Analysis

Pakistan Thwarts JPMorgan’s Efforts to Buy Historic New York Hotel

The Roosevelt Hotel saga — a century-old Midtown landmark, a cash-strapped Pakistani state airline, and Wall Street’s most powerful bank — has taken a turn that no one on Madison Avenue saw coming.

The Grand Dame Falls Silent Again

Walk past 45 East 45th Street on a winter morning in 2026 and you will find a building that once defined Midtown Manhattan’s glamour standing derelict and dark. The Roosevelt Hotel — a 22-story Beaux-Arts colossus designed by George B. Post and opened in 1924, named after President Theodore Roosevelt — once hosted Fiorello LaGuardia’s mayoral campaigns in its ballrooms, saw Guy Lombardo ring in the New Year from its bandstand for three decades, and appeared on the silver screen in The French Connection and Wall Street. Today its lobby is silent, its 1,025 rooms stripped of guests, and its fate the subject of one of the most convoluted geopolitical real-estate sagas in New York history.

At the center of this drama: Pakistan International Airlines, the state-controlled carrier that has owned the Roosevelt since 2000; JPMorgan Chase, the most powerful bank on earth, whose gleaming new headquarters at 270 Park Avenue looms just two blocks away; and, most improbably, the Trump White House, which has now inserted itself as Islamabad’s unlikely development partner.

Pakistan has effectively thwarted JPMorgan’s serious efforts to acquire the site — not through formal regulatory action, but through a strategic pivot that locked Wall Street out and invited Washington in.

JPMorgan’s Midtown Empire Play

To understand why JPMorgan wanted the Roosevelt, look north from Grand Central Terminal. The bank has spent years assembling one of the most formidable corporate campuses in American history. Its supertall headquarters at 270 Park Avenue — built after acquiring air rights from neighboring churches — rises 60 stories over Midtown. The adjacent property at 383 Madison Avenue, acquired following Bear Stearns’ collapse, is currently being reclad in a matching bronze facade.

The Roosevelt site sits precisely in the gap between these two towers, spanning the full block between Madison and Vanderbilt Avenues and East 44th and 45th Streets. For Jamie Dimon’s bank, acquiring it would not merely be a real-estate investment — it would be a generational campus consolidation, potentially giving JPMorgan control over roughly 7 million square feet of prime Midtown space.

JPMorgan emerged as one of the advanced bidders for the Roosevelt site, submitting a proposal to ground-lease the property for 99 years The Promote — a structure that would have allowed Pakistan to retain nominal ownership of the land while effectively ceding control for a century. According to reporting by The Promote, industry sources described JPMorgan as being among the most serious contenders, with a proposal that could have created “one of the most formidable corporate campuses in recent New York history.”

A JPMorgan analyst had separately noted that the Roosevelt “has essentially been a placeholder for a major office tower for many years” Crain’s New York Business — a recognition that the site’s value lies not in its hospitality bones but in the steel-and-glass tower that could replace them.

The bank was not alone. JPMorgan kicked the tires alongside Shahal Khan’s Burkhan World Investments, which pitched a plan to co-develop the site The Real Deal, while names including SL Green, Tishman Speyer, Related, and Vornado were variously reported to be circling.

Pakistan’s Long History of Indecision

That so many serious buyers materialized — and that none closed a deal — speaks to a dysfunction at the heart of PIA’s ownership that has frustrated New York’s development community for years.

PIA has leased or owned the Roosevelt Hotel since 1979 and has several times since sought to get rid of it. The Real Deal As far back as 2007, the airline put the hotel on the market asking $1 billion. In 2018, a Pakistani prime minister personally blocked a selloff plan, declaring that “apart from being a valuable property, the hotel also carries cultural significance for Pakistan.” PIA, meanwhile, refinanced the hotel’s debt that same year — notably with a $105 million loan from JPMorgan Chase itself, a detail that gives the bank’s subsequent acquisition bid a particularly layered quality.

In 2024, Pakistan hired JLL to market the property either for an outright sale or a joint venture development partnership — but after JPMorgan kicked the tires on it, JLL resigned in July, citing a conflict of interest from clients who were interested in bidding on the site. The Real Deal The explanation was widely viewed in the industry as a gracious exit from a messy situation.

Pakistan’s privatization commission was once again trying to find a broker, putting out a call for brokers and financial advisors with “proven experience of successful completion of similar transactions” in the New York metropolitan area. The Real Deal Five of the seven subsequent proposals were rejected for non-compliance. The reset had begun.

The Strategic Pivot: No Sale, Just JV

The decisive blow to JPMorgan’s ambitions came not from a regulator, a court, or a rival bidder — but from Islamabad’s own change of strategy.

Pakistan’s government approved a “transaction structure for the Roosevelt Hotel,” saying it won’t do an outright sale but has decided to adopt a joint venture model to maximize long-term value. Hotel Online The government’s position: it would contribute the land, while a development partner would inject approximately $1 billion in equity. Pakistan expected a $100 million initial payment from any JV partner by June 2026. The country’s privatization adviser, Muhammad Ali, was emphatic — the land was not for sale.

This single decision effectively killed JPMorgan’s 99-year ground-lease proposal. A ground lease over a century is an unusual instrument, but it is not ownership. If Pakistan won’t sell outright, won’t entertain a century-long lease, and insists on a JV where it retains strategic control, then the deal structure JPMorgan had in mind simply ceased to exist.

Analysts estimated the property could fetch at least $1 billion in an outright open-market sale AOL, and the site can be built up to nearly 2 million square feet if a developer exploits zoning bonuses tied to transit and public amenities. The prize remains enormous. Pakistan’s refusal to sell it reflects both strategic calculation and the Islamabad bureaucracy’s chronic inability to make a final decision.

Trump Enters the Building

Then came the twist no Manhattan power broker anticipated.

The Pakistani government signed a deal to cooperate with the U.S. federal government on the redevelopment and operation of the property. The Real Deal The agreement — negotiated by Trump’s special envoy Steve Witkoff, the New York developer who has become an unlikely global diplomat — was formalized in a Memorandum of Understanding between the U.S. General Services Administration and Pakistan’s Ministry of Finance.

The two parties “formally launched a strategic economic initiative, including collaboration with the U.S. General Services Administration regarding the operation, maintenance, renovation, and redevelopment of the Roosevelt Hotel in New York,” Pakistan’s finance division announced. Costar The stated goal: to “secure maximum value for this property while strengthening Pakistan-United States economic ties.”

The MOU is nonbinding. It says nothing about equity splits, financial contributions, or which side controls the design brief. The role of the GSA, which typically only manages federal properties, remains unclear. 6sqft Real estate professionals reacted with bewilderment — “Unbelievable,” said one Manhattan power broker. Others speculated that Witkoff, who built his career financing Manhattan hotels including the Times Square Edition, sees longer-term opportunity in the site.

What is clear: with the U.S. government now formally in the picture as a “partner,” an outright sale to any private buyer — JPMorgan included — becomes politically and practically far more complicated.

The Financial Pressure Behind Pakistan’s Moves

Islamabad’s posture throughout this process is impossible to understand without the context of Pakistan’s sovereign debt crisis.

The Pakistani government is $7 billion in hock to the International Monetary Fund and is desperate to sell off assets to pay off the debt. AOL That desperation explains why a deal was always theoretically possible. The obstruction comes from the countervailing force of political sensitivity — the Roosevelt is one of Pakistan’s most visible foreign assets, and any selloff carries domestic political risk.

Compounding the irony: the Pakistani government-owned Roosevelt Hotel pocketed $146.6 million to house migrants for two years, but now owes $13.6 million in overdue property taxes and nearly $1 million in unpaid water bills. National Today A potential federal joint venture could trigger a tax exemption, further inflaming New York City officials already frustrated by the situation.

The hotel’s annual property tax bill is $7.7 million, and a potential joint venture between Pakistan and the U.S. government to demolish and redevelop the Roosevelt could trigger a federal tax exemption, potentially costing the city tens of millions per year. National Today

What It Means: U.S.-Pakistan Relations, Wall Street, and Midtown’s Future

Geopolitical Chess in a Midtown Ballroom

The Roosevelt Hotel saga has become a microcosm of the broader U.S.-Pakistan bilateral relationship — transactional, frustrating, and perpetually unresolved. The Witkoff MOU is, on one reading, a diplomatic gesture: bringing Pakistan closer to Washington at a moment when geopolitical alignments in South Asia matter enormously. On another reading, it is a sign of the Trump administration’s comfort with inserting the federal government into unusual real-estate plays, particularly in New York City.

