China Economy

China Housing Market Turnaround: White‑List Model Stabilises Prices

China’s real estate sector, the single largest drag on the world’s second‑largest economy for over three years, is showing the first consistent signs of life. According to the National Bureau of Statistics, new‑home prices in the four tier‑1 cities—Beijing, Shanghai, Guangzhou, and Shenzhen—ticked up 0.2% month‑on‑month in May, the third consecutive monthly increase (National Bureau of Statistics of China, May 2026 Housing Data). While the uptick is modest, it represents a psychological turning point after prices fell for 24 of the previous 30 months. The catalyst: a government‑engineered “white‑list” model that channels credit exclusively to healthy, systemically important developers while allowing weaker players to exit.

The White‑List Project Funding Mechanism

In early 2025, the People’s Bank of China and the Ministry of Housing and Urban‑Rural Development jointly launched the “Real Estate Sector Normalization Facility,” commonly called the white‑list. The mechanism designates about 60 developers—both state‑owned and private—as eligible for new bank lending, bond issuance, and equity refinancing, provided they meet strict criteria: no default history, completion of at least 80% of presold units, and a commitment to “reasonable” pricing. As of May 2026, 1.4 trillion yuan ($195 billion) in new credit had been approved, with 900 billion yuan actually disbursed (PBoC Monetary Policy Implementation Report, Q1 2026). The funds are escrowed and released only against verified construction milestones, a safeguard that prevents the diversion of capital that plagued the Evergrande and Country Garden crises.

This targeted approach is a departure from the indiscriminate liquidity injections of 2023 and 2024. The government has allowed some 35 mid‑tier developers, burdened with unviable projects in third‑ and fourth‑tier cities, to enter bankruptcy restructuring. The message is clear: moral hazard is being contained, and the state will backstop only the core of the housing supply chain. The strategy echoes the US TARP program of 2008, but with Chinese characteristics—directed credit rather than equity injections.

Developer Bond Revival and Equity Rebound

The credit market has responded with surprising enthusiasm. Dollar‑denominated bonds of white‑listed developers have returned 18% year‑to‑date in 2026, making Chinese property high‑yield debt the top‑performing sector in emerging markets (J.P. Morgan EMBI Global China Property Index, June 2026). China Vanke, the bellwether state‑backed firm, saw its 2029 bond price rally from 60 cents on the dollar in January to 92 cents by June. The Shanghai Composite Real Estate Index has climbed 22% from its February lows, though it remains 55% below its 2020 peak.

Investor confidence is being slowly rebuilt by the white‑list’s transparency. Regular updates on fund disbursement, project completion rates, and sales data create a data‑driven narrative that contrasts with the opacity of the Evergrande era. Analysts at UBS now forecast that the sector’s contribution to GDP, which swung from a positive 1% to a negative 2.5% drag between 2021 and 2025, could be nearly neutral by Q4 2026 (UBS China Real Estate Outlook, June 2026).

Fragile Recovery: Tier‑City Divergence

Beneath the headline stabilization, a stark divergence persists. Tier‑1 and strong tier‑2 cities like Hangzhou and Nanjing are seeing inventory drawdowns, and some have even reinstated cooling measures to prevent a rapid rebound. In contrast, tier‑3 and tier‑4 cities, which account for 60% of national housing stock by area, remain oversupplied. Inventories in these cities stand at 28 months of sales, against a healthy benchmark of 12–14 months. The government has recently approved a 500‑billion‑yuan relending facility for local government‑owned platforms to purchase unsold completed apartments and convert them into affordable rental housing, a measure reminiscent of the Spanish “bad bank” (Sareb) model (State Council of China, Notice on Affordable Housing Facility, April 2026). This should gradually absorb excess stock, but the process will take years.

The consumer side remains hesitant. Despite the PBOC cutting the five‑year loan prime rate to 3.6%, household leverage is already elevated, and the “precautionary savings” motive is strong. A People’s Bank survey found that 63% of urban households consider now a “bad time” to buy a home, down from 72% in 2024 but still high. The culture of speculative property investment, which drove decades of growth, has been broken—perhaps permanently. The market is transitioning to one driven by genuine end‑user demand and demographic fundamentals.

