Analysis

Asia’s Next Economic Leap Won’t Come From More Tech — It Will Come From Better Leaders

As Asia’s GDP growth cools to 4.4% in 2026, the continent’s greatest untapped resource isn’t artificial intelligence or green energy. It’s the human judgment required to deploy them wisely.

Key Data at a Glance

| Economy | GDP Growth 2026 | Source |

|---|---|---|

| Asia-Pacific | 4.4% | UN WESP 2026 |

| China | 4.8% | Goldman Sachs |

| India | 6.6% | UN |

| Vietnam & Philippines | 6%+ | Asia House Outlook 2026 |

In a gleaming conference hall in Singapore last January, the chief executive of one of Southeast Asia’s largest conglomerates leaned across the table and said something that stopped me mid-note. “We have the tools,” he said quietly. “We’ve always had the tools. What we’ve lacked — and what no algorithm can give us — is the wisdom to know which door to open with them.” He wasn’t being philosophical. His company had spent $400 million on a digital transformation program over three years. Adoption was near-total. Results were almost nonexistent.

His story is not a cautionary tale about technology. It is, at its core, a story about leadership — and it is one being repeated, with varying degrees of pain, from Jakarta to Shenzhen to Mumbai. As Asia’s GDP growth eases to 4.4% in 2026 from 4.9% in 2025, according to the United Nations’ World Economic Situation and Prospects report, the deceleration has reignited familiar conversations about investment, innovation, and demographic dividends. But the more uncomfortable conversation — the one that will ultimately determine whether this region realizes its extraordinary potential — is about leadership as the essential, irreplaceable catalyst for harnessing tech in Asia.

The central argument here is simple, if politically inconvenient: Asia already has abundant technology. What it often lacks is leadership capable of deploying it with precision, purpose, and strategic clarity. The continent’s next great economic leap — its most consequential since the manufacturing revolutions of the late twentieth century — will not be triggered by another wave of AI investment or another cluster of smart cities. It will come from a new generation of leaders who understand that technology creates value only when a human hand is guiding it toward the right ends.

The Slowdown That Tells the Real Story: Asia Economic Growth 2026

Numbers, by themselves, rarely tell the full story. But the 2026 Asian GDP projections carry an important subtext that too many analysts are missing. On the surface, China’s 4.8% growth projection, powered largely by a surging export machine, looks respectable. India’s 6.6% expansion, fueled by domestic consumption and a demographic engine that most of the world can only envy, looks impressive. And Vietnam and the Philippines, both surpassing the 6% threshold according to the Asia House Annual Outlook 2026, offer genuine bright spots in a global economy still navigating the aftershocks of geopolitical fragmentation.

Yet the aggregate slowdown — a full half-percentage-point drop in Asia’s collective growth rate — is not simply the product of external shocks or cyclical headwinds. It reflects something more structural: the growing gap between the technology these economies have acquired and the institutional and leadership capacity to translate it into sustained, broad-based productivity gains. Technology adoption, as the IMF’s landmark analysis of Asia’s digital revolution made clear, is a necessary but emphatically insufficient condition for growth. The missing ingredient is harnessing tech in Asia at the leadership layer — the place where strategy, culture, and judgment intersect.

Consider the contrast: Japan and South Korea, two of Asia’s most technologically advanced economies, have struggled for years to convert world-class R&D spending into commensurate productivity growth. Both rank highly on standard innovation indices. Both lag on measures of organizational agility and leadership adaptability. This is not a coincidence. It is a pattern — one that stretches from Tokyo boardrooms to state-owned enterprises in Beijing to family-controlled conglomerates across Southeast Asia.

“Technology is the new electricity. Every economy in Asia has access to the grid. But the question that determines winners from also-rans is this: who knows how to wire the building?”

— Senior economic adviser, Asian Development Bank, 2025

Technology Leadership Asia: What “Harnessing” Actually Means

The word “harnessing” does real intellectual work in this conversation, and it deserves unpacking. It does not mean simply deploying AI tools or purchasing enterprise software. Harnessing technology — in the sense that distinguishes the leaders who create value from those who accumulate costs — involves three distinct leadership capacities that most corporate governance frameworks and most public policy discussions systematically ignore.

The first is contextual intelligence: the ability to understand which technologies are suited to an organization’s specific competitive context, workforce culture, and long-term strategic objectives. Asia’s diversity — spanning democratic market economies, authoritarian state-capitalist systems, middle-income manufacturing hubs, and high-income financial centers — means there is no universal playbook. A leader who blindly imports Silicon Valley frameworks into a Taiwanese semiconductor firm, or a Jakarta fintech startup, is not harnessing technology. They are gambling with it.

The second is organizational translation: the often underappreciated skill of remaking internal structures, incentives, and cultures so that technological investments actually change behavior at scale. The World Bank’s East Asia and Pacific Economic Update has documented the persistent gap between technology adoption rates and productivity outcomes across the region. That gap is, almost without exception, an organizational and leadership failure, not a technological one. Tools do not transform companies. Leaders do — by building the conditions under which tools become embedded habits.

The third is ethical navigation: the capacity to make hard choices about AI deployment, data governance, and automation’s distributional consequences in ways that maintain public trust and social license to operate. This is, increasingly, not a soft skills issue. It is a hard commercial and geopolitical one. Leaders who fail at it — whether running a ride-hailing platform in Indonesia or a state-backed AI initiative in China — face regulatory backlash, talent flight, and reputational damage that erodes the very productivity gains they sought.

