Analysis

Ackman’s €55bn Gambit: Wall Street Reaches for the Soul of Music

Bill Ackman’s Pershing Square bids €55.75bn for Universal Music Group — a bold SPARC merger, NYSE relisting play, and activist masterstroke that could reshape global entertainment finance.

There is a particular kind of audacity that separates the truly great dealmakers from the merely wealthy ones. It is the ability to look at a €31 billion company, one that controls the recordings of Taylor Swift, Drake, Lady Gaga, and The Beatles’ entire back catalogue — and declare, publicly, with the full force of a non-binding term sheet, that the world has been catastrophically wrong about its value. Bill Ackman did exactly that on Tuesday morning, submitting a €55.75 billion proposal to the board of Universal Music Group that is simultaneously a takeover bid, a structural intervention, a corporate governance manifesto, and perhaps the most consequential single act in the history of music-industry finance.

The numbers alone are theatrical. Pershing Square’s cash-and-stock deal, worth approximately €55.8 billion ($64.4 billion), would see UMG shareholders receive a total of €9.4 billion in cash and 0.77 shares of new stock for each share currently held. That equates to roughly €30.40 per share — a 78% premium to last week’s closing price of €17.10. In a market still nursing tariff-induced vertigo, it reads less like a merger proposal and more like a declaration of war against misvaluation itself.

The Deal, Deconstructed: What Ackman Is Actually Proposing

Strip away the financial engineering and what emerges is a thesis of elegant simplicity: Universal Music Group is one of the finest businesses on the planet, systematically mispriced by structural noise. Pershing Square cited six specific factors it believes have depressed UMG’s stock: uncertainty over the Bolloré Group’s 18% stake; the postponement of a US listing; balance sheet underutilisation; the absence of a disclosed capital allocation plan; a failure of investors to credit UMG’s €2.7 billion Spotify stake in its valuation; and what Ackman termed “suboptimal” shareholder communications.

Each point is surgical. Each is addressable. Together they constitute not a diagnosis of a failing business — Ackman himself praised CEO Sir Lucian Grainge effusively — but a bill of indictment against the governance architecture surrounding an excellent one. “Since UMG’s listing, Sir Lucian Grainge and the company’s management have done an excellent job nurturing and continuing to build a world-class artist roster and generating strong business performance,” Ackman said, before pivoting: “UMG’s stock price has languished due to a combination of issues that are unrelated to the performance of its music business.”

Under the proposed structure, Pershing’s SPARC Holdings would merge with UMG, and the combined entity — incorporated as a Nevada Corporation — would be listed on the New York Stock Exchange. The cash component, funded through SPARC’s rights holders, committed debt financing, and proceeds from Pershing’s Spotify stake, is carefully calibrated. It is designed primarily to offer the Bolloré Group — holder of an 18.5% stake that has hung over UMG like a Gallic storm cloud since its 2021 Euronext Amsterdam listing — a clean exit.

Pershing Square said all equity financing would be backstopped by itself and its affiliates, with debt financing committed at signing, and expects the deal to close by end of 2026.

The proposed deal mechanics, summarised:

| Element | Detail |

|---|---|

| Total deal value | ~€55.75bn ($64.4bn) |

| Price per share | €30.40 (78% premium to last close) |

| Cash component | €9.4bn (€5.05/share) |

| Stock component | 0.77 shares of New UMG per UMG share |

| Vehicle | Pershing Square SPARC Holdings (SEC-registered SPARAC) |

| New listing | New York Stock Exchange |

| Target close | End of 2026 |

| Board refresh | Michael Ovitz proposed as chair; 2 Pershing Square directors |

Why Ackman Wants the World’s Biggest Music Machine

The superficial answer is that Ackman saw a bargain. UMG has lost 26% of its market value in the past 12 months and was valued at just €31.4 billion before Tuesday’s announcement — a staggering discount for a company that generates consistent double-digit earnings growth and sits at the absolute commanding heights of intellectual property capitalism.

But the deeper answer is structural. Ackman purchased 10% of UMG in 2021 through a deal with Vivendi at approximately €18.27 per share, making him an early believer in its potential. Since then, he has watched the share price grind lower despite the business performing admirably — revenues and earnings growing at 11% and 13% per year respectively, while the Amsterdam listing provided insufficient liquidity and suppressed institutional access for US investors unable to purchase non-US-listed securities.

