Analysis

Greg Abel’s Patient Baton: How Discipline—Not Drama—Will Define Berkshire Hathaway’s Next Century

Greg Abel’s first annual meeting as Berkshire Hathaway CEO delivered a clear signal: patience and disciplined capital allocation will define the post-Buffett era. With a record $397.4 billion cash pile and operating earnings up 18%, here’s what investors need to understand.

The Morning After a Legend Leaves the Stage

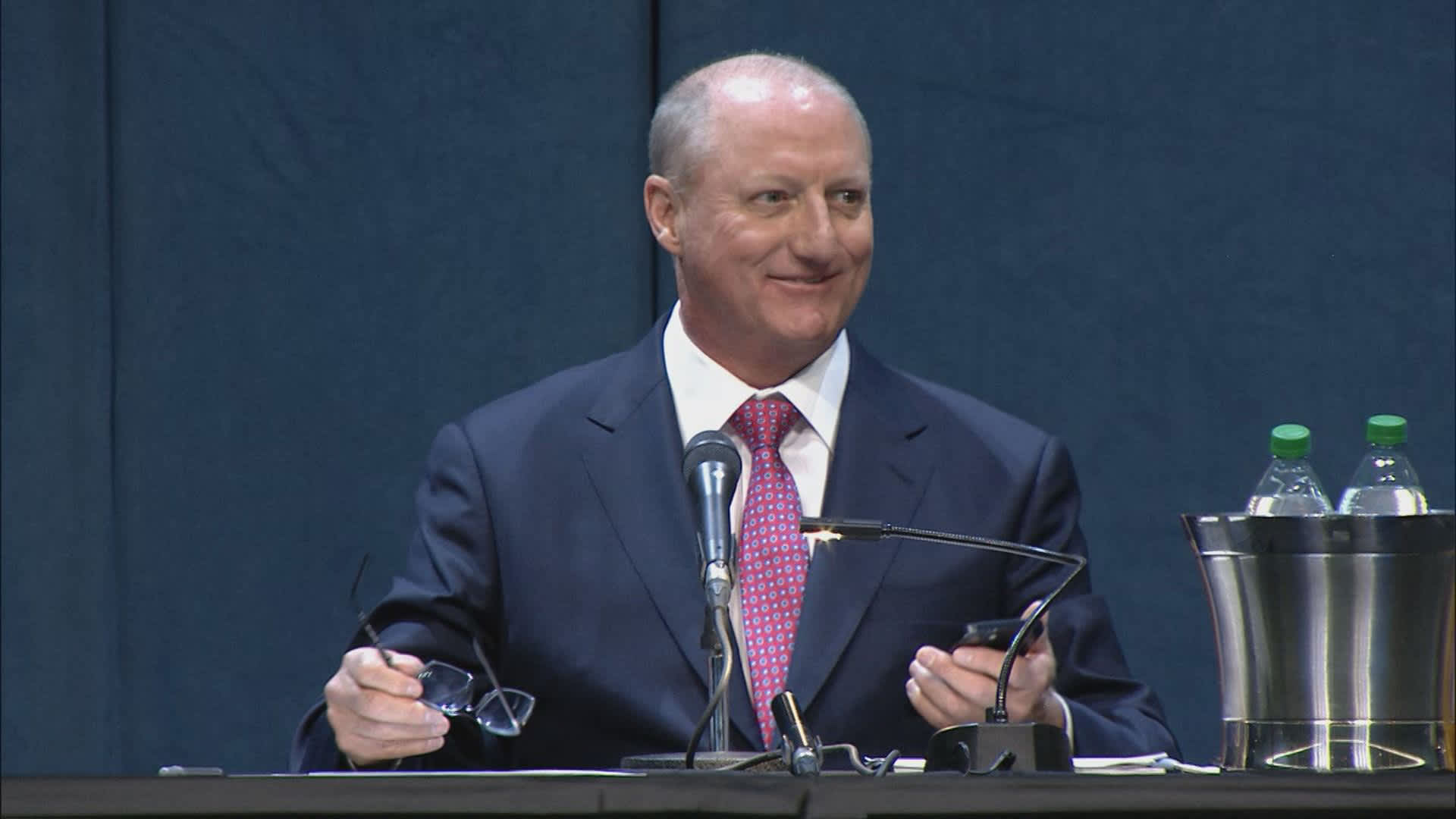

When someone really special steps down, it gets really quiet. On May 2, 2026, at the CHI Health Center in Omaha, Nebraska, the people who own parts of Berkshire Hathaway got together for their yearly meeting. This was the first time in 60 years that Warren Buffett wasn’t in charge of the meeting. The big room was only half full, which was really different from the 40,000 people who used to come every year. And the simple, wise sayings that Warren Buffett used to share with everyone were mostly gone.

