Analysis

Strait of Hormuz Crisis 2026: How Trump’s Toll U-Turn Exposes Global Economic Risk

Oil markets spent Tuesday whipsawing between a one-month high and a partial retreat after President Donald Trump first threatened a 20% “reimbursement fee” on all cargo transiting the Strait of Hormuz, then abandoned the levy hours later in favour of bilateral investment pledges from Gulf states. Brent crude settled near $84–85 a barrel, roughly a third below April’s war peak but well above the pre-conflict baseline, as the US Navy reimposed a blockade on Iranian ports and Tehran’s Revolutionary Guard struck tankers with their transponders switched off (CNBC; Washington Post).

What most coverage has missed is that the toll episode, however short-lived, has functioned as a live stress test of exactly how exposed nine very different economies are to a chokepoint that carries roughly a fifth of the world’s oil and gas in peacetime. Vessel traffic through Hormuz collapsed from 37 ships a week earlier to just 14 on the Sunday before Trump’s announcement, according to Kpler tracking data, and the International Energy Agency’s hoped-for return to surplus by year-end now looks conditional on a durable ceasefire that has already broken down twice (CNBC; Al Jazeera).

The Toll That Never Was — But the Precedent That Might Be

The International Maritime Organization rejected the fee outright, calling mandatory transit tolls illegal under international law, while the US Treasury simultaneously warned that any shipper paying Iran for safe passage would be exposed to sanctions (NBC News). Shipping executives, including Chevron’s leadership, warned that a US-imposed toll would set a precedent allowing any country bordering an international strait — the Malacca Strait among them — to demand transit payments, a risk with direct relevance to Malaysia and Singapore’s shipping-dependent economies.

Asia’s Buffer Is Thinner Than Last Time

The South China Morning Post’s Hong Kong desk notes that Asian economies are “better placed to absorb the blow” than during April’s peak, but the buffer has eroded. Analysts at Sparta Commodities in Singapore flagged that strategic reserves drawn down during the earlier phase of the conflict leave less room to smooth a renewed shock (SCMP). For Singapore, whose Q2 growth already decelerated to 5.7% from a stronger prior quarter as AI-driven electronics exports failed to fully offset Middle East uncertainty, the mathematics are unforgiving (Free Malaysia Today).

Pakistan’s Remittance Channel Is the Overlooked Transmission Line

Pakistan receives roughly 9% of GDP in annual remittances, with 55% originating from the Gulf Cooperation Council states, according to the IMF’s most recent country report. A sustained disruption to GCC economies, or a return migration of workers amid regional instability, would strike directly at one of Pakistan’s most important financing sources for consumption and the balance of payments — a risk the Fund flags explicitly alongside compressed capital inflows from GCC banks, Pakistan’s largest source of short-term commercial financing (IMF Country Report 26/101). Islamabad’s current account is projected to worsen by 0.2 percentage points of GDP in FY26 and 0.4 points in FY27 under the Fund’s baseline, with the adverse scenario nearly doubling that hit.

The UK’s Energy Bill Arrives Months Late

British households and industry are only now absorbing the inflationary tail of the spring shock. The Bank of England’s Andrew Bailey has warned that higher energy costs already “in the pipeline” will keep headline inflation elevated into the fourth quarter even as spot oil prices ease, while the House of Commons Library estimates the indirect pass-through could add roughly a third of a percentage point to UK CPI through supply chains alone (UK Finance; Commons Library).

Why This Matters Beyond the Headline Number

The pattern across markets is consistent: the direct oil-price shock is only the first-order effect. The second-order effects — remittance flows, strategic reserve depletion, freight and insurance premiums, and the precedent risk to other global chokepoints — are where the durable economic damage is likely to concentrate, and where most competitor coverage has stopped short.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Russia’s GDP contracted 0.2% year-on-year in the first quarter of 2026, and full-year growth projections have been cut to just 0.4%, worse than 2025’s 1% expansion that narrowly avoided recession (Forbes). The ruble, meanwhile, has told a confusing story: it strengthened to roughly 69.90 per dollar in June — its best level since February 2023 — before weakening again to 77.55 by mid-July, a 7% slide in a single month (Trading Economics).

The Iran War Lifeline That Undermined Its Own Purpose

The Iran conflict initially offered Moscow a genuine reprieve. Brent crude’s surge past $120 a barrel at the conflict’s peak in April lifted Russia’s oil-and-gas revenues after a brutal start to 2026, when Urals crude fell below $73 and budget revenues from energy halved in January (Forbes). But the war’s chaos cut both ways: two Russian-backed power plants in Iran were paused, and Moscow’s ambitions to diversify transit routes linking Russia to India via Iran stalled — meaning the same conflict that briefly lifted revenues also damaged Russia’s longer-term energy diversification strategy.

