Analysis

Singapore-Australia LNG Pact: The Indo-Pacific’s Most Important Energy Deal of 2026

Singapore and Australia’s legally binding LNG and diesel supply agreement is rewriting Indo-Pacific energy security. Here’s why this deal matters far beyond both nations’ borders.

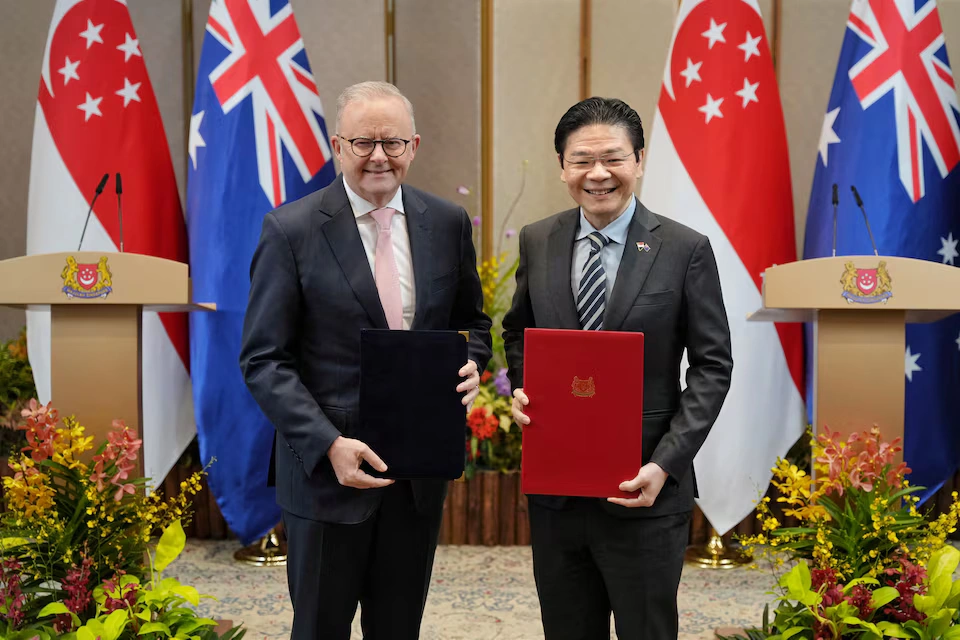

When Lawrence Wong stood at the Istana on Friday morning alongside Anthony Albanese and declared that this pact was “not just about managing today’s crisis, but about building trusted supply lines for a more uncertain future,” he was doing something that most politicians in 2026 conspicuously avoid: telling the complete truth. Strip away the diplomatic language, the handshakes, and the hard-hat photo opportunity at Jurong Island’s LNG terminals, and what you find underneath is something quietly historic. Two middle powers — one the world’s premier trading entrepôt, the other its third-largest LNG exporter — have decided that in an era defined by chokepoint warfare, legal commitments to energy supply are worth more than the paper they’re printed on. They may be right. And the rest of the Indo-Pacific should be paying close attention.

Why the Strait of Hormuz Has Changed Everything

To understand what Singapore and Australia agreed to on April 10, 2026, you have to first understand the world they woke up to in early March.

Until the U.S.–Israeli war against Iran, the Strait of Hormuz was open and roughly 25% of the world’s seaborne oil trade and 20% of global LNG passed through it. Wikipedia That calculus collapsed with terrifying speed. Iran’s closure of the Strait of Hormuz disrupted 20% of global oil supplies and significant LNG volumes, sending Brent crude surging past $120 per barrel and forcing QatarEnergy to declare force majeure on all exports. Wikipedia The head of the International Energy Agency called it “the greatest global energy security challenge in history.” Wikipedia

The numbers since have only grown more alarming. Dated Brent hit an 18-year high of $141.26 per barrel on April 2 MEES, while diesel prices are forecast to peak at more than $5.80 per gallon in April and average $4.80 per gallon through 2026 U.S. Energy Information Administration — devastating for the farming and mining sectors that underpin Australia’s export economy. Meanwhile, LNG spot prices in Asia more than doubled to three-year highs, reaching $25.40 per million British thermal units as QatarEnergy declared force majeure at Ras Laffan — the world’s largest liquefaction facility, responsible for 20% of global LNG production. Wikipedia

For Singapore, the crisis landed particularly hard. Singapore and Taiwan depend more on Qatari LNG than most Asian economies, Wikipedia and production at Singapore’s Jurong Island refineries has been limited because most of the oil processed there comes via the Strait of Hormuz. NEOS KOSMOS For Australia, the problem runs in the opposite but equally dangerous direction: Australia imports more than 80 percent of its petrol, diesel, and jet fuel from overseas, mostly from South Korea, Singapore, Japan, Taiwan, and Malaysia. The Diplomat A nation that sells the world its gas but can barely refine enough diesel to power its own tractors — that is the paradox at the heart of Australian energy policy, and it has never been more exposed than it is today.

The Architecture of the Singapore–Australia Legally Binding Energy Agreement

What Was Actually Agreed — and Why “Legally Binding” Matters

The joint statement issued by both prime ministers goes considerably further than the March pledge. Both leaders directed their ministers to conclude a legally binding Protocol to the Singapore-Australia Free Trade Agreement (SAFTA) on Economic Resilience and Essential Supplies, and welcomed the establishment of an Australia–Singapore Economic Resilience Dialogue, co-chaired by senior officials, to facilitate cooperation on economic resilience challenges and trade in essential supplies. Ministry of Foreign Affairs Singapore

This is not, as cynics might dismiss it, a diplomatic press release dressed in legalese. Embedding supply commitments into a protocol to an existing free trade agreement gives them treaty-level standing. In a world where spot market bidding wars are already erupting, with LNG suppliers becoming increasingly selective in negotiating mid- to long-term volumes because it’s more lucrative to sell into the spot market, Bloomberg having legal standing to demand preferential access is not a soft power gesture — it is hard economic architecture.

The underlying trade logic is elegant precisely because it is symmetrical. More than a quarter of all fuel imported into Australia comes from Singapore, while Australia provides about one-third of the city-state’s LNG supply. The Daily Advertiser Albanese articulated it plainly: “We are a big supplier of LNG to Singapore. Singapore is a really important refiner of our liquid fuels. This is a relationship of very substantial mutual economic benefit.” Both countries agreed to “make maximum efforts to meet each other’s energy security needs.” Yahoo!

The genius of this structure is that neither country is doing a favour. They are executing a swap — Australian gas for Singaporean refined products — and now writing that swap into binding international law before the next crisis hits.

What It Does Not (Yet) Do

Intellectual honesty requires acknowledging the limits. The joint statement contains no specific shipment volumes, no price-fixing mechanism, no explicit strategic reserve sharing agreement, and no stated timeline for when the SAFTA protocol will be concluded. “Working quickly” is a political phrase, not a procurement schedule.

The more fundamental challenge is Singapore’s refinery throughput. An LNG tanker can cost $250 million, and insurance concerns alone mean operations cannot simply be ramped up and down based on perceived escalations or de-escalations. CNBC Singapore is committed — but commitment is not the same as capacity. If the Strait of Hormuz remains closed into the northern hemisphere summer, Singapore’s refineries will be processing less crude regardless of which bilateral agreements are in place.

