Property

China’s Export Miracle Masks a Property Disaster: Growing Without Its People

China’s exports surged 19.6% in May 2026, with semiconductor shipments up 110% year over year. But behind the headline growth lies a collapsing property market, falling consumer spending, and a looming Japan-style deflationary trap. Here is the full analysis.

The Paradox at the Heart of China’s Economy

China in 2026 presents one of the most striking paradoxes in modern economic history. On the surface, the data looks impressive: exports were up 19.6% from a year earlier in May 2026 — the second biggest increase since January 2022. Exports of semiconductors soared 110% year over year, while mobile phones rose 44% and automatic data-processing machines jumped 66%. The manufacturing engine is roaring.

Beneath the surface, a different China is visible — one where property values are collapsing, households are saving rather than spending, youth unemployment remains elevated at 16.9%, and consumer price inflation has been near zero for years. China’s GDP stands at $20.8 trillion in 2026, but deflation has persisted for a tenth consecutive quarter and property investment has collapsed 50–80% from peak.

The paradox resolves when you understand the structure: China is growing because of exports and government investment, not because its people are getting richer and spending more. That is an inherently fragile foundation.

The Export Surge: AI Demand Driving China’s Manufacturing Machine

The headline numbers on China’s export performance are extraordinary. Semiconductor exports rising 110% year over year reflect two intersecting forces: booming global AI infrastructure demand sucking in chips and electronics components, and Chinese manufacturers stockpiling inventories ahead of anticipated further disruptions to global supply chains from the Iran conflict.

China holds a dominant position in many semiconductor supply chain stages below the most advanced chips — packaging, substrates, legacy node chips — and these have been in extreme demand from AI data center builders worldwide. The AI economy is, perhaps inadvertently, providing a significant lifeline to China’s export sector at precisely the moment when domestic demand remains depressed.

The Property Collapse: A Crisis Now in Its Fifth Year

While the export engine hums, China’s property sector — for decades the central pillar of household wealth and economic growth — continues its multi-year implosion. Property investment fell 16.2% year over year in the first five months of 2026 — the steepest decline in fixed-asset investment since May 2020.

Secondary home prices have declined for 44 consecutive months, and rents have fallen for 23 months. For a country where residential property constitutes approximately 70% of urban household assets, this sustained decline has had a devastating effect on consumer psychology. Falling housing prices have made people feel poorer. As a result, people choose to spend less and save more. In the past five years, household deposits in Chinese banks have almost doubled.

The property downturn is estimated to have reduced annual real GDP growth by about 2 percentage points per annum in 2024 and 2025, according to Goldman Sachs. Though this drag is expected to narrow, it has fundamentally altered the trajectory of the world’s second-largest economy.

The Japan Comparison: Is China Walking Into a Deflationary Trap?

The comparison that haunts Chinese policymakers — and that has been referenced repeatedly by leading economists including Harvard’s Kenneth Rogoff — is Japan’s “Lost Decade” that followed the burst of its property and equity bubble in 1990.

China’s policymakers are acutely aware of this risk. The PBOC has announced a series of financial sector measures including steps to increase the use of overnight reverse repo operations and support the offshore use of the renminbi. But these measures did not appear to represent a major broad-based monetary stimulus package — suggesting Beijing is still reluctant to unleash the scale of fiscal intervention that might break the deflationary psychology.

The Global Implications

China’s export surge, paradoxically, creates pressure for its trading partners. A country growing primarily through exports necessarily runs trade surpluses — which creates political friction with trade partners, particularly the United States and the European Union, who already face domestic pressure on trade deficits with China.

Meanwhile, China’s weak domestic demand is deflationary for the global goods sector — exporting low prices to the world at a time when services inflation remains stubbornly elevated in most developed economies. This creates a complex environment for central banks: cheap goods from China pushing inflation down, expensive services keeping it up.

For investors, China in 2026 presents an asymmetric opportunity clouded by structural uncertainty. The export machine is delivering, but the domestic recovery remains elusive.

FREQUENTLY ASKED QUESTIONS (FAQs)

Q: Why are China’s semiconductor exports up 110%? AI infrastructure buildout worldwide is driving massive demand for chips and electronic components. China holds significant market share in many semiconductor supply chain stages, and AI data center builders are a major buyer of these products. Additionally, anticipation of further supply chain disruptions is driving inventory stockpiling.

Q: Is China’s economy in a recession? No — GDP growth remains positive, projected around 4–5% in 2026. However, deflation has persisted for over two years, property investment is collapsing, and consumer spending growth is far below historical norms. Economists describe it as “growth without demand.”

Q: How severe is China’s property crisis? Property investment in the first five months of 2026 fell 16.2% year over year, the steepest decline since May 2020. Secondary home prices have fallen for 44 consecutive months. The property sector, which at its peak accounted for nearly 30% of China’s GDP including related industries, has shrunk dramatically.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