This is, at its core, a thesis about listing arbitrage — the premium that New York capital markets attach to great businesses versus their European equivalents. The S&P 500 trades at roughly 20x forward earnings. Amsterdam’s AEX sits closer to 13x. For a business of UMG’s quality and growth trajectory, that gap represents tens of billions in unrealised value. Ackman intends to unlock it via relisting.

There is also the artist economy argument, which deserves more attention than it has received. The music industry’s economics have been fundamentally restructured by streaming. Spotify, Apple Music, and their successors have converted what was once a lumpy, piracy-damaged revenue model into something approaching a recurring subscription business. UMG, home to global artists including Taylor Swift, Drake, and Lady Gaga, was spun out of Vivendi and listed on Euronext Amsterdam in 2021 with an initial valuation of €46 billion — and the business case for premium valuations has only strengthened since as streaming penetration has deepened globally. The irony is that UMG has executed precisely the transformation it promised, and the market has responded with indifference.

The Blank-Cheque Masterstroke: SPARC, Not SPAC

Much will be written conflating this deal with the SPAC boom of 2020-21 — that frothy, ultimately discrediting period of blank-cheque company proliferation that ended in regulatory scrutiny and spectacular write-downs. The conflation is understandable but wrong.

Pershing Square SPARC Holdings is technically a SPARAC — a Special Purpose Acquisition Rights Company — a vehicle Ackman designed precisely to avoid the structural defects of its SPAC predecessor. Where traditional SPACs forced investors to commit capital before a deal was identified, SPARAC rights holders only invest once a specific target is announced and they have full information to evaluate it. There is no dilutive warrant structure. There is no forced redemption dynamic. The optionality resides entirely with the investor, not the promoter.

It is, in essence, a rights-based acquisition vehicle that aligns incentives in ways the original SPAC format catastrophically failed to do. The SEC registered SPARC Holdings four years ago, and Ackman has been patient — waiting, as great investors do, for a target worthy of the vehicle’s ambition. Universal Music Group, one suspects, was always the destination.

Pershing’s move comes after UMG last month delayed a plan for a US listing, walking back on an agreement with Pershing, which had exercised its right to request a US offering and had argued a New York listing would boost UMG’s share price and liquidity. That reversal appears to have been the proximate trigger. When the elegant solution — a consensual secondary listing — was blocked, Ackman reached for the bolder instrument: full acquisition.

Strategic and Cultural Implications for the Music Industry

The implications extend far beyond the balance sheet. Universal Music Group is not merely a large corporation; it is, in important respects, the custodian of recorded culture. It controls the catalogues of artists spanning a century of popular music — from The Beatles to Bad Bunny — and its decisions about licensing, royalties, artificial intelligence, and streaming economics ripple through the entire creative ecosystem.

Ackman’s proposed governance changes are, on balance, more activist than revolutionary. He wants Michael Ovitz, the former CAA co-founder and Walt Disney president, to chair the board, alongside two Pershing Square representatives as directors. Ovitz’s reputation in talent representation and entertainment strategy is formidable; his appointment would signal a reorientation toward artist relationships and content strategy, not merely financial engineering.

The AI dimension cannot be overstated. Music labels are currently engaged in a defining legal and commercial battle over the use of their catalogues to train AI systems. UMG has been among the most aggressive in asserting rights — suing AI audio companies and demanding licensing frameworks. A NYSE-listed UMG, with a US activist shareholder structure and American governance norms, will likely pursue this battle with greater institutional firepower and investor support. American capital markets tend to reward IP maximalism. The implications for artists, AI companies, and streaming platforms are profound.

Key stakeholders and their likely positions:

| Stakeholder | Position | Strategic Implication |

|---|---|---|

| Bolloré Group (18.5%) | Seeking exit; cash component designed for them | Deal cannot proceed without their support |

| Vivendi (~10%) | Complex position as ex-parent | Likely supportive if premium maintained |

| Sir Lucian Grainge (UMG CEO) | Praised by Ackman; contract renegotiation proposed | Retention critical; may seek enhanced terms |

| UMG Artists | No direct vote; indirect interest in stability | NYSE listing may attract greater US investor coverage |

| Spotify | UMG holds €2.7bn stake | Complex licensing interdependence; deal may reassess |

Financial Engineering and Market Reaction

The market’s immediate verdict was unambiguous. UMG shares jumped as much as 28% in early Amsterdam trading following the announcement, before paring gains to trade approximately 15% higher. The stock had been down roughly 11% year-to-date entering Tuesday. Shares of Vivendi and the Bolloré Group were both higher — Vivendi up 11% and Bolloré up 6.3% — a clear signal that the broader conglomerate structure around UMG views this as a liquidity event long overdue.