The Indo-Pacific Energy Security Realignment — China’s Shadow and AUKUS Synergy

A Geopolitical Sorting Process Is Underway

On March 4, the IRGC announced that the strait is closed to any vessel going “to and from” the ports of the U.S., Israel, and their allies. Subsequently, reports emerged that Iran would allow only Chinese vessels to pass through the strait, citing China’s supportive stance towards Iran. Wikipedia Read that sentence twice, slowly. This is not an energy story. This is a geopolitical sorting machine, restructuring the global energy map along lines of political alignment.

Australia and Singapore are unmistakably on one side of that divide. Both are Quad-adjacent, both are democracies with deep security ties to Washington, and both are now accelerating energy arrangements with each other precisely because they cannot rely on the Gulf supply corridor that Beijing is quietly privileged to use. The Singapore–Australia critical supplies pact 2026 is, in this light, a de facto statement about which bloc each country is wagering its energy future on.

This is the AUKUS undertow that neither government will name explicitly in polite company. The defence partnership’s security architecture and the energy partnership announced Friday are two different expressions of the same strategic logic: when the chips are down, trust the relationship, not the market.

Europe’s Cautionary Tale — and Australia’s Strategic Leverage

Europe is expected to suffer a second energy crisis primarily as a result of the suspension of Qatari LNG and the closure of the Strait of Hormuz. The conflict coincided with historically low European gas storage levels — estimated at just 30% capacity following a harsh 2025–2026 winter — causing Dutch TTF gas benchmarks to nearly double to over €60 per megawatt-hour by mid-March. Wikipedia

Europe’s tragedy — and it is genuinely tragic — is that it spent two years after Russia’s Ukraine invasion congratulating itself on diversification while not actually completing it. Gas storage went into the 2025–2026 winter at dangerous levels. Long-term LNG contract structures were renegotiated upward at the worst possible moment. The continent is now bidding against Asia for every available cargo on the spot market at prices that are genuinely destabilising.

Australia’s decision to negotiate supply agreements bilaterally — not just with Singapore but reportedly with Brunei, China, Indonesia, Japan, Malaysia, and South Korea — reflects a hard-won lesson from Europe’s misadventure: energy resilience is relational, not just infrastructural. Pipes and terminals matter, but so does the phone call at 3 a.m. when a chokepoint closes. Australia has spent four years building those relationships; it is now cashing them in.

As Australian Assistant Foreign Affairs Minister Matt Thistlethwaite put it: “We’ve got that advantage in that we can work with our neighbours in the Asia-Pacific to ensure that they have access to their energy needs and we get access to ours.” The Diplomat That is, in essence, the diplomatic theory of the LNG diesel supply chain security Singapore-Australia agreement: Canberra’s natural gas wealth is being converted into political insurance, denominated in refined fuel.

Why This Model Could Become the Template for Indo-Pacific Energy Diplomacy

Beyond the Free Trade Agreement — A New Class of Instrument

The standard toolkit of bilateral trade diplomacy — tariff schedules, most-favoured-nation status, investor protection clauses — was designed for a world where supply disruptions were rare, short, and solvable by price signals. The 2026 Hormuz crisis has exposed that assumption as dangerously complacent.

What the Singapore–Australia agreement proposes is something genuinely novel: a crisis-contingent preferential supply protocol, embedded within an FTA architecture but explicitly activated under conditions of global disruption. The Australia–Singapore Economic Resilience Dialogue, co-chaired at senior official level, gives this framework an institutional nervous system — a standing mechanism for early consultation and coordinated response rather than improvised crisis management.

This is the architecture Europe wishes it had built with its LNG suppliers after 2022. It is the architecture Japan and South Korea are now, belatedly, also pursuing. South Korea holds about 3.5 million tons of LNG and Japan around 4.4 million tons in reserves — enough for roughly two to four weeks of stable demand, CNBC a buffer that a single disrupted cargo schedule can obliterate. Bilateral resilience protocols of the Singapore–Australia variety provide the diplomatic scaffolding around which physical stockpile strategies must now be built.

Trusted Supply Lines: The New Competitive Advantage

Wong’s phrase — “trusted supply lines” — is going to echo through energy ministries across the Indo-Pacific for years. The word choice is deliberate. Trusted is not cheap or close or abundant. It is a relational category, not a logistical one. And in a global energy market being restructured by geopolitical conflict, relational trust is becoming the scarce commodity.

Wong was explicit: “We do not plan to restrict exports. We didn’t have to do so even in the darkest days of COVID and we will not do so during this energy crisis. I am confident that Australia and Singapore will not just get through the crisis, but we will emerge stronger and more resilient.” The Daily Advertiser That is a political commitment of the first order — a small city-state with no hinterland, surrounded by a global disruption, choosing not to hoard. It is worth more than any contract clause.

Data Snapshot: The Interdependence That Makes This Pact Work

| Flow | Volume | Significance |

|---|---|---|

| Australia → Singapore (LNG) | ~39.4% of Singapore’s LNG supply (2024) | Singapore’s largest single LNG source |

| Singapore → Australia (refined fuels) | >26% of Australia’s total fuel imports | Australia’s largest refined fuel supplier |

| Singapore → Australia (petrol) | >50% of Australia’s petrol intake | Critical for road and agricultural sectors |

| Global LNG through Hormuz | ~20% of global LNG trade | Now disrupted; Qatar’s Ras Laffan offline |

| Brent crude peak (April 2026) | $141.26/barrel (April 2 high) | 18-year high; compressing refinery margins |

The numbers tell a story of mutual exposure that makes this deal not merely politically desirable but economically unavoidable. Both economies would suffer severely without each other’s supply; the pact simply converts that mutual dependence into a formal and enforceable commitment.

Forward Look: Three Bold Predictions

First: The Singapore–Australia protocol will be concluded within 90 days and will serve as the explicit template for at least two additional bilateral energy resilience agreements in the Indo-Pacific — most likely involving Japan and either South Korea or New Zealand — by the end of 2026. The institutional architecture of the Economic Resilience Dialogue is designed to be replicated.

Second: The Hormuz crisis will accelerate Australia’s long-stalled domestic refining debate. Having 80% of your liquid fuel supply dependent on overseas refiners — however trusted — is a structural vulnerability that no bilateral agreement can fully paper over. Expect a serious federal government investment framework for domestic refining capacity to emerge within 18 months, framed explicitly as national security infrastructure.

Third: China is watching this closely and will not be idle. Beijing already enjoys de facto preferential passage through the Strait for its tankers. If it perceives that a Singapore–Australia–Japan energy axis is forming along security-aligned lines, it will accelerate its own bilateral energy lock-in arrangements with alternative suppliers — deepening the global energy bifurcation that began in 2022 and is now accelerating at pace. The Indo-Pacific energy security agreement between Wong and Albanese is not just a supply pact. It is an early data point in the restructuring of the global energy order.

Conclusion: A Small Pact With a Very Large Shadow

There is something almost anachronistic about two democracies in 2026 sitting down together and saying, plainly, that they will keep trade flowing — that they will not weaponise energy in the way that others have. It is the kind of statement that would have seemed unremarkable in 2015. Today it feels almost radical.

