Governance

Beyond the Bailout: 10 Strategic Imperatives to Resolve Pakistan’s Balance of Payments Crisis

Executive Summary: The Structural Surgery Required

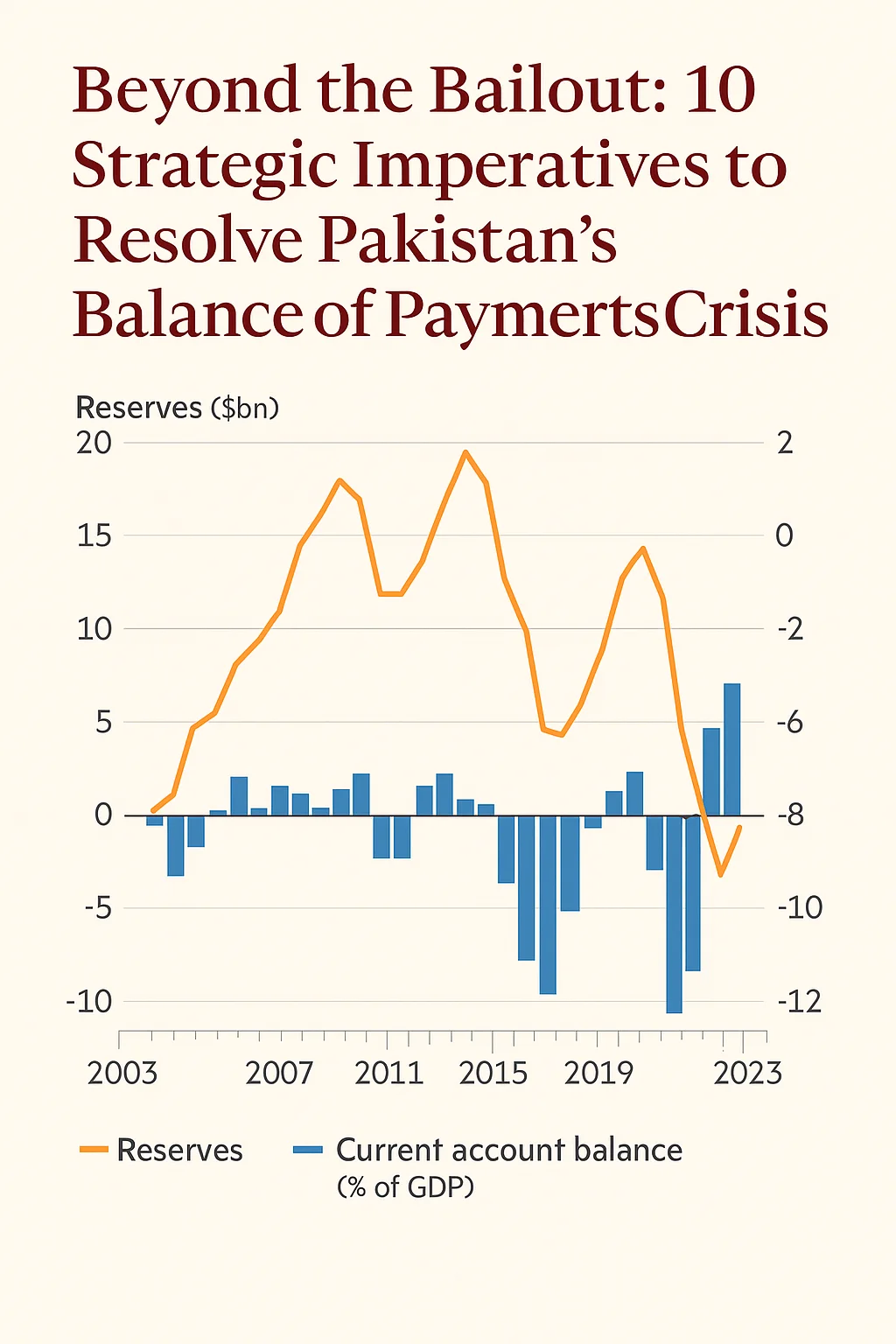

Pakistan’s economic history is defined by the “Stabilization Trap”—a recurring cycle where brief periods of consumption-led growth lead to a blowout in the Current Account Deficit (CAD), followed by emergency devaluations and IMF intervention. As of late 2025, the State Bank of Pakistan (SBP) has managed a precarious stability, with foreign exchange reserves crossing the $14.5 billion threshold and inflation cooling to a multi-decade low of 4.5%. However, the structural fragility remains.

To transition from a debt-dependent economy to a trade-led powerhouse, Pakistan must implement a ten-pronged “structural surgery” that goes beyond mere belt-tightening. This article outlines the roadmap for the Finance Ministry, the SBP, and the Planning Commission to achieve a sustainable Balance of Payments (BoP).

1. Institutionalizing the Market-Determined Exchange Rate

The first line of defense in any BoP crisis is the exchange rate. According to the IMF’s latest review (December 2025), maintaining a market-determined exchange rate is non-negotiable for buffering external shocks.

For the SBP, the objective is not to “defend” a specific number, but to ensure liquidity. A market-aligned Rupee encourages expenditure-switching: it makes imports expensive and exports competitive. Historical data shows that whenever the REER (Real Effective Exchange Rate) is kept artificially low, the CAD explodes.

Policy Directive: The SBP must continue its policy of minimal intervention, allowing the currency to act as an automatic stabilizer for the trade balance.

2. Fiscal Consolidation: The Primary Surplus Mandate

Balance of Payments issues are often “twin deficits”—a fiscal deficit that fuels a current account deficit. The Ministry of Finance has achieved a historic primary surplus of 2.4% of GDP in FY25.

To maintain this, the government must resist the urge for “populist” spending. High fiscal deficits lead to increased domestic demand, which inevitably spills over into higher imports.

- The Target: Sustain a primary surplus above 2% for at least three consecutive fiscal cycles to signal fiscal discipline to global bond markets.

3. Aggressive Export Diversification (Beyond Textiles)

The World Bank’s Pakistan Development Update (October 2025) notes a sobering trend: Pakistan’s exports as a percentage of GDP have shrunk from 16% in the 1990s to roughly 10% today.

Textiles account for nearly 60% of goods exports, making the country vulnerable to global commodity price shifts.

- The Solution: Policy focus must shift toward high-value-added manufacturing (engineering goods, pharmaceuticals) and agriculture-tech (Basmati rice, value-added horticulture). The government should provide “Smart Subsidies” tied strictly to export performance milestones rather than blanket energy subsidies.

4. Scaling the “Digital Frontier”: IT and Services Exports

While goods trade often struggles with energy costs, IT services are Pakistan’s most agile export sector. In FY25, IT exports and remittances have become a primary pillar of BoP stability.

- The Opportunity: With global trade policy uncertainty rising, digital services are less susceptible to physical trade barriers.