Either way, JPMorgan — an institution that famously operates on the principle that relationships and proximity to power matter — now finds itself on the outside of a deal involving two governments rather than one.

The Manhattan Office Market in 2026

The Roosevelt site remains one of the most consequential undeveloped parcels in Midtown. The office market around Grand Central Terminal — what analysts call the Plaza District — has continued to tighten even as the broader Manhattan market wrestles with remote-work headwinds. The hotel is located near marquee New York destinations such as Grand Central Terminal, One Vanderbilt, and JPMorgan Chase’s own headquarters, placing it in one of Manhattan’s most valuable commercial zones. Costar

Whatever ultimately rises on the site — whether under a U.S.-Pakistan JV, a reconstituted private deal, or some hybrid structure — it will be among the defining towers of Manhattan’s next decade. The question is whether Pakistan’s government can make a final, binding decision before the market moves on.

Sovereign Wealth Strategy — and Its Limits

Pakistan’s refusal to sell is not irrational. Sovereign wealth theory argues that revenue-generating or appreciating assets should not be liquidated under distress; they should be leveraged. By holding the land and seeking equity partners, Pakistan theoretically captures upside while preserving a strategic asset. The problem is execution: Pakistan has been “waffling over what to do with the hotel since acquiring it in 2000,” as The Real Deal noted recently, and every year of indecision is a year of $7.7 million in property taxes, maintenance costs on a shuttered building, and opportunity cost on a billion-dollar site earning nothing.

For sovereign fund analysts watching from Abu Dhabi, Singapore, or Oslo, Pakistan’s Roosevelt Hotel management is a cautionary tale — not of bad strategy, but of institutional dysfunction masquerading as strategy.

Looking Ahead: 2026 and Beyond

The MOU signed between Washington and Islamabad is nonbinding and time-bounded, and Pakistan’s privatization commission has already demonstrated a flair for restarting processes from scratch. It is entirely possible that the U.S. government partnership dissolves, that JPMorgan — or another Wall Street player — re-enters with a revised structure, or that Pakistan finally names a JV partner from among the several serious bidders who have circled the site.

Pakistan’s government is estimating the redevelopment will take four to five years, with “interest level extremely high” among potential partners. Hotel Online

What is not in doubt: the Roosevelt Hotel will be demolished. The economics of Manhattan’s office market are too compelling, and the structural condition of a century-old property shuttered since 2020 too deteriorated, for any other outcome. The only question — as it has been for a quarter century — is who will control what rises in its place, and whether Pakistan can bring itself to finally answer that question.

For now, JPMorgan will have to content itself with the view of the empty building from the glass spire of 270 Park Avenue.

Key Facts at a Glance

| Detail | Information |

|---|---|

| Property | Roosevelt Hotel, 45 East 45th Street, Manhattan |

| Year Built | 1924, designed by George B. Post (Beaux-Arts) |

| Current Owner | Pakistan International Airlines (state-controlled) |

| Ownership Since | 2000 |

| Estimated Site Value | $1 billion+ |

| Maximum Buildable Area | ~2 million sq ft (with zoning bonuses) |

| JPMorgan Proposal | 99-year ground lease |

| Pakistan’s Debt to IMF | $7 billion |

| Roosevelt Back Taxes Owed | $13.6 million |

| Migrant Housing Revenue | $146.6 million (2023–2025) |

| U.S. Government Deal | MOU via GSA / Steve Witkoff (Feb. 2026) |

| Pakistan’s Decision | No outright sale; JV only |

FAQ: People Also Ask

Q1: Why did Pakistan block JPMorgan from buying the Roosevelt Hotel? Pakistan did not block JPMorgan through a regulatory order, but its decision to rule out an outright sale and pursue only a joint-venture model effectively ended JPMorgan’s 99-year ground lease proposal. Pakistan’s government insists on retaining ownership of the land while seeking an equity development partner.

Q2: What is the Roosevelt Hotel in New York City? The Roosevelt Hotel is a landmark 22-story Beaux-Arts hotel at 45 East 45th Street in Midtown Manhattan, built in 1924 and named after President Theodore Roosevelt. It has been owned by Pakistan International Airlines since 2000 and closed in 2020.

Q3: What is JPMorgan’s interest in the Roosevelt Hotel site? JPMorgan submitted a proposal to ground-lease the Roosevelt site for 99 years, which would have extended its growing Midtown campus — anchored by 270 Park Avenue and 383 Madison — into a potential 7 million square foot corporate compound near Grand Central Terminal.

Q4: What deal did the U.S. government sign with Pakistan over the Roosevelt Hotel? In February 2026, the Trump administration’s General Services Administration signed a nonbinding Memorandum of Understanding with Pakistan’s government to jointly redevelop, renovate, and maintain the Roosevelt Hotel site. The deal was negotiated by Trump special envoy Steve Witkoff.

Q5: How much is the Roosevelt Hotel site worth? Real estate analysts estimate the site is worth at least $1 billion for its development potential, given its location in Midtown Manhattan’s Plaza District near Grand Central Terminal. With zoning bonuses, the site could accommodate nearly 2 million square feet of new construction.

Q6: What happened to the Roosevelt Hotel migrant shelter? New York City leased the Roosevelt Hotel from PIA for approximately $220 million to serve as the city’s primary migrant intake center from 2023 to early 2025. The lease was terminated when the migrant crisis abated, and Pakistan has since pursued redevelopment.

Q7: What is Pakistan’s financial situation with the Roosevelt Hotel? Pakistan owes $13.6 million in overdue property taxes and nearly $1 million in unpaid water bills on the Roosevelt, despite earning $146.6 million from the city’s migrant housing contract. Pakistan is also carrying $7 billion in IMF debt, making the Roosevelt one of its most strategically important foreign assets.

Targeted Keyword List

| Keyword | Est. Monthly Volume | Difficulty |

|---|---|---|

| Pakistan JPMorgan Roosevelt Hotel | 1,200–2,400 | Low–Medium |

| Pakistan blocks JPMorgan hotel deal | 800–1,600 | Low |

| Roosevelt Hotel New York sale 2025 2026 | 2,000–4,000 | Medium |

| historic New York hotel sale thwarted | 500–900 | Low |

| JPMorgan Chase New York real estate bid | 1,200–2,000 | Medium |

| Roosevelt Hotel Pakistan redevelopment | 1,500–3,000 | Low–Medium |

| Pakistan sovereign asset Roosevelt Hotel | 300–700 | Low |

| Roosevelt Hotel JV deal New York | 600–1,200 | Low |

| Steve Witkoff Roosevelt Hotel deal | 400–800 | Low |

| Pakistan IMF privatization hotel | 500–1,000 | Low |

| New York landmark hotel ownership dispute | 300–600 | Low |

| JPMorgan Midtown campus expansion | 700–1,400 | Medium |

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

A market battered by geopolitics and panic-selling staged one of its most convincing recoveries of the year — but seasoned investors know the hard work is just beginning

There is a peculiar kind of quiet that settles over a trading floor the morning after chaos. The screens are the same. The tickers keep scrolling. But the fingers on keyboards move with a different energy — cautious, calculating, then, as the session matures, something closer to conviction. That was the texture of Thursday’s session at the Pakistan Stock Exchange. By the time the closing bell rang on March 5, the benchmark KSE-100 Index had gained 5,433.46 points, settling at 161,210.67 — a rise of 3.49% that confirmed, at least for now, that the worst of the week’s freefall was behind Pakistan’s equity markets.

The intraday high of 161,476.84, touched in the closing minutes of trade, told an even more bullish story: buyers were not merely nibbling at discounts. They were pressing into the market with force.

The Week That Broke Records — and Nerves

To appreciate Thursday’s significance, one must first reckon with the magnitude of what preceded it. On March 2 — a session that Pakistani financial historians will struggle to contextualise — the KSE-100 collapsed by 16,089 points, or 9.57%, closing at 151,972.99. It was the single largest one-day point decline in the exchange’s history. The trigger: escalating Middle East hostilities following joint US-Israeli strikes on Iranian military infrastructure and Tehran’s retaliatory strikes on US installations across Gulf states. Panic-led liquidation, amplified by mutual fund redemptions and retail stop-losses, turned an anxious morning into a rout.