It felt like something was missing, like the air in the room wasn’t the same without him. The meeting was still important, but it wasn’t the same without the person who had been leading it for so long. People were probably thinking about how things would change now that Warren Buffett wasn’t in charge. The quiet in the room was like a sign that something big had happened, and everyone was waiting to see what would come next. Instead of flashy announcements, the CEO focused on in-depth business talks, key performance numbers, and a well-structured approach. As the sole leader of the sixth-largest company in the world, he gave his first public presentation and said exactly what long-term investors wanted to hear. He showed that he is a careful and disciplined CEO, which is what the company needed at this time. This approach was a breath of fresh air for investors who are in it for the long haul.

“One of our greatest strengths at Berkshire is patience and being disciplined at allocating our capital. We’re not anxious to deploy capital into subpar opportunities.” — Greg Abel, Berkshire Hathaway CEO, Omaha, May 2, 2026

Greg Abel, 63, the Canadian-born engineer-turned-conglomerate-executive who spent more than 25 years earning Buffett’s trust, stood before shareholders and said something profoundly unfashionable in an era of algorithmic trading, AI hype cycles, and relentless activist pressure: we are not in a hurry.

That restraint is not timidity. It is strategy. And understanding why it may be the most sophisticated capital allocation posture available to a $1 trillion enterprise in today’s market environment is the central task of this analysis.

Abel’s First Letter: Stewardship, Not Showmanship

Before the Omaha meeting, Abel authored his first annual shareholder letter as CEO—a document that financial analysts, value investors, and institutional allocators parsed with the intensity usually reserved for Federal Reserve minutes. The letter’s opening paragraph set the tone with elegant simplicity: “Your capital is commingled with ours, but it does not belong to us. Our role is stewardship.”

That single sentence—eight words distilled from decades of Buffett doctrine—tells you nearly everything about how Abel intends to run Berkshire. He is not positioning himself as a disruptor. He is positioning himself as a custodian.

The letter repeatedly invoked net operating cash flow as the true compass for evaluating Berkshire’s varied businesses, comparing current performance against five-year averages rather than quarterly analyst estimates. Abel committed to assessing value carefully, acting patiently, and holding for the long term—”preferably forever.” He reiterated the fortress balance sheet as a non-negotiable asset, writing that Berkshire’s liquidity ensures the company “can act decisively when opportunities appear and remain resilient during difficult periods.”

This is the language of a man who has read the entire Buffett canon, internalized it, and is now authoring the next chapter in the same idiom—without copying the syntax.

The $397 Billion Question: Patience or Paralysis?

The most provocative number hovering over the 2026 annual meeting was not an earnings figure but a bank balance. Berkshire’s cash, Treasury bills, and short-term securities reached a record $397.4 billion at the end of Q1 2026, up from $373 billion at year-end 2025—itself a record inherited from Buffett’s 13-consecutive-quarter streak as a net seller of equities.

For context, $397 billion is roughly the GDP of Malaysia. It exceeds the market capitalization of most S&P 500 companies. It is not a liquidity buffer. It is a strategic arsenal.

Critics will frame this as elephantine inertia—a conglomerate so large it can no longer find elephants large enough to hunt. That framing mistakes constraint for character. Berkshire is not sitting on cash because it cannot decide what to buy. It is sitting on cash because, as both Abel and Buffett made clear on Saturday, the prices being asked for most assets do not reflect the returns Berkshire requires.

Buffett, now 95 and attending as chairman emeritus, said it plainly in a sideline interview with CNBC’s Becky Quick: “It isn’t our ideal environment in terms of deploying cash for Berkshire,” citing elevated market valuations as the central obstacle. He noted that prices for “an awful lot of things will look awfully silly,” channeling the same sensibility he expressed in his famous 1999 Fortune essay warning against extrapolating a decade of equity returns into the next.

Abel echoed the sentiment from the stage with characteristic operational precision: “It doesn’t mean you need to deploy all your capital and spend all your money.” He acknowledged that Berkshire had identified several firms with interesting management and operations but wasn’t interested in paying current valuations to own them. This is not indecision—it is the Ted Williams strike zone philosophy applied to corporate finance. Wait for your pitch.

The brilliance of that posture becomes clearer when you consider the alternative. A CEO who felt compelled to spend $400 billion to demonstrate decisiveness would almost certainly overpay, diluting decades of compounding in the process. The history of corporate M&A is a graveyard of such urgency.

Operating Results: The Unglamorous Engine Keeps Humming

While the cash pile attracts the headlines, the underlying engine of Berkshire’s operating businesses continues to generate returns that most conglomerates can only envy. Q1 2026 operating earnings came in at $11.35 billion, up nearly 18% year-over-year—a number that reflects the durable cash generation of Berkshire’s 60-plus operating subsidiaries rather than the volatility of mark-to-market investment gains.

Net income attributable to shareholders more than doubled, rising to $10.1 billion from $4.6 billion in Q1 2025, as the value of Berkshire’s equity portfolio—still anchored by Apple, American Express, Coca-Cola, and Moody’s—appreciated sharply.