The Macro Impact and Policy Outlook

A stable housing market removes the largest downside risk to China’s 2026 GDP growth target of “around 5%.” Construction‑related industries, from steel to appliances, are seeing restocking demand. The financial system’s exposure to real estate, estimated at 40% of bank collateral, becomes less perilous if prices cease falling and transaction volumes recover. The PBOC, now more comfortable with the property outlook, can focus on managing the exchange rate and domestic liquidity without being forced into ad‑hoc bailouts.

Going forward, the test will be whether the white‑list model can catalyze a self‑sustaining recovery. Key indicators to monitor are floor space sold (recovering slowly), new starts (still contracting), and the time taken to complete presold homes (improving). The government’s commitment to “housing is for living, not speculation” remains unchanged, but the policy toolkit has evolved from crackdown to calibrated support. If the tier‑1 price stabilization spreads to second‑tier cities in the autumn, China’s housing market turnaround will be confirmed, providing a significant tailwind to global commodity demand and emerging market sentiment.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

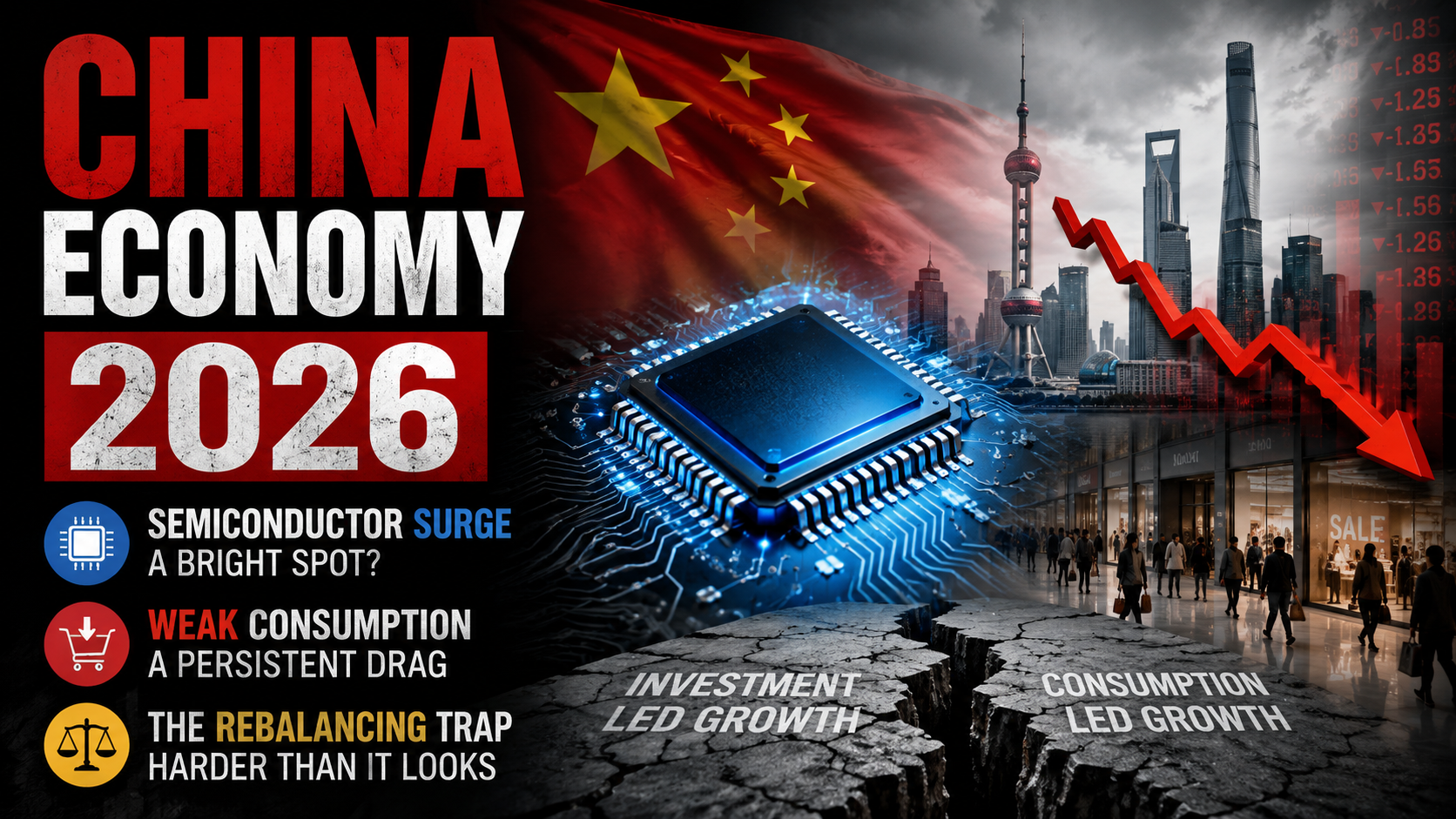

China’s semiconductor exports surged 87% in May 2026 even as retail sales stagnated and property investment fell 16%. Inside the structural divergence threatening Beijing’s growth model.A single statistic from China’s May 2026 industrial output report captures the country’s economic condition better than any official growth headline: semiconductor production surged 87% year-on-year, even as retail sales remained muted and property investment fell at its steepest rate since the pandemic. The gap between China’s industrial machine and its domestic consumption economy has never been wider. And unlike earlier cycles, there is no obvious policy lever that closes it quickly.

China officially reported 5.0% GDP growth in Q1 2026, but the US-China Economic and Security Review Commission and independent economists identified three reasons for scepticism: ongoing downward revisions to prior-year numbers, a statistical rebound effect, and the absence of genuine domestic demand recovery. The government’s own fiscal deficit target of 4% of GDP — the highest since 1991 and set in the 15th Five-Year Plan passed at the March “Two Sessions” — implies that official growth is being propped by state investment rather than organic household consumption.

The Export Machine: Strength Built on Structural Weakness

China’s trade surplus in 2025 crossed $1.2 trillion — a record — and the export surge has continued in 2026. In May, exports denominated in US dollars rose 19.6% year-on-year, the second-largest increase since early 2022. Semiconductor exports rose 110%. Mobile phone exports rose 44%. Auto parts and computing hardware rose 66%.