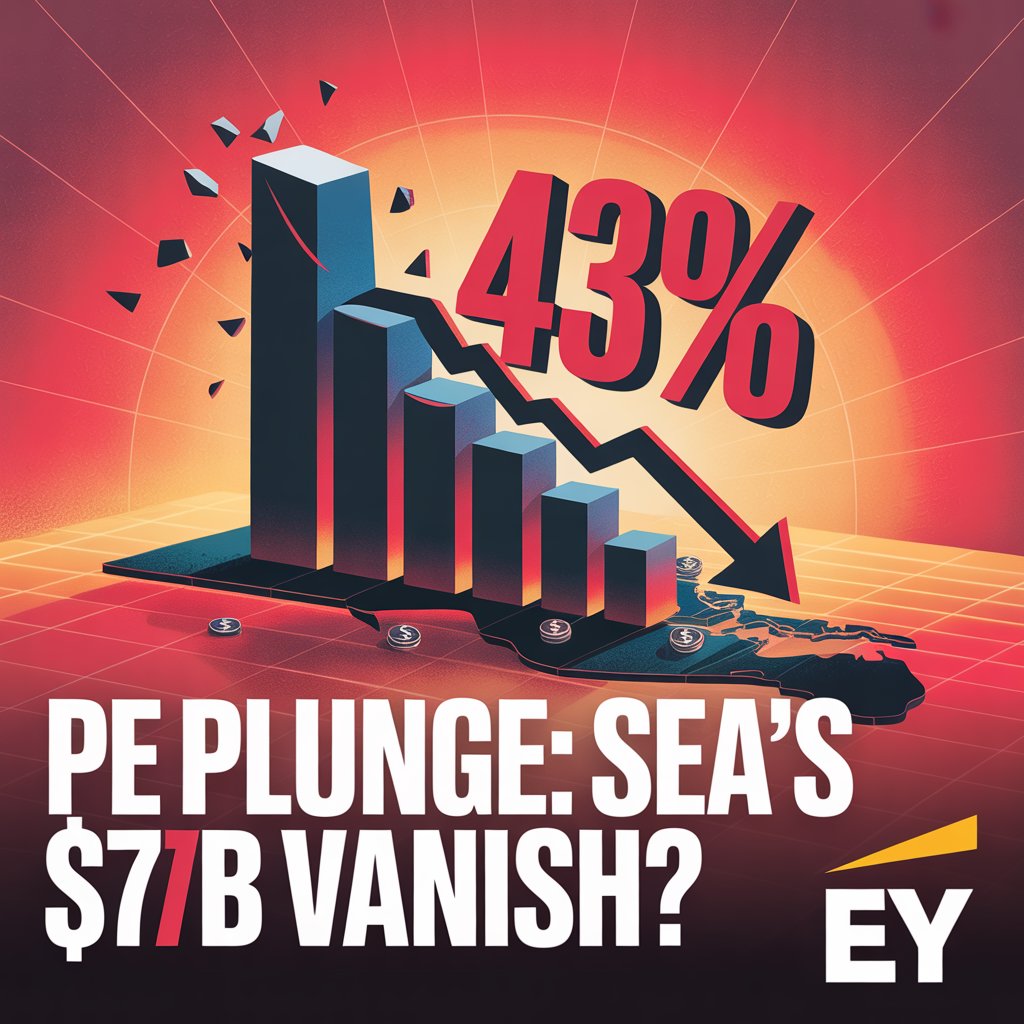

Southeast Asia Private Equity Confronts 43% Value Decline in 2025: A Turning Point in Regional Capital Markets

The champagne that flowed freely through Singapore’s financial district just a year ago has given way to something more sobering: a recognition that Southeast Asia’s private equity landscape is undergoing its most significant recalibration in a decade. According to EY’s Southeast Asia Private Equity Pulse 2025 year-end report, deal value across the region plummeted 43% year-on-year to US$9.1 billion, spread across 59 transactions—a stark retreat from the US$16 billion deployed across 67 deals in 2024.

This isn’t merely a statistical blip. It represents a fundamental shift in how institutional capital views one of the world’s most dynamic emerging markets, driven by an confluence of geopolitical uncertainty, valuation discipline, and a sobering reassessment of exit pathways that has rippled from Hong Kong boardrooms to Jakarta trading floors.

The Anatomy of a Downturn: Megadeals Disappear, Average Sizes Contract

The most telling indicator lies not in the headline number, but in the composition of deals. Southeast Asia witnessed just four megadeals exceeding US$1 billion in 2025, half the eight recorded in 2024. Consequently, the average deal size contracted to US$267 million from US$356 million—a 25% decline that signals investors’ preference for calculated bets over transformational plays.

Luke Pais, EY-Parthenon Asia-Pacific Private Equity Leader, captured the prevailing sentiment succinctly: “Amid geopolitical and macroeconomic uncertainties, deal activity and exits are expected to slow over the next few quarters.” This caution reflects broader Asia-Pacific trends, where Bain & Company’s 2025 regional analysis indicates that while deal value across the wider region increased modestly, Southeast Asia’s trajectory diverged sharply from India’s double-digit growth and Japan’s steady buyout pipeline.

The narrative becomes more nuanced when examining quarterly fluctuations. Q1 2025 opened with unexpected strength—deal value surging 5.5 times year-on-year to US$2 billion across 14 transactions, primarily driven by two large-ticket investments contributing 77% of total value. Yet this momentum proved fleeting. Q2 witnessed deal value plummet to US$1 billion across 22 deals as megadeals evaporated, while Q3 recovered to US$2.5 billion—again propelled by outsized transactions rather than broad-based activity.

Singapore’s Dominance and Sectoral Realignment

Geography tells its own story. Singapore commandeered approximately 74% of regional deal value in 2025, cementing its position as Southeast Asia’s undisputed private equity hub. This concentration reflects not just the city-state’s regulatory sophistication and connectivity, but also the infrastructure and digital transformation investments that have become magnets for institutional capital.

Sector dynamics reveal where conviction remains strongest. Infrastructure and energy transactions accounted for 53% of investments, as general partners gravitated toward policy-supported, scalable platforms—particularly data centers and telecommunications towers responding to the region’s insatiable digital appetite. According to Deloitte’s Asia Pacific Private Equity 2025 Almanac, consumer goods, technology, media, and telecommunications (TMT), and healthcare remained key drivers, though valuation compression forced investors to recalibrate their underwriting assumptions.

Real estate, once a darling of regional allocators, captured just 11% of deal value—a precipitous fall reflecting both valuation concerns and persistent questions about commercial property fundamentals in a hybrid work environment. Meanwhile, ESG-linked themes continued their ascent, with renewable energy and sustainability-focused platforms attracting capital from investors increasingly mindful of regulatory tailwinds and consumer preference shifts.

The Exit Conundrum: A Market Searching for Liquidity

Perhaps most concerning for limited partners awaiting distributions is the exit landscape. PE-backed exits totaled just US$4.4 billion across 33 deals in 2025, down 47% from the previous year. This liquidity drought mirrors a global phenomenon—KPMG’s Q4 2025 Pulse of Private Equity notes the Asia-Pacific region suffered from a continued mismatch between capital flowing into private markets and money returning to investors, exacerbated by the region’s underdeveloped secondary market infrastructure.