The insurance segment, long the golden goose of Berkshire’s float-driven model, delivered an underwriting profit of $1.7 billion, up from $1.34 billion in the same period last year. Ajit Jain, the legendary insurance chief who joined Abel onstage in Omaha, reinforced the discipline-over-volume philosophy: insurance premiums are only written when they can be done profitably, on terms that make sense for the long haul. When the market softens and competitors chase volume at inadequate rates, Berkshire pulls back—even if the resulting numbers look temporarily rough.

BNSF railroad and Berkshire Hathaway Energy both showed improved operating results, with Abel spending considerable time on his energy businesses’ pivotal role in the AI infrastructure buildout. His observation that hyperscalers and data centers “have to bear the full cost” of the energy they consume was both a policy statement and a revenue signal: Berkshire’s utility assets are positioned to be among the key beneficiaries of the data center boom, provided the regulatory and cost frameworks are structured fairly.

Continuity vs. Evolution: What Actually Changes Under Abel?

The meeting carried the branding “The Legacy Continues”—a phrase that could read as reassurance or as obligation, depending on your disposition. For investors trying to map Abel’s tenure against Buffett’s, three meaningful differences are worth tracking closely.

Communication style. Buffett translated capitalism into parable. Abel translates it into operations. Where Buffett might invoke Ben Franklin, Abel will cite net operating cash flow and five-year averages. This is not a deficiency—it is a different skill set. Abel spent decades as the hands-on operator of Berkshire Hathaway Energy, running a complex regulated utility empire across multiple jurisdictions. He thinks in infrastructure, not allegory. Shareholders who were drawn to Omaha for Buffett’s wit will need to recalibrate; those drawn for financial substance will find Abel’s style more directly useful.

Collaborative leadership. Abel notably shared the stage with his top lieutenants—a departure from the Buffett-Munger bilateral that defined the meeting’s format for decades. CEOs of Dairy Queen, See’s Candies, Brooks Running, and Jazwares were given time to address shareholders. NetJets CEO Adam Johnson, who now oversees 32 retail and service businesses, was prominently featured. This distributed model signals something important: Abel is building an institutional structure, not a cult of personality. When the latter is inevitable (as it was with Buffett), it is also irreplaceable. When the former is constructed deliberately, it endures.

Technology posture. Buffett famously avoided technology investments for most of his career, then made an extraordinarily well-timed bet on Apple. Abel is carving out a more nuanced stance. He told shareholders that Berkshire “isn’t going to do AI for the sake of AI,” but acknowledged that AI presents both significant opportunities (particularly through the energy infrastructure that powers data centers) and existential risks—including the cybersecurity vulnerabilities illustrated, somewhat surreally, when the first shareholder question of the day arrived via a deepfake of Buffett himself.

The Cultural Moat: Berkshire’s True Durable Advantage

Perhaps the most underappreciated element of Berkshire’s post-Buffett positioning is the cultural architecture that Buffett spent 60 years constructing. Dan Sheridan, CEO of Brooks Running, captured it well from the floor of the exhibit hall: “I think this is a very deeply rooted culture that Warren has created, and I believe the transition to Greg is going to be rooted in those values that Warren has for 60 years instituted and will continue.”

That culture operates on several levels simultaneously. At the subsidiary level, Berkshire’s radical decentralization—CEOs run their businesses with minimal headquarters interference, maximizing accountability and entrepreneurial energy—has survived multiple management transitions at the operating company level without degradation. At the capital allocation level, the aversion to what Abel called the “ABCs”—arrogance, bureaucracy, and complacency—functions as an immune system against the empire-building tendencies that have destroyed shareholder value at comparable conglomerates.

Critically, the float model—insurance premiums invested in equities and bonds before claims are paid—remains structurally intact and irreplaceable. No competitor can simply choose to replicate it. It took Buffett and Jain decades to build GEICO and General Re and the reinsurance operations into the capital generation machines they are today. This is the moat that other moats flow from, and Abel understands it at the granular operational level that the job requires.

The Japan Chapter: Patient Capital’s Finest Recent Chapter

One of Buffett’s most celebrated late-career decisions—accumulating roughly $20 billion in stakes across five major Japanese trading houses (Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo)—remains a template for how Berkshire approaches patient capital deployment at scale. Those positions, initiated quietly in 2019 and revealed on Buffett’s 90th birthday, have since generated substantial gains as the trading companies reported record profits, increased dividends, and bought back shares aggressively.

The Japan investments embody the Berkshire thesis in concentrated form: identify businesses with durable economics trading at irrational discounts, accumulate quietly, hold without the pressure to demonstrate activity, and let compounding do the heavy lifting. Abel has signaled that Berkshire’s relationship with its Japanese partners will continue and deepen. More broadly, the Japan playbook offers a template for how $397 billion in dry powder might eventually be deployed—not in a single transformative acquisition, but in patient accumulation of concentrated positions in undervalued, cash-generative businesses, wherever global dislocations create them.

