Mining

EU Readies Crisis Team for Potential China Rare Earths Stand-Off as Supply Chain Risks Mount

BRUSSELS — The European Union is establishing a dedicated crisis task force to prepare for a possible escalation in tensions with China over rare earth exports, reflecting growing concern that renewed restrictions on critical minerals could disrupt Europe’s manufacturing, technology, and defense industries if current trade arrangements expire later this year.

The move highlights Brussels’ increasing focus on economic security as geopolitical tensions reshape global supply chains. Rare earth elements, while produced in relatively small quantities, are indispensable for electric vehicles, wind turbines, semiconductors, military equipment, smartphones, and advanced industrial machinery.

Europe Braces for Supply Disruptions

According to reports, the European Commission is assembling an emergency group comprising senior officials from multiple departments to anticipate and coordinate responses to strategic supply chain shocks.

Officials are particularly concerned that China could tighten export controls on rare earth materials once the existing temporary understanding on exports reaches its expected expiry later this year. The task force would monitor market conditions, identify vulnerabilities, coordinate with member states, and develop contingency plans for industries most exposed to supply disruptions.

The initiative forms part of the European Commission’s broader strategy of strengthening the bloc’s economic resilience amid an increasingly uncertain geopolitical environment, according to reporting by the Financial Times. (Financial Times)

China’s Dominance Gives Beijing Significant Leverage

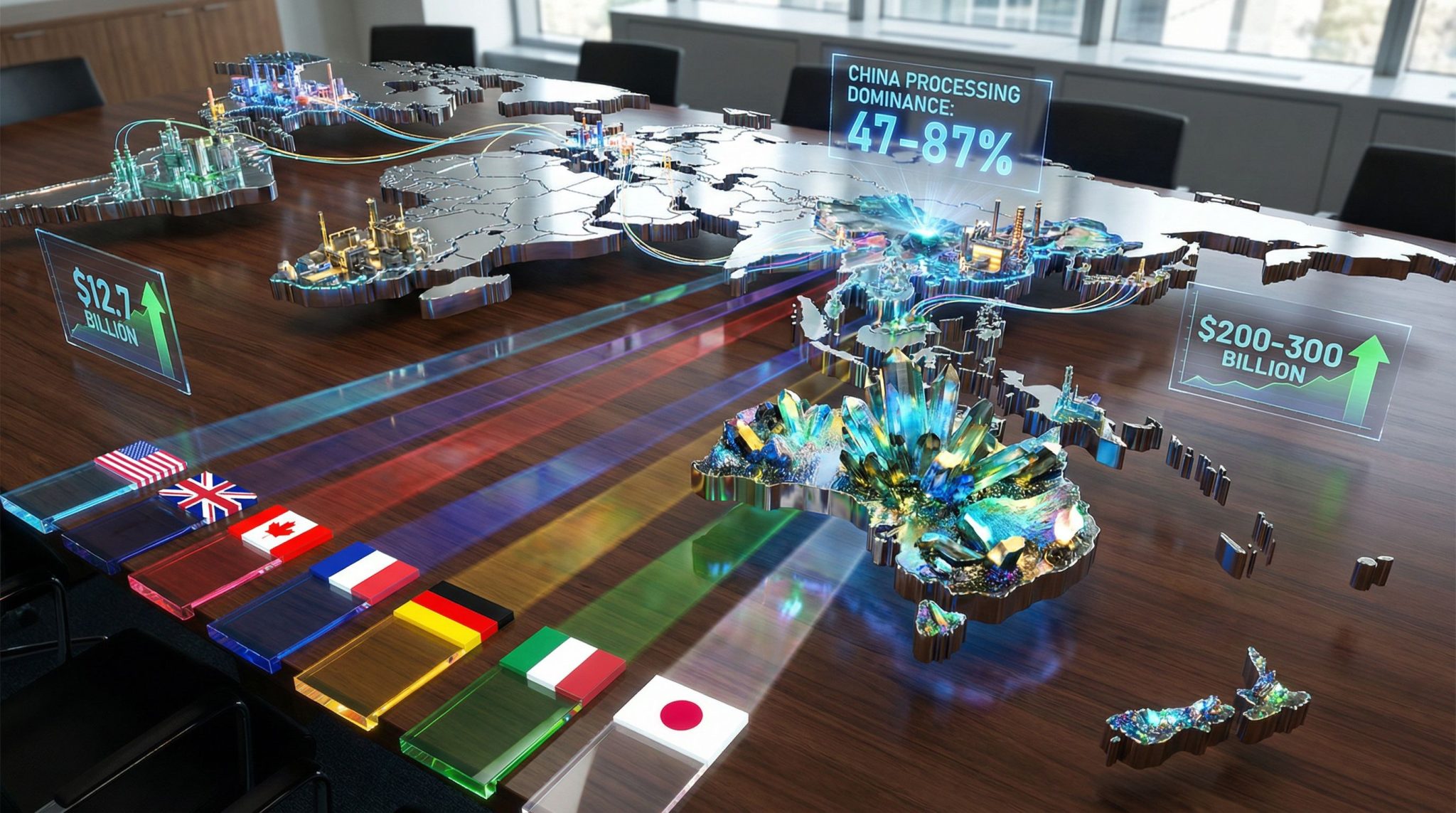

China occupies an exceptionally strong position in the global rare earth industry.

Industry estimates indicate that China accounts for roughly two-thirds of global rare earth mining while controlling nearly 90% of worldwide refining capacity. This means that even minerals extracted elsewhere often depend on Chinese processing before entering global manufacturing supply chains. (Reuters)

That concentration has become an increasingly important geopolitical issue after Beijing introduced export controls on several strategic minerals in recent years, demonstrating its ability to influence global supply chains during periods of heightened trade tensions.

Industries Most at Risk

A prolonged disruption could affect numerous European industries, including:

- Automotive manufacturing

- Electric vehicle production

- Aerospace

- Defense equipment

- Renewable energy technologies

- Consumer electronics

- Semiconductor manufacturing

European manufacturers rely heavily on a stable supply of permanent magnets and other components produced using rare earth elements.

Even temporary shortages could increase production costs, delay manufacturing schedules, and slow investment in Europe’s green energy transition.

Crisis Team Expected to Coordinate Emergency Response

The proposed task force is expected to serve as a rapid-response mechanism rather than a permanent regulatory body.

Among its anticipated responsibilities are:

- Monitoring critical mineral markets.

- Identifying alternative international suppliers.

- Coordinating emergency responses across EU institutions.

- Assessing industrial vulnerabilities.

- Exploring financial support mechanisms for affected sectors.

- Strengthening strategic stockpile planning.

Officials have also discussed the possibility of deploying European funding instruments to help maintain supplies should significant disruptions occur. (Financial Times)

Broader Strategy to Reduce Dependence

The crisis team is only one element of a wider European strategy aimed at reducing excessive dependence on a single supplier for strategically important materials.

European Commission President Ursula von der Leyen has repeatedly argued that Europe must “de-risk” rather than completely decouple from China by diversifying supply chains while maintaining commercial engagement.

Earlier proposals include legislation encouraging companies to diversify suppliers, increased recycling of rare earth magnets, and investment in alternative mining and refining projects both within Europe and among trusted international partners. (Reuters)

Trade Frictions Continue to Build

The rare earth issue comes amid broader economic tensions between Brussels and Beijing.

EU officials have expressed growing concern over persistent trade imbalances, industrial subsidies, market access restrictions, and the increasing use of export controls on strategic materials.

European Trade Commissioner Maroš Šefčovič has warned that without meaningful progress in addressing structural trade concerns, Brussels may pursue additional defensive trade measures.

At the same time, European leaders continue to emphasize dialogue with China, seeking to balance economic cooperation with greater strategic autonomy.

Diversification Will Take Years

While Europe is accelerating efforts to develop alternative supply chains, analysts caution that reducing dependence on China will not happen quickly.

Building new mines, refining facilities, processing plants, and downstream manufacturing capacity requires substantial investment, environmental approvals, and years of development.

Experts argue that diversification rather than complete replacement is the more realistic objective, as China’s established infrastructure and processing expertise remain difficult to replicate in the short term. (Financial Times)

Outlook

The creation of a European crisis task force underscores how critical minerals have become central to global economic and geopolitical competition.

As governments race to secure reliable access to strategic resources, rare earth supply chains are emerging alongside energy security and semiconductor production as key pillars of national economic resilience.

Whether the EU ultimately faces renewed export restrictions or reaches a longer-term understanding with Beijing, policymakers appear determined to ensure that Europe is better prepared for future disruptions than it has been during previous supply chain crises.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

US shipments of yttrium — a rare earth element critical to advanced semiconductor manufacturing — have collapsed roughly 95%, from 333 tons to just 17 tons, in the eight months following Beijing’s April 2025 export controls. China controls approximately 90% of global rare earth processing capacity, and industry executives now warn of potential production halts before the end of 2026 if the bottleneck isn’t resolved.

The Scale of the Chokepoint

China’s dominance isn’t primarily about mining rare earths — it’s about processing them into usable industrial form, a capability the country has spent decades building and that has no scalable near-term substitute elsewhere. Beijing’s October 9, 2025 export control expansion put yttrium, scandium, dysprosium, terbium and other elements under an opaque licensing regime that determines who receives shipments and when (TFTC).

The May 2026 US-China trade truce produced only a vague commitment to “address concerns” about rare earth shortages, with no binding timeline, no removal of specific controls, and no verification mechanism — leaving the underlying bottleneck largely unresolved months later (TFTC).

Why Yttrium and Scandium Specifically Matter

These are not obscure materials to the AI hardware story — they are load-bearing:

- Photonic chips rely on indium phosphide as a substrate material with no currently scalable commercial substitute, and one manufacturer holds roughly 40% of the global market for indium phosphide optical components (Discovery Alert).

- Scandium has become increasingly important in certain deposition processes used in leading-edge semiconductor fabrication, and shortages have already created measurable impacts on chip manufacturing yield (Discovery Alert).

- If a pending “Wave 2” suspension of controls expires without renewal, five additional rare earth elements would return to full restriction simultaneously — a compounding shock for industries that haven’t yet secured alternative sources, leaving manufacturers with a planning horizon of less than six months, according to critical minerals analysis (Discovery Alert).

A Sophisticated Form of Leverage

The October 2025 expansion marked what analysts describe as a qualitative shift: by extending restrictions to cover not just the raw materials but processing equipment, technical documentation, and accumulated operational refining knowledge, Beijing effectively weaponized decades of processing expertise as a strategic asset — targeting capabilities rather than simply commodities (Discovery Alert).

China escalated the response further in June 2026, blocking dual-use exports to ten US companies, including two rare earth producers whose output feeds directly into the US semiconductor and AI hardware production chain (Cryptopolitan). Researchers at the Center for Strategic and International Studies have warned that the pattern risks triggering “an export control and economic statecraft arms race” that could undermine global security and economic prosperity (Cryptopolitan).

The Market Is Already Repricing This

Domestic Chinese markets have responded aggressively: since the start of 2026, rare earth concept stocks on China’s A-share market have surged, with Grinm Advanced Materials up 200% and Oulai New Materials up as much as 350%, reflecting a market-led revaluation of who captures profit across the global semiconductor supply chain (BigGo Finance). The report notes that the combined annual net profit of 177 A-share semiconductor companies has historically been less than one-twentieth of a single US chipmaker’s profits — a gap Beijing’s rare earth leverage is explicitly aimed at closing.

The US Regulatory Backdrop

Washington’s own January 2026 export control rule tightened restrictions on advanced AI chips destined for China, introducing new total processing power thresholds and shifting licensing for chips like Nvidia’s H200 and AMD’s MI325X from presumptive denial to case-by-case review, subject to a 25% tariff, a 50% volume cap relative to domestic shipments, and mandatory US-based third-party testing (Informed Clearly). China’s rare earth controls function as the direct retaliatory counterpart to this regime.

Key Takeaways

- US yttrium shipments from China fell roughly 95% following Beijing’s April 2025 export controls, with prices up about 60% since.

- China controls approximately 90% of global rare earth processing capacity, giving it leverage that goes well beyond raw material supply.

- A pending expiration of “Wave 2” control suspensions could add five more restricted elements simultaneously, with manufacturers facing under six months of planning certainty.

- Chinese domestic rare earth stocks have surged as markets price in a structural shift in global semiconductor supply chain economics.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

The New Resource Geopolitics: How G7 Critical Minerals Strategy Is Forcing ASEAN Into a Careful Balancing Act

As the United States and its G7 partners race to build critical minerals supply chains outside China’s control, ASEAN economies — sitting on some of the world’s largest reserves of nickel, tin and rare earth-adjacent minerals — are increasingly practicing a strategy of deliberate hedging: courting Western investment in processing and manufacturing capacity while avoiding formal alignment against China, their largest trading partner and dominant regional investor.

Why This Has Become Urgent

China’s near-total dominance of global rare earth processing — controlling roughly 90% of capacity, according to industry analysis — has turned critical minerals into one of the sharpest instruments of economic statecraft in the current cycle (see our companion coverage). Beijing’s escalating export controls on yttrium, scandium and other elements essential to AI chip manufacturing have made clear to Washington and its allies that dependence on a single-country supply chain for these inputs is a structural vulnerability, not a temporary inconvenience.

Researchers at the Center for Strategic and International Studies have warned explicitly that the pattern of escalating export controls between the US and China risks triggering “an export control and economic statecraft arms race that could severely undermine global security and economic prosperity” (Cryptopolitan).

Where ASEAN Fits

Southeast Asia holds a genuinely pivotal position in this contest, but its individual economies are responding in structurally different ways:

- Indonesia has leaned into resource nationalism, banning raw nickel ore exports to force domestic processing investment — a strategy that has driven record foreign investment but risks entrenching a narrow, commodity-dependent industrial base if it fails to move into higher-value battery manufacturing (see our companion coverage).

- Malaysia has instead captured the manufacturing layer of the battery and electronics supply chain, positioning itself as ASEAN’s leading battery exporter while AMRO credits “robust electronics exports and AI-related investment” for cushioning growth against broader “geoeconomic fracturing” (see our companion coverage).

- Singapore continues to function as the region’s financial and logistics anchor, benefiting from rerouted shipping traffic during the Hormuz conflict while its manufacturing sector rides the same AI-driven semiconductor supercycle reshaping demand for the critical minerals underlying chip production (see our companion coverage).

The Regional Coordination Angle

Rather than each country negotiating individually with Washington or Beijing, ASEAN members have been building horizontal coordination mechanisms. Indonesia and the Philippines have proposed a nickel supply chain corridor explicitly framed around regional integration, with the Philippine Chamber of Commerce and Industry’s president describing the goal as ensuring “ASEAN is strongest when it acts as one unit” (Tribune.net.ph). Separately, Malaysia’s Selangor state has deepened bilateral cooperation with Indonesia’s West Java Province across manufacturing, infrastructure and Islamic finance, reflecting a broader pattern of intra-ASEAN economic deepening running in parallel with — rather than as a substitute for — engagement with both Washington and Beijing (ACN Newswire via Barchart).

Why Neither Superpower Can Simply Bypass ASEAN

For Washington, ASEAN’s mineral reserves and manufacturing capacity represent one of the few credible near-term paths to diversifying critical minerals and electronics supply chains away from China — a strategic priority underscored by the UAE’s own recent upgrade in US technology export access (see our companion coverage), part of a broader pattern of Washington deepening ties with trusted partners outside China’s orbit. For Beijing, ASEAN remains both an enormous export market and, increasingly, a manufacturing base for goods designed to route around US tariffs and export restrictions — making continued economic engagement equally indispensable.

This dual dependency is precisely what gives ASEAN economies room to hedge rather than choose. It also means the region’s trade and investment data over the next several years will likely be read closely by policymakers in Washington, Beijing, Brussels and Tokyo as a real-time indicator of how the broader US-China economic rivalry is actually being resolved on the ground, rather than in policy statements.

Key Takeaways

- China’s dominance of rare earth processing has made critical minerals a central front in US-China economic rivalry, with ASEAN’s mineral reserves newly strategically significant.

- Indonesia, Malaysia and Singapore are pursuing distinct national strategies — resource nationalism, manufacturing capture, and financial/logistics hubbing, respectively — rather than a unified regional approach.

- ASEAN nations are building horizontal coordination mechanisms, like the proposed Indonesia-Philippines nickel corridor, to strengthen collective bargaining power.

- Both the US and China have deep enough economic stakes in ASEAN that the region can credibly hedge between them rather than being forced to align with either bloc.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China posted a record export month in June 2026. Nearly every outlet covering it led with the same number — $412 billion, up 27% — and largely missed the quieter, more consequential story running in the opposite direction: a 34% monthly drop in rare earth exports.

The headline number

China exported a record $412 billion worth of goods in June 2026, blowing past all forecasts as the global AI investment supercycle turbocharged demand for chips and computing equipment, according to Bloomberg. Exports climbed 27% year-on-year — the fastest pace in four months — while imports jumped 36%, a five-year high that easily beat the 24% growth economists had forecast, according to Daily Sabah. China’s monthly car exports topped 1 million for the first time in June, and the country sold 32 billion integrated circuits to the world, per Reuters, via Investing.com.

The trade surplus hit $125.6 billion in June, keeping China on track for a second consecutive year with a surplus topping $1 trillion, per the same Reuters report.

The number almost nobody led with

Buried well below the headline in most coverage: the volume of China’s rare earth exports fell 34% in June and is down 6.4% year-to-date, as Beijing tightened restrictions on the critical elements, according to Daily Sabah. China accounts for around two-thirds of global rare earths production — materials used in everything from smartphones to missiles — and has “wielded its dominance” as leverage in trade negotiations, per the same report.

This is arguably the more important story of the two, and it’s being systematically underreported relative to the AI-export headline. A record trade month built substantially on AI-chip demand is happening at the exact same time Beijing is deliberately constraining exports of the minerals that chip and defense manufacturing depend on. That combination — surging exports of finished high-tech goods, alongside tightening control of upstream raw material exports — is a much more strategically significant signal than the aggregate trade number suggests, because it points to China consolidating leverage at both ends of the AI and defense supply chain simultaneously.

The domestic demand problem the export boom is masking

Julian Evans-Pritchard, head of China economics at Capital Economics, cautioned that the strong import figure “should not be taken as evidence that domestic demand is booming,” per Reuters. Xu Tianchen, senior economist at the Economist Intelligence Unit in Beijing, echoed this: “domestic demand remains a drag. Retail sales remain pretty flat and fixed asset investment was negative last month.”

China’s oil imports hit their lowest level since October 2016, and China appears to be drawing down existing energy stockpiles rather than paying up amid regional disruption — while coal imports jumped 29% annually in June, suggesting a shift back toward coal to fill the gap, per Reuters. In effect, China’s headline growth engine right now is almost entirely external (AI-linked exports), while the domestic economy — consumption, retail, fixed investment — continues to lag.

The trade friction this is generating

China’s trade surplus with the European Union alone hit $32.9 billion in June, up from $30.7 billion in May, according to Daily Sabah, a gap Zhang Zhiwei of Pinpoint Asset Management said “puts further pressure on the trade tension between China and its trading partners, Europe in particular.” Ties with Washington have stabilized somewhat since President Trump’s May visit to Beijing, but the persistent imbalance remains a friction point.

What this means for global businesses

For manufacturers and investors dependent on China’s supply chain — including Pakistani textile and electronics importers — the signal to watch isn’t the trade surplus headline. It’s whether Beijing’s rare earths tightening becomes a broader tool for leverage as AI-chip demand keeps China’s export engine running hot despite domestic softness. A country simultaneously dominating AI-linked exports and constraining upstream critical mineral supply has more geopolitical leverage than the trade balance alone conveys.

FAQ

How much did China’s exports grow in June 2026? Exports rose 27% year-on-year to a record $412 billion, driven largely by AI-related chip and computing equipment demand.

Why did China’s rare earth exports fall even as overall exports hit a record? Beijing tightened restrictions on rare earth exports, which fell 34% month-on-month in June, as China leverages its roughly two-thirds share of global production.

Is China’s domestic economy also growing at a record pace? No — economists including Capital Economics’ Julian Evans-Pritchard note that retail sales remain flat and fixed asset investment was negative in the most recent month, even as export-driven trade data surged.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Anthropic Offers Up to $600,000 Salary for Critical IPO Role as AI Giant Prepares for Wall Street Debut

EU Readies Crisis Team for Potential China Rare Earths Stand-Off as Supply Chain Risks Mount

Singapore Weighs Hedge Fund Tax Cuts to Counter Hong Kong’s Growing Financial Challenge

Facebook and Instagram Experience Global Outage

Inside the $1 Billion Tap-to-Pay Fraud Rings Targeting Banks and Retailers

Anthropic’s Trillion-Dollar Race: Inside the Path to an October 2026 IPO

Southeast Asia’s Two-Speed Economy: AI Chips Boom While a Quieter Halal Corridor Expands

Pakistan’s Fiscal Tightrope: How the Hormuz Oil Shock Is Colliding With IMF Ceilings

Why Fed Independence Is Hanging by a Thread

Strait of Hormuz Bypass: Inside the $14M-BPD Pipeline Race Reshaping Global Oil

Markets May Have Just Had Their Second “DeepSeek Shock”

China’s Rare Earth Squeeze Is Quietly Throttling the AI Chip Boom

Malaysia’s Quiet Semiconductor Boom: How AI Demand Is Cushioning a Country Caught Between Superpowers

Singapore’s Growth Beat Hides a Harder Question: Can MAS Keep Tightening Into a War-Driven Inflation Shock?

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

AI Bubble Warning 2026: Why BIS, IMF and Bank of England Fear a Market Crash

Male Labor Force Participation Rate 2026: Why Men Are Leaving & Economic Impact

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Strait of Hormuz Blockade 2026: Oil Prices Surge 9% as US-Iran Conflict Reignites

IMF Cuts Pakistan Growth Forecast, Raises Inflation to 8.4%

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Private Credit Warning: Most BDCs Turn Unprofitable in 2026, Reuters Finds

India Economic Rise 2026: How the Subcontinent Toppled Japan

Strait of Hormuz 2026: Why Markets Still Don’t Trust It’s Open

Bitcoin $150k Milestone Achieved as US Sovereign Crypto Pivot Looms

The AI Super Bubble Is Ready to Burst

Chipmakers Just Lost 6.7% in Two Days: Inside the Great AI Trade Rotation

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy7 months ago

Global Economy7 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy7 months ago

Global Economy7 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025