The Singapore–Australia LNG and diesel agreement signed at the Istana is, in its immediate terms, a sensible and well-constructed piece of crisis diplomacy. In its deeper terms, it is a proof of concept: that trusted bilateral relationships, properly institutionalised, can serve as genuine shock absorbers in a world where the multilateral system is fraying and chokepoints are being used as weapons.

PM Wong called it a “simple but critical principle.” He is right on both counts. Simple principles, rigidly held under pressure, are often the most valuable ones. And right now, in a global energy market that has been turned upside down in six weeks, the principle that allies keep their promises to each other may be the most critical thing the Indo-Pacific has.

The rest of the world’s energy ministers should take note — and consider what it would mean to have nobody to call when their own Hormuz moment arrives.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Bangladesh’s Bank Resolution Act 2026: Doors Re-Opened for Ex-Owners — Reform Reversal or Pragmatic Bailout?

In April 2026, as Dhaka’s political calendar accelerates toward general elections and the IMF watches every legislative move from Washington, Bangladesh’s newly elected BNP-led parliament has quietly detonated a grenade in the middle of a still-fragile banking reform. The Bank Resolution Act 2026, enacted on Friday, April 11, paves a wide — some would say suspiciously wide — road for former bank owners to reclaim institutions they drove into distress. The question hardening in the minds of depositors, reform economists, and international creditors alike is brutally simple: is this pragmatic crisis management, or the most elegant act of regulatory impunity Bangladesh has ever legislated?

What the Bank Resolution Act 2026 Actually Says — and What It Doesn’t

Let’s start with the architecture of the law, because the devil lives in its fine print.

Under the Bank Resolution Act 2026, former directors or owners of banks that are merging or listed for mergers can pay just 7.5 percent upfront of the amount injected by the government or Bangladesh Bank to reclaim their institutions. The remaining 92.5 percent is repayable within two years at 10 percent simple interest. The Daily Star Before any approval is granted, Bangladesh Bank must conduct due diligence and seek government clearance. Even after approval, the central bank will closely monitor the merged entity for two years, with a special committee reviewing compliance — and failure to meet conditions could lead to cancellation of approval and further regulatory action. The Daily Star

On paper, the safeguards sound serious. In practice, economists who have spent years watching Bangladesh’s banking politics are not reassured. Zahid Hussain, former lead economist at the World Bank’s Dhaka office and a member of the interim government’s banking reform task force, warned that the amendment destroys the credibility of the reform process, saying that “a clear roadmap has been provided for former owners to re-occupy banks that were distressed due to their own mismanagement and the siphoning of funds.” The Business Standard

The numbers Hussain cites are staggering in their implication. He estimated that for the five merged banks, the total required payment would be roughly Tk 35,000 crore — and expressed concern that the terms are so lenient that former owners could easily pay the initial 7.5 percent and borrow the remainder from the banking sector itself. The Business Standard That is not a bailout mechanism. That is a round-trip ticket funded by the very system that was looted.

The Sommilito Islami Bank Merger: A Reform That May Never Have Happened

To understand what is now at stake with the Bank Resolution Act 2026, you must first understand what the 2025 Ordinance was attempting to accomplish — and why it mattered beyond Bangladesh’s borders.

As part of its reform drive, in May 2025, the interim administration had approved the Bank Resolution Ordinance 2025 to merge five troubled Shariah-based private banks into a state-run entity titled Sommilito Islami Bank. The five institutions — First Security Islami Bank, Social Islami Bank, Union Bank, Global Islami Bank, and Exim Bank — had collectively become symbols of politically directed lending and governance failure. The Daily Star

The boards of four of the banks were dominated by the controversial S Alam Group, led by its Chairman Mohammed Saiful Alam, while Exim Bank was long controlled by Nassa Group Chairman Md Nazrul Islam Mazumder. The Daily Star The S Alam Group banks return 2026 scenario — which the new Act explicitly enables — is not abstract; these are the same ownership structures whose related-party lending created the crisis in the first place.

The Shariah banks merger reversal risk is now real enough that even Bangladesh Bank’s own officials are alarmed. Bangladesh Bank officials told The Daily Star that concerns remain over how these banks will be managed if former owners return, whether depositors will be able to recover their money, and that if a bank is returned to its previous owners, it cannot easily be taken back again. “This raises doubts about whether they would be able to run the banks properly and ensure full legal and regulatory compliance,” one official said, adding that the return of previous owners could hinder the ongoing merger process. The Daily Star

That is a central bank quietly sounding an alarm about a law passed by its own government. Read that again.

The Macroeconomic Context: A Sector Already on Life Support

No assessment of the Bank Resolution Act 2026 can be divorced from the catastrophic baseline it is operating against. The World Bank’s Bangladesh Development Update released in 2025 documented a sector in acute distress. Banking sector-wide non-performing loans reached 24.1 percent by March 2025, significantly above the South Asian average of 7.9 percent. The capital-to-risk-weighted asset ratio fell to 6.3 percent, well below the regulatory minimum of 10 percent. World Bank

These are not technical footnotes. A CRAR of 6.3 percent — against a required 10 percent minimum, and a Basel III-compliant effective floor closer to 12.5 percent when capital conservation buffers are included — means Bangladesh’s banking system is operating with a structural capital hole that is visible from space.

The IMF’s 2025 Article IV Consultation, concluded on January 26, 2026, was characteristically blunt. Directors highlighted the urgent need for a credible banking sector reform strategy consistent with international standards to restore banking sector stability. Such a strategy should include estimates of undercapitalization, define fiscal support, and outline legally robust restructuring and resolution plans. They also cautioned against unsecured liquidity injections into weak banks. International Monetary Fund The ink on that consultation was barely dry when parliament passed the Bank Resolution Act 2026 — a law whose principal mechanism is, functionally, a structured return of capital to distressed institutions controlled by their original owners.

The IMF’s language about “prolonged reliance on forbearance measures” was not accidental. Fund staff specifically stated that “any approach to dealing with weak banks should ensure healthy balance sheets, sustained profitability, and adequate liquidity without prolonged reliance on forbearance measures.” International Monetary Fund What the new Act provides — a 7.5 percent entry ticket and 10 percent simple interest on a two-year repayment — is, by any global standard, forbearance in a legislative costume.

The International Standard: What the BRRD, FDIC, and India’s IBC Actually Require

To appreciate why the Bank Resolution Act 2026 troubles international observers, compare it against the frameworks Bangladesh has nominally aligned itself with.

The European Union’s Bank Recovery and Resolution Directive (BRRD) operates on a “no creditor worse off” principle, with resolution authorities empowered to impose losses on shareholders and unsecured creditors before any public money is committed. Critically, the BRRD explicitly prohibits the return of equity to former shareholders whose mismanagement contributed to resolution proceedings. The message is structural: resolution is not a waiting room for rehabilitation. It is a point of no return.

The US Federal Deposit Insurance Corporation (FDIC) model is similarly unambiguous. When an institution enters FDIC resolution, former owners lose their equity entirely. The FDIC then sells assets, transfers deposits, or establishes bridge banks — without reopening a window for the people who broke the bank in the first place. The concept of a former owners Bangladesh Bank Resolution Act mechanism — paying back a fraction upfront and recovering control — would be legally inconceivable under FDIC rules.

India’s Insolvency and Bankruptcy Code (IBC), enacted in 2016, went further: its Section 29A specifically bars promoters who have defaulted from participating in resolution plans for their own companies. After years of politically connected promoters recycling distressed assets back to themselves, India drew an explicit legislative line. Bangladesh, in April 2026, appears to be drawing that line in the opposite direction.

The Chambers and Partners Banking Regulation 2026 Guide for Bangladesh acknowledges that the regulatory agenda of Bangladesh Bank for 2025 and 2026 is “exceptionally dynamic, driven by a national push for enhanced governance, financial sector stability, and compliance with IMF programme conditions.” Chambers and Partners The Bank Resolution Act 2026 as enacted tests whether that dynamism is substantive or cosmetic.

The Government’s Defence: Fiscal Pragmatism or Political Convenience?

Finance Minister Amir Khosru Mahmud Chowdhury presented the Act in parliament as a “market solution” — a phrase that in emerging market contexts tends to arrive dressed as economic logic and leave as political cover. The minister described the government as having already invested approximately Tk 80,000 crore into weak banks and potentially needing another Tk 1 lakh crore — a financial burden he called unsustainable. “This new arrangement places the obligation of recapitalisation and liability settlement on the applicants, reducing the pressure on the government and the Deposit Insurance Fund,” he stated. The Business Standard

This argument has a kernel of validity that cannot be entirely dismissed. A sovereign that has already pumped the equivalent of several GDP percentage points into failing banks and faces the prospect of doubling down — during a period when, as the IMF notes, Bangladesh’s debt service-to-revenue ratio exceeds 100 percent — has a legitimate interest in finding private recapitalization. The question is not whether to seek private capital. It is from whom, and on what terms.

The Act’s critics, including Zahid Hussain, argue the answer currently provided is: the same people who caused the crisis, on terms lenient enough to enable regulatory arbitrage. Hussain warned that the provision undermines past reform efforts, noting: “If, under this law, the previous owners return and reclaim their organisations, the integrity of the new structure created after the merger could be lost. In that case, all merger-related work would effectively become meaningless.” The Daily Star

He is right. And the S&P Global Islamic Banking Outlook 2026 context makes this more acute: Islamic finance institutions globally are under increased scrutiny for governance standards, with rating agencies increasingly marking down Shariah-compliant lenders in frontier markets where board independence and related-party transaction controls are weak. The Som milito Islami Bank ex-owners returning to manage the merged entity would face an uphill battle establishing the governance credibility that international Islamic finance counterparties — Gulf investors, sukuk markets, multilateral development banks — now routinely require.

The Post-Hasina Governance Test: Is Bangladesh Building Institutions or Recycling Networks?

The deepest concern about the Bank Resolution Act 2026 is not technical. It is political economy.

Bangladesh’s post-August 2024 moment — the political transition that followed the uprising ending Sheikh Hasina’s government — was described by reformers and development partners as a generational opportunity to rebuild institutional integrity. Finance Adviser Dr. Salehuddin Ahmed himself described the inherited banking system as one hollowed out by “rampant embezzlement, unchecked corruption, and politically driven loan rescheduling.” BBF Digital

The three-year reform roadmap — backed by the IMF, World Bank, and Asian Development Bank — committed Bangladesh to asset quality reviews, risk-based supervision, the Distressed Asset Management Act, and legally robust restructuring frameworks. The overarching goal was to “ensure banks are financially sound and to end the long-standing practice of granting regulatory forbearance to weaker institutions.” The Daily Star

The Bank Resolution Act 2026 as enacted is not a clean break from that narrative. It is, at minimum, an asterisk — and at worst, a structural loophole that future actors will exploit regardless of what due diligence and monitoring clauses say on paper. Bangladesh Bank officials themselves acknowledge the asymmetry: once a bank is returned to former owners, recovering it is legally and operationally far harder than the two-year monitoring clause implies.

The former owners Bangladesh Bank Resolution Act pathway, combined with the ex-owners reclaim banks Bangladesh mechanism at 7.5 percent upfront, sets a precedent that future distressed bank owners will study carefully. The message it sends to the market — domestic and international — is that Bangladesh Bank resolution is a negotiated exit, not a structural consequence. That signal will outlive any monitoring committee.

What a Credible Reform Would Look Like

This article does not argue for leaving the five merged Shariah banks in permanent regulatory limbo. Merger uncertainty damages depositors. Extended state management creates moral hazard in the other direction. Bangladesh does need a resolution pathway.

But a credible pathway, consistent with the BRRD model and India’s IBC experience, would require: mandatory and independent forensic audits of all related-party transactions before any return of ownership is considered; an open competitive bidding process for new strategic investors — not a preferential window for former owners; full equity writedowns for shareholders whose mismanagement contributed to resolution triggers; enhanced personal liability provisions backed by asset freezes, not merely regulatory monitoring; and independent board composition certified by Bangladesh Bank before any operational handback.

The IMF, in its January 2026 Article IV, called for “swift action to operationalize new legal frameworks that facilitate orderly bank restructuring while safeguarding small depositors” alongside “robust asset quality reviews for all large and systemic banks, bank restructuring aimed at forward-looking viability, strengthened risk-based supervision, and enhanced governance and transparency.” International Monetary Fund The Bank Resolution Act 2026 addresses the first clause and largely bypasses the rest.

The Verdict: Alarming Precedent, Redeemable Only by Enforcement

Bangladesh’s Bank Resolution Act 2026 is not beyond redemption. The due diligence requirement, BB monitoring provisions, and cancellation clauses are meaningful — if enforced with the independence the law’s critics doubt Bangladesh Bank can summon under a newly elected government whose political networks overlap uncomfortably with the very ownership groups seeking re-entry.

The Tk 35,000 crore question is not whether former owners can write the initial cheque. It is whether Bangladesh’s regulatory institutions have the spine to cancel approvals when compliance conditions are not met, to withstand political pressure during the two-year supervision window, and to protect the 17 million depositors whose savings are concentrated in institutions whose balance sheets remain deeply impaired.

For international investors, IMF programme managers, and World Bank country teams watching from Washington and Jakarta, the Bank Resolution Act 2026 is a stress test of post-crisis institutional credibility. Bangladesh passed the legislative test of enacting a resolution framework in 2025. It now faces the harder test: proving that the framework means what it says, even when the politically connected come knocking.

History suggests that in emerging markets, that second test is the one that matters — and the one most frequently failed.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

A decade after 1MDB shook Malaysia, a new scandal targets the anti-graft agency itself. Are the rules still being applied fairly — or is the watchdog now the predator?

The Gunman in the Restaurant

On a June afternoon in 2023, Tai Boon Wee was summoned to The Social, a Kuala Lumpur suburb restaurant famous for football screenings and chicken wings. He had just been questioned by the Malaysian Anti-Corruption Commission over accounting irregularities at GIIB Holdings, the rubber products company he founded. When he arrived, a man named Andy Lim — a new shareholder — was waiting. Before long, Lim raised his arms to reveal a pistol beneath his jacket. He wanted two board seats, and the weapon was his negotiating tool.

The CCTV footage of that meeting, reviewed by Bloomberg journalists Tom Redmond and Niki Koswanage, would become the combustible heart of one of the most consequential investigative reports in Southeast Asian financial journalism in years. Published on February 11, 2026, the Bloomberg feature — titled “Who’s Watching Malaysia’s Anti-Corruption Watchdog?” — described how a commission set up to fight graft was allegedly helping a group of businessmen seize control of companies, with questions about its conduct going all the way to the top. Bloomberg

That question — all the way to the top — is the one that Kuala Lumpur has been unable to shake since. And for global investors already edgy about rule-of-law risks in Southeast Asia, it is exactly the kind of question that changes capital allocation decisions.

Malaysia is facing a new governance test. One that may prove more corrosive to institutional credibility than even 1MDB — because this time, the allegation is not that the watchdog failed. It is that the watchdog became the wolf.

A Different Kind of Scandal

The 1MDB affair — in which an estimated $4.5 billion was looted from a state investment fund and spent on superyachts, Picassos, and Hollywood productions — was breathtaking in its brazenness but ultimately comprehensible. It was a straight-line theft: powerful men used state resources as a personal treasury. International prosecutors, from Washington to Singapore to Zurich, followed the money. Najib Razak was convicted. Goldman Sachs paid. The architecture of the crime, however grotesque, was legible.

What Bloomberg’s 2026 investigation describes is something structurally different — and, in some ways, more insidious. The report details how the MACC, led by chief commissioner Azam Baki, is alleged to have assisted rogue businessmen in forcibly taking over public-listed companies by using the agency’s extensive powers to arrest, intimidate, and threaten charges against company founders and executives. MalaysiaNow The alleged playbook is precise and repeatable: targeted investors take stakes, MACC probes are triggered against company founders, bank accounts are frozen, board seats reshuffled, and in some instances founders are pushed out altogether. Dimsum Daily

This is not theft by subtraction — the pillaging of a state fund. It is theft by substitution: the weaponisation of the state’s anti-corruption apparatus to facilitate corporate predation in the private sector. It attacks the engine of market confidence itself.

Victor Chin, a Malaysian businessman himself under investigation for alleged involvement in the scheme, put it with chilling clarity in a March statement: “The corporate mafia is not just about a person or single organisation. It is a tactic, and it is ongoing. The individuals may change, and the target companies may differ, but the method remains the same in each corporate attack.” Bloomberg

When the alleged perpetrators of a scheme are the ones best placed to describe its mechanics, you know the system has entered a complex moral inversion.

The Architecture of the ‘Corporate Mafia’

At the operational centre of the Bloomberg investigation is a MACC unit known as “Section D,” which handles complaints and arrests related to corruption in listed companies. The unit was led by Wong Yun Fui, currently MACC’s deputy director of investigations. MalaysiaNow According to the report, this unit became the enforcement arm that businessmen allegedly used to apply pressure on company founders.

The gunman episode at The Social restaurant crystallised the alleged methodology. After Tai Boon Wee was approached by Andy Lim — who demanded board seats at GIIB Holdings with a firearm — police eventually arrested Lim and confiscated the pistol. But sources told Bloomberg that Azam subsequently called the police to request the return of Lim’s gun, and that conversations within MACC revealed Lim was “very close with Azam Baki,” a friendship also referenced in an internal memo circulated within the agency. MalaysiaNow

Azam has denied the allegations comprehensively and filed a lawsuit against Bloomberg seeking RM100 million in damages. The MACC’s advisory board urged an end to speculation, arguing assessments must be grounded in verifiable facts.

But the Bloomberg investigation did not rest on a single incident. Another businessman, Brian Ng, recounted a similar experience to that of Tai: facing an MACC investigation, he was summoned to a restaurant meeting with one Francis Leong, allegedly a member of the same “corporate mafia” network linked to Victor Chin. MalaysiaNow The pattern recurs: MACC investigation, unexpected meeting, coercive demand.

Then came Victor Chin’s own allegations. In April 2026, Chin filed suit against Aminul Islam — also known as Amin — a labor tycoon involved in Malaysia’s foreign worker recruitment sector, alleging that Aminul orchestrated pressure from law enforcement agencies and applied other tactics in an attempt to take over NexG Bhd, a provider of identification systems, where Chin had served as chief operating officer until September 2025. Bloomberg

NexG is not a minor player. The company holds lucrative government contracts worth over RM2.5 billion to supply identification documents, including passports, foreign worker IDs, and driving licences. Asia News Network In other words, at the centre of an alleged “corporate mafia” operation is a company controlling some of the most sensitive state-issued identity infrastructure in the country. The governance implications are not merely financial.

The Azam Baki Question — and Anwar’s Dilemma

Azam Baki’s tenure at MACC has been extended three times by Prime Minister Anwar Ibrahim MalaysiaNow, a remarkable act of institutional loyalty — or political insulation — given the accumulation of controversies. Bloomberg reported that corporate filings showed Azam held 17.7 million shares in Velocity Capital Partner Bhd as of last year, a stake worth roughly RM800,000 at recent prices, above guideline thresholds for public officials. Dimsum Daily Azam subsequently admitted to purchasing the shares while serving as MACC chief but maintained he had broken no laws, saying the holdings were acquired transparently and disposed of within the year.

This was notably not the first time. Azam was previously implicated for the same alleged violation back in 2021 and was absolved after the Securities Commission determined his brother had used his trading account. MalaysiaNow The pattern of allegation, denial, and institutional absolution has cycled twice now, each rotation generating less public credulity than the last.

Anwar’s handling of the crisis has drawn intense scrutiny. Bloomberg reported that Anwar urged officials to avoid immediately releasing a report on Azam’s shareholdings to the public — a report produced by a three-person committee of senior civil servants led by the attorney-general, which had reported its findings to cabinet and been referred to the chief secretary for next steps. Bloomberg The delay — combined with the composition of the investigative panel, all members of which are appointed by and report directly to the prime minister — prompted civil society groups to question whether an “independent” panel was anything of the sort.

Civil society groups called for any commission to be led by a figure of genuine judicial stature, such as former Chief Justice Tengku Maimun Tuan Mat, and to operate outside the orbit of executive appointment. Bloomberg That call has gone unanswered.

Anwar’s own position has been contradictory to a degree that has frustrated even his allies. In Parliament on March 3, he said he disagreed with Bloomberg’s allegations but acknowledged the investigations remained open. When questioned about the government’s level of transparency, he told the Dewan Rakyat: “Both of these are not closed — that is the difference.” The Star It is a distinction that fails to satisfy an electorate watching police visit Bloomberg’s office in the Petronas Towers — the physical centrepiece of Malaysia’s modernity — to demand the names of the journalists who wrote the stories.

Police launched a criminal defamation investigation into Bloomberg under Section 500 of the Penal Code and Section 233 of the Communications and Multimedia Act 1998 — both laws frequently used to silence government critics, journalists, and whistleblowers. MalaysiaNow Shooting the messenger is never a good look for a government committed, rhetorically at least, to institutional reform.

Why This Is More Corrosive Than 1MDB

The comparison to 1MDB is unavoidable, but it can mislead. The 1MDB scandal was, in its grotesque way, a monument to old-school kleptocracy: money looted, laundered, and spent. It was recoverable — legally, reputationally, institutionally — because it was a crime committed against the state’s governance apparatus, not through it.

What the MACC “corporate mafia” allegations describe, if credible, is a crime committed through the state’s governance apparatus. And that distinction matters enormously for investor confidence.

When you corrupt a state fund, you destroy one institution. When you allegedly corrupt the anti-corruption institution itself — instrumentalising it as the enforcement arm of private predation — you undermine the entire architecture of market governance. Every listed company becomes a potential target. Every MACC investigation becomes a source of uncertainty rather than assurance. The cost of doing business in Malaysia rises not because of regulatory overreach, but because of regulatory arbitrage by the powerful.

Malaysia is already facing a threat of investor flight in cases of transparency lapses — FDI reportedly declined 15% in the fourth quarter of 2025, a drop analysts have linked to the accumulation of governance-related uncertainty. TECHi The country’s Corruption Perceptions Index score has stagnated at around 50 out of 100, a reflection of persistent concerns about public sector integrity that have remained largely unaddressed despite the post-1MDB reform rhetoric. Ainvest

The geopolitical stakes compound this domestic governance failure. Malaysia sits at the intersection of the US-China technology competition, hosting semiconductor facilities critical to both Western supply chain diversification and China’s regional ambitions. The United States alone reported $7.4 billion in approved investments in Malaysia in 2024, with Germany and China following closely. U.S. Department of State Investors selecting between Kuala Lumpur, Ho Chi Minh City, and Penang as regional bases are doing so in an environment where governance credibility is a quantifiable competitive variable, not a soft consideration.

A country that cannot guarantee that its anti-corruption agency will not be weaponised against the companies that foreign investors have backed is a country that will see capital quietly redirect to neighbours less entangled in institutional scandal.

The Political Fallout: Alliances Fracturing

The corporate mafia allegations have metastasised beyond a governance controversy into a political crisis for Anwar’s unity coalition. Human Resources Minister Ramanan Ramakrishnan — a senior figure in Anwar’s Parti Keadilan Rakyat — was compelled to publicly deny in late March that he had solicited or received a RM9.5 million bribe from Victor Chin, allegedly to help resolve Chin’s legal troubles with the police and MACC. Bloomberg “I never met him. I don’t know him,” Ramanan insisted. The denial may be truthful, but the requirement to make it is itself a measure of how deeply the scandal has penetrated.

Even within Anwar’s coalition, frustration has reached breaking point: DAP, a key coalition partner, moved its national congress two months earlier — from September to July — so members could vote on whether to remain in Anwar’s government depending on whether genuine reforms actually materialise. The Rakyat Post That is a live tripwire beneath an already fragile coalition arithmetic.

When three young protestors interrupted an Azam Baki speech on integrity in early April with placards calling for his arrest, they were detained — prompting lawyers to condemn what they described as a violation of constitutionally guaranteed free speech. MalaysiaNow The irony of arresting citizens for protesting at an integrity event is the kind of tableau that writes itself into the international press cycle.

As of mid-April, Azam’s contract as MACC chief is set to expire on May 12, and reporting by Singapore’s Straits Times — citing high-level sources — suggests his tenure will not be renewed, with Anwar himself reportedly telling cabinet in recent weeks: “Azam is done.” The Star If confirmed, this would mark a significant reversal after three contract extensions — and would almost certainly be read less as a principled reform decision than as political triage, the abandonment of a liability rather than a genuine reckoning with institutional failure.

What Global Governance Frameworks Are Saying

The World Bank’s Worldwide Governance Indicators consistently flag Malaysia’s “Rule of Law” and “Control of Corruption” scores as weak relative to the country’s income level — a divergence that academics have termed the “Malaysian governance paradox”: sophisticated economic management coexisting with institutional opacity.

The IMF’s Article IV consultations on Malaysia have repeatedly emphasised the need for transparent anti-corruption enforcement as a prerequisite for sustained productivity-led growth. The MACC’s alleged weaponisation, if substantiated, would represent precisely the type of governance failure IMF analysts flag as most damaging to private sector confidence — not because it increases regulatory burden, but because it makes regulatory enforcement unpredictable and politically transactional.

ASEAN peers are watching closely. Thailand’s Securities and Exchange Commission has accelerated its own listed-company protection framework in the past 18 months. Indonesia’s Financial Services Authority (OJK) has strengthened minority shareholder protections. Vietnam has passed sweeping anti-corruption amendments. Malaysia, which marketed itself aggressively as a reformed investment destination post-1MDB, risks ceding ground in the regional governance competition at precisely the moment when FDI is being reshuffled by supply-chain decoupling and the semiconductor buildout.

The Path Forward: Five Prescriptions

The question of whether Malaysia is facing a new governance test has been answered — it plainly is. The more urgent question is whether its institutions retain the capacity to pass it.

First, a genuinely independent Royal Commission of Inquiry is the necessary minimum. The current multi-agency task force — comprising the police, Securities Commission, MACC, and Inland Revenue Board — suffers from an obvious conflict: the MACC is both an investigating body and a subject of investigation. Civil society groups have rightly called for a commission led by figures of judicial stature entirely outside the executive appointment chain. Bloomberg

Second, the long-delayed reform to separate the Attorney General’s dual role as both chief legal adviser to the government and public prosecutor must be enacted as a matter of urgency. As long as the same official advises the cabinet and controls prosecution decisions, the structural incentive for political interference in high-profile cases remains intact.

Third, the MACC’s internal oversight architecture — specifically the “Section D” unit and its relationship to listed-company investigations — requires forensic external audit. This is not simply an accountability exercise; it is a market integrity imperative. The Bursa Malaysia cannot operate as a transparent exchange if its listed companies are subject to coercive manipulation through regulatory channels.

Fourth, whistleblower protection legislation must be materially strengthened. The current framework explicitly excludes protection for those who disclose allegations to the media — a provision that chills the very disclosures necessary for public accountability.

Fifth, and perhaps most fundamentally, Prime Minister Anwar Ibrahim must choose between political calculation and institutional credibility. He cannot occupy both positions simultaneously. His decision to repeatedly extend Azam’s tenure, to resist the rapid release of the investigative committee’s findings, and to characterise Bloomberg’s reporting as a “foreign-backed” operation has forfeited credibility with precisely the international investor and civil society audience whose confidence is essential to his economic reform agenda.

The reputational cost of delay compounds with time. Every week that the corporate mafia inquiry remains procedurally murky is another week in which fund managers in Singapore, London, and New York quietly update their country-risk matrices.

Conclusion: The Watchdog Must Be Watched

Ten years ago, 1MDB forced the world to ask whether Malaysia’s institutions could survive political capture. The answer, eventually, was yes — at enormous cost, over a decade, and only with the weight of international law enforcement bearing down on Kuala Lumpur from multiple continents.

The corporate mafia allegations present a more structurally dangerous question: not whether an institution failed, but whether an institution was deliberately inverted — turned from a shield for market integrity into a weapon against it. If the allegations are substantiated, the damage is not confined to the MACC. It radiates outward to the Securities Commission, to Bursa Malaysia, to every listed company where founders must now wonder whether an unexpected call from a new shareholder is a market transaction or the opening gambit of a coordinated predation.

Malaysia has the economic fundamentals to absorb governance shocks. Its semiconductor positioning, its infrastructure, its skilled workforce — these are genuine competitive assets. But assets depreciate when institutions corrode. And institutions corrode fastest when the people charged with preventing corruption become, in the vocabulary of the street, part of the mafia.

The answer to the question — is Malaysia facing a new governance test? — is unambiguous. What remains uncertain is whether Kuala Lumpur’s political class has learned, from the long, expensive, humiliating lesson of 1MDB, that the cost of institutional failure is paid not in one dramatic reckoning, but in thousands of small decisions made by investors and companies who quietly chose to build elsewhere.

The watchdog must be watched. Malaysia’s institutions know this. The question is whether they have the will to act on it before the window closes.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Employment Rights Act 2026: The Day-One Revolution SMEs Can’t Ignore – What the April Changes Really Mean for Small Business

The Employment Rights Act changes of April 2026 rewrote the rules overnight. From day-one SSP to the new Fair Work Agency, here’s what UK SME owners must do now – and why smart leaders will treat compliance as competitive advantage.

Six days ago, the UK’s employment landscape changed more dramatically than at any point since the Thatcher era. On 6 April 2026, a clutch of reforms drawn from the Employment Rights Act 2025 quietly came into force — no fanfare, no countdown clock, no prime ministerial press conference. Just a dense legislative update that landed in the inbox of every HR manager, employment lawyer, and small business owner in Britain, demanding immediate compliance from firms that, frankly, had their hands full dealing with Making Tax Digital for sole traders, a record National Minimum Wage rise, and the continuing aftershocks of business rates revaluation.

These are not trivial tweaks. The employment law changes of April 2026 represent a fundamental reorientation of the balance of power between employer and employee — the most worker-friendly legislative shift since the Blair government’s Working Time Regulations. For the 5.5 million small and medium-sized enterprises that form the spine of the UK economy, employing roughly 16 million people, they are a double-edged sword: a genuine step forward for worker dignity and, simultaneously, a cash-flow, compliance, and cultural challenge that will test even well-run small firms.

The question isn’t whether you agree with the reforms. The question is whether you’re ready for them.

SSP From Day One: A Small Change With Large Consequences

Let’s begin with what looks, on the surface, like a minor administrative adjustment. Statutory Sick Pay is now payable from the first day of illness, not the fourth. The old three-day waiting period — a relic of 1980s legislation designed to deter absenteeism — has been abolished. Simultaneously, the Lower Earnings Limit has been removed, meaning that workers earning below the previous threshold of £123 per week now qualify for SSP for the first time. The rate itself sits at the lower of £123.25 per week or 80% of average weekly earnings.

For a seasonal café in Cornwall with eight part-time staff, or a micro-manufacturer in the West Midlands with twelve employees on variable-hours contracts, this is not an abstraction. It is a real and immediate cost. The Federation of Small Businesses has consistently flagged that the SSP burden falls disproportionately on micro-firms, which lack the HR infrastructure to manage absence strategically and rarely have occupational sick pay schemes to fall back on. The government’s modelling assumes the change will reduce “presenteeism” — the economically damaging phenomenon of unwell workers dragging themselves into work and spreading illness — and there is good evidence for this from comparable reforms in Denmark and the Netherlands. Over a five-year horizon, that argument likely holds. Over a five-week payroll cycle in a cash-constrained small business, it bites.

What you should do now: Review your absence management policy immediately. If you don’t have one, write one. Ensure your payroll software is updated to calculate SSP from day one — several legacy systems used by SMEs default to the old four-day trigger and may require a manual update or vendor patch.

The deeper reform, however — and the one most likely to reshape workplace culture in small firms — is the removal of SSP eligibility thresholds entirely. Millions of low-paid, part-time, and gig-adjacent workers who were previously invisible to the statutory safety net now have a legal floor beneath them. Oppose it philosophically if you wish, but recognise what it signals: the era of building a workforce strategy around disposable low-cost labour is, legislatively speaking, over.

Day-One Family Leave: The Hiring Conversation You Weren’t Having

The second tranche of changes is, in some ways, more disruptive than SSP — because it doesn’t just affect costs. It affects how you hire, how you plan projects, and how you structure teams.

Under the new rules, paternity leave and unpaid parental leave are available from the first day of employment. No qualifying period. No six-month threshold. No waiting for your new hire to “prove themselves” before they become entitled to take time with a newborn or an adopted child. The notice period for paternity leave has been cut to 28 days, down from 15 weeks. The restriction preventing shared parental leave from being taken before 26 weeks of service has been removed.

And then there is Bereaved Partner’s Paternity Leave — a reform that deserves to be named plainly for what it is: a recognition that grief does not wait for a contract anniversary. Bereaved partners may now take up to 52 weeks of unpaid leave from day one of employment. It is, without question, the right thing to do. Any employer who argues otherwise will find themselves on the wrong side of not just the law, but of an increasingly values-driven talent market.

For SMEs, the practical implication is that hiring a new employee now involves accepting a wider range of contingencies from week one. This is not unprecedented — it is, in fact, how most EU member states have operated for years. France, Germany, and the Nordics impose family-leave obligations on employers from day one without qualification. UK small firms competing for international talent or operating in sectors with high graduate turnover have long been at a disadvantage on this metric. Now, at least partially, that gap has closed.

The candid truth is this: if a member of your team takes paternity leave in their first week, you had a resourcing problem before they arrived. The reform is revealing a vulnerability that already existed — it isn’t creating one.

Collective Redundancy: The Doubled Protective Award Is Not a Footnote

Of all the new UK employment rights changes of April 2026, the doubling of the protective award for collective redundancy consultation failures may be the one that most concentrates minds in boardrooms — including small ones.

The maximum protective award for failing to properly consult employees during a collective redundancy — defined as 20 or more redundancies at a single establishment within 90 days — has been doubled to 180 days’ uncapped pay per employee. Read that again: uncapped. For a firm making 25 redundancies and facing a tribunal finding of procedural failure, the liability exposure has moved from serious to potentially existential.

The policy logic is sound: collective consultation requirements exist to ensure workers have genuine notice, genuine engagement, and genuine alternatives explored before jobs disappear. The ACAS guidance on collective redundancy is comprehensive and, frankly, not difficult to follow. The firms that face protective award claims are, by and large, firms that either didn’t know the rules or chose to ignore them. Doubling the penalty is a proportionate response to a compliance gap that has persisted too long.

But here is the SME-specific concern: the 20-employee threshold means that a 40-person firm proposing to make 20 redundancies — perhaps after losing a major contract — is now operating in territory where a process failure could exceed the firm’s annual turnover in liability. Legal advice before any restructuring of this scale is no longer optional. It is the cost of doing business.

Whistleblowing, Record-Keeping, and the Quiet Reforms You Missed

Amid the noise around SSP and family leave, two quieter changes deserve SME attention.

First: sexual harassment disclosures are now explicitly classified as “protected disclosures” under whistleblowing law. This is a clarification rather than a revolution, but it matters — it means employees who raise concerns about sexual harassment internally or externally cannot be dismissed, demoted, or disadvantaged without an employer facing potentially significant tribunal risk. For SMEs without formal whistleblowing policies, now is the time to establish one. ACAS has published practical guidance on what a proportionate policy looks like for small firms.