Key Investor Takeaways

For investors assessing Berkshire in the post-Buffett era, several signals deserve close attention:

- The buyback signal. Berkshire repurchased $234.2 million in stock during Q1 2026—modest but meaningful, its first buyback activity since May 2024. The resumption suggests Abel views current prices as at or below intrinsic value, a useful calibration data point. The average Class A repurchase price of $729,701 and Class B price of ~$486.92 establish implicit floor valuations.

- The valuation discipline signal. Abel explicitly told shareholders that Berkshire has identified companies with excellent management and operations but won’t pay current prices. This is Berkshire’s version of a disciplined capital deployment framework: the opportunity set exists, but the entry prices do not yet justify action.

- The insurance discipline signal. Jain’s comments about pulling back in competitive market conditions—even at the cost of volume—confirm that Berkshire’s insurance profitability is structural, not cyclical. The $1.7 billion underwriting profit in a quarter when peers were facing elevated catastrophe losses is not accidental.

- The AI infrastructure signal. Abel’s emphasis on Berkshire’s energy businesses as essential infrastructure for the data center boom represents the most actionable near-term growth vector for a company of Berkshire’s scale. Unlike direct AI investments, utilities provide regulated, predictable returns with AI-driven tailwinds—precisely the kind of investment profile Berkshire has always preferred.

The Elephant in the Room: Scale as Berkshire’s Primary Challenge

Any honest analysis of Berkshire’s post-Buffett prospects must grapple with the constraint that Abel himself will never quite name directly: size. At roughly $1 trillion in market capitalization and $397 billion in available capital, Berkshire has effectively outgrown the universe of investments that can move the needle. A $10 billion acquisition that would transform a mid-cap company is almost irrelevant to Berkshire’s per-share value. Only acquisitions in the $50 billion–$150 billion range register meaningfully—and at current valuations, such acquisitions are nearly impossible to execute at returns Berkshire would accept.

This is the fundamental tension of the Abel era, and it has no clean resolution. The most likely outcome is a gradual shift toward more international exposure (building on the Japan template), larger bolt-on acquisitions within existing verticals like energy and industrials where Abel has the deepest expertise, and continued share repurchases when prices are attractive.

What the scale constraint definitively rules out is the kind of transformative bet—a General Re in 1998, a Burlington Northern in 2009—that Buffett made at critical junctures to reshape Berkshire’s future. Those opportunities required not just capital but a market dislocation severe enough to offer Berkshire-sized targets at Berkshire-acceptable prices. They are rare, and when they appear, Abel will need to act with the conviction of someone who has never previously managed an investment portfolio at the public company level. That is a legitimate and unresolved question.

Why Patience Remains a Superpower

Buffett, in his sideline CNBC interview, made an observation that cuts to the heart of why Berkshire’s cash patience is a genuine competitive advantage rather than institutional inertia: “We’ve never had more people in a gambling mood than now.”

The evidence is abundant. Retail options volumes at record highs. Meme stocks cycling in and out of speculative manias. Cryptocurrency valuations that defy discounted cash flow analysis. AI-adjacent companies trading at revenue multiples that price in decades of flawless execution. In this environment, a company with $397 billion in dry powder and the institutional culture to resist deployment pressure is not being passive—it is accumulating an option on the next dislocation.

Those dislocations come. They always do. In 2008, Berkshire deployed capital into Goldman Sachs and General Electric at terms available only to lenders of last resort. In 2020, Berkshire was slower to deploy than the historical record would suggest it should have been—a fact Buffett himself acknowledged—but the Japanese trading house accumulation that began in 2019 proved masterful timing in retrospect. The lesson is not that Berkshire is infallible. It is that a company with permanent capital, a fortress balance sheet, and the patience to wait for its pitch will consistently outperform over the full cycle, even if it lags in the middle innings of a bull market.

Berkshire’s Class B shares have underperformed the S&P 500 by 12.4% since Abel was named CEO—a datapoint that bears watching but almost certainly reflects the transition anxiety of a shareholder base recalibrating to a new face rather than any deterioration in the underlying business. For long-term investors, this is exactly the kind of sentiment-driven dislocation that Berkshire’s own investment framework would identify as an opportunity.

Conclusion: The Long Game Is the Only Game Berkshire Plays

Greg Abel is not Warren Buffett. He will never be Warren Buffett. And the sooner investors stop expecting him to be, the sooner they will be able to see what he actually is: a disciplined, operationally sophisticated, culturally literate steward of one of the greatest capital allocation machines ever assembled.

His first shareholder letter established the terms of engagement with clarity and humility. His first annual meeting—delivered without the safety net of Buffett’s presence on stage—demonstrated that he can hold the room, manage the Q&A, honor the legacy, and chart a forward course, all simultaneously. Warren Buffett himself, watching from the audience, told the crowd that Abel is “very, very smart about businesses” and expressed satisfaction with the timing and execution of the transition.

The fundamental premises of Berkshire’s model—permanent capital, decentralized operations, float-funded investing, cultural alignment, and an absolute refusal to deploy capital into subpar opportunities—remain intact under Abel’s stewardship. The $397 billion in cash is not a problem to be solved. It is a testament to sixty years of disciplined refusal to be rushed. In an investment landscape increasingly defined by the tyranny of the quarterly calendar, that refusal is rarer and more valuable than ever.