The IMF estimated in early 2026 that the renminbi was undervalued by 16%, and pressed Beijing to allow revaluation to reduce the trade imbalance. China demurred, pledging only that the currency would remain “generally stable.” Meanwhile, China’s passenger car exports rose 60.6% year-on-year in Q1 — many of them cheaper models subsidised into foreign markets after Beijing’s “anti-involution” policy created domestic oversupply. Developing markets bore the brunt: the US-China Economic and Security Review Commission documented a 14% surge in “China Shock 2.0” export pressure on emerging economies.

But the export machine’s strength is inseparable from the domestic market’s weakness. When local demand softens, manufacturers redirect capacity toward international markets. The result is not a virtuous cycle of industrial upgrading; it is a pressure valve that delays, but does not resolve, the underlying consumption deficit.

The Consumption Deficit: Property, Wealth, and Japanification

Roughly two-thirds of Chinese household wealth is held in the form of property. The ongoing correction in that market is therefore not merely a sectoral issue — it is a household balance sheet crisis that suppresses the propensity to consume across the entire economy. Fixed-asset investment fell 4.1% in the first five months of 2026 year-on-year — the steepest decline since May 2020. Property investment dropped 16.2%. Government stimulation efforts — trade-in subsidies for EVs and appliances, value-added tax rebates — have produced modest and temporary retail bounces without addressing the underlying confidence deficit.

Mao Zhenhua, a professor at the University of Hong Kong, put it plainly: “Apart from high-tech and export sectors, the Chinese economy is very cold.” The producer price index has fallen for 41 consecutive months since October 2022 — a textbook sign of deflationary overcapacity. Some economists describe this as “Japanification”: prolonged deflation, declining investment returns, and a debt overhang — except that China’s greater dependence on real estate, local government financing vehicles, and exports makes the structural comparison more severe than Japan’s experience from the 1990s.

The Semiconductor Bet: Strategic Necessity and Competitive Exposure

Beijing’s response to the consumption deficit is to accelerate investment in industries deemed strategically vital: semiconductors, AI, electric vehicles, batteries, and green energy. The 15th Five-Year Plan explicitly frames this as building “New Quality Production Forces” — a move away from cheap manufactured goods toward technological self-sufficiency.

Progress is real but uneven. SMIC and Hua Hong are advancing at mature-node chip production, used in vehicles and industrial equipment. Equipment vendors Naura and AMEC are gaining global market share in manufacturing tools. Tungsten — a chipmaking input China controls at 79% of global mine production — has seen export controls imposed, pushing tungsten prices up 557% in just over a year.