IPO windows remained stubbornly shut across most Southeast Asian exchanges in 2025. Secondary transactions gained traction as sponsors sought alternative monetization routes, with Navis Capital among the firms pivoting toward secondaries driven by rising liquidity requirements. Yet these represented tactical responses rather than systemic solutions, leaving aging portfolios—some dating to 2018-2019 vintages—stuck in limbo.

The median Distribution to Paid-In (DPI) capital for recent fund vintages has declined markedly compared to earlier cohorts, creating what Herbert Smith Freehills Kramer’s fourth-quarter analysis characterizes as “a growing pool of privately held assets accumulating over several vintages.” This dynamic has intensified LP pressure on general partners to demonstrate exit readiness, fundamentally reshaping how deals are underwritten from inception.

Geopolitical Headwinds and the Tariff Shadow

No discussion of Southeast Asia’s private equity market in 2025 is complete without acknowledging the geopolitical elephant in the room. The Trump administration’s “Liberation Day” tariffs, implemented in early 2025, sent shockwaves through export-oriented economies, though exemptions on key categories like semiconductors, electronics, and pharmaceuticals mitigated the worst-case scenarios.

Yet uncertainty itself became a transaction cost. As PineBridge Investments’ 2026 Asia Equity Outlook observes, Liberation Day tariffs unexpectedly singled out certain economies with elevated effective rates, though the impact on Southeast Asia was comparatively muted given beneficiary status under the “China+1” supply chain diversification strategy. Still, the potential for policy volatility—particularly around US-China relations—kept many institutional allocators on the sidelines.

The one-year trade truce between Washington and Beijing announced in late 2025 has injected cautious optimism into 2026 planning, but investors remain acutely aware that structural tensions persist. This has accelerated a pivot toward domestic consumption-oriented assets—healthcare facilities, financial services, education infrastructure—insulated from export dynamics.

The 2026 Inflection Point: Value Creation Trumps Multiple Expansion

Looking forward, industry leaders anticipate a market characterized by operational rigor rather than financial engineering. With interest rates having normalized across most Southeast Asian central banks following aggressive monetary easing in 2025, the easy returns generated by multiple expansion during the zero-rate era have evaporated. According to Partners Group’s Private Markets Outlook 2026, the emphasis has shifted decisively toward control investments that allow sponsors to actively steer companies through uncertainty, complemented by thematic exposure to structural trends like demographic shifts and digital adoption.

Mid-market deals are expected to dominate 2026 activity. The US$100-500 million sweet spot offers sufficient scale for operational transformation while avoiding the valuation friction and competitive intensity that plague billion-dollar auctions. Sector focus will likely crystallize around digital infrastructure (data centers, fiber networks, towers), healthcare (hospitals, diagnostic chains, specialized clinics), and financial inclusion platforms capitalizing on Southeast Asia’s underbanked population.

Fundraising dynamics also merit attention. While 2025 saw only one Southeast Asia-focused fund close during Q3 (raising US$500 million), several vehicles with regional exposure reported interim closures by August. The power balance in fundraising is shifting from Western institutional LPs toward Asian private wealth and family offices, particularly in Singapore, Hong Kong, and Dubai, where advisers report clients lifting PE allocations from low single-digits into the 10-15% range.

Strategic Imperatives for an Uncertain Decade

The private equity firms that will thrive in Southeast Asia’s next chapter are already adapting their playbooks. Portfolio company support has intensified, with general partners helping evaluate tariff exposure, manufacturing footprints, and currency hedges. Due diligence has become more rigorous, with stress-testing across multiple macroeconomic scenarios standard practice.

Notably, multinationals are increasingly partnering with private equity to accelerate growth in regional operations—the recent Starbucks and Burger King joint ventures signal a template that could proliferate in 2026. These hybrid structures offer brands local expertise and patient capital while providing sponsors access to established platforms with proven unit economics.

The bifurcation between top-quartile and median performers is widening. As Bain & Company’s research indicates, investors continue migrating toward quality funds with demonstrated performance, pushing average fund sizes to US$174 million—up 28% year-on-year and 17% above the five-year average. This flight to quality will likely intensify as aging portfolios force some sponsors to crystallize losses or accept suboptimal exit multiples.

The Verdict: Resetting, Not Retreating

Southeast Asia’s 43% private equity value decline in 2025 represents recalibration, not capitulation. The region’s underlying fundamentals—4.7% GDP growth, rising consumption, digital adoption, and supply chain realignment—remain compelling. What’s changed is the market’s appreciation for complexity.

The era of indiscriminate capital deployment fueled by cheap leverage and multiple expansion has ended. What emerges is a more surgical approach: smaller checks, operational focus, domestic orientation, and exit planning embedded from day one. For investors with conviction and operational capabilities, this reset creates opportunities to acquire quality assets at rational valuations—precisely the conditions from which the next vintage of superior returns will emerge.

As February 2026 unfolds, the question isn’t whether Southeast Asia’s private equity market will recover, but rather what shape that recovery will take. Early indicators—stabilizing geopolitical tensions, monetary easing reaching terminal rates, a pipeline of interim fund closures—suggest the building blocks are assembling. Whether 2026 delivers on this cautious optimism will depend on factors both local and global, measurable and unpredictable—the very essence of emerging market investing.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Tokyo’s Soaring Property Prices: Supply Constraints as a Double-Edged Sword Under PM Sanae Takaichi’s Watch

A landslide electoral victory has empowered Japan’s first female Prime Minister to reshape immigration and housing policy—but her agenda may deepen the affordability crisis gripping Asia’s megacities

Two days after Japan’s historic February 8 election, Tokyo’s real estate brokers are fielding anxious calls from foreign buyers wondering if their property dreams are about to evaporate. Prime Minister Sanae Takaichi’s landslide victory—securing 316 of 465 seats in the Diet, the largest mandate since World War II—has crystallized a political pivot with profound implications for one of Asia’s most overheated housing markets. Her campaign promises of stricter immigration controls and tougher requirements for foreign property owners are colliding with an uncomfortable economic reality: Tokyo’s property prices averaged ¥91.8 million ($597,810) in 2025, a 17% surge that reflects not foreign speculation, but a structural crisis decades in the making.