The valuation case is compelling when stress-tested. UMG generates approximately €10 billion in annual revenues with EBITDA margins expanding toward the mid-twenties as streaming cost structures mature. Apply the multiple of peers — compare it to, say, Live Nation’s trading multiples or the private market transaction comps for music IP — and €30.40 per share begins to look not generous but fair. The 78% premium to a depressed share price does not, in this analysis, represent aggressive overpayment. It represents correction of a persistent anomaly.

The Spotify stake alone — valued at approximately €2.7 billion — represents nearly 9% of UMG’s current market capitalisation and has never been adequately reflected in analyst valuations. In the transaction structure, its monetisation becomes explicit rather than embedded and ignored.

One structural observation deserves attention: 17% of UMG shares will be bought back and cancelled as part of the transaction, concentrating ownership in the new entity while reducing dilution for remaining shareholders. This is the quiet architecture of a deal designed to maximise value in the hands of long-term holders rather than short-term arb traders.

Risks, Regulatory Roadblocks, and Counter-Moves

This is where intellectual honesty demands a departure from the deal’s considerable charms.

The Bolloré problem is real, and it is large. Nicolas Marmurek, an analyst at M&A specialists Square Global, noted bluntly: “Unless Bolloré supports the move, the proposal looks very much dead from the start. We doubt Bolloré will accept such terms.” The Bolloré Group is not a passive portfolio investor; it is a French conglomerate with its own regulatory entanglements, a controlling patriarch in Vincent Bolloré, and a history of strategic opacity. The cash component — €9.4 billion — is designed to offer them an exit. Whether they want an exit, on these terms, at this moment, is the $64 billion question. Literally.

Regulatory complexity compounds this. A transaction of this scale, involving a Dutch-listed company with French shareholders, a US acquisition vehicle, and a proposed NYSE relisting, traverses at least three major jurisdictions and regulatory regimes. EU merger control, Dutch financial market authority oversight, SEC registration requirements, and French market regulator AMF scrutiny of the Bolloré/Vivendi stake all represent genuine friction — not necessarily fatal, but time-consuming and expensive. Ackman’s year-end target may prove optimistic.

There is also the question of what this deal does to competitive dynamics. A US-listed, Pershing Square-controlled UMG would face heightened scrutiny in its licensing and AI negotiations — both from counterparties emboldened by antitrust concern and from legislators increasingly attentive to Big Culture’s market power. Warner Music Group and Sony Music, UMG’s two major competitors, will not be passive observers. Both have the scale and relationships to complicate regulatory approval processes.

Finally — and this is rarely discussed — there is the artist dimension. Major recording artists command extraordinary negotiating leverage in 2026. The consolidation of ownership around activist shareholder structures has historically produced cost discipline that artists and their managers experience as pressure on royalty terms and advance commitments. Any perception that a Pershing Square-controlled UMG would prioritise financial returns over artist relationships could accelerate the movement toward independent labels, direct licensing, and artist-owned catalogues that has already begun reshaping the industry’s edges.

My Expert Opinion: The Bigger Picture for Global Entertainment and Capital Markets

Let me be direct: this is one of the most interesting large transactions attempted in global capital markets in years, and it is more likely to succeed than the sceptics assume — but for reasons that extend beyond the deal’s immediate mechanics.

Bill Ackman is not primarily a music industry investor. He is a capital allocation activist who identified, five years ago, that the world’s most valuable IP business was being systematically underpriced by European listing constraints and governance ambiguity. The SPARC vehicle, the Lucian Grainge relationship, the Bolloré exit structure — none of this is improvised. This is the end of a long-form strategic play, executed with the patience and deliberateness that distinguishes Ackman’s best campaigns from his more turbulent episodes.

The broader thesis — that great businesses listed in small-liquidity markets are systematically undervalued relative to NYSE-listed equivalents — is not just true; it is increasingly obvious to sophisticated allocators globally. Arm Holdings’ relocation to Nasdaq, the parade of European companies exploring dual listings, the premium that US institutional capital demands for domestically-listed assets — all of these are manifestations of the same phenomenon Ackman is now monetising at scale.

For the music industry specifically, a successful UMG-Pershing transaction would have generational consequences. It would cement music IP as a mainstream institutional asset class, driving capital allocation toward royalty funds, catalogue acquisitions, and artist-equity structures at a scale that would transform the economics of every recording artist signed to a major label. The money that follows a NYSE-listed, S&P-eligible Universal Music Group into the sector would dwarf the private equity inflows of the past decade.

And on AI: a better-capitalised, US-governance-aligned UMG will be a more formidable adversary for technology companies seeking to licence or circumvent music rights. That is good for artists, good for label economics, and potentially very good for the broader case that creative IP deserves robust legal protection in the generative AI age.

Forward-Looking Outlook: Three Scenarios

Scenario A — The Deal Closes (Probability: ~45%): Bolloré agrees to the cash exit terms; UMG’s board, satisfied with the governance concessions and premium, recommends acceptance; regulatory approvals are secured by Q3. New UMG lists on NYSE in December 2026, immediately entering institutional indices, attracting US-oriented fund flows, and trading at a multiple that vindicates Ackman’s thesis. The 0.77-share component ultimately prices above the implied €30.40 equivalent. Ackman books one of the great activist trade completions.

Scenario B — Partial Success (Probability: ~35%): Bolloré refuses the exit terms; Ackman’s public pressure, however, forces UMG’s board to commit to a US listing without the full merger. A secondary NYSE listing proceeds in 2027, share price recovers meaningfully, and Pershing’s existing stake is vindicated without the complexity of full acquisition. Messier, but profitable.

Scenario C — Collapse (Probability: ~20%): Bolloré, exercising shareholder veto power, rejects the terms. Regulatory pushback in France and the Netherlands proves intractable. Ackman withdraws; UMG shares give back their premium; the saga continues. Even in this scenario, the public articulation of UMG’s undervaluation likely places a floor under the stock that did not exist before Tuesday morning.

In all three scenarios, one thing is clear: the world’s most valuable music business will never be invisible again.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

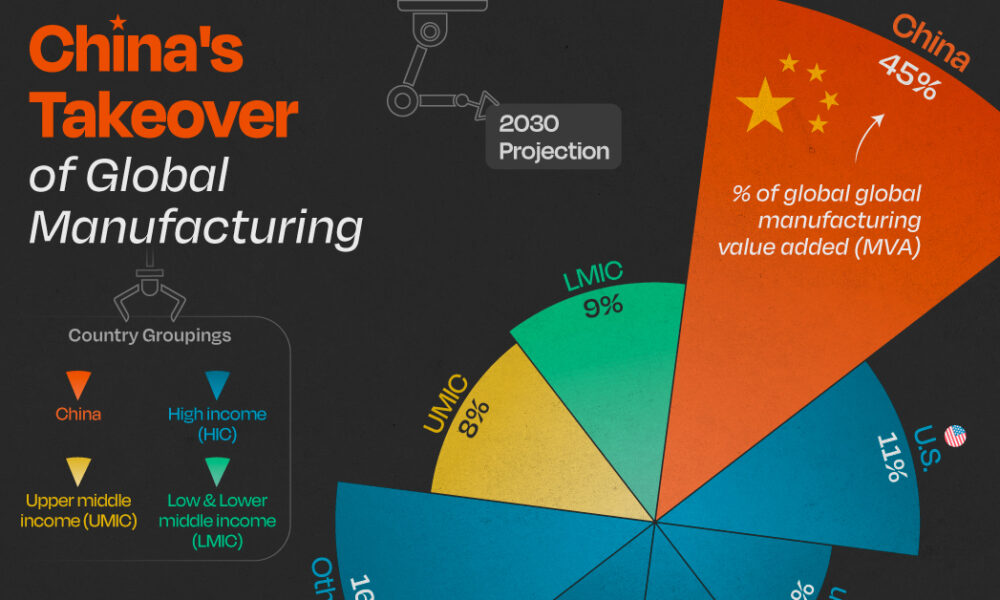

China’s exports have been the good-news story in an otherwise mixed economic picture. They’re not just holding up; through the first four months of 2026 they were running about 14% to 15% above the same period a year earlier, according to figures cited by the US-China Economic and Security Review Commission and Vanguard’s economic outlook. That’s the kind of number that would normally signal a healthy economy. The complication is what’s happening underneath it.

A growth model showing its age

Manufacturing capacity utilization fell to 73.9% in early 2026 — near a decade low outside of the pandemic shutdowns, per the Commission’s bulletin. That’s the tell. China is producing and shipping more, but a growing share of its industrial base is running under capacity, which points to a structural mismatch: the country’s manufacturing engine has outgrown both its domestic consumption and, increasingly, what the rest of the world is willing to absorb without pushback.

Goldman Sachs Research, in a report cited by Goldman Sachs’ own analysis, forecasts 4.8% real GDP growth for 2026 — above consensus expectations of 4.5% — driven substantially by continued export strength and a softening drag from the property downturn. But that same report flags the labor market as a genuine weak spot: hiring, measured across a weighted average of PMI employment sub-indexes, is at its most depressed level in a decade outside Covid, and urban nominal wage growth slowed to just 3.8% year-on-year in Q3 2025.

Why Beijing isn’t reaching for stimulus

Given the export strength, one might expect policymakers to feel less urgency about consumption-side stimulus. That’s roughly what’s happening — and it’s a deliberate choice, not an oversight. Xi Jinping’s government remains committed to dominating high-value manufacturing, which means comprehensive fiscal stimulus aimed at consumers remains unlikely even as domestic demand stays soft, according to the Commission’s bulletin.

The People’s Bank of China is expected to hold its policy rate steady through the rest of the year, preferring targeted structural tools over a broad-based rate cut, per Vanguard’s forecast. That’s a notably cautious stance given how weak the property sector remains — property investment indicators are down 50% to 80% from their 2020–21 peaks, and a “meaningful domestic-demand turnaround remains elusive,” in Vanguard’s own words.

The regulatory push to keep capital at home

Two moves by Chinese regulators in mid-2026 point to where Beijing’s real priority sits: keeping household savings and private capital funneled toward domestic industrial policy rather than flowing overseas. New rules taking effect July 1 restrict outbound investment that could be used to export restricted technology or expertise under the guise of ordinary capital flows, with violations carrying fines, visa restrictions and industry blacklisting, according to the Commission’s bulletin. The regulations follow Beijing’s move to block the founders of AI firm Manus from completing a sale to Meta, even after the company had relocated its headquarters from China to Singapore — a signal that Beijing is willing to reach across borders to keep promising tech assets tethered to domestic or Hong Kong listings.

The currency and trade angle

Goldman’s team makes an out-of-consensus call worth flagging: it expects China’s current account surplus to rise to 4.2% of GDP in 2026, up from 3.6% in 2025, while the broader analyst consensus surveyed by Bloomberg expects a decline to 2.5%. The divergence comes down to export resilience — falling export prices are making Chinese goods more competitive even as the yuan is expected to appreciate slightly, with export-price inflation in dollar terms forecast to turn positive, rising to 0.7% from -2.7% the prior year.

The bottom line

China’s economy in 2026 is a study in contrasts: robust headline export growth sitting on top of underutilized factories, a weak labor market, and a property sector still in its fifth year of decline. The World Bank’s own baseline, published in its country program materials, projects growth moderating toward 4.0% by 2026 — a more conservative read than Goldman’s. Either way, the consensus across forecasters is the same: exports are carrying more of China’s growth than is healthy for the long run, and Beijing’s policy choices this year suggest it’s betting on technological dominance to eventually solve the demand problem, rather than opening the stimulus taps to solve it directly.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

There’s a number that keeps showing up in every conversation about Pakistan’s economy, and it keeps getting bigger: circular debt. As of early July 2026, the gas sector’s share of that debt alone has topped Rs 3.44 trillion, and Islamabad has missed a deadline the IMF set for tariff reforms meant to arrest the slide, according to Dawn.

What circular debt actually is, and why it won’t go away

Circular debt is the chain of unpaid obligations that builds up when the price consumers pay for electricity or gas doesn’t cover what it actually costs to produce and deliver it. Someone in the chain — a power producer, a gas utility, a state-owned enterprise — ends up carrying an IOU, and that IOU gets passed down the line. Earlier this year, IMF officials pressed Pakistan on exactly this dynamic, questioning the government’s plan to zero out gas-sector circular debt, according to Aaj English. At the time, officials said around Rs 150 billion remained payable to companies including Oil and Gas Development Company Limited and Pakistan Petroleum Limited.