Patience, as Abel put it in Omaha, is one of Berkshire’s greatest strengths. The market will spend the next several quarters deciding whether to believe him. The long-term record suggests it probably should.

Key Takeaways at a Glance

- Berkshire’s Q1 2026 cash pile hit a record $397.4 billion, up from $373 billion at year-end 2025

- Operating earnings rose 18% year-over-year to $11.35 billion in Q1 2026

- Abel’s core message: patience in capital allocation is a strength, not a failure to act

- Abel explicitly confirmed Berkshire has identified good companies but won’t pay today’s elevated prices

- Insurance underwriting profit of $1.7 billion confirms the structural strength of the float model

- The first share buybacks since May 2024 ($234.2 million) signal Abel’s view on intrinsic value

- The culture of decentralization, anti-bureaucracy, and long-term holding is explicitly preserved

- Energy/utility infrastructure is positioned as Berkshire’s primary near-term AI-era growth vector

- Buffett publicly praised Abel as “very, very smart about businesses”

Frequently Asked Questions

Q: Who is Greg Abel and why is he running Berkshire Hathaway? Greg Abel, 63, is a Canadian-born executive who spent more than 25 years at Berkshire Hathaway, primarily as the head of Berkshire Hathaway Energy. He was publicly identified as Buffett’s successor in 2021 and became CEO on January 1, 2026, after Buffett announced his retirement at the 2025 annual meeting. Buffett remains chairman emeritus.

Q: Why is Berkshire Hathaway not deploying its $397 billion cash pile? Abel has stated clearly that Berkshire will not deploy capital into “subpar opportunities”—meaning companies whose current market prices do not offer the return profile Berkshire requires for long-term compounding. With equity markets trading at historically elevated valuations, the opportunity cost of patience is low while the risk of overpaying is high. Buffett separately noted that the current environment is “not ideal” for deploying Berkshire’s cash.

Q: How did Berkshire perform in Q1 2026 under Greg Abel? Berkshire reported operating earnings of $11.35 billion in Q1 2026, up nearly 18% from the prior year. Net income more than doubled to $10.1 billion. The insurance segment reported a $1.7 billion underwriting profit, up from $1.34 billion. The cash pile grew to a record $397.4 billion from $373 billion at year-end 2025.

Q: Is Greg Abel’s investment style different from Warren Buffett’s? Abel communicates in operational specifics rather than Buffett’s parables, but the underlying investment philosophy—patience, discipline, long holding periods, cultural alignment, refusal to overpay—is explicitly preserved. Abel has also signaled a more systematic approach to leadership, sharing the stage with subsidiary CEOs and building an institutional rather than personality-driven culture.

Q: What is Berkshire Hathaway’s approach to artificial intelligence under Greg Abel? Abel stated that Berkshire will not “do AI for the sake of AI.” The conglomerate’s most direct AI exposure comes through Berkshire Hathaway Energy, whose utility assets power data centers. Abel argued that hyperscalers must bear the full cost of the energy they consume, positioning Berkshire’s utilities as infrastructure beneficiaries of the AI buildout. He also flagged cybersecurity as a significant risk being actively managed, particularly within the insurance businesses.

Q: Should long-term investors hold Berkshire Hathaway stock under Greg Abel? This is a financial decision that depends on individual circumstances, and readers should consult a financial advisor. Analytically, Berkshire’s Class B shares have underperformed the S&P 500 by approximately 12.4% since Abel was named CEO—likely reflecting transition anxiety rather than fundamental deterioration. The underlying business continues to generate record operating earnings and a growing cash reserve, and Abel has demonstrated cultural continuity with the Buffett playbook. Investors with long time horizons who value capital preservation and disciplined compounding have hi

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Thursday, August 6, 2026, is not an ordinary session for SpaceX shareholders. It is the day the company’s first post-IPO lockup period expires, freeing up to roughly 911.5 million insider-held shares — worth close to $123 billion at recent prices — for potential sale on the open market, according to The Motley Fool. To put that in perspective: SpaceX’s entire public float has stood below 280 million shares since its record-breaking June 12 IPO, meaning the unlock could roughly triple the number of tradable shares in a single day.

This is the story competitor outlets are covering as a single-day news event. Few are explaining why the structure of SpaceX’s lockup makes this particular date so unusual — or what it signals about how the company priced risk into its unprecedented listing.

Why this lockup is different from a typical IPO unlock

Most companies use a single 180-day lockup. SpaceX instead built a staggered, performance-linked release schedule tied to its earnings calendar. Insiders became eligible to sell an initial 20% tranche on the second full trading day after the company’s first quarterly earnings report as a public company — which landed on August 4, pushing the unlock date to August 6, per The Motley Fool’s original lockup breakdown.