Tuesday brought a partial reprieve — the index clawed back 5,159 points to close at 157,132 — but the recovery lacked staying power. Wednesday saw a renewed retreat of 1,354 points, the index settling at 155,777.21 as investors, still shaken, remained unwilling to commit. It was the scale of Thursday’s surge — 5,433 points, or 3.49%, marking one of the strongest single-day gains in recent sessions — that finally signalled a genuine shift in sentiment. Minute Mirror

Despite the turbulence, the KSE-100 remains approximately 41.73% higher than it was a year ago TRADING ECONOMICS, a fact that sophisticated international investors, scanning Bloomberg’s KSE-100 quote page for entry points, will not have missed.

Anatomy of a Rally: Sectors That Drove the 5,433-Point Surge

Thursday’s PSX buying momentum was emphatically broad-based. This was not a sector-specific bounce driven by a single commodity supercycle or a policy announcement. It was, as Arif Habib Limited’s Deputy Head of Trading Ali Najib put it, a market-wide expression of renewed confidence.

A widespread buying spree swept across oil and gas exploration companies, oil marketing companies, power generation, automobile assemblers, cement, commercial banks, and refinery stocks. Profit by Pakistan Today The breadth of that buying matters: when rally participation is narrow, it often reflects short-covering rather than genuine re-engagement. When cement producers and automobile assemblers move alongside refiners and banks, it suggests institutional portfolios are being rebuilt from the ground up.

The index-heavy names that drove the arithmetic were formidable. Attock Refinery, Hub Power Company, Mari Petroleum, OGDC, Pakistan Petroleum Limited, Pakistan Oilfields, Pakistan State Oil, Sui Northern Gas Pipelines, Sui Southern Gas Company, MCB Bank, Meezan Bank, National Bank of Pakistan, and UBL all traded firmly higher. Profit by Pakistan Today Collectively, the leading contributors added approximately 3,334 points to the overall benchmark gain. Minute Mirror

The energy complex’s outperformance deserves special attention. Oil and gold prices moved higher globally amid ongoing supply concerns — a direct tailwind for Pakistan’s upstream exploration players and refiners, whose dollar-linked revenues benefit from any crude price elevation. For a country that imports a significant share of its energy needs, the calculus is complex: higher oil prices widen the current account deficit even as they lift exploration-sector equities. Investors, for now, chose to focus on the equity upside.

Total traded volume reached 718.6 million shares, with total transaction value standing at approximately PKR 35 billion Minute Mirror — robust figures that suggest this was not a low-liquidity, technically-driven drift upward but a session characterised by genuine two-way price discovery tilting decisively toward buyers.

Why It Matters: The Global Mirror

Pakistan’s markets rarely move in isolation from global risk appetite, and Thursday was no different. Asian equities advanced broadly as US Treasury prices declined, reflecting improved risk appetite after recent volatility linked to Middle East tensions. MSCI’s broad index of Asia-Pacific shares outside Japan rose 2.9%, South Korea’s KOSPI led the region with a gain of 10.4%, and Japan’s Nikkei added 2.9%. Profit by Pakistan Today

That global backdrop provided critical cover for PSX’s recovery. When risk-off sentiment dominates globally, frontier and emerging markets suffer disproportionately — capital flees to safe-haven assets and Pakistan’s thin foreign investor base tends to compress valuations sharply. Thursday’s shift in that global dynamic gave local institutional investors — the real swing factor in PSX liquidity — permission to re-engage without fear of being caught on the wrong side of an international tide.

US benchmark 10-year Treasury yields rose 2.7 basis points to 4.109%, while the 30-year bond yield climbed 3.1 basis points to 4.748%. Profit by Pakistan Today Rising yields typically signal a rotation away from bonds and into risk assets — including equities in frontier markets that had been beaten down to historically attractive valuations. Trading Economics data confirms that despite Thursday’s sharp recovery, the KSE-100 has still declined roughly 12.47% over the past month, leaving ample room for further mean-reversion if geopolitical anxieties continue to subside.

The IMF Variable and Pakistan’s Macro Scaffolding

No analysis of PSX momentum is complete without interrogating the broader macroeconomic architecture in which these market swings occur. Pakistan is currently operating within the framework of an IMF Extended Fund Facility — a programme that has done much of the structural heavy lifting to stabilise the rupee, compress the current account deficit, and begin unwinding the circular debt that has long strangled the power sector.

In a telling development this week, the IMF mission team decided to conduct virtual discussions for the third review of the Extended Fund Facility and the second review of the Resilience and Sustainability Facility, citing the prevailing security situation. The Express Tribune The decision to proceed virtually rather than suspend the review process entirely is significant. It signals that the Fund considers Pakistan’s reform trajectory sufficiently credible to maintain engagement — even as security conditions complicate standard operations. For foreign investors monitoring Pakistan’s sovereign risk profile, this is a quiet but meaningful confidence signal.

The rupee’s relative stability through this turbulent week also merits attention. A currency that holds its ground during an equity market shock of the magnitude seen on March 2 suggests underlying foreign exchange reserves and current account dynamics that are meaningfully more resilient than Pakistan’s position even eighteen months ago. That stability reduces hedging costs for international portfolio investors and lowers the barrier to re-entry.

Reading the Road Ahead: Catalysts and Risks

The KSE-100 Index closes at 161,210.67 with a convincing recovery narrative — but the intelligent investor must resist the temptation to extrapolate a single session into a trend.

The central risk remains geopolitical. The Middle East situation that triggered the March 2 sell-off has not resolved; it has merely paused. Any resumption of direct military exchanges between Iran and US-Israeli forces would almost certainly reignite the risk-off impulse that sent the KSE-100 to its worst single-day performance in history. Pakistan’s geographic proximity to multiple regional flashpoints — including continued uncertainty along the Afghan border — means that geopolitical tail risks are not abstract for PSX investors; they are priced with a premium.

On the domestic side, the upcoming IMF review outcome, energy sector reform progress, and any revision to the State Bank’s monetary policy stance will serve as the next key inflection points. The central bank has been cautiously easing — a trajectory that supports equity valuations by compressing the discount rate applied to future earnings — but inflation’s stickiness could complicate any further cuts.

The catalysts for sustained recovery are equally real. Analysts attributed Thursday’s rally partly to bargain hunting after recent heavy losses and improved sentiment among institutional investors Minute Mirror — the classic post-crash dynamic of sophisticated money stepping into the vacuum left by panic-sellers. If earnings season in the coming weeks confirms that the underlying corporate performance of Pakistan’s blue-chips remains intact, the valuation case for KSE-100 at these levels is compelling by any regional comparison.

The cement sector’s participation in Thursday’s rally is worth watching as a leading indicator of domestic economic momentum — cement volumes are a proxy for construction and infrastructure activity. Similarly, automobile assembler performance tracks consumer credit and disposable income trends. Both sectors buying in suggests that the damage to domestic economic confidence, while real, may be shallower than the March 2 panic implied.

A Market Finding Its Level

There is a question that every serious investor in frontier markets must eventually confront: at what point does volatility become opportunity? The KSE-100’s journey this week — from an all-time high earlier this year, through the historic 9.57% single-session collapse, through the grinding partial recoveries and renewed selloffs, to Thursday’s broad-based KSE-100 gains 3.5% vindication — has been, in miniature, the story of Pakistan’s equity market itself: high-drama, technically oversold, and carrying within its volatility the seeds of disproportionate returns for those with the patience and conviction to stay the course.

The PSX buying momentum on Thursday was not merely a technical bounce. It was a signal — tentative, yes, and hedged with legitimate near-term risks — that the market’s fundamentals have not broken. The index’s trajectory over the next four to six weeks will determine whether March 5 is remembered as the first day of recovery or merely as a false dawn. History suggests that in markets like Pakistan’s, where institutional depth is growing but retail sentiment remains prone to panic, the truth usually lies somewhere instructively between the two.

The KSE-100’s next chapter is unwritten. But Thursday’s 5,433-point script was, at minimum, a compelling opening act.

FAQ (FREQUENTLY ASKED QUESTIONS)

Q1: Why did the KSE-100 gain 3.5% today on March 5, 2026? The KSE-100 rebounded 5,433 points as broad-based buying returned across energy, banking, cement, and automotive sectors, aided by improving global risk appetite following easing Middle East tensions and a 2.9% rise in Asian equity indices.