The Leadership Gap: Where Asia’s Real Vulnerability Lies

None of this is to suggest that Asia lacks talented individuals. The region produces an extraordinary pool of engineers, data scientists, and technical specialists. What it consistently struggles to produce — at scale, across sectors, and across the public-private divide — is the integrated leader: the executive or policymaker who combines deep technological literacy with strategic vision, human judgment, and the organizational courage to drive change against institutional inertia.

The reasons for this gap are partly historical and partly structural. Many of Asia’s most powerful institutions — state enterprises, family conglomerates, hierarchical bureaucracies — were built for a world of incremental optimization, not adaptive transformation. They rewarded compliance over creativity, seniority over capability, and risk avoidance over intelligent experimentation. These cultural and structural patterns do not dissolve simply because a company installs a new AI platform. They require deliberate, sustained leadership intervention to change.

The Economist’s coverage of Asian business has repeatedly highlighted a paradox: the very organizational cultures that enabled Asia’s first great economic leap — discipline, collective cohesion, long-term orientation — can become liabilities in environments that reward speed, iteration, and decentralized decision-making. The tech-driven productivity gains that Asia’s next chapter demands require precisely those latter qualities. Bridging that gap is, fundamentally, a leadership challenge.

Case Studies in Technology Leadership Asia: Who Is Getting It Right

India: The IT-to-AI Pivot — Leadership as the Differentiator

India’s 6.6% growth story in 2026 is widely attributed to consumption and demographic tailwinds. But behind the headline number lies a more instructive story about leadership transformation in the technology sector. Firms like Infosys and Tata Consultancy Services have spent the last three years not simply adding AI capabilities, but systematically rebuilding their leadership pipelines to produce executives who can bridge technical expertise and strategic client partnership.

The result is not just revenue growth — it is a qualitatively different kind of value creation, moving Indian IT firms up the global value chain in ways that pure engineering investment never could. The lesson is direct: tech-driven productivity in Asia accelerates when leadership development is treated as a core strategic investment, not an HR function.

Vietnam: State Leadership in a Transition Economy

Vietnam’s consistent above-6% growth reflects something more interesting than FDI attraction. It reflects deliberate government leadership in managing a complex economic transition — from low-cost assembly to higher-value manufacturing — without sacrificing the social stability and investor confidence that underpin that growth.

Vietnamese policymakers have, often quietly and without fanfare, made sophisticated decisions about which technology partnerships to pursue, which industrial clusters to prioritize, and how to sequence workforce upskilling alongside automation investment. This is harnessing tech in Asia at the policy level — and it stands in instructive contrast to economies that have adopted similar technologies with far less coherent strategic intent, generating disruption without corresponding value creation.

China: Export-Tech at Scale — and the Translation Gap That Remains

China’s 4.8% growth, driven significantly by its formidable export engine, represents a genuine achievement in technology deployment at scale. Chinese firms in electric vehicles, solar manufacturing, and industrial robotics have moved from technology followers to global leaders in less than a decade.

Yet even here, the leadership question reasserts itself. The domestic productivity challenge — converting technological capability into broad-based efficiency gains across a vast and heterogeneous economy — remains formidable. Financial Times analysis of Asian growth patterns has consistently noted the divergence between China’s frontier technology companies and the much larger universe of firms still struggling with basic digital transformation. Bridging that divide requires leadership capacity, not more technology investment.

The Asian Innovation Economy: Rethinking What “Innovation” Requires

The dominant narrative about the Asian innovation economy — the one repeated at Davos panels and in WEF white papers — focuses on inputs: AI investment, patent filings, university research budgets, startup ecosystems. These inputs matter. But they have a tendency to crowd out the harder conversation about the organizational and leadership conditions that determine whether innovation translates into economic value.

Consider a comparison that illuminates the point. South Korea and Taiwan both have world-class semiconductor industries. Both spend heavily on R&D relative to GDP. Yet their innovation outcomes diverge significantly when you look beyond the flagship firms — Samsung, TSMC — to the broader economic ecosystem. The difference lies substantially in leadership quality and organizational culture in the second and third tier of each country’s industrial base.

Technology diffusion — the spread of innovation-derived productivity gains across an economy — is fundamentally a leadership problem. It happens when leaders at every level of an organization understand what new tools make possible and have the authority, incentives, and capability to act on that understanding.

Five Leadership Strategies for Harnessing Tech in Asia

- Invest in “bilingual” leadership. Develop executives who speak both the language of technology and the language of business strategy — people who can translate between engineering teams and boardrooms without losing meaning in the process.

- Redesign incentive structures. Align performance metrics and reward systems with innovation and adaptive risk-taking, not just operational efficiency and hierarchical compliance. This is the most consistently overlooked lever in Asia’s corporate governance toolkit.

- Build adaptive learning cultures. Create institutional environments where failure is analyzed rather than punished, and where experimentation is treated as a legitimate strategic method, not an aberration from the plan.

- Anchor technology decisions in human outcomes. Require every significant technology investment to be evaluated not just on cost and capability, but on its implications for workers, communities, and the public trust that underpins long-term social license.

- Invest in public-sector leadership capacity. In most Asian economies, government plays an active role in shaping industrial and technology strategy. The quality of public-sector leadership — its technological literacy, strategic coherence, and adaptive capacity — is therefore central to national competitiveness.

Policy Implications: Leadership as Infrastructure

If the argument above is correct — and the evidence increasingly suggests it is — then the policy implications are significant and, in some respects, counterintuitive. The conventional policy response to economic deceleration in Asia focuses on macroeconomic levers: interest rates, fiscal stimulus, trade policy, and technology investment incentives. These tools remain necessary. But they are insufficient if they are not accompanied by equally deliberate investment in the leadership infrastructure that determines whether technology creates value or merely creates costs.