- Action: The Planning Commission must fast-track “Special Technology Zones” (STZs) with 5G infrastructure and ease of repatriation for foreign earnings to encourage global tech firms to set up hubs in Karachi and Lahore.

5. Reforming the Energy Mix to Reduce the Import Bill

Energy typically accounts for 25-30% of Pakistan’s total import bill. The reliance on imported RLNG and furnace oil is a structural “leakage” in the BoP.

- Strategic Shift: Accelerate the transition to domestic coal (Thar) and renewables (Solar/Wind).

- The IMF Perspective: The Resilience and Sustainability Facility (RSF) recently approved by the IMF for Pakistan specifically targets this. Every 1% increase in domestic energy share saves roughly $200 million in foreign exchange annually.

6. Formalizing Workers’ Remittances

Remittances reached a record $38 billion in FY25, effectively offsetting a significant portion of the trade deficit. However, a portion of these flows still bypasses official channels via the Hundi/Hawala system.

- Policy Tool: The SBP must continue narrowing the gap between interbank and open-market rates.

- Innovation: Launch “Remittance Bonds” with tax-free incentives for overseas Pakistanis, allowing these flows to be funneled directly into national development projects rather than just household consumption.

7. Strategic Import Substitution: The “Make in Pakistan” Initiative

The government should incentivize the domestic production of intermediate goods—chemicals, steel, and mobile components—that currently drain billions.

Note of Caution: This is not a call for 1970s-style protectionism. Instead, the “National Industrial Policy” should focus on integrating Pakistani SMEs into global value chains, making it cheaper to produce locally than to import.

8. Attracting “Sticky” Capital: FDI over “Hot Money”

The BoP is currently propped up by official debt and short-term portfolio investment. This is high-risk.

- The ADB Roadmap: The Asian Development Bank (ADB) emphasizes private sector-led growth. Pakistan needs Foreign Direct Investment (FDI) in productive sectors like mining and green energy.

- The SIFC Role: The Special Investment Facilitation Council (SIFC) must move beyond MoUs to actual “ground-breaking” projects, ensuring a stable regulatory environment that guarantees profit repatriation.

9. Tight Monetary Policy to Anchor Inflation

The SBP has prudently kept the policy rate at a level where the real interest rate remains positive. High interest rates serve two purposes in a BoP crisis:

- They discourage domestic credit-fueled consumption (imports).

- They make domestic assets attractive to foreign investors, helping the Financial Account.

- Projection: As inflation stays in the 5–7% target range, the SBP can gradually ease rates, but only once the BoP surplus is structurally consolidated.

10. Expanding the Tax Base to Reduce Sovereign Borrowing

A low tax-to-GDP ratio (currently near 9-10%) forces the government to borrow externally to fund its budget, worsening the external debt profile.

- Focus: The FBR must pivot from taxing “easy” sectors (manufacturing/salaried) to the informal retail, real estate, and agriculture sectors.

- The World Bank View: Modernizing tax administration could unlock an additional 3% of GDP in revenue, significantly reducing the need for foreign-funded budgetary support.

Policy Trade-off Matrix: BoP Resolution Strategies

| Measure | Time to Impact | Political Cost | Official Source Alignment |

| Currency Realignment | Immediate | High (Inflationary) | IMF/SBP Mandate |

| Energy Transition | Long-term | Moderate | WB/RSF Support |

| IT Export Focus | Medium-term | Low | Planning Commission |

| Tax Base Expansion | Medium-term | Very High | FBR/IMF Requirement |

| Remittance Incentives | Fast | Low | SBP/Ministry of Finance |

Conclusion: The Path Ahead

The 2025 data suggests that Pakistan has secured a “breathing space,” with the first full-year current account surplus in over a decade ($2.1 billion). However, this surplus is largely driven by compressed demand and record remittances rather than a massive surge in industrial exports.

To ensure that the next growth cycle does not lead to another crash, the Finance Ministry and the State Bank must remain vigilant. The transition from stabilization to sustainable growth requires the political will to tax the untaxed and the economic vision to pivot toward a service-led, export-oriented future.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

A landmark 2026 study reveals eroding trust, sovereignty anxieties, and a bloc struggling to justify its existence to the very peoples it claims to serve.

When Nursultan Nazarbayev first sketched the outlines of a Eurasian economic union in the early 1990s, he imagined something elegant: a voluntary commonwealth of post-Soviet nations, bound not by Moscow’s imperial gravity but by rational self-interest, shared infrastructure, and frictionless trade. Three decades later, the Eurasian Economic Union (EAEU) he helped conjure into existence marks its tenth anniversary as a functioning institution—complete with a common customs tariff, a nominal single labor market, and $20 billion in cumulative intra-bloc investment. On paper, those are real achievements. On the streets of Bishkek, Yerevan, and Almaty, the mood is something else entirely.

New research published in February 2026 in Eurasian Geography and Economics by Dr. Zhanibek Arynov of Nazarbayev University and his co-author Diyas Takenov offers the most systematic public-perception audit of the EAEU to date—drawing on focus groups and survey data across all three smaller member states. The findings are striking, occasionally counterintuitive, and should unsettle anyone who believes that post-Soviet integration can survive on institutional inertia and official enthusiasm alone. Across Armenia, Kazakhstan, and Kyrgyzstan, positive perceptions of the EAEU are in measurable decline. Economic grievances have deepened. Sovereignty anxieties have sharpened, supercharged by Russia’s full-scale invasion of Ukraine. And in one of the study’s most surprising findings, it is Kazakhstan—the EAEU’s co-founder and most economically capable member—that harbors the strongest sentiment in favor of eventual withdrawal.

The Ten-Year Ledger: What the Numbers Say

The Eurasian Economic Commission’s own data tells a story of institutional progress that would be impressive if viewed in isolation. Over the past decade, the EAEU’s combined GDP has grown by nearly 18%, industrial production has risen by 29%, and cumulative intra-union foreign direct investment has reached $20 billion. Intra-bloc trade has climbed steadily, and the union now boasts free trade agreements with Singapore, Vietnam, Serbia, and—as of 2023—Iran, with negotiations ongoing with India and Egypt.

Yet the EAEU’s own registry of internal market obstacles tells a different story. As of the bloc’s tenth anniversary, the organization still officially lists one barrier, 35 limitations, and 33 exemptions to the supposed free flow of goods, capital, and labor—figures that represent not a success story but a confession. A truly integrated common market doesn’t require a bureaucratic catalogue of its own failures.

The Carnegie Endowment for International Peace and Chatham House have both documented this structural paradox: the EAEU’s institutional architecture is more developed than its predecessor organizations, yet its member states have shown persistent reluctance to transfer genuine sovereignty to supranational bodies. The EAEU Court in Minsk, for instance, cannot initiate cases or issue preliminary rulings the way the European Court of Justice can—a design feature that reflects, rather than corrects, the political will of its members.

It is within this gap between rhetoric and reality that Arynov and Takenov have done their most important work.