Yet China imported a record $135 billion in semiconductors in a single quarter, driven by surging AI investment. Dependency on advanced foreign chips — particularly Nvidia’s H200 GPUs — remains acute. The path to true semiconductor self-sufficiency runs through advanced lithography technology that China has not yet replicated, and through memory chip manufacturing where domestic producer CXMT is still racing to achieve viable high-bandwidth memory yields.

The Rebalancing Trap

The structural paradox Beijing faces is that the industries it is investing in to generate new growth — semiconductors, AI, renewable energy — are highly capital-intensive and relatively employment-light. They generate industrial output and export revenue. They do not, by themselves, create the mass consumer purchasing power needed to rebalance toward domestic demand. As the Asia Society Policy Institute has documented, China’s capital-intensive industrial push could widen income inequality even as it advances national technological capacity, leaving the rural and lower-income population increasingly detached from the growth being generated.

Until Chinese households recover confidence in property as a store of value, until youth unemployment — officially 17% but widely estimated closer to 40% by independent economists — materially declines, and until local government debt overhangs are resolved, the consumer-led rebalancing that global markets have been anticipating for a decade will remain deferred.

The world’s second-largest economy, in 2026, is a machine that produces extraordinary technology and exports it to a world not fully ready to absorb the volume — while the domestic audience watches from the sidelines.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China’s May 2026 data shows high-tech manufacturing up 15.1% while property investment fell 16.2%. How Beijing’s export-led gamble is reshaping global supply chains.

The National Bureau of Statistics’ May 2026 release confirmed what economists had begun calling China’s “industrial divergence.” Scale-above industrial value-added output grew 4.5% year-on-year in May, accelerating 0.4 percentage points from April, with high-tech manufacturing surging 15.1%. The semiconductor sector was the standout: domestic output jumped 87% from the prior year, while China’s exports of semiconductors were up 110% from a year earlier, exports of mobile phones climbed 44%, and automatic data-processing machines rose 66%.

The Export Engine Running at Full Throttle

China‘s May exports (denominated in US dollars) were up 19.6% from a year earlier — the second biggest monthly increase since January 2022. The first two months of 2026 had registered an extraordinary 39.6% gain. Over all of 2025, China recorded a trade surplus exceeding $1.2 trillion — the largest ever posted by any country — as manufactured goods, particularly in advanced technology categories, poured into global markets.

The strength carries a double driver. First, the global AI boom has generated extraordinary demand for semiconductors and related hardware, where China‘s manufacturing base has rapidly scaled. Second, as domestic demand softened, manufacturers redirected capacity toward export markets. Gary Ng, senior Asia Pacific economist at Natixis, characterised this as the operative dynamic: “China’s exports have decelerated as the Iran war starts to affect global demand and supply chains,” though he noted the moderation was from record levels.

China’s economy in mid-2026 resembles a dual exposure photograph — one frame showing a technology powerhouse outpacing global rivals, the other depicting a property market in structural retreat that is slowly draining household wealth.

Goldman Sachs had projected 5–6% annual growth in China’s exports and raised its 2026 real GDP forecast to 4.8% — above both IMF projections and Bloomberg consensus. That upgrade rested on the observation that Chinese exports demonstrated resilience even against elevated US tariffs that hit 100% in April 2025 before settling at 30% in May following a bilateral agreement. Chinese exports of chips, semiconductors, autos, and auto parts continued to expand despite the tariff headwinds.

The Property Hole That Will Not Close

The other side of the ledger is less encouraging. In the first five months of 2026, fixed-asset investment fell 4.1% year-on-year — the steepest decline since May 2020. Within that, property investment dropped 16.2%. Given that roughly two-thirds of Chinese household wealth is held in real estate, the wealth destruction is persistent and consequential. Consumers saving to restore depleted balance sheets rather than spending is the logical response — and it explains why domestic retail demand has been chronically soft despite headline economic growth of 5% in 2025.

The Economist Intelligence Unit’s Nick Marro captured the strategic bet underlying Beijing’s trajectory: “There’s a strong emphasis on doubling down on manufacturing and ensuring that China’s competitive positioning in global supply chains remains sticky.” China‘s 15th Five-Year Plan (2026–2030), approved in late 2025, explicitly prioritises advanced manufacturing, semiconductors, AI, renewable energy, and digital infrastructure — doubling down on supply-side transformation rather than demand-side stimulus.