A bonus 10% tranche would have unlocked early had SPCX traded at least 30% above its $135 IPO price for five of the ten sessions before earnings. That threshold — above $175 — was never reached; the stock has instead spent recent weeks trading near or below its offer price, having fallen more than 40% from the post-IPO high of $225.64 it touched four days after listing, according to StartupHub.ai.

Further pressure is scheduled, not speculative. Additional 7% employee tranches are due around August 21 and September 10, and analysts at 22V Research estimate insiders could collectively be free to sell as much as 44% of total shares by early September — an roughly ninefold increase in the tradable float from where it stood at listing, per Yahoo Finance.

The fundamentals behind the slide

The unlock is landing on a stock that was already under pressure for reasons beyond supply mechanics. SpaceX reported a $4.9 billion net loss for 2025 and lost a further $4.28 billion in the first quarter of 2026, a burn rate that has cooled post-IPO enthusiasm even among investors who back the long-term Starship and Starlink thesis, according to analysis from DayTradingToolkit. Despite posting stronger-than-expected earnings this week, SPCX shares tumbled roughly 14% as the market looked past the results and priced in the incoming supply, based on Bloomberg’s markets desk.

What history suggests happens next

Lockup expirations do not automatically trigger crashes — the actual price impact depends on how much of the newly eligible stock insiders choose to sell, and at what price they’re willing to part with it. Some analysts argue the reaction could be a useful signal in itself: if SPCX absorbs this wave of supply without breaking to fresh lows, that would suggest the market has already priced in the dilution risk, a view echoed by commentary from The Motley Fool’s investing desk. Others counsel patience, arguing the stock’s valuation looks stretched even before accounting for the added float.

For investors weighing an entry point, the practical takeaway is that August 6 is the first of several tests, not the last. The rolling 7% employee releases in late August and September mean supply pressure is likely to recur through the fourth quarter, with the float expected to expand roughly sixfold by late September and to around a third of total shares by Halloween, according to earlier lockup modelling reported by Investing.com.

Key takeaways

- SpaceX’s first lockup expiration frees up to 911.5 million shares (~$123 billion) for potential sale starting August 6, 2026.

- The bonus early-unlock trigger — a 30% share-price premium to the $135 IPO price — was not met, so this is the baseline release, not an accelerated one.

- SPCX has fallen over 40% from its post-IPO peak and briefly traded below its offer price.

- Further 7% tranches are scheduled for late August and mid-September, meaning supply-driven volatility is likely to continue into Q4 2026.

- The stock’s slide reflects both the lockup mechanics and underlying losses of roughly $4.28 billion in Q1 2026 alone.

FAQ

When does SpaceX’s stock lockup expire? The first tranche expired August 6, 2026, two trading days after SpaceX’s first quarterly earnings report as a public company. Additional tranches are scheduled through December 8, 2026.

How many SpaceX shares could be sold? Up to approximately 911.5 million shares — about 20% of eligible insider holdings — became sellable on August 6, against a public float that had been below 280 million shares.

Why did SpaceX stock fall despite strong earnings? Investors appear to be pricing in the incoming supply from the lockup expiration rather than reacting purely to quarterly results, alongside continued losses tied to Starship development costs.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China’s global hunt for billions in unpaid taxes is rewriting the rules for its wealthy citizens.

Just after the Lunar New Year in 2026, a Shenzhen-based family office manager began fielding a new, unwelcome kind of call from his clients. Chinese tax authorities were asking them to settle liabilities on overseas capital gains—some dating back to 2017, others as far as 2000. He had no explanation for the arbitrary five-year window, only the stark reality of a new era: the era of Beijing’s global tax hunt.

Within weeks, the picture became clearer and more alarming for the country’s ultra-wealthy. Banks in mainland China had received instructions to freeze the accounts of wealthy depositors until they could prove taxes on foreign assets, trusts, and investments had been paid. As one banker put it, speaking to the Financial Times under the condition of anonymity: “These wealthy individuals now immediately need to pay penalties and taxes in cash to reactivate their accounts.” The policy response is unambiguous: the People’s Republic has launched a campaign to recover what it believes to be hundreds of billions of dollars in unpaid taxes.

It is, by any measure, a foundational shift in China’s fiscal policy, prompted by a grinding budget deficit and a genuine overhaul of its tax system to align more closely with the United States’ model of global taxation.

The Crunch and the Crackdown

The reason for the campaign’s urgency is a stark one: Beijing is running out of money. The traditional engines of state revenue have seized. Total government land sales, once a core source of funding for local governments, have collapsed from a peak of 8.7 trillion yuan ($1.3 trillion) in 2021 to just 4.15 trillion yuan after the spectacular unwinding of the property market .

This is not a short-term liquidity crisis. It is a structural fiscal realignment. Since the pandemic, overall budget revenue in China has largely stagnated, falling by 1.7% to 21.6 trillion yuan ($3.2 trillion) in 2025 . With the property sector no longer the reliable cash cow it once was, the state has been forced to look elsewhere, and it has set its sights on the billions of dollars in wealth held offshore by its citizens. The State Taxation Administration and the Ministry of Finance confirmed the new measures, formalising a pursuit that was already well underway .