What does leadership infrastructure look like in practice? It means education systems that prioritize adaptive thinking, ethical reasoning, and cross-disciplinary integration alongside technical training. It means corporate governance reforms that create accountability for leadership quality and succession planning. It means public-sector talent strategies that attract individuals capable of navigating the intersection of technology policy, economic strategy, and social impact.

And it means, frankly, a willingness among policymakers across Asia to acknowledge that the leadership deficit — not the technology deficit — is the binding constraint on the region’s next phase of growth. This is not a comfortable message for governments and business elites that have built their legitimacy on delivering technological progress. It is considerably easier to announce a new AI national strategy or a smart city initiative than to undertake the slow, difficult, institution-by-institution work of building better leaders. But ease and importance are not the same thing.

Asia’s Next Economic Leap: The Human Equation

There is a particular kind of optimism that Asia inspires — not the naive optimism of those who mistake dynamism for destiny, but the earned optimism of those who have watched this region repeatedly confound skeptics and rewrite economic history. That optimism remains warranted in 2026. The fundamentals — a young and growing population in South and Southeast Asia, deepening regional integration, expanding middle classes, and genuine world-class technological capability in multiple countries — are real. Asia’s next economic leap is not a fantasy. It is a genuine possibility.

But the path to that leap runs directly through the leadership question. The region’s most consequential investment in 2026 is not in another data center or another AI research lab — though both matter. It is in the development of leaders who can look at the extraordinary technological resources now available to Asian firms and governments and ask, with clarity and courage: What problem are we actually trying to solve? Who benefits? What do we need to change about ourselves to make this work?

Those are human questions. They always have been. The technology changes. The questions don’t. And Asia’s future — its extraordinary, still-unwritten future — will be determined by how well its leaders learn to answer them.

A Call to Action for Asia’s Policymakers and Business Leaders

The window for building leadership infrastructure at scale is open — but it will not remain open indefinitely. Three immediate steps deserve priority attention:

- Commission independent leadership capability audits in your organizations, measuring not just technical literacy but adaptive capacity and strategic judgment.

- Reform executive education to prioritize interdisciplinary thinking, ethical reasoning, and cross-cultural leadership alongside functional expertise.

- Elevate the leadership question in national technology strategies — not as a footnote to AI investment plans, but as a primary pillar of economic policy.

The technology is ready. The question is whether you are.

Sources & References

- UN World Economic Situation and Prospects 2026 — United Nations DESA (DA 94)

- China’s Economy Expected to Grow in 2026 Amid Surging Exports — Goldman Sachs (DA 92)

- Asia House Annual Outlook 2026 — Asia House (DA 70+)

- Asia’s Digital Revolution — IMF Finance & Development (DA 93)

- East Asia and Pacific Economic Update — World Bank (DA 93)

- Asia Coverage — The Economist (DA 92)

- Asia-Pacific — Financial Times (DA 93)

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

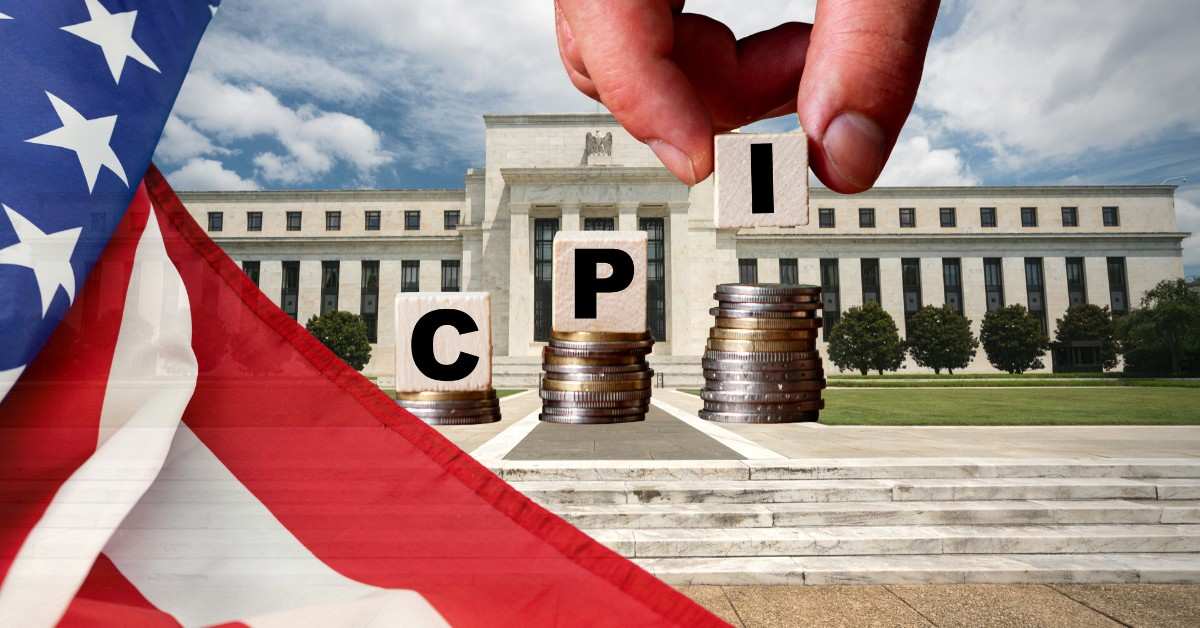

At 8:30 AM Eastern on report days, the trading floors of Lower Manhattan go completely silent. Traders stare at their Bloomberg terminals, waiting for a single data release that dictates the cost of capital for the entire global economy. The latest US CPI report has arrived, and it has violently disrupted Wall Street’s carefully calibrated consensus.