The newly empowered Prime Minister faces a dilemma that echoes across Asia’s booming capitals, from Seoul to Sydney. Housing affordability has become a political lightning rod, and the instinct to blame foreign buyers is politically expedient. Yet the data tells a different story—one where supply constraints, demographic shifts, and domestic demand dynamics are the true architects of this affordability catastrophe.

The Anatomy of Tokyo’s Price Explosion

Walk through Tokyo’s Minato ward on a Tuesday morning and the construction cranes tell only half the story. Despite the skyline’s perpetual evolution, Tokyo’s new condominium supply in 2025 plunged to its lowest level since 1973. This supply drought, combined with surging construction costs and a labor shortage that has contractors competing ferociously for workers, has created a perfect inflationary storm.

The numbers are staggering. In March 2025, the average price of new apartments in Greater Tokyo hit ¥104.85 million, representing a 37.5% year-over-year increase—only the second time in history that monthly averages exceeded ¥100 million. In Tokyo’s central 23 wards, prices soared even higher, reaching ¥136.1 million, a 21.8% jump from 2024. The six core municipalities—Chiyoda, Chūō, Minato, Shinjuku, Shibuya, and Bunkyō—saw the average new condominium price rocket to ¥195 million.

Even the used apartment market, traditionally more stable, experienced unprecedented turbulence. Used apartments in Tokyo’s 23 wards posted a 28.3% year-over-year increase in April 2025, the highest growth rate since data collection began. Property analysts project that Tokyo property prices will continue to increase by 5-6% annually in 2026, representing a slight deceleration from 2025’s blistering pace but still far outstripping wage growth.

“Developers are focusing on central locations where they can sell luxury condos and justify the pricing,” Zoe Ward, CEO of brokerage Japan Property Central, explains. “A lot of their inputs will be construction costs and land pricing.” This concentration on high-margin luxury developments has created a bifurcated market where the wealthy secure prime real estate while middle-class Japanese families are increasingly priced out of ownership in their own capital.

Takaichi’s Conservative Mandate and the Immigration Scapegoat

Takaichi’s electoral triumph on February 8 was built partly on promises to address what she frames as “anxiety and a sense of unfairness” about foreigners in Japan. During her campaign, she pledged tougher immigration policies, including stricter requirements for foreign property owners and caps on foreign residents. Her coalition agreement with the Japan Innovation Party includes formulating a “population strategy” by the end of fiscal year 2026, complete with numerical targets for accepting foreigners.

Within days of taking office in October 2025, Takaichi established a ministerial meeting on foreign policy and created a new cabinet position—minister of “a society of well-ordered and harmonious coexistence with foreign nationals”—headed by Economic Security Minister Kimi Onoda. The government has already announced that starting in fiscal year 2026, foreign nationals will be required to declare their nationality when purchasing property, with copies of passports or residence cards submitted to authorities.

The political calculus is clear. Japan’s property prices have become a flashpoint for public frustration, and immigration provides a convenient target. Takaichi’s rhetoric taps into genuine anxieties—real wages have stagnated while housing costs have skyrocketed—but directs blame toward a demographic that represents just 3% of Japan’s population and accounts for roughly 27% of property transactions nationwide (and 20-40% of new apartments in central Tokyo, according to Mitsubishi UFJ Trust & Banking Corp).

Yet here’s the uncomfortable truth the data reveals: foreign buyers aren’t driving Tokyo’s affordability crisis. They’re beneficiaries of it.

The Real Culprits: Supply Shortages and Structural Dysfunction

Tokyo’s housing crisis is fundamentally a supply story. New condominium supply in the Tokyo metropolitan area declined 4.5% in 2025 to just 21,968 units—the lowest point in more than half a century. Meanwhile, demand remains robust. Net migration continues to favor Tokyo and the capital region as young professionals flee provincial cities for better opportunities. Household formation rates, driven by younger workers and an increasing number of single-person households, continue to outpace new construction.

The weak yen has certainly attracted foreign capital—the currency’s depreciation has increased the costs of imported raw materials while making Japanese assets cheaper for international buyers. But foreign investment is flowing into a market already constrained by:

Labor shortages: Japan’s construction industry faces a severe demographic crunch, with an aging workforce and insufficient young workers entering the trades. This scarcity drives up labor costs and slows project timelines.

Rising construction costs: Beyond labor, material costs have surged. New buildings must meet stricter energy efficiency standards to qualify for tax incentives, further inflating development expenses.

Regulatory complexity: Land use regulations and planning processes remain byzantine, delaying projects and limiting density in areas where demand is highest.

Investor behavior: With ultra-low interest rates (the Bank of Japan only recently raised its policy rate to 0.75%, still historically modest), Japanese investors and homeowners have reinvested massive capital gains back into the housing market, widening the gap for first-time buyers.

The residential property price index in the Tokyo Metropolitan Area rose 8.14% year-over-year in January 2025—but when adjusted for inflation, growth was a more modest 3.95%. Nationally, residential prices increased 10.7% in 2025. These aren’t speculative bubbles driven by foreign money; they’re the inevitable consequence of structural undersupply meeting persistent demand.

Asia’s Affordability Crisis: A Regional Epidemic

Tokyo is not an outlier. Across the Asia-Pacific region, major cities are grappling with parallel crises that expose the limits of blaming foreign investment for homegrown policy failures.

In Seoul, apartment prices rose roughly 8.7% in 2025—the fastest annual gain in nearly two decades, according to Korea Real Estate Board data. Prime districts like Songpa-gu, Yongsan-gu, and Seocho-gu posted monthly gains above 2% in late 2025. Seoul homes now average 1.4 billion KRW while the national average sits near 470 million KRW, making Seoul roughly three times pricier than the rest of South Korea. The city’s unique jeonse rental system—where tenants pay lump-sum deposits of 50-80% of property value—is pushing more renters toward outright purchases, further inflaming demand.

Seoul’s affordability crisis shares Tokyo’s structural DNA: supply constraints driven by limited land availability, high construction costs, and regulatory hurdles. Foreign investors now account for a significant portion of Seoul’s premium real estate market, but as with Tokyo, they’re capitalizing on—not creating—the supply-demand imbalance.

Further south, Australia presents perhaps the starkest illustration of housing dysfunction. Over the past five years, median advertised rents rose approximately 48% for both houses and units, with the strongest increases in Hobart (64%), Adelaide (57%), and Perth (50%). Australian home values climbed 47.3% since March 2020, adding about $280,000 to the median dwelling value, while median annual household income increased just 15%. Tenants now dedicate a record 33.4% of their income to rent.

The Australian case exposes the futility of immigration scapegoating. Despite foreign buyer restrictions implemented in recent years, supply shortages persist. The National Housing Supply and Affordability Council projects that 938,000 new dwellings will be built over the five-year Housing Accord period—a shortfall of 262,000 dwellings relative to the 1.2 million target. Labor shortages, high material costs, and financing constraints continue to weigh on new supply.

The Double-Edged Sword of Supply Constraints

Supply constraints function as a double-edged sword in Tokyo’s housing market. On one edge, limited new construction protects existing property owners’ equity, creating a politically powerful constituency that benefits from scarcity. Homeowners who purchased properties years ago have seen valuations soar—wealth accumulation that reinforces the LDP’s traditional base.

On the other edge, this same scarcity devastates affordability for younger Japanese, first-time buyers, and middle-class families. The price-to-income ratio has stretched to unsustainable levels. In Tokyo’s eastern suburbs, it would take an average wage earner 35 years to save a 20% deposit for a median-priced house. Even clearing that hurdle, servicing the mortgage would consume one-and-a-half times their income.

Takaichi’s immigration restrictions, even if fully implemented, won’t resolve this fundamental tension. Requiring foreign buyers to declare nationality and submit documentation may provide political theater, but it does nothing to address the core problem: Japan isn’t building enough housing where people want to live.

The government’s own data shows a cumulative shortfall of approximately 600,000 housing starts over the past four years due to delays in permits and construction. Seoul’s apartment move-in volume in 2026 is projected to fall to 16,412 units, a 48% drop from 2025. These supply crunches dwarf any impact from foreign investment flows.

What Takaichi’s Government Should Actually Do

If the new Prime Minister is serious about addressing Tokyo’s housing affordability crisis—and the cost-of-living pressures that animated her electoral mandate—her government must confront the structural impediments to supply expansion. Political expedience will tempt her toward performative restrictions on foreign buyers, but meaningful reform requires harder choices:

1. Streamline Planning and Zoning: Tokyo’s land use regulations must be modernized to allow greater density near transit hubs and employment centers. The current system protects low-density neighborhoods at the expense of housing abundance.

2. Invest in Construction Capacity: Address labor shortages through vocational training programs, immigration pathways for skilled construction workers (yes, immigration can be part of the solution), and productivity improvements through technology adoption.

3. Reduce Development Costs: Review energy efficiency mandates and other regulatory requirements that, while well-intentioned, inflate construction costs without proportionate benefits. Standardize processes to reduce complexity.

4. Public Housing Expansion: Increase government investment in public and social housing to provide affordable options for low- and middle-income families. This addresses demand pressure without relying solely on market mechanisms.

5. Tax Incentives for Developers: Offer targeted tax breaks for developers who build affordable housing units, particularly in high-demand areas currently dominated by luxury developments.

6. Transparency on Foreign Investment: Rather than restricting foreign capital outright, implement comprehensive data collection to understand its actual impact. Evidence-based policy requires understanding the problem’s true scale.

7. Address the Weak Yen Strategically: The weak yen makes Japanese assets attractive to foreign buyers but also inflates construction costs through expensive imports. Coordinated monetary policy that stabilizes the currency could ease both dynamics.

The Cost of Political Convenience

Takaichi’s electoral success demonstrates the political potency of immigration skepticism in an era of economic anxiety. Her pledge to “stand firm” against foreigners resonates with voters struggling to afford housing in their own capital. But scapegoating immigration for Japan real estate supply constraints—and by extension, Tokyo property prices 2026 projections—risks squandering Japan’s best chance at securing the workforce it needs for economic vitality.

Japan’s demographic crisis is severe. The working-age population is shrinking, birth rates remain stubbornly low, and without immigration, labor shortages will only intensify. The construction sector—already constrained—will face even greater challenges replacing aging workers. Takaichi’s administration created a ministerial post for “harmonious coexistence with foreign nationals” while simultaneously pursuing policies that frame foreigners as threats. This contradiction epitomizes the challenge: Japan needs foreign labor and capital, but political expediency demands treating both as problems to be managed rather than assets to be cultivated.

The data from Seoul and Australia reinforces a sobering lesson: restricting foreign investment doesn’t automatically increase housing affordability. What it does is provide political cover for avoiding harder structural reforms. Seoul implemented various restrictions on foreign land purchases, yet prices in prime districts continue surging. Australia tightened foreign buyer rules, yet the housing shortage persists and rents have climbed 48% in five years.

A Regional Reckoning

Tokyo’s crisis is a microcosm of a broader Asian and global phenomenon. Cities worldwide face similar pressures: rapid urbanization concentrating demand in limited geographic areas, construction industries struggling with labor and cost constraints, and political systems that find restricting foreign investment easier than confronting NIMBYism and regulatory dysfunction.

The Asia-Pacific commercial real estate market, as CBRE’s 2025 outlook notes, will see “steady growth, split performance” reflecting these divergent dynamics. Tokyo, Seoul, and Australian cities will continue experiencing rental and price growth driven by supply constraints, while secondary markets struggle with oversupply and demographic headwinds.

For Tokyo specifically, the forecast is clear: absent meaningful supply-side reforms, property prices will continue rising 5-6% annually through 2026 and beyond, with luxury properties potentially seeing 6-7% growth. The contract rate for new condominiums remains robust at 68.8% in Tokyo’s 23 wards, indicating that despite high prices, demand persists among those who can afford it—a self-reinforcing dynamic that further marginalizes middle-class aspirations.

Conclusion: The Path Forward

Sanae Takaichi’s historic electoral mandate gives her the political capital to pursue transformative reforms. Her landslide victory, fueled by “Sanamania” among young voters and conservatives disillusioned with previous LDP leadership, provides a rare opportunity to tackle Japan’s structural challenges head-on.

The question is whether she will spend that capital on performative restrictions that provide political satisfaction but economic dysfunction, or on the harder work of actually increasing Tokyo’s housing supply. The latter requires confronting powerful constituencies—existing homeowners who benefit from scarcity, construction companies comfortable with the status quo, local governments protective of low-density neighborhoods, and NIMBYs who oppose any development near them.

Japan’s demographic trajectory—declining population, shrinking workforce, aging society—leaves little room for error. The nation cannot afford to alienate foreign capital and foreign workers while simultaneously failing to build enough housing for its own citizens. Affordable housing Japan immigration policy must recognize this dual imperative: Japan needs both foreign contributions and domestic supply expansion.

Tokyo property prices 2026 will continue their upward march unless fundamental reforms materialize. The supply constraints that drive this crisis are double-edged precisely because solving them requires political courage—the willingness to prioritize long-term housing abundance over short-term electoral advantage.

Prime Minister Takaichi has demonstrated political acumen and charisma. She’s built an unlikely coalition, connected with young voters through social media, and positioned herself as a decisive leader willing to make bold moves. Now she must decide: will she channel that boldness toward the structural reforms Japan desperately needs, or will she take the politically convenient path of blaming foreigners for a crisis rooted in decades of policy failure?

Asia’s housing affordability epidemic—from Tokyo to Seoul to Sydney—awaits her answer. The region’s other leaders are watching closely, because Tokyo’s choices will either illuminate a path forward or demonstrate, once again, how political convenience trumps economic rationality in the housing policy arena.

The February 8 election results are two days old. The real test of Takaichi’s premiership begins now.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The world’s second-largest economy faces a reckoning that no amount of information control can erase

The construction cranes stand frozen against Shanghai’s skyline like monuments to excess. In Guangzhou, half-finished apartment towers cast long shadows over streets where homebuyers once lined up with cash deposits. Across China’s tier-two and tier-three cities, the evidence is impossible to ignore: new home prices dropped 2.4% year-on-year in November 2025, marking the 29th consecutive month of price declines.

This isn’t just another market correction. It’s the unraveling of a $60 trillion real estate ecosystem that powered four decades of unprecedented growth—and here’s what keeps global economists awake at night: despite aggressive government intervention and increasingly sophisticated censorship machinery, this crisis won’t bottom out until 2030.

The Staggering Scale of China’s Property Collapse

Numbers tell stories that social media censors can’t delete. The Index of Selected Residential Property Prices registered a 6.40% year-on-year contraction in Q2 2025, but the human cost cuts deeper. Zhang Wei, 34, has dutifully paid mortgage installments for two years on an apartment in Chongqing that remains a concrete skeleton, unfinished and uninhabitable. His story echoes across hundreds of cities.

The developer collapses read like a who’s who of China’s corporate giants. China Evergrande Group, with over $300 billion in debt, received a liquidation order in January 2024 and was delisted from the Hong Kong Stock Exchange in August 2025. But Evergrande wasn’t alone. China Vanke Co. reported a record 49.5 billion yuan ($6.8 billion) annual loss for 2024, sending shockwaves through a sector that believed state-backed developers were immune to failure.

Country Garden, once China’s largest private developer with 3,000 projects nationwide, defaulted on international bonds in October 2023 after missing payments within a 30-day grace period. Investment in real estate development declined by 14.7% in the first ten months of 2025, with sales of new homes projecting an 8% decrease for the full year, marking the fifth consecutive year of negative growth.

The construction sector tells an equally grim story. The total area of residential projects started declined by 22.55% year-on-year to 536.6 million square meters, while completed residential units fell by 25.81% to 537 million square meters. Construction workers remain unpaid, suppliers face bankruptcy, and the entire supply chain—from cement manufacturers to elevator installers—struggles to survive.

Why This Isn’t Just Another Downturn: The Structural Trap

Understanding why recovery will take until 2030 requires examining the unique architecture of China’s economy. Unlike typical real estate downturns, this crisis strikes at the foundational model that has powered Chinese growth since the 1990s.

The Property-Dependency Problem

Real estate and related industries accounted for approximately 25% of China’s GDP in 2024, despite the ongoing decline. This isn’t simply about construction—it’s about land sales, furniture manufacturing, home appliances, property management, legal services, and financial products all built around housing.

Housing prices have fallen 20% or more since they peaked in 2021, and with 70% of household wealth tied to property, falling home prices directly erode family balance sheets. This creates a vicious cycle: declining wealth leads to reduced consumption, which slows economic growth, which further pressures property values.

The Local Government Fiscal Catastrophe

Here’s where the crisis becomes truly intractable. Revenue from land sales by China’s local governments dropped 16% in 2024 compared with the previous year, after a 13.2% decline in 2023. But land sales aren’t just one revenue stream among many—they’ve been the primary funding mechanism for local governments since the 1990s.

Local Government Financing Vehicles (LGFVs), the shadow banking entities that local officials created to circumvent borrowing restrictions, are now drowning. Total debt raised directly by local governments and via their financing vehicles now stands at around 134 trillion yuan, equal to roughly $19 trillion.

These LGFVs were designed with a simple assumption: land values would continue rising, providing both collateral for new loans and revenue from sales to service existing debt. That assumption has catastrophically failed. The call for LGFVs to buy land to create revenue for local governments made matters worse, turning land from a key source of revenue into a source of new debt.

The Inventory Overhang

The inventory turnover ratio in China shortened by five months from its peak of 25.9 months in April 2025, but at the current pace, it may take another year and a half for the clearance cycle to reach 12-18 months—a relatively healthy range. That’s optimistic. In many tier-three and tier-four cities, years’ worth of unsold inventory sits vacant, with no clear demand in sight.

The math is unforgiving. Even if sales stabilize tomorrow, clearing existing inventory while developers and local governments simultaneously restructure trillions in debt requires time measured in years, not quarters.

Censorship vs. Economic Reality: When Propaganda Meets Balance Sheets

Beijing has deployed its formidable censorship apparatus with surgical precision. In less than three weeks, social media platforms Xiaohongshu and Bilibili removed more than 40,000 posts under a “special campaign” to regulate online real estate content. The Shanghai branch of the Cyberspace Administration led efforts to scrub negative sentiment about housing markets from social media.

The censorship strategy extends beyond simple post deletion. After authorities urged platforms to clean up material containing problems such as “provoking extreme opposition, fabricating false information, promoting vulgarity, and advocating bad culture,” the Cyberspace Administration of China announced in early 2025 that platforms had removed more than a million pieces of content.

This represents a coordinated campaign to control the narrative around the property crisis. Posts discussing falling home values, developer defaults, or economic pessimism are systematically removed. Even discussions of the Zhuhai vehicular attack in November 2024 were censored, part of a broader effort to suppress anything that might undermine social stability.

But here’s the fundamental problem with censoring an economic crisis: you can delete social media posts, but you can’t delete non-performing loans. You can remove hashtags about Evergrande’s default, but you can’t remove the actual debt from bank balance sheets. You can silence influencers discussing property values, but you can’t force buyers into a market where confidence has evaporated.

The contrast between official statements and ground-level reality grows starker by the month. State media emphasizes “stability” and “gradual recovery,” while sales of the top 100 developers plunged 36% in terms of value in November 2025 from a year earlier. Beijing announces stimulus packages, yet investment in fixed assets, which includes property, contracted 2.6% over the January through November period compared with a year earlier.

The 2030 Timeline: Breaking Down the Recovery Math

Why 2030? The projection isn’t arbitrary—it’s based on the time required to work through structural imbalances that took decades to build.

Inventory Clearance: 3-4 Years Minimum

Even optimistic scenarios require 2027-2028 to clear excess housing inventory in major cities, and potentially 2029-2030 for tier-three and tier-four cities. This assumes sales don’t deteriorate further—an assumption that grows shakier as demographic headwinds intensify.

Developer Balance Sheet Repair: 4-6 Years

Dozens of Chinese developers have been approved for debt restructuring plans since the start of 2025, clearing more than 1.2 trillion yuan ($167 billion) in liabilities. But this represents a fraction of total developer debt. The restructuring process—negotiating with creditors, selling assets, and gradually rebuilding financial viability—typically requires multiple years even in the best circumstances.

Local Government Fiscal Restructuring: 5-7 Years

This is the longest and most complex component. Beijing authorized 10 trillion yuan in local debt issuance—to be disbursed over five years—to address hidden obligations in 2024. But this merely refinances existing debt at lower interest rates; it doesn’t create new revenue sources.

The fundamental problem remains: local governments structured their finances around continuously rising land values. Rebuilding fiscal sustainability requires either dramatically cutting expenditures (politically painful and economically damaging) or finding alternative revenue sources (difficult and slow to implement).

Demographic Drag: Permanent Headwind

China’s working-age population is shrinking, and urbanization—the force that drove housing demand for three decades—has plateaued. These aren’t cyclical issues that resolve with stimulus; they’re structural realities that reduce baseline housing demand permanently.

Historical Parallels: Lessons from Japan’s Lost Decades

The comparison to Japan’s 1990s property bubble isn’t perfect, but it’s instructive. By 2004, prime “A” properties in Tokyo’s financial districts had slumped to less than 1 percent of their peak, and Tokyo’s residential homes were less than a tenth of their peak. It took until 2007—16 years after the bubble burst—for property prices to begin rising again.

From 1991 to 2003, the Japanese economy grew only 1.14% annually, while the average real growth rate between 2000 and 2010 was about 1%. What was initially called the “Lost Decade” became the “Lost Two Decades,” and many economists now reference “Lost Three Decades.”

Japan’s experience demonstrates several sobering realities:

Balance sheet recessions take years to resolve. Even with aggressive monetary easing (Japan pioneered zero-interest-rate policy in the late 1990s) and massive fiscal stimulus, deleveraging proceeds slowly. Households and corporations prioritize debt repayment over spending and investment.

Zombie companies drain economic vitality. Banks kept injecting funds into unprofitable firms that were too big to fail, preventing capital reallocation to productive uses. China faces a similar risk with its state-owned enterprises and developers.

Property-driven wealth effects create powerful negative feedback loops. As Japanese real estate values declined, household wealth evaporated, consumption stagnated, and deflation became entrenched. China’s even greater concentration of household wealth in property suggests potentially worse wealth effects.

The key difference: China’s crisis is arguably more structurally complex. Japan’s property bubble was primarily driven by speculative excess and loose monetary policy. China’s bubble involved speculation plus local government fiscal dependency plus shadow banking plus a fundamental economic model built around property development. Unwinding this requires more than monetary and fiscal tools—it requires redesigning the growth model itself.

Global Ripple Effects: No Crisis Is an Island

China’s property troubles send shockwaves far beyond its borders. Australia and Brazil, major commodity exporters, already face reduced demand for iron ore, copper, and other construction materials. European luxury brands that catered to China’s affluent property developers and homebuyers report softening sales.

The exposure runs deeper than trade flows. Foreign investors hold portions of Chinese developer bonds, though many have already taken massive losses. More concerning are the indirect linkages: Chinese state-owned companies with overseas investments potentially scaling back as domestic pressures mount, Chinese tourists and students spending less abroad as household wealth declines, and geopolitical implications of a economically stressed superpower.

Financial contagion risks remain contained for now—China’s capital controls and state banking sector provide insulation. But the growth drag is unavoidable. China’s housing market correction continues as an ongoing headwind, with KKR’s chief economist for Greater China estimating a 1.5 percentage point dent on China’s gross domestic product in 2025, compared with 2.5 percentage points in 2022.

What Tier-1 Companies Should Do Now

For multinational corporations and investors, the 2030 timeline requires strategic adjustments:

Diversify China exposure. Companies heavily dependent on Chinese property-related demand should accelerate diversification into other Asian markets or sectors. The “China-only” growth strategy needs fundamental reevaluation.

Watch local government creditworthiness. Companies with receivables from Chinese local governments or infrastructure projects face rising payment risks. Credit insurance and careful monitoring of local fiscal conditions are essential.

Reconsider real estate collateral. Lenders and investors using Chinese property as collateral should reassess valuations aggressively. The assumption that property values provide a floor has proven catastrophically wrong.

Monitor consumer wealth effects. Consumer-facing businesses should prepare for years of constrained spending as household wealth remains depressed. The Chinese consumer, long expected to drive global growth, faces significant headwinds.

Prepare for policy volatility. Beijing will likely cycle through various stimulus measures, creating temporary market movements. Distinguishing genuine structural improvements from short-term liquidity injections is critical.

The Painful Path Forward

Beijing recognizes that the core issue lies in reducing local governments’ dependence on LGFVs, with Premier Li Qiang underscoring the need to “remove government financing functions from local financing platforms and press ahead with market-oriented transformation”. This is the right diagnosis, but the treatment will be painful and prolonged.

“China’s property crisis represents more than a cyclical downturn—it’s the unwinding of a growth model that took 30 years to build. Recovery to sustainable equilibrium requires 5-7 years minimum, with 2030 representing the earliest realistic bottom under optimistic scenarios. Censorship can control information but cannot alter the underlying economics.“

China needs to rebuild its entire fiscal architecture. This means new tax structures, revised central-local government responsibilities, transparent budget constraints, and allowing insolvent entities to actually fail rather than propping them up indefinitely. Each of these reforms faces powerful resistance from vested interests.

The alternative—continuing to refinance bad debts, prop up zombie developers, and hope for a return to property-driven growth—merely extends the crisis. It’s Japan’s playbook from the 1990s, and the results speak for themselves.

Conclusion: When Censorship Meets Economic Gravity

Beijing’s censors can scrub social media clean of negative sentiment. They can delete posts, suspend accounts, and create the digital appearance of stability. What they cannot do is delete the structural imbalances in China’s economy, rewrite the math of debt-to-GDP ratios, or manufacture demand in a demographically declining society with excess housing supply.

The 2030 timeline isn’t pessimism—it’s arithmetic. Clearing inventory, restructuring debt, rebuilding local government finances, and allowing new economic models to emerge requires time measured in years, not quarters. Japan’s experience, with similar structural challenges but arguably simpler economics, took more than a decade even with aggressive policy responses.

For global businesses, investors, and policymakers, the implications are profound. The Chinese growth engine that powered the global economy for three decades is fundamentally transforming. The property-driven model is over, and what replaces it remains uncertain.

The censors can control the narrative on Weibo. They cannot control economic reality. And economic reality suggests that 2030 marks not the beginning of recovery, but merely the year when China might finally hit bottom—if, and only if, Beijing pursues genuine structural reforms rather than continued extend-and-pretend tactics.

For hundreds of millions of Chinese families like Zhang Wei’s, still paying mortgages on unfinished apartments, that timeline offers cold comfort. But it offers something perhaps more valuable: honesty about the scale of the challenge ahead. No amount of censorship can change what the numbers tell us—this is a crisis that will define China’s next decade.

Data Sources :

This analysis draws from National Bureau of Statistics of China, International Monetary Fund reports, Bloomberg Intelligence, Goldman Sachs research, and major property developer financial statements through December 2025. Statistical projections are based on historical recovery timelines from comparable property crises, adjusted for China-specific structural factors.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Global Stock Markets 2026: S&P 500 at Record Highs Amid War, Inflation & Rate Risk

Spain Near 100M Tourists: A Structural Travel Map Shift : Booming Travel Economy

Wellness Tourism’s $1 Trillion Rise Is Rewriting Travel Rules

Warsh’s Fed Kills the Rate-Cut Trade:Inflation, and Your Money

Indonesia vs. MSCI, Greenspan’s Legacy vs. Warsh’s Revolution, Micron vs. the Memory Shortage: A Global Finance Scorecard for Mid-2026

The End of Visa and Mastercard’s Monopoly? Rise of Alternatives

AI’s Energy Hunger Is Rewriting Global Power Markets: Reshaping the World Economy

UK Political and Economic Turmoil: Rachel Reeves’ Fall, Britain’s Fiscal Crisis

China’s Export Miracle Masks a Property Disaster: Growing Without Its People

Indonesia’s $1.5 Trillion Economy on the Edge: chances of MSCI Downgrade

Oil Falls to $70 as US-Iran Peace Talks Advance: Global Energy Markets

Micron’s $41.5 Billion Quarter: How AI’s Insatiable Memory Hunger Is Reshaping the Semiconductor Industry

Alan Greenspan Dead at 100: The Rise, Reign, and his Complicated Legacy

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

KPMG Australia CEO Resigns After Whistleblower Claims Exposed Investigation Failures

PwC China Partner Payouts Cut Amid Evergrande Audit Fraud

Broadcom Market Value Loss: Revenue Forecast Disappoints

Pakistan Budget FY 2026-27: Relief, Prospects, and the Tightrope Walk

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Here’s How Much It’ll Cost You to Be Part of SpaceX’s Record-Breaking $75 Billion IPO

Nasdaq Tumbles 4% as Chip and Memory Stocks Sink: A $1.2 Trillion Wipeout

Japanese Mid-Sized Firms Flock to Southeast Asia for Growth

Smash Capital Leads $200M Funding for Allen Control Systems

How to Fix Pakistan’s Debt Economy: A Structural Blueprint

New Investment Super-Cycle: AI, Green Energy & Re-Shoring

Democrats Draw a Red Line Around Military AI — And the Pentagon Is Already Pushing Back

Chip Stocks Race Toward Biggest Gains Since Dotcom Era on AI Demand

Russia Overspends on Putin’s War in Ukraine by $28bn

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 months ago

Analysis4 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks5 months ago

Banks5 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025