Islamabad’s proposed fix included a Rs 5-per-unit levy on gas, dividends from state-owned companies redirected toward debt reduction, and the sale of 35 LNG cargoes annually on the international market. The IMF, per that same reporting, raised pointed questions about whether the plan was actually viable.

The commitments Pakistan has already made

Under its Extended Fund Facility, Pakistan has committed to capping circular debt growth at Rs 300 billion for FY2027 and cutting power-sector subsidies from 0.7% of GDP to 0.6%, according to details reported by ProPakistani. The government has also shifted Nepra’s annual tariff-rebasing cycle from July to January, and Ogra now revises gas tariffs twice a year instead of once.

Structurally, some of this is working. The IMF’s own review in May 2026 credited Pakistan with a primary fiscal surplus of 1.6% of GDP for FY26, broadly in line with program targets, and noted gross reserves had climbed to $16 billion by end-December, up from $14.5 billion six months earlier, according to the IMF’s own press release. That progress unlocked roughly $1.1 billion under the EFF and $220 million under a parallel climate-resilience facility, bringing total disbursements under the two arrangements to about $4.8 billion.

Where the fault lines actually are

The uncomfortable part of this story, laid out by commentary reported in The Hans India, is that revenue targets get IMF scrutiny with great precision, while structural reform of loss-making public enterprises — Pakistan International Airlines and Pakistan Steel Mills chief among them — moves far more slowly. Those enterprises’ losses are absorbed by the national exchequer through subsidies, guarantees, and debt restructuring year after year, and privatization plans keep slipping because the political cost of confronting them is high.

Distribution company inefficiency compounds the problem. In FY25, Discos posted Rs 265 billion in losses, an improvement on FY24’s Rs 276 billion but still a substantial drag, according to Geo News, with Quetta, Peshawar and Hyderabad among the worst-performing utilities.

What happens if the pattern holds

Pakistan’s debt-to-GDP ratio sits between 70% and 80% as of 2026, according to Wikipedia’s economic summary, with debt servicing occasionally consuming two-thirds of government spending. That’s the backdrop against which every circular-debt conversation happens: there is very little fiscal room left to absorb another missed deadline.

The missed gas tariff deadline doesn’t automatically trigger a program breakdown — Pakistan has weathered similar friction points before during its current EFF arrangement. But with the IMF’s own documentation showing persistent concern about the credibility of debt-reduction plans, and with global energy prices still elevated in the aftermath of the Iran war, the margin for further slippage is thin. The next review will likely hinge less on the rhetoric around reform and more on whether the Rs 5 levy and LNG cargo sales actually show up in the numbers.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Malaysia’s government has declared 2026 a year of “execution” and “discipline” as the Anwar Ibrahim administration races to deliver on the 13th Malaysia Plan (RMK13) ahead of elections that could come as early as February 2028, according to Fortune’s interview with economy minister Akmal Nasrullah Mohd Nasir.

A Strong Base to Build From

Malaysia’s economy grew 4.9% in 2025 following 5.1% growth the year before, with unemployment falling to 2.9% — the lowest in a decade — and the ringgit trading at its strongest level in five years. HSBC’s ASEAN economist Yun Liu forecasts 4.6% growth for 2026, citing strength in electrical equipment manufacturing, tourism, and sound government policy, while Nomura economists have projected an even more bullish 5.2%, pointing to infrastructure spending under RMK13.

The ASEAN+3 Macroeconomic Research Office (AMRO) projects growth moderating slightly to 4.6% from an estimated 4.9% in 2025, describing Malaysia’s performance as reflecting its “entrenched position in global semiconductor and electronics value chains” and the broader global tech upcycle, according to AMRO’s assessment of Malaysia’s investment upcycle.

Navigating Washington Without Picking Sides

Malaysia’s trade relationship with the US has been turbulent. Washington imposed 25% tariffs on Malaysian goods in April 2025, rattling the country’s export-led economy, before a deal reduced US duties to 19% in exchange for Malaysia lowering tariffs on select American products, with exemptions carved out for aviation components and electrical equipment. Malaysia’s trade hit a record high of more than 3 trillion ringgit (roughly $780 billion) last year despite the friction.

Deputy finance minister Liew Chin Tong has framed Malaysia’s positioning explicitly around neutrality: the country is “not China, not the US,” a stance he argues gives Malaysia a strategic advantage in both geopolitical and supply-chain terms, according to Fortune’s reporting from the Forum Ekonomi Malaysia summit.

Capital Is Flowing In — From Everywhere

Malaysia recorded 22.8 billion ringgit (about $5.8 billion) in foreign direct investment in the first quarter of 2026, a 6.0% year-on-year increase, moderating from the prior quarter’s 48.7% surge. Inflows into information and communication technology services remained particularly strong, with China, Hong Kong, and Singapore serving as the primary capital sources, according to McKinsey’s Southeast Asia quarterly economic review. Bank Negara Malaysia has held its policy rate steady following a pre-emptive 25 basis-point cut in July 2025, with headline inflation projected to average just 2.0% in 2026.

The Long Game: Semiconductors, Rare Earths, and Nuclear Power

Beyond RMK13’s near-term targets, Malaysian officials are positioning the country’s industrial strategy around decades, not years. Minister Akmal has reiterated commitments to eliminate coal use by 2044 and reach net zero by 2050, while confirming Malaysia is actively “exploring the potential” of nuclear power to meet the energy demands of its expanding data-center and semiconductor sectors. AMRO’s structural policy guidance urges Malaysia to develop domestic semiconductor and rare-earth capabilities as a hedge against ongoing US-China “geoeconomic fracturing,” positioning the country as a trusted neutral hub for global manufacturers diversifying away from concentrated exposure to either superpower.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

China Economy 2026: Export Growth Masks Manufacturing Overcapacity

Pakistan Iran-US Ceasefire Mediation 2026: Diplomatic Gains, Economic Risks

Pakistan Circular Debt Crisis 2026: IMF Deadline Missed, Rs 3.44 Trillion

Indonesia Russian Oil Imports 2026: Why Jakarta Is Diversifying Crude Supply

Russia Bans Diesel Exports 2026: Global Fuel Market Impact Explained

Gulf Sovereign Wealth Funds Hit Record $53.9B in H1 2026 Despite Iran War

America’s Workers Are Vanishing From the Labor Force — And It’s Not the Usual Reasons

ASEAN+3 Enters 2026 From a Position of Strength — But Two Storms Are Building Offshore

US Tariff Investigation 2026: 60 Countries, Forced Labor Claims and the EU Trade Fight

UK Digital Identity Framework 2026: The £5bn Plan to Reshape Financial Verification

The Money Is Drying Up: How US Pressure Is Choking Off Russia-China Payment Channels

Indonesia GDP Growth 2026: 5.61% Expansion Marks Fastest Pace in Three Years

Singapore Makes Its Move to Become Asia’s Precious-Metals Capital

Malaysia Bets Its 2026 on “Execution” — And the Semiconductor Upcycle Is Doing the Heavy Lifting

Top 20 PSX Stocks for Investment in 2027: Your Complete Guide to Pakistan’s Best Investment Opportunities

Investors Pile Into Bullish Dollar Bets as ‘US Exceptionalism’ Trade Returns

Carry Trade Unwind 2026: How the Yen’s Snapback Triggered a Global Margin Call

Pakistan Textile Body Welcomes FY27 Budget, Seeks FTR

Japan’s Nikkei Scales Record Peak as AI Shares Track US Chip Rally

Why China’s Demand Stimulus Still Isn’t Working

Grinding the Already Ground: Pakistan’s Inflation Crisis

JPMorgan Cuts Anthropic AI Access in Hong Kong

Weak Demand at Treasury Auctions Is Quietly Rattling Bond Investors

China Tungsten Export Curbs: Is Japan’s AI Chip Supply at Risk?

Xponential Fitness Franchise Lawsuit: The $3.97M Judgment

SpaceX IPO opens door for retail savers via X Money

SpaceX IPO: Musk Raises $75bn in History’s Largest Listing

Pakistan’s FY27 Budget Bets on 4% Growth While Defence Spending Crosses Rs3 Trillion

-

Markets & Finance6 months ago

Markets & Finance6 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis5 months ago

Analysis5 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis5 months ago

Analysis5 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Analysis5 months ago

Analysis5 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Banks6 months ago

Banks6 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment6 months ago

Investment6 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Global Economy6 months ago

Global Economy6 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy6 months ago

Global Economy6 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025