Q2: What caused the KSE-100 to crash 16,000 points on March 2, 2026? The KSE-100 recorded its worst-ever single-day fall of 16,089 points (-9.57%) after joint US-Israeli airstrikes on Iran triggered global risk-off sentiment, panic selling, and mutual fund redemption pressure at the Pakistan Stock Exchange.

Q3: What is the KSE-100 intraday high for March 5, 2026? The KSE-100 hit an intraday high of 161,476.84 during the final minutes of Thursday’s trading session before closing at 161,210.67.

Q4: Which sectors led the KSE-100 recovery on March 5, 2026? Oil and gas exploration, oil marketing companies, commercial banks, power generation, cement, automobile assemblers, and refinery stocks all participated in the broad-based rally, contributing approximately 3,334 index points collectively.

Q5: Is the KSE-100 still down from its all-time high after the March 2026 crash? Yes. Despite Thursday’s 3.49% gain, the KSE-100 remains approximately 12.47% below its level from a month prior and well below its all-time high, though it remains roughly 41.73% higher year-on-year.

Q6: How does the IMF programme affect Pakistan Stock Exchange performance? Pakistan’s ongoing IMF Extended Fund Facility has stabilised the rupee and improved Pakistan’s macro fundamentals. The IMF’s decision to continue virtual review discussions despite security concerns signals sustained programme engagement, which supports investor confidence in PSX-listed equities.

Q7: What are the key risks that could reverse the KSE-100 recovery? The primary risks include a re-escalation of Middle East hostilities, a negative outcome from the IMF’s third EFF review, rupee instability, persistent inflation limiting State Bank rate cuts, and any deterioration in regional security along Pakistan’s borders.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Kremlin’s signal that it could voluntarily exit the European gas market is part bluff, part genuine pivot — and entirely consequential for global energy security in 2026 and beyond.

Russia may halt gas supplies to Europe as Putin exploits the Iran energy spike. Analysing the real stakes behind the Kremlin’s threat, TTF price surge, and Moscow’s Asian pivot.

Introduction: A Threat Dressed as a Business Decision

On the morning of March 4, 2026, Russian President Vladimir Putin sat down with Kremlin television correspondent Pavel Zarubin and appeared to do something unusual for a man whose public statements are rarely accidental: he thought out loud. Against the backdrop of global energy markets in full-blown crisis — triggered by the U.S.-Israeli military campaign against Iran and Tehran’s counter-strikes across the Gulf — Putin mused that Russia might halt gas supplies to Europe entirely, and do so immediately, rather than wait to be formally ejected under the European Union’s own phase-out timeline.

“Now other markets are opening up,” Putin said, according to the Kremlin transcript. “And perhaps it would be more profitable for us to stop supplying the European market right now. To move into those markets that are opening up and establish ourselves there.”

He was careful, almost lawyerly, in his framing. “This is not a decision,” he added. “It is, in this case, what is called thinking out loud. I will definitely instruct the government to work on this issue together with our companies.” But in the language of energy geopolitics, where a single presidential signal can move commodity markets by double digits, the distinction between thinking out loud and making policy is narrower than it appears. What Putin said on March 4 was not a bluff — or at least, not entirely one. It was a calculated reflection of a structural shift already underway, supercharged by a Middle East crisis that has remade the arithmetic of global gas markets in just seventy-two hours.

To understand what this means, you have to understand where Europe stands today — and where Russia has been heading for the past three years.

Background: A Market Already Departing Itself

The story of Russia’s decline as Europe’s dominant gas supplier is one of the most dramatic commercial collapses in modern energy history. Before February 2022, Russia supplied approximately 40% of the EU’s pipeline gas, making Gazprom — then valued at over $330 billion — the third-largest company in the world. By early 2026, that figure had fallen to just 6%, and Gazprom’s market capitalisation had cratered to roughly $40 billion, a destruction of value that no Western sanctions regime alone could have engineered without Moscow’s own strategic miscalculations.

Europe’s REPowerEU programme — launched in the immediate aftermath of the Ukraine invasion — has proven surprisingly effective. Norway, the United States, and Algeria have collectively absorbed most of what Russia once provided. LNG import terminals that did not exist three years ago now dot Europe’s Atlantic coastline. The continent’s dependence on pipeline gas from a single adversarial supplier has been structurally dismantled.

What remained of Russia’s European gas footprint was a dwindling rump of legacy contracts, principally serving Hungary and Slovakia — nations whose governments had maintained warmer diplomatic relationships with Moscow. It was a commercially marginal position, but one that gave the Kremlin a residual foothold in Europe’s energy map and, more importantly, a psychological card to play. That card is what Putin attempted to deploy on Wednesday.

The European Commission has approved a binding phase-out schedule that accelerates significantly this spring. The key EU ban milestones are: April 25, 2026, for short-term Russian LNG contracts; June 17, 2026, for short-term pipeline gas; January 1, 2027, for long-term LNG contracts; and September 30, 2027, for long-term pipeline contracts. Putin’s suggestion — that Russia should exit now rather than wait to be shown the door — is, on one level, a face-saving exercise. But on another, it is a genuine strategic calculation being shaped by events thousands of kilometres away, in the Persian Gulf.

The Iran Crisis: How a Middle East War Changed European Gas Arithmetic Overnight

The convergence of the Iran crisis with Putin’s remarks is not coincidental. In late February 2026, European gas markets had entered what traders described as a period of “prolonged dormancy.” The Dutch TTF benchmark — Europe’s primary gas pricing index — had drifted to roughly €32 per megawatt hour, the lower half of Goldman Sachs’s estimated coal-to-gas switching range. Norwegian output from the Troll field was at peak efficiency. The energy crisis of 2022 seemed a distant, if instructive, memory.

Then, over the weekend of February 28 to March 1, came the military escalation that markets had not priced in. Iranian strikes on Gulf Arab neighbors, the effective closure of the Strait of Hormuz, and — most critically for gas markets — QatarEnergy’s announcement that it was halting all LNG production after Iranian drone attacks targeted two of its facilities. QatarEnergy accounts for nearly one-fifth of global LNG exports. The impact was immediate and seismic.

By Tuesday, March 3, the TTF had surged more than 60% to a three-year high, peaking intraday at €65.79/MWh. Goldman Sachs — which had entered the week forecasting a €36/MWh April TTF price — raised its April forecast to €55/MWh and warned that a full one-month Strait of Hormuz closure could drive TTF toward €74/MWh, the level that triggered large-scale demand destruction during the 2022 crisis. Brent crude climbed to around $83 a barrel mid-week, some 25% above its pre-strike close.

Chart: European TTF Gas Price vs. Iran Crisis Timeline (February–March 2026) TTF at ~€32/MWh (Feb 28) → €46.41/MWh (Mar 2, Hormuz closure) → €65.79/MWh intraday peak (Mar 3, Qatar halt) → ~€60/MWh (Mar 4, Putin statement). Goldman Sachs scenario range: €74–€90/MWh if disruption extends beyond 30 days. 2022 crisis peak for reference: €345/MWh (August 2022). Source: ICE TTF, Goldman Sachs Commodity Research, ICIS.

The scale of Europe’s structural vulnerability was made even more vivid by the storage data. EU gas storage entered March 2026 at approximately 46 billion cubic metres — compared to 60 bcm in 2025 and 77 bcm in 2024. Facility fill rates were sitting at around 30% of capacity, with Germany at roughly 21.6% and France in the low-20s. Oxford Economics warned that European storage was now on track to fall below 20% by the end of the summer refill season, making the EU’s mandated 80% target for December virtually unreachable without a rapid restoration of Qatari output and Hormuz shipping lanes.

It was into this environment — with European buyers suddenly desperate for any available molecule and willing to pay premium prices — that Putin delivered his “thinking out loud” signal.

Deep Analysis: What Putin Actually Said, and What It Means

Strip away the diplomatic language and the Kremlin’s careful framing, and Putin’s message on March 4 had three distinct layers.