This is the hard data behind the crackdown: a fiscal imperative. It signals that the government is willing to reach decades back into the past—some accounts are being scrutinised as far back as the year 2000—to plug the hole in the present.

The Core Development: A Data-Driven Manhunt

What makes this campaign different from previous sporadic efforts is its technological sophistication and its sheer scope. The hunt is not merely targeted; it is systematic and data-driven.

Chinese authorities are leveraging the full force of modern financial surveillance, utilising data obtained through the OECD’s Common Reporting Standard (CRS), which China has been an active participant in since 2018. As tax lawyer Ye Yongqing of Anli Partners noted, regulators are steadily strengthening the supervision of cross-border capital flows and foreign exchange transactions, narrowing the scope for wealthy Chinese to transfer assets offshore .

Private bankers and wealth managers are already seeing the impact. Singapore-based bankers who manage assets for Chinese families have confirmed that new rules on foreign trusts have “shocked” their clients . Last month, China introduced comprehensive tax rules on assets transferred to foreign trusts, closing a long-standing loophole. Under the new regime, income generated by overseas trusts will be taxed at 20% across multiple stages.

The specific assets under scrutiny are varied, including real estate, stocks, precious metals, and even cryptocurrencies . Financial institutions are being asked to verify whether income from these assets has been declared to Beijing. The retroactive nature of the campaign—in some cases extending more than 25 years—has been confirmed by multiple officials, bankers, and advisors .

Why are banks freezing accounts?

Chinese banks have been instructed to cooperate with tax authorities by freezing the accounts of wealthy depositors until they settle tax liabilities on their overseas assets. This includes gains from foreign stocks, real estate, trusts, and insurance policies. The freeze is only lifted when the individual pays the outstanding tax and penalties in cash, creating powerful leverage for the state to enforce compliance quickly.

An American Model, A Chinese Reality

The structural ambition of this campaign reaches well beyond a one-off tax grab. It represents a deliberate strategy to move China’s tax system closer to the US model.

Just as the US Internal Revenue Service taxes American citizens on their worldwide income regardless of where they reside, China is beginning to adopt a similar territorial approach. This is a significant escalation. For years, wealthy Chinese individuals have used offshore trusts and other complex structures to defer or eliminate tax liabilities on foreign earnings. These structures were often established during the heyday of Hong Kong IPOs, providing a “perfect income tax shield,” according to a Singapore-based banker . The new rules aim to dismantle those shields.

The implications are profound. When the taxman begins to treat offshore gains the same as domestic profits, the calculus of wealth management for high-net-worth individuals changes entirely. As Ye Yongqing noted, this “reduces the scope for wealthy Chinese to transfer their assets abroad or structure their tax affairs through offshore vehicles” .

Victor Shih, a professor of political economy at the University of California, San Diego, summed up the driving force simply: “The motive behind the new campaign is clearly fiscal” . That fiscal necessity is now reshaping the legal architecture of Chinese wealth.

The Second-Order Effects: Compliance and Capital Flight

Downstream consequences of this policy are already rippling through the economy and across borders.

For those in the cross-border trade business, the squeeze is tangible. Zhejiang-based exporter Henry Huang told the South China Morning Post that the heightened scrutiny of unreported overseas income is “taking a real bite out of profits,” forcing him to rethink cross-border operations with little room to pass on costs to price-sensitive US and European customers .

Chinese authorities are also ramping up the legal and psychological pressure. The public security ministry’s “Fox Hunt” campaign, which focuses on extraditing economic fugitives, has already captured over 880 overseas suspects, demonstrating a hardened stance on economic crime .

Yet the most significant risk might be a self-inflicted wound. There is a growing concern that such an aggressive enforcement posture, while potentially lucrative, could accelerate the very capital flight it is designed to reverse. If the wealthy feel they are being pursued relentlessly and facing punitive fines, they may seek to move not just their cash but their entire operations to jurisdictions they perceive as safer.

A Dissenting View: The Cost of Compliance

Of course, the narrative is not without its critics. Some experts warn that the crackdown could have unintended consequences that outweigh the potential revenue gains. The shift in policy, while designed to boost state coffers, might create an exodus of talent and capital.

Furthermore, the operational challenges for tax authorities are immense. While big data and the CRS give them a new level of visibility, they are still largely in the dark about the total quantum of overseas assets. A Bloomberg report from January noted that “even in Beijing’s tightly controlled society, the crackdown is proving spotty,” with local authorities largely unaware of the amount of wealth stashed abroad .

The risk is that a “one-size-fits-all” approach could drive the most mobile taxpayers away. A banker in Singapore managing Chinese wealth observed that many trust owners now face “one-off tax liabilities” and may be forced to sell assets to cover the bills . The campaign may ultimately shrink the tax base it is trying to capture, a classic Laffer Curve dilemma applied to capital.

The “global tax hunt” is, at its heart, a story of transformation. It illustrates a China trying to build a modern welfare state without the traditional safety net of property speculation. The era of the tax-free offshore account for Chinese citizens is ending, not with a whimper but with a series of account freezes and data-driven audits. The policy represents a historic pivot, a move to international norms that at once strengthens Beijing’s fiscal position and challenges the global mobility of its wealthiest citizens. The state’s appetite for its own citizens’ foreign wealth has only just begun, and it is ravenous.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The Federal Reserve’s rate-setting committee held its benchmark borrowing rate steady on July 29, keeping it in a range of 3.5% to 3.75% — but the calm on the surface masked one of the most contested votes of the post-pandemic era. The Federal Open Market Committee split 9 to 3, with three members pushing to raise rates rather than hold, according to NPR’s coverage of the decision.

Chair Kevin Warsh, who took over the Eccles Building earlier this year after a nomination process that rattled bond markets, used his post-meeting press conference to make a point of not making a point. Rather than signal where rates are headed next, Warsh told reporters the Fed would judge market reaction “direct and unfiltered” instead of offering the rolling forecasts investors have come to expect, a stance detailed in CNBC’s meeting recap.

A rate hike was genuinely on the table

What made this meeting unusual wasn’t just the dissent — it was how close markets came to pricing in a hike rather than a cut. Fed funds futures tracked by CME Group put the odds of a rate increase at roughly 35% heading into the decision, up sharply from 26% a week earlier, according to CNBC’s markets analysis. That is a striking reversal from the rate-cutting cycle many investors had expected when Warsh’s nomination was first floated as a “productivity-led growth” pivot away from his predecessor’s caution.

The market reaction told its own story. The S&P 500 slid roughly 0.6% during Warsh’s press conference, the Dow shed more than 840 points intraday, and the 10-year Treasury yield rose to 4.657%, even as the Fed opted for a hold rather than a hike.

Why Warsh is playing it differently

Warsh’s approach reflects both economic and political calculus. Treasury yields have climbed since the Fed’s prior meeting despite the hold, a dynamic Warsh acknowledged directly. And unlike his predecessor, Warsh has been explicit that he intends to set policy independent of the White House’s preferences — even as he awaits a possible additional ally on the Board once a pending internal review concludes, according to CNBC’s analysis of the political backdrop.

Why this matters beyond Washington

A genuinely undecided Fed has knock-on effects well past US borrowers. Higher-for-longer Treasury yields pull global capital toward dollar assets, complicating rate paths in London, Ottawa, and emerging markets alike — a dynamic playing out in parallel with the UK’s own fiscal squeeze (see our companion report on the Autumn Budget) and China’s deflationary drag on global demand. For businesses and investors across the Gulf, Southeast Asia, and South Asia weighing dollar-denominated debt or dollar-pegged currencies, an unpredictable Fed chair is arguably a bigger variable than the rate level itself.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Pakistan Economy 2026: Why GDP Growth Isn’t Reaching Ordinary Households

Strait of Hormuz Deal 2026: Iran-Oman Talks, Oil Price Impact & What Happens Next

SpaceX Stock Lockup Expiration Explained: Why $123B in Shares Could Hit the Market

The Taxman Cometh from Beijing

Pakistan IMF Program 2026: Inside the Push Toward an Interest-Free Economy

Russia Oil Revenue 2026: How Sanctions on Rosneft and Lukoil Are Draining the War Chest

Canada US Trade War 2026: Inside Carney’s Push to Cut Ties With Trump’s Tariffs

Rachel Reeves’s £25 Billion Problem: What the Autumn Budget Gap Means for Britain

Inside the Fed’s Most Divided Vote in Years: Why Warsh Held the Line on Rates

Pakistan Passed Its Third IMF Review

The Fed Is Fractured — And a New Chair Just Made It Louder, Not Quieter

The UK Economy in 2026 Is Neither Recession Nor Recovery :Stagflaton

Indonesia’s $121 Billion Nickel Bet Is Facing a Battery Chemistry

Why Ultra-Wealthy Families Are Splitting Between Singapore and Dubai inmarkets 2026

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gold Price Forecast 2026: Fed’s July 29 Decision and Record Central Bank Buying Explained

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

China Politburo July 2026: Stimulus Signals Explained

Pakistan Economy 2026: GDP Grows 3.7% as IMF Completes EFF Review Amid Middle East Risk

Apple vs OpenAI Lawsuit: The Economic Story Behind the Headline

Down But Not Out: Inside the Slow Sinking of Russia’s War Economy

Gulf Capital Retreat From Pakistan 2026: UAE Loan Freeze & What It Means

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

The Yuan Now Settles 67% of Russian Oil Payments — Quiet De-Dollarization in Action

AI Capex Bubble 2026: The Hidden $662B Debt Nobody Reports

Global Stock Market Selloff 2026: Stagflation Fears Return as Iran Conflict Reignites

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

-

Markets & Finance7 months ago

Markets & Finance7 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis6 months ago

Analysis6 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis6 months ago

Analysis6 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks7 months ago

Banks7 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment7 months ago

Investment7 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025