For months, the prevailing narrative was one of immaculate disinflation. Markets had priced in a smooth glide path toward aggressive rate cuts, assuming the worst of the post-pandemic price shocks were entirely behind us.

The data tells a different story.

Instead of a decisive break below the psychological 3% threshold, consumer prices have flatlined at an uncomfortable plateau. This stubbornness in the data has immediate, brutal consequences for the bond market and fundamentally alters the calculus inside the Eccles Building.

The Macroeconomic Collision Course

To understand the gravity of the current moment, one must look at the broader mechanical forces acting on the US economy. The bond market is currently pricing in a reality that equity investors have largely ignored. Yields on the 10-year Treasury note have marched upward, reflecting a creeping realisation that the era of zero-interest-rate policy is dead and buried.

This is not merely an American domestic issue. When the cost of borrowing rises in the United States, it acts as a giant vacuum, pulling capital away from emerging markets and forcing foreign central banks to defend their currencies. The Bank of Japan and the European Central Bank are watching Washington closely.

Yet, the domestic picture remains the primary driver. According to the International Monetary Fund, the US economy has expanded at a pace that continuously defies tight financial conditions, fueled by relentless consumer spending and structural labor shortages. This resilience is a double-edged sword. It keeps recessionary fears at bay, but it guarantees that inflation will not die a quiet death.

Decoding the Latest US CPI Report

The mechanics of the latest US CPI report reveal exactly why Federal Reserve Chair Jerome Powell has adopted a strictly data-dependent posture. Headline inflation—the raw number that includes volatile food and energy costs—ticked higher. But the central bank rarely makes policy based on the headline figure. They look under the hood.

The true problem lies within the core inflation data.

Excluding food and energy, core prices have proved remarkably sticky, annualising at a rate that is structurally incompatible with the Federal Reserve’s 2% target. The primary culprit is shelter. Rent and housing costs make up roughly one-third of the consumer price index basket, and they are refusing to cool at the pace policymakers require.

This creates a mechanical trap for the central bank.

To bring core inflation down to target, the Fed needs shelter costs to collapse. But high interest rates are actually exacerbating the housing shortage. Homeowners who locked in 3% mortgages in 2021 refuse to sell, artificially restricting housing supply and keeping property prices artificially elevated. It’s a textbook policy paradox.

The Bureau of Labor Statistics compiles this data meticulously, but the lag in how they measure housing—specifically through a metric known as Owner’s Equivalent Rent (OER)—means the US CPI report often reflects the housing market of six months ago rather than today. You can see the official breakdown of these lagging indicators directly via the Bureau of Labor Statistics.

Still, policymakers cannot ignore the official print. If the data says inflation is running hot, the Fed interest rate decision is essentially made for them. They cannot cut.

The Analytical Layer: Core vs Supercore

Beyond shelter, the Federal Reserve monetary policy apparatus has developed a new obsession over the last two years: “supercore” inflation. This metric tracks core services excluding housing. It encompasses everything from auto insurance and medical care to haircuts and restaurant meals.

It is the purest reflection of the domestic labor market.

When wages rise, service providers pass those costs directly onto the consumer. Auto insurance alone has seen double-digit annual increases, driven by more expensive car parts and higher mechanic wages. Until the labor market cools and wage growth moderates, supercore inflation will remain elevated.

How does the US CPI report affect interest rates? The US CPI report directly influences interest rates by dictating Federal Reserve policy. When consumer prices rise faster than the central bank’s 2% target, the Fed typically raises or maintains high interest rates to cool the economy. Conversely, falling inflation gives policymakers the runway to cut rates and stimulate borrowing.

This mechanical relationship is why the bond market reacts so violently to minor decimal deviations in the data. A CPI print that comes in just 0.1% above consensus expectations can trigger a massive sell-off in short-dated Treasuries. Traders instantly recalculate the probability of a rate cut at the next FOMC meeting, shifting trillions of dollars in capital in milliseconds.

The European Central Bank recently found itself in a similar predicament, though their economic growth profile is vastly weaker than America’s. The US economy’s ability to absorb higher rates without snapping is historically unprecedented. But this strength delays the very rate cuts that corporate America is banking on.

Downstream Consequences: A World Priced in Dollars

The implications of a delayed Fed pivot extend far beyond the borders of the United States. We are living in a dollar-dominated global financial system. When the Federal Reserve holds rates “higher for longer,” the US dollar strengthens against almost every other fiat currency.

This phenomenon, often referred to by currency strategists as the “dollar smile,” wreaks havoc on developing nations.

Countries that issue debt denominated in US dollars suddenly find their interest payments exploding. Furthermore, because commodities like oil are priced in dollars, a stronger greenback imports inflation directly into Europe and Asia. The Bank for International Settlements recently warned that prolonged tightness in US monetary policy could trigger isolated sovereign debt crises in vulnerable emerging markets.

For American businesses, the pain is concentrated in the middle market. Mega-cap tech companies are largely insulated; they hold billions in cash and actually earn money on high interest rates. But regional manufacturers, commercial real estate developers, and heavily leveraged private equity portfolio companies are suffocating.

They need the cost of debt to fall.

They are effectively held hostage by the monthly inflation data. Every time a hot CPI print hits the wire, the timeline for debt refinancing gets pushed further out into the horizon, increasing the likelihood of corporate defaults. The transmission mechanism of monetary policy is blunt, and it operates with long, variable lags. We are only now feeling the true bite of the rate hikes executed in late 2023.

The Doves’ Dissent: Are We Chasing Ghosts?

Not everyone agrees with the Federal Reserve’s current orthodox approach. A growing chorus of prominent economists and dovish policymakers argue that the central bank is fighting the last war.

Their argument is structurally compelling.

They suggest that the inflation we are measuring today is a statistical mirage, driven by the lagging nature of shelter costs and anomalous spikes in highly specific categories like financial services. Real-time data providers, such as Zillow and Apartment List, show that asking rents for new leases have actually been flat or declining for nearly a year.

If you strip out the lagging shelter data, inflation is already running below the 2% target.

By anchoring policy to a flawed US CPI report, the Fed risks overtightening and triggering a recession entirely by accident. This counterargument suggests that the central bank should look past the headline numbers and cut rates proactively before the labor market fractures.

“Monetary policy is notoriously forward-looking, yet we are making decisions based on rent data from six months ago,” noted a former Fed governor during a recent symposium. You can track the evolution of this internal debate through the historical minutes provided by the Federal Reserve Board.

That said, the ghosts of the 1970s haunt the corridors of the Eccles Building. Chair Powell is acutely aware of the Arthur Burns era, where the Fed cut rates prematurely only to watch inflation roar back with a vengeance. The current regime is terrified of repeating that historical error. They would rather cause a mild recession than allow inflation to become permanently unanchored in the psychology of the American consumer.

The risk of doing too little far outweighs the risk of doing too much.

The Final Calculation

The global economy is currently balanced on the head of a pin, and that pin is the American consumer. As long as retail spending holds up and unemployment remains near historic lows, inflation will refuse to die quietly. The latest US CPI report is not an anomaly; it is a reflection of a structurally tight economy that simply has not felt enough pain to cool down.

Investors must stop waiting for a return to the zero-interest-rate environment of the 2010s. That era was a historical aberration.

What follows, however, is a much more difficult environment for capital allocation. The Federal Reserve is locked in a staring contest with sticky prices, and until the data breaks, the cost of money is not going anywhere.

Capital is no longer free, and the data proves it.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

The trading floors across Tokyo, Taipei, and Hong Kong rarely register systemic panic in silence, yet the synchronized drop across Asian bourses this week carried a distinct, quiet finality. It was not a flash crash born of algorithmic errors, but a calculated repricing of structural risk. Within 90 minutes of the opening bell, selling pressure in high-growth technology equities widened into a broad-based retreat, demonstrating how quickly concentrated supply chain vulnerabilities can turn localized policy changes into regional market contagion. As capital pulled back toward defensive havens, the core reality became clear: the foundational assumptions that have underpinned Asian technology valuations for three years are fundamentally shifting.

The immediate catalyst lies in the intersection of restrictive industrial policies and tightening liquidity conditions across the Pacific. For quarters, institutional investors treated the hardware ecosystems of East Asia as insulated profit engines, assuming that secular demand for artificial intelligence infrastructure would bypass traditional macroeconomic gravity. That insulation has dissolved. A coordinated tightening of cross-border technology transfers, combined with an unexpected hawkish shift from regional central banks, has exposed bloated equity multiples to immediate revision. According to comprehensive data tracked by the Bloomberg Global Markets Dashboard, aggregate equity value across the region contracted by $310 billion in a 48-hour window, marking the sharpest contraction since the macro shifts of late 2024.

Section 1 — The Core Development

The scale of the current Asia-Pacific markets slide reflects a fundamental shift in institutional sentiment, moving from optimistic growth modeling to defensive capital preservation. In Tokyo, the Nikkei 225 plummeted 3.1%, led by a severe contraction in semiconductor equipment manufacturers, while Taipei’s Taiex slid 3.4%, its worst single-day performance in 18 months. This regional rout was mirrored in Seoul, where the Kospi dropped 2.7%, and Hong Kong, where the Hang Seng Index erased its quarterly gains with a 2.9% decline. These losses were driven by a widespread selloff of high-volume tech equities, which previously served as the primary anchors for regional index weightings.

+───────────────────────────────────────────────────────────────+

| REGIONAL MARKET PERFORMANCE |

+───────────────────────────────────────────────────────────────+

| Index | Daily Change (%) | Primary Drag Sector |

+────────────────┼──────────────────┼───────────────────────────+

| Taiex (Taipei) | -3.4% | Contract Chip Foundries |

| Nikkei 225 | -3.1% | Advanced Lithography/Etch |

| Hang Seng | -2.9% | E-Commerce & AI Platforms |

| Kospi (Seoul) | -2.7% | Memory Architecture |

+────────────────┴──────────────────┴───────────────────────────+

This market correction stems directly from newly announced bilateral export restrictions targeting the global semiconductor supply chain. On June 8, policy shifts restricted the shipment of advanced ultraviolet lithography components and specialized chemical vapor deposition tools to specific manufacturing hubs in East Asia. Analysts at the Reuters Financial Markets Bureau noted that these supply chain interventions directly disrupt the forward earnings guidance for top-tier chip manufacturers. When capital equipment cannot be deployed on schedule, projected fabrication yields drop, rendering current tech sector valuation models unsustainable.

The disruption is amplified by the sheer concentration of market value within a handful of advanced manufacturing entities. For example, Tokyo Electron saw its shares slide 6.4% in a single session, while Advantest dropped 5.8%. In Taipei, institutional asset managers liquidated positions in contract manufacturing firms, driven by concerns that capital expenditure plans would need to be delayed or cancelled entirely. When a small group of advanced component suppliers experiences this level of regulatory disruption, the effects ripple through the entire regional ecosystem. This pressure impacts everything from raw material miners in Australia to downstream precision assembly operations across Southeast Asia.

Section 2 — Analytical Layer

To view this market correction as a temporary bump in the road is to misunderstand the deeper changes occurring within the global tech sector valuation architecture. For several years, global asset allocation models treated Asian technology firms as high-margin operations with virtually guaranteed demand. This dynamic allowed corporate price-to-earnings multiples to expand far beyond historical averages. Yet, these high valuations assumed that the global semiconductor supply chain would remain efficient, borderless, and free from geopolitical friction. Now, as governments prioritize national security and supply chain independence over pure economic efficiency, investors are demanding a higher geopolitical risk premium to hold these assets.

[Regulatory & Export Controls]

│

▼

[Supply Chain Fractionation]

│

▼

[Higher CapEx & Lower Output Density]

│

▼

[Compressed Margins & Multiples Compression]

This shift forces a major reassessment of asset pricing, especially as monetary policy divergence complicates regional liquidity. While the Federal Reserve has maintained elevated terminal rates to anchor core inflation, regional central banks are facing competing economic pressures. The Bank of Japan’s recent move to normalize its yield curve control mechanism has strengthened the yen, reversing the popular carry-trade allocations that previously supported domestic equities. Consequently, international fund managers are encountering both operational headwinds and currency-driven margin calls, accelerating capital flight from emerging market assets back to US dollar-denominated short-term paper.

Why are tech stocks driving the current Asia-Pacific market downturn?

Tech stocks are driving the current Asia-Pacific market downturn because their high valuations relied on unhindered access to global components and markets. Recent export restrictions have disrupted these supply chains, forcing institutional investors to quickly de-risk their portfolios and compress equity multiples across the entire sector.

This compressed valuation environment quickly exposes corporate balance sheets that lack sufficient cash reserves. When capital costs rise alongside rising operational barriers, companies are forced to choose between lowering their research budgets or taking on expensive debt. As a result, the premium for true balance sheet quality has surged. Large-cap tech giants with deep cash reserves are showing relative resilience, while secondary suppliers and highly leveraged component makers bear the brunt of the liquidations. This dynamic is reshaping the competitive landscape, concentrating long-term market influence within a shrinking group of highly capitalized entities.

Section 3 — Implications & Second-Order Effects

The downstream consequences of this Asia-Pacific markets slide will likely reshape international capital flows and corporate supply chain strategies for years to come. As institutional capital exits overexposed electronics manufacturers, a noticeable reallocation toward defensive sectors is underway. Real estate investment trusts, local infrastructure funds, and sovereign-backed utilities are seeing steady inflows, acting as capital cushions across regional financial hubs. This rotation suggests a structural shift away from high-beta growth stories toward predictable, domestic-oriented cash flows, reflecting a broader trend toward lower risk tolerance globally.

TRADITIONAL ASSET FLIGHT GEOPOLITICAL REALIGNMENT

┌───────────────────────────┐ ┌───────────────────────────┐

│ High-Beta Tech Growth │ │ Broad Cross-Border Access │

└─────────────┬─────────────┘ └─────────────┬─────────────┘

│ │

▼ (Capital Flight) ▼ (Policy Shift)

┌───────────────────────────┐ ┌───────────────────────────┐

│ Cash & Defensive Havens │ │ Localized Subsidized Hubs │

└───────────────────────────┘ └───────────────────────────┘

Concurrently, the push for chip manufacturing localization is accelerating, though it brings considerable structural inefficiencies. Governments in Washington, Brussels, and Tokyo continue to pour billions into domestic fabrication facilities. However, duplicate factories lack the efficiency and deep talent pools of the highly integrated hubs they are meant to replace. According to a comprehensive trade study by the Financial Times Policy Institute, fracturing these specialized industrial clusters increases structural production costs by 22% to 30% across the broader hardware ecosystem. Over time, these higher costs act as a persistent drag on corporate profit margins, limiting long-term earnings potential even if consumer demand recovers.

Furthermore, these shifts are triggering wider currency volatility across emerging markets. Currencies closely tied to technology exports, such as the New Taiwan Dollar and the Korean Won, have come under sustained depreciation pressure against a strengthening US dollar. This trend raises the local cost of importing dollar-denominated commodities, creating inflationary pressures that limit the ability of regional central banks to cut interest rates. Consequently, policymakers face a difficult choice: they must either defend their currencies by raising interest rates into a slowing economy, or accept currency depreciation and the domestic inflation that comes with it.

Section 4 — Competing Perspectives or Counterargument

While prevailing market sentiment points toward an extended downturn, a distinct counter-narrative is forming among long-horizon value investors and sovereign wealth managers. Proponents of this view argue that the current selloff reflects a necessary and healthy correction, flushing out speculative retail capital that flooded the market during the AI boom of the past two years. They note that structural demand for advanced computing hardware, automotive electrification, and global telecommunications infrastructure remains fundamentally unchanged. From this perspective, the current drop offers an attractive entry point to acquire high-quality, cash-generating businesses at valuations not seen in years.

BEARISH INSTITUTIONAL OUTLOOK BULLISH VALUE INVESTOR PERSPECTIVE

┌──────────────────────────────────────────┐ ┌──────────────────────────────────────────┐

│ • Structural regulatory barriers │ │ • Essential, irreplaceable IP portfolio │

│ • Margin contraction via fragmentation │ │ • Secular tailwinds (AI, Automation) │

│ • Flight to domestic safe havens │ │ • Multiples resetting to historical norms│

└──────────────────────────────────────────┘ └──────────────────────────────────────────┘

Furthermore, data from the International Monetary Fund (IMF) Data Portal shows that regional balance-of-payments positions are considerably more resilient today than during past market crises. Most major technology exporters in the region maintain substantial foreign exchange reserves and carry low levels of external, dollar-denominated sovereign debt. This financial stability limits the risk of a wider balance-of-payments crisis, even during periods of heavy capital flight. If these underlying economic fundamentals hold, the current equity downturn may remain confined to corporate valuations, rather than triggering a systemic crisis across the broader financial system.

Closing

The current slide across Asia-Pacific markets highlights the deep tension between modern industrial policy and the realities of global capital markets. For decades, global financial markets operated on the assumption that economic efficiency would consistently override geopolitical friction. That era has ended. The ongoing reorganization of the global technology sector demonstrates that national security priorities and supply chain independence are now the dominant factors shaping international commerce. As capital continues to adjust to this fragmented landscape, the valuations of the world’s most vital technology companies are being fundamentally rewritten. Investors and policymakers alike must now adapt to a global market where safety and supply chain security matter more than raw corporate efficiency.

Ultimately, the true test for global markets will not be whether they can prevent this fragmentation, but how effectively they can price its long-term costs.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Super Micro Computer filed to raise up to $7 billion in mixed securities to fund its AI infrastructure build-out, spooking investors who sent the stock down 12% on Tuesday. The sell-off erased more than $4 billion in market value, the sharpest one-day decline since accounting irregularities first surfaced in August 2024. The registration statement, lodged with the Securities and Exchange Commission on 9 June, gives the company the flexibility to issue common stock, preferred shares, debt, or warrants. It is the largest capital-raising ambition in Super Micro’s three-decade history, and it lands at a moment when the server maker can ill afford a misstep in investor confidence.

The artificial intelligence infrastructure boom has turned once-sleepy server assemblers into strategic gatekeepers. Global spending on data-centre hardware and software will exceed $400 billion in 2026, according to [Gartner’s latest IT spending forecast](https://www.gartner.com/en/newsroom/press-releases/2026-01-15-gartner-forecasts-worldwide-it-spending-to-grow-9-percent-in-2026), with server and storage systems growing at a double-digit clip. Super Micro, a favourite of hyperscalers building NVIDIA-accelerated clusters, has ridden this wave to breakneck revenue growth: from $7.1 billion in fiscal 2023 to an estimated $25 billion in the fiscal year ending this month. Yet that expansion has stretched the balance sheet. Free cash flow turned negative in three of the past five quarters, and the company ended the March quarter with just $1.4 billion in cash against $2.8 billion in short-term debt. Wall Street had been expecting a capital raise; the sticker shock came from the sheer size of the ask.

The core development

Super Micro’s shelf registration, detailed in an SEC filing published after Monday’s close, authorises the sale of up to $7 billion in securities “for general corporate purposes, including working capital, capital expenditures, and potential acquisitions.” Chief executive Charles Liang told investors in a brief statement that the financing would “accelerate our capacity to deliver the most advanced AI platforms to customers who are scaling at an unprecedented pace.” The company gave no breakdown of how much would be raised via equity versus debt, nor a timetable. That opacity fed the worst-case assumptions embedded in Tuesday’s trading.

Shares of Super Micro, which had closed at $38.50 on Monday, dropped as low as $33.42 in the first hour of New York trading before settling at $33.90. The 12.2% decline sliced roughly $4.2 billion from the company’s market capitalisation. It was the stock’s worst single-day performance since 28 August 2024, when the company disclosed it would delay its annual report. The subsequent months brought an auditor resignation, a damning short-seller report from Hindenburg Research, and a near-death experience with Nasdaq delisting — a sequence that cost the stock more than 70% from its all-time high.

Analysts at Bloomberg Intelligence estimated that if Super Micro funded the entire $7 billion with new common equity, the share count would expand by roughly 20%, diluting earnings per share by a similar proportion. “Management is asking investors to take a leap of faith that the return on this capital will outweigh the mechanical hit to per-share metrics,” wrote senior analyst Woo Jin Ho in a note to clients on Tuesday. “In a sector where gross margins hover around 15%, that is a tall order.”

Dilution maths and the AI arms race

Why did Super Micro stock drop today? The immediate trigger is the arithmetic of dilution: a $7 billion equity raise at current market prices would swell Super Micro’s outstanding share count from roughly 580 million to approximately 700 million. All else equal, that shrinks each shareholder’s claim on future earnings by a fifth. For a stock that only regained Nasdaq compliance in February after restating two years of financials, the timing reawakens questions about whether the house is fully in order before the company knocks on the door for fresh capital.

The structural story is more uncomfortable. The AI server market is a capital-intensive, low-margin business where scale determines survival. Super Micro competes against Dell Technologies and Hewlett Packard Enterprise, both of which carry investment-grade credit ratings and have the luxury of funding customer orders through vendor-financing programmes that Super Micro cannot easily replicate. As NVIDIA accelerates its product cadence — moving from a two-year to a one-year rhythm between GPU generations — server builders must constantly retool assembly lines and hold ever-larger inventories of high-cost components. A single Blackwell Ultra rack can carry a bill-of-materials exceeding $3 million. For Super Micro, which builds to order and prides itself on rapid delivery, the working-capital demands have become voracious.

“This isn’t a company raising money because it’s in distress; it’s a company raising money because the TAM is sprinting away from it,” said Stacy Rasgon, senior analyst at Bernstein, in a research note that nonetheless trimmed his price target to $42 from $48. “The question is whether management can execute at a level that justifies the incremental capital. The track record there is mixed.”

Indeed, Super Micro’s liquid-cooling technology — a genuine competitive advantage that allows data centres to pack more GPUs into a single rack without overheating — has won it coveted slots at leading AI labs. But those design wins require upfront investment in manufacturing capacity, testing facilities, and service teams. The company has already committed $800 million to a new campus in San Jose, California, and is scouting sites in Malaysia and Mexico. A $7 billion war chest would transform its industrial footprint. It would also, if history is any guide, invite the scrutiny of short-sellers who have long argued that Super Micro’s reported margins are too good to be true.

Implications and second-order effects

The financing plan will ripple well beyond Super Micro’s shareholder register. First, it signals that the AI infrastructure build-out is entering a phase where even well-capitalised equipment suppliers need external funding to keep pace. That has implications for the broader supply chain: component suppliers such as Vicor, Monolithic Power Systems, and Amphenol may face intensified pressure to extend payment terms, while competitors may be forced to follow suit with their own dilutive raises.

Second, the debt market’s reception will be a crucial test. Super Micro currently carries a BB- rating from S&P, three notches below investment grade. Loading an additional $3 billion or $4 billion in leverage onto the balance sheet — assuming a roughly 50-50 equity-debt split — could push leverage ratios above 4x EBITDA, a level that would make credit committees nervous. A downgrade to B+ territory would lift borrowing costs at precisely the moment the company needs the cheapest possible capital to finance razor-thin-margin hardware sales. The OECD’s latest capital-market monitor notes that credit spreads for tech hardware issuers have widened by 85 basis points since January, reflecting growing anxiety about overcapacity in AI-adjacent industries.

Third, for the wider AI ecosystem, the scale of Super Micro’s ask is a data point in the debate over whether AI infrastructure is overbuilding. Venture-capital firm Sequoia Capital recently estimated that the gap between AI infrastructure revenue expectations and actual end-user demand now exceeds $500 billion. If Super Micro needs $7 billion to meet its order book, the implied capex cycle is still accelerating — a bullish signal for NVIDIA, TSMC, and Arista Networks, but a warning for anyone betting on a near-term plateau.

Competing perspectives

Not everyone reads the filing as a bearish signal. Rosenblatt Securities analyst Hans Mosesmann, a long-time Super Micro bull, reiterated his buy rating on Tuesday and described the shelf registration as “a necessary prerequisite for capturing a $100 billion AI server TAM by 2028.” In a note titled “Blink and You’ll Miss the Opportunity,” Mosesmann argued that the company’s direct-liquid-cooling expertise and its close design collaboration with NVIDIA give it a “structural moat that is undervalued by a market fixated on near-term dilution.” He points to the fact that Super Micro’s server revenue grew 110% year-on-year in the March quarter even as gross margins ticked up to 15.6%, evidence that pricing power is not yet eroding.

The counterargument, articulated most forcefully by short-seller Jim Chanos in a television appearance on Tuesday, is that Super Micro’s history of accounting irregularities makes any large-scale capital raise inherently risky. “You’re handing a blank cheque to a management team that couldn’t file its financials on time for two consecutive years,” Chanos told Bloomberg Television. “The $7 billion number is so large relative to the company’s tangible book value that it looks less like a growth plan and more like a bailout we don’t yet understand.” Super Micro settled an SEC investigation in late 2025 with a $40 million penalty and a restatement that wiped $340 million from retained earnings, but the episode left scars that the latest filing has reopened.

Between these poles sits a more pragmatic view: the company has little choice. Demand for AI compute is voracious, lead times on NVIDIA’s highest-end GPUs remain long, and the cost of being a sub-scale player in merchant silicon integration is obsolescence. If Super Micro does not raise capital now, it cedes ground to Dell, which has already announced a $2.5 billion AI server financing facility of its own, and to the hyperscalers’ in-house server designs

Super Micro’s $7 billion shelf filing is a Rorschach test for how an investor views the AI infrastructure cycle. To the optimist, it is the prelude to a revenue breakout that will make the dilution arithmetic look quaint. To the sceptic, it is the latest chapter in a corporate saga that has repeatedly tested the limits of credulity. Both narratives can’t be true, but the market’s job is to price the probability of each.

Charles Liang built Super Micro from a San Jose garage in 1993 into an essential cog in the world’s most important technology trend. That history buys him a measure of patience from long-term shareholders, but it does not insulate the stock from the cold mechanics of supply and demand. On Tuesday, the supply of new paper overwhelmed the demand for the story. Super Micro just placed the largest bet of its life on the table. The roulette wheel is still spinning.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance5 months ago

Markets & Finance5 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis4 months ago

Analysis4 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Analysis4 months ago

Analysis4 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks5 months ago

Banks5 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment5 months ago

Investment5 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Analysis4 months ago

Analysis4 months agoJohor’s Investment Boom: The Hidden Costs Behind Malaysia’s Most Ambitious Economic Surge

-

Global Economy5 months ago

Global Economy5 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis

-

Global Economy5 months ago

Global Economy5 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025