The first was commercial. With global spot LNG prices surging alongside TTF, the opportunity cost of continuing to sell residual pipeline volumes to a market that has legislated for your exit has genuinely shifted. “Customers have emerged who are willing to buy the same natural gas at higher prices, in this case due to events in the Middle East, the closure of the Strait of Hormuz, and so on,” Putin told Zarubin. “This is natural; there’s nothing here, there’s no political agenda — it is just business.” This is not entirely a confection. The disruption to Qatari and Gulf supply has created a genuine spot-market premium that makes diverting flexible LNG cargoes to Asian buyers financially attractive.

The second layer was geopolitical. Ukraine’s government immediately characterised Putin’s remarks as “Energy Blackmail 2.0”, arguing that Moscow is attempting to exploit the global energy shock to pressure Europe into softening its next round of gas sanctions — specifically the April 25 deadline for banning new short-term Russian LNG contracts. That reading is credible. Putin linked his remarks directly to the EU’s “misguided policies” and singled out Slovakia and Hungary as “reliable partners” who would continue to receive Russian gas — a studied wedge aimed at splitting the bloc along its most familiar fault lines.

The third layer is structural, and it is the one that matters most for the medium term. Russia is not simply threatening to leave Europe’s gas market. It is trying, under conditions of genuine commercial pressure, to accelerate a pivot that is already underway — but that faces serious bottlenecks. Russia’s pipeline gas exports to China via the Power of Siberia 1 line are expected to hit 38–39 bcm in 2025, up from 31 bcm the previous year. A legally binding memorandum to build the 50 bcm Power of Siberia 2 pipeline — running from the Yamal Peninsula through Mongolia to northern China — was signed in September 2025. But key commercial parameters, including price, financing, and construction timeline, remain unresolved. The pipeline could not realistically begin deliveries before 2030.

That gap — between the rhetoric of an Asian pivot and its physical reality — is the central vulnerability in Putin’s position. Russia can talk about redirecting gas to “more promising markets.” It cannot actually do so at scale, quickly, without the infrastructure that does not yet exist.

The Asymmetry of Pain: Who Needs This More?

The critical question any serious analyst must ask is: who is in the weaker negotiating position? And the honest answer is that both sides are weaker than they publicly admit.

Europe is, right now, more exposed than at any point since 2022. Low storage, a Qatari production halt, a constrained Hormuz corridor, and the structural dependency on spot LNG that replaced Russian pipeline gas — all of this has placed the EU in a position where any additional supply disruption narrows the margin between a price shock and a supply crisis. The European Commission told member states on March 4 that it saw no immediate threat to supplies and was not planning emergency measures — technically accurate, but dependent on the Hormuz situation resolving within weeks rather than months. A sustained shutdown beyond thirty days would likely trigger EU emergency coordination mechanisms and, potentially, renewed industrial demand rationing in Germany and Italy.

Russia, meanwhile, is not in a position of strength it can easily monetise. Gazprom’s finances have been devastated by the loss of the European market. The company that was worth $330 billion in 2007 is now a shadow institution, sustained by domestic subsidies and Chinese pipeline flows priced at significant discounts to European rates. Before the war, Russia earned $20–30 billion annually from 150 bcm of gas sales to Europe. Even the completion of Power of Siberia 2 would replace only a fraction of that revenue, at lower unit prices. Nature Communications’ modelling suggests that under even the most optimistic Asian pivot scenario, Russia’s gas exports in 2040 would remain 13–38% below pre-crisis levels.

The Iran crisis is, therefore, a short-term opportunity for Moscow — a window in which spot prices are high enough to make diverting LNG cargoes look commercially rational, and in which Europe’s anxiety is visible enough to potentially extract political concessions. The window may be narrow, but Putin, characteristically, is using it.

Europe’s Alternatives and the Long-Term Structural Outlook

For European policy desks, the Iran crisis and the Putin signal converge into a single, uncomfortable lesson: the substitution of Russian pipeline gas with global LNG has increased Europe’s resilience against one specific geopolitical actor, while simultaneously increasing its exposure to a different category of risk — global market volatility and shipping lane disruption.

The diversification has been real and substantial. Norway remains the most stable and geographically proximate anchor of European supply. U.S. LNG — whose export volumes have grown dramatically since 2022 — provides a flexible, if expensive, buffer. Algeria and Azerbaijan offer incremental pipeline capacity. The EU’s REPowerEU framework — which accelerated renewable deployment alongside supply diversification — has also reduced the bloc’s structural gas demand.

But Bruegel’s analysis is pointed: “Europe’s exposure to geopolitical shocks remains rooted in its continued reliance on imported fossil fuels traded on volatile global markets — even if it has shifted dependency from Russia to other suppliers.” A continent that spent 2022 learning that pipeline dependency is a strategic liability spent 2023–2025 building LNG infrastructure — only to discover in March 2026 that LNG, too, has a geopolitical chokepoint problem. The Strait of Hormuz handles roughly one-fifth of global LNG trade. That is a structural risk that no European Commission regulation can address directly.

The medium-term policy implications are significant. Europe must continue to accelerate domestic renewable capacity at a pace that reduces structural gas demand — not merely substitutes one supplier for another. The ambition to hit 80% renewable electricity by 2030 under the Green Deal framework looks, against this backdrop, less like an environmental aspiration and more like an energy security imperative.

The Russia-China Variable: Beijing Holds the Cards

Perhaps the most consequential long-term dynamic in this story is not Russia’s leverage over Europe, but China’s leverage over Russia. Beijing has watched Moscow’s European collapse with the cool patience of a buyer who knows the seller has nowhere else to go. China’s share of Russia’s gas imports rose from 10% in 2021 to over 25% by 2024, and Power of Siberia 1 is now delivering above its planned annual capacity. But the pricing dynamic tells the real story: China is reportedly seeking gas prices closer to domestic levels around $60 per thousand cubic metres, while Russia has historically priced European contracts at approximately $350. That gap is not merely a commercial negotiating point — it is a measure of Russia’s strategic desperation.

When Putin instructs his government to “work on this issue together with our companies,” the companies in question face a market reality that the Kremlin’s rhetorical confidence does not reflect. The molecules that currently flow to residual European buyers cannot, in the near term, be physically rerouted to Asia without the infrastructure that will not exist for years. In the meantime, Russia’s attempt to leverage the Iran crisis into a position of energy market strength is constrained by its own strategic isolation — and by Beijing’s entirely rational decision to extract maximum commercial advantage from a supplier with limited alternatives.

What This Means for Global Energy Markets in 2026–2027

The Putin signal and the Iran crisis, taken together, define the contours of a global gas market that has entered a structurally more volatile phase. Several dynamics deserve close attention over the next twelve to eighteen months.

The TTF price range is not reverting to pre-crisis levels quickly. Goldman Sachs’s revised Q2 2026 forecast of €45/MWh represents a structural step-up from pre-crisis pricing, even under a relatively benign resolution of the Hormuz situation. The combination of low European storage, disrupted Qatari supply, and elevated geopolitical risk premia will keep European gas prices meaningfully above their late-2025 baseline.

Russia’s European exit is happening on Europe’s terms, not Moscow’s. Putin’s attempt to frame a forced commercial retreat as a voluntary strategic pivot is partly theatre. The EU’s phase-out timeline is legally binding, broadly supported across member states, and operationally advanced. The April 25 ban on new short-term Russian LNG contracts will proceed regardless of Putin’s “thinking out loud.” Hungary and Slovakia may retain some residual pipeline flows under existing long-term contracts, but these are margin cases, not strategic leverage.

The Power of Siberia 2 is not yet a solution. The September 2025 memorandum between Gazprom and CNPC was significant — but it left pricing, financing, and construction timing unresolved. The pipeline cannot realistically deliver first gas before 2030. Russia’s “pivot to Asia,” for the medium term, remains a slogan with better infrastructure than revenues.

The global LNG market is entering a period of structural tightness. The convergence of Qatari disruption, the Hormuz closure, and strong Asian demand growth means that the spot-market flexibility that Europe has relied upon since 2022 will be more expensive and less reliable than buyers had assumed. The ICIS-modelled €90/MWh scenario is not a tail risk — it is a realistic outcome if Hormuz shipping remains constrained through April and May. European industrial competitiveness, already under severe pressure, faces another energy cost headwind.