The Uncovered Story: Fiscal Exhaustion, Not Just Sanctions

Coverage of Russia’s economy tends to default to a binary sanctions narrative. The more precise story, per the Bloomsbury Intelligence and Security Institute, is fiscal exhaustion: a stronger ruble combined with falling oil prices has cut roughly a quarter of the value of Urals crude revenue, creating an estimated $25–30 billion energy revenue shortfall even before accounting for the latest US legislative push to sanction buyers of Russian oil, uranium and natural gas (BISI; Forbes).

Taxes Are Rising Because the War Chest Is Shrinking

The Moscow Times reports that Russia collected less budget revenue in 2025 than originally planned for the first time since the pandemic — roughly 36.6 trillion rubles against a planned 40.3 trillion. In response, Moscow is raising VAT from 20% to 22% from January 2026, lowering the mandatory VAT registration threshold for small businesses from 60 million to 10 million rubles, and introducing a new levy on finished electronics (The Moscow Times). These are the fiscal signatures of a government refilling war financing through domestic taxation rather than resource windfalls.

No Collapse, But No Recovery Either

CSIS’s structural analysis notes the Kremlin abandoned its own “fiscal rule” — the mechanism that historically capped spending of oil windfalls — allowing nearly all oil revenue to flow into current spending, primarily military procurement and subsidised loans (CSIS). Unemployment remains low and the banking system stable, meaning the “new baseline scenario” described by BISI is one of a wilting but standing economy, sustained by state direction of scarce resources rather than genuine productive capacity.

Why This Matters to Pakistan and China

Russia’s pivot of energy exports toward Asia — China, India and Turkey — since 2022 has structural implications for Pakistan’s own energy diversification discussions and for China’s crude sourcing strategy, particularly as Beijing simultaneously cut monthly crude imports to near decade lows during the second quarter, suggesting Chinese refiners are diversifying suppliers even as political ties with Moscow deepen.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

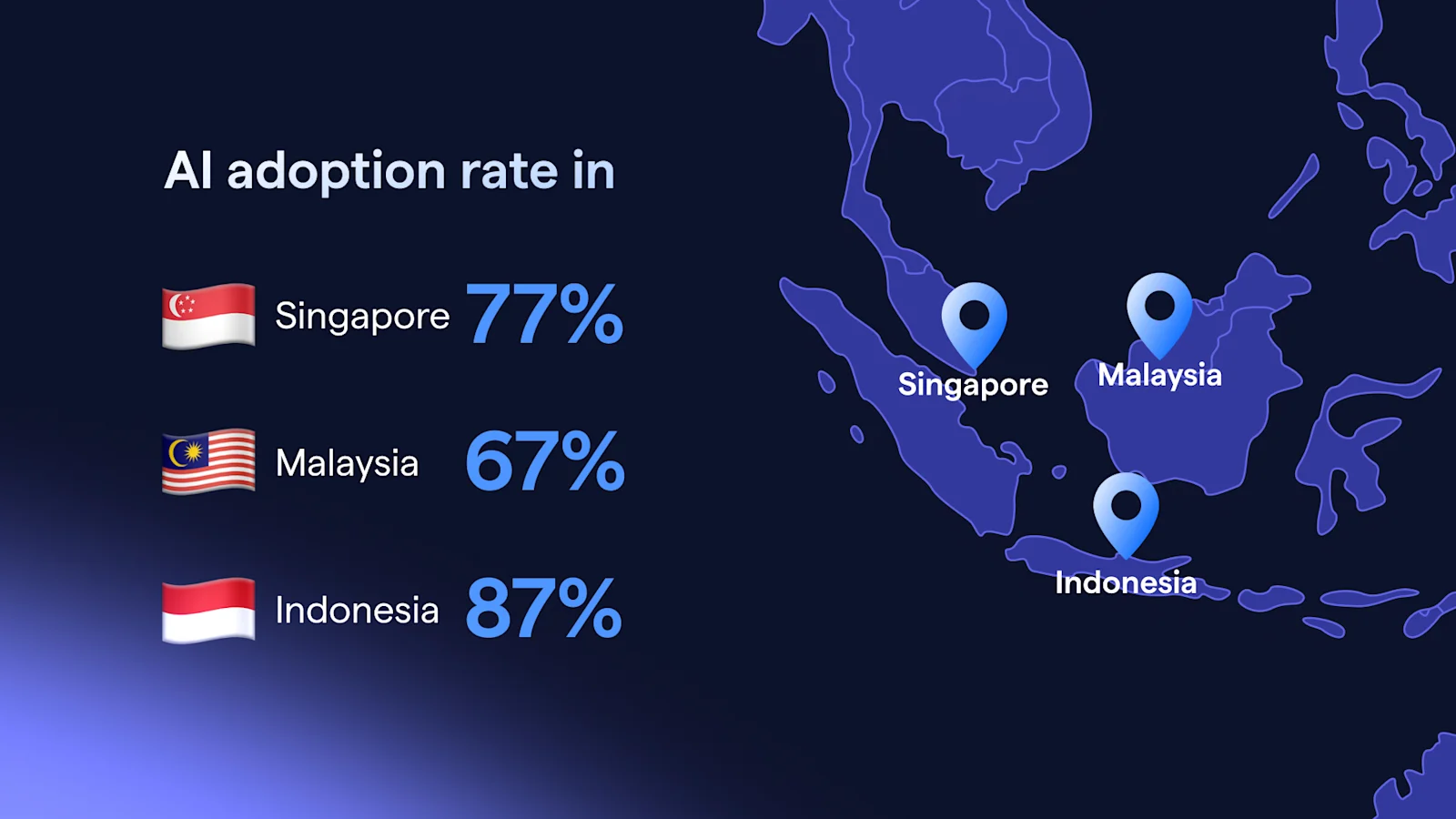

Malaysia Singapore AI Boom 2026: Inside the Sovereign AI Policy Shift Behind the Growth Numbers

Research houses have repeatedly upgraded Malaysia’s 2026 growth forecast through the summer, with Maybank Investment Bank raising its estimate to 4.9% from 4.4%, citing resilient domestic demand, robust exports and the global AI-driven technology upcycle even after the bank had cut its outlook in May over Strait of Hormuz concerns (Xinhua). HSBC Private Bank separately held its 4.5% forecast, pointing to Malaysia’s position as a net oil exporter and its emerging role leading the region’s data-centre market as key buffers against global instability (The Rakyat Post).

The Semiconductor Pipeline Story Everyone Is Covering

Maybank’s chief executive Michael Oh-Lau told the bank’s Invest ASEAN conference in Singapore that energy transition, supply-chain reconfiguration and AI-led digital transformation dominated this year’s agenda, as $23 trillion in assets under management descended on the summit (BigGo Finance). Malaysia’s semiconductor testing and assembly infrastructure is feeding directly into the regional AI trade, according to HSBC’s Desmond Kuang, while Singapore’s manufacturing sector accelerated to 12.2% growth in Q2, driven by electronics and precision engineering tied to AI-related semiconductor demand (Vietnam Plus).

The Angle Competitors Are Missing: Governance, Not Just GDP

What most business coverage has not connected is a parallel policy shift documented by trade-law specialists at MLex: both Malaysia and Singapore are quietly redefining what “sovereign AI” means for smaller economies. Rather than pursuing full technological self-sufficiency, both governments are combining targeted domestic capability with governance frameworks, trusted partnerships and selective investment — a middle path distinct from the US-China AI arms race (MLex). The defining question, per MLex’s analysis, is not how much governments should own, but what they need to control.

Singapore’s Growth Deceleration Is a Warning Sign, Not Just a Data Point

Singapore’s economy grew 5.7% year-on-year in Q2, decelerating from the prior quarter despite the near-doubling of electronics exports, suggesting AI-related demand alone cannot fully insulate a trade-dependent economy from Middle East volatility (Free Malaysia Today). Prime Minister Lawrence Wong warned in June that the economy had not yet felt the full impact of the conflict, a caution that stands in tension with the more bullish AI-investment narrative dominating research-house forecasts.

The AMRO Warning Beneath the Optimism

The ASEAN+3 Macroeconomic Research Office’s annual consultation flagged a sharper-than-expected cooling of the global AI cycle as Malaysia’s principal downside risk — one capable of dampening electronics and data-centre demand and triggering broader financial market volatility, alongside renewed tariff frictions and tighter technology controls (AMRO). That is a meaningfully different risk framing than the “AI boom insulates Southeast Asia” narrative currently dominating headlines.

What This Means for Investors and Policymakers

The structural story is real: Malaysia and Singapore have entrenched positions in global semiconductor and AI infrastructure value chains, and institutional capital is responding accordingly. But the sustainability of that story now rests on governance choices around sovereign AI policy as much as on the capex cycle itself — a dimension largely absent from mainstream financial coverage of the region.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan’s Economic Survey for FY2025–26, presented by Finance Minister Muhammad Aurangzeb in June, recorded GDP growth of 3.7%, the fastest pace in four years and above the prior year’s 3.18%, though still short of the government’s 4.2% target (Dawn). The KSE-100 index climbed 18.4% in the July–March period, public debt-to-GDP fell to 68.5% from 75% in 2023, and the fiscal deficit narrowed to 0.7% of GDP. Yet the IMF’s own July update projects Pakistan will miss its FY27 growth target too, holding its 3.6% 2026 estimate broadly unchanged from April (ProPakistani).

The Headline Resilience Story Most Coverage Repeats

Local press has largely framed the survey as a story of “resilience and discipline,” pointing to reserves built through the IMF’s Extended Fund Facility, a primary surplus, and Naya Pakistan Certificate inflows of $2 billion contributing to $6.1 billion in external budgetary disbursements (Dawn). That framing is accurate but incomplete.

What the IMF Country Report Actually Flags

The Fund’s most recent Article IV-linked staff report highlights a structural vulnerability that has received far less attention: Pakistan’s remittance dependence on the Gulf Cooperation Council. Remittances account for roughly 9% of GDP, and 55% of that flow originates in GCC states. The report warns explicitly that a significant disruption to Gulf economies, or a return migration of Pakistani workers, “could weigh on these flows, a major source of financing for consumption and the balance of payments” (IMF Country Report 26/101). With GCC banks also Pakistan’s primary source of short-term commercial financing, any deterioration in regional risk sentiment tied to the Iran war threatens both sides of the external accounts simultaneously.

Inflation Is Not as Tame as the Growth Number Suggests

Core inflation stood at 7.6% year-on-year in March, and headline inflation rose to 7.3% as higher commodity prices began passing through to domestic energy costs — a direct transmission channel from the Strait of Hormuz disruption. The State Bank of Pakistan held its policy rate at 10.5% through January and March after a 50-basis-point cut in December, while projecting reserves to climb to roughly $18 billion by June 2026, contingent on continued IMF program access (IMF Country Report 26/101).

The FY27 Revenue Gap

Achieving Pakistan’s FY27 fiscal target requires additional revenue measures worth 0.6% of GDP, according to the Fund, to correct chronically low tax buoyancy. An FBR revenue collection floor is proposed as a quantitative performance criterion from December 2026, alongside provincial efforts to broaden the GST base on services — reforms that carry real political cost in an economy still recovering from last year’s floods, which nonetheless pushed FY26 H1 growth to 3.8% on the back of autos, construction and garments.

Why This Is the Uncovered Story

Most business coverage of Pakistan’s economy treats the growth and inflation numbers in isolation from the geopolitical risk running through the Gulf. The IMF’s own modelling shows the adverse Iran-war scenario could add up to 1.5 percentage points of cumulative GDP damage by FY27, with the current account deficit and inflation impact both roughly doubling relative to a pre-conflict baseline. That is the number that determines whether Islamabad’s hard-won reserve buffer holds — not the headline growth print alone.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Russia Economy 2026: Why Fiscal Exhaustion, Not Just Sanctions, Is the Real Story

Malaysia Singapore AI Boom 2026: Inside the Sovereign AI Policy Shift Behind the Growth Numbers

Indonesia MSCI Downgrade Risk 2026: Why $13 Billion Still Hangs Over the Rupiah

Pakistan’s Economic Growth: Resilience Amid Challenges

China’s Q2 GDP Growth Misses Targets: Analyzing Economic Trends

Strait of Hormuz Crisis 2026: How Trump’s Toll U-Turn Exposes Global Economic Risk

SK Hynix’s Nasdaq Debut Just Exposed a Crack in the AI Trade

Pakistan’s Economic Survey FY26: Inflation Spike Insights

Indonesia’s Nickel U-Turn Could Reshape Global EV Battery Prices

Russia’s War Economy Model Is Starting to Crack, Think Tank Warns

China’s Record Exports Hide a Rare Earths Warning Sign

Malaysia’s GDP Upgrade Signals a $23 Trillion Bet on Southeast Asia

Singapore’s AI Export Boom Is Masking a Real Growth Slowdown

Dubai’s Real Growth Driver in 2026 Isn’t Real Estate — It’s Healthcare

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Top 7 Banking Stocks for Investment in PSX: Pakistan’s Lenders Are Still Printing Money

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

JPMorgan Cuts Anthropic AI Access in Hong Kong

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

India Economic Rise 2026: How the Subcontinent Toppled Japan

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025