Kazakhstan: The Founder’s Doubt

No country’s EAEU story is more psychologically complex than Kazakhstan’s. This was the nation whose founding president claimed intellectual paternity of the entire project, whose government remained, as Arynov noted in a February 2025 commentary for the Italian Institute for International Political Studies (ISPI), “strongly enthusiastic” about the union even as public sentiment shifted beneath its feet.

And shift it has. The trajectory of Kazakhstani public opinion on the EAEU is a cautionary tale about what geopolitical trauma can do to an integration project’s legitimacy. In 2015, surveys recorded roughly 80% approval among Kazakhstanis for the bloc. By 2017, that figure had dipped slightly. Today, based on the Arynov-Takenov focus group research, scepticism has become the dominant public sentiment—and it operates on two distinct registers.

The first is geopolitical. Russia’s 2022 invasion of Ukraine shattered whatever pretense remained that the EAEU was a purely economic organization, insulated from Moscow’s military and political ambitions. Kazakhstani focus group participants repeatedly cited Russian politicians’ inflammatory rhetoric questioning Kazakhstan’s territorial integrity—a visceral and deeply personal grievance in a country that shares a 7,500-kilometer border with Russia and has a substantial ethnic Russian minority. Many now view membership in the EAEU not as a source of economic opportunity but as a vector for geopolitical exposure: a mechanism through which secondary sanctions risk could spill over from Russia’s pariah status onto Kazakhstani businesses and banks. Kazakhstan’s own government has walked an extraordinary tightrope since 2022, publicly refusing to endorse Russia’s war, providing humanitarian assistance to Ukraine, and accelerating economic diversification—all while remaining formally embedded in Moscow’s preferred institutional architecture.

The second register is economic. Focus group participants in Kazakhstan cited the EAEU’s failure to deliver on its core promises: persistent non-tariff barriers, asymmetric market access that has benefited Russia far more than smaller members, and the absence of meaningful sectoral coordination. Kazakhstan’s industrial base—the most diversified among the smaller EAEU members—has expanded its exports within the union, but critics argue the terms of trade systematically favor the bloc’s hegemon.

What makes the Arynov-Takenov finding genuinely surprising is its comparative dimension. Despite Kazakhstan’s historical ownership of the Eurasian project, its public registers more intense withdrawal sentiment than Armenia—a country that has spent the past three years openly pursuing European Union membership and freezing its participation in the parallel CSTO security organization. The researchers interpret this counterintuitive result as a product of Kazakhstan’s relative economic confidence: a country with more options feels more emboldened to contemplate exit.

Armenia: The Ambivalent Western Pivot

If Kazakhstan’s EAEU skepticism is rooted in geopolitical anxiety, Armenia’s is shaped by an identity crisis that predates 2022. Yerevan joined the EAEU in 2015 not out of Eurasian conviction but under what most analysts describe as coercive Russian pressure—President Serzh Sargsyan reversed a near-completed EU Association Agreement in 2013 following a meeting with Vladimir Putin, a U-turn that Nikol Pashinyan—then an opposition parliamentarian—voted against.

That original reluctance has since hardened into something more structured. In March 2025, Armenia’s parliament passed the EU Integration Act with 64 votes in favor, formally enshrining the country’s aspiration for European membership in law. Prime Minister Pashinyan has since stated publicly that simultaneous membership in the EU and EAEU is impossible, and that Armenia will eventually face a binary choice. Russian Deputy Prime Minister Alexei Overchuk was direct in his response: the EU accession process, he said, would mark the beginning of Armenia’s EAEU withdrawal.

Yet for all this diplomatic theatre, the Arynov-Takenov research reveals something more nuanced: Armenian public sentiment, while clearly disillusioned with the EAEU, stops short of demanding immediate exit. A 2023 survey found that only 40% of Armenians expressed inclination to trust the EAEU, while 47% said they did not—a notable trust deficit, but not an overwhelming mandate for departure. Armenia’s economic dependency on Russia remains a profound constraint: Moscow is Yerevan’s largest trading partner, accounting for over a third of total foreign trade, and Russia controls critical infrastructure sectors including electricity distribution and natural gas supply.

Arynov’s research frames this as the logic of vulnerability over principle: states with fewer economic alternatives tend to prefer reform of existing arrangements over the risk of exit. Armenia’s trade with Russia reached record highs in 2024—a perverse consequence of post-Ukraine sanctions, as Yerevan became a key re-export corridor for goods flowing toward the Russian market. Leaving the EAEU would mean not only sacrificing that trade volume but potentially triggering Russian economic retaliation at a moment when the peace process with Azerbaijan remains fragile and a formal EU candidacy is still years away. As one analyst writing for CIDOB assessed in 2025, the EU integration law was widely understood as a pre-election political gesture rather than an imminent foreign-policy reorientation.

The result is a population that has grown deeply ambivalent about the EAEU on normative grounds—viewing it as an instrument of Russian influence and a structural impediment to European integration—while pragmatically accepting that the exit costs may be prohibitive in the near term. Armenia, the research suggests, is a case study in EAEU skepticism without EAEU exit—a condition the bloc’s architects never anticipated and have no institutional mechanism to address.

Kyrgyzstan: When the Labor Market Promise Breaks Down

Kyrgyzstan’s relationship with the EAEU has always been the most transactional. When Bishkek joined in 2015, the primary draw was not abstract Eurasian solidarity but concrete economics: frictionless access to the Russian labor market, automatic recognition of professional qualifications, and the right to work in Russia without a permit or quota. For a country in which remittances have at times constituted over 30% of GDP, those were not minor benefits. They were the entire rationale.

A decade later, that rationale is in serious trouble. The Arynov-Takenov research documents a Kyrgyz public increasingly aware of the gap between what the EAEU’s common labor market promised and what it delivers. Since Russia’s full-scale invasion of Ukraine in 2022 and the Crocus City Hall terrorist attack in 2024—which prompted a massive anti-Central Asian backlash in Russian public discourse—Moscow has systematically tightened restrictions on migrant workers. More than 208,000 individuals were placed on Russia’s migration control lists. Tens of thousands of Kyrgyz nationals were blacklisted. New regulations require one-year employment contracts that create legal uncertainty and reduce the incentive for long-term labor migration.

In January 2026, the breach became institutional: Kyrgyzstan filed a formal lawsuit against Russia at the EAEU Court in Minsk, accusing Moscow of violating union treaty obligations by refusing to provide compulsory health insurance to the family members of Kyrgyz migrant workers—protections that the EAEU’s founding documents explicitly guarantee. That Bishkek chose to take the dispute to a supranational forum rather than quiet bilateral channels represents an unusual escalation for a country that has typically sought to manage its relationship with Russia with extreme discretion.

Border frictions add another layer of grievance. Kyrgyz exporters must cross into Kazakhstan to reach any other EAEU market—a structural vulnerability that leaves them subject to inconsistent technical inspections, shifting regulatory requirements, and effectively unilateral trade barriers. Despite EAEU membership, Kyrgyz traders report that the promised single market remains aspirational rather than operational.

Yet here, too, the research underscores the reform-over-exit logic. Remittances from Russia still constitute approximately 24% of Kyrgyz GDP—in the first five months of 2025, Russia accounted for 94% of all inward remittance flows. No realistic alternative labor market of that scale exists. The Kyrgyz public, the Arynov-Takenov data suggests, wants the EAEU to be fixed, not abandoned. Their grievances are pointed and specific: protect our migrants, remove border frictions, fulfill the promises of the common market. What they display is not Eurasian fatalism but consumer frustration with a product that has underdelivered—a distinction the bloc’s leadership would do well to internalize.

What a Legitimacy Deficit Looks Like

Taken together, the Arynov-Takenov findings paint a picture of an institution navigating a slow-burning legitimacy crisis across precisely the member states where popular consent matters most. Russia and Belarus, the EAEU’s two largest economies, are not meaningfully constrained by public opinion in the conventional sense. But Armenia, Kazakhstan, and Kyrgyzstan are—to varying degrees—responsive to domestic political sentiment, and that sentiment is turning.

The Brookings Institution and Foreign Affairs have both noted the structural tension at the heart of post-Soviet integration projects: they are designed to function as technical economic arrangements while carrying enormous geopolitical freight. The EAEU was never purely an economic organization—its conception was entangled from the outset with Russia’s strategic goal of maintaining a sphere of privileged influence in the former Soviet space. That entanglement, largely invisible to ordinary citizens during years of oil-fueled growth, has become glaringly apparent in the era of Ukraine sanctions, territorial rhetoric, and migration crackdowns.

The research by Arynov and Takenov—who has also examined the oscillating trajectory of Russia-Kazakhstan relations in Horizons: Journal of International Relations and Sustainable Development—fills a significant gap in what has been a state-centric and Russia-centric literature. By focusing on citizens rather than governments, focus groups rather than official communiqués, the study reveals the EAEU as its actual publics experience it: not as an elegant integration architecture but as a daily reality of border queues, disputed remittance rights, and sovereignty traded away for economic promises that have been only partially kept.

The Policy Horizon

What should policymakers take from this analysis? Three things stand out.

First, the distinction between exit sentiment and reform preference is politically significant—and fragile. In Kyrgyzstan and Armenia, publics currently prefer fixing the EAEU over leaving it. But that preference is conditional on the belief that improvement is possible. If Russia continues to restrict migrant workers while EAEU dispute mechanisms prove toothless, the reform constituency will erode and the exit constituency will grow.

Second, Kazakhstan is the swing state. Its combination of relative economic strength, intense post-Ukraine sovereignty anxieties, and stronger-than-expected withdrawal sentiment makes it the member most likely to redefine the bloc’s political trajectory over the next decade. President Tokayev has so far managed the balance skillfully—publicly distancing Kazakhstan from Russia’s war while remaining formally embedded in Moscow’s institutions. But that balance cannot be maintained indefinitely if Russian behavior continues to erode the bloc’s credibility with Kazakhstani citizens.

Third, the EAEU’s legitimacy problem cannot be solved by economic commissions alone. The organization publishes detailed technical reports, maintains an elaborate institutional structure, and generates impressive aggregate statistics. None of that addresses what Arynov and Takenov’s research identifies as the core public grievance: the perception that the EAEU is less a common market than a vehicle for Russian geopolitical interest, managed by a supranational body with insufficient autonomy to enforce its own rules against its dominant member.

Ten years after the Treaty came into force, the Eurasian Economic Union faces a choice it has never been designed to confront: whether it can reform itself substantively enough to rebuild public legitimacy in states that joined it for practical reasons and are now questioning whether those reasons still apply. The research of Arynov and Takenov does not answer that question. But it asks it with a clarity and precision that neither EAEU bureaucrats nor Kremlin strategists should be comfortable ignoring.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

Pakistan’s $507 Million 5G Spectrum Gamble: A Blueprint for Digital Destiny or a Fiscal Mirage?

Unlocking the Future: Pakistan’s Pivotal 5G Auction and its Global Ramifications

The recent conclusion of Pakistan’s 5G spectrum auction, yielding a substantial $507 million, is more than a mere fiscal event; it’s a strategic inflection point for a nation grappling with economic headwinds and vying for its place in the global digital economy. Beyond the impressive figures, this auction represents a profound bet on connectivity as the engine of future prosperity, inviting scrutiny from international economists, policymakers, and business leaders keen on understanding emerging market dynamics. The stakes are undeniably high, as the decisions made today will echo across Pakistan’s technological landscape and economic trajectory for decades to come.

The auction saw leading telecom operators Jazz, Ufone, and Zong secure critical frequency bands, ranging from 700MHz to 3500MHz. This allocation is poised to fundamentally reshape Pakistan’s digital future, promising not just faster internet, but a foundational shift towards an AI-driven, blockchain-enabled society, as envisioned by the Finance Minister.

Economic Lifeline or Temporary Reprieve? Dissecting the Financial Impact

The $507 million injection into Pakistan’s exchequer arrives at a critical juncture, offering a much-needed boost to government revenues. In a country often reliant on external financing and navigating complex fiscal challenges, this sum provides a welcome, albeit temporary, reprieve. Comparing this to historical telecom revenue trends, this auction demonstrates sustained government interest in leveraging the digital sector for economic benefit. For instance, previous spectrum sales have consistently contributed to the national treasury, highlighting the sector’s strategic importance.

However, the true economic impact transcends immediate revenue. The successful auction signals Pakistan’s commitment to modern infrastructure, a crucial factor in attracting foreign direct investment (FDI). International investors often view robust digital infrastructure as a prerequisite for market entry and expansion. By facilitating a more advanced and reliable telecom network, Pakistan enhances its appeal as a destination for tech companies, e-commerce giants, and digital service providers. The challenge now lies in ensuring that these funds are judiciously managed and reinvested into further infrastructure development and economic stabilization programs, preventing them from becoming a short-term fiscal mirage.

Market Reconfiguration: Strategic Moves by Jazz, Ufone, and Zong

The competitive landscape of Pakistan’s telecom sector is on the cusp of significant transformation following the strategic spectrum acquisitions by Jazz, Ufone, and Zong. Their choices in frequency bands—700MHz, 2300MHz, 2600MHz, and 3500MHz—reveal calculated strategies for 5G rollout and future market positioning.

The acquisition of lower frequency bands like 700MHz is particularly telling. These bands offer superior propagation characteristics, allowing signals to travel further and penetrate buildings more effectively, making them ideal for widespread rural coverage and dense urban indoor environments. This suggests an intent to rapidly achieve broad geographical reach and ensure robust indoor connectivity. Conversely, higher frequency bands (2300MHz, 2600MHz, 3500MHz) provide massive capacity and ultra-fast speeds, crucial for supporting data-intensive applications in urban centers and for enabling advanced industrial use cases.