The real winner may be Washington. Putin himself acknowledged that if premium buyers emerge elsewhere, American LNG exporters “will, of course, leave the European market for higher-paying markets.” This is accurate — but it also reflects a constraint on U.S. flexibility. American LNG export facilities are capacity-constrained and cannot rapidly increase volumes. In the short term, the Iran crisis helps the case for additional U.S. LNG export investment. It also strengthens the hand of American negotiators in any bilateral energy diplomacy with European allies.

The deeper lesson, one that transcends any single news cycle, is that the post-2022 European energy reordering has produced greater supply diversity but not necessarily greater supply security. Swapping a pipeline from Moscow for LNG from a global market that transits through contested choke points is a trade-off, not a solution. Putin’s remarks on March 4 are best read not as a threat, but as a symptom — of Russia’s commercial decline, of Europe’s structural exposure, and of a global gas market in which the old certainties have been permanently dissolved.

The age of cheap, abundant gas flowing reliably through predictable corridors is over. What comes next will be shaped not by any single leader’s calculations, but by the hard physics of where the molecules are, how they move, and who controls the routes between them.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Understanding the Digital Economy: More Than a Sector, a System

There is a persistent category error at the heart of Pakistan’s economic policymaking. Officials speak of the “digital economy” the way an earlier generation spoke of textiles or agriculture — as a discrete sector, a line on an export ledger, a portfolio to be managed rather than a platform to be built. This confusion is not merely semantic. It shapes budget allocations, regulatory frameworks, institutional mandates, and, ultimately, the trajectory of a nation of 240 million people standing at a crossroads between chronic underdevelopment and a genuinely plausible economic transformation.

The digital economy, properly understood, is not a sector. It is the operating system upon which all modern economic activity increasingly runs. It encompasses the digitisation of production processes, the datafication of consumer behaviour, the platformisation of labour markets, and the emergence of knowledge as the primary factor of production. When the World Bank’s April 2025 Pakistan Development Update frames digital transformation as Pakistan’s most credible path toward export competitiveness and sustained growth, it is not advocating for a bigger IT park in Islamabad. It is arguing for a wholesale reimagining of what the Pakistani economy produces, and for whom.

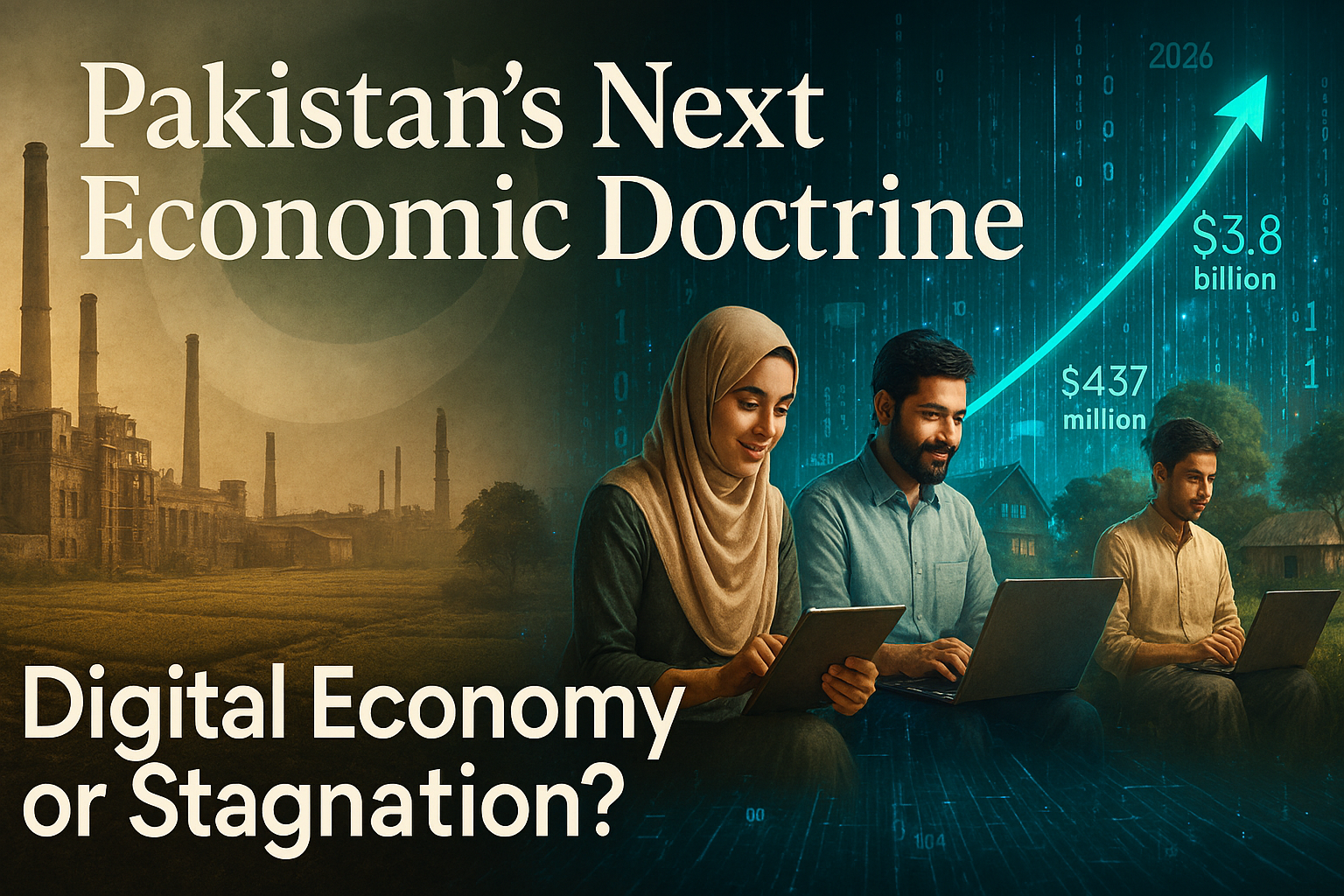

That reimagining has begun — tentatively, unevenly, and against considerable institutional resistance. The numbers, for once, are genuinely exciting. Pakistan IT exports reached $3.8 billion in FY2024–25, with the momentum building sharply into the current fiscal year: $2.61 billion in IT and ICT exports were recorded between July and January of FY2025–26, a 19.78% increase year-on-year, according to data released by the Pakistan Software Export Board (PSEB). December 2025 delivered a record single-month figure of $437 million — the highest in the country’s history. These are not marginal gains. They are signals of structural potential.

The question this analysis addresses is whether Pakistan possesses the institutional architecture, policy coherence, and political will to convert those signals into doctrine — or whether it will allow a historic opportunity to dissolve into the familiar entropy of short-termism, infrastructure neglect, and regulatory dysfunction.

Pakistan’s Emerging Digital Base: A Foundation That Defies the Headlines

The pessimistic narrative about Pakistan — fiscal crisis, security fragility, political instability — dominates international discourse and obscures a digital demographic reality that is, by most comparative metrics, extraordinary. Pakistan now has 116 million internet users, with penetration reaching 45.7% in early 2025 and accelerating. The PBS Household Survey 2024–25 found that over 70% of households have at least one member online, with individual usage approaching 57% of the adult population. Against the baseline of five years ago, this represents a compression of the connectivity timeline that took wealthier economies a generation to traverse.

Mobile is the primary vector. Pakistan’s 190 million mobile connections and 142 million broadband subscribers — figures corroborated by GSMA’s State of Mobile Internet Connectivity — reflect a population that has leapfrogged fixed-line infrastructure entirely and gone straight to smartphone-mediated internet access. Smartphone ownership has surged with the proliferation of affordable Chinese handsets, democratising access in a way that no government programme could have engineered.

The identity infrastructure is strengthening in parallel. NADRA’s digital ID system now covers the vast majority of the adult population, providing the authentication backbone without which digital financial services, e-commerce, and government-to-citizen digital delivery cannot scale. The State Bank of Pakistan’s (SBP) digital payments architecture — including the Raast instant payment system — has facilitated a measurable shift in transaction behaviour, particularly among younger urban cohorts.

What Pakistan has, in other words, is a digital base: not yet a digital economy, but the preconditions for one. The distinction is critical. A digital base is necessary but not sufficient. Converting it into export-generating, job-creating, productivity-enhancing economic activity requires deliberate policy architecture — something Pakistan has so far delivered only in fragments.