The Global Spillover: China Shock 2.0

The US-China Economic and Security Review Commission flagged a “14 percent surge in China Shock 2.0,” noting that developing markets are bearing the brunt of an export deluge driven by China’s market distortions. Unlike the original China Shock of the 2000s — which displaced labour-intensive, low-value manufacturing in rich economies — China Shock 2.0 is crowding out high-tech, high-value manufacturing in Europe and Japan. Goldman Sachs estimates that for every 1 percentage point of export-driven boost to Chinese GDP, other economies may see a 0.1 to 0.3 percentage point drag, with tech-intensive producers facing acute pressure.

Meanwhile, China’s voracious appetite for advanced chips it cannot yet manufacture domestically has produced a paradox: China imported a record $135 billion in semiconductors in the most recent quarter as AI investment accelerates. The country remains dependent on foreign-made advanced logic chips dominated by ASML, creating a structural vulnerability that its Five-Year Plan is designed to remedy — but may not resolve within this decade.

The Endgame of the Xi Gamble

The Economist captured the existential dimension of Beijing‘s strategy by quoting Johns Hopkins University‘s Yuen Yuen: “At no time in modern history has a large country gone all in on investment in high-end technology while also navigating a slowing economy and a local-government debt crisis.” Xi Jinping’s wager is that the technology-driven growth model scales faster than the old property-and-construction model collapses. The data through mid-2026 suggest the race is closer than Beijing’s official narrative acknowledges.

China’s GDP growth target for 2026 is the lowest since 1991 at 4.5–5%. Meeting it will depend on whether AI and green technology exports can sustain momentum against an Iran-related global slowdown that is already beginning to weigh on overall demand. The outcome will shape global trade balances, supply chain geography, and the AI chip economy for the next decade.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China’s exports surged 19.6% in May 2026, driven by AI semiconductors. But property investment fell 16.2% and fixed-asset investment hit its worst decline since COVID. Here’s the full picture.

China’s economy in 2026 is running a structural split that masks deep fragility behind impressive headline numbers. Exports are booming—up 19.6% in May from a year earlier, the second largest increase since January 2022—while the property sector, which underpins roughly two-thirds of household wealth, is contracting at its fastest pace since the early months of the COVID-19 pandemic.

The divergence is not sustainable indefinitely. Until the housing market stabilizes, the export engine—however powerful—cannot compensate for the structural drag on domestic demand, household confidence, and private investment that the property collapse creates.

The Export Machine Is Running on AI

The export numbers are genuinely striking. Semiconductor exports from China were up 110% year-over-year in May 2026, according to data from Deloitte Insights. Mobile phone exports grew 44%. Automatic data-processing machines—a category that captures computers and data storage equipment used in AI infrastructure—rose 66%. Between January and February 2026, total exports surged 39.6% from the prior year period, the largest two-month gain since 2022.

Two forces are driving this export strength. The first is genuine technological demand: global AI infrastructure buildout, particularly across Southeast Asia, the Gulf states, and Europe, is creating enormous appetite for Chinese-produced hardware components at every tier of the supply chain. The second is a more defensive dynamic—inventory building. Companies in trade-sensitive markets are pulling forward purchases in anticipation of further global supply chain disruptions linked to the Middle East conflict and continued U.S.-China trade friction.

That second driver carries embedded risk. If the supply chain disruption that motivated the inventory building does not materialize at the severity that buyers feared, a demand hangover could follow—slowing export growth sharply in the back half of 2026 and into 2027.

Property Investment Is Collapsing

Against the export strength, the property picture is alarming. Property investment fell 16.2% in the first five months of 2026 compared to the same period a year earlier. Fixed-asset investment overall declined 4.1% in the same period—the steepest contraction since May 2020. Even excluding property, fixed-asset investment was down 1.2% year-on-year. Manufacturing investment grew just 0.4%, suggesting businesses are reluctant to expand capacity when demand signals are uncertain.

The property crisis matters disproportionately because of its wealth effect. Roughly two-thirds of Chinese household wealth is held in real estate. When home prices fall, households do not merely lose nominal value—they respond by saving more and spending less, attempting to rebuild or stabilize balance sheets. That behavioral response deepens the demand shortfall, reinforces the cycle of developer distress, and makes a bottom in the market harder to reach.

National home prices continued falling in May, at a faster pace than April. Weakness was evident across most cities. The one pocket of relative stability was in first-tier cities—Beijing, Shanghai, Guangzhou, Shenzhen—where new-home prices rose for the third consecutive month, suggesting that government support measures may be gaining marginal traction in the most liquid and desirable markets. But analysts describe the national recovery as “uneven rather than broad-based.”

The PBOC Moves on Infrastructure, Not Stimulus

The People’s Bank of China Governor Pan Gongsheng announced a series of financial market measures in late June, including steps to increase the use of overnight reverse repo operations, narrow the short-term interest rate corridor, and promote offshore use of the renminbi. The announcements appeared to be part of a longer-term effort to strengthen monetary transmission and support yuan internationalization.

Critically, the package did not represent broad-based monetary stimulus. No major rate cuts were announced. No large-scale property rescue fund was launched. Analysts interpreted the measures as policymakers signaling continued focus on financial market development and liquidity management rather than a shift toward aggressive easing.

The restraint reflects a genuine policy dilemma. Chinese household debt levels have risen significantly. Property developers are burdened by debt accumulated during the excess-capacity boom of the 2010s. Aggressive stimulus risks inflating new bubbles rather than resolving underlying imbalances. Until organic demand—rather than government support—can fill the gap left by falling property investment, the recovery will remain patchy.

Industrial Production Holds, Investment Doesn’t

Industrial production grew 4.5% year-on-year in May, slightly below the average of the past two years. By subsector: manufacturing output grew 4.4%, utilities climbed 7.6%, and mining rose 2.3%. These are positive numbers—not crisis-level readings—but they reflect an economy in which output is sustained by export demand rather than by the kind of capital formation and domestic consumption that generate self-reinforcing growth cycles.

China’s full-year 2026 GDP growth is expected to remain in positive territory, driven by the export surge and infrastructure spending, but the Deloitte forecast notes that growth is “not being fueled by domestic demand”—meaning the economy is not generating inflationary pressure at home. That permits the PBOC to maintain a relatively stable interest rate environment, but it also means that any slowdown in export demand could quickly transmit into a broader growth deceleration with limited domestic offsets available.

The medium-term question for China’s economy in 2026 is whether the property market finds a floor before the export tailwind fades. The historical precedent for property-led downturns in emerging markets suggests the adjustment period is measured in years, not quarters.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

S&P 500 7000 Target: Wall Street’s Bullish Case for Year‑End 2026

EU Greenwashing Enforcement Hits New Peak with €1.2 Billion Fast‑Fashion Fine

India Economic Rise 2026: How the Subcontinent Toppled Japan

Sovereign Debt Crisis 2026: The ‘Lost Decade’ Is Already Here for 40 Nations

Crude Oil Price Rally June 2026: OPEC+ Extends Cuts, Targets $100

China Housing Market Turnaround: White‑List Model Stabilises Prices

US Sovereign Debt Risk 2026: CBO Projects $50 Trillion, Fitch Warns

BRICS De‑Dollarization Strategy Takes Shape with $15 Billion Local‑Currency Push

Digital Euro Cross‑Border Pilot Goes Live: What It Means for Banks

AI Impact on Wages 2026: Productivity Soars, Paychecks Stagnate

Global Economic Outlook June 2026: Trade Fragmentation Bites

SpaceX IPO 2026: Inside the $2 Trillion Valuation That Remade Wall Street

Kevin Warsh’s Regime Change: The Federal Reserve in the Age of War, Inflation, and Political Pressure

Private Credit Crisis 2026: $3 Trillion Shadow Market Faces Its Biggest Test

PwC China Partner Payouts Cut Amid Evergrande Audit Fraud

Broadcom Market Value Loss: Revenue Forecast Disappoints

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Here’s How Much It’ll Cost You to Be Part of SpaceX’s Record-Breaking $75 Billion IPO

Nasdaq Tumbles 4% as Chip and Memory Stocks Sink: A $1.2 Trillion Wipeout

How to Fix Pakistan’s Debt Economy: A Structural Blueprint

Smash Capital Leads $200M Funding for Allen Control Systems

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Grinding the Already Ground: Pakistan’s Inflation Crisis

Democrats Draw a Red Line Around Military AI — And the Pentagon Is Already Pushing Back

New Investment Super-Cycle: AI, Green Energy & Re-Shoring

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

Middle East Conflict Oil Prices: The $4 Surge Explained

The End of the Chatbot: Why OpenAI is Tearing Up Its Most Successful Product

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 months ago

Analysis4 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks5 months ago

Banks5 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025