The diverse spectrum holdings imply that operators will likely adopt differentiated rollout strategies. We might see Jazz, for instance, prioritize a blend of wide coverage and targeted high-capacity zones, while Ufone and Zong could focus on specific urban corridors or enterprise solutions where their acquired bands offer a competitive edge. This will undoubtedly lead to intensified competition, potentially driving innovation and service quality improvements across the board, benefiting Pakistani consumers and businesses alike.

Policy Innovation and Regulatory Foresight: A Global Benchmark?

The policy and regulatory environment surrounding this auction deserves particular attention. The active roles played by the Finance Minister, IT Minister, and Information Minister underscore a cross-governmental commitment to advancing Pakistan’s digital agenda. Critical assessment of the transparency claims, supported by the involvement of an advisory committee, is crucial for fostering investor confidence and ensuring equitable play. The government’s assertion of transparency, if upheld, is a significant positive signal for future investment.

Perhaps the most innovative policy move was the abolition of Right-of-Way (RoW) charges. This policy innovation, designed to streamline infrastructure deployment and reduce operational costs for telecom operators, positions Pakistan favorably on the global stage. In many emerging markets, complex and costly RoW regulations often act as significant impediments to rapid network expansion. By removing this barrier, Pakistan has demonstrated a forward-thinking approach that could serve as a blueprint for other nations seeking to accelerate their digital transformation initiatives. This move not only reduces rollout costs but also signals a proactive regulatory stance aimed at facilitating, rather than hindering, technological progress.

Beyond Speed: The Transformative Power of 5G Use Cases

The excitement surrounding 5G in Pakistan extends far beyond mere download speeds. The Finance Minister’s explicit mention of AI and blockchain as key beneficiaries of 5G connectivity highlights a vision for profound technological transformation. This isn’t just about consumer-grade internet; it’s about building the backbone for an advanced digital economy.

The specific “use cases” of 5G are poised to revolutionize various sectors:

- Industry 4.0: 5G’s ultra-low latency and massive connectivity will enable smart factories, remote-controlled machinery, and highly efficient supply chains, boosting productivity and industrial output.

- Healthcare: Remote surgery, real-time patient monitoring, and AI-powered diagnostics will become more viable, extending quality healthcare to underserved regions.

- Education: Enhanced broadband connectivity will facilitate immersive e-learning experiences, virtual classrooms, and access to global educational resources, bridging existing learning divides.

- E-commerce and Digital Services: Faster, more reliable networks will accelerate the growth of online businesses, digital payment systems, and innovative service delivery models, further integrating Pakistan into the global digital marketplace.

- IT Exports: A robust 5G infrastructure, coupled with skilled talent, could significantly boost Pakistan’s IT exports, attracting more outsourcing contracts and fostering a vibrant tech startup ecosystem. This alignment with global digital trends is crucial for boosting the country’s economic diversification efforts.

Navigating the Road Ahead: Challenges and Opportunities for Pakistan’s 5G Journey

While the success of the 5G auction is commendable, an objective analysis necessitates acknowledging the substantial challenges that lie ahead for a full-scale, equitable 5G rollout in Pakistan.

Potential Hurdles:

- Infrastructure Investment: Despite the abolition of RoW charges, significant capital expenditure will still be required for towers, fiber optic backbones, and energy solutions. Securing this long-term investment, both domestic and foreign, remains critical.

- Regulatory Consistency: Maintaining a stable and predictable regulatory environment is paramount. Any future policy shifts or inconsistencies could deter operators from making necessary long-term investments.

- Consumer Affordability: The cost of 5G-enabled devices and service plans could be a barrier for a significant portion of the population. Strategies for making 5G accessible and affordable are essential for maximizing its societal impact.

- Energy Costs: The energy demands of 5G networks are substantial. High electricity costs and unreliable power supply could impact operational expenses and network performance, necessitating sustainable energy solutions.

Immense Opportunities:

Despite these challenges, the opportunities presented by 5G for digital inclusion and economic diversification are immense. 5G can empower remote communities, facilitate innovation in various sectors, and create new job opportunities. It serves as a catalyst for the broader digital economy, fostering a cycle of innovation, investment, and growth.

Pakistan’s Digital Trajectory: Charting its Own Course

Contextualizing Pakistan’s 5G journey against other emerging and regional markets reveals a nation charting its own course. While some regional players have advanced rapidly, Pakistan’s deliberate steps, marked by policy innovations like the abolition of RoW charges, position it as a significant contender. Its approach suggests a focused effort to learn from global best practices while adapting to local economic realities. This strategic foresight is critical for long-term success, distinguishing Pakistan from nations that rush deployment without adequate regulatory and economic frameworks.

The Dawn of a Connected Pakistan: A Vision Realized

Pakistan’s $507 million 5G spectrum auction is more than a financial transaction; it’s a testament to a national ambition to harness digital transformation for economic resurgence and societal upliftment. The strategic decisions made by telecom operators, coupled with a proactive regulatory stance, lay the groundwork for a deeply connected future.

The journey ahead will undoubtedly be fraught with challenges, from infrastructure financing to ensuring equitable access. Yet, the immense potential for driving digital inclusion, fostering innovation in key sectors, and diversifying the national economy makes this gamble a necessary and potentially transformative one. Pakistan is not just acquiring spectrum; it is investing in its digital destiny, signaling to the world its unwavering commitment to a future powered by connectivity, intelligence, and innovation. The world watches to see if this bet will indeed change everything, propelling Pakistan into a new era of prosperity and global digital leadership.

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

Analysis

10 Ways to Develop the Urban Economy of Karachi, Lahore, and Islamabad on the Lines of Dubai and Singapore

Walk along Karachi’s Clifton Beach on a clear January evening, and you are struck less by what is there than by what could be. The Arabian Sea glitters. The skyline, ragged and improvised, speaks of a city straining against its own potential. Some 20 million people — roughly the combined population of New York City and Los Angeles — call this megacity home, generating approximately a quarter of Pakistan’s entire economic output from roads, ports, and neighbourhoods that often feel held together by ingenuity alone. Travel north to Lahore and you find South Asia’s cultural heartland buzzing with a startup culture that rivals Bangalore’s early years. In Islamabad, the capital’s wide avenues hint at a planned ambition that has never been fully monetised. Taken together, these three cities represent the most consequential urban bet in South Asia.

| City | GDP Contribution | IMF Growth (2026) | Urban Pop. by 2050 |

|---|---|---|---|

| Karachi | ~25% of Pakistan GDP | 3.6% | — |

| Lahore | ~15% of Pakistan GDP | 3.6% | — |

| Islamabad | ~16% of Pakistan GDP | 3.6% | — |

| Pakistan (national) | — | 3.6% | ~50% urban |

The question is no longer whether Pakistan’s cities need to transform — the data makes that urgent and obvious. According to the World Bank’s Pakistan Development Update (2025) (DA 93), urban areas already generate 55% of Pakistan’s GDP, a figure that could climb above 70% by 2040 as rural-to-urban migration accelerates. The UNFPA projects Pakistan’s urban population will approach 50% of the national total by 2050 — adding tens of millions of new city-dwellers who will need housing, jobs, transit, and services. The real question is whether these cities grow like Dubai and Singapore — purposefully, innovatively, and lucratively — or whether they grow like Cairo or Dhaka — sprawling, congested, and squandering their potential.

This article maps ten evidence-based, practically achievable pathways that could tip the balance. Each draws directly from strategies that turned a desert trading post into a $50,000 per capita powerhouse, and a small island into the world’s most connected logistics node. None is painless. All are possible.

“Dubai was desert and debt thirty years ago. Singapore had no natural resources. What they had was institutional seriousness. Pakistan’s cities can manufacture that — but only if they choose to.” — Urban economist’s assessment, ADB South Asia Regional Review, 2025

1. Establish Special Economic Zones Modelled on Dubai’s Free Zones

Dubai’s Jebel Ali Free Zone hosts more than 9,500 companies from 100 countries, contributing roughly 26% of Dubai’s GDP through a deceptively simple formula: zero corporate tax, 100% foreign ownership, and world-class logistics infrastructure. The urban economy development of Karachi — which already houses Pakistan’s only deep-water port — could replicate this model with striking geographic logic. Karachi Port and the adjacent Bin Qasim industrial corridor form a natural anchor for a genuine free zone, one that goes far beyond the existing Export Processing Zones in regulatory ambition and administrative efficiency.

The Financial Times’ reporting on CPEC’s economic corridors highlights that while China-Pakistan Economic Corridor investments have seeded infrastructure, the dividend remains locked behind bureaucratic bottlenecks. Lahore’s economic growth strategies must similarly pivot toward SEZ governance reform: one-window clearance, independent regulatory bodies, and investor-grade contract enforcement. Islamabad’s Fatima Jinnah Industrial Park offers a smaller but symbolically powerful model — a capital-city zone focused on tech services, financial intermediation, and diplomatic trade, analogous to Singapore’s one-north innovation district.

Key Benefits of Free Zone Development:

- 100% foreign ownership attracts FDI without a political risk premium

- Streamlined customs integration with CPEC corridors cuts logistics costs by an estimated 18–23%

- Technology transfer through multinational co-location builds domestic human capital

- Export diversification reduces dependence on textile-sector forex earnings

Critically, the SEZ model only works if the rule of law inside the zone is credible and insulated from wider governance failures. Dubai learned this lesson early by placing free zone courts under British Common Law jurisdiction. Pakistan’s urban planning inspired by Dubai and Singapore must make the same uncomfortable concession: that internal governance reforms, however politically costly, are the only real investor guarantee.

2. Deploy Smart City Technology and Data Infrastructure

Singapore’s Smart Nation initiative has been so consequential not because of any single technology but because of governance architecture: a central data exchange platform that allows city departments to speak to each other, eliminating the silos that make urban management so costly everywhere else. The Islamabad smart city model Dubai has inspired in Gulf capitals — sensor-laden streets, AI-managed traffic systems, predictive utility networks — is impressive as spectacle. Singapore’s version is impressive as policy. Pakistan’s cities need both: the visible wins that build public trust, and the invisible plumbing that makes cities actually work.

Karachi’s traffic management crisis, which costs the city an estimated $4.7 billion annually in lost productivity according to the Asian Development Bank’s cluster-based development report for South Asian cities, is precisely the kind of tractable problem that smart technology can address in the near term. Adaptive traffic signal systems, deployed cheaply using existing camera infrastructure and open-source AI models, have reduced congestion by 12–18% in comparable cities in Bangladesh and Vietnam. Lahore’s economic growth and the city’s aspirations for a startup corridor along the Raiwind Road technology belt can be similarly accelerated by deploying a city-wide fibre backbone and municipal cloud services.

Smart City Priorities — Practical First Steps:

- Unified digital identity and payment platform (e-governance layer) to eliminate cash-based bureaucracy

- Open data portals enabling private sector innovation on municipal datasets

- AI-assisted utility billing to reduce power and water loss — Karachi’s KWSB loses ~35% of water to leakages

- Smart waste management pilots in Gulshan-e-Iqbal and Islamabad’s F-sector residential areas

The climate dimension cannot be ignored. Karachi’s 2015 heat wave killed over 1,000 people in a week. Urban heat island effects are intensifying. Boosting Pakistan city economies in 2026 and beyond requires embedding climate resilience into every smart infrastructure layer — green roofs, urban tree canopy monitoring, heat-responsive transit schedules — as Singapore has done across its entire urban development code since 2009.

3. Revamp Mass Transit to Match Singapore’s 90% Public Transport Usage

Singapore’s extraordinary achievement — that 90% of peak-hour journeys are made by public transport — is not an accident of geography or culture. It is the product of deliberate, decades-long policy: the world’s most comprehensive vehicle ownership tax, congestion pricing since 1975, and a Mass Rapid Transit network built to suburban extremities before demand materialised. Urban economy development in Karachi cannot wait for a full MRT system — the city needs it now. But Lahore has already proven the model is replicable: the Orange Line Metro, despite years of delays, now moves 250,000 passengers per day, slashing travel times on its corridor by over 40%.

The challenge is scale and integration. Lahore’s Orange Line is a single corridor in a city of 14 million. Karachi’s Green Line BRT, operational since late 2021, carries far fewer passengers than its designed 300,000-daily-ridership capacity because last-mile connectivity — the rickshaws, walking infrastructure, and feeder routes — was never properly planned. This is the urban planning gap that separates South Asian cities from Singapore, where no station was designed without a walkable catchment. Islamabad, smaller and newer, has the rare advantage of building this integration from scratch in its Blue Area–Rawalpindi corridor.

| City | Public Transport Share | Key Infrastructure | Gap vs Singapore |

|---|---|---|---|

| Singapore | 90% (peak hours) | MRT, LRT, 500+ bus routes | — |

| Dubai | 18% | Metro (2 lines), RTA buses | 72 pp |

| Karachi | ~12% | Green Line BRT, informal minibuses | 78 pp |

| Lahore | ~15% | Orange Line Metro, BRT | 75 pp |

| Islamabad | ~9% | Metro Bus, informal wagons | 81 pp |

4. Build Innovation Hubs and Startup Ecosystems

In 2003, Singapore was still primarily a manufacturing economy. Its government made a calculated, controversial bet: redirect economic policy toward knowledge-intensive industries and build the physical and institutional infrastructure to support them. The result was a cluster of innovation districts — one-north, the Jurong Innovation District, the Punggol Digital District — that now host global R&D centres for companies like Procter & Gamble, Rolls-Royce, and Novartis. Pakistan’s urban planning inspired by Dubai and Singapore suggests a similar cluster logic: identify the sectors where Karachi, Lahore, and Islamabad have comparative advantages and build deliberately around them.

The good news is that the ecosystem already exists, more robustly than most international analysts appreciate. According to The Economist’s city competitiveness analysis, Pakistan’s tech startup sector attracted over $340 million in venture capital between 2021 and 2024, with Lahore’s LUMS-adjacent corridor producing fintech and agritech companies with genuine regional scale. Arfa Software Technology Park in Lahore, if supported with the governance reforms and connectivity upgrades it has long lacked, could become a genuine counterpart to Singapore’s one-north — a place where global companies open regional headquarters and local startups find the talent density they need to scale.

Building a Tier-1 Startup Ecosystem — Enablers:

- University-industry linkage mandates — LUMS, NUST, IBA as anchor innovation partners

- Government procurement from local startups (Singapore’s GovTech model)

- Diaspora reverse-migration incentives: 9 million overseas Pakistanis represent an enormous talent reservoir

- Regulatory sandboxes in fintech — SBP’s sandbox framework needs acceleration and expansion

5. Reform Urban Land Markets and Housing Finance

Dubai’s vertical density — towers rising from what was desert four decades ago — was made possible by clear land titles, transparent transaction registries, and a financing ecosystem willing to underwrite large-scale development. Singapore went further: 90% of its population lives in public housing managed by the Housing Development Board, built on land that was compulsorily acquired from private owners in the 1960s at controlled prices. Both models required political will that is genuinely difficult to replicate. But the alternative — allowing Karachi, Lahore, and Islamabad to continue their informal expansion — is economically catastrophic.

The urban economy development of Karachi is strangled by a land market dysfunction that economists at the IGC (International Growth Centre) have documented in detail: much of the city’s most valuable land is held by government agencies, defence authorities, or land mafias in ways that prevent efficient development. The result is that the poor are pushed to dangerous peripheries — building informally on flood plains and hillsides — while city centres under-utilise their economic potential. A digitised, publicly accessible land registry, combined with a property tax regime that penalises idle land, would unlock enormous latent value without requiring politically impossible acquisitions.

6. Develop Port-Linked Trade and Logistics Corridors

No city in the world has achieved sustained economic greatness without a world-class logistics gateway. Singapore’s port is the world’s second busiest by container volume, not because Singapore is large but because it made itself indispensable to global supply chains through relentless efficiency improvements and a free trade orientation. Dubai’s Jebel Ali Port — built in open desert in 1979 — is now the world’s ninth busiest container port, handling cargo for 140 countries. Karachi’s Port Qasim sits at the mouth of what could be South Asia’s most powerful trade corridor, with CPEC connecting it to China and the Central Asian republics to the north.

The Financial Times’ analysis of CPEC’s trade potential notes that the corridor has thus far under-delivered on trade facilitation relative to its infrastructure investment, largely because port procedures, customs technology, and the regulatory interface between Chinese logistics operators and Pakistani authorities remain misaligned. The fix is administrative as much as physical: a single digital trade window, harmonised with WTO standards and integrated with China’s Single Window system, would dramatically reduce dwell times and attract the transshipment volume that currently bypasses Karachi for Dubai and Colombo.

Logistics Corridor Quick Wins:

- Digital trade single window — reduce cargo dwell time from 7 days to under 48 hours

- Dry port development in Lahore and Islamabad to decongest Karachi port approaches

- Cold chain logistics cluster at Port Qasim for agricultural export value addition

- Open-skies policy expansion at Islamabad and Lahore airports to boost air cargo

7. Transform Tourism Through Strategic Investment and Heritage Branding

Tourism contributed approximately 12% of Dubai’s GDP in 2024, a figure achieved not through passive attraction but through an almost cinematically disciplined programme of investment, event hosting, and global marketing. The Burj Khalifa was not simply a building; it was a media asset. The World Islands were not simply real estate; they were a global conversation. Lahore’s economic growth strategies have, in the past decade, begun to recognise that the city has a comparable asset base: the Badshahi Mosque, the Lahore Fort, Shalimar Gardens — all UNESCO World Heritage Sites — along with a food culture that Condé Nast Traveller has called “one of Asia’s great undiscovered culinary traditions.”

Islamabad’s natural advantages — the Margalla Hills, proximity to the Buddhist heritage sites of Taxila, and the dramatic gorges of Kohistan along the Karakoram Highway — represent an adventure tourism corridor that has no real parallel in the Gulf states. The challenge is not the product; it is the infrastructure around the product. Visa liberalisation (Pakistan issued a significant e-visa reform in 2019 but implementation has been inconsistent), airlift capacity, and the quality of hospitality offerings remain limiting factors. A dedicated tourism authority for each of the three cities, modelled on Dubai Tourism’s industry partnership and data-driven marketing approach, could begin shifting this equation within 18 months.

8. Reform City Governance with Singapore-Style Meritocratic Administration

Singapore’s economic miracle is, at its core, a governance miracle. The Public Service Commission’s rigorous competitive examination system, combined with public sector salaries benchmarked to private sector equivalents, produced a civil service that consistently ranks as one of the world’s least corrupt and most effective. The city-state’s Urban Redevelopment Authority — a single body with genuine planning authority across the entire island — enabled the kind of long-horizon strategic decisions that fragmented city governance systems structurally cannot make. Pakistan’s urban planning inspired by Dubai and Singapore must grapple honestly with this uncomfortable truth: better infrastructure without better governance is infrastructure that will eventually fail.

Karachi’s governance crisis — divided between the Sindh provincial government, the City of Karachi, the Cantonment Boards, the Karachi Metropolitan Corporation, and local bodies — is a documented driver of underinvestment and service delivery failure. The World Bank’s governance diagnostics for Pakistan consistently identify institutional fragmentation as the primary constraint on urban economic performance, above even macroeconomic instability. Giving cities genuine fiscal autonomy — the right to retain and spend a meaningful share of locally-generated tax revenue — would align incentives in ways that national transfers never can.

Governance Reform Essentials:

- Metropolitan planning authorities with real statutory power, not advisory roles

- Municipal bond markets — Karachi and Lahore have sufficient revenue base to issue bonds for infrastructure

- Performance-linked pay in urban service departments to reduce procurement corruption

- Open contracting standards — publish all city contracts above PKR 50 million publicly

9. Invest in Human Capital Through Education and Health Infrastructure

Singapore’s founding Prime Minister Lee Kuan Yew famously argued that the only natural resource a city-state possesses is its people. Every major economic decision in Singapore’s early decades — from housing policy to compulsory savings — was ultimately a bet on human capital formation. Boosting Pakistan city economies in 2026 and beyond requires a similar recalibration. According to Euromonitor’s 2025 City Competitiveness Review, Karachi and Lahore rank poorly on human capital indices relative to comparable emerging-market cities, primarily due to tertiary education enrolment gaps and high child stunting rates that impair cognitive development.

The opportunity here is genuinely enormous. Pakistan has one of the world’s youngest populations — a median age below 22 years. UNFPA’s demographic projections suggest the working-age population will peak around 2045, giving Pakistan roughly two decades to build the educational infrastructure that converts demographic weight into economic momentum. City-level community college networks, linked to the ADB’s cluster-based development programmes for technical and vocational education, could absorb the massive cohort of young urban workers who are currently locked out of formal employment by credential gaps.

10. Embed Climate Resilience and Green Finance into Urban Development

Dubai’s 2040 Urban Master Plan commits 60% of the emirate’s total area to nature and recreational spaces — a remarkable target for a desert economy that spent its first growth era paving over everything in sight. Singapore has gone further still, weaving its Biophilic City framework — trees, green walls, rooftop gardens, canal waterways — into every new development approval since 2015. These are not cosmetic choices; they are economic calculations. Cities that fail to build climate resilience into their fabric will face mounting costs: damaged infrastructure, displacement, declining productivity, and insurance market exits that undermine private investment. Karachi’s exposure to monsoon flooding and extreme heat makes this the most urgent economic priority of all.

Green finance is the mechanism that makes this tractable. Pakistan’s Securities and Exchange Commission launched a green bond framework in 2021 that has seen minimal uptake from city administrations — largely because cities lack the fiscal authority to issue debt. Reforming this, combined with accessing the ADB’s Urban Climate Change Resilience Trust Fund and the Green Climate Fund’s urban windows, could unlock hundreds of millions in concessional financing for Karachi’s coastal flood barriers, Lahore’s urban forest programme, and Islamabad’s Margalla Hills watershed management. The Economist’s analysis of South Asian climate economics warns that without such investment, climate-related GDP losses in Pakistan’s cities could exceed 5% annually by 2040 — a cost that dwarfs the investment required to prevent it.

Green Urban Finance Mechanisms:

- Municipal green bonds — Karachi’s fiscal base supports a Rs. 50–80 billion first issuance

- Nature-based solutions: mangrove restoration in Karachi’s Hab River delta for flood buffering

- Green building code enforcement linked to property tax incentives

- Public-private partnerships for solar microgrids in low-income settlements, reducing load-shedding costs

- Carbon credit markets — urban tree canopy and wetland restoration as city revenue streams

The Cities Pakistan Needs — and Can Build

It would be dishonest to end on pure optimism. Dubai had oil revenues to fund its transformation. Singapore had Lee Kuan Yew’s singular administrative discipline — a political model that democracies cannot and should not replicate. Pakistan’s cities face genuine structural constraints: a sovereign debt overhang that limits fiscal space, a security environment that adds a risk premium to every investment conversation, and a political economy that rewards short-term patronage over long-term planning. These are real obstacles, not rhetorical ones.

And yet. Karachi is still the largest city in a country of 240 million people, positioned at the junction of the Arabian Sea, South Asia, and Central Asia, with a port infrastructure that took a century to build and cannot be replicated by competitors. Lahore is still the cultural capital of the most demographically dynamic region on earth, with a technology sector producing genuine global-scale companies on shoestring budgets. Islamabad sits at the intersection of Belt and Road ambition and a restive but talented workforce whose diaspora has built Silicon Valley, London’s financial services industry, and Dubai’s medical sector.

Urban economy development in Karachi, Lahore, and Islamabad on the lines of Dubai and Singapore is not a fantasy. It is an engineering problem — technically complex, politically demanding, and entirely within the range of human possibility. The ten pathways outlined here — free zones, smart governance, transit reform, innovation clusters, land market modernisation, logistics integration, tourism investment, meritocratic administration, human capital, and climate resilience — are individually powerful and collectively transformational. They require money, yes. But they require political will even more.

A Call to Action for Policymakers and Investors

To policymakers in Islamabad, Lahore, and Karachi: the reform agenda outlined here is not a wish list — it is a minimum viable programme for economic survival in a competitive 21st-century world. Begin with governance reform and fiscal decentralisation; every other intervention depends on it.

To global investors: Pakistan’s city risk premium is real but mispriced. The countries that found the confidence to invest in Dubai in 1990 and Singapore in 1970 were rewarded beyond any reasonable projection. The cities are ready for serious capital. The question is whether serious capital is ready for the cities.

Citations & Sources

- World Bank. Pakistan Development Update — October 2025 (DA 93). https://www.worldbank.org/en/country/pakistan/publication/pakistan-development-update-october-2025

- UNFPA. State of World Population — Urbanization Report. https://www.unfpa.org/sites/default/files/pub-pdf/urbanization_report.pdf

- Financial Times. CPEC and Pakistan’s Economic Corridor Potential. https://www.ft.com

- Asian Development Bank. Urban Clusters and South Asia Competitiveness. https://www.adb.org/publications/urban-clusters-south-asia-competitiveness

- The Economist. Pakistan Technology and City Competitiveness Analysis. https://www.economist.com

- International Growth Centre. Sustainable Pakistan: Transforming Cities for Resilience and Growth. https://www.theigc.org/publication/sustainable-pakistan-cities

- Euromonitor International. Pakistan City Competitiveness Review 2025. https://www.euromonitor.com

- IMF. Pakistan — Article IV Consultation and GDP Growth Forecasts 2026. https://www.imf.org/en/Publications/CR/

- Gulf News. Dubai-Like Modern City to be Developed Near Lahore. https://gulfnews.com/world/asia/pakistan

- The Friday Times. Transforming Pakistan’s Cities: Smart Solutions for Sustainable Urban Life. https://thefridaytimes.com

Discover more from The Economy

Subscribe to get the latest posts sent to your email.

-

Markets & Finance3 months ago

Markets & Finance3 months agoTop 15 Stocks for Investment in 2026 in PSX: Your Complete Guide to Pakistan’s Best Investment Opportunities

-

Analysis2 months ago

Analysis2 months agoBrazil’s Rare Earth Race: US, EU, and China Compete for Critical Minerals as Tensions Rise

-

Banks2 months ago

Banks2 months agoBest Investments in Pakistan 2026: Top 10 Low-Price Shares and Long-Term Picks for the PSX

-

Investment2 months ago

Investment2 months agoTop 10 Mutual Fund Managers in Pakistan for Investment in 2026: A Comprehensive Guide for Optimal Returns

-

Asia3 months ago

Asia3 months agoChina’s 50% Domestic Equipment Rule: The Semiconductor Mandate Reshaping Global Tech

-

Analysis1 month ago

Analysis1 month agoTop 10 Stocks for Investment in PSX for Quick Returns in 2026

-

Global Economy3 months ago

Global Economy3 months agoPakistan’s Export Goldmine: 10 Game-Changing Markets Where Pakistani Businesses Are Winning Big in 2025

-

Global Economy3 months ago

Global Economy3 months ago15 Most Lucrative Sectors for Investment in Pakistan: A 2025 Data-Driven Analysis