Geography Is Being Rewritten: The Location Dividend

For most of economic history, geography was fate. A landlocked country, a country far from major shipping lanes, a country without navigable rivers or natural harbours faced structural disadvantages that compounded over centuries. Pakistan’s geographic position — bordering Afghanistan, Iran, India, and China, with access to the Arabian Sea — has historically been as much a source of strategic anxiety as economic opportunity.

The digital economy rewrites this calculus. In knowledge-intensive digital services, physical location is increasingly irrelevant to market access. A software engineer in Lahore can serve a fintech client in Frankfurt. A data scientist in Karachi can work for a healthcare analytics firm in Houston. A UX designer in Peshawar can deliver to a product team in Singapore. The barriers that historically constrained Pakistani talent to domestic labour markets — or forced emigration — are structurally dissolving.

This is the location dividend: the ability to monetise Pakistani human capital in global markets without the friction costs of physical migration. It is a form of comparative advantage that requires no natural resources, no preferential trade agreements, and no proximity to wealthy consumer markets. It requires only talent, connectivity, and institutional conditions that allow value to flow across borders.

Pakistan’s digital economy growth model, at its most ambitious, is predicated on precisely this arbitrage: world-class technical skill delivered at emerging-market cost, routed through digital platforms, and paid in foreign exchange. The macroeconomic implications — for the current account, for foreign reserves, for wage convergence — are profound. The World Bank’s Digital Pakistan: Economic Policy for Export Competitiveness report identifies this services export channel as among the most scalable dimensions of the country’s growth potential.

The geography dividend is real. The question is whether Pakistan can build the institutional infrastructure to fully claim it.

The Freelancer Paradox: Scale Without Structure

Perhaps nowhere is the tension between Pakistan’s digital potential and its institutional constraints more vividly illustrated than in its freelance economy. The headline numbers are startling. Pakistan’s 2.37 million freelancers — an estimate from the Asian Development Bank (ADB) — generate a scale of digital services exports that places the country consistently in the top three to four globally on platforms including Upwork, Fiverr, and Toptal. Freelance earnings in H1 FY2025–26 reached $557 million, a 58% year-on-year increase from $352 million — a growth rate that no traditional export sector can approach.

This is the “freelancer paradox Pakistan” faces: enormous revealed comparative advantage, operating almost entirely outside formal policy architecture. The vast majority of Pakistan’s freelancers work without contracts, without access to institutional credit, without social protection, and without the kind of professional certification or dispute resolution frameworks that would allow them to move up the value chain from commodity task completion to complex, high-margin engagements.

The income ceiling is real and consequential. A Pakistani freelancer completing logo designs or basic data entry tasks on Fiverr earns at the low end of the global digital labour market. The same talent, operating through a structured agency model, with portfolio development support, client management training, and access to premium platforms, could command rates three to five times higher. The gap between what Pakistan’s freelance workforce earns and what it could earn is, effectively, a measure of what institutional neglect costs.

The foreign exchange dimension compounds the problem. Payments routed through platforms like PayPal — where availability for Pakistani users remains restricted — or through informal hawala networks, often bypass the formal banking system entirely. The SBP has made progress in facilitating formal remittance channels, but significant friction remains. Pakistan freelance exports are growing despite the system, not because of it.

A comprehensive Pakistan digital economy doctrine must address the freelancer economy not as an afterthought but as a strategic asset requiring dedicated institutional support: access to formal banking, skills certification, contract facilitation, and platform-level advocacy.

Infrastructure Reliability as Export Competitiveness: The Invisible Tax

Ask any Pakistani software engineer working on an international client project what their single biggest operational constraint is, and the answer is rarely regulatory. It is the power cut that interrupted a client call. It is the bandwidth throttling that corrupted a code repository push. It is the VPN restriction that prevented access to a cloud development environment. These are not edge cases. They are the daily texture of doing business in Pakistan’s digital economy.

Infrastructure reliability is not a background variable. In digital services exports, it is export competitiveness. A Pakistani IT firm competing against Indian, Ukrainian, or Filipino counterparts is not merely selling talent — it is selling reliable, on-time, high-quality delivery. A single missed deadline caused by a grid outage can cost a client relationship worth hundreds of thousands of dollars. Cumulatively, infrastructure unreliability functions as an invisible tax on Pakistan’s digital exports Pakistan is uniquely ill-positioned to afford.

The electricity crisis is the most acute dimension of this problem. Pakistan’s circular debt overhang — exceeding Rs. 2.4 trillion — continues to produce load-shedding that falls hardest on small businesses and home-based workers, who constitute the backbone of the freelance and micro-enterprise digital economy. Large IT firms in tech parks have access to backup generation; individual freelancers in Multan or Faisalabad do not.

Broadband quality is the second constraint. Pakistan’s average fixed broadband speed, while improving, remains well below regional competitors. Mobile data costs have declined, but network congestion in urban cores during peak hours frequently degrades the quality of experience to levels incompatible with professional digital work. The GSMA has consistently highlighted last-mile connectivity gaps as the primary barrier to realising Pakistan’s mobile internet dividend.

A credible Pakistan digital economy doctrine must treat infrastructure investment — in power stability, fibre optic expansion, and spectrum management — not as a public works programme but as export infrastructure, directly analogous to port expansion for goods trade.

Cyber Risks and the Trust Deficit: The Hidden Vulnerability

Digital economies are only as robust as the trust that underpins them. Trust operates at multiple levels: consumer trust in digital financial services, business trust in cloud infrastructure, investor trust in data governance frameworks, and international partner trust in Pakistan’s regulatory environment. On all of these dimensions, Pakistan faces a significant trust deficit that constrains the Pakistan digital economy growth trajectory.

Cybersecurity incidents affecting Pakistani financial institutions have multiplied. The banking sector has faced card data breaches, phishing campaigns targeting mobile banking users, and SIM-swap fraud at scale. The Pakistan Telecommunication Authority’s (PTA) record of internet shutdowns and platform restrictions — including prolonged access restrictions to major social media platforms during periods of political tension — has created a perception among international digital businesses that Pakistan’s internet governance is unpredictable.

This unpredictability carries a direct economic cost. International clients contracting Pakistani firms for sensitive data processing work — healthcare records, financial data, personal information — conduct due diligence on the regulatory and security environment. A country with a history of arbitrary platform restrictions and limited data protection enforcement does not inspire confidence for high-value data contracts.

Pakistan’s Personal Data Protection Bill, in legislative limbo for several years, represents the most visible symptom of this institutional gap. Without a credible, enforced data protection framework, Pakistan cannot credibly bid for the categories of digital services work — cloud processing, AI training data, health informatics — where the highest margins and fastest growth lie. Closing this gap is not merely a legal formality; it is a prerequisite for moving up the digital value chain.

Institutional Constraints and Policy Incoherence: The Structural Brake

Pakistan’s digital economy governance is fragmented across a proliferation of bodies — the Ministry of IT and Telecom (MoITT), PSEB, PTA, the National Information Technology Board (NITB), provincial ICT authorities, and the Special Investment Facilitation Council (SIFC) — with overlapping mandates, inconsistent coordination, and chronic under-resourcing. This fragmentation is not accidental; it reflects the accumulation of institutional layering that characterises Pakistan’s economic governance more broadly.

The policy incoherence is manifested in contradictions that would be almost comic if they were not so economically costly. Pakistan simultaneously promotes itself as a top destination for IT outsourcing while maintaining VPN restrictions that its own IT workers require to access client systems. It celebrates freelance export earnings while allowing the forex payment infrastructure for those earnings to remain dysfunctional. It announces ambitious digital skills programmes while underfunding the higher education institutions that produce the graduates those programmes are supposed to train.

The Pakistan IT exports 2026 growth trajectory — impressive as it is — is occurring largely in spite of, rather than because of, this governance architecture. The question for policymakers is not whether the current momentum can continue; it can, for a time, on the basis of demographic dividend and individual entrepreneurial energy alone. The question is whether that momentum can be compounded into the kind of structural transformation that moves Pakistan from an exporter of digital labour to an exporter of digital products and platforms.

That transition requires a qualitatively different institutional environment: one capable of regulating without strangling, facilitating without distorting, and investing at the horizon of a decade rather than the cycle of a fiscal year.