Second, and perhaps most underestimated: mandatory six-year retention of detailed annual leave records. This includes ordinary and additional leave taken, carry-over arrangements, pay elements used to calculate holiday pay, and any payments in lieu. Six years. For firms that currently track leave via a shared spreadsheet or a paper diary on the office wall — and there are more of these than policymakers acknowledge — this represents a genuine operational lift. It also creates an audit trail that the new Fair Work Agency (more on this below) can follow.

If your leave management is informal, formalise it before an inspection, not after.

The Fair Work Agency: The Regulator That Could Change Everything

Here is where the April 2026 reforms acquire their teeth.

On 7 April 2026 — one day after the legislative changes took effect — the Fair Work Agency launched as the UK’s new single enforcement body for employment rights. It replaces the fragmented architecture of HMRC’s minimum wage enforcement, the Employment Agency Standards Inspectorate, and the Gangmasters and Labour Abuse Authority, consolidating them into a single agency with inspection powers, penalty powers, and the ability to support workers in bringing tribunal claims.

The significance of this cannot be overstated. For years, employment rights in the UK have existed on paper in ways they have not existed in practice. The enforcement gap — between what the law says and what workers actually receive — has been well documented, particularly in sectors like hospitality, logistics, social care, and retail where SME employers dominate. The new Fair Work Agency is the government’s statement that this gap will be closed.

For compliant employers, this should be welcome news. A level playing field benefits firms that do things properly. The restaurateur paying correct minimum wage while a competitor undercuts them by £1.50 an hour has, for too long, been told to accept that unfairness. The FWA represents a structural shift toward genuine competitive equality.

For non-compliant employers — whether through negligence or deliberate practice — the risk calculus has changed fundamentally. An inspection is no longer a theoretical possibility. It is a question of when.

What Every SME Leader Should Do This Month

The April 2026 reforms are not a future problem. They are a current one. Here is a pragmatic action checklist drawn from the specific changes now in force:

- Update your payroll system to trigger SSP from day one of illness, and ensure it calculates the lower-of-£123.25-or-80%-of-average-weekly-earnings correctly for variable-hours workers.

- Remove qualifying-period references from your paternity leave, parental leave, and bereavement leave policies. Any policy that still references a 26-week qualifying period for shared parental leave is now non-compliant.

- Brief your line managers on the 28-day paternity leave notice requirement. A manager who rejects or penalises a new joiner’s paternity leave notice is exposing your business to a day-one tribunal claim.

- Establish or audit your whistleblowing policy to ensure it explicitly covers sexual harassment disclosures as protected.

- Implement a digital leave management system that captures and stores the data required under the new six-year retention rules. CIPD’s Good Work index includes useful benchmarks for what good leave administration looks like in firms of different sizes.

- Take legal advice before any collective redundancy involving 20 or more employees. The doubled protective award means the cost of a procedural error now vastly exceeds the cost of proper legal support.

- Register your awareness of the FWA and conduct an internal audit of your employment practices against minimum wage, holiday pay, and working time obligations. Do it proactively — before an inspector does it for you.

The Productivity Question Nobody Is Asking Loudly Enough

Step back from the compliance checklist for a moment and ask a harder question: will these reforms make the UK economy more productive?

The honest answer is: probably yes, over time, but not without friction.

The UK’s productivity puzzle — the stubborn gap between output per hour here and in comparable economies — has multiple causes, but workforce insecurity is a significant one. Economists at the Resolution Foundation and the CIPD have consistently found that workers without basic protections — no sick pay, no leave entitlements, high job insecurity — invest less in their roles, move between employers more frequently, and are harder to train effectively. The business case for basic protections is not merely ethical; it is microeconomic.

The comparative context matters too. An SME in Stuttgart or Stockholm already operates in an environment with substantially stronger worker protections than April’s reforms introduce in the UK. German small businesses, famously, operate under co-determination structures that give employees genuine governance rights — a concept that remains politically distant in Westminster. The UK is not leaping ahead of international norms; it is closing a gap with them.

The genuine implementation burden, however, falls disproportionately on small firms that lack the HR infrastructure of large corporates. A 400-person firm with an HR director can absorb these changes into existing workflows. A 12-person firm whose owner also handles payroll, business development, and client work on the same day has a real capacity problem. The government’s rollout support — guidance documents, ACAS resources, FWA advisory functions — needs to be proportionate to this reality.

Trade union recognition has also been simplified under the April reforms, with the membership threshold for applying to the Central Arbitration Committee now reduced to 10% and the 40% ballot turnout requirement removed. For sectors where collective bargaining has been historically weak — logistics, hospitality, much of the care sector — this may prove, over time, to be the most structurally significant reform of all. It is certainly the one that will take longest to play out.

Looking Ahead: The October 2026 Cliff Edge

If April felt significant, October 2026 deserves a prominent entry in your planning calendar. The next wave of reforms will include:

- Extension of tribunal claim windows to six months (up from three), meaning employees will have twice as long to bring unfair dismissal, discrimination, and related claims.

- A new duty to include union rights in Section 1 employment statements — the written particulars of employment every employer must provide.

- “All reasonable steps” standard for harassment prevention, extended explicitly to third-party harassment. If your staff interact with customers, clients, or contractors, you are being placed under a proactive duty to prevent harassment from those parties — not just to respond to it.

- Fire-and-rehire restrictions, making such practices automatically unfair dismissal unless business collapse is genuinely unavoidable. This closes a loophole that became deeply controversial during the pandemic and its aftermath.

- Union access rights to workplaces for organising purposes.

October will require another round of policy updates, manager training, and legal review. Build this into your business calendar now rather than scrambling in September.

The fuller government timeline is available directly from gov.uk, and it is essential reading for any business planning headcount, restructuring, or new contracts over the next 18 months.

Compliance as Competitive Advantage

Here is the argument I want to leave you with, because it is the one that rarely gets made clearly enough.

Every reform cycle creates winners and losers — not between employers and workers, but between employers. The firms that treat the April 2026 employment law changes as a compliance burden to be minimised will spend the next year in a defensive crouch, reacting to queries, patching policies, and hoping the Fair Work Agency doesn’t come knocking.

The firms that treat these reforms as an invitation to build genuinely great workplaces will find themselves with a structural talent advantage that no recruitment budget can easily replicate.

Day-one family leave, properly communicated in your hiring process, becomes a recruitment asset — particularly in a tight labour market for skilled workers in their thirties. A well-run whistleblowing process becomes a signal of organisational integrity to the customers, suppliers, and investors increasingly asking ESG questions of small businesses. SSP from day one, framed honestly, becomes part of a conversation about psychological safety that the best candidates actively want to have.

The Employment Rights Act changes of April 2026 are not the end of the world for small business. In the hands of an SME leader willing to think strategically rather than reactively, they are a framework for building something better.

The question is what kind of employer you want to be. The law has just made that question harder to avoid.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance3 months ago

Markets & Finance3 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis2 months ago

Analysis2 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks3 months ago

Banks3 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Analysis2 months ago

Analysis2 months agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Investment3 months ago

Investment3 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Asia3 months ago

Asia3 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Global Economy4 months ago

Global Economy4 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy4 months ago

Global Economy4 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis