pipeline and UAE’s Fujairah pipeline together represent 2.6 mb/d of bypass capacity against a 20 mb/d strait flow. A multilateral infrastructure fund to expand and harden these alternatives is not just prudent; it is now an urgent civilizational priority.

- Resist the siren call of short-term shale bingeing — US producers face intense pressure to ramp output rapidly. But the lesson of every prior oil shock is that supply responses built on panic investment create the next crash. Disciplined, long-cycle capital allocation — not a shale free-for-all — will better serve global energy stability.

The Long View: A Region Diminished, a World Reconfigured

In the weeks since February 28, a great deal of commentary has focused on when the Strait of Hormuz will reopen. That is the wrong question. The right question is: what kind of Middle Eastern energy order will exist on the other side of this crisis?

The Gulf producers will recover. Kuwait and Iraq will pump oil again; Saudi Aramco will restore its formidable output; even Qatar will eventually restart its LNG trains, once replacement turbines arrive from the handful of manufacturers who make them. But the aura of invincibility — the sense that Persian Gulf energy infrastructure was somehow sheltered from the logic of warfare — has been permanently shattered. Every insurer, every long-term LNG contract negotiator, every sovereign wealth fund manager will price geopolitical risk in the Gulf differently for the next generation. Capital will diversify away from the region at the margin, year after year, compounding into a structural decline in Gulf market share even before physical recovery is complete.

The deeper irony is that Iran — by striking Qatar, a Muslim neighbour with whom it shares the world’s largest gas reservoir — has accelerated precisely the outcome it most fears: a world that finds its way around the Middle East’s energy geography. US LNG will lock in long-term supply contracts with Europe and Asia that were previously occupied by Qatari molecules. Australian and Norwegian exporters will sign deals that, under normal conditions, they could never have won on price. The energy transition, messy and painful as the crisis is making it, will receive a political mandate in Tokyo, Berlin, and Seoul that no climate conference could have generated.

History will record the 2026 Strait of Hormuz crisis as an inflection point — the moment when the post-1970s global energy order, already creaking under the weight of decarbonisation pressures and geopolitical fragmentation, finally broke. What replaces it will be more diversified, more expensive to build, and more resilient by design. The scars from Ras Laffan’s bombed LNG trains will fade, in time. The strategic wounds — to Gulf leverage, to the reliability premium that Middle Eastern energy once commanded — will not.

Every delay deepens the disruption, Sultan Al Jaber warned. He was speaking about tankers. He might just as well have been speaking about history.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Malaysia posted its biggest trade surplus on record and second-quarter GDP growth of 5.8% in 2026, yet its stock market has stubbornly refused to rally — a disconnect that is puzzling investors even as the country climbs global competitiveness rankings and hosts record investor turnout at its largest retail investing event.

Record Growth Meets a Muted Market

Malaysia’s economy expanded 5.8% year-on-year in the second quarter of 2026, underpinning what former senior investment banker Ian Yoong Kah Yin describes as one of the most competitive economies globally, buoyed by the country’s largest-ever trade surplus, according to reporting in The Star. Yet with the exception of the semiconductor and plantation sectors, Yoong notes that many shares on Bursa Malaysia remain undervalued relative to that underlying strength — a gap he summarised memorably: “It’s like we held a party and no one came.”

The disconnect comes even as Hong Leong Investment Bank upgraded Malaysia’s full-year 2026 growth forecast to 4.7% from 4.5%, citing stronger-than-expected performance in the electrical and electronics sector alongside resilient domestic demand, according to BusinessToday. Household loans grew 5.2% year-on-year and credit card spending rose 10.2%, signalling that consumer demand remains a genuine pillar of growth rather than a statistical artefact of export strength alone.

A Competitiveness Ranking Jump — and a Retail Investing Boom

Malaysia’s underlying reform story has been validated externally. The country climbed eight places to rank 15th among 70 economies in the 2026 IMD World Competitiveness Ranking, its best showing in recent years, following an 11-place jump the year before, according to The Star. Economists attribute the climb to policy reforms improving government and business efficiency, streamlined investment approvals, accelerated digitalisation, and stronger fiscal management.

Retail investor enthusiasm, meanwhile, appears robust even if institutional capital has been slower to follow. INVEST Fair 2026, Malaysia’s largest retail investment event, drew an expected 20,000 visitors across more than 70 hours of programming at Kuala Lumpur’s Mid Valley Exhibition Centre in July, according to event coverage on TradingView. Separately, a survey of more than 3,500 active users by digital wealth platform Versa found that 70% of respondents would prioritise investing over debt repayment or emergency savings if they received a sudden windfall, according to The Star — evidence of a pronounced retail “investment reflex” even amid broader questions about household financial resilience.

Fixed Income Is Where the Real Money Is Flowing

While equities lag, Malaysia’s fixed income market tells a different story. Employees Provident Fund chief investment officer Mohamad Hafiz Kassim told the Sasana Symposium 2026 that Malaysia is “punching above its weight” on global fixed income indexes, drawing outsized capital allocation given interest rate and yield differentials between Malaysian Government Securities and US Treasuries — a dynamic occurring even as the ringgit has remained notably stable, according to The Star. Speakers at the same event pointed to the broader global shift toward passive investing as a structural tailwind Malaysia is well-positioned to capture with continued policy follow-through.

What Explains the Equity Gap

Analysts point to several possible explanations for the growth-market disconnect: persistent foreign investor caution tied to regional and Middle East-driven geopolitical risk, a valuation overhang from prior years, and sector concentration that leaves broad indices under-exposed to the semiconductor and technology names actually capturing AI-linked investment flows. Whatever the cause, the gap represents either an opportunity for value-focused investors or a warning sign that Malaysia’s headline growth figures are not yet translating into corporate earnings momentum broad enough to move the market.

What to Watch

The second half of 2026 will test whether Malaysia’s fixed income strength and competitiveness gains eventually pull equity valuations upward, or whether the stock market’s caution proves to be the more accurate signal about underlying corporate health. Continued data centre and semiconductor investment, alongside any further IMD-style competitiveness validation, will be key catalysts to track.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Monetary Authority of Singapore nudged its exchange-rate-based policy stance slightly tighter in its July review, a modest but notable shift after the city-state’s economy grew a stronger-than-expected 5.7% year-on-year in the second quarter, powered by an AI-driven manufacturing boom that is increasingly reshaping the country’s growth mix.

Growth Beats Expectations Again

Singapore’s economy expanded 5.7% year-on-year in the second quarter of 2026, according to advance estimates from the Ministry of Trade and Industry released 14 July, moderating only slightly from an upwardly revised 6.3% in the first quarter, according to MAS’s own July policy statement. On a quarter-on-quarter seasonally adjusted basis, GDP rose 1.1%, continuing an unbroken run of above-trend expansion. Manufacturing has been the standout performer, posting 12.2% year-on-year growth in the second quarter — up from 8.0% in the first — driven by the electronics and precision engineering clusters riding the global AI capital expenditure wave, according to data reported by Indiplomacy.

The strength has prompted a wave of forecast upgrades. UOB Global Economics and Markets Research lifted its 2026 GDP growth forecast to 4.8% from 4%, while S&P Global Market Intelligence matched that upgrade, and Nomura flagged upside risk to its own 4.6% forecast, according to Xinhua — all comfortably above the Ministry of Trade and Industry’s official 2.0–4.0% guidance range.

MAS Leans Against Rising Core Inflation

The growth surprise has not been without cost. MAS Core Inflation, which excludes accommodation and private transport costs, rose to 1.5% year-on-year in the second quarter, up from 1.2% in the January–February period before the Middle East conflict began, according to the central bank’s own policy statement. Fuel-price surges have pushed up point-to-point transport and non-cooked food inflation, while retail goods prices have climbed on higher import costs and a tobacco tax increase.

In response, MAS increased the slope of the Singapore dollar nominal effective exchange rate (S$NEER) policy band slightly in its July review — a modest tightening move that builds on an April 2026 tightening step, according to the bank’s Macroeconomic Review. Singapore uses its exchange rate, rather than interest rates, as its primary monetary policy tool, managing the currency’s path within an undisclosed band against a basket of trading partner currencies.

The Positive Output Gap Is Widening

Perhaps the most telling technical signal in MAS’s July statement is its acknowledgment that Singapore’s positive output gap — the extent to which the economy is running above its estimated potential — is now forecast to widen further in 2026, rather than narrow as previously expected. That reflects both the stronger-than-anticipated first-half growth data and MAS’s expectation that GDP will be sustained at elevated levels near-term, powered by continued AI-related capital expenditure, a robust construction pipeline, and steady credit-driven expansion in the financial sector.

Singapore’s central bank, MAS, slightly tightened its S$NEER exchange-rate policy band in July 2026 after GDP grew 5.7% year-on-year in Q2, driven by AI-linked manufacturing growth of 12.2%. Core inflation rose to 1.5%, prompting the modest policy shift even as growth forecasts were upgraded to as high as 4.8%.

Why This Matters Beyond Singapore

As a bellwether for Asian trade and technology cycles, Singapore’s data offers one of the clearest real-time signals of how durable the global AI infrastructure buildout has become, even as broader Asian growth forecasts have been trimmed elsewhere in the region due to Middle East-driven energy costs. For global investors, the combination of resilient growth and rising core inflation puts MAS in a position other regional central banks may soon face: managing an AI-driven boom that is proving inflationary in ways that are only loosely connected to traditional demand-side overheating.

What to Watch

MAS’s next scheduled policy review will be closely watched for whether the central bank continues its gradual tightening path or judges that easing global energy costs — following the partial reopening of the Strait of Hormuz — have done enough of the disinflationary work on their own. Singapore’s full second-quarter economic survey, due after the advance estimate, will offer a fuller sectoral breakdown of where the AI-driven strength is concentrated.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Indonesia has taken its first concrete legislative step toward building a financial centre intended to compete with Singapore, Hong Kong, and Dubai, as President Prabowo Subianto pushes an ambitious plan to draw foreign capital into Southeast Asia’s largest economy and lift growth toward 8% by the end of his term in 2029.

Parliament Passes Enabling Legislation

Indonesia’s parliament passed the enabling legislation for the new financial hub, laying its legal foundation, according to reporting by the South China Morning Post. The milestone marks the most tangible progress yet on a project analysts say is projected to attract billions of dollars in investment — though they caution that crucial details on tax incentives, investor eligibility requirements, and regulatory safeguards still need to be finalised before the centre can credibly compete with established regional players.

The ambition is unmistakable: a financial centre capable of pulling capital away from Singapore’s deep, established markets, Hong Kong’s China-gateway status, and Dubai’s fast-growing wealth-management ecosystem is a tall order, and observers note that persuading global institutional investors to relocate meaningful operations to a new jurisdiction is a multi-year undertaking that has only just begun in earnest.

Indonesia’s parliament passed enabling legislation in July 2026 for a new financial hub designed to rival Singapore, Hong Kong, and Dubai, as President Prabowo Subianto targets 8% GDP growth by 2029. Singapore remains Indonesia’s top foreign investor at $8.8 billion in H1 2026, ahead of Hong Kong and China.

A Broader Investment Story Already Taking Shape

The financial-hub push arrives alongside signs that Indonesia is already deepening its role as a regional investment destination. Singapore remained Indonesia’s largest foreign investor in the first half of 2026, contributing $8.8 billion, followed by Hong Kong at $7.8 billion, China at $3.9 billion, Japan at $1.9 billion, and the United States at $1.7 billion, according to investment data reported by the New Straits Times. Malaysia ranked fifth, contributing $700 million in the second quarter alone, as Indonesia’s total realised investment reached Rp511.8 trillion.

Indonesian Investment Minister Rosan Roeslani has pointed to regulatory reform — including Government Regulation No. 28, introduced last October, which he said has provided greater licensing certainty — as a key driver of investor interest, while explicitly acknowledging that neighbouring economies are reforming in parallel, requiring Indonesia to keep pace.

Growth Outlook Holds Steady Amid Regional Headwinds

The financial-hub push comes as Indonesia’s broader macroeconomic backdrop remains comparatively resilient. The Asian Development Bank’s July 2026 outlook kept Indonesia’s growth forecast unchanged at 5.2% for both 2026 and 2027, even as the bank lowered its overall developing Asia and Pacific growth projection to 4.9% amid Middle East-driven energy cost pressures. That stability stands in contrast to Malaysia, whose 2026 growth forecast was revised only marginally higher to 2%, according to the same ADB report — even as Maybank Investment Banking Group separately upgraded its own Malaysia forecast more aggressively, to 4.9%, citing strong regional investor interest at July’s Invest ASEAN conference in Singapore, which drew 200 institutional investors managing a combined $23 trillion in assets.

Rice Diplomacy as a Parallel Economic Thread

Indonesia’s regional economic engagement extends beyond high finance. State logistics agency Bulog is continuing negotiations with Malaysia and Singapore over proposed rice export deals, with pricing and commercial terms still under discussion as of mid-July, according to The Star. The talks illustrate the breadth of Indonesia’s economic diplomacy push across ASEAN even as its flagship financial-hub ambitions dominate headlines.

What It Means for Global Investors

For asset managers and multinationals weighing where to locate Southeast Asian operations, Indonesia’s financial-hub legislation is a signal of intent rather than an immediate call to relocate. The real test will come as tax-incentive structures, licensing rules, and investor-protection frameworks are finalised over the coming months — details that will determine whether Jakarta can credibly compete with Singapore’s decades-long regulatory head start, or whether the hub instead becomes a complementary gateway focused on domestic Indonesian capital markets and Belt-and-Road-adjacent regional flows.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Nvidia’s H200 Chips Are Finally Reaching China — In Numbers Too Small to Matter Yet

Oil Prices Fall as Strait of Hormuz Reopens: 2026 Update

Malaysia GDP Growth vs Stock Market: The 2026 Disconnect

Singapore MAS Tightens Policy as GDP Growth Hits 5.7%

Fed Holds Rates Under Warsh as Trump Rolls Out New Tariffs

Indonesia Financial Hub 2026: Can It Rival Singapore, Dubai?

Russia Fuel Shortages 2026: Inside a Cracking War Economy

China Politburo July 2026: Stimulus Signals Explained

Andy Burnham, UK Gilts and Mortgages: July 2026 Explainer

Pakistan’s 2026 Monsoon Floods Threaten Fragile Economic Recovery as Inflation Nears 9%

Pakistan Gulf Investment Outflows 2026: Peace Deal Stakes Explained

Canada Trade Diversification 2026: China, Indonesia, UAE Deals Explained

US Forced-Labour Tariffs on 60 Countries: The Hidden Trade Shock of 2026

Global Central Banks 2026: Fed, BoE and BoJ Decisions Could Reshape Markets

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

The AI Super Bubble Is Ready to Burst

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

Bitcoin $150k Milestone Achieved as US Sovereign Crypto Pivot Looms

Gold Price Forecast 2026: Fed’s July 29 Decision and Record Central Bank Buying Explained

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

India Economic Rise 2026: How the Subcontinent Toppled Japan

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

China Housing Market Turnaround: White‑List Model Stabilises Prices

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025