Digital Sovereignty and Platform Dependency: The Strategic Dimension

Beneath the growth narrative lies a geopolitical and strategic question that Pakistan’s digital economy debate has been slow to engage: the question of digital sovereignty Pakistan must navigate. As Pakistani businesses and individual workers increasingly integrate into global digital platform ecosystems — Upwork, Fiverr, AWS, Google Cloud, Microsoft Azure — they gain access to markets, infrastructure, and tools that would be impossible to replicate domestically. They also incur structural dependencies that carry long-term risks.

Platform dependency is not a uniquely Pakistani problem. Every country that has embraced the global digital economy faces some version of this tension. But for Pakistan, the risks are heightened by the country’s limited regulatory leverage, its absence from the standard-setting bodies that govern international digital trade, and the concentration of critical digital infrastructure in the hands of a small number of US-headquartered technology corporations.

The practical implications are significant. When a major freelance platform adjusts its fee structure or payment policies, Pakistani freelancers — who have no collective bargaining mechanism, no government-backed alternative platform, and no domestic digital marketplace of comparable scale — absorb the consequences. When a cloud provider raises prices or discontinues a service, Pakistani startups that have built their infrastructure on that provider face switching costs that can be existential.

Digital sovereignty does not mean autarky. It means building sufficient domestic digital capacity — in cloud infrastructure, in payment systems, in data storage, in platform development — to maintain meaningful optionality. It means participating in the governance of the global digital economy rather than passively receiving its terms. It means developing the regulatory expertise to negotiate with platform giants on terms that protect Pakistani economic interests.

This is a long-game strategic agenda, not a short-cycle policy fix. But without it, Pakistan’s Pakistan digital economy growth risks being permanently extractive — generating value that is captured elsewhere.

Government as Digital Market Creator: The Enabling State

One of the most durable insights from the comparative study of digital economy development — South Korea, Estonia, Singapore, Rwanda — is that the private sector alone does not build digital economies. Governments create the conditions: the infrastructure, the standards, the skills pipeline, the procurement signals, and the regulatory certainty without which private investment cannot take root at scale.

Pakistan’s government has the opportunity — and, given the fiscal constraints, the obligation — to be a strategic market creator rather than a passive regulator. Government digitalisation is not merely an efficiency play; it is a demand-side signal to the domestic digital industry. When the government digitises land records, health systems, tax administration, and public procurement, it creates contract opportunities for Pakistani IT firms, validates the commercial viability of digital solutions, and builds the reference clients that domestic companies need to compete internationally.

The PSEB’s facilitation role — connecting international clients with Pakistani IT firms, providing export certification, and advocating for payment infrastructure improvements — represents the embryo of a more active industrial policy. The SIFC’s mandate, if properly operationalised for the digital sector, could provide the high-level coordination that has been missing. But these institutions need resources, autonomy, and political backing to function at the scale the opportunity demands.

The most immediate lever available is public digital procurement: a committed pipeline of government IT contracts awarded to domestic firms under transparent, merit-based processes. This single policy — properly designed and consistently executed — could do more to develop Pakistan’s digital industry than any number of incubator programmes or innovation fund announcements.

From Factor-Driven to Knowledge-Driven Economy Pakistan: The Structural Leap

Pakistan’s economic growth model has, for most of its history, been factor-driven: growth generated by deploying more labour, more land, more capital, in sectors with relatively low productivity — agriculture, low-complexity manufacturing, commodity exports. The digital economy represents the most credible pathway to a fundamentally different model: one in which growth is driven by increasing productivity, accumulating human capital, and generating returns from knowledge rather than from raw inputs.

The knowledge-driven economy Pakistan needs is not a distant aspiration. The ingredients exist, in nascent form: a young population with demonstrated aptitude for digital skills, universities producing engineers and computer scientists at scale, a diaspora with global networks and capital, and a domestic entrepreneurial ecosystem generating startups in fintech, healthtech, agritech, and edtech that are beginning to attract international venture investment.

The transition from factor-driven to knowledge-driven growth is not automatic or inevitable. It requires deliberate investment in research and development, in higher education quality, in intellectual property protection, and in the kind of long-term institutional stability that allows firms to make multi-year investment commitments. Pakistan’s R&D expenditure as a share of GDP remains among the lowest in Asia — a structural constraint that no amount of IT export promotion can overcome if sustained.

The ADB’s research on Pakistan freelancers earnings and digital service exports consistently emphasises that the earnings ceiling for task-based freelance work is far lower than for product-based or IP-based digital exports. Moving Pakistani digital workers up this value curve — from executing tasks to building products, from selling hours to licensing software — is the central challenge of knowledge economy transition.

Policy Priorities for a Digital Doctrine: What Must Be Done

A credible Pakistan digital economy doctrine for the period to 2030 requires six interlocking policy commitments, each necessary but none sufficient in isolation.

First, infrastructure as export policy. Pakistan must treat reliable electricity supply and high-quality broadband as preconditions for digital export competitiveness, not as welfare goods. This means prioritising digital economic zones with guaranteed power supply, accelerating fibre optic backbone expansion into secondary cities, and reducing spectrum costs for business-grade mobile broadband.

Second, the forex plumbing must be fixed. The SBP must complete the liberalisation of digital payment channels, enabling Pakistani freelancers and digital firms to receive, hold, and deploy foreign currency earnings without the friction that currently drives significant volumes into informal channels. Every dollar that flows through informal networks is a dollar that does not build Pakistan’s foreign reserves or generate formal tax revenue.

Third, data protection legislation must be enacted and enforced. The Personal Data Protection Bill must be passed in a form that meets international standards — not as a regulatory box-ticking exercise, but as a genuine market access instrument. Pakistan cannot compete for high-value data services contracts without credible data governance.

Fourth, skills investment must match ambition. Pakistan’s Pakistan IT exports 2026 targets require a quantum expansion of the technical skills pipeline — not through low-quality short courses, but through sustained investment in computer science education at the tertiary level, curriculum modernisation, and industry-academia partnerships that ensure graduates enter the workforce with market-relevant capabilities.

Fifth, institutional consolidation. The fragmented governance architecture for the digital economy must be rationalised. A single, adequately resourced Digital Economy Authority — with a clear mandate, cross-ministerial coordination powers, and direct accountability to the Prime Minister — would reduce the transaction costs of doing business in Pakistan’s digital sector by orders of magnitude.

Sixth, a digital sovereignty strategy. Pakistan needs a national cloud strategy, a digital platform policy, and active participation in international digital trade negotiations. These are not luxury items for a mature digital economy; they are foundational choices that, once deferred, become progressively more expensive to make.

Conclusion: A Decisive Economic Choice

Pakistan’s Pakistan digital economy moment is real, and it is now. The combination of demographic scale, demonstrated digital talent, accelerating connectivity, and record IT and freelance export earnings constitutes a rare convergence of factors that, in other economies, has served as the launching pad for durable structural transformation.

But potential is not destiny. History is littered with countries that glimpsed the digital transformation horizon and then allowed institutional inertia, political short-termism, and infrastructure neglect to ensure they never reached it.

The debate Pakistan is currently having about its digital economy is, at its deepest level, a debate about what kind of economic future the country chooses to construct. The old paradigm — commodity exports, remittances, periodic IMF bailouts, growth that barely keeps pace with population — has delivered recurrent crisis and chronic underinvestment in human capital. The digital paradigm offers something genuinely different: a pathway to prosperity grounded in the one resource Pakistan has in abundance, its people, and their capacity for knowledge work in a globally connected economy.

Digital sovereignty Pakistan must claim is not merely about technology. It is about economic agency — the ability to participate in the global economy on terms that capture value domestically rather than exporting it. Every reform deferred, every institutional bottleneck left unaddressed, every dollar that flows through informal channels rather than the formal banking system, is a cost Pakistan cannot afford.

The choice between a Pakistan whose digital economy remains a promising footnote and one whose Pakistan digital economy growth becomes the defining story of the coming decade is not a technical question. It is a political one. And it must be answered decisively — before the window that demographics, technology, and global market demand have opened begins, once again, to close.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance2 months ago

Markets & Finance2 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 weeks ago

Analysis4 weeks agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Investment2 months ago

Investment2 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Banks2 months ago

Banks2 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Asia2 months ago

Asia2 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Global Economy2 months ago

Global Economy2 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy2 months ago

Global Economy2 months agoWhat the U.S. Attack on Venezuela Could Mean for Oil and Canadian Crude Exports: The Economic Impact

-

Global Economy2 months ago

